Portfolio Management Diary - Dec 2020 Kotak Special Situations Value Investment Approach - Kotak Mutual Fund

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Portfolio Management Diary – Dec 2020

Kotak Special Situations Value

Investment Approach

1

2

Focus On Key Themes In Portfolio - Domestic Revival India is becoming ready for its mega vaccine rollout after saying goodbye to a 2020, a year everyone would like to forget. If there was ever and unanticipated, high impact event, which shook the world, it was the Covid pandemic which had its origins in Wuhan, China. This Black Swan event shook global markets with lockdowns becoming the norm across the globe. In response to the pandemic, Central Banks undertook Monetary and Fiscal measures to pump liquidity into the system and support ailing households and businesses. On the medical front a concerted & joint effort was put in place to develop a vaccine. As the year ended there are at least 6 vaccines which are believed to be efficacious. The roll out of these vaccines would give some succor to the global markets regarding a pickup in demand in CY21. In order to play the demand recovery, we are focusing on the following themes in our portfolio. Domestic Revival The propensity of households to save appears to have risen significantly during the pandemic. Households have been unable to consume up to normal levels and have raised their precautionary savings. In the first three quarters of FY20, household financial savings stood at between ₹3.3-4.3-lakh crore and went up to ₹5.32-lakh crore in the fourth quarter. Owing to seasonal factors, household financial savings generally peak in the fourth quarter but moderate in the first quarter. However, in the April-June quarter this year, household financial savings shot up to ₹8.16-lakh crore. Flow of financial assets increased to ₹8.27-lakh crore in the June quarter, more than double the level seen in the same quarter last year (₹3.9-lakh crore) and up from ₹7.1-lakh crore in the March quarter. On the other hand, flow of financial liabilities shrunk to ₹11,000 crore in the June quarter, from ₹1.8-lakh crore in the March quarter. Note: The names mentioned in this note are for reference only, actual portfolio may differ as per fund manager’s discretion and the underlying stocks mentioned in the note does not guarantee future performance/return. Source: The Hindu Business Line 3

Domestic Revival

According to the RBI report, the increase in household financial assets was led by significant increase in the households’ holdings of mutual

funds, insurance products and currency.

There are considerable savings on account of not opting for Travel & Tourism, curtailment of entertainment, etc. Since the good news on the

vaccine front is already making headlines, the trend is visible through the increased consumption numbers across sectors, for instance..

• Auto industry is expected to post a double digit recovery in FY 22 after their de-growth in last couple of years.

• Auto sales recorded 17% increase YOY in Sep 2020 quarter and is expected to be with around 14% increase in Dec 2020 quarter.

• As per Knight Frank India, Housing sales jump 67% YoY in Mumbai in Nov 2020.

• Domestic air travel back to 65% of pre-Corona times as per Indian Civil Aviation Department in Nov 2020.

• A surge in hotel bookings has been recorded in many tourist destinations across Maharashtra, seen as a silver lining to a bleak year for

hospitality.

The portfolio is positioned in the following sectors/ companies to take advantage of this trend.

• Automobile cos. like Motherson Sumi, Carborundum

• Real Estate and Building Material Companies like Oberoi Realty, APL Apollo Tubes, Century Ply & Sheela Foam

• Travel & Tourism plays like VIP Industries

• Infrastructure and Construction businesses like Kalpataru Power and RVNL

• FMCG and Agriculture oriented plays like Kaveri Seeds, Balrampur Chini and KRBL Ltd

• Financials like HDFC, ICICI Bank, City Union Bank

Note: The names mentioned in this note are for reference only, actual portfolio may differ as per fund manager’s discretion and the underlying stocks mentioned

4

in the note does not guarantee future performance/return. Source: KIE, Internal

China + 1 Theme The US-trade tension along with Covid disruption has catalyzed diversification of supply chains away from China. The objective of such a diversification is to supplement current supply lines from China. The Indian government is mindful of this global trend and has put in place multiple incentives to attract businesses toward India. For instance, implementation of far reaching reforms like GST, IBC, Cut in Corporate tax rates (17% for setting up new manufacturing facilities) & recent Production Linked Incentive schemes in sectors like electronics, durables, chemicals, pharmaceuticals, etc. are expected to make India an attractive investment destination. Businesses in these sectors are witnessing enhanced enquiries and order inflows. Companies are gearing up to take advantage of this prospective order inflow by adding to capacities and R&D Capabilities. For instance Deepak Nitrite, a portfolio company, has given guidance of Rs 400 Cr capital expenditure in FY21 and a larger number in FY22. Additionally it will be setting up one more R&D center to undertake cutting edge research in developing value added products. Deepak Nitrite has over the years built its business on two key principles, 1) Import Substitution, 2) Backward Integration. These two principles are helping the company gain contract research and manufacturing (CRAMs) business since marquis customers are seeking backward integrated suppliers to ensure price stability. Similarly SRF Ltd, another portfolio company, has indicated that growth in Specialty Chemicals segment will sustain at 20-25% levels for the ensuing few years. The company is looking to invest Rs 1,600-1,800 Cr in building capacities to capture future growth opportunities. Despite the Covid led lockdowns, the company has raised its revenue guidance for FY21 to 25%. Note: The names mentioned in this note are for reference only, actual portfolio may differ as per fund manager’s discretion and the underlying stocks mentioned in the note does not guarantee future performance/return. Source: Internal 5

Outsourcing And Technology Revenue trajectory of Indian IT companies is expected to witness sharp mean reversal, as enterprises embrace Digital to combat Covid-19 triggered disruption. Agile Indian IT companies quickly adapted to changing needs of enterprises. The deep entrenched relationship with clients and Work From Home have reinforced outsourcing/offshoring model. The lockdowns had near-term impact on IT services companies due to lower volumes and pricing (select verticals). Though the economies are gradually reopening, the pandemic risk remains. Hence, remote working and virtual customer engagements are new normal not only for IT services business, but also for client businesses. Steady improvement in deal closures, revenue tailwind, and margin resilience for Indian IT is likely going forward. Indian IT companies command 35-40% market share in application maintenance in terms of value, making them critical for digital transformation journey of any large enterprise. TCS conducted a survey of over 300 large enterprises in North America, Europe & Asia. Even though revenues of 68 of the companies declined, 90 of them would either “maintain or increase” IT budgets. The companies’ priorities for IT spending were (in order): collaborative technologies, cyber security, cloud-native technologies and advanced analytics. Good demand was seen for business initiatives in end-to-end customer experience. Companies have also been trying to use AI and analytics to improve customer experience; 24 of them have already deployed such measures; 39 of them are developing them. Lastly, automation for core businesses is also seeing good traction. We anticipate demand to remain strong in the Outsourcing & Technology space and are participating in this trend through companies like Tech Mahindra & Oracle Financial Services Software Ltd. With investments in 5G technology likely to pick up over the next few years, Tech Mahindra will be a key beneficiary. Oracle Financial offers Core Banking solutions and an integrated Cloud service. The company’s services are likely to witness tailwinds with remote banking and an integrated customer experience become critical in today’s banking environment. Note: The names mentioned in this note are for reference only, actual portfolio may differ as per fund manager’s discretion and the underlying stocks mentioned in the note does not guarantee future performance/return. Source: Internal 6

Global Economy

7

Global Economy Has Rebounded Strongly

Citi Economic Surprise Index* (global)

*The CESI compares economic data against economists expectation , rising when the exceeds consensus estimates and falling when the data are below estimates

Source: Refinitv 8

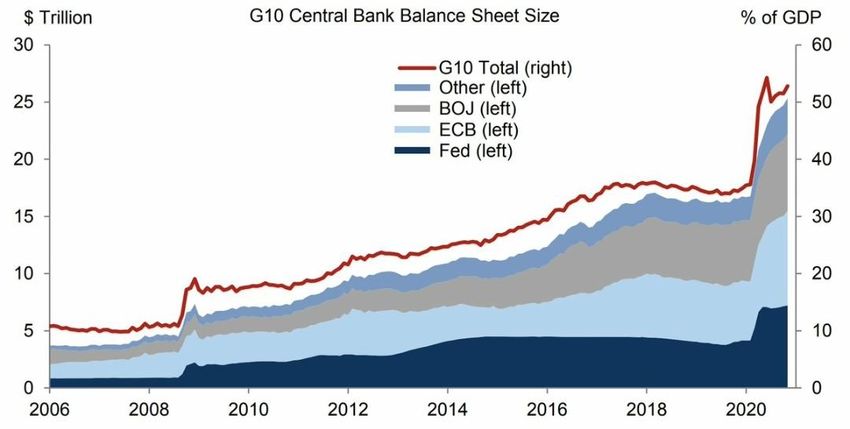

Record Money Printing By Central Banks

9

Source: Goldman Sachs Global Investment Research

Excess Liquidity Supports Global Equities Source: Refinitiv, Credit Suisseresearch 10

Record Debt Now Trades At Negative Yield

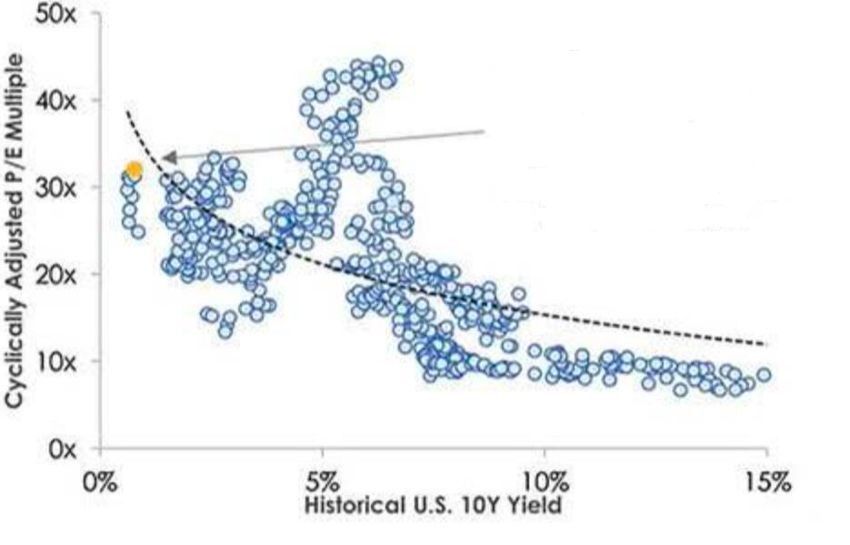

11Low Interest Rates Support Equity Valuations

Equity valuations will remain a big part of the

market narrative in 1H21. However, history

indicates today’s valuation are supported by

historically low interest rates

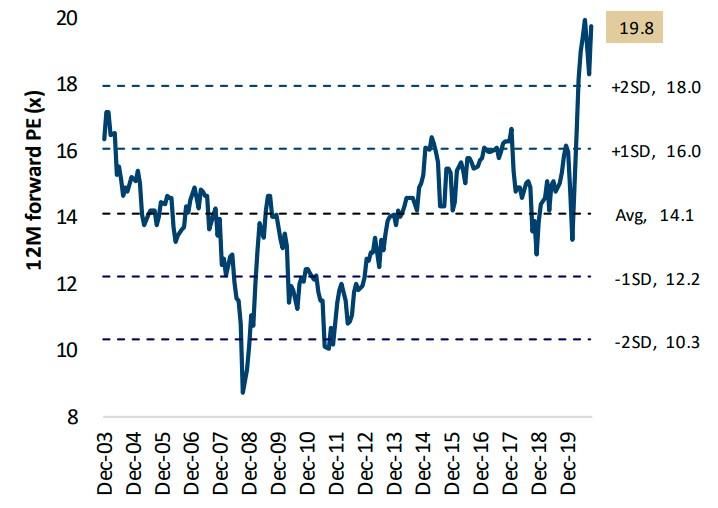

Source: Market Desk Research, Yale / Robert Shiler 12 12Global Valuations At Elevated Levels After A Sharp Rerating

MSCI AC World – 12-month forward PE band

Source: Jefferies, FactSet, As on Nov 2020 13Big Becoming Bigger Source: Bloomberg 14

lndian Economy

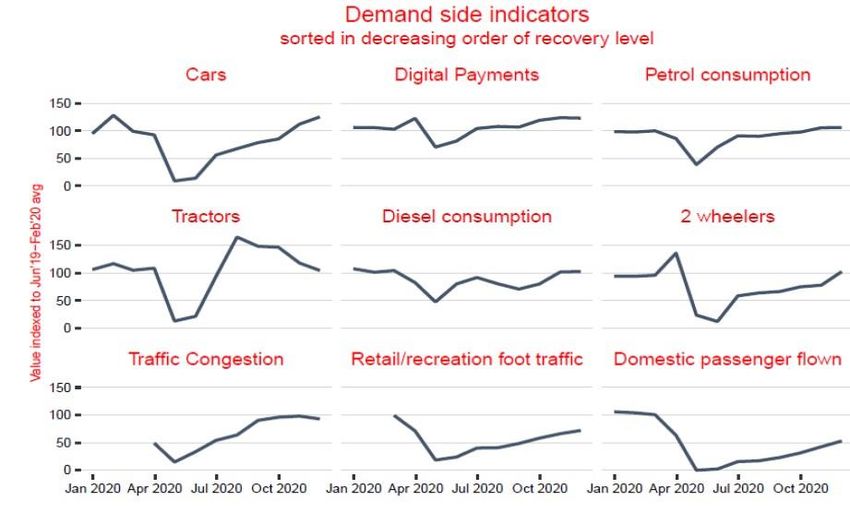

15Activity Tracker: India : Majority Of Demand Side Indicators Showing Improving Trends Source: CMIE, RBI, Vahan, UBS 16

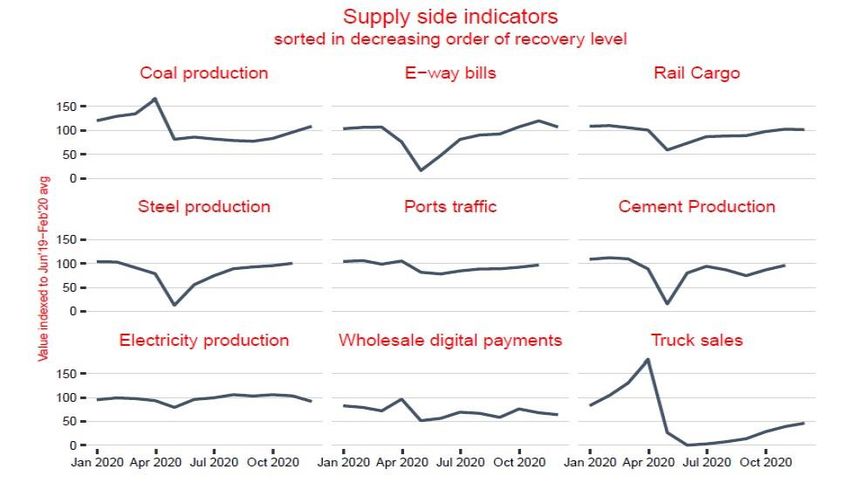

Activity Tracker: India :Supply Side Indicators Also Showing Improving Trends Source: CMIE, RBI, GSTN, Vahan, UBS 17

Recovery Is Getting Broad Based

18

18Economy Back In Green Red- Negative, Amber-Watch, Blue-Neutral, Green-Positive; Source: Nirmal Bang Institutional Equities Research, Google-mobility report, CMIE, Reserve Bank of India, Government of India, CEIC,Bloomberg. 19

Economic Normalisation Continues Apace Source: Google, Apple, CMIE, Bloomberg and Nomura Global Economics 20

Record High GST Collections Source: Ministry of Finance, moneycontrol.com 21

Manufacturing PMI Shows Momentum Holding Up

Manufacturing momentum stabilizes in Dec Services could show sequential improvement

Source: CEIC, Bloomberg, Markit

22Real Estate Should Support Economic Recovery

Affordability levels at all-time high Mortgage rates have fallen to record lows

Source: SBI, HDFC, Jefferies Source: The BLOOMBERG PROFESSIONALTM service, Credit Suisse estimates

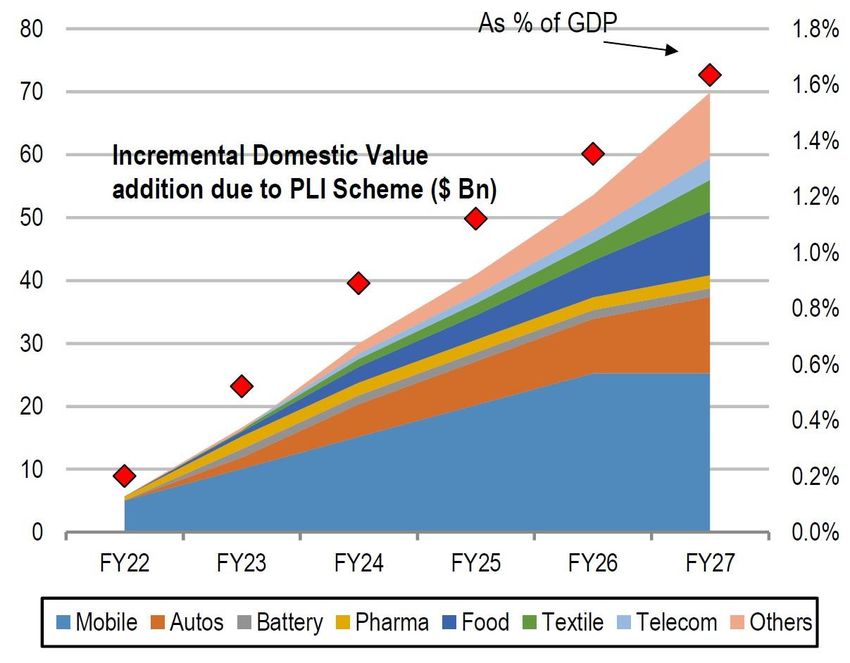

23PLI Schemes Can Add 1.6% To FY27 GDP Source: RAVE, Credit Suisseestimates 24

Rabi Season Sowing Strong Growth Reservoir levels higher in central and southern India Rabi sowing strong for wheat, pulses, and oilseeds Source: CEIC, IMD, Agricoop , Axis Capital 25

Centre’s 2H Spending Is Likely To Grow Vs Fall In 1H

26

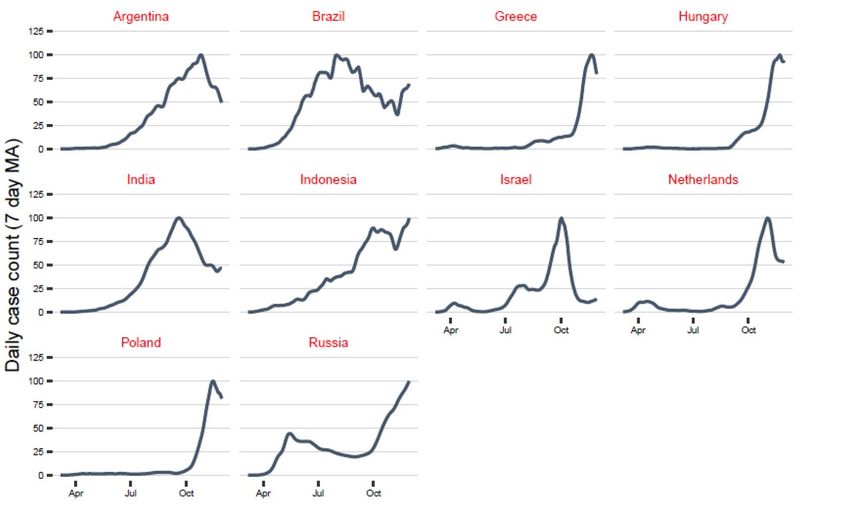

Source: CGA, Credit Suisse estimatesIndia Has Clearly Passed Peak On Daily Covid Case Counts;

Risk Of Second Wave Remains

Source: Bloomberg, Datastream, UBS Estimates, As on Nov 2020

27Vaccination Will Begun In 1 Q CY 21

28Budget Has Raised Expectations

29Unemployment Is High

CMIE Series of Unemployment : Unemployment Rate : 30 day moving Unemployment Rate 4th Jan

Unemployment rate (UER)(>=15) average (%) 2021

Source: CMIE

30Jobs Demanded Under MGNREGA Remain High

Employment demanded by persons under MGNREGA (inmn)

Source: CMIE, Kotak Economics Research 31Equity Markets

32Rising Ownership Of FII’s In Indian Equities Source: CMIE, Bloomberg, UBS India 33

$1 Trillion Could Flow Into The Stock Market In 2021

Change in flows per year in $bn.

Source: J.P. Morgan 34EM Equities Are The Most Preferred Asset Class Source: BofA Securities fund managers survey 35

India Is Attractive Destination For FPI Flows

30.0 12 Months FPI Flows (Dec’ 19 to Dec’ 20) USD Bn

25.0 23.0

20.0

15.0

10.0

5.0

0.0

-5.0 India Philippines Indonesia Malaysia South Thailand Brazil Taiwan South

-2.5 -3.2

Africa Korea

-10.0 -5.8

-7.4 -8.3 -8.5

-15.0

-16.2

-20.0

-20.1

-25.0

Source: Axis Capital 36Sept 20 Results Were Above Expectations

37

Source: BloombergEarnings Upgrades After 23 Quarters Of Downgrade

Consensus Nifty EPS growth estimates

Source: Credit Suisse 38Earnings Growth Likely To Rebound Strongly

`

Source: Bloomberg estimates, Bernstein analysis 39Nifty Trading Rich Relative To Its Own History But Not Relative

To EM Peers

Nifty trading at rich valuations on 12m fwd PE: India's premium to EM at 5 year mean

Source: Datastream, Bloomberg, UBS 40Small Cap Still Below Its Peak Of 2018

Price as on

Indices Absolute Returns

15/01/2018 31/12/2020

Nifty 50 10742 13982 30.2%

Nifty Midcap 100 21697 20843 -3.9%

Nifty Smallcap 100 9580 7088 -26.0%

Source: Capital Line

41Nifty At Lifetime High Levels Due To Few Stocks –

But Mid & Small Caps Still Below January 2018 Levels

27,000

Nifty-50 (TRI) Top-15 Stock (Re-based) Next-35 Stock (Re-based)

24,000 24,575

Top 15 stocks delivered return of 75%

21,000

19,494

18,000 Index delivered 39% return

15,000 14,790

14,072

12,000

Next 35 stocks delivered return of 5%

9,000

Return (%)

Index Name (Dec 2017 to Dec 2020) Nifty Index TRI Nifty Midcap 100 TRI Nifty Small Cap 100 TRI

145 Nifty 50 TRI 38.5 139

125 Nifty Midcap 100 TRI 2.1

Nifty Smallcap 100 TRI -19.0

105 102

85 81

65

Rebased

45 to 100

25

Jun-18

Jun-19

Aug-20

Dec-17

Feb-18

Sep-18

Feb-19

Aug-19

Sep-19

Oct-18

Dec-18

Dec-19

Oct-20

Dec-20

Apr-20

Mar-18

May-18

Jul-18

Jan-19

May-19

Jan-20

Mar-20

May-20

Jul-20

Nov-19

Nov-20

Apr-19

Source: Motilal Oswal & internal analysis Past performance may or may not be sustained in future. 42Performance Across Market Cap

Performance as on 31st Dec 2020 Sectoral Performance CY20 YTD (%)

30 61%

55%

21.9 21.5

20

14.9

12.0

9.9 9.2 8.9

10 8.6 22% 21%

7.8 7.8

5.7 5.6 15% 16%

4.6 13% 12%

11%

6% 5% 4%

0

(0.5)

-3% -3%

-9%

(10) (8.0)

Secvices

Bank

Financials

IT Services

Metals

Private Banks

Smallcap 100

Auto

Energy

FMCG

Realty

NIFTY 50

Pharma

Media

Midcap 100

Nifty-50 Nifty Midcap 100 NSE SmallCap 100

1m returns 1y returns 3 yr CAGR 5 yr CAGR 10 yr CAGR

Source: Bloomberg, Axis Capital. As on 31st Dec 2020. Past Performance may or may not sustain in the future 43Corrections Are Part Of Market Cycle

Nifty -10% correction from 6 month highs

Source: Bloomberg, As on Dec 2020 44Market Surprises Even The Experts

In March / April 2020 In November 2020

45 45Market Cap-to-GDP Ratio – Above Long Term Average

Market cap-to-GDP ratio: Market rebound brings ratio above long term average

103 Average of 75% for the period

95 98

88

82 83 83

81 79 79

71

66 69

64

55 56

52

FY09

FY05

FY06

FY07

FY08

FY10

FY11

FY12

FY13

FY14

FY15

FY16

FY17

FY18

FY19

FY20

FY21E

OW Equities =Ratio Below Historical Lows Neutral Equities = Ratio at Historical Average

Source: Motilal Oswal 46Disclaimer

Investments in securities are subject to market risk and there is no assurance or guarantee of the objectives of the Portfolio being achieved or

safety of corpus. Past performance does not guarantee future performance. The performance related information in the presentation is not

verified by SEBI. Investors must keep in mind that the aforementioned statements/presentation cannot disclose all the risks and

characteristics. Investors are requested to read and understand the investment strategy, and take into consideration all the risk factors

including their financial condition, suitability to risk return profile, and the like and take professional advice before investing. Opinions

expressed are our current opinions as of the date appearing on this material only.

These materials are not intended for distribution to or use by any person in any jurisdiction where such distribution would be contrary to local

law or regulation. The distribution of this document in certain jurisdictions may be restricted or totally prohibited and accordingly, persons

who come into possession of this document are required to inform themselves about, and to observe, any such restrictions

We have reviewed the document though its accuracy or completeness cannot be guaranteed. Neither the company, nor any person connected

with it, accepts any liability arising from the use of this document. The recipients of this material should rely on their own investigations and

take their own independent professional advice. While we endeavor to update on a reasonable basis the information discussed in this

material, there may be regulatory, compliance, or other reasons that prevent us from doing so. Investors and others are cautioned that any

forward - looking statements are not predictions and may be subject to change without notice.

Statutory Details: Portfolio Manager: Kotak Mahindra Asset Management Company Ltd. SEBI Reg No: INP000000837- Registered Office: 27

BKC, C-27, G Block, Bandra Kurla Complex, Bandra (E), Mumbai - 400 051, Principal Place of Business: 2nd Floor, 12 BKC, Plot No. C-12, ‘G’

Block, Bandra Kurla Complex, Bandra East, Mumbai – 400 051,India. Address of correspondence:6th Floor Kotak Towers, Building No 21

Infinity Park, Off W. E. Highway, Gen A K. Vaidya Marg, Malad (E), Mumbai 400097. - Contact details:02266056825

47You can also read