Deloitte 2021 M&A Tax Virtual Conference Break-out Session Germany: W&I Insurance update for investments in Germany - 04 MARCH 2021

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Deloitte 2021 M&A Tax Virtual Conference Break-out Session Germany: W&I Insurance update for investments in Germany 04 MARCH 2021

Day 4: Trends and future of corporate M&A

Introduction and Contacts

Andrea Bilitewski

Partner, Tax & Legal | M&A

Hamburg, Germany

E-Mail: abilitewski@deloitte.de

W&I Insurance is a growing solution not

only for PE Investors but also for

corporate deals.

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 2

Contents Distribution of Risk with the Help of W&I 4 Contingent Tax Risk Insurance 11 Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 3

W&I Insurance Distribution of Risk with the Help of W&I Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 4

Day 4: Trends and future of corporate M&A W&I Insurance – Agenda Agenda • W&I Insurance – Coverage of Unknown Transaction Risks • Available Insurance Products • W&I Insurance – Importance of the Due Diligence Process • W&I Insurance – Scope of Coverage and Costs • Excursus: Contingent Tax Risk Insurance Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 5

Day 4: Trends and future of corporate M&A

W&I Insurance – Coverage of Unknown Transaction Risks

Known Risks Unknown Risks

If the Seller is already familiar with

existing risks, he can disclose them Unknown risks are generally

within the SPA (disclosure schedules) economically allocated to the Seller by

or agreeing on warranties & indemnities

Risks are being discovered within the within the SPA.

Due Diligence Process

Known risks must be They cannot be

considered by the buyer considered when

when calculating the calculating the purchase

purchase price. price.

NOT INSURABLE INSURABLE

Allocation of risks:

• Risks, that are known or that are assumed to be known (because they could have been identified from the

documents in the data room) are no longer born by the Seller, but instead by the Buyer.

• In case the Seller‘s liability for unknown risks is excluded or limited within the SPA, the implementation of a

W&I Insurance, serving as an alternative solution, is possible.

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 6

Day 4: Trends and future of corporate M&A

Available Insurance Products

Product Description

W&I Insurance • Insures unknown risks resulting from violation of

guarantees/exemptions by the Seller

• The W&I Insurance Policy is built upon the SPA and assumes the

liabilities of the Seller arising from the SPA – with regard to both,

cause and amount.

• However, certain risks are not typically insurable.

• Nevertheless, extending the insurance scope is possible in

particular cases.

Contingent Risk Insurance • Insures potential losses that results from known, but uncertain or

non-quantifiable risks

• Upcoming trend in practice: Contingent Tax Risk Insurance

(Insurance of known risks)

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 7

Day 4: Trends and future of corporate M&A

Importance of the Due Diligence Process

• The Due Diligence serves to uncover previously unknown risks or risks not expressly disclosed by the seller.

• Therefore, a comprehensive Due Diligence is a mandatory prerequisite for the insurability of the transaction.

• Principle: Insurance only of risks that have been subject to a Due Diligence

• Periods of investigation

• Certain areas of topics (e.g., tax types)

• Scope and depth of investigation

• Materiality thresholds

• Thus, the Scope of Work of all DD-work streams needs to be adjusted to the desired insurance scope.

• Quality of the DD as well as transparent documentation is of major importance for the insurance company

and accelerates underwriting.

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 8

Day 4: Trends and future of corporate M&A

W&I Insurance – Scope of Coverage and Costs

Costs

• The policy causes a one-time insurance fee

• Real Estate: pricing ranges between 0.6% - 0.8% of the maximum coverage.

• Operational Businesses: pricing ranges between 0.8% - 1,5% of the maximum coverage

(depending on kind of business and jurisdiction).

• Insurance deductible:

• Real Estate: often 0%.

• Operational Businesses: 0.25-1% of the enterprise value.

• Coverage of specific knows risks sometimes possible, but mostly dependent on facts.

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 9

Day 4: Trends and future of corporate M&A

W&I Insurance – Common Coverage Exemptions and Market Trends

Common Coverage Exemptions Market Trends

• Fines and judicially not insurable penalties

• Environmental risks (contamination/pollution) – however,

licenses and authorizations can be covered)

• Sanctions

• Product liability

• Conditions of property Assessment and coverage of IP becomes more common

• Bribery and corruption Negotiable in particular cases

• Cyber risks

• Under financed pension plans Negotiable in particular cases

• Consequential and multiplied damage Negotiable in particular cases

• Transfer prices In certain industries and jurisdictions, risks resulting from

transfer prices are more often negotiable.

• Pricing adjustments after closing/ compensation of leakage However, hedging of clearly defined risks might be possible.

• Tax-loss carryforwards Usage of tax-loss carryforwards are increasingly negotiable

• Tax risks resulting from future changes in law In some cases negotiable, i.e. in the area of German Real Estate

transfer tax.

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 10Excursus Contingent Tax Risk Insurance Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 11

Day 4: Trends and future of corporate M&A

Conditions & Pricing for Contingent Tax Risk Insurance

Conditions

• Tax risks with limited probability, but high value.

• Resulting from a historical or planned transaction, where the legal position is ambiguous.

• No interest in insuring aggressive tax structures/ tax prevention.

• The own legal position must be resilient on the basis of the applicable laws and existing case law - presented by a so-called

should-opinion of a qualified advisor.

• The market expands beyond M&A, to non-transactional risks, like restructuring and transfer pricing.

Pricing

Generally 2% - 6% of maximum • Strength of the technical position • Market Conditions

coverage

• Discovery risk • Size of risk

• Affected legal system / country • Time frame

• Quality of broker services

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 12Deloitte 2021 M&A Tax Virtual Conference Break-out Session Germany: German tax reforms in light of international investments 04 MARCH 2021

Day 4: Trends and future of corporate M&A

Introduction and Contacts

Dr. Stefan Berg

Director M&A Tax

Munich

E-Mail: sberg@deloitte.de

Change is the only constant.

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 2Contents Passed Tax Reform Agenda 4 Pending Tax Reform Agenda 7 Hybrid mismatch rules 10 German CFC rules 12 Future Tax Reform Agenda 14 Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 3

Passed Tax Reform Agenda Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 4

Day 4: Trends and future of corporate M&A German tax reforms in light of international investments Tax Reform Agenda Passed: • Corona Subsidies • DAC 6 Reporting Pending: • Additional Corona Subsidies • RETT share deals • ATAD transformation State of play: Federal elections in autumn – real progress questionable before election date; governing parties have switched into campaign mode To come: • Digital Services Tax? • Pillar 1 and 2 transformation • Tax Haven - ”Defense” Act Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 5

Day 4: Trends and future of corporate M&A German tax reforms in light of international investments Tax Reform Agenda – Passed: Corona Subsidies: 1st and 2nd Corona-Tax-Aid Act (June 2020 each) • Topics of interest from an inbound M&A perspective: Extension of period for retroactively tax effective reorganizations from 8 to 12 months; Temporary reduction of (i) standard VAT rate from 19% to 16% and (ii) reduced VAT rate from 7% to 5%, each from 1 June 2020 until 31 December 2020 (only); Tax losses can carried back in previous FY in amount of 5m EUR, instead of 1m EUR only; plus – upon application – preliminary tax loss carryback from FY2020 into FY19 in amount of 30% of taxable income of 2019, if (inter alia) prepayments for FY202 set to zero; 1m EUR threshold of German minimum taxation rule for TLCF lifted to 5m EUR for FY20 and FY21; (change-in-ownership rules unchanged, however) Asset deals: Digressive amortization for (permanent) movables, acquired in FY20 or FY21, reintroduced, max. 25% or 2.5x of standard amortization per FY; TT interest expense add-back: Threshold of 100k EUR lifted to 200k EUR per FY; and Filing deadline for CIT/TT returns for 2019 extended to August 2021 (if prepared by tax adviser). DAC 6 Reportings: First reactions of FTA: Investigating on correct declaration of applicable statutory tax rules Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 6

Pending Tax Reform Agenda Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 7

Day 4: Trends and future of corporate M&A German tax reforms in light of international investments Tax Reform Agenda – Pending: 3rd Corona-Tax-Aid Act Increase of tax loss carry-back from 5m EUR to even 10m EUR, plus preliminary carry-back also for 2020 • Status: Very likely to come RETT on share deals • Core features of new rules: Blocker threshold reduced from 5% to 10% Introduction of watching period for corporate share transfers, similar to existing 5Y watching period for partnership interests Extension of (existing) watching period from 5 years to 10 years Retroactive implementation • Status: Unclear, hot topic on government’s agenda last year – radio silence currently, disputed among government parties; likely to come after federal elections Unclear status affects the market more than new rules themselves, given uncertainty of possible structures and interpretation/approach of German tax authorities Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 8

Day 4: Trends and future of corporate M&A German tax reforms in light of international investments Tax Reform Agenda – Pending: Implementation of ATAD – of interest from an M&A perspective: Hybrid mismatch rules: Limitations to expense deduction – inbound investments German CFC rules: Limited changes only, EU Directive followed German approach more or less – relevant for outbound investments • Status: Government was to decide in April 2020 on “ATAD Implementation Act” – radio silence since then Transfer pricing rules: transfer of functions and transfer pricing of intra group transactions – of relevance e.g. for intra group acquisition financing and service agreements, as well as profit allocation for permanent establishments, “exit tax” due to cross-border transfer of functions, and well as arm’s length dealing • Status: Initially also part of the “ATAD Implementation Act”, now included into recent draft of “WHT Modernization Act”, dated January 2021 – again unclear whether implemented prior to elections, but outsourcing sign for minimal compromise among governmental parties? Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 9

Hybrid mismatch rules Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 10

Day 4: Trends and future of corporate M&A

German tax reforms in light of international investments

Hybrid mismatch rules – limitations on expense deduction, esp. for inbound acquisitions

§ 4k (1) EStG-E

Mismatch between financial income and expense Art. 2 (9) lit. a ATAD II

§ 4k (2) EStG-E

Deduction/ Mismatch between qualification of taxpayer or Art. 2 (9) lit. e ATAD II

underlying agreement; deemed payments

Non-Inclusion Art. 2 (9) lit. f ATAD II

(D/NI)

§ 4k (3) EStG-E

Mismatch of allocation of payments to hybrid entities, Art. 2 (9) lit. b ATAD II

permanent establishments or unrecognized permanent

Art. 2 (9) lit. c ATAD II

establishments

Art. 2 (9) lit. d ATAD II

Art. 9a ATAD II

Double § 4k (4) EStG-E

Deduction Mismatch of allocation of exclusive deduction or Art. 2 (9) lit. g ATAD II

(DD) mismatch of tax residence

Art. 9b ATAD II

§ 4k (5) EStG-E

Art. 9 (3) ATAD II

Imported mismatch of taxation

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 11German CFC rules Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 12

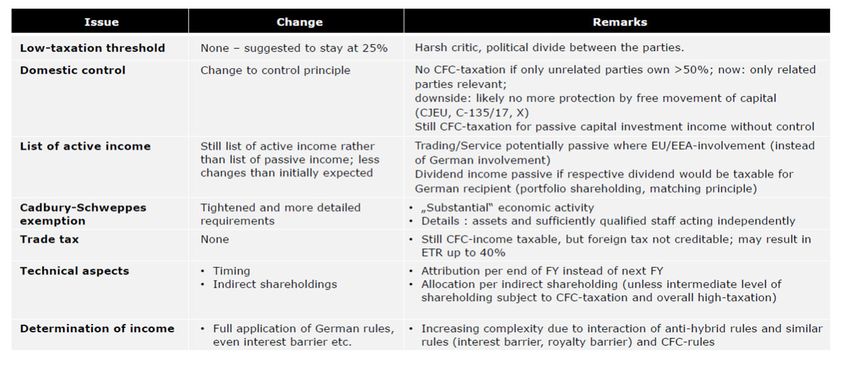

Day 4: Trends and future of corporate M&A German tax reforms in light of international investments German CFC rules – to be monitored for outbound investments Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 13

Future Tax Reform Agenda Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 14

Day 4: Trends and future of corporate M&A German tax reforms in light of international investments Tax Reform Agenda – To come: • Digital Services Tax? – not yet in Germany, but moving ahead at European level; so far only certain VAT rules implemented • Pillar 1 and 2 transformation: Supported by German MoF Not directly of relevance for M&A currently, but going forward focus of tax DD exercises will shift from standalone or country analysis to comprehensive tax (allocation) analysis Tax Haven - ”Defense” Act – First draft Punitive measures on taxpayers having (i) shareholders in, (ii) subsidiaries in, and/or (iii) (deemed) business relationships with counterparties located in “non-cooperative” (i.e. black listed) jurisdictions Limitation of business expense deduction; unlimited CFC taxation; no WHT relief for foreign shareholders; no participation exemption; application of German tax regime for non-residents; increased compliance/documentation obligations To become effective as of 1 January 2022/ resp. 1 January 2023 Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 15

Deloitte 2021 M&A Tax Virtual Conference Break-out Session Germany: Corporate: Carve out structures and challenges 04 MARCH 2021

Day 4: Trends and future of corporate M&A

Introduction and Contacts

Stella Posnak

Partner M&A Tax

Düsseldorf

E-Mail: sposnak@Deloitte.de

Due the pandemic, the corporates are

adjusting their strategy faster then ever,

which among others implies higher rate

of carve-outs and disposals of the

performing and non-performing

business lines

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 2Day 4: Trends and future of corporate M&A

Corporate: Carve-out structures and challenges

Identification phase

• Identifying the assets, liabilities, shareholdings, employees, rights,

M GmbH contracts subject to carve-out.

IP &

FTEs Analysis phase

PLTA • Alternatives of how carve-out can be structured from the legal and

tax perspective, including

− Timing considerations, i.e. retroactive effect, point in time for

T GmbH termination of the fiscal unities

BU − Addressing the potential exit / acquisition structure issues, e.g. all

carve-out assets and liabilities to be transferred to a NewCo

PLTA GmbH followed by a share deal vs. asset deal

Implementation phase

E GmbH • Preparation of the required documentation

• Actual execution of the transfer

Fiscal unity for corporate

income tax, trade tax and

VAT

Transaction perimeter

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 3Day 4: Trends and future of corporate M&A

Corporate: Carve-out structures and challenges

Analysis phase

• Example: Classification of the spin-off or hive down of the Business

M GmbH Unit for tax neutral transfer:

IP &

FTEs − The spin-off (“Abspaltung”) or hive-down (“Ausgliederung”) of a

business unit may be carried out tax neutrally only if the

PLTA

transferred assets, rights and agreements at least have the quality

of a “Teilbetrieb” that – from an organizational point of view –

constitutes an independent business division resp. an entity

capable of functioning by its own means. In addition, in case of a

T GmbH spin-off a “Teilbetrieb” must remain at T GmbH. All business

NewCo

assets that are operationally essential for “Teilbetrieb” must be

BU GmbH

transferred. Any assets that are not essential for the business

PLTA division have to follow the business division to the extent an

Hive-down economic relationship with the business division can be

Spin-off established. Only non-essential assets that do not have any

economic relationship with a business division can be allocated

E GmbH

freely between various business divisions.

− In terms of timing: Retroactive effect of up to 12 months is

Fiscal unity for corporate possible in 2021 (otherwise 8 months) prior to the filing of the

income tax, trade tax and

VAT spin-off or hive-down. However, retroactive effect applies for

hive-down only if “Teilbetrieb” is given, and always for a spin-off.

Transaction perimeter

− Holding periods of 5 years in case of spin-off, respectively 7 years

for hive-down arise.

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 4Day 4: Trends and future of corporate M&A

Corporate: Carve-out structures and challenges

Analysis phase

• Example: Termination of the fiscal unities:

M GmbH

IP &

− Termination of fiscal unities for income tax purposes could be

FTEs triggered by termination of the PLTA or lack of financial

integration, whatever earlier

PLTA

− Termination of VAT fiscal unity takes place if one of the

requirements of financial, economic or organizational integration

is not given anymore

T GmbH

NewCo − Financial integration: Point in time of transfer of economic

BU GmbH ownership

PLTA Example: VAT treatment of the transfers:

Hive-down

Spin-off − Transfer of the shares

E GmbH − Transfer of a going concern

− Transfer of the assets generally subject to VAT

Fiscal unity for corporate

income tax, trade tax and Example: Transaction costs and RETT

VAT

− Tax treatment of transaction costs

Transaction perimeter

− RETT being triggered several times

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 5Deloitte 2021 M&A Tax Virtual Conference Break-out session France: Trends and futures of corporate M&A Capital gain taxation, ATAD II, DAC 6, VAT 04 MARCH 2021

Day 4: Global and regional trends - France

Introduction and Contacts

Arnaud Mourier Bertrand Jeannin

Partner Partner

M&A tax, Paris VAT / M&A tax, Paris

E-Mail: amourier@taj.fr E-Mail: bjeannin@taj.fr

Eric Couderc

Director

M&A tax, Paris

E-Mail: ecouderc@taj.fr

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 2Contents Interest rate on shareholders’ loans 4 Capital gain taxation 6 Sale & lease back 9 Free revaluation of fixed assets 11 ATAD II 13 DAC6 21 VAT 29 Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 3

Interest rate on shareholders’ loans (Article 244 bis B of the FTC) Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 4

Day 4: Global and regional trends - France Interest rate on shareholders’ loans – overview The French tax authorities have been very challenging in the past few years on the interest rate on related-party debt, and notably shareholder’s loans in LBO structures. Several decisions rendered recently by French courts were favourable to the taxpayers, in relation to the documentation that could be utilized to support the interest rate utilized. Reference to interest rate on bonds for instance is now accepted. Based on our experience of tax audits and on recent guidance provided by the FTA in January 2021, it seems crucial to have: - a debt pricing analysis prepared by a third-party advisor supporting the rate utilized; - the debt pricing analysis should be quite comprehensive and notably include an analysis of the credit rating of the borrowing company and a benchmark of interest rates on the market. In case of on-lending (i.e. third-party debt is borrowed by a company outside of France and on-lent to the French borrowing entity), reference to the interest rate on the third-party debt is not sufficient. Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 5

Capital gain taxation (Article 244 bis B of the FTC) Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 6

Day 4: Global and regional trends - France Capital gain taxation realized by foreign shareholders Based on French tax law, capital gain realized upon the transfer of shares in a French entity by a foreign shareholder may be taxed in France if there shareholding in the French company entitled them to more than 25% of the profit of the French entity (at the time of the transfer or at any moment during the past 5 years). Capital gain is taxed at standard CIT (27.5% for 2021) but: - EU / EEA shareholders could benefit from the participation exemption if conditions are met, allowing a 88% capital gain exemption (i.e. c. 3.3% tax rate); - No taxation should occur in France if the tax treaty applicable between France and the foreign jurisdiction provides for a taxation of capital gain only at the level of the seller. Two recent case law have considered that no taxation could be levied in France if: - The Seller is located in the EU (as this taxation is in contradiction to EU law): French administrative Supreme Court, 14 October 2020, 421524, Sté AVM International Holding; - The Seller is located in a non-EU country (Cayman) with no tax treaty (as this taxation is in contradiction with EU freedom of capital movement): Court of Appeal of Versailles, 20 October 2020, 18VE03012. This Court decision may not be final as the FTA may take this case to the French Supreme Court. Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 7

Day 4: Global and regional trends - France Capital gain taxation realized by foreign shareholders Claims opportunities Outcome of these case law may create claims opportunities if disposal of shares have occurred as from 2019 and have been taxed in France under the provision of article 244 bis B if: - The Seller / transferor is established in Spain, Italy, Sweden, Netherlands, Austria, Hungary, Malta, Cyprus or Bulgaria (i.e. a EU country with a a tax treaty with a substantial participation clause) or in Denmark (i.e. EU country with no tax treaty with France); - The French company is not a real estate company and is subject to CIT in France; - The Seller would have been French, he would have benefitted from the participation exemption regime in France (88% capital gain exemption); - The Sellers held at least 25% of the French entities right to profit at the time of the sale or at any moment during the 5 years preceding the sale. Opportunities may also be applicable for Sellers located in non-EU jurisdictions, but a case-by-case analysis should be performed / outcomes are not certain as the Court of Versailles decision may not be final. Please note that a change in French tax law may occur in the near future to change future taxation rules. Timing: Claims must be submitted to the FTA before 31 December of the 2nd year following tax payment, i.e. : - before 31 December 2021 for capital gain tax paid in 2019; and - before 31 December 2022 for capital gain tax paid in 2020. Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 8

Sale & Lease back Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 9

Day 4: Global and regional trends - France Sale & lease back – overview The Finance Bill for 2021 also provides for a favourable tax treatment of sale & lease back transactions. In principle, the capital gain upon a sale & lease back is immediately taxable. Under the new regime, applicable until 30 June 2023, the taxation of the capital gain is spread over the term of the lease agreement up to a maximum of 15 years. Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 10

Free revaluation of assets Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 11

Day 4: Global and regional trends - France Free revalutation of assets – overview French Finance Bill for 2021 provides for a favourable tax treatment of free revaluations of assets. In principle, the net asset increase resulting from the free revaluation is treated as a taxable income and is immediately taxable. Under the new regime, applicable until 31 December 2022, the taxation of the net asset increase will be either postponed until the sale of the assets (for non amortizable assets) or spread over 5 or 15 years (for amortizable assets, depending of their nature – real estate or others). The revaluation enables a company to improve the presentation of its balance sheet and may also have positive tax impacts (especially when computing ratios assessed on its net equity). Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 12

ATAD II Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 13

Day 4: Global and regional trends - France ATAD 2 – overview French Finance Bill for 2020 has enacted into French tax law new EU “anti-hybrid” rules (so called ATAD 2 rules – applicable as from 1 January 2020). These rules aimed at preventing multinational companies from using “hybrid” arrangements to limit the taxation of their profits. Scope of ATAD 2 rules Broadly, arrangements targeted by ATAD 2 rules are mainly the following: • Situations that give rise to a deduction without inclusion of a payment (interest or any other expenses) made under a hybrid instrument, or to a hybrid entity / reverse hybrid or involving permanent establishment; • Situations that give rise to a double deduction; • Other specific situations involving an imported hybrid, payment to disregarded PE, hybrid transfer, dual resident tax-payer. ATAD 2 rules are applicable if hybrid mismatches arise between a taxpayer and its associated enterprises (which would generally require a 50% interest / 25% interest in some cases). Consequences If a hybrid arrangement is characterized, France can disallow the deduction of the payment that is not taxed or deducted in another country, or France can tax income resulting from a payment that is deducted or not taxed in the other country. In practice ATAD 2 rules are complex and not self explanatory. No French administrative guidelines available to date. Application of these rules to Private Equity structure raised questions / uncertainties. Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 14

Day 4: Global and regional trends - France

ATAD 2 – application to PE structure with French portfolio

Structure 1: Payments to a low tax jurisdiction

Fund

SHLs

• Interest deduction in France

Inclusion at Cayman Co

Cayman level? (Cayman) • Inclusion in Luxembourg but interest income is compensated by

interest expenses (back-to-back financing)

CPECs

Lux Holdco

(Lux) Management

need to analyze if a non-inclusion / double deduction occurs in

the upper structure (Cayman level) + existence of a hybrid

instrument / hybrid entity – reverse hybrid entity

CBs

Non-inclusion at Cayman Co level?

French Topco

(France)

Deduction of - 0% CIT rate (or CIT rate close to 0%) should not be assimilated to

interest in France I/c loan(s) a non-inclusion (based on OECD comments / to confirmed based

on FTA guidelines).

French Bidco

Senior Debt (France)

- Non-inclusion may occur if CPECs income are seen in Cayman as

an equity return (exempted dividend). CPECs may be

characterized as a hybrid instrument.

Target Group

(France) Conclusion:

Interest deductibility in France could be denied if no inclusion occurs

at Cayman Co level due to the insertion of a hybrid instrument (i.e.

CPECs seen as a debt instrument in Lux and as an equity instrument

in Cayman).

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 15Day 4: Global and regional trends - France

ATAD 2 – application to PE structure with French portfolio

Inclusion at fund

Structure 2: application of ATAD 2 rules?

level? Fund

SHLs

• Interest deduction in France

Lux TopCo

(Lux)

• Inclusion in Luxembourg but interest income is compensated by

SHLs interest expenses (back-to-back financing)

Lux Holdco

(Lux) Management

need to analyze if a non-inclusion / double deduction occurs in

the upper structure (fund level) + existence of a hybrid instrument

CBs / hybrid entity –reverse hybrid entity

French Topco Non inclusion at Fund level?

(France)

Deduction of

interest in France I/c loan(s)

• Funds are generally tax transparent entity: no inclusion at Fund

French Bidco level

Senior Debt (France)

Existence of a hybrid instrument/ entity/ reverse hybrid?

• Qualification as a hybrid or reverse hybrid is key as eligible funds

Target Group

(France) that qualify as a reverse hybrid entity should benefit from a

safeguard provision and not be caught by ATAD 2 rules (1).

(1): eligible funds are investment funds with a large number of investors, diversified portfolio

and subject to investor protection rules in its country of incorporation

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 16Day 4: Global and regional trends - France

ATAD 2 – application to PE structure with French portfolio

Inclusion at fund

• Based on wording of the law, a fund could be characterized as a

level? Fund

hybrid entity (as transparent in country of incorporation / opaque

SHLs

for some investors)

Lux TopCo

(Lux) • Based on French law marker comments:

SHLs - Hybrid entity is an entity considered as (i) opaque in its country

Lux Holdco of incorporation (i.e. a taxable entity) and transparent by its

Management

(Lux) foreign stakeholders;

CBs

- Reverse hybrid entity is defined as an entity considered as (i)

transparent in its country of incorporation and (ii) opaque by its

French Topco

(France)

foreign stakeholders

Deduction of

interest in France I/c loan(s)

=> French law marker comments seems to support that funds should

French Bidco qualify as a reverse hybrid entity (and thus should not fall within

Senior Debt (France)

ATAD 2 limitation) but wording of the law may contradict this

analysis.

Target Group

(France)

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 17Day 4: Global and regional trends - France

ATAD 2 – application to PE structure with French portfolio

Inclusion at fund

• Even if funds fall within the application of ATAD 2 limitation (as

level? Fund

hybrid entities or if they cannot benefit from the safeguard

SHLs

provision, application of ATAD 2 limitations to fund raises

Lux TopCo uncertainties.

(Lux)

SHLs • Notably, ATAD 2 rules should be applicable between associated

enterprises. Qualification of an associated enterprises between a

Lux Holdco

(Lux) Management fund and its investors is debatable as:

CBs • A fund should not qualify as a hybrid entity / reverse hybrid

entity if the mismatch result from minority investors (as they

French Topco

(France)

should not qualify as associated enterprise);

Deduction of

interest in France I/c loan(s)

• However, OECD comments consider that powers given by

Senior Debt

French Bidco investors to the fund management company should

(France)

characterize a joint control of investors over the funds /

portfolio, so that minority investors may be seen as associated

to the fund.

Target Group

(France)

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 18Day 4: Global and regional trends - France

ATAD 2 – application to PE structure with French portfolio

Inclusion at funds

Conclusion:

level? Fund

SHLs

Although wording of the law and French law marker commentary are

Lux TopCo not crystal clear, we believe that arguments could be put forward to

(Lux)

sustain that the payments made by a French entity to a fund

SHLs (directly or indirectly via back-to-back arrangements) should not fall

within ATAD 2 limitations (assuming no other hybridity in the

Lux Holdco

(Lux) Management structure).

CBs Some clarification from the FTA are however needed to confirm

that:

French Topco

(France)

Deduction of

I/c loan(s)

- Funds may be qualified as reversed hybrid if they are transparent

interest in France

in their country of incorporation and opaque for some investors so

Senior Debt

French Bidco that they can benefit from the exemption applicable to investment

(France)

funds;

- Confirm that minority shareholders stake should not be

Target Group

(France) aggregated (joint control situation when investors delegate their

powers to a Management company) so that the fund should not

qualify as a hybrid entity if the mismatch originates from minority

stakeholders.

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 19Day 4: Global and regional trends - France s

ATAD 2 – application to PE structure with French portfolio

Structure 3: application of ATAD 2 rules?

US Fund

SHLs

• Interest deduction in France

Lux TopCo

(Lux)

• Check-the-box of Luxcos and French Topco / Bidco for US tax

SHLs purposes

Lux Holdco

Management

(Lux) • French Bidco is opaque in France and tax transparent (disregarded)

for US investors.

CBs

A double deduction may then arise (deduction of interest in

French Topco

(France) France and in the US)

I/c loan(s)

French Bidco may qualify as a hybrid entity

French Bidco

Senior Debt (France)

Conclusion:

Target Group

Check-the-box election may entail adverse tax consequences in

(France) France as they may create a double deduction situation (with no

double inclusion if a tax consolidation is in place).

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 20DAC 6 Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 21

Day 4: Global and regional trends - France DAC 6 – overview France has enacted DAC 6 rules into its domestic law by an Ordinance dated 21 October 2019. DAC 6 rules provide for new reporting obligation of cross-border tax planning seen as aggressive. DAC 6 scope: Pursuant to DAC 6 rules, cross border arrangements must be reported only if they contain certain indications or “hallmarks” of tax avoidance, which can be summarized in two categories: - Hallmarks whose mere existence entails the obligation to report the arrangement; - Hallmarks which requires that the main benefit or one of the main benefit of the arrangement is to obtain a tax advantage (Main Benefit Test). Who should report? Reportable arrangements should be disclosed by intermediaries if they (i) are involved in designing, marketing, organizing or managing the implementation of a reportable arrangement or if they (ii) provide assistance or advice in such implementation. Please note that the definition of an intermediary is wide and not limited to external advisors. Notably Funds management entities or group holding companies may qualify as intermediaries. Please note that intermediaries benefitting from legal privilege cannot report, unless their legal privilege is waiver by their clients. What information should be included in the DAC 6 report ? Information to be reported are quite wide as they include information on the parties to the arrangements, identification of intermediaries, detailed information on the hallmark(s), value of the arrangement at stake, etc. Some information to report may be hard to assess (e.g. level of information to disclose, value of the arrangement, etc.). Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 22

Day 4: Global and regional trends - France

DAC 6 – overview

Reporting deadline:

- 30 days after the reportable arrangement is made available for implementation (e.g. for structure paper, 30 days after final version is

made available) or is ready for implementation;

- Specific deadlines:

- For arrangements implemented between 25 June 2018 and 30 June 2020: reporting to be made before 28 February 2021;

- For arrangements implemented between 1 July 2020 and 21 December 2020: reporting was to be made before 31 January 2021.

What if a reportable arrangement is not declared?

- €10k penalty per infringement (€5k in case of first infringement)

- Max of €100k per entity per year

=> Reporting should then be assessed on a case-by-case basis, taking also into account other factors such as:

- the impact of a reporting on future tax audit (notably if criminal sanctions may be due) vs penalty at stake;

- Reputation impact.

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 23Day 4: Global and regional trends - France

DAC 6 – focus on PE structure

Reporting obligation under Hallmark B.2?

Fund

SHLs

• Hallmark B.2 targets arrangements allowing a conversion of

Lux TopCo revenue into another type of revenue (less taxed).

(Lux)

SHLs • Hallmark B.2 is trigger only if one of the main benefit of the

Lux Holdco

arrangement is tax.

(Lux) Management

• MEP could then fall within Hallmark B.2 as it could be argued that

CBs they allow a conversion of income (salaries into capital gain).

French Topco

(France) • In our view, reporting should be assessed on a case-by-case basis

I/c loan(s) and will depend on the MEP features (notably if conversion arise

due to the use of legal scheme such as qualifying free share plan

Senior Debt

French Bidco or not).

(France)

• Primary reporting obligation should lie with Manager’s advisors as

the conversion risk lies with Managers.

Target Group

(France)

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 24Day 4: Global and regional trends - France

DAC 6 – focus on PE structure

Reporting obligation under Hallmark C.1 a)?

Fund

SHLs

• Hallmark C.1.a) targets arrangements that would allow a

Lux TopCo deduction of a payment made between associated enterprises if

(Lux)

the beneficiary of this payment has its tax residency in no

SHLs jurisdiction.

Lux Holdco

(Lux) Management • Hallmark C.1.a) do not require the Main Benefit Test.

CBs • Back-to-back financing arrangement between the funds and

French Topco could fall within C.1.a) as generally funds are tax

French Topco

(France) transparent entities (i.e. not tax resident in any jurisdiction).

I/c loan(s)

• However, if the fund is located in the EU (and incorporated under

Senior Debt

French Bidco EU laws), the beneficiary should not be the fund itself but its

(France)

qualifying stakeholders (i.e. share holders qualifying as associated

enterprise).

Target Group

(France) • It is unclear if the beneficiary should be Lux Holdco (as payment

of interest is primarily made by French Topco to Lux Holdco and

not directly to the Fund) or the Fund (due to the back-to-back

arrangement)

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 25Day 4: Global and regional trends - France

DAC 6 – focus on PE structure

Reporting obligation under Hallmark C.1 c)?

Fund

SHLs

• Hallmark C.1.c) targets arrangements that would allow a

Lux TopCo deduction of a payment made between associated enterprises if

(Lux)

the payment is tax exempt at beneficiary level.

SHLs

Lux Holdco

• Hallmark C.1.c) is trigger only if one of the main benefit of the

(Lux) Management arrangement is tax.

CBs • French administrative guidelines comments on the notion of tax-

exempt payment are quite wide / unclear as they consider as tax-

French Topco

(France) exempt any payment that is not taxed due to a rebate, a

I/c loan(s)

compensation or an offset of NOL or any other deductible

expenses or tax credit.

French Bidco

Senior Debt (France)

• In this context, it could be argued that interest income received by

LuxHoldco (if considered as the beneficiary) are tax-exempt as

they are offset by tax deductible expenses on the SHL (back-to-

Target Group

(France) back financing).

• Although this hallmark may be reached, it could also be argued

that the MBT may prevent reporting as SHL financing is generally

not put in place for tax reasons but for cash repatriation / legal

reasons.

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 26Day 4: Global and regional trends - France

DAC 6 – focus on PE structure

Reporting obligation under Hallmark C.1 b i)?

Fund

SHLs

• Hallmark C.1.b i) targets arrangements that would allow a

Cayman Co deduction of a payment made between associated enterprises if

(Cayman)

the payment is tax at a 0% CIT rate (or very low rate) at

SHLs beneficiary level.

Lux Holdco

(Lux) Management • Hallmark C.1.c) is trigger only if one of the main benefit of the

arrangement is tax.

CBs

• In this context, it could be argued that interest income received by

French Topco

(France) Caymanco (if considered as the beneficiary) should trigger this

I/c loan(s)

hallmark if interest income are taxed at a 0% CIT rate (or at a CIT

rate below 2%).

French Bidco

Senior Debt (France)

• Although this hallmark may be reached, it could also be argued

that the MBT may prevent reporting as SHL financing is generally

not put in place for tax reasons but for cash repatriation / legal

Target Group

(France) reasons.

• In addition, if Lux Holdco has proper substance, it could also be

argued that the beneficiary is Lux Holdco and not Caymanco.

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 27VAT Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 28

Day 4: Global and regional trends - France

French VAT current trends interesting holding companies (1/2)

Advisor costs related to the disposal of shares

• Costs inherent to the transaction

− Input VAT recovery remains challenging

• Costs in view of preparing the transaction

− Input VAT recovery should be possible further to proper structuring

− Drafting of SPA

− Redistribution of the proceeds of the disposal

Costs charged by arranging banks

• French marketplace and tax authorities position not favorable on VAT

− No application of the VAT exemption on the negotiation activities related to share deals

• Concrete consequences

− Activated holding companies => VAT costs can be avoided

− Non activated holding companies

− Since Brexit UK banks could be required to charge French VAT

− Prefer EU banks in the chain where possible

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 29Day 4: Global and regional trends - France

French VAT current trends interesting holding companies (2/2)

“Beware to the “taxe sur les salaires” (tax on wages)

• “Necessary” tax cost incurred by French holding companies

− However tax leakage inferior to potential input VAT cost

• Wage tax cost can be highly mitigated further to proper structuring

Receipt of convertible bond income = > no impact on VAT cost in France

• Tax authorities tried to challenge full input VAT recovery on acquisition costs

• Per a long court litigation interest deriving from convertible bond holding are assimilated to dividends

• Neutral impact of such income on French holding’s input VAT recovery

Recharge of advisors costs by a holding company = > VAT recovery recognized by French tax courts

• Tax authorities tried to challenge input VAT recovery on advisors costs related to the strategic organization of the group

• Per French tax courts a recharge of costs is an activity in the scope of VAT (assuming the French holding is properly activated)

• Neutral impact of such recharge on French holding’s input VAT recovery

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 30Deloitte 2021 M&A Tax Virtual Conference Break-out Session Luxembourg: Corporate M&A transactions in light of the Biden tax policy 04 MARCH 2021

Day 4: Trends and future of corporate M&A

Introduction and Contacts

Christian Bednarczyk, CPA

Partner

Luxembourg

E-Mail: cbednarczyk@deloitte.lu

M&A transaction are expected to increase

over the next 12 month in the US

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 2Contents Overview 5 Taxation of M&A Transactions 10 Overview of Potential Implications for AIF Funds 17 Regulatory Watch 22 Conclusion 24 Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 3

Overview Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 4

Day 4: Trends and future of corporate M&A Biden Tax Proposal – Implications for M&A Transactions Overview Although the economic impact of the coronavirus pandemic (and the federal response to it) dominated the fiscal policy debate during the campaign, one of the issues implicitly on the ballot was the fate of the tax code overhaul— known informally as the Tax Cuts and Jobs Act (TCJA, P.L. 115-97) — which congressional Republicans approved and President Trump signed into law in 2017. Among other things, TCJA lowered the tax burden for many businesses, whether structured as corporations or passthrough entities, as well as for individuals, trusts, and estates — although for budgetary and procedural reasons, the individual and passthrough provisions are generally scheduled to expire at the end of 2025. TCJA’s corporate and business provisions are generally permanent, although there are certain changes on this side of the code that phase in or out before 2025. Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 5

Day 4: Trends and future of corporate M&A Biden Tax Proposal – Implications for M&A Transactions Corporate and business tax proposal One of the signature provisions of the Tax Cuts and Jobs Act was the reduction in the corporate tax rate to 21 percent from its prior-law level of 35 percent. Biden proposes to increase that rate to 28 percent. Biden would encourage domestic manufacturing—and discourage offshoring of US jobs and production activity— through a combination of tax penalties and incentives. He has called for an “offshoring tax penalty” that would impose a 10 percent surtax—on top of his proposed 28 percent corporate rate—on the profits of foreign production (including call centers and services) intended for sale back into the United States. As a result, according to a campaign fact sheet, “[c]ompanies would pay a 30.8 percent tax rate on any such profits.” The plan would also deny deductions associated with moving jobs and production offshore while also implementing “strong anti-inversion regulations and penalties.” Biden also has proposed an advanceable “Made in America” credit of 10 percent that could be applied to several enumerated categories of qualifying expenses, including those related to returning production to the United States, revitalizing existing closed or closing manufacturing facilities, incrementally increasing wages paid to US manufacturing workers, and retooling facilities to advance manufacturing competitiveness and employment. Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 6

Taxation of M&A Transactions Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 7

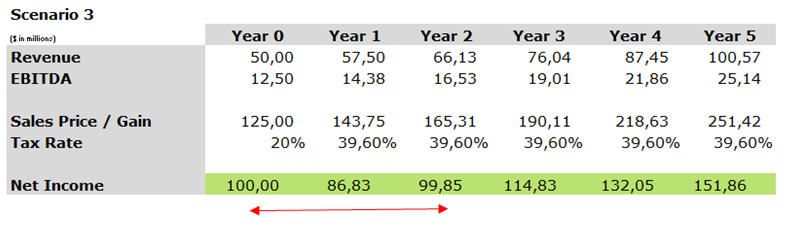

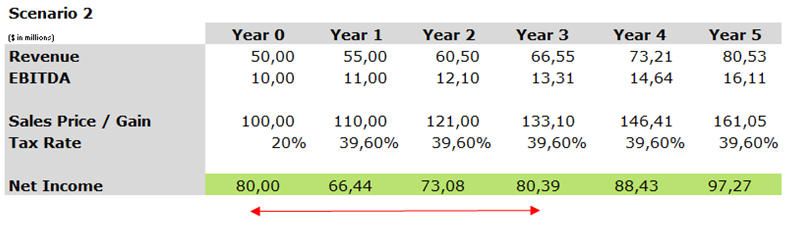

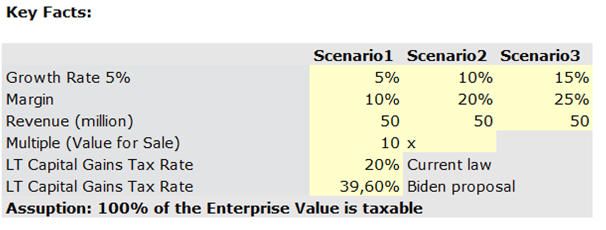

Day 4: Trends and future of corporate M&A Biden Tax Proposal – Implications for M&A Transactions Section 1(h)(11) – Planning Current Law: 20% tax rate applies to long-term capital gains and qualified dividends. Proposed Law: Tax long-term capital gains and dividends at ordinary income rates (i.e. 39.6%) for those with taxable income >$1 million. Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 8

Day 4: Trends and future of corporate M&A Biden Tax Proposal – Implications for M&A Transactions M&A Considerations - Sale Ownership is generally structured that the proceed are ultimately taxed by an the US individual (i.e. transparent for the seller) to be taxed at a “moderate” rate of 20%. Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 9

Day 4: Trends and future of corporate M&A

Biden Tax Proposal – Implications for M&A Transactions

M&A Considerations - Sale

Observation:

If the potential sale is

envisaged in the next

few years, query

whether the sale

transaction should occur

“earlier” than “ later”…

Multiple will need to

increase in order to

achieve the same after

tax return.

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 10Day 4: Trends and future of corporate M&A Biden Tax Proposal – Implications for M&A Transactions M&A Considerations - Sale "Scrutiny of Chinese takeovers of U.S. companies, which intensified under Trump, is expected to continue," Reuters reported. "In the last four years, the United States blocked many Chinese acquisitions, especially of U.S. technology firms, on national security grounds, and even ordered some Chinese firms, such as the owners of social media apps TikTok and Grindr, to divest them.“ It is expected that under Biden this will not change and an additional focus could be the healthcare industry. Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 11

Day 4: Trends and future of corporate M&A Biden Tax Proposal – Implications for M&A Transactions M&A Carried Interest (US Insiders) The Tax Proposal would impact the carried interest in the following way: Gains from the sale of property held three or fewer year is re-characterized as short-term capital gain for so called “applicable partnership interests.” Short-term capital gains are taxed at the ordinary rates (i.e. 39,6%). If to compare with the earlier mentioned proposal, even the long-term capital gains will be taxed at the ordinary rates. De facto eliminating the long-term capital gain rate for private equity insiders / owners. Private equity firms should revisit their compensation model which could impact both the private equity as well as the investors. Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 12

Day 4: Trends and future of corporate M&A

Biden Tax Proposal – Implications for M&A Transactions

M&A US Taxable Investors

The Tax Proposal would impact the return of certain US taxable investors.

Foreign asset managers with US taxable investors may face unhappy investors due to the higher tax burden

they may face in the future.

Tax long-term capital gains and dividends at ordinary income rates (i.e. 39.6%) for those with taxable

income >$1 million.

Can the income be spread over the investment horizon?

Private equity firms with a high number of US taxable investors may think about alternative return

policies – feasible?

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 13Overview of Potential Implications for AIF Funds Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 14

Day 4: Trends and future of corporate M&A

Biden Tax Proposal – Implications for M&A Transactions

Overview of Potential Implications of Different Fund Structures

Fund Structure 1 – US Investments / No US Asset Manager

Non-US

Investors

• Restore and make permanent solar ITC (LPs)

• Expand deduction for emissions-reducing

investments

• Increase incentives for energy-efficient

technologies

• Encourage development of low-carbon GP

manufacturing sector through tax credits and

subsidies for businesses to upgrade

equipment and processes, invest in expanded

or new factories, and deploy low-carbon

technologies

• Reform and extend incentives that generate Fund

energy efficiency and clean energy jobs;

promote tax incentives for technology that

captures carbon and then permanently

sequesters or utilizes that captured carbon

(including lowering cost of carbon capture Higher Tax burden – 28% tax

retrofits for existing power plants) rate compared to 21%

US Alternative US Portfolio US Portfolio

Energy Company Company

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 15Day 4: Trends and future of corporate M&A

Biden Tax Proposal – Implications for M&A Transactions

Overview of Potential Implications of Different Fund Structures

Fund Structure 2 – None - US Investments / US Investors / No US Asset Managers

Generally higher taxation

depends on the type of US

US Investors taxable investor.

(LPs)

Tax exempt investors –

generally no implications

GP

Fund

None-US

Investment

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 16Day 4: Trends and future of corporate M&A

Biden Tax Proposal – Implications for M&A Transactions

Overview of Potential Implications of Different Fund Structures

Fund Structure 3 – None - US Investments / US Investors / US Asset Managers

US Investors

US Insiders

(LPs)

Generally higher taxation depends on

the type of US taxable investor.

Generally higher taxation – elimination Tax exempt investors – generally no

of long term capital gains taxation on the GP implications

carry

Fund

None-US

Investment

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 17Day 4: Trends and future of corporate M&A

Biden Tax Proposal – Implications for M&A Transactions

Overview of Potential Implications of Different Fund Structures

Fund Structure 4 – Foreign Investments / No US Asset Manager

Non-US

Investors

(LPs)

GP

Fund Generally no implications

to the structure.

None-US

Investment

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 18Regulatory Watch Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 19

Day 4: Trends and future of corporate M&A

Biden Tax Proposal – Implications for M&A Transactions

SEC & Governance

The presidency of Joe Biden may have an impact on the SEC and the corporate governance. This could include

the following:

• Who will lead the SEC? Will the new chair be more left?

• Impact on Wall Street (enforcement and investigations)

• More regulation?

• Biden called for “an end to the era of shareholder capitalism – the idea only the responsibility a

corporation has is to its shareholders”

• ESG Reporting

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 20Conclusion Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 21

Day 4: Trends and future of corporate M&A

Biden Tax Proposal – Implications for M&A Transactions

Summary

Before the Tax Plan is passed: After the Tax Plan is passed:

• It is expected that sales transaction in the US • EBITDA multiples to be impacted (in order to

is increasing. Query whether there are any achieve the same after tax proceeds the EBITA

negotiation potential (e.g. lower sales price). multiple needs to increase – unlikely?)

• COVID implications to be analyzed to • Deal activity should not be impacted as much

determine the M&A transaction value • Leverage to be used to manage return

• Buy-Side and Sell-Side interest to increase for • Inversion transaction to be more difficult to

both strategic transactions and “cashing out” perform

• Protective measures for certain foreign buyers

to be analyzed

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 22Deloitte 2021 M&A Tax Virtual Conference Break-out Session CEE: Tax deductibility of interest and acquisition financing after ATAD 04 MARCH 2021

Day 4: Trends and future of corporate M&A

Introduction and Contacts

Adrian Hammer

Senior Manager

Zagreb, Croatia

Email: ahammer@deloittece.com

Debt push downs have become a highly

controversial tax topic.

Deloitte 2021 Deloitte 2021 M&A Tax Virtual Conference 2You can also read