COVERED BONDS INVESTOR PRESENTATION - JUNE, 2019 - Tatra banka

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

COVERED BONDS INVESTOR PRESENTATION JUNE, 2019

DISCLAIMER

The information and the opinions in this presentation have been prepared by Tatra banka, a.s. (Tatra banka) solely for general information purposes in

connection with a proposed offering of covered notes issued by Tatra banka (the Notes). This presentation and its contents are intended for information purposes

only and may not be reproduced in any form or further distributed to any other person or published, in whole or in part, for any purpose. Failure to comply with

this restriction may constitute a violation of applicable securities laws. Raiffeisen Bank International AG and other members of RBI group have not prepared or

approved this documents and have no liability in connection with this document or information therein or the Notes.

This presentation shall not constitute an offer to sell, or the solicitation of an offer to purchase or otherwise acquire the Notes or to enter into any legally binding

relationship with Tatra banka. This presentation is not for distribution in, nor does it constitute an offer of securities in any jurisdiction or an inducement to enter

into investment activity or any advice or recommendation with respect to the Notes. Specifically, the Notes have not been, and will not be, registered under the

United States Securities Act of 1933, as amended (the US Securities Act),or the securities laws of any state of the United States or other jurisdiction. The Notes

may not be offered or sold, directly or indirectly, within the United States or to, or for the account or benefit of U.S. Persons (as defined in Regulation S under the

US Securities Act) except pursuant to an exemption from, or in a transaction not subject to, the registration requirements of the US Securities Act.

This presentation is being directed only at persons having professional experience in matters relating to investments in financial instruments. This presentation

is not for distribution to retail customers (non-professional clients).

Any investment decision concerning the Notes should be made only on the basis of evaluation by each prospective investor of the base prospectus, all financial

and other information incorporated therein by reference, supplements to the base prospectus (if any) and relevant final terms of the Notes, each as published on

the website of Tatra banka: www.tatrabanka.sk.

Some information in this presentation has been obtained or is based on the publicly available sources. Information has been reproduced carefully, but has not

been independently reviewed and Tatra banka cannot guarantee accuracy, adequacy, correctness or completeness of such information. Accordingly, undue

reliance should not be placed on any such information contained in this presentation. All information and opinions contained in this presentation are provided as

at the date of this presentation and are subject to change without notice.

Page | 2

TATRA BANKA: PRESENTERS

Mag. Dr. JOHANNES SCHUSTER – CHIEF FINANCIAL OFFICER

PAVOL TRUCHAN, CFA – HEAD OF TREASURY

JURAJ VALACHY, Ph.D. – SENIOR ANALYST, RESEARCH AND STRATEGY DEPARTMENT

Page | 3

KEY FACTS

Slovakia Tatra banka

o Competitive and fast converging economy that is fully integrated o Stable and well-established universal bank on Slovak market (Nr.3

into the Western economies in terms of total assets)

o Low and decreasing public debt (under 50% of GDP) o Bank deposit rating at A3 with positive outlook by Moody’s

o Rating: A+ and stable outlook by S&P and Fitch, A2 and positive o Provisional rating of Covered bond: Aaa (Moody’s)

outlook by Moody’s

o Residential prices generally in line with fundamentals Cover Pool

o Mortgage loans with max. maturity 30 years and max. LTV 80%

Banking sector secured by residential properties – base assets (min. 90% of cover

o Stable and well-capitalized banks belonging to the strong western pool)

banking groups with solid profitability o Cash, bonds – substitute assets (max. 10% of cover pool)

o Regulated jointly by ECB and NBS o Buffer of liquid assets – to cover liquidity gap in following 180 days

o No FX loans and very low volume of non-performing loans due to o Hedging derivatives – if any (currently not included in cover pool)

prudent risk management policy of all major banks

o Further potential for loan growth and cover bond issuance Covered bonds

o Dual recourse, bankruptcy remoteness, no automatic

Raiffeisen Bank International acceleration

o Leading banking group in CEE with 16.3 million customers, o Envisage orderly transfer of CB programme (in case of issuer´s

covering 14 CEE markets (including Austria), market capitalization ~ involuntary administration or bankruptcy proceeding)

6.6 billion EUR o Soft bullet structure (12/24 months)

o Rating: A3 and stable outlook by Moody’s, BBB+ and positive o Minimum mandatory OC 5%, possible voluntary OC

outlook by S&P

Page | 4

CONTENT

RBI and Tatra Banka at Glance

Slovak Republic

Slovak Banking Sector

Tatra Banka Financials

Covered Bonds and Cover Pool

Annex

Page | 5

RBI – LEADING BANKING GROUP IN CEE

~ 16.3 million customers

~ 47,000 employees

> 2,100 business outlets

Tatra banka

is a member

of RBI Group 27 markets worldwide

14 markets in CEE (incl. AT)

Market cap.: ~ € 6.6 billion

> 30 years

Page | 6

GEOGRAPHIC FOOTPRINT OF RBI

Austria, #3

Central Europe (CE) Eastern Europe (EE)

• Loans: EUR 32.3 bn

Southeastern Europe (SEE)

• Branches: 21

Czech Republic, #5 Russia, #10 o Top 5 market position in 11 countries

• Loans: EUR 11.3 bn • Loans: EUR 9.9 bn

• Branches: 137 • Branches: 184

o Strong market position with Austrian corporates focusing

on CEE

Hungary, #5 Ukraine, #4

• Loans: EUR 3.6 bn • Loans: EUR 1.5 bn

• Branches: 71 • Branches: 499

Slovakia, #3 Belarus, #6 RBI Ratings

• Loans: EUR 10.4 bn • Loans: EUR 1.1 bn

• Branches: 186 • Branches: 87 Rating Agency Long term Outlook Short term

Albania, #3 Serbia, #5

S&P BBB+ positive A-2

• Loans: EUR 0.7 bn • Loans: EUR 1.4 bn

• Branches: 78 • Branches: 88

Moody's A3 stable P-2

Bosnia & Herz., #2 Bulgaria, #6 Croatia, #5 Kosovo, #1 Romania, #4

• Loans: EUR 1.3 bn • Loans: EUR 2.7 bn • Loans: EUR 2.4 bn • Loans: EUR 0.6 bn • Loans: EUR 5.5 bn

• Branches: 102 • Branches: 146 • Branches: 79 • Branches: 48 • Branches: 422

Page | 7

TATRA BANKA OWNERSHIP STRUCTURE

Tatra Banka

78.78% 11.59% 9.63%

RB CEE region holding Tatra Banka employees Free float

o In 1991, the Austrian Raiffeisen o Introduced in 1998 o 4.8% owned by private individuals,

Group acquired 33.6% share from rest by local and foreign companies

o Returned shares sold back to

Slovak state owned banks employees via auction o Limited fluctuations of owners

o Later, Raiffeisen group acquired o No voting rights

additional shares

Source: Consolidated financial statements of Tatra banka 2018

Page | 8

TATRA BANKA GROUP OVERVIEW

Tatra Banka

The bank with the highest number

of quality banking awards in the SR

#3 in Slovak market in terms of Total assets

Tatra Asset Management

Tatra Leasing Share owner: 100%

Share owner: 100% Innovative market leader in the Slovak asset

management market.

DDS Tatra banky Tatra Residence

Share owner: 100%

Share owner: 100% Real estate agency focusing on providing services in

Supplementary pension asset management company the field of sale and leasing of residential and

(3rd pillar) commercial properties

Source: Consolidated financial statements of Tatra banka 2018

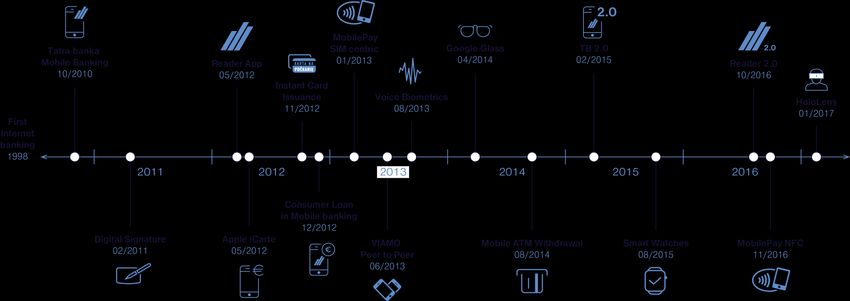

Page | 9THE MOST INNOVATIVE BANK IN SLOVAKIA

History of innovations: snapshot 1998 – 2018

Face Biometrics

06/2018

Page | 10THE SUCCESS STORY OF TATRA BANKA

o Tatra banka was established in 1990, as the first private bank in Slovakia, and quickly grew up to number 3 on the Slovak market (total assets)

o Tatra banka is a universal bank and and has a strong footprint in premium (private individuals) and corporate segment

o Steering the bank with a clear strategy:

The book of the bank

− Mission: We breakthrough the boundaries of banking

− Vision: We are the largest or the second largest bank in each of the client segments we serve

− Values: Ambition – Creativity – Courage – Partnership

o Roadmap – the execution plan of our strategy

o Strong brand promise – Leadership in innovations on the Slovak market

o Multibrand – Raiffeisen Banka and Tatra Banka

Page | 11CONTENT

RBI and Tatra Banka at Glance

Slovak Republic

Slovak Banking Sector

Tatra Banka Financials

Covered Bonds and Cover Pool

Annex

Page | 12SLOVAK ECONOMY BENEFITS FROM AUTOMOTIVE AND THE EU RECOVERY

Real GDP growth, in %

o Slovak economy demonstrated a healthy structural growth

of 3.7% in Q1 2019

5,0

4,2 4,1

o In the next couple of years, the GDP growth should be

4,0 3,2

3,1

supported by:

3,0 2,8

2,4 continued favorable external conditions (modest GDP

2,1 growth in euro area and low interest rate environment)

1,5 1,9 1,9

2,0 1,7

1,4

projected production capacity increase in the

1,0 automotive sector (Jaguar – Land Rover, Volkswagen)

-0,3

in 2019-2020

0,0

-0,9

new infrastructure projects

-1,0

2012 2013 2014 2015 2016 2017 2018

high EU funds inflow (inflow of EU fund will be strong

till 2022)

Slovakia Eurozone

Source: Eurostat

Page | 13SLOVAK ECONOMY IS A COMPETITIVE ECONOMY BASED ON STRONG

INDUSTRIAL SECTOR

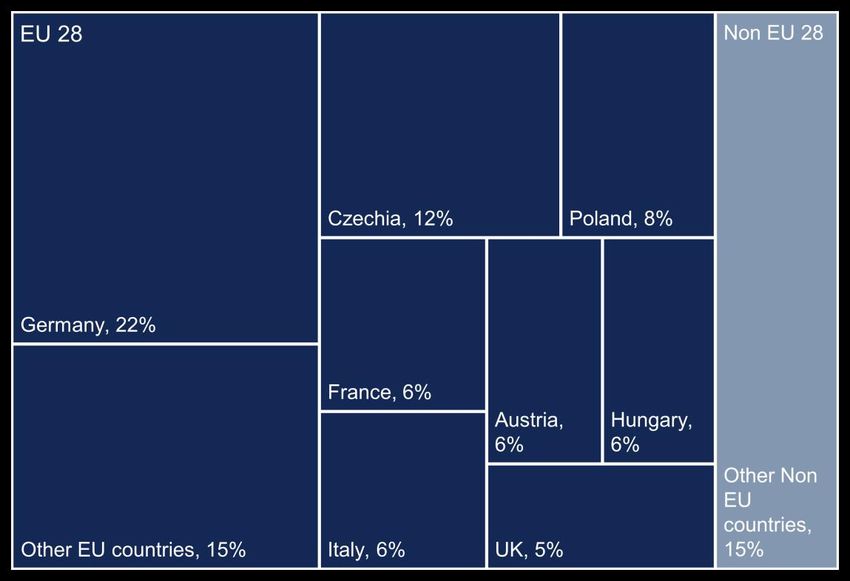

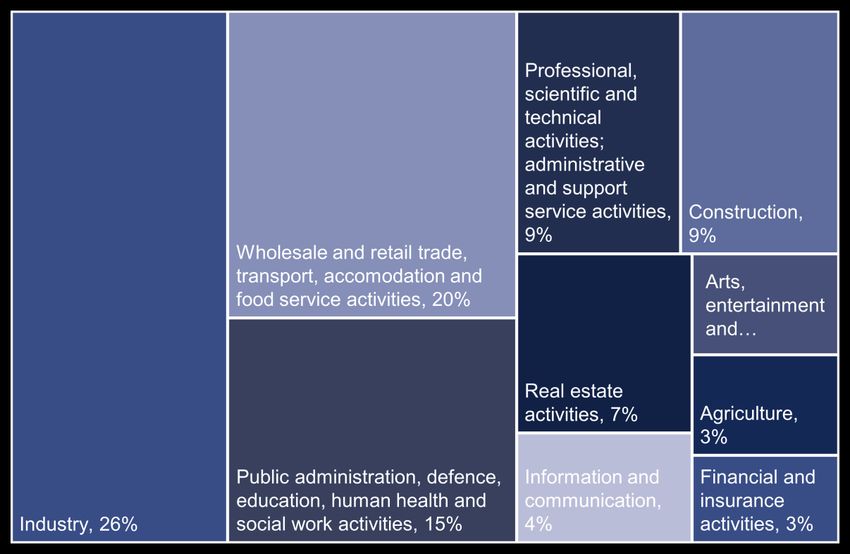

Slovakia’s export destinations, % of total in 2018 Share of GVA in Slovak economy, % of total in 2018

Source: Eurostat

o Slovakia is fully integrated into the EU production chain

o The structure of Slovak economy is very similar to Germany with a strong accent on industry

Page | 14LOW GOVERNMENT DEBT, GOOD RATING AND LOW YIELDS

Government debt to GDP for 2018YE, in % Government bond rating

Moody‘s Standard and Poor's Fitch

200 Aaa AAA

Aa1 AT AA+ AT AT

150 Aa2 AA

Aa3 AA- CZ CZ

100

66 A1 CZ(+) A+ SK, SL SK

49

50 A2 SK(+), PL A

A3 A- PL PL, SL

0 Baa1 SL(+) BBB+

Denmark

Slovakia

Lithuania

Romania

Czechia

Latvia

Neth.

Greece

Finland

Austria

Lux.

Hungary

Spain

UK

Slovenia

France

Italy

Poland

Croatia

Sweden

Average

Cyprus

Belgium

Bulgaria

Malta

Ireland

Portugal

Germany

Baa2 BBB HU HU

Baa3 HU BBB-

Source: Moody’s, S&P, Fitch

Source: Eurostat

o Slovak constitutional law on „Debt brake“ prohibits government

10Y Government bond yield, in % debt to rise above 50% of GDP

2 Slovakia Germany

o Government finances are to fend off any external economic

1,5

shocks

1

o Spreads of Slovak government bonds vs. German Bunds are stable

0,5

Slovak rating reflects good and solid economy, strong

0 institutions and euro area membership

-0,5 o Still relatively low income per capita prevents agencies to give

2016 2017 2018 2019

Slovakia a better rating

Source: Macrobond

Page | 15HOUSEHOLDS ENJOY IMPROVING INCOME SITUATION

Unemployment rate (LFS), in % Nominal wage growth in economy, y-o-y in %

16% 7%

6,2%

14% 6%

12% 4,6%

5%

10% 4,2%

8% 4% 3,3%

2,9%

6% 3%

4% 2%

2%

1%

0%

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

0%

2014 2015 2016 2017 2018

Source: Eurostat Source: Statistical Office of the SR

Loans for house purchase/GDP, in %, End of March 2019

100 o In the following years, nominal wage growth should stay

at the higher level due to:

80

– stable inflation around 2% in medium term;

60

33 – productivity rise;

40

– tight labor market conditions;

20

– public wage growth by 10% in 2019 and also in

0

2020.

Czechia

Portugal

UK

France

Ireland

Romania

Estonia

Slovakia

Belgium

Spain

Sweden

Lithuania

Poland

Germany

Netherlands

Latvia

Italy

Finland

Austria

Bulgaria

Greece

Malta

Cyprus

Luxembourg

Hungary

Slovenia

Croatia

Denmark

o Households‘ indebtedness at par with the average in

other European countries

Source: Macrobond

Page | 16HOUSE PRICE DEVELOPMENT IN LINE WITH WAGE GROWTH

House price, in EUR per m2 House price/Annual Wage, Years

2 000 14

1 822

13

1 800

12

1 600 11

1 400 10

9 8,2

1 195

1 200

8

1 000 7

6

800 Flats Houses

5

600 4

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

o House price development is in line with fundamentals – strong nominal wage and employment growth

o Prices are growing across the country

o We expect house prices to grow in line with fundamentals also in the next years

Note: Price of the hypothetical 68m2 flat divided by average annual gross salary in economy

Source: NBS, Statistical Office of the SR Page | 17CONTENT

RBI and Tatra Banka at Glance

Slovak Republic

Slovak Banking Sector

Tatra Banka Financials

Covered Bonds and Cover Pool

Annex

Page | 18STRONG AND STABLE SLOVAK BANKING SECTOR

Stable banking sector Room for growth

o Not dependent on external financing - Loan/Deposit ratio o Well equipped with capital - Capital Tier 1 ratio at 16.7%

100.6%

o Room for loan growth - Loan to GDP is 67% (110% in euro-area)

o Low amount of bad loans - Share of Non-Performing Loan is

o Room for CB issuance - Only 8% of bank funding is from bonds

3.1% (2.9% in retail and 3.9% in corporate)

o No FX loans - Only 4.1% loans (0% in retail) are in FX

o No bank bail-out during 2008-2010

o Not overheated

Banking assets to GDP, in %, end of 2018 Funding structure of Slovak banking sector, end of 2018

2%

8%

400

300

Deposits from customers

200

88 Debt securities

100 Other liabilities (without equity)

0

Poland

Denmark

Portugal

Slovakia

Estonia

Czechia

Belgium

Spain

Sweden

Euro Area

Romania

Lithuania

Germany

Netherlands

Latvia

Italy

Finland

UK

Austria

Bulgaria

Greece

Slovenia

Croatia

Cyprus

Malta

France

Hungary

Ireland

90%

Source: NBS

Page | 19MACROPRUDENTIAL POLICY OF NBS

o National Bank of Slovakia closely monitors trends in financial sector

o NBS’s aim is to balance loan growth with the long-term sustainability of financial sector

o Main impact:

Restricted Debt-to-Service:

− Cost of living + Additional financial reserve over costs of living – 20 x (income - living costs)

− Stressed instalment for mortgage loans: Additional financial reserve over monthly payment for existing loans with maturity over 8Y

New legislative limit for Debt-to-Income: DTI = 8, max exposure of client up to 8 x yearly net salary (limited amount of exception is allowed)

Restricted LTV for Mortgage Loans

− LTV more than 90% - not allowed

− LTV more than 80% - currently 30% from 07/2019 20% of new volume per quarter

Loans with maturities of 30 years

Real estate value in case of purchase / building up is given as minimum of sale price, internal valuation and expert’s price

Page | 20SLOVAK BANKING SECTOR (1/2)

o Slovak banking sector keeps a strong pace of growth of average 6.2% during the last 5 years

o The sector is dominated by big international banking groups like Erste, IntesaSanPaolo, Raiffeisen, KBC, Unicredit

o Tatra banka group is the 3rd largest bank in terms of assets and keeps this position for more than a decade

o Growth in retail loans segment was dominant during the last couple of years, corporate loans were growing in a more modest way

Total assets, as of EOY, bn EUR Total assets by Slovak bank groups, Q1 2019, bn EUR

CAGR +6,2%

75 79 83 17,4 16,7

66 71 13,2

9,8

5,2 4,3 3,6 1,4

2014 2015 2016 2017 2018 SLSP VUB TB CSOB* UNCR POB Prima* OTP*

Source: NBS Source: Consolidated financial statements of banks, banks with * have individual fin.statement

Retail loans, as of EOY, bn EUR Corporate loans, as of EOY, bn EUR

CAGR +12,6% CAGR +6,5%

3,6

3,3 5,8

3,1 5,1

3,1 4,6

3,7 3,9

3,4 17 18 19

26,0 14 16

20,5 23,2

15,0 17,7

2014 2015 2016 2017 2018 2014 2015 2016 2017 2018

Source: NBS Other Consumer Housing Source: NBS Page | 21SLOVAK BANKING SECTOR (2/2)

o Very favorable macroeconomic environment visibly decreases the non-performing loans for households (HH) and corporates as well

o Slovak banks maintain capital well above required levels, this opens the door for further growth

o Slovak banks deliver stable and solid profit even in an environment of low interest rate. ROE is well above the western peers

Non-performing loans/Total loans, EOY, in % Tier 1 ratio, EOY, in %

6% 18%

5%

16%

4%

3% 5,5% 14%

5,0% 4,5% 16,0% 16,5% 16,3% 16,8% 16,7%

2% 3,7%

3,1% 12%

1%

0% 10%

2014 2015 2016 2017 2018 2014 2015 2016 2017 2018

Return on Equity, EOY in %

Total profit of the sector, EOY, in mn EUR

15%

800

600 10%

400 13,2%

742 5% 10,3% 11,1%

560 626 612 640 9,2% 9,2%

200

0%

0 2014 2015 2016 2017 2018

2014 2015 2016 2017 2018

Source: NBS Page | 22LOANS TO HOUSEHOLDS SLOWING DOWN, CORPORATE LOANS KEEP

DECENT DYNAMICS

Annual growth of banking sector loans, in % based on monthly outstanding stock of loans

16%

Retail loans

14%

12%

10% 9,7%

8%

6,6%

6%

4%

Corporate loans

2%

0%

-2%

2014 2015 2016 2017 2018 2019

Source: NBS

o Retail loans were growing faster than fundamentals, but recent NBS measures should bring this development in line with strongly evolving

fundamentals

o Corporate loans are following the nominal GDP growth

Page | 23HOUSING LOANS – MARKET SHARE

Market share of Tatra Banka in housing loans Market Share of individual banks on housing loans, March 2019

35%

17%

30%

25%

16%

15,6% 20%

15% 29%

15% 24%

10%

16%

13%

5% 9%

6%

1% 3%

14% 0%

03 04 05 06 07 08 09 10 11 12 01 02 03 Tatra SLSP VUB CSOB UNCR Prima Poštová Others

2018 2019 banka

Source: NBS

Source: Tatra banka, NBS

o Tatra Banka historically keeps a slightly growing market share of Slovak housing loan market of around 16%

o The Bank is not hunting for market share. We keep our risk standard, while improving the client service

Page | 24CONTENT

RBI and Tatra Banka at Glance

Slovak Republic

Slovak Banking Sector

Tatra Banka Financials

Covered Bonds and Cover Pool

Annex

Page | 25TATRA BANKA GROUP

o Tatra Banka keeps strong and healthy growth of assets Total Assets, EOY, in EUR mn

o We keep pace with market and our retail loan portfolio went by 15 000

mainly thanks to mortgage loans

10 000

o In the corporate segment we keep our leading position in

segment of domestic non-financial corporations 12 503 13 196

5 000 11 373

0

2016 2017 2018

Retail loans, EOY, in EUR mn Corporate loans, EOY, in EUR mn

7 000

Housing Consumer Other 5 000

6 000

1 017

5 000 4 000

896

871

4 000 867 777 3 000

3 000 616

2 000 4 126 4 388 4 377

2 000 3 999

3 469

2 935 1 000

1 000

0 0

2016 2017 2018 2016 2017 2018

Source: Consolidated financial statements of Tatra banka, 2016-2018

Page | 26KEY PERFORMANCE INDICATORS

o Prudent risk policy helps us to decrease NPL to the very low level

o Our capital is high enough to safeguard further growth and meet all regulatory requirement by wide margin

o Tatra banka is able to deliver decent and very stable profit every year

o Our ROE was at the level of 12% in 2018 and these results make Tatra Banka very important part of RBI group

Non-Performing loans, as % of total loans Tier 1 indicator of Tatra banka group, %

16%

4,0%

3,0% 14%

2,0% 3,6% 15,3% 15,1% 15,4%

2,9% 12%

1,0% 2,4%

0,0% 10%

2016 2017 2018 2016 2017 2018

Profit after tax of Tatra banka group, in EUR mn ROE of Tatra banka group, %

150 15%

100 10%

126 124 13,5% 13,4% 12,0%

120 5%

50

0 0%

2016 2017 2018 2016 2017 2018

Source: Consolidated financial statements of Tatra banka, 2016-2018 Page | 27BELOW MARKET NPL RATE ON HOUSEHOLD LOANS AND MORTGAGE LOANS

Loans to Households: NPL/Total Loans in %, from 2014 to March 2019 Housing Loans: NPL/Total Loans in %, from 2014 to March 2019

6% 4,0%

5% 3,5%

3,0%

4%

2,5%

2,9%

3% 2,0%

1,5% 1,2%

2%

2,0% 1,0%

1% 1,1%

0,5%

0% 0,0%

2014 2015 2016 2017 2018 2019 2014 2015 2016 2017 2018 2019

Tatra banka Banking Sector Tatra banka Banking Sector

o Prudent risk policy of Tatra banka results in lower NPL in household loans than banking sector has

o The similar holds also for the Housing loans segment

Source: Tatra banka, NBS Page | 28CAPITAL ADEQUACY RATIOS – STRONG AND SUSTAINABLE CAR

CAD Ratios, EOP value in %

o Tatra banka comfortably operates above minimum regulatory

21% capital requirements (as of March 2019):

19,72% CET1 ratio 10,97% (11,97% including Pillar 2 guidance)

20%

Required total CAD ratio of 14,47%

19%

17,95%

17,74% 17,69%

18%

o Tatra banka replaced part of its subordinated debt at amount

17% of EUR 100 mn with the higher quality AT1 capital (high

trigger of 7%)

16% 15,62% 15,58% 15,61%

15%

14,11% 13,96% 13,91%

14%

13%

12%

12.2016 12.2017 12.2018 03.2019

CAD CET1 CAD T1 CAD

Source: Consolidated financial statements of Tatra banka 2017 and 2018 Page | 29CAPITAL ADEQUACY REQUIREMENTS – MARCH 2019

TBG Capital requirements/Actual (03/2019)

o 2018 SREP P2R of 1.25%, and P2G of 1.0% (unchanged from 2017).

Actual

Tatra banka is one of the banks with best SREP rating in Slovakia.

Buffer 17,95%

3,48%

o Combined buffer requirement in 03/2019:

Buffer Actual

3,14% 15,61% Tier2R

2.50% capital conservation buffer

Buffer Actual 2,00%

13,91% 1.00% systemic risk buffer

2,94% AT1R

1,50% 0.50% other systematically important institutions

0.22% countercyclical buffer (for domestic transactions)

CBR+P2R Total capital requirement = 14,47% Legend:

CET1 requirement = 10,97%

TIER1 requirement = 12,47%

6,47%

Tier1R P1R Pillar 1 requirement

CET1R 12,47% P2R SREP Pillar 2 requirement

10,97% P2 Guidance Pillar 2 guidance

CBR Combined buffer requirement, includes:

• Capital conservation buffer

• Countercyclical buffer

P1R

4,50% • Systemic risk buffer

• O-SII buffer

AT1R Additional Tier 1 requirement

CET1 Tier 1 Total Capital

Source: Tatra banka Page | 30ASSETS AND LIABILITIES BY SEGMENTS

Assets, in EUR mn Liabilities, in EUR mn

13.196 13.196

12.503 12.503

2.831

3.819 2.532 (21%)

3.912 (29%) (20%)

(31%) 754

581 (6%)

176 (5%)

239 (1%)

(2%)

6.126 6.721 7.255

5.251 (46%) (54%) (55%)

(42%)

2.739 2.667 1.455 1.008

(22%) (20%) (12%) (8%)

1.215 1.349

362 407 (10%) (10%)

(3%) (3%)

31. 12. 2017 31. 12. 2018

31. 12. 2017 31. 12. 2018

Corporate customers Retail customers Equity and other

Financial institutions and public sector Investment banking and treasury

Source: Consolidated financial statements of Tatra banka, 2016-2018

Page | 31MATURITY PROFILE OF ISSUED BONDS

Volumes as of 31/5/2019, in EUR mn

300

250

Covered bonds Senior unsecured (Tatra Leasing)

200

150 281

100

50 10

50 46 60 50 50

29 10

0

2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031

o As of 31st of May 2019 the outstanding amount of bonds issued by Tatra banka group was 585 mn EUR

o The majority of issued bonds (575 out of 585 mn EUR) are covered bonds (re-registered mortgage bonds issued under legislation valid till

the end of 2017)

o Senior unsecured bonds represent only 10 mn EUR from total outstanding (issued by Tatra Leasing)

o Tatra banka intends to regularly tap the covered bond market going forward

Page | 32CONTENT

RBI and Tatra Banka at Glance

Slovak Republic

Slovak Banking Sector

Tatra Banka

Covered Bonds and Cover Pool

Annex

Page | 33SLOVAK COVERED BONDS LEGAL FRAMEWORK – OVERVIEW (1/4)

o New covered bonds (CB) legislation valid since January 2018

o Issuer can be only a bank with prior consent of National Bank of Slovakia (NBS) to issue covered bonds

o NBS supervision, issuer´s reporting obtained quarterly

o Covered bonds Administrator/Monitor – an independent individual appointed by NBS

verifies issuer´s compliance with all legal requirements in respect of covered bonds

issues a written certificate confirming that the issuer has sufficient coverage for a new bond that is to be issued

yearly submits to NBS report on covered bonds programme for previous year

o Mandatory maintenance of Covered Bonds Register by issuer

keeping records of all components of the CB programme

all cover assets entered in the CB Register constitute a separate estate of the issuer and may only be used to satisfy claims of CB bondholders (i.e.

on-balance sheet segregation of cover assets from the issuer´s general estate)

o Enhanced insolvency regime

dual recourse, bankruptcy remoteness, no automatic acceleration of CB

envisage orderly transfer of CB programme (in case of issuer´s involuntary administration or bankruptcy proceeding) –> soft bullet structure (12/24

months)

Page | 34SLOVAK COVERED BONDS LEGAL FRAMEWORK – OVERVIEW (2/4)

o Cover Pool Composition:

Base (Primary) Assets

- At least 90% of the cover pool (excl. LA)

- Residential mortgage loans only to consumers, max. tenor 30y

- LTV max. 80%

- Properties in the Slovak Republic; first rank security (subject to very limited exemptions)

- Exclusion of loans if debtor is considered defaulted (as per Article 178 (1) of Regulation (EU) No. 575/2013 - CRR)

Substitute Assets

- Max. 10% of the cover pool (excl. LA)

- Cash or deposits with NBS, ECB, EU Member state central bank and other assets that meet conditions under Article 129 (1) (c) of CRR

Hedging derivatives (if any)

- Purpose is to manage and mitigate currency risk or interest risk connected with issued covered bonds

Buffer of Liquid Assets (LA)

- Required to cover the maximum liquidity gap within the CB programme over next 180 days, if any

- Tier 1 and Tier 2A assets under Articles 10 and 11 of Regulation (EU) 2015/61

- Value of LA is a part of coverage ratio

Page | 35SLOVAK COVERED BONDS LEGAL FRAMEWORK – OVERVIEW (3/4)

o Other key requirements for the CB programme/issuer:

Minimum overcollateralization of 5%

- Value of the cover pool must be at least 105% of issuer´s liabilities under CB programme (i.e. outstanding covered bonds and related costs)

- Voluntary higher OC enabled

- Obligatory calculation of coverage ratio at the end of a month

180-day liquidity coverage test

- Daily calculation of expected positive and negative cash flows within the CB programme during the following 180 days

- In case of negative gap, liquid assets must be allocated in the cover pool to cover it

Stress testing

- Performed at least once a year (on data as of 31 December of preceding year)

- Includes test for credit risk, interest rate risk, currency risk, liquidity risk, counterparty risk, operational risk and risk of decrease in prices of immovable

property

Page | 36SLOVAK COVERED BONDS LEGAL FRAMEWORK – OVERVIEW (4/4)

o Insolvency, Transfer of CB programme

No automatic acceleration; the trustee operates the CB programme separately from the general estate of the issuer

Process governed by the Bankruptcy Act and under NBS supervision

The trustee considers the level of satisfaction of the CB holder in all scenarios and acts with due professional care for the benefit of all CB holders

Preferred scenario – orderly transfer of the CB programme

- The transfer should be completed within one year from notification of the NBS; another one year extension can be requested

- The payment terms of the CBs are modified upon notification (soft bullet extension):

- 1st month: all obligation in full according to original terms

- 2nd – 12th months: interest payments of CBs in full, but maturity of CBs with residual maturity expiring within 11 months is prolonged

by another 12 months (or max. 24 months in case of another extension)

- The transferee bank will assume the whole cover pool and all CB obligations without modifications

In case of failure to transfer the whole CB programme, the trustee can sell individual cover assets (loans) in order to satisfy due claims of CB

holders

Failing all above, the trustee terminates the operation of the CB programme – CB will accelerate and the cover pool will be liquidated

Page | 37COMPARISON OF COVERED BONDS FRAMEWORKS

Slovakia Austria Poland Germany (Pfandbriefe)

Universal credit institution with a prior Universal credit institution with a special

Specialized credit institution Universal credit institution with a special

Issuer approval from National Bank of license

license

Slovakia for issuing covered bonds

Polish Financial Supervision

Bundesanstalt fur

Regulatory supervision National Bank of Slovakia (NBS) Financial Market Authority (FMA) Authority (Komisja Nadzoru

Finanzdienstleistungsaufsicht (BaFin)

Finansowego, KNF)

Mortgages, public sector loans,

Residential mortgage loans, up to 30 Mortgages, public sector loans, eligible Mortgages, public sector loans

Primary Assets registered ship mortgages, registered

years granted to consumers bonds

liens on registered aircrafts

EEA, USA, Canada, Switzerland, Japan,

Underlying Assets Location Slovakia EEA/ Switzerland Poland (Mortgage CBs)

Australia, New Zealand and Singapore

Max. LTV 80% 60% (HypBG) 80% (Residential), 60% (Commercial) 60%

10% of cover pool (excl. liquid

Substitution Assets 15% of the amount of issued CBs 15% of the amount of issued CBs 20% of the amount of issued CBs

assets)

Minimum legal OC 5% 2% 10% 2%

Coverage of the maximum liquidity Liquidity buffer to cover CB interest Specific coverage of liquidity risk over a

gap within CBs programme over the “Natural” matching (matching without the payments in 6M; 180 day period;

next 180 days (daily performance); use of off-balance sheet instruments) and

Mitigation of risks Coverage test (at least semi-annually), Hedging derivatives might be registered

Hedging derivatives possible; stress testing; Hedging derivatives might

liquidity tests (at least quarterly); in the cover pool;

Stress testing at least yearly be registered in the cover pool

Mandatory FX risk limitation Stress testing weekly

Assets in the cover pool are fully In case of bankruptcy of a mortgage bank

segregated from the general the cover register shall constitute a

Assets within the cover register are

insolvency estate of the bankrupt separate bankruptcy estate which may

exempt from bankruptcy proceedings.

bank. The general insolvency trustee No acceleration of covered bonds be used exclusively to satisfy claims of

After the launching of the insolvency

Bankruptcy observes special procedures that are Covered bond creditors have preferential covered bondholders. The court appoints

proceedings, a special cover pool

aimed to extend covered bonds' claim on the cover assets the curator who represents the rights of

administrator carries out the

maturity in the event of bankruptcy covered bondholders. The soft-bullet

administration of the cover assets

and postpone immediate maturity of the covered bonds is triggered

acceleration. automatically after insolvency.

Independent Cover Pool Monitor Yes Yes Yes Yes

Source: EBA report on covered bonds as of 20 December 2016, www.ecbc.eu Page | 38REGULATORY OVERVIEW

o Regulatory classification for different rating levels of a typical Slovak EUR covered bond benchmark

UCITS CRR

EEA Solvency II LCR ECB repo CBPP3

Art. 52 (4) risk weight

AAA ✔ ✔ 10% ✔ 1(B)* ✔ ✔

Slovak

covered AA ✔ ✔ 10% ✔ 1(B) ✔ ✔

bonds

A ✔ ✔ 20% 2A ✔ ✔

DE, FR, NL, … ✔ ✔ 10% ✔ 1(B) ✔ ✔

Other

selected POL, NOR ✔ ✔ 10% ✔ 1(B) ✔

covered

bonds CAN 20% 2A ✔

AUS, NZD 20% 2A

*Level 1(B) LCR assumes min EUR 500mn issue size, covered bonds with min EUR 250mn can achieve 2A LCR level

Page | 39COVERED BONDS IN TATRA BANKA – BONDS OVERVIEW

o Nominal Value of Outstanding Bonds1) : 573 800 000 EUR o Provisional rating by Moody´s: Aaa

o Currency: EUR o Programme Size2): EUR 3,000,000,000

o Average Residual Life: 2,8Y o Listing: Bratislava Stock Exchange

o Interest Rate Type: 52% float, 48% fix o Clearing: Central Securities Depository,

Euroclear, Clearstream

o Number of Issues: 9

o Paying Agent: Tatra banka

o Governing Law: Slovak

o Over-collateralisation: 49,68%

300 Maturity Profile

250

200

In mn EUR

150

280

100

50

50 46 60 50 50 10

28

0

2019 2020 2021 2023 2024 2025 2026 2031

1) As of 31.5.2019, covered bonds programme contain only Mortgage bonds issued till 31.12.2017, which were on 14 December 2018 reregistered in the CB Register and since then are deemed as the covered bonds

2) includes covered bonds/ senior /senior non-preferred/ subordinated bonds Page | 40COVERED BONDS IN TATRA BANKA – COVER POOL OVERVIEW (1/2)

o Total Assets (incl. accrued interest), o/w: EUR 860 675 788 Residual Life (in years)

3%

Primary assets (outstanding nominal 9%

EUR 807 964 385

value) (25; 30>

30%

13% (20; 25>

Liquid assets (market value) EUR 52 711 403

(15; 20>

Substitute assets (market value) -- (10; 15>

(5; 10>

o Type of primary assets Slovak residential mortgage loans

22%

o Average Residual Life of Loans 17.37 years 23%

o Number of Borrowers 19 610

Purpose of loans

o Number of Loans 19 802

2%

9%

o Currency of Loans EUR

acquisition

13%

o Interest Rate Type of Loans administrated fixed rate construction

repayment

o Average Time of Drawing 5.34 years other

58%

maintenance

18%

o Average Actual LTV 48.76%

o Loans more than 90 days past due 0.00%

Source: Cover Pool Report as of 31/5/2019

Page | 41COVERED BONDS IN TATRA BANKA – COVER POOL OVERVIEW (2/2)

Distribution by actual LTV Size of Outstanding Loans, in EUR ths

9% (70%; 80%>

41%

22% (60%; 70%>

19%

11% 11% 9%

6% 4%

(0; 25> (25; 50> (50; 75> (75; 100> (100; 125> (125; 150> >150

21% (50%; 60%>

Loans by Regions

17% (40%; 50%>

39%

31%

11% 10% 10% 9% 9% 7% 6%

31. 5. 2019 Bratislava Košice Žilina Trnava Prešov Nitra Trenčín Banská Bystrica

Source: Cover Pool Report as of 31/5/2019

Page | 42CONTENT

RBI and Tatra Banka at Glance

Slovak Republic

Slovak Banking Sector

Tatra Banka

Covered Bonds and Cover Pool

Annex

Page | 43UNDERWRITING PROCESS

o Target segment defined as:

Citizen of Slovak Republic that has verified income

- employees – verified in governmental Social Insurance Application (automated verification)

- entrepreneurs – verified official Tax declaration in Tax office

- clients with salary certificate (not possible to be verified in SIA)

- in some cases additional documentation is needed (CA statements, income confirmation from employer)

Foreign permanent residents have stricter acceptance criteria (e. g. lower max. LTV, limited loan purpose)

All clients must reach creditworthiness criteria required by the bank

o Income is always checked. However, only exception is Refinancing loan when (1) it does not exceed increase of 2,000 Eur or 5% of loan amount; (2) new

instalment is lower than current one and (3) client fullfils creditworthiness of the bank

o Application and behavioral scorecards in place - statistical, developed internally on in-house historical data, validated in line with regulation and HO

market standards, quarterly recalibrated to adjust for changes in recent risk profile

o Maximum instalment (also stressed) based on risk parameters and interest rate has to comply with disposable - and debt to income limits

o The maximum LTV is determined by a matrix that takes into account collateral location and Universal Rating Grade of client (PD rating according RBI

Master Scale)

o Eligibility criteria

K.O. criterion: Execution orders, Bankruptcy, Internal payment history and other internal databases checks are in place, Internal negative

information

Credit Bureau information about payment history and existing loan products is transferred and evaluated automatically. It is used also for

check of existing instalments amount (repayment capacity calculation purposes) and for refinancing loans (comparison of existing and new

instalment, outstanding approximation, etc.) and for calculation of maximum acceptable limit of customer on market level.

Page | 44COLLATERAL MANAGEMENT

o Description of the appraisal process - initial valuation: o In case the loan payment is past-due

External appraiser chosen by client (max 12m old, w/o negative Usually after 90 Days-Past-Due - voluntary auction sale or a voluntary

experience of appraisers) + full review by TB internal appraiser auction. It can be done anytime - with or without prior contract termination

External appraiser chosen by TB (selected by TB ) + full review Termination of loan is usually 180-200 DPD

by TB internal appraiser Auction is always after termination, usually between 360-720 DPD.

During internal review process, we use price map or web sites

of reliable real estate agencies as a support tool to verify value o Encumbrance

estimated by the external appraiser

Tatra banka accepts when a property is subject of more than one

Anyway, the collateral is always appraised by certified encumbrance only in following cases:

appraiser

-preferential rights of Housing Cooperatives;

-any rights (incl. preferential) of the State Housing Development Fund

o Collateral periodical valuation

Yearly statistical revaluation method is applied, based on o In the all other cases Tatra banka shall have preferential rights, since the

comparative method and price map national legislation regulates the payment of claims based on their order.

Ex-post quality check of appraisals are done in collateral The priority in the order is important in case of execution of sale deed.

management on regular basis Preferential claim is paid first.

Whitelist and blacklist appraisers are monitored

o Property insurance

Real estate insurance is a basic condition during whole life of

loan

Not insured real estates are covered by portfolio insurance with

UNIQA.

Page | 45AWARDS

o Bank of the Year 2018

"Best Slovak Bank " awarded by Euromoney – for the 14th year in a row

"Best Bank" by Global Finance and EMEA Finance magazines.

o Private banking recognized as a leader once again

"Best Private Bank" from EMEA Finance in 2018 - bank’s private banking service

o Winner in Central and Eastern Europe

"Best Digital Bank in Slovakia " from Global Finance - Our innovative approach has been recognized by this magazine. Our online offering

of savings, loans, and investment products as well as our web design were declared the best in Central and Eastern Europe, as was our

corporate business banking service.

Page | 46more than

130

awards since its

foundation

in 1990

Page | 47CONTACTS

Tatra banka

Pavol Truchan, CFA

Head of Treasury

Tel: +421-2-5919 1702

e-mail.: pavol_truchan@tatrabanka.sk

Dana Rudkovská

Primary Issuance Specialist

Treasury Department

Tel.: +421 2 5919 1468

e-mail: dana_rudkovska@tatrabanka.sk

Juraj Valachy, Ph.D.

Senior Analyst

Reserch and Strategy Dept.

Tel.: +421 2 5919 2033

e-mail: juraj_valachy@tatrabanka.sk

Page | 48You can also read