PREDICTION OF THE INDIAN STOCK INDEX USING NEURAL NETWORKS

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Jharkhand Journal of Development and Management Studies

XISS, Ranchi, Vol. 16, No.1, March 2018, pp. 7609-7621

PREDICTION OF THE INDIAN STOCK INDEX USING

NEURAL NETWORKS

Sitaram Pandey1 & Amitava Samanta2

Stock prices prediction is an issue of interest in stock markets.

Many prediction techniques have been reported in stock forecasting.

Now a days, neural networks are viewed as one of the most suitable

techniques. In this study also, an experiment on the forecasting of

the nifty index of national stock exchange was conducted by using

feed forward back propagation neural networks. The local and global

fac to rs influencing the natio nal sto ck mark et we re used in

developing the models that includes gold prices, dollar-rupee

exchange rates & nifty volume. Three years’ historical data were

used to train and test the models. Four suitable neural network

models identified by this research are a four layer neural network.

But it was found through performance measure MSE (Mean Square

Error) that movement of nifty index is insensitive to gold prices’

fluctuations & dollar exchange rate fluctuations.

Keywords : Artificial Neural Network, Nifty Index, Stock Prediction,

Performance measures

Introduction

Prediction of future trends of any financial market is still a most

lucrative field of research. Here, we are focusing our research on Indian

stock market. There are innumerable numbers of researches based on

different models from fundamental analysis to machine learning

techniques are available globally on this topic but fewer in Indian

context. Prediction in the stock market is the need of all the stock

traders to take informed decisions in trading of stocks. Many

researchers have concluded that Indian stock market does not follow

efficient market hypothesis (EMH) which specifies that there is a room

for stock market forecasting. While the debate on the various issues

related to efficiency of market, predictive models, tools etc. is ongoing,

this encourages various researchers to seek better model for stock

prediction. Techniques of prediction vary greatly based on the availability

of data, quality of data, requirement specification, and the underlying

assumptions used.

There are various linear and non-linear models to describe the

behavior of time series but their success rate is diminishing in predicting

the financial markets, though these techniques are statistically powerful.

1

Assistant Professor, Department of MBA, Cambridge Institute of Technology,

Ranchi Jharkhand. Phone No. 7858882626, Mail Id : spandey1203@gmail.com

2

Associate Professor, Department of Commerce & Management, Vinoba Bhave

University, Hazaribag, Jharkhand. Phone Number: 09431795999, Email ID:

dramitava1@yahoo.com

7609

7610 Pandey & Samanta

As we know, stock markets are very unpredictable so their high

frequency data are highly time-variant and in non-linear pattern. It is

a challenging task to predict future prices of a stock based on past

experiences. Bollerslev (1986) has given a solution in the form of general

autoregressive conditional heteroscedasticity (GARCH) model which has

solved the problem of time-series data to a greater extent. This model

was proven as one of the strongest weapon since it was invented for the

analysis of time-series data and successfully has been used for last 20

years. This model has a capacity to capture all the irregularities of

economic time series data but these days the model has started losing

its shine now. Now, neural networks has started replacing these models.

Now a days, neural networks are regarded as more suitable for stock

prediction than other techniques. Unlike other techniques that construct

functional forms to represent relationships of data, neural networks

are able to learn patterns of relationship from data itself. In modern

quantitative and empirical finance, Artificial neural networks (ANN)

are proven as one of the most powerful tool and have emerged as a

significant statistical modeling technique. The ANN models are

emerging technology that has capacity to detect the underlying

functional relations within a set of data and perform data analysis in

applications such as pattern recognition, prediction, classification,

modeling, evaluation and control. Therefore, a variety of neural network

models have been created. Several features of ANN model making it

successful now a day. Firstly, it can handle non-linear data and able to

model nonlinear systems without prior knowledge of relationship

between the input and output variables. The back propagation neural

network is a popular neural network model; there are many successful

applications for back propagation neural networks in science,

engineering and finance. Secondly, ANN models are capable of handling

the limitations of time series data.

Stock market is considered as the mirror of the economy whether

developed or developing. It is now considered as a barometer to measure

the economic condition of a country because every major change in

economy is reflected in the prices of share. The rise and fall in the

share prices indicates the boom or recession cycle of the economy. Now,

it has been proved by various researchers that a well regulated stock

market renders various economic services to their people. Emerging

stock markets have recently been of great importance to the worldwide

investment community. So, India is considered as one of the fastest

emerging markets in the world due to its established stock exchanges

with a long history of organized trading in securities. Over the last few

years, there has been a rapid change in the Indian capital market in

terms of technology, trading styles & settlement processes. According

to the recent survey, there are around 28 emerging markets in the

Prediction of the Indian stock index using neural networks 7611

world out of which India ranks in the second place. Currently, India is

the 4th largest economic system in the world in terms of the purchasing

power parity. In this research, we are basically focusing on the behavior

of share prices which are governed by the various rational, emotional,

economic, geographical and psychological factors.

In this study, we are taking the S&P CNX Nifty as our national

stock index for study, it is a stock market index and benchmark index

for Indian equity market. The S&P CNX Nifty covers 22 sectors of the

Indian economy and offers investment managers exposure to the Indian

market in one portfolio. The S&P CNX Nifty stocks represent about

67.27% of the free float market capitalization of the stocks listed

at National Stock Exchange (NSE) as on September 30, 2017.

This study investigated the Indian stock market using feed

forward back propagation neural networks. It aimed to find suitable

neural network models for the prediction of the next day of the S&P

CNX Nifty index by applying three time series data, expected to be the

factors influencing the stock market, to the models created. The rest of

the paper is organized as follows: Section 2 examines the literature

review. Section 3 presents the objective of the study. Section 4 discusses

the variables, data sources, research design & methodology, ANN &

performances measures. Section 5 presents the data analysis &

discussion and Section 6 summarizes and concludes.

Artificial Neural Network

According to Christos Stergiou and Dimitrios Siganos, Artificial neural

network (ANN) is an information processing model where the

constituents called neurons, process the information and is motivated

by biological nervous system of human brain. The key element of this

model is its unique method of information processing system. It is made

up of several numbers of interconnected processing constituents working

together to solve specific problems. As per Burgund and Marsolek (1997),

in Advances in Psychology, any ANN can be thought of as a set of

interconnected units broadly categorized into three layers of processing

units. These three layers are the input layer, the hidden layer and the

output layer. Inputs are fed into the input layer, and its weighted outputs

are passed onto the hidden layer . The input signal passes through the

network in the forward direction. These processing units can be referred

as nodes. The directed graphs consists of nodes and each nodes are

connected to perform some basic calculations and each connection

carries a signal from one node to another labeled by some unique number

termed as weight that modulate signal. Here in this paper, we are

taking into account feed forward networks , in which connection is

forwarded from layer 0 to layer 1 , layer 1 to layer 2 & layer 2 to layer

3. Each layer consists of nodes. The connection is represented by a7612 Pandey & Samanta

sequence of numbers indicating number of nodes in each layer. For

example, 3-3-2-1 feed forward network; it indicates three nodes in the

input layer (layer 0), three nodes in the first hidden layer (layer 1) , two

nodes in second hidden layer (layer 2) , and two nodes in the output

layer (layer 3). Here back propagation algorithm (Rumelhart, Hinton

& McClellnad, 1986) is used in layered feed-forward ANNs. The network

is a multi-layer perception that contains at least one hidden layer along

with input and output layers.

Review of literature

Bashambu, Sikka & Negi (2018) in their paper applied machine learning

techniques on the past data to predict the movement of the stock prices

and found that although neural networks are not perfect in prediction

but they are outperforming all other methods.

Hafezi, Shahrabi & Hadavandi (2015) in their research proposed a new

intelligent model in a multi-agent framework called bat-neural network

multi-agent system (BNNMAS) to predict stock prices of DAX. The

results have shown that BNNMAS is better than the genetic algorithm

neural network (GANN) and some standard models like generalized

regression neural network (GRNN), etc.

Laboissiere, Fernandes & Lage (2015) through their research

proposed a methodology that forecasts the maximum and minimum

day stock prices of three Brazilian power distribution companies and

actual prediction was carried out by ANNs whose performances were

evaluated through MAE, MAPE & RMSE calculations and found results

effective and helpful for investors.

Adebiyi, Adewumi & Ayo (2014) in their paper “comparison of

ARIMA and artificial neural networks models for stock price prediction”

examined the forecasting performance of ARIMA and artificial neural

networks model with data of NYSE and concluded superiority of neural

networks model over ARIMA model.

Al-Radaideh, Assaf, & Alnagi (2013) used data mining techniques

for prediction of stock prices. In their study, they tried to help the

investors in the stock market to decide the better timing for buying or

selling stocks on the basis of information obtained from the historical

prices of stocks. Their decisions based on decision tree classifier, which

is based on CRISP-DM methodology, are used over real historical data

of major companies listed in Amman Stock Exchange (ASE).

Niaki & Hoseinzade (2013) have tried to forecast S&P 500 index

using artificial neural networks and design of experiments. The results

of employed methodology show that the ANN is able to forecast the

daily direction of S&P 500 significantly better than the traditional logitPrediction of the Indian stock index using neural networks 7613

model and ANN could significantly improve the trading profit as

compared with the buy-and-hold strategy.

Sureshkumar & Elango (2012) analyzed the performance of model

of stock price prediction using artificial neural network. They found

that multi layer perception (MLP) architecture with back propagation

algorithm has the ability to predict with greater accuracy than other

neural network algorithms. This would help the investor to analyze

better in business decisions such as buy or sell a stock.

Dase, Pawar & Daspute (2011) elaborated methodologies for

prediction of stock market and focused on an artificial neural network

and found that ANN model was more useful for stock market prediction.

Artificial neural network, a computing system containing many simple

non-linear computing units as neurons interconnected by links, is a

well-tested method for financial analysis on the stock market.

Dase & Pawar (2010) used artificial neural network model (ANN)

for stock market predictions and found that prediction of stock index

with ANN model is easier and more suitable than traditional time series

analysis. A neural network has the ability to extract useful information

from large set of data.

Ahangar, Yahyazadehfar, & Pournaghshband (2010) in their

research paper “The comparison of methods artificial neural network

with linear regression using specific variables for prediction stock price

in Tehran stock exchange” considered 10 macro economic variables

and 30 financial variables to estimate the stock price using Independent

components analysis (ICA) and later they found that artificial neural

network method is more efficient than linear regression method.

Ganatr & Kosta (2010) focused to build neural network for stock

market predictions. Authors used R tool to implement the neural

network with closing price, turnover, global indices, interest rate, and

inflation as a neural network input. Authors also proposed to include

other indicator like news, currency rate and crude price as input to the

neural network. Subsequently, an attempt was made to build and

evaluate a neural network with different network parameters and also

with technical and fundamental data and found that the price prediction

proves to be successful.

Dutta, Jha, Laha & Mohan (2006) have used artificial neural

network models for forecasting stock price index in the Bombay stock

exchange. They study the efficacy of ANN in BSE Sensex weekly closing

values. They had developed two networks with three hidden layers for

the purpose of this study. The root mean square error (RMSE) and

mean absolute error (MAE) are chosen as indicators of performance of

the networks.7614 Pandey & Samanta

Thenmozhi (2006) has applied neural network models to predict

the daily returns of the BSE (Bombay Stock Exchange) Sensex.

Multilayer perception network is used to build the daily return’s model

and the network is trained using Error Back Propagation algorithm. It

was found that the predictive power of the network model is influenced

by the previous day’s return than the first three-day’s inputs. The study

showed that satisfactory results can be achieved when applying neural

networks to predict the BSE Sensex.

Objectives of the study

The main objective of this study is to use neural networks prediction

tool to predict stock prices with more accuracy and to use performance

measures for their evaluation. The study makes an attempt to identify

extent of impact of various factors on stock prices through neural

networks. The study wants to help participants of the market to predict

the prices more accurately by reducing error percentage.

Data collection & methodology

The actual problem discussed in this paper is to forecast the Nifty index

of national stock exchange of India. For this purpose, we have used

available daily data of Nifty from the NSE beginning from 01 –January-

2015 to 31- December- 2017. For this study, we have taken data of

closing prices of three above mentioned years, Volume of Nifty, Data of

exchange rates & Gold prices of said years. In order to predict the stock

price, past data is necessary and it has been collected for the trading

days from 01 –January-2015 to 31- December- 2017. The historical

data was collected from different websites1,2,3.

The main task is to predict whether the price of nifty index will

be up or down tomorrow by using the historical values of the Nifty

index. In this research we have chosen three important dependent

variables which include gold prices, exchange rates of dollar-rupees &

Nifty volumes. The result of any neural network is mostly dependent

on the composition of the neural network. Intricacy of any neural

network depends on the level of task and accordingly hidden layers can

be added to the network to achieve the desired level of accuracy. The

software chosen in this paper for creating, training and testing the

networks is MATLAB Neural Network Toolbox, which has an extensive

capability in terms of creating and training different types of networks.

Input data variables & methodology

The two types of input variables can be used for stock market index

forecasting with neural networks. The first type of variables is related

to macroeconomic indicators such as GDP rate, Inflation, FDI, Currency

exchange rates, gold prices, developed market indicators etc, the otherPrediction of the Indian stock index using neural networks 7615

types of variables are market related indicators such as prices, dividends,

trading volume, turnover, etc. In this study we have used exchange

rates & gold prices as macroeconomic indicators and prices & volumes

as market indicators.

Input data was processed to achieve better predictive results in

the application of neural networks on financial time series. In this study,

data were collected and transformed through first differencing and

logarithmic transformation of the return variable.

As in the most other studies (Maciel & Ballini, 2010), in this

study also for neural networks the time series data was partitioned

into three different sets, first set for the training, second set for the

testing and the third set for the validation of networks and it is the

common practice to split dataset into three partitions with different

quantum of data set in different partitions to make the network more

robust. The training set is the largest set and it is used in the neural

networks to learn the patterns present in the data. The testing set

whose range vary up to 30% of the training set is used to figure out the

generalization capacity of estimated trained network. At last, validation

set should be of size that can evaluate a trained network efficiently and

this set should consist of most recent observations. Although validation

set uses past values to test the neural networks and to evaluate the

generalization capability of the model. In this work we have partitioned

data as follows: training set -70%, testing set -15% & validation set -

15%. The application of these three divided sets are as follows: Training

set was used to adjust the network to make it error free. Validation set

was used to measure network generalization and testing set was used

to measure the network performance during and after training. In this

model, random regression function was split to overcome over fit models.

Neural Network Structure

In neural network algorithm each independent variable that has been

processed is represented by its own input neurons. A two-layer-feed-

forward network, with sigmoid hidden and soft max output neurons,

can classify vectors arbitrarily well, given enough neurons in its hidden

layer. Tansig is used here as a neural transfer function. Transfer

functions calculate a layer’s output from its net input. This is

mathematically equivalent to tanh (N). N is the S-by-Q matrix of net

input vectors. The network will be trained with scaled conjugate gradient

back propagation. In the broadest sense, there are three main

requirements for any successful ANN model:

In-sample accuracy

The ability of the model to perform with new data.

Stability, consistency of the network output.7616 Pandey & Samanta

To ensure the above points are successfully met, a large number

of considerations need to be taken into account. Our tests included data

pre-processing techniques, the number of layers, the choice of activation

function, learning rate, training time and the number of hidden neurons.

After several combinations of experiments, the architecture was finalized

for all the main experiments. The goal is to use the least amount of

neurons which generate the best results for out-of-sample. A simple

approach was used in this paper based on starting with very small

number of neurons and training and testing the networks to a fixed

number of iterations. The hidden neurons are increased gradually until

the optimal number of neurons is found. There is no any rule of thumb

to find optimal number of neurons required in hidden layers. Here, it

was found through trial and error method for the minimum squared

error (MSE) and through test set. Every time a new input (or lagged

value of the same variable) was added, we started with 1 hidden neuron

and added one each time up to 10.

Performance measures

The ultimate goal of this study is to forecast the direction of the price,

since it is very difficult to correctly predict the magnitude of the price

for financial data. Hence, prediction of direction of nifty index is sufficient

to fulfill this goal. The success ratio for direction prediction (or the hit

rate) was considered.

h= (1)

z =1 if , > 0, and 0 otherwise.

Where: n is the sample size, +1 , +1 , are the value of the

target and the output at time t+1 consecutively.

The MSE (Mean squared error) is by far the most used metric for

ANN performance regardless of the network goal. Furthermore, the

correlation coefficient R and 2 was also used; as a measure of the

linear correlation between the forecasted value and the actual one. Mean

squared error was calculated. Finally, the information coefficient given

by equation 2 was used.

∑ =1( − )2

IC = (2)

∑ =1( − −1 )2

Where: y is the predicted value, and x is the actual value. This

ratio provides an indication of the prediction compared to the trivial

predictor based on the random walk, whereas IC >1 indicates poor

prediction, and IC < 1 means the prediction is better than the random

walk. The different neural network models were constructed by usingPrediction of the Indian stock index using neural networks 7617

the three input nodes in an input layer. Some models are shown in

table 1, where the first number is the number of nodes in the input

layer, the second number is the number of nodes in the first hidden

layer and so on. The last number is the node of the output layer, which

is 1.

Results & analysis

Starting from one lag up to 20 lagged value of the spot price was tested.

The results obtained from input transformed by equation (3) were very

poor and the hit rate was 46% for out-of-sample.

− −1

=( ) (3)

−

−2 −1 +

=( −2

) (4)

−

While the results generated by equation (4) was much better

around 60% (equation 4 contains 2 step differencing) the combination

of eq (3) & eq (4) as input with eq (4) alone as output seems to produce

much better results. For different combinations of data and parameters,

this performance curve varies. Training of the model stops either when

it reaches to the stated number of epochs (fig.1) or when Mean Squared

Error (MSE) is almost not improving after certain epochs. The circle in

the performance curve shows the best validation performance. The

following networks were trained to identify the best performing networks.

The networks trained and retrained using levenberg-marquardt and

scaled conjugate gradient. The first network is 3-3-1-1 which is trained

and retrained using levenberg-marquardt and scaled conjugate gradient.

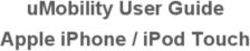

Fig-1. Performance curve of Primary Working Set Data of network 3-3-1-1

Source : Matlab7618 Pandey & Samanta

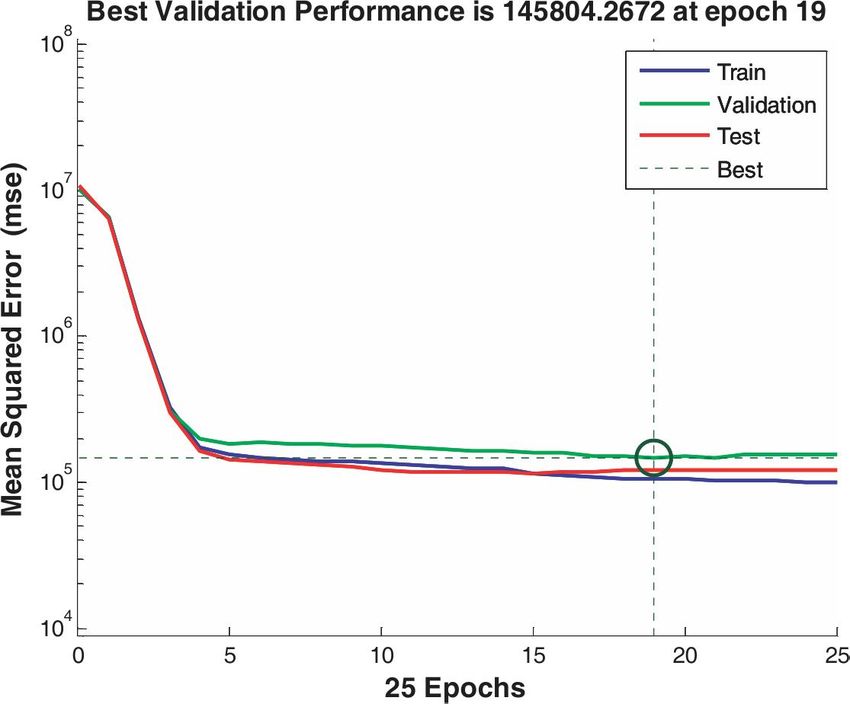

Next network is 3-7-1-1 which is also trained using above method.

Fig-2 : Performance curve of Primary Working Set Data of

network 3-7-1-1

Source : Matlab

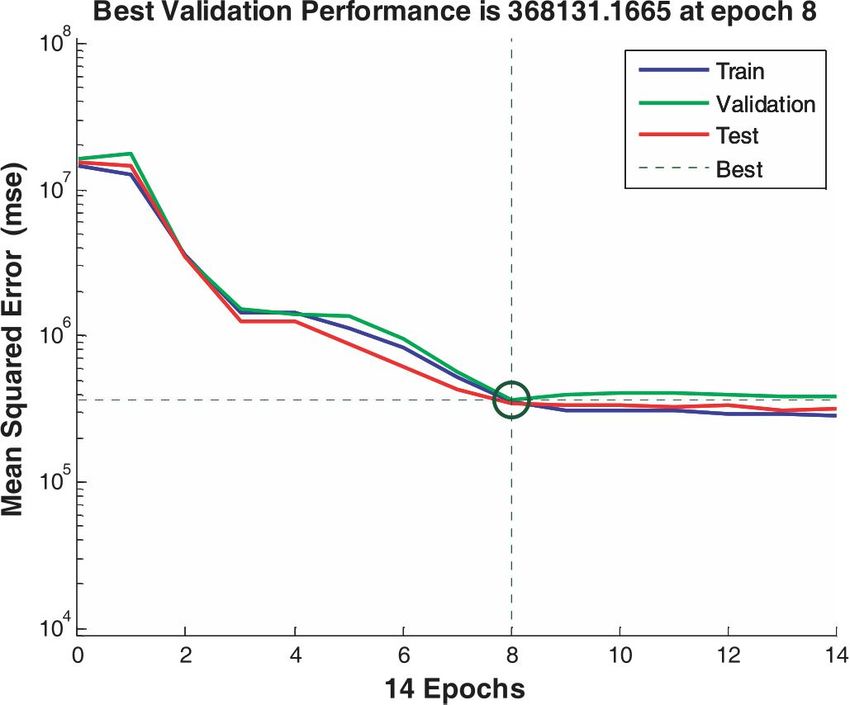

The other network is 3-10-1-1 trained as above.

Fig-3 : Performance curve of Primary Working Set Data of

network 3-10-1-1

Source : MatlabPrediction of the Indian stock index using neural networks 7619

Next network is 3-13-1-1 which is also trained by the same procedure.

Fig-4 : Performance curve of Primary Working Set Data of

network 3-13-1-1

Source : Matlab

The best model for four layered neural networks was 3-7-1-1.

The summary of performance measures of the nifty Index through

the network 3-7-1-1.

Metrics Samples MSE R2

Training 521 0.0002 0.21

Validation 111 0.0005 0.23

Testing 111 0.0007 0.19

Source : Matlab

The network structure for the benchmark consisted of four layers

feed forward with 7 hidden neurons and 0.01 learning rate. The network

was trained with Levenberg-Marquardt algorithm & scaled conjugate

gradient.

Conclusions

The study has presented the prediction of the Nifty index using multi

layer feed forward back propagation neural networks. The most suitable

network model for the Nifty index production is 3-7-1-1 but their

prediction performance measured by MSE is nil and correlation is also

found as nil. Thus this study supports that movement of Nifty index is

insensitive to gold prices’ fluctuations & dollar exchange rate

fluctuations.7620 Pandey & Samanta

REFERENCES

Adebiyi, A. A., Adewumi, A. O., & Ayo, C. K. (2014). Comparison of ARIMA and

artificial neural networks models for stock price prediction. Journal of

Applied Mathematics. Retrieved from file:///C:/Users/Welcome/Downloads/

614342.pdf

Ahangar, R. G., Yahyazadehfar, M., & Pournaghshband, H. (2010). The comparison

of methods artificial neural network with linear regression using specific

variables for prediction stock price in Tehran stock exchange. International

Journal of Computer Science and Information Security, IJCSIS, 7(2), 038-

046.

Al-Radaideh, Q. A., Assaf, A. A., & Alnagi, E. (2013). Predicting stock prices using

data mining technique s. In The Inter national Ar ab Confere nce on

Information Technology (ACIT’2013). Retrieved from http://acit2k.org/ACIT/

2013Proceedings/163.pdf

Bashambu, S., Sikka, A., & Negi, P. (2018). Stock price prediction using neural

networks. International Journal of Advance Research, Ideas and Innovations

in Technology, 4(1), 603-606.

Bollerslev, T. (1986). Generalized autoregressive conditional heteroskedasticity.

Journal of econometrics, 31(3), 307-327.

Burgund, E. D., & Marsolek, C. J. (1997). Case-specific priming in the right cerebral

hemisphere with a form-specific perceptual identification task. Brain and

Cognition, 35(2), 239-258.

Dase, R. K., & Pawar, D. D. (2010). Application of artificial neural network for stock

market predictions: A review of literature. International Journal of Machine

Intelligence, 2(2), 14-17.

Dase, R.K., Pawar, D. D., & Daspute, D.S. (2011). Methodologies for Prediction of

Stock Market: An Artificial Neural Network. International Journal of

Statistika and Mathematika, 1(1), 08-15.

Dutta, G., Jha, P., Laha, A. K., & Mohan, N. (2006). Artificial neural network

mo dels for for ecasting sto ck price index in the Bo mbay sto ck

exchange. Journal of Emerging Market Finance, 5(3), 283-295.

Ganatr, A., & Kosta, Y. P. (2010). Spiking back propagation multilayer neural

network design for predicting unpredictable stock market prices with time

ser ies analysis. Internatio nal Jour nal of Computer Theo ry and

Engineering, 2(6), 963.

Hafezi, R., Shahrabi, J., & Hadavandi, E. (2015). A bat-neural network multi-agent

system (BNNMAS) for stock price prediction: Case study of DAX stock

price. Applied Soft Computing, 29, 196-210.

Laboissiere, L. A., Fernandes, R. A., & Lage, G. G. (2015). Maximum and minimum

stock price forecasting of Brazilian power distribution companies based on

artificial neural networks. Applied Soft Computing, 35, 66-74.

Maciel, L.S., & Ballini, R.(2010). Neural networks applied to stock market forecasting:

An empirical analysis. Journal of the Brazilian Neural Network Society,

8(1), 3-22.

Niaki, S. T. A., & Hoseinzade, S. (2013). Forecasting S&P 500 index using artificial

neural networks and design o f experiments. Jo urnal o f Indus trial

Engineering International, 9(1), 1.

Rumelhart, D. E., Hinton, G. E., & McClelland, J. L. (1986). A general framework

for parallel distributed processing. In Jerome A. Feldman, Patrick J. Hayes

& David E. Rumelhart (Eds.), Parallel distributed processing: Explorations

in the mic rost ruct ure of cognitio n, 1(pp. 45-76). MA, USA: MIT

Press Cambridge.Prediction of the Indian stock index using neural networks 7621

Sureshkumar, K. K., & Elango, N. M. (2012). Performance analysis of stock price

prediction using artificial neural network. Global Journal of Computer

Science and Technology, 2(1). Retrieved from file:///C:/Users/Welcome/

Downloads/426-1-426-1-10-20150122.pdf

Thenmozhi, M. (2006). Forecasting stock index returns using neural networks. Delhi

Business Review, 7(2), 59-69.

Websites

1

https://www.nseindia.com/products/content/equities/indices/

historical_index_data.htm, retrieved on 20/01/2018

2

https://in.investing.com/commodities/gold-historical-data, retrieved on 20/01/2018

3

https://in.investing.com/currencies/usd-inr-historical-data, retrieved on 20/01/2018You can also read