DECARBONISING EUROPEAN INDUSTRY: HYDROGEN AND OTHER SOLUTIONS 'CARBON-FREE STEEL PRODUCTION'

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

DECARBONISING EUROPEAN INDUSTRY:

HYDROGEN AND OTHER SOLUTIONS

‘CARBON-FREE STEEL PRODUCTION’

1/03/2021 Frank Meinke-Hubeny, 01.03.2021

©VITO – Not for distribution 1

BACKGROUND

Publication of the Scientific Foresight Unit (STOA)

EPRS | European Parliamentary Research Service

Jan/Feb 2021

Authors:

Frank Meinke-Hubeny, Juan Correa Laguna,

Joris Valee and Jan Duerinck (EnergyVille/Vito NV)

1/03/2021

©VITO – Not for distribution 2

SCOPE OF THE STUDY

Steel Production in Europe Production & Supply of Hydrogen

Established steel production paths Hydrogen Infrastructure

Steel products and applications Hydrogen Backbone

Decarbonisation paths Transmission and distribution

Hydrogen-based steel production Transmission costs

Blending and retrofitting

Case Study “A Long-term vision on Storage of Hydrogen

steel production”

1/03/2021

©VITO – Not for distribution 3

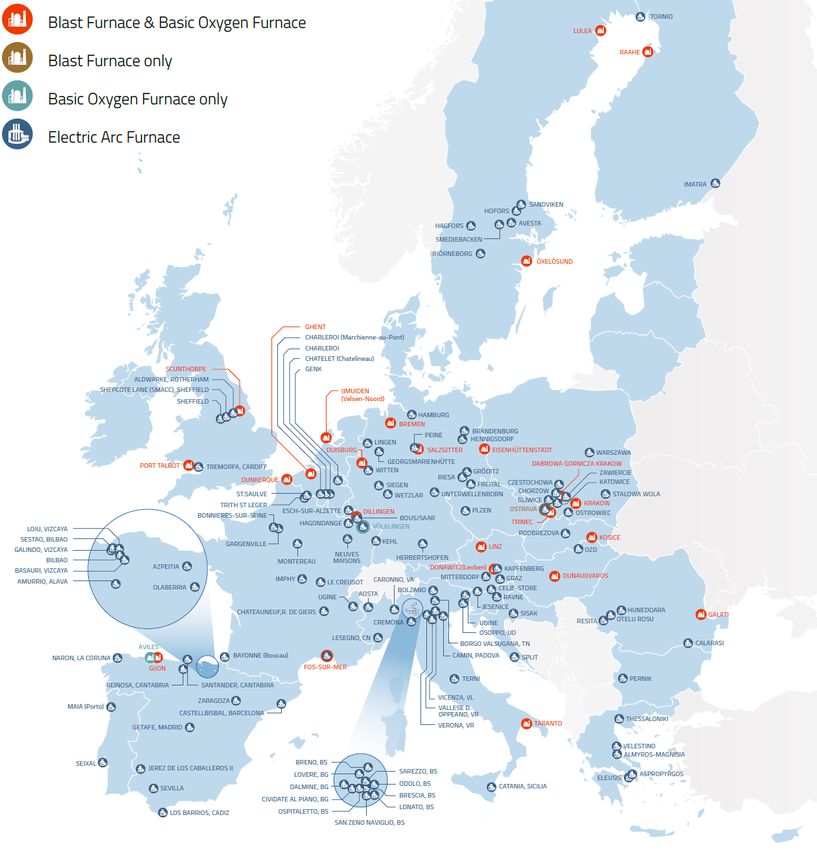

STEEL PRODUCTION

IN EUROPE

Steel is produced throughout Europe

But the main steel plants are located

in clusters

Share per country …

Germany 25.1%

Italy 14.8%

France 9.2%

Spain 8.6%

Poland 5.7%

Belgium 4.9%

Austria 4.7%

UK 4.6%

Netherlands 4.2%

…

1/03/2021

©VITO – Not for distribution 4

STEEL PRODUCTION IN EUROPE

Steel is produced

in different routes

Each route has a

specific CO2 footprint

Primary route

BF/BOF

~1.9 tCO2/tsteel

Secondary route

Scrap/EA

~0.4 tCO2/tsteel

Primary route

Source: Secondary route

1/03/2021 ~60% or 94 Mt World steel association, 2019

©VITO – Not for distribution 5

STEEL USES AND FINAL PRODUCTS

Different steel

applications

require different

steel qualities

2 main categories

Long steel

(= lower quality)

Flat steel

(= higher quality)

Source: EUROFER, 2020

1/03/2021

©VITO – Not for distribution 6

HYDROGEN-BASED STEELMAKING

To make Europe’s primary flat steel of

94 Mt carbon neutral requires …

37-60 GW of electrolyser capacity

EU Hydrogen Strategy aims for

40 GW installed within the EU by 2030

296 TWh of green electricity equal to ….

~10% of all EU electricity (2 724 TWh)

~1.7 x Germany’s green electricity (2020)

1/03/2021

©VITO – Not for distribution

Source: Own elaboration 7

PROJECTS IN EUROPE H2-DRI projects in Europe

HYBRIT 1: LKAB4:

Hydrogen Breakthrough Ironmaking The mining group plans to integrate

Technology is a joint venture of SSAB, downstream and initiate trading sponge iron

LKAB, and Vattenfall, launched in 2016 in produce entirely using H2 from renewable

Several H2-DRI pilot projects Sweden, with the aim to have a fossil-free

steel production solution by 2035. This will

energy sources. In other words, it will install

hydrogen shafts (H-DRI), without the EAF

help SSAB to be practically carbon-free by step.

within the EU 2045. Voestalpine5:

ArcelorMittal :2

The production facility in Linz, Austria, in

In 2019, ArcelorMittal started association with VERBUND, Siemens, Austrian

Targeted time frame from 2035 to collaborating with Midrex to build a Power Grid, K1-MET, and TNO are under

production plant able to annually produce development. With 6 MW of electrolyzer

2050 0.1 Mtsteel using only H2 as a reductant capacity, the project expects to reduce by

agent in Hamburg, Germany. It will initially 30% the emissions of Voestalpine by 2035,

start production using grey hydrogen and with the final goal of reducing the emission

be ready for when green hydrogen supply by over 80% by 2050.

All projects in early development is reliable and affordable.

Salzgitter6:

Thyssenkrupp 3:

stages, meaning high uncertainty In partnership with REW, the steel

With the project SALCOS, the company

expects to develop and demonstrate the

about … producer expects to convert its current

BF/BOF production into H-DRI by 2050.

techno-economic feasibility of hydrogen-

based steel production. The project is divided

Technical parameters (efficiency at Starting with the facilities in Duisburg (2% into several stages: demonstration of MW

of Germany's CO2 emissions) in 2025, one scale electrolyzer, wind power production

large scale, etc.) of the main challenges is the need for a onsite, pipe for H2 transport and storage, and

pipeline to transport H2 from Lingen to the final profitability for steel production.

Cost (CAPEX, OPEX, fuel H2) plant. If H2 is not available in the quantities

Liberty Steel Group7:

needed, the plant will start running on

natural gas. Constriction of a DRI/EAF plant to produce 2

Mtsteel. It will be designed to phase into H2

from natural gas (grey H2), reaching carbon

neutrality by 2030.

1/03/2021

©VITO – Not for distribution Source: Own elaboration 8

PROJECTED STEEL PRODUCTION COST

By 2030, the alternative routes will By 2050, H2-DRI could be the least

increase the end product cost by 5-24%, costly way to produce steel (given a

Equal to an abatement cost of €73-€166 CO2 price).

per ton of CO2 (compared to BF/BOF)

H2-DRI cost decrease -

cheaper electricity & electrolyzer costs

2050

Primary route -

cost increase due to

1/03/2021

©VITO – Not for distribution

EU ETS (84€ -> 160€) Source: Own calculation & elaboration 9

PROJECTED STEEL PRODUCTION COST – HYDROGEN BASED DRI

Delivery of low cost carbon-free electricity essential € 716/t

Impact of electricity price in H-DRI steel production - 2050

steel

(€80/MWh) 20%

Alternative: Hydrogen delivery to the steel sites at competitive prices 39%

€20/MWh

Impact of electricity price in H-DRI steel production - 2050

€ 446/tsteel

2050 € 716/tsteel

(€80/MWh)

(€20/MWh)

Impact of electricity price in H-DRI steel production - 2050

Production20%

price 39%

€20/MWh €50/MWh

sensitivity

€ 716/tsteel

(€80/MWh)

€ 446/tsteel 20%

(€20/MWh) to €(€80/MWh)

716/tsteel

20% 39% 50% €80/MWh

electricity Share of

€20/MWh €50/MWh39%

prices electricity

€ 446/tsteel €20/MWh €50/MW

(€20/MWh) cost

€ 446/tsteel

(€20/MWh) in final steel

50% €80/MWh

Others Electric

product

H2-DRI/EAF

Others Electricity 50% €80/MWh

H2-DRI/EAF 50% €80/MWh

Others Electricity

1/03/2021 H2-DRI/EAF Others Electricity

Source: Own calculation & elaboration

©VITO – Not for distribution H2-DRI/EAF 10LONG-TERM GLOBAL STEEL PRODUCTION AND SCRAP AVAILABILITY

Case Study “A Long-term vision on steel production “ (Vito & KTH, 2018)

13 world regions,

Projected demand for long and flat steel,

Projected availability of steel scrap,

Projected trade among the world regions. Steel scrap

+167% by

2070

Global Flat steel +87% by 2070 Global Long Steel +30% by 2070

Source:

Vito, KTH (2018)

1/03/2021

Global Steel production by Technology

©VITO – Not for distribution 11LONG-TERM GLOBAL STEEL PRODUCTION AND SCRAP AVAILABILITY

Case Study “A Long-term vision on steel production “ (Vito & KTH, 2018)

Trade of scrap and finished products among regions balances demand & supply

Well developed regions (e.g. Europe) net-exporters, maintaining production capacities

Results are highly sensitive to unilateral GHG policies (e.g. CO2 taxes)

Stable demand & Steel scrap

production for high (recycling) in long

quality steel in EU products

1/03/2021

European Steel Production Scenarios Source: Vito, KTH (2018)

©VITO – Not for distribution 12used.

HYDROGEN PRODUCTION

Obtained by electrolysis

It faces the public acceptance

Purple/ of nuclear plants and the

linked to a nuclear power CO2 free

Pink phase-out plans defined by

plant.

Established ‘colour scheme’ for hydrogen by technology & fuel several Member States.

Turquoise hydrogen is a by- It is highly energy-intensive.

Type of Hydrogen Production

product of methane

Considerations

The current market will not be

Emission Factor

Turquoise

Selected ‘colours’- see report for full overview

(natural

Produced

which

gas) pyrolysis,

through

splits methane

coal

into

able to absorb the massive

It is a highly

amounts ofpolluting

carbon process

black

CO2 free

Brown/ gasification. The colour

hydrogenongas and ofsolid since both CO and CO are not

produced (Wiley-VCH-GmbH,

2 19 tCO2/tH2

Black depends the type coal

carbon. reused

2020). and, thus, released into (IEA, 2019)

used: brown (lignite) or

the atmosphere.

black

It does(bituminous)

not havecoal. yet an

Type of Hydrogen Production Considerations Emission Factor

established colour to be

Produced from fossil fuels, Although it is a mature

classified. through

Produced Produced coal by Several technologies are being

most commonly from It is a highlyitpolluting

technology, involves process

Grey

Sunlight

Brown/ photocatalytic

gasification. The colourwater developed but are stillnotable

at the CO2 free

natural since both CO2 and COasaremass

not 19 tCO22/tH22

Black splitting gas

depends on the

with through

typeenergy,

solar the

of coal disadvantages such

lab or small prototype scales. 10

SMR process. Less reused

and heat transfer issues, as into

and, thus, released well (IEA,

(IEA, 2019)

2019)

used:

withoutbrown (lignite) the

going through or

commonly it uses coal.

the ATR thecoke

as atmosphere.

deposition during the

black (bituminous)

electrolysis step.

process reaction.

Produced frombyfossil water

Produced fuels, Although it is a mature Power grid factor

Yellow electrolysis

It is produced

most utilising

commonly in the using

same

from technology, it involves notable

Grey Since the origin of the power is (gCO2/kWh).

the

way power

natural as gasof through

brownmixed or origin

grey

the Depends on thesuch

disadvantages availability of

as amass 10 tCO /tH

Blue not carried, it could have high Incurred

0.64 T&D

– 20.99 losses

2 tCO 2/tH2

from

SMR the process.

hydrogen, grid

but(others

its COrefer

2 is

Less carbon

and storage (CCS) or carbon

CO2 heat transfer

emission issues,

factor as well

associated. (IEA,

should

(CE 2019)

be2018)

Delft, accounted

to hydrogen

captured

commonly itproduced

anduses the from

stored or

ATR use (CCU).

as coke deposition during the for.

solar

used.

processpower) reaction.

It is produced by

It faces the public acceptance

It is produced

Obtained

electrolysis by inelectrolysis

the using

of water, same Availability of RES and water

Green

Purple/ of nuclear plants and the CO2 free

Blue way

solely asto electricity

linked brown

a nuclear or power

grey

from Depends

play a keyon the availability of

role. CO2 free

Pink phase-out plans defined by 0.64 – 0.99 tCO2/tH2

hydrogen, but itssources.

renewable energy

plant. CO2 is carbon storage (CCS) or carbon

several Member States. (CE Delft, 2018)

captured and stored or use (CCU).

used.

Turquoise hydrogen is a by- It is highly energy-intensive.

Turquoise product of methane The current

It faces the market will not be

public acceptance

Obtained gas)

(natural by electrolysis

pyrolysis, able to absorb the and

massive

Purple/ of nuclear plants the CO

linked splits

which to a nuclear

methanepower

into amounts CO22 free

free

Pink phase-out plans definedblack

of carbon by

1/03/2021 plant.

hydrogen gas and solid produced (Wiley-VCH-GmbH,

several Member States.

©VITO – Not for distribution carbon. 2020). 13HYDROGEN PRODUCTION

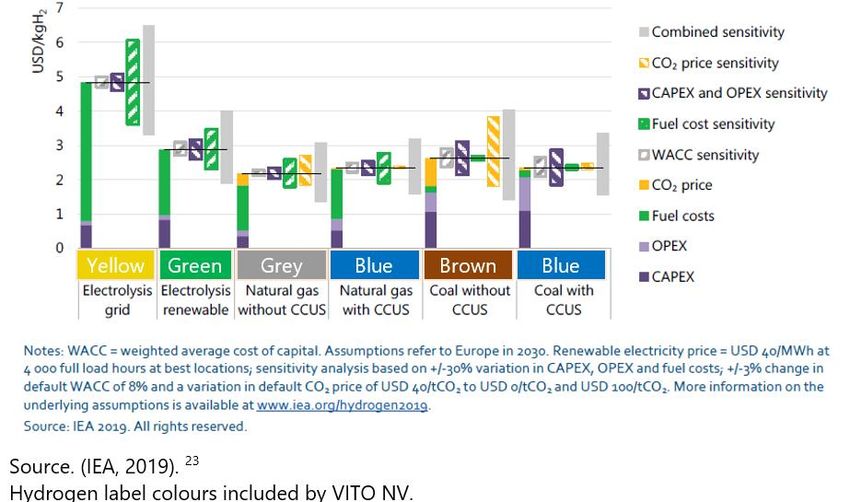

Hydrogen production costs for different technology options in 2030

Selected colours

1/03/2021

©VITO – Not for distribution 14HYDROGEN OVERALL DEMAND

Vision on Europe’s future hydrogen demand by sector 2030 & 2050 (FCH-JU)

TWh

by 2050:

Hydrogen demand

New Industries 7.8 Mt H2

of which …

Steel Sector 4.2 Mt H2

(own calculation ~6.6 Mt)

1/03/2021

©VITO – Not for distribution 15HYDROGEN INFRASTRUCTURE

Europe’s gas transmission ~260 000 km & distribution pipelines of 1.4 million km

Compared to appr. 2 000 km of existing hydrogen pipelines

The natural gas grid is operated by different organizations across the EU

Existing European natural gas network Existing European non-natural gas network

1/03/2021

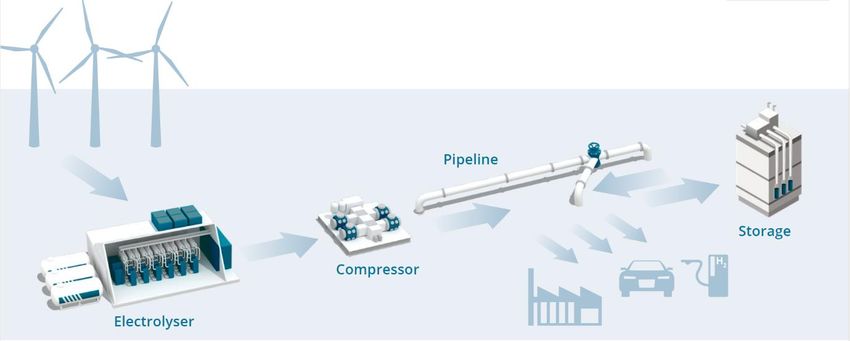

©VITO – Not for distribution 16HYDROGEN PRODUCTION AND TRANSPORT ROUTE USING PIPELINES

High CAPEX of new H2 pipelines are a challenge for

the infrastructure deployment and demand proliferation.

Potential technical challenges:

Hydrogen embrittlement → pipelines cracks and fractures at stresses

Hydrogen leaks and safety conditions

Improved compression system for hydrogen required

Asses potential, location and needs for hydrogen storage at big scale

1/03/2021

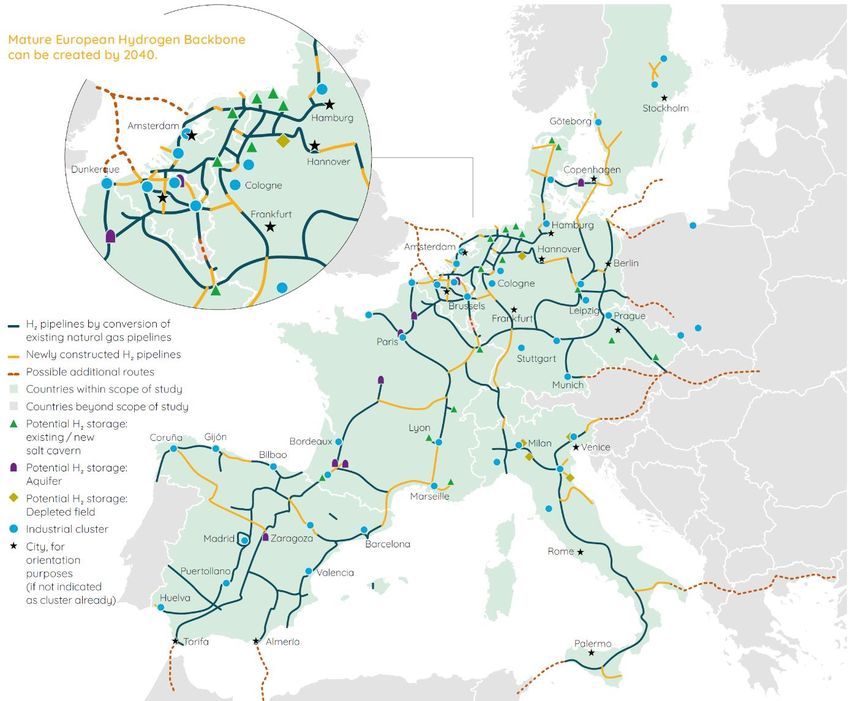

©VITO – Not for distribution 17EUROPEAN HYDROGEN BACKBONE – MAIN TAKE AWAYS

The European backbone to follow

~23 000 KM of

hydrogen valleys -> existing dense hydrogen network,

industrial clusters 75% repurposed

pipes

Blending 10% of hydrogen will lead

to a carbon emission reduction of

only 3%.

Storing hydrogen requires 3 times

more space than natural gas for the

same amount of energy.

Blending might create fragmentation

in the EU gas market due to

differences in the quality of the gas.

Regulatory frameworks required for

network operators to own, operate

and finance hydrogen pipelines.

1/03/2021

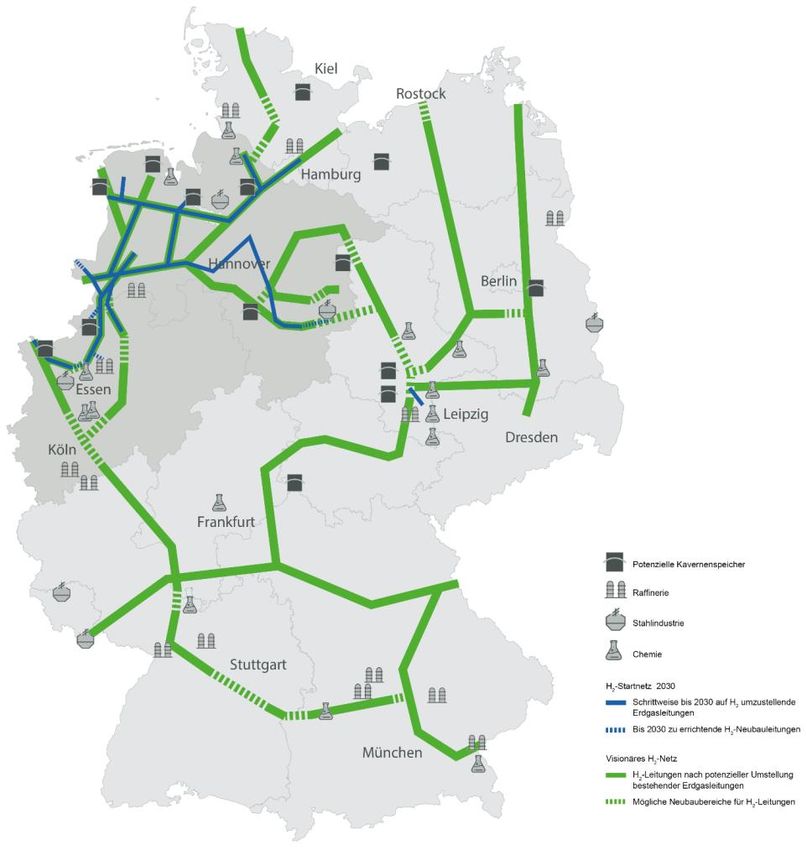

©VITO – Not for distribution 18NATIONAL HYDROGEN BACKBONE IN DE (2030) – PROPOSED BY FNB GAS

Connect H2 imports, local hydrogen

production from wind and solar with

steel and petrochemicals sites.

The plan is to build a 5 900 km

hydrogen grid (90% repurpose

pipelines).

FNB Gas estimates the cost to be 10-

20% of the cost of building new H2

pipelines.

1/03/2021

©VITO – Not for distribution 19‘FIRST’ INSIGHTS IN COSTS - PIPELINES

Component Value (2019) Comment Source

Current projects are pilot or research Investment

repurposing existing

M€ 0.37/km Germany based case, cost of repurposing

15% compared to the new pipeline

[1]

pipelines

projects and context specific (excl. compressors).

Investment cost new M€ 0.93/km 16-inch average diameter. Costs for [2]

pipeline (range) transmission of 6 300 km in the UK.

Repurposing offers cost savings and M€ 2.1/km The 48-inch pipeline, operating between [3]

30-80 bar with a length of 300 km in the

reduced execution time (limited M€ 3.28/km

UK.

[4]

48-inch pipeline.

permitting) (excl. compressors)

Investment New M€ 0.65/MW Costs for a 5.8 MW compressor, with a 240 [5]

Focus on strategic connections and compressor (range)

M€ 1.07/MW

t/day throughput.

5.8 MW capacity for compressor, calculated [4]

advantageous conditions for first according to cost curve in source

(compressors are required every 100-600

implementations km, highly case-specific)

LCOT for H2 M€ 3.7/MWh H2 Repurposing existing gas infrastructure for [6]

transmission – per 600km 100% hydrogen.

‘Later stage’ capacity increase possible by repurposing natural

gas infrastructure

upgrade of compressors (higher flow LCOT for H2 M€ 4.6/MWh H2 48-inch pipeline. Includes pipeline and [6]

transmission - New per 600km compressor CAPEX and OPEX and

rate) natural gas compression fuel-related costs.

infrastructure (range)

M€ 11.4/MWh Transportation over 1500 km is assumed [7]

H2 per 600km by source, considering all capital and

operating costs. Normalised to 600 km.

M€ 45/MWh H2 Estimated including compression costs for [8]

per 600km pipes of diameters between 7-10 inches

1/03/2021 over 100 km as assumed by source.

Normalised to 600 km.

©VITO – Not for distribution 20‘FIRST’ INSIGHTS IN COSTS - STORAGE

Investment Costs

Similar to natural gas, end-use Technology Range (2019) Comment Source

Depleted gas field €280 - 424 /MWh CAPEX including compressors and pipes, [1]

sectors will require constant H2 stored 4% OPEX.

molecule flow, but context &

Salt caverns €344 /MWh H2 CAPEX for 1,160 t of working capacity (+1/3 [1]

application specific stored additional for cushion gas), but highly

dependent on geography. 4% OPEX,

includes compressors and pumps.

Hydrogen storage needed, Rock caverns €1 232 /MWh H2 4% OPEX. [1]

approximately 3x volume vs. stored

Levelized Cost of Storage

natural gas

Technology Range (2019) Comment Source

Tank €0.17 kg H2 Compressed state hydrogen at 5 – 1 100kg [1]

First pilot projects under per container

€4.1 kg H2 Liquid state hydrogen at 0.18 - 4 500t H2

evaluation per tank

Depleted gas field €51 - 76 /MWh H2 Cost for working gas capacity, 1 cycle/year. [1]

Including the cost of compression and

See report for overview of pipelines needed for the facility to

initiatives & cost projections function.

Salt caverns €6 - 26 /MWh H2 300-10,000 t per cavern, lower bound: [1]

monthly cycling, upper value: bi-annual [2]

€17 /MWh H2 cycling.

Rock caverns €19 - 104 /MWh 300-2,500 t per cavern, lower bound: [1]

H2 monthly cycling, upper bound: bi-annual

1/03/2021 cycling.

©VITO – Not for distribution 21… keep in touch!

Frank Meinke-Hubeny

Sr. Researcher | Project Manager – Sustainable Energy

Unit Smart Energy & Built Environment

HQ: VITO NV | Boeretang 200 | BE-2400 Mol

Office: EnergyVille I | Thor Park 8310 | BE-3600 Genk

Phone +3214335820 | Frank.Meinke-Hubeny@vito.be

1/03/2021

©VITO – Not for distribution 22You can also read