CREATING A LEADING AFRICAN GOLD PRODUCER - Denver Gold Forum | September 15-18, 2019

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Denver Gold Forum | September 15-18, 2019

CREATING A LEADING

AFRICAN GOLD PRODUCER

NYSE AMERICAN: GSS | TSX: GSC 1

DISCLAIMER

SAFE HARBOUR: Some statements contained in this presentation are forward-looking statements or In this presentation, we use the terms "cash operating cost per ounce", "All-In Sustaining Cost per

forward-looking information (collectively, “forward-looking statements”) within the meaning of the ounce" and "AISC per ounce". These terms should be considered as Non-GAAP Financial Measures as

United States Private Securities Litigation Reform Act of 1995 and applicable Canadian securities defined in applicable Canadian and United States securities laws and should not be considered in

laws. Investors are cautioned that forward-looking statements are inherently uncertain and involve isolation or as a substitute for measures of performance prepared in accordance with International

risks and uncertainties that could cause actual results to differ materially. Such statements include Financial Reporting Standards ("IFRS"). "Cash operating cost per ounce" for a period is equal to the

comments regarding: estimated gold production, cash operating costs, All-in Sustaining Costs and cost of sales excluding depreciation and amortization for the period less royalties, the cash

capital expenditures for 2019; the expansion potential at Wassa and Prestea; ongoing investment to component of metals inventory net realizable value adjustments and severance charges divided by

increase drill density, increase stope availability and expand development at Wassa; the sourcing of the number of ounces of gold sold (excluding pre-commercial production ounces) during the period.

ore at Prestea in H2 2019; an expected grade increase at Prestea in H2 2019; underground ,"All-In Sustaining Costs per ounce" commences with cash operating costs and then adds sustaining

productivity mining rate and throughput being expected to increase at Prestea in H2 2019; open pit capital expenditures, corporate general and administrative costs, mine site exploratory drilling and

production being expected to continue at a similar grade at Prestea during Q3 2019; completion of greenfield evaluation costs and environmental rehabilitation costs, divided by the number of ounces

the refurbishing of the underground railway at Prestea in Q3 2019 resulting in improved throughput; of gold sold (excluding pre-commercial production ounces) during the period. This measure seeks to

the installation of a new larger rock breaker at Prestea; the implementation of initiatives identified represent the total costs of producing gold from operations. These measures are not representative

by CSA Global at Prestea; the conversion of Inferred resource to Indicated resource at Wassa Deep in of all cash expenditures as they do not include income tax payments or interest costs. Changes in

H2 2019 and providing a Resource and Reserve update in early 2020; the timing of a decision on the numerous factors including, but not limited to, mining rates, milling rates, gold grade, gold recovery,

Father Brown deposit; a resource update and assessment of project viability for Father Brown in Q3 and the costs of labor, consumables and mine site general and administrative activities can cause

2019; the Company’s anticipated debt maturity schedule; and the exploration upside of the Wassa these measures to increase or decrease. We believe that these measures are the same or similar to

and Prestea Undergrounds. Factors that could cause actual results to differ materially include the measures of other gold mining companies but may not be comparable to similarly totaled

timing of and unexpected events at the Prestea and/or the Wassa processing plants; variations in ore measures in every instance. Please see our "Management's Discussion and Analysis of Financial

grade, tonnes mined, crushed or milled; delay or failure to receive board or government approvals Condition and Results of Operations for the three and six months ended June 30, 2019" for a

and permits; construction delays; the availability and cost of electrical power; timing and availability reconciliation of these Non-GAAP measures to the nearest IFRS measure.

of external financing on acceptable terms or at all; technical, permitting, mining or processing issues,

including difficulties in establishing the infrastructure for Wassa Underground or Prestea INFORMATION: The information contained in this presentation has been obtained by Golden Star

Underground, inconsistent power supplies, plant and/or equipment failures and an inability to from its own records and from other sources deemed reliable, however no representation or

obtain supplies and materials on reasonable terms (including pricing) or at all; changes in U.S. and warranty is made as to its accuracy or completeness. The technical information relating to Golden

Canadian securities markets; heavy rainfall and flooding of underground mines; and fluctuations in Star's material properties disclosed herein is based upon technical reports prepared and filed

gold price and input costs and general economic conditions. pursuant to National Instrument 43-101 - Standards of Disclosure for Mineral Projects ("NI 43-101")

and other publicly available information regarding the Company, including the following: (i) "NI 43-

There can be no assurance that future developments affecting the Company will be those 101 Technical Report on a Feasibility Study of the Wassa Open Pit Mine and Underground Project in

anticipated by management. Please refer to the discussion of these and other factors in our Annual Ghana" effective December 31, 2014; and (ii) "NI 43- 101 Technical Report on Resources and

Information Form for the year ended December 31, 2018 filed and available at www.sedar.com. The Reserves, Golden Star Resources, Bogoso/ Prestea Gold Mine, Ghana" effective December 31, 2018.

forecasts contained in this presentation constitute management's current estimates, as of the date Additional information is included in Golden Star's Annual Information Form for the year ended

of this presentation, with respect to the matters covered therein. We expect that these estimates December 31, 2018 which is filed and available on www.sedar.com. Mineral Reserves were prepared

will change as new information is received and that actual results will vary from these estimates, under the supervision of Dr. Martin Raffield, Senior Vice President Technical Services for the

possibly by material amounts. While we may elect to update these estimates at any time, we do not Company. Dr. Raffield is a "Qualified Person" as defined by NI 43- 101. The Qualified Person

undertake to update any estimate at any particular time or in response to any particular event. reviewing and validating the estimation of the Mineral Resources is Mitchel Wasel, Golden Star

Investors and others should not assume that any forecasts in this presentation represent Resources Vice President of Exploration.

management's estimate as of any date other than the date of this presentation.

CURRENCY: All monetary amounts refer to United States dollars unless otherwise indicated.

NYSE AMERICAN: GSS | TSX: GSC 2

GOLDEN STAR SNAPSHOT

AFRICA

2019

Strong Cash Balance

Production

$66.2 million 1

Guidance

190,000-205,000oz

2019 AISC 2 Mineral Reserves &

Guidance Resources

Prestea Wassa

$1,100-1,200/oz P&P 1.8 Moz Gold Mine Gold Mine

M&I 5.9 Moz

Inferred 7.2 Moz Father Brown ACCRA

Satellite Deposit

TAKORADI

1. As at June 30, 2019.

NYSE AMERICAN: GSS | TSX: GSC 2. See note on slide 2 regarding Non-GAAP Financial Measures. 3

MARKET INFORMATION

Analyst Coverage Key Institutional Shareholders Ownership Breakdown 1

▪ Beacon Securities La Mancha Holding 30%

▪ CIBC Capital Markets

CPMG Inc. (Condire) 7.5%

▪ Clarus Securities

▪ Desjardins Capital Markets Van Eck 5.2%

Retail/Other

▪ HC Wainwright & Co Franklin Templeton 4.1% 27%

▪ National Bank Financial Oppenheimer Funds 2.6% Institutional

▪ Numis Securities 43%

Renaissance Technology LLC 2.5%

▪ Scotiabank La Mancha

Invesco Advisers Inc. 2.4% 30%

Market Information 1

Victory Capital Management 1.6%

NYSE American / TSX / Konwave AG 1.6%

Markets

GSE

Tocqueville Asset Management 1.4% ▪ Strong support from the 30% strategic

NYSE: GSS

shareholder La Mancha, a proven and

Tickers TSX: GSC

GSE: GSR successful investor in the gold sector

▪ Recently requested (and was granted) ability

Shares in Issue 109,141,742

to increase their holding to 35%

Options 3,938,683

Share Price (NYSE) $3.08

Market

$336m

Capitalization

1. As at August 29, 2019 1. As at September 11, 2019

NYSE AMERICAN: GSS | TSX: GSC 4

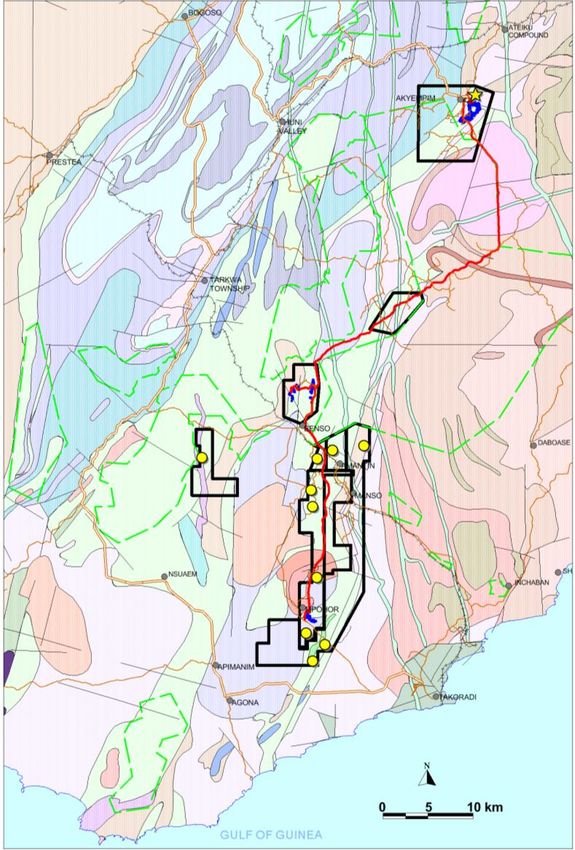

AN UNDERGROUND MINING COMPANY, OPERATING IN GHANA

Wassa: Wassa Southern Extension: Father Brown: Across the Company:

▪ Golden Star’s Flagship ▪ 47% increase in reserves ▪ Drill data being analyzed ▪ A culture where safety is

Asset during 2019 to determine next steps never compromised

▪ Long life, low cost, ▪ Rapidly approaching 4,000 Wassa: ▪ Working hard to ensure

growing production tpd throughput ▪ 4 Drills running on the best team and people

Prestea: ▪ Mill capacity of ~8,000 tpd surface are in place

▪ Focus on near term Prestea ▪ 4 Drills running ▪ Setting clear goals to

operational ▪ High grade extension underground reach intermediate

improvements and drilling results producer status

longer term mine plan ▪ Opportunity to expand to

redesign additional levels

NYSE AMERICAN: GSS | TSX: GSC 5

WASSA MINE QUICK FACTS

Wassa Quick Facts (ON 100% BASIS)

Ownership 90% GSR (Wassa) Ltd., 10%

Ghana

M&I Mineral Resources 3.4 Moz

Inferred Mineral Resources 6.4 Moz

P&P Mineral Reserves 1.5 Moz

Processing Plant CIL (capacity 7,800 tpd)

Gold Recovery 95.7%

Mining Type Underground (Longhole)

Wassa is in south-western Ghana, approximately 40 km from the Ramp capacity 4,000 tpd

Prestea Gold Mine. Golden Star commenced production from the

surface operation at Wassa in 2005 and commercial production was Production 2017A 137 koz

achieved at Wassa Underground on January 1, 2017. In early 2018, 2018A 150 koz

Wassa transitioned into an underground-focused operation. 2019E 150-160 koz

Wassa Underground has exploration upside through extension drilling Cash Operating Cost(1) 2017A - $880

of B Shoot North, step out drilling on B Shoot South, step out drilling 2018A - $629

on the 242 Trend and the extension of the F Shoot. This work is 2019E - $600-$650

expected to increase the mine life of Wassa Underground in the short,

medium and long term.

NYSE AMERICAN: GSS | TSX: GSC 1. See note on slide 2 regarding Non-GAAP Financial Measures.

6

PRESTEA MINE QUICK FACTS

Prestea Quick Facts (ON 100% BASIS)

Ownership 90% GSR (Prestea/Bogoso) Ltd.,

10% Ghana

M&I Mineral Resources 2.6 Moz

Inferred Mineral Resources 701 koz

P&P Mineral Reserves 317 koz

Processing Plant CIL (capacity 4,000 tpd)

Gold Recovery 87.4%

Mining Type Underground (Alimak)

Prestea is in south-western Ghana, approximately 40 km from the Shaft capacity 1,500 tpd

Wassa Gold Mine. Previously, production was being delivered from

the Prestea Open Pits and the Prestea Underground Gold Mine. In the Production 2017A 130koz

second half of 2018, Prestea became an underground-focused 2018A 75koz

operation. 2019E 40-45koz

Prestea Underground has exploration upside through the extension Cash Operating Cost(1) 2017A $632

and definition of the West Reef ore body, with the objective of 2018A $1,292

increasing the supply of high grade ore to the processing plant in the

2019E $1,450-$1,650

near term. Other focuses of the exploration program include initial

testing of the Main Reef and South Gap areas, which have the

potential to add ore to the mine plan in the medium to long term.

NYSE AMERICAN: GSS | TSX: GSC 1. See note on slide 2 regarding Non-GAAP Financial Measures.

7

WASSA - FLAGSHIP ASSET

NYSE AMERICAN: GSS | TSX: GSC 8

WASSA: 80,000 OUNCES PRODUCED IN H1 2019 AT 3,500 TPD OF ORE MINED

Q2 2019 Results

42,910

▪ Underground material mined (ore + waste) increased over 38,097 37,562 37,356

the quarter

▪ Slightly lower underground ore mined in Q2 2019 compared

to previous quarter

▪ Ore mining rate affected by limited stope access in

June

▪ Lower than planned grades encountered during the quarter

in several stopes

Q3 2018 Q4 2018 Q1 2019 Q2 2019

3.6 3.8 4.3 Gold Production (ounces)

3.5

Q2 2019 Q1 2019 Q2 2018

4,203 4,335 4,255 4,289 Ore Mined UG kt 312,115 326,747 238,953

3,406 3,364 3,631 3,430

Grade Mined UG g/t 3.51 4.31 4.99

Ore Processed kt 364,901 366,790 375,932

Q3 2018 Q4 2018 Q1 2019 Q2 2019

Recovery % 95.9 95.6 96.1

UG Ore Mining rate (tpd) UG Ore + Waste Mining rate (tpd)

UG Gold Grade mined (g/t) Gold Produced oz 37,356 42,910 38,532

NYSE AMERICAN: GSS | TSX: GSC 9

WASSA: COSTS IMPACTED BY LOWER PRODUCTION

Costs 991

946

▪ Cash operating and costs(1) AISC(1)

per oz impacted by the lower

807

production during Q2 760

▪ Underground mining and processing costs per tonne stable 613 614

656

552

quarter over quarter

Outlook

▪ The grade and mining rate are expected to stay at similar levels for

the rest of the year

▪ Revised 2019 Guidance:

▪ Production: 150,000 to 160,000 ounces (from 170,000 to Q3 2018 Q4 2018 Q1 2019 Q2 2019

180,000 ounces) Cash Operating Costs (US$/oz) AISC (US$/oz)

▪ Cash operating costs(1): $600/oz to $650/oz (from $560/oz

to $600/oz)

▪ AISC(1): $880/oz to $940 per oz (original guidance not Q2 2019 Q1 2019 Q2 2018

disclosed)

UG Mining Cost $/t ore 40 37 38

Processing Cost $/t ore 22 21 22

G&A Cost $/t ore 10 10 12

Cash Operating Costs $/oz 655 552 610

1. See note on slide 2 regarding Non-GAAP Financial Measures. AISC $/oz 941 760 994

NYSE AMERICAN: GSS | TSX: GSC 10WASSA: INCREASING VOLUME

N S

Outlook

▪ Ongoing investment to increase drill density to

anticipate lower-grade stopes and sequence them

accordingly

▪ Target 12 months of definition drilling Mined out pits

available

▪ 26,000 m of definition drilling to be

completed in H2 2019

▪ Ongoing investment to increase stope availability

Paste plant construction to start in H2 2019

▪ Commissioning expected in H2 2020

▪ Capital cost: $23 million

▪ Operating cost: $5-7 per tonne

▪ Ongoing investment to expand development to get

to 5,000 tpd

▪ Strengthen mining fleet: purchase of In Grey, mined out stopes/pits and H1 2019 definition drilling

In Blue, stopes and development for H2 2019

loaders, jumbo, 60t trucks

1,100 m

Wassa long section

NYSE AMERICAN: GSS | TSX: GSC 11PRESTEA - OPERATIONAL REVIEW UNDERWAY

NYSE AMERICAN: GSS | TSX: GSC 12PRESTEA: MINING RATE STABLE, GRADE REMAINS THE FOCUS

Q2 2019 Production Results 19,016

▪ Open pit grade and throughput higher than previous quarter

▪ Improved grade reconciliation during the quarter

▪ Low strip ratio (1.4:1) 11,284

10,374

11,065

▪ Underground mining rate slightly lower than previous quarter

▪ Rock breaker upgrade in June impacted skipping for 15 days

▪ Adjusted underground mining rate of 489 tpd excluding rock

breaker downtime

▪ Underground grade lower than previous quarter

▪ Ore sourced from stopes with low grade Q3 2018 Q4 2018 Q1 2019 Q2 2019

▪ Ongoing high level of dilution Gold Production (ounces)

10.4

8.6

6.3

Q2 2019 Q1 2019 Q2 2018

4.1

Ore Mined

kt 195,455 83,385 76,920

(Open Pit and UG)

Ore Processed kt 211,873 134,332 373,599

489 4.1 UG 6.3 UG 13.6 UG

430 408 Grade Processed g/t

376

322

1.6 OP 1.3 OP 2.3 OP

Recovery % 83.2 87.4 88.0

Q3 2018 Q4 2018 Q1 2019 Q2 2019 Gold Produced oz 11,066 10,374 22,677

UG Ore Mining rate (tpd) Adjusted UG Ore Mining rated (tpd)

UG Gold Grade mined (g/t)

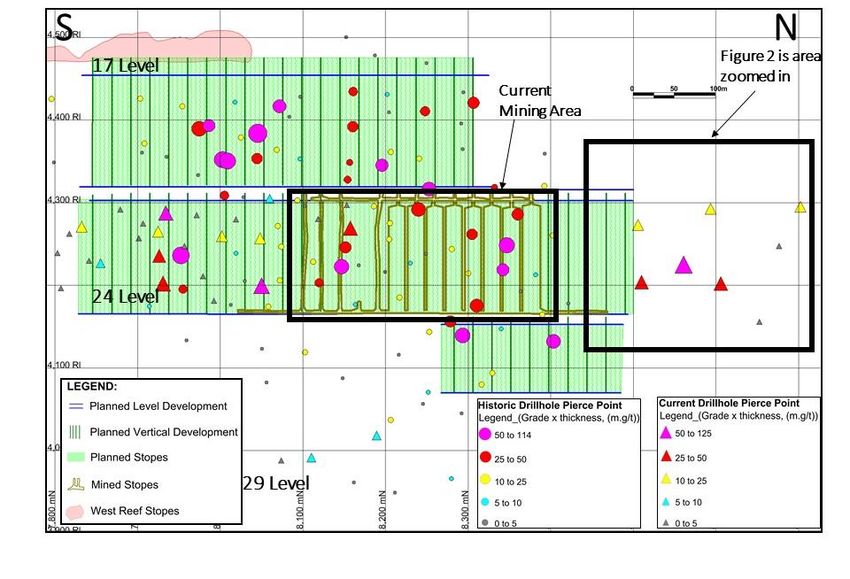

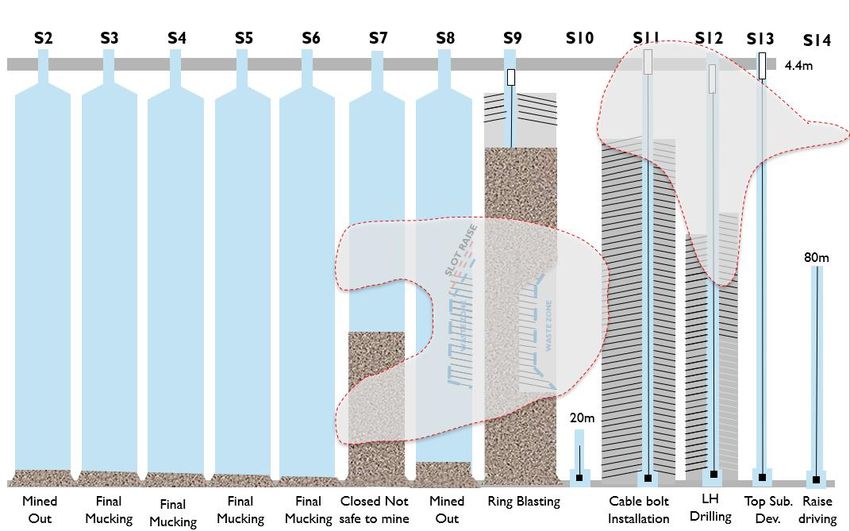

NYSE AMERICAN: GSS | TSX: GSC 13PRESTEA: WASTE ZONES CONTINUED TO AFFECT THE GRADE MINED

Q2 2019 Production Results

▪ Q2 ore sourced from S2, S4, S6, S8 and S9 Waste zones identified with definition drilling

▪ Low grade in those stopes due to:

▪ Waste zones not identified beforehand due to

lack of definition drilling

▪ High dilution related to limited QAQC on long hole 21 Level

drilling and blasting and stope height

Outlook

▪ Definition drilling at 25x25 m spacing completed

between 21 and 24 level

▪ Introduced finger raising and shorter raises to

work around the waste zones

▪ Drilling has been deferred to 2020 to help with

cash burn

▪ Positive results observed from QAQC implemented on

long hole drilling and blasting from S9 and onwards

▪ Waste from 17L skipped separately from ore since May

to improve dilution 24 Level

▪ Looking at similar options for 24L

▪ For H2 2019, ore to be sourced from S9, S11, S12, S13, Prestea Alimak stopes with status as of June 30th, 2019

S14 and development ore

▪ Grade expected to improve

NYSE AMERICAN: GSS | TSX: GSC 14PRESTEA: COSTS IMPACTED BY UNDERGROUND GRADE AND VOLUME

Costs

▪ Costs impacted by low production grade and below target throughput 2,120 2,143

▪ Largely fixed cost at Prestea Underground 1,865

▪ Cost very sensitive to grade

1,867

Outlook 1,363 1,677

▪ Underground productivity, mining rate and throughput expected to increase for H2 1,463

2019, with rock breaker, railway and ventilation raise work completed 1,110

▪ Open pit production expected to continue at similar grade during Q3

▪ Revised 2019 Guidance:

▪ Production: 40,000 to 45,000 ounces (from 50,000 to 60,000)

▪ Cash operating costs (1): $1,450/oz to $1,650/oz (from $840/oz to $1,000/oz)

▪ AISC (1): $1,900/oz to $2,150/oz (original guidance not disclosed) Q3 2018 Q4 2018 Q1 2019 Q2 2019

▪ Focus on cost reductions to minimize cash outflows

Q2 2019 Q1 2019 Q2 2018 Cash Operating Costs (US$/oz) AISC (US$/oz)

$/t Projects

UG Mining Cost 191 191 276

ore ▪ 60% of the underground railway refurbished during the quarter

$/t ▪ 80% to be refurbished by end of Q3 2019

Processing Cost 30 36 22 ▪ Reliable railway will improve throughput

ore

▪ Underground rock breaker and tipping area upgraded

$/t ▪ Rock breaker responsible for significant downtime in Q1 2019

G&A Cost 22 14 10

ore ▪ Better availability observed since installation in early June

Cash Operating Costs $/oz 1,677 1,463 1,149 ▪ New larger rock breaker to be installed in coming month to

handle higher volume

AISC $/oz 2,143 1,865 1,293

1. See note on slide 2 regarding Non-GAAP Financial Measures.

NYSE AMERICAN: GSS | TSX: GSC 15PRESTEA: INDEPENDENT REVIEW OBSERVATIONS

OBSERVATIONS INITIAL RECOMMENDATIONS AND NEXT STEPS

Well established operation Aug 2019 – Feb 2020 - Prioritisation and implementation of low-cost quick win initiatives

▪ Resource model aligned with standard Industry ▪ Increase definition drilling to provide accurate information on reef location and grade distribution

Practice within the reef

▪ Processing plant well adapted to lower throughput ▪ More than 100 low-cost initiatives identified by CSA, including:

▪ Competent workforce ▪ Develop geotechnical block model

▪ Highly prospective land package ▪ Improve supervision, implement KPIs and management operating system

▪ Multiple upside options ▪ Purchase critical small equipment (e.g. forklift) for Alimak installation and supervision

Lower grade than planned: Excessive dilution & ore loss ▪ Run a workshop on site to prioritize and cost initiatives

▪ Insufficient geological and geotechnical data ▪ Initiatives to be implemented by the operational team supported by a dedicated project team

▪ Poor definition of reef position Oct 2019 – Implementation of long-term plan

▪ Inadequate alignment of Alimak raises to reef position

▪ Low QAQC on long hole drilling and blasting ▪ Establish whether existing or modified Alimak mining is appropriate

▪ Lack of geotechnical expertise ▪ Assess whereas to introduce a complementary mining method to bring additional flexibility (trade

off review)

Lower productivity than planned

▪ Revise production and cost targets

▪ Alimak raise length (150-160 m) contributing to

poor geotechnical conditions Feb 2020 - Improvements embedded and new plan starting to deliver

▪ Low equipment mechanical availability

▪ Lack of access to top level

NYSE AMERICAN: GSS | TSX: GSC 16EXPLORATION

NYSE AMERICAN: GSS | TSX: GSC 17WASSA DEEP: EXTENDING MINERALISATION by 200m

2,000 m

Q2 2019 Results

19400N

19350N

19200N

19000N

18900N

18700N

18500N

N Mined out pits S ▪ Four rigs on site, 27 holes and 23,271 m drilled in H1 2019

▪ High grade mineralization extended 200 m south of the known

mineralization

BSDD19-394D2 ▪ Deposit remains open to the south and at depth

22.7m @ 8.9 g/t

▪ Improved understanding of the orebody thanks to infill drilling

BS18DD394D1 ▪ Confirmed continuity of the deposit grade and thickness

13.9m @ 3.2 g/t ▪ Newly converted Indicated resources expected to

17.6m @ 34.1 g/t

15.7m @ 4.1 g/t increase mine life

BSDD19004

14.8m @ 2.6 g/t BSDD19-400M Outlook

19.5m @ 5.4 g/t

1,500 m

BSDD19-396D1

14.3m @ 6.2 g/t

▪ Focus on infill drilling to convert Inferred resource to Indicated

BSDD19-394D3 resource in H2 2019

BSDD19-396D2 15.9m @ 4.5 g/t

25.6m @ 4.1 g/t ▪ 1,500 m to 2,000 m drilling remaining for 2019

BSDD19-388D3 ▪ Potential to increase mine life

25.2m @ 3.3 g/t

▪ Resource and Reserve update early 2020

OPEN

4.3m @ 12.2 g/t

29m @5.5 g/t ▪ Further work on defining geological structures

6m @12.6 g/t

8.4m @ 6.5 g/t

BSDD19-388D3

32.5m @ 5.3 g/t

4.8m @ 5.7 g/t

OPEN BS18DD392D3

12.8m @ 2.1 g/t

All drill holes represent H1 2019 drilling

22.4m @ 2.5 g/t

7.7m @ 3.7 g/t

NYSE AMERICAN: GSS | TSX: GSC 18WASSA BROWNFIELD: HIGHLY PROSPECTIVE TARGETS ALONG THE TREND

CLOSE TO HAUL ROAD Wassa Plant

SAK & Ballyebo Prospects Capacity: 7,800 tpd

Current utilization: ~3,500 tpd

Existing GSR Haul Road

85 km long from Wassa to Father

SAK Brown

Wassa Main

Ballyebo

Chichiwelli

Indicated Resources: 52 koz

(850 kt at 1.9 g/t)

Benso

Indicated Resources: 112 koz (1,200 kt at 2.9 g/t)

Abada & Apotunso Prospects Under pit intercept 15.5 m at 6.2 g/t

Veining similar to Prestea

Historical intercepts including 8 m

at 5.48 g/t Father Brown

See next slides

NYSE AMERICAN: GSS | TSX: GSC 19FATHER BROWN COMPLEX: HIGH GRADE SHOOT EXTENDED by 200m

▪ Potential ore feed to utilize available capacity at Wassa

plant located 85km north of the Father Brown Complex

▪ Infrastructure available on site

▪ Two high grade underground structures identified,

Adoikrom and Father Brown

Q2 2019 Results

▪ Improved understanding of the orebody:

▪ ADK structure interpreted as being the primary gold

bearing fluid pathway

▪ Focus drilling on ADK

▪ ADK high grade shoot confirmed by recent drilling

▪ 200m extension identified, with a 8.1 m intersect

Tonnage grading 8.7 g/t, 825 m below surface

(kt) Grade (g/t) Gold (koz) ▪ Assay results received and will be released once resource

Father Brown Indicated 656 8.67 183 update and ENTECH independent evaluation is completed

▪ Decisions on further drilling anticipated to be made in 2020

Inferred 997 5.44 174 or sooner

Adoikrom Indicated 327 5.3 55 Outlook

Inferred 1,316 7.1 300 ▪ Next resource update expected early Q4 2019

Total Indicated 982 7.5 238 ▪ 28 holes drilled since the last resource update (Dec

2018)

Inferred 2,313 6.4 475 ▪ Project viability currently being assessed

▪ Results will drive future drilling decisions

NYSE AMERICAN: GSS | TSX: GSC 20PRESTEA – HIGH GRADE EXTENSION DRILLING RESULTS

▪ 25 x 25 m infill drilling completed on the North extension, further

indicated resources in this area are anticipated to be converted to

reserves

▪ Opens additional exploration targets

▪ Potential addition to the resources and reserves on 24L

NYSE AMERICAN: GSS | TSX: GSC 21CORPORATE RESPONSIBILITY

NYSE AMERICAN: GSS | TSX: GSC 22CORPORATE RESPONSIBILITY & HEALTH AND SAFETY

LEADING PRACTICE

LOCAL CONTENT

▪ Featured in UN Global Compact Canada Leading Practice

Guide Sustainable Development Goal (SDG) 1,3 & 81 ▪ Employees 30% host community and 98% Ghanaian

▪ Over 250 workforce safety champions ▪ Contractors 74% host community

▪ Oil palm plantation supports over 700 families

▪ Featured in UN Global Compact Canada Leading Practice PARTNERSHIP

Guide SDG 1 & 8 ▪ Community agreements in development for Wassa operations

▪ World Environment Day celebrations

LEADERSHIP & PERFORMANCE

▪ 93% of leaders completed leadership training WORLD GOLD COUNCIL

▪ 10 safety standards developed by workforce

▪ TRIFR of 1.19 in line with peer group ▪ Golden Star is a member of the World Gold Council (“WGC”)

▪ Near miss reporting 2.5 times better than 2017 ▪ 10 Responsible Gold Mining Principles (“RGMPs”) were recently

▪ Systems enhanced disclosed by the WGC which are aligned with the approach

▪ No reportable environmental incidents Golden Star carries out its business:

▪ 100% conformance to statutory monitoring and 1. Ethical conduct

regulatory guidelines 2. Understanding our impacts

3. Supply chain

MALARIA 4. Safety & Health

▪ Least cases in 7 years 5. Human rights & conflict

▪ Order of magnitude better than background 6. Labour rights

▪ Case rates just 0.35 per capita 7. Working with communities

8. Environmental stewardship

9. Biodiversity, land use & mine closure

10. Water, energy and climate change

NYSE AMERICAN: GSS | TSX: GSC 23

1. Details available on the Company website , or here http://www.gsr.com/responsibility/SDG/default.aspxWRAP-UP

▪ Proven focus on responsible mining recognized with several industry awards

in Ghana and internationally

▪ Two operating assets and significant landholding in highly prospective,

under explored proven Ashanti gold belt

▪ Wassa: underground deposit in excess of 5.6 Moz of Inferred and 1.7 Moz

of M&I Mineral Resources with estimated 2019 production of 150-160 Koz

with significant growth potential

▪ Prestea: high grade underground deposit with current operational review

underway to improve performance and return to free cash generation

▪ Optionality from other satellite deposits, including Father Brown, to utilize

latent installed processing capacity at both sites

▪ Long track record of operating successfully in Ghana, a well developed and

stable mining jurisdiction in West Africa with excellent relationships with

our stakeholders

▪ New COO with extensive underground mining expertise

NYSE AMERICAN: GSS | TSX: GSC 24

24THANK YOU – Q&A

CONTACT US

Tania Shaw, VP, Investor Relations &

Corporate Affairs

+1.416.583.3800

investor@gsr.com

NYSE American: GSS

TSX: GSC

NYSE AMERICAN: GSS | TSX: GSC 25You can also read