CORONOMICS Munich 22 September 2020 - institutional assets AWARDS

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

CORONOMICS

Munich · 22 September 2020

DR. DANIEL STELTER ·

CORONOMICS – the new economic order

Weak recovery from the financial crisis

Fragile financial system

Mother of all recessions

Central Banks go “all-in”

Eurozone fundamentally ill

How to deal with too much debt?

A bold proposal for the Euro

Coronomics for Germany

CORONOMICS – the new economic order

Weak recovery from the financial crisis

Fragile financial system

Mother of all recessions

Central Banks go “all-in”

Eurozone fundamentally ill

How to deal with too much debt?

A bold proposal for the Euro

Coronomics for Germany

Financial Crisis reduced growth worldwide

4

Italian Tragedy – but even Germany not great

5

Central Banks aggressive Source: JP Morgan

Lowest interest rates in 5,000 Years Source: BofA

Cheap money feeds zombies

Zombie share and policy rates Zombie duration and policy rates

6 0.0 2.50 0.0

2.5 2.25 2.5

4

5.0 2.00 5.0

2 7.5 1.75 7.5

10.0 1.50 10.0

0

12.5 1.25 12.5

-2 15.0 1.00 15.0

1985 1990 1995 2000 2005 2010 2015 1985 1990 1995 2000 2005 2010 2015

Zombie share (lhs)1 Policy rate (rhs)2 Zombie duration (lhs)3 Policy rate (rhs)4

1. Mean of country zombie shares; narrower definition; 2. Mean of country (nominal) policy rates;

Source: BIS 3. Mean of zombie firm duration in years; narrower definition; 4. Mean of (nominal) policy rates

Zombies in Europe

Share of capital sunk in “zombie” firms 2013 (%)

Italy

Spain

Belgium

Portugal

Luxembourg

Germany

Sweden

South Korea

Austria

UK

Finland

France

Slovenia

0 5 10 15 20

Source: The Telegraph

Auch in USA Zombies auf dem Vormarsch

USA: Anteil von Zombie-Unternehmen

Anteil (in %) der börsennotierten

Unternehmen, die mehr als 10 Jahre

alt sind und deren Zinsdeckungsgrad

drei Jahre in Folge unter 1 liegt

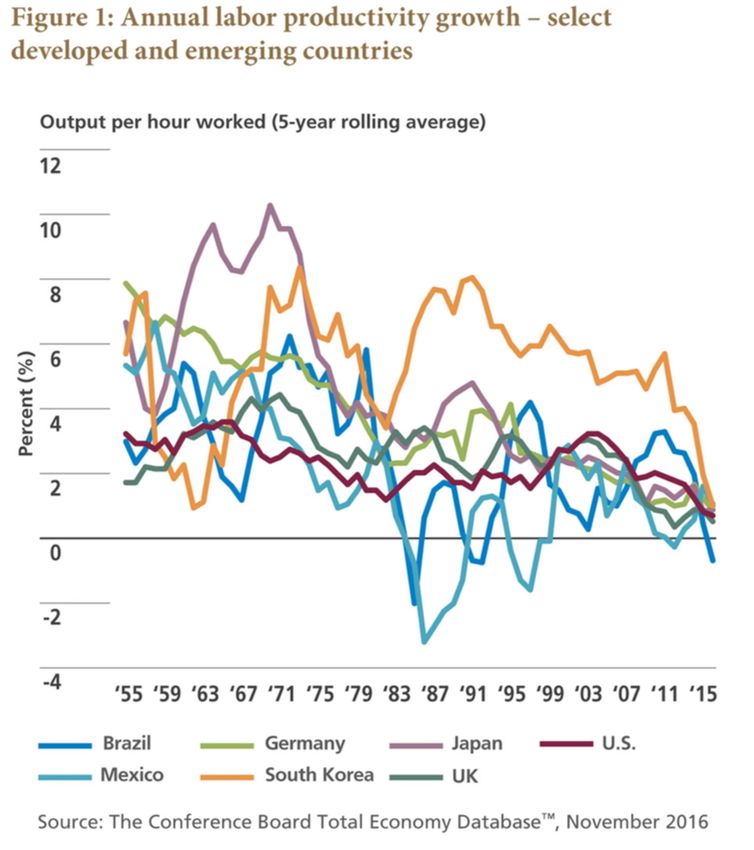

Quelle: DB Global Research 10Productivity growth slows down

Annual labor productivity growth

5-year

rolling

average

(%)

USA

Germany

UK

Japan

South Korea

Brasil

Mexico

output per hour worked

Source: Conference Board, November 2016Peak youth

Young children and old people as % of the population

16

14

12

10

8

6

4 Under 5

65+

2

0

1950 1960 1970 1980 1990 2000 2010 2020 2030 2040 2050

Source: BofAIMF warned in autumn 2019

» After slowing sharply in the last three quarters of 2018, the pace of

global economic activity remains weak. Momentum in manufacturing

activity, in particular, has weakened substantially, to levels not

seen since the global financial crisis. Rising trade and geopolitical

tensions have increased uncertainty about the future of the global

trading system and international cooperation more generally, taking a

toll on business confidence, investment decisions, and global trade. A

notable shift toward increased monetary policy accommodation—

through both action and communication—has cushioned the impact of

these tensions on financial market sentiment and activity, while a

generally resilient service sector has supported employment growth.

That said, the outlook remains precarious.«

13IMF warned in autumn 2019

» (…) we need urgent co-ordinated political action to restore

confidence, boost inclusive growth and raise living standards; global

trade is stagnating and is dragging down economic activity in

almost all major economies; and policy uncertainty is undermining

investment and future jobs and incomes. Moreover, risks of even

weaker growth remain high, including from an escalation of trade

conflicts, geopolitical tensions, the possibility of a sharper-than-

expected slowdown in China, and climate change.«

14CORONOMICS – the new economic order

Weak recovery from the financial crisis

Fragile financial system

Mother of all recessions

Central Banks go “all-in”

Eurozone fundamentally ill

How to deal with too much debt?

A bold proposal for the Euro

Coronomics for GermanyCorrelation is not causation… still...

Central banks balance sheet (USD)

US 2,400 14,000 G3

stocks central

2,200 13,000 bank

G3 central bank balance sheet

balance

2,000 US stocks 12,000 sheet

1,800 11,000

1,600 10,000

1,400 9,000

1,200 8,000

1,000 7,000

800 6,000

600 5,000

2009 2010 2011 2012 2013 2014 2015 2016 2017

Source: bto analysisThird bubble in 25 years?

Central

Asset prices vs. GDP – growth rates

Bankers’

(index; December 31, 1997 = 100)

bubble

400

Housing

350

bubble

300

250 Dot-com

bubble

200 Recession

US nominal GDP

150

Net worth of US households

100

0

1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

Source: BloombergOur monetary order supports inflation

Number of years to double the global median price level

250

1571

200

150 1698

1363 1917

1805

100

50 1248

1942 1973

1952 1995 2011

1979 1987

0

1 2 3 4 5 6 7 8 9 10 11 12 13

Source: Deutsche Bank; bto analysisExample UK

(% of GDP)

125

100

75 100%

Unproductive loans

50

35%

Unproductive loans1

25

25% 25%

Loans to productive sector2

0

1990 Today

Source: bto analysis

1. Construction sector and mortgages

2. Excl. construction sectorCentral Banks „asymmetrical reaction“

Fed Funds rate vs. 10-year treasury (%)

20

Black Monday

Fed Funds rate

S&L crisis

US 10-year treasury

15

Japanese bubble

Tequila crisis

10 Asia crisis

Dotcom bubble GFC

5 ???

0

1980 1984 1988 1992 1996 2000 2004 2008 2012 2016

Source: IncremetumExploding debt

Global Debt (Trillion US-$)

Households

166 169

Non-financial corporations 156

148

138

Government 42 43

39

111 116 38

105 36

97

33 33

32 65 66

31 56 61

64 52

42 43

18 41

37

25 59 60

50 54 56

32 36 40

21 29

2000 2007 2008 2009 2011 2013 2014 2015 2016 1. HY 2017

Total debt/

198 207 213 226 224 227 232 234 237 236 GDP (%)

Source: bto analysisSomehow financial stability deteriorated… Years with a financial crisis since 1600. Internet search. Source: Deutsche Bank 22

Debt drives asset values and inequality

Capital/income ratio 1980 – 2010 (%)

700

600 676

500 575 601 1980

Wealth

522

400

434 2010

412 410

300

321 322 355

309

200 253

100

0

France UK Germany Italy USA Japan

Debt government, private households, non-financial corporations (% of GDP)

500

400 456 1980

2009

Debt

300

321 322 308

265 290

200 241

100 160 160 136 151

109

0

France UK Germany Italy USA Japan

Source: Bank of International Settlement, Working Papers No 352 (2011); Alvaredo, Facundo, Anthony B. Atkinson, Thomas Piketty and Emmanuel Saez, The World Top Incomes Database,

http://topincomes.g-mond.parisschoolofeconomics.eu/ , 06/06/2014Piketty doesn`t understand the leverage effect

PIKETTY: STELTER:

»Debt is »Debt is not

neutral.« neutral, but

drives wealth.«

• Gross asset: e.g., 500 • Gross asset: e.g., 500

• Debt: e.g., 200 • Debt: e.g., 200

• Net asset: = 300 • Net asset < 300

Government debt a result of wrong Public and private debt influence the gross

distribution of wealth between the and the net value of all assets

private and the public sector. Private

debt not included in analysis. No

mentioning in index of the book.Leverage effect: example 1 Asset: e.g. a stock. Price: 100, yearly return: 10 2 100% equity financing: yield 10% 3 Bank credit available for 5% 4 Bank credit: 50, equity: 50 5 Interest expense: 2.5, return on equity: 7.5 = yield: 15% 6 Bank Credit: 80, equity: 20 7 Interest expense: 4.0, return on equity: 6.0 = yield: 30% And: You can buy stocks for 500 instead of 100! Total return: 30

Debt with less impact

GDP generating capacity of global debt: all major economies

2007

2017

-37.3%

1.0 1.0

-42.6% 0.83

0.8 0.8

0.68

-17.4% -14.6% -14.6%

-20.5% -11.1%

-14.3%

0.6 0.6

-18.2% 0.52

0.46 0.48 0.48

0.44 0.45

0.40 0.41 0.41 0.42

0.38 0.39

0.4 0.35 0.4 0.36

0.33

0.27

0.2 0.2

0.0 0.0

Euro zone UK Japan USA China G (20) Emerging All reporting Advanced

aggregate markets countries economies

(aggregate) (aggregate) (aggregate)

Source: HoisingtonCredit quality gets worse and worse… Proportion of cov-lite loans Source: Deutsche Bank, S&P 27

2,500

3,000

1,000

1,500

0

BUSD

2,000

Source: SocGEn

Dec. 1998

July 1999

Feb. 2000

Sept. 2000

April 2001

Nov. 2001

June 2002

Jan. 2003

Aug. 2003

March 2004

Oct. 2004

May 2005

Dec. 2005

July 2006

US corporate debt at all time high

Feb. 2007

Sept. 2007

April 2008

Nov. 2008

June 2009

Jan. 2010

Aug. 2010

March 2011

Oct. 2011

May 2012

Dec. 2012

July 2013

Feb. 2014

Sept. 2014

Net debt

April 2015

Nov. 2015

June 2016

EBITDABBB a problem in the next recession? Share of market value in Bloomberg Barclays USD IG (%) Source: Deutsche Bank

Buy-Backs main driver of stock returns in the US US companies have been the biggest net buyers of stocks over the last decade through buybacks Cumulative net purchase of US stocks (in $ billions) Source: Deutsche Bank 30

Big worries in front of the next recession Out of Space: Central banks have no room to cut rates like they did in the last slump Source: Bloomberg data 31

CORONOMICS – the new economic order

Weak recovery from the financial crisis

Fragile financial system

Mother of all recessions

Central Banks go “all-in”

Eurozone fundamentally ill

How to deal with too much debt?

A bold proposal for the Euro

Coronomics for GermanyThe Mother of all Recessions The Eurozone economy endured its worst downturn on record in March Source: IHS MARKIT 33

CORONOMICS – the new economic order

Weak recovery from the financial crisis

Fragile financial system

Mother of all recessions

Central Banks go “all-in”

Eurozone fundamentally ill

How to deal with too much debt?

A bold proposal for the Euro

Coronomics for Germany“All-in” of States and Central Banks I Largest bailouts in history in 2020 USD ($bn) vs. G7 public and private debt to GDP Source: Deutsche Bank, Haver, IMF. Dotted line shows our forecast for 2020. 35

“All-in” of States and Central Banks II Extraordinary central bank stimulus has eased financial stresses Source: Citi ©FT 36

No wonder, stock markets are up Too much money chasing too few assets in 2021? Source: Nordea and Macrobond 37

CORONOMICS – the new economic order

Weak recovery from the financial crisis

Fragile financial system

Mother of all recessions

Central Banks go “all-in”

Eurozone fundamentally ill

How to deal with too much debt?

A bold proposal for the Euro

Coronomics for GermanyA debt driven Boom

Kredite an HH und Nicht-Finanzunternehmen (Mrd. €) Realzinssatz und Inflation 1999 – 2007

D Jährlicher Inflationsrate (%)

5 4

Wohnbau, Immobilien, Bau R2 = 0,9649

4

Greece

Konsum und Dienstleistungen 3 Ireland

3 Spain

Industrie und Agrar Portugal Italy

France

2 Austria

2 Netherlands

Belgium

1

Germany

Finland

0 1

1992 1995 1998 2001 2004 2007 2010 2013 1,0 1,5 2,0 2,5 3,0

D Realzinssatz

Realzinsrate und Kreditwachstum 1999 – 2007 Kreditwachstum und Handelssaldo 1999–2007

D Jährliche Kreditwachstumsrate (%)

D Jährliche Handelssaldo (%)

25 1,0

R2 = 0,7754 Germany Austria R2 = 0,7786

20 0,5 Netherlands

Ireland

Greece Finland

15 Spain

0,0

Italy Portugal

Portugal Belgium

10 Austria -0,5

France Belgium Italy Ireland

5 Netherlands Finland -1,0 Spain

France

Greece

Germany

0 -1,5

1,0 1,5 2,0 2,5 3,0 -1 0 1 2 3 4 5 6 7 8 9 10 11

D Realzinsrate (%) D Jährliches Kredit-/BIP-Wachstum (%)

Source: IMFConvergence? – Less than before the Euro (I)

Treiber BIP-Wachstum

4

Länder mit hoher Produktivität Länder mit niedriger Produktivität

3

2

1

0

-1

-2

1990-1999 2000-2007 2008-2016 1990-1999 2000-2007 2008-2016

Labor Kapital TFP Durchschnittliches Wachstum

Quelle: IMFConvergence? – Less than before the Euro (II) Intra- and Extra-EA Trade in Goods Intra-EA 12 Trade in Goods Sum of exports and imports in % of GDP Sum of intra-EA 12 exports and imports in % of total trade Sources: OECD Monthly Statistics on International Trade; AMECO

Fighting a debt crisis with more debt

» The Euro Zone must go

towards more solidarity

and integration: a common

budget, a common

borrowing capability,

and fiscal convergence. «

The „Reconstruction Fund“ and debt on

EU level buys time but does not solve the

problem.Dabei geht das nicht – sagt der IWF!

Anteil der aufgefangenen Fiskalische Transfers

externen Schocks Kapitalmärkte und private Verluste

Kreditmärkte

100

80

60

40

20

0

-20

EU EMU Switzerland USA Germany Source: IMFThe fairness question with transfers Private Wealth/GDP Source: James Davies, Rodrigo Lluberas und Anthony Shorrocks, Global wealth databook 2019 44

Countries with “M” have more in common… Source: JP Morgan 45

Keine leichte Lösung

Abbau fauler Ausgleich Wett-

Schulden bewerbsfähigkeit

1. Interne Abwertung

2. Transferunion

3. Höheres Wirtschaftswachstum ? ?

4. Schuldenrestrukturierung und Wachstum

5. Höhere Inflation ? ?

6. Pleiten und EuroaustritteCORONOMICS – the new economic order

Weak recovery from the financial crisis

Fragile financial system

Mother of all recessions

Central Banks go “all-in”

Eurozone fundamentally ill

How to deal with too much debt?

A bold proposal for the Euro

Coronomics for GermanyHow to deal with too much debt?

Austerity?

Growing out of the problem?

Back to Mesopotamia?

Inflation?

48How to deal with too much debt?

Austerity?

Growing out of the problem?

Back to Mesopotamia?

Inflation?

49How to deal with too much debt?

Austerity?

Growing out of the problem?

Back to Mesopotamia?

Inflation?

50How to deal with too much debt?

Austerity?

Growing out of the problem?

Back to Mesopotamia?

Inflation?

51How to deal with too much debt?

Austerity?

Growing out of the problem?

Back to Mesopotamia?

Inflation?

52How to deal with too much debt?

Austerity?

Growing out of the problem?

Back to Mesopotamia?

Inflation?

53Debt restructuring already in the Bible and Mesopotamia

Debt restructuring in the Bible: Debt restructuring in

"The Jubilee Year" ancient Mesopotamia

In the Biblical Book of Leviticus, a Jubilee year is mentioned to In ancient Mesopotamia, debt was commonplace;

occur every fiftieth year, in which slaves and prisoners would individual debts were recorded on clay tablets.

be freed and debts would be forgiven Periodically, upon the ascendancy of a new

monarch, debts would be forgiven: in other words,

» And ye shall hallow the fiftieth year, and proclaim liberty

the slate would be wiped clean

throughout all the land unto all the inhabitants thereof: it shall be

a jubile unto you; and ye shall return every man unto his

possession, and ye shall return every man unto his family. A jubile

shall that fiftieth year be unto you: ye shall not sow, neither reap

that which groweth of itself in it, nor gather the grapes in it of thy

vine undressed. For it is the jubile; it shall be holy unto you: ye

shall eat the increase thereof out of the field. In the year of this

jubile ye shall return every man unto his possession.«

Leviticus 25:10–13

Source: WikipediaMacron’s advisors think big

Dealing with

legacy debt in

the Euro area

»While public debt has increased over the past twenty years, so has

household wealth – particularly when it comes to real-estate – with

large distributional consequences. An avenue could therefore consist of

a highly indebted country decreeing that it becomes part-owner of all

lands on which dwellings are built, up to a given fraction of their

value (establishing a leasehold in effect on part of the land). The

payment for the right of occupancy by the homeowner would generate

an annual revenue stream for the state. Homeowners could chose to

defer annual payments, the total amount of which would become due

only upon the sale or inheritance of the home.«

Source: France Strategie, http://www.strategie.gouv.fr/english-articles/dealing-legacy-debt-euro-area, October 2017 55France is the biggest debtor

Schuldenstände der verschiedenen Sektoren in % des BIP

Private Private

Country State Companies Households Sector Total Total

Germany 61.0 59 54 114 175

Austria 71.1 90 49 139 210

Italy 137.3 69 41 111 248

Spain 97.9 95 57 152 250

Portugal 120.5 100 65 164 285

Netherlands 49.3 163 101 264 313

Belgium 102.2 150 61 212 314

France 100.4 155 61 216 317

Source: Bank für Internationalen Zahlungsausgleich, Stand Q3/2019 · erstellt mit Datawrapper 56How to deal with too much debt?

Austerity?

Growing out of the problem?

Back to Mesopotamia?

Inflation?

57How to deal with too much debt?

Austerity?

Growing out of the problem?

Back to Mesopotamia?

Inflation?

58Helicopters on the way Source: I, Igge, CC BY-SA 3.0, https://commons.wikimedia.org/w/index.php?curid=2436263 59

The idea of helicopter money is gaining popularity

» Let us suppose that one day a helicopter flies over this Milton Friedman

The Optimum

community and drops an additional $1000 in bills

Quantity of Money,

from the sky, which is, of course hastily collected by Chapter 1

members of the community …« 1969

» Today I will argue for a different approach and suggest Ben Bernanke

that the Bank of Japan cooperate temporarily with the Speech before the

government to create an environment of combined Japan Society of

monetary and fiscal ease to end deflation and help Monetary Economics

Tokyo, May 31, 2003

restart economic growth in Japan.«

» … in some extreme circumstances – those in which there is Adair Turner

a simultaneous and significant fall in both the price level Financial Services Authority

and real output – it is unambiguously clear that OMF would Chairman, Lecture at the

be the best policy, and in some circumstances may be the Cass Business School

London, February 6, 2013

only policy available to prevent continual deflation.«

60Deleveraging is deflationary

Deflationary

risk levers

• Deleveraging need

• Austerity programs

• Excess capacity

• Potential global slowdown

Source: bto analysis 61Deleveraging is deflationary, printing money is inflationary

Deflationary

risk levers

• Deleveraging need

• Austerity programs

• Excess capacity

Inflationary

• Potential global slowdown

risk levers

• Inflate away high debt levels

• Liquidity glut

• High commodity prices

• Internal EMU imbalances

Source: bto analysis 62M*V = P*Y: Watch out for the velocity of money!

Increase in money supply is offset by low velocity of money

25 2500 Money velocity 1

Monetary base(B$)2

20 2000

15 1500

1 Velocityis a ratio of nominal GDP to

the monetary base as measure of the

10 1000 money supply. It can be thought of as

the rate of turnover in the money

supply--that is, the number of times

one dollar is used to purchase final

5 500

goods and services included in GDP

2 Monetary base: money supply directly

0 0 controlled by the central bank

Note: M = money supply, V = velocity,

1980 2010 P = Price level, Y = GDP

Source: Thomson Datastream; Federal Reserve 63Alterung setzt mit voller Kraft ein

Erwerbsbevölkerung in den Industrieländern vor Schrumpfung

1,5 % 75

Entwicklung der Bevölkerung im erwerbsfähigen Alter (%)

Quote der Altersabhängigkeit 70

1,0 %

65

0,5 % 60

55

0,0 %

50

-0,5 % 45

Quelle: Twitter @SoberLook 64How to deal with too much debt?

Austerity?

Growing out of the problem?

Back to Mesopotamia?

Inflation?

65How to deal with too much debt?

Austerity?

Growing out of the problem?

Back to Mesopotamia?

Inflation?

66CORONOMICS – the new economic order

Weak recovery from the financial crisis

Fragile financial system

Mother of all recessions

Central Banks go “all-in”

Eurozone fundamentally ill

How to deal with too much debt?

A bold proposal for the Euro

Coronomics for GermanyJoint restructuring the euro zone debt overhang

Pooling of debt of 75% of GDP Refinancing with „Eurobonds“

160% 160%

Eurozone

redemption Features:

fund

130% 130%

► Jointly guaranteed to obtain

AAA rating and low rates

► Repayment over 100+ years

80%

► Interest free for some years

75%

► Debt does not count to

Accompanying country debt.

measures

• Structural and fiscal

...

reforms Funding by the ECB –

Italy

Spain

Portugal

France

Germany

• Limits on new very long period of time.

indebtedness Mutual understanding that

• Measures to reduce debt will be grandfathered

Roll-in of government debt private debt LT

of 75% of GDP per country

< 60% of GDP

Remaining debt on

country-level > Manageable

Source: Eurostat; bto analysisJust retire the QE debt?

» Instead of selling the debt back

into the market, the BoE can retire

the debt. At a stroke, £325bn of UK

» After buying government debt disappears. If the

£325B of debt US follows suit, about $1.5T of US

from the market, government debt will be retired.«

the public sector

(the Treasury) is

paying interest to » The main obstacle to retiring the debt lies with

itself (the BoE) on the markets and credit rating agencies. They

debt that it owes may see this as a slide towards Weimar Republic

to itself.« economics: monetary financing of government

debt by printing money. Consequently, both the

BoE and the Treasury cannot be seen to advocate

retiring QE-acquired debt at this stage.«

69CORONOMICS – the new economic order

Weak recovery from the financial crisis

Fragile financial system

Mother of all recessions

Central Banks go “all-in”

Eurozone fundamentally ill

How to deal with too much debt?

A bold proposal for the Euro

Coronomics for GermanyDie schwarze Null ist ...

• keine echte Leistung, da sie Mario Draghi, der EZB und damit vor allem

der nach wie vor ungelösten Eurokrise zu verdanken ist (Zinsersparnis!).

• eine große Dummheit, weil sie die Ersparnisse der Deutschen in das

Ausland treibt, wo sie deutlich schlechter angelegt sind.

• eine Lüge, weil in Wirklichkeit die Staatsschulden explodiert sind, weil die

Politiker immer mehr Leistungsversprechen für die Zukunft abgegeben

haben (in Gesetze gegossen!), für die aber keine Rückstellungen gebildet

wurden. Würde der Staat wie ein Unternehmen bilanzieren, würde man

das sofort an steigenden Lasten sehen.Implizite Schulden von fast 100 Prozent des BIP

825

Das EU-Nachhaltigkeitsranking 2016 Nachhaltigkeitslücke 765 788

(in Prozent des BIP, Basisjahr 2015) Explizite Schulden 22

Implizite Schulden

603 79

100

549

458

432 106

381 390 83

311 356

331 337

249 254 256 266 272 64 108 803

38

199 89 665 710

107 109 135 147

161 179 85 64 65

40 43 177 466 497

62 86 87 96 369 351

39 51 44 273 291

343 301

39 53

26 75 71 214 169 170 229 259

132 129 155 164 153

10 87 36 22 83 61 90 128

18

29 16 40 -25

-48

Malta

Zypern

Bulgarien

Slowenien

Ungarn

Deutschland

Frankreich

Estland

UK

Kroatien

Slowakei

Griechenland

Dänemark

Belgien

Lettland

EU28

Schweden

Niederlande

Finnland

Luxemburg

Tschechien

Irland

Polen

Litauen

Österreich

Rumänien

Spanien

Italien

Portugal

Quelle: Stiftung MarktwirtschaftThank you for

your attention.

www.think-beyondtheobvious.com

DR. DANIEL STELTER ·Jetzt neu: der

bto-Podcast

Jeden Sonntag 9 Uhr

auf der bto-Homepage

oder in Ihrer Player-App:

Apple Podcasts · Deezer ·

Soundcloud · Spotify

www.coronomics.deYou can also read