Investor Day | 17 July 2018 - Amazon AWS

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Investor Day | 17 July 2018

Welcome and agenda for the day

Presentations

Welcome and Wrap up

Overview by senior

Strategic and Finish

of Retail managers in

overview Questions

small groups

1.00pm 1.30pm 2.15pm 4.30pm 5.30pm

2. Trustpower Investor Day 17 July 2018

Trustpower leadership team – depth of experience and talent 3. Trustpower Investor Day 17 July 2018

Trustpower key facts

1923 $1.8b

Tauranga based

History dates back FY19 EBITDAF

national electricity Market Key shareholders

to 1923 as the forecast to be

generator and capitalisation Infratil (51.0%) and

Tauranga Electric $205 million to

retailer of energy circa $1.8 billon TECT (26.8%)

Power Board $225 million

and telco

1,954 GWh 100,000

New Zealand generation Approximately customers

capacity (hydro) 487MW 247,000 have more Approximately 803

producing an customers than one FTE employees

average of circa product

1,954GWh per annum

4. Trustpower Investor Day 17 July 2018

Electricity industry poised for growth

The NZ economy is electrifying! Transpower’s view

“Synlait commits to never building another coal fired boiler – “ the major 100 89

new boiler to be electric”1 difference between

80 75

We are already starting to see the evidence the last 10 years

58

and the next 30 60

TWh

44

EV fleet size² EV’s will soon start to make a difference years will be 39

40

significantly more

10,000 electrification” ³ 20

Registrations

8,000

0

Vehicle

6,000

2015

2020

2030

2040

2050

4,000

2,000 Estimated

delivered electricity Industrial Transport Commercial

0

Apr-13 Apr-14 Apr-15 Apr-16 Apr-17 Apr-18 demand by sector Residential Primary

1. Synlait announcement 28 June 2018, 2. https://www.transport.govt.nz/resources/

vehicle-fleet-statistics/ monthly-electric-and-hybrid-light-vehicle-registrations/ 3. Te Mauri Hiko Energy Futures – Transpower White Paper 2018 (page 20)

5. Trustpower Investor Day 17 July 2018

Fibre rollout and data consumption

driving significant telco growth

Actual and forecast fibre connections Trustpower’s customers are showing no signs of slowing down

Fibre opportunity growing fast Average data use per customer per month

• Driven by data hungry customers

• Creates new opportunity for customer engagement 200

Data Used (GB)

1,000 150

Fibre Connections (000s)

Forecast

750

100

500

50

250

0 0

Apr-15

Apr-16

Apr-17

Apr-18

Oct-14

Jul-15

Oct-15

Jul-16

Oct-16

Jul-17

Oct-17

Jan-15

Jan-16

Jan-17

Jan-18

Dec-14

Dec-15

Dec-16

Dec-17

Dec-18

Dec-19

Dec-20

Jun-15

Jun-16

Jun-17

Jun-18

Jun-19

Jun-20

6. Trustpower Investor Day 17 July 2018

Summary of key messages

Our retail business is well positioned Our generation assets are well placed to

• Our differentiated bundled strategy is adding value with a significant growth opportunity capitalise on a renewable future

due to the fibre rollout • Geographical diversity and high levels of

• Being a value led rather than price lead competitor is a long term sustainable and availability

profitable position

We are facing a high level of regulation

• We have made significant progress in our digital strategy and are well positioned for the

both in energy and in telco

digital future

• This could be positive or negative for

We have developed a high level of capability that gives us the flexibility and agility to Trustpower. However we are fully

perform well in a changing future engaged and believe we have the

flexibility and capability to prosper

• A highly capable organisation that focuses on collective learning and fast decision making

whatever the outcome.

• A strong focus on the communities in which we operate and a commitment to be a

positive contributor We are well positioned to grow both

• Agile and flexible technology platforms that support our commitment to digital initiatives organically and through acquisition

• We are extracting significant scale benefits from our telco platform

7. Trustpower Investor Day 17 July 2018

Trustpower’s key strategic convictions

Irrespective of which political party is in government societal pressures will lead towards lower Extensive use of digital technology

carbon and increased renewable generation such as AI and machine learning will

• Transition to a lower carbon world will lead to increased demand for electricity become the norm

• Existing and new renewable generation will be well placed in both the lower carbon and • Customers will expect to be able to

increased renewable generation scenarios interact via multiple channels of

their choice

• Transitioning NZ to an increased renewable generation portfolio will lead to periods of

instability and short term high prices benefitting generators with flexible generation which have • The cost efficiencies from

high levels of availability digitisation will be a necessity to

keep customers and stay profitable

Not all customers make their decisions based solely on price over the long term

• Customers will continue to see value in the bundle and will be attracted to it without the need • Digital benefits will be available

to price discount without the need for expensive large

• The current fibre rollout provides a significant opportunity for continued growth scale computer systems making

agility and speed to market key

• Trustpower can maintain its loyal energy only customer base for an extended period without

differentiators

the need for aggressive price discounting by continuing to provide excellent service and value

enhancements

8. Trustpower Investor Day 17 July 2018

Trustpower’s strategy – to create executable

options driving shareholder returns

Bundling Energy Generation Portfolio Maximising Identifying New

and Telco Performance Electricity Value Markets

Strategic

Pillars

Shareholder

Value

Driving action based Meeting our Strong, positive Lean, agile, scalable Open culture

on data, analytics and customers’ needs relationships technology platforms with a collective

Capabilities

To deliver

Strategic

insight and processes learning focus a total

shareholder

return in the top

quartile of the

NZX while

maintaining a

strong focus on

total societal

Values

impact.

Passion Respect Integrity Innovation Delivery Empower

9. Trustpower Investor Day 17 July 2018

Retail Overview Craig Neustroski – GM Markets

Electricity segment – not for the faint hearted

Consumer market highly competitive Electricity only

• Electricity segment remains highly competitive with consolidation and

failures likely

• Trustpower has a balanced portfolio across Commercial, Industrial,

Government and Consumer

• We have opportunity in new energy and emerging technology

• Cross sell within the Consumer segment is moving our customers out of

this category

Commercial and Industrial market

• Diverse customer base, typical contract term 2-3 years

• Average tenure over 7 years, supply relationships with some of New

Comment Zealand’s most recognised corporates for over 15 years

• Circa 40 retail brands now present • Profitable and sustainable circa 1,700GWh p.a.

11. Trustpower Investor Day 17 July 2018Electricity segment – diversity & tenure

Consumer market Product innovation

Electricity customer base by region

25%

Bay of Plenty

Metro

57% 18% Regional

Comment

• Electricity only customer base biased away from the metros

• Around 60% of customers have 5+ years tenure

12. Trustpower Investor Day 17 July 2018Trustpower the leading multi-utility business

Our achievements

Over 100,000 customers have more than one product

• Growth from a base of around 20,000 multi-utility customers in

mid 2013

Comment • We continue to see strong telecommunications growth

• We created a new category and others have followed • We are now realising material scale and cost to serve benefits

• There is plenty of room for growth in this category

• E.g. caching delivering savings of ~$3m p.a.

13. Trustpower Investor Day 17 July 2018We are building value

Total customers by region Current connections

2015 2018

273,000 38,000 89,000

electricity gas telco

Comment

• We are creating a diverse and resilient customer base

• We are creating a high value customer base

Over 100,000 customers have

• Significant opportunity remains for us more than one product

14. Trustpower Investor Day 17 July 2018Differentiated from competition

Bundle customers by region Bundle customers by tenure

Targeted acquisition Focused cross sell and retention in FY18

• Growth coming largely from the metros • Over 3,000 existing energy customers added Telco

• Targeted outbound campaigns are seeing 80% of new • 1,200 electricity customers added gas

customers taking two or more products

• 5,600 customers upgraded from DSL to Fibre

15. Trustpower Investor Day 17 July 2018Value based offers outperform simple price discounting

Electricity only vs multi-product churn

20%

Annualised churn

15%

Our acquisition incentive costs are similar to other in 10%

market discounts or cash incentives, however value based

offers outperform: 5%

Jun-16 Nov-16 Apr-17 Sep-17 Feb-18

• Better sales conversion and lower sales leakage

• Higher energy consumption and larger data plans driving Electricity Only Dual Fuel

higher margin per customer Triple Play Electricity and Telco

• Lower churn and lower credit risk Linear (Electricity Only) Linear (Dual Fuel)

• We have a solid suite of offers aimed at our target segments Linear (Triple Play) Linear (Electricity and Telco)

16. Trustpower Investor Day 17 July 2018Customer Operations Fiona Smith – GM Customer Operations

Our digital journey so far…

• Virtual Agent:100 topics • Virtual Agent: 300+ topics • Virtual Agent: 400 topics

• Virtual Agent:

• Faults • Webchat Launch • App launch: Account, Outages, Order & • App: Track & Trace all products

30 topics

IVR • Email Virtual Agent Pay features • Chatbot: Readings, PPD,

• Webchat Pilot

• Text • App Pilot • Chatbot: Balance & Payment Arrangement

• Credit Card

Balance • Robotics Pilot: 9 • Fibre Install Support • Fibre Automation Sprints x 3

Self Service

processes • Robotics: 15 processes • Robotics 20 processes

2015 2016 2017 2018 2018

(delivered) (year end)

• Call centre staff • Fibre roll out drives • Robotics & Bot capability secured • Predictive AI & machine learning skill gap

capability moderate skill and capability lift • Drive to support staff to embrace the shifting closed

• High volume - low • Effort & handle technology • Value differentiated service model analysis

complexity queries metrics • Wait times replace service levels complete

• Call quality & • People power • Customer feedback prioritises improvement • Predictive telephony bot intervention

service level protects the customer • Data and insight enables proactive analysis

metrics • External customer intervention • Journey mapping – simplify & automate

• Customer feedback survey & NPS with • Complex problem solving, agility & resiliency • Strengthen insight: Where does human

or engagement low feedback loop capability growth intervention drive value?

18. Trustpower Investor Day 17 July 2018With measurable outcomes …

FY-16 FY-17 FY-18 FY-19 Budget 39% increase in total services

with 54% growth in Telco

On Queue FTE 163 160 147 140

Number of services (000s) 270 330 359 375 62% ratio of services to CEA2

improvement (mitigating 86 FTE)

Services per FTE 1,656 2,061 2,442 2,677

Total contacts (000s) 891 1,018 1,440 1,651 85% growth in total contacts

Total staffed contacts (000s) 873 906 937 875 Staffed Volume controlled

Staffed contacts % 98% 89% 65% 53% through digitisation , & efficiency

with volume of complexity rising

Staffed contacts per FTE 5,355 5,665 6,371 6,249

Labour cost per service

Labour cost¹ per service $36.41 $35.23 $34.96 $34.07

decreasing

1. Labour cost : Total salary cost of the Service , Provisioning , Billing , Cash & Collections Teams

2. CEA = Customer Experience Agent or call centre staff member

19. Trustpower Investor Day 17 July 2018And digital success…

• 47% of all customer contacts are now 53% Staffed Interactions

serviced without human intervention

2018

46%

(YTD)

• Goal to reduce staffed contacts by

61% Staffed Interactions

another 12% across the next 18 months

& reduce on queue FTE by 10% 2017 54%

• Delivering a hybrid staffed/non-staffed 91% Staffed Interactions

model with a focus on value add human

interactions 2016 87%

Phone Email Webchat

Virtual Agent Trustpower App Credit Card Self Serve

Balance Self Serve IVR Outages Chat Bot

20. Trustpower Investor Day 17 July 2018While getting the balance right...

• Non Staffed interactions receive customer satisfaction Satisfaction ratings by channel

ratings on par with agent channels

90%

• Automating with a full understanding of the

75%

consequences

60%

• Analysis supports our conviction that staffed channels

45%

remain important

30%

• Staffed channels focus on the moments that matter,

the complex and the emotional, where propensity to 15%

churn spikes

0%

Webchat Agent Phone Agent Chatbot App

21. Trustpower Investor Day 17 July 2018And we know where to tackle next…

Bundled customers drive higher contacts up front (Cost to Acquire)

but in line with electricity-only customers longer term.

Staffed contact % driven by tenure & product mix Bundled Product Electricity Only

12.0%

10.0%

8.0%

6.0%

4.0%

2.0%

0.0%

0 2 4 6 8 10 12 14 16 18 20 22 24 26 28 30 32 34 36 38 40 42 44 46 48 50 52 54 56 58 60

Number of months post sale

22. Trustpower Investor Day 17 July 2018By understanding the data…

Why When Who

Contact Distribution New Fibre:

35% Week One

30%

25%

20%

15%

10%

5%

0%

Day 0Day 1Day 2Day 3Day 4Day 5Day 6Day 7

23. Trustpower Investor Day 17 July 2018And building capability… • Driving the human-robot relationship takes careful planning & collaboration • Starting early & experimentation builds new capability & supports agility • Understanding that sometimes human contact is the answer, not the problem & building their capability to adapt 24. Trustpower Investor Day 17 July 2018

To deliver on our convictions

We become We become & maximise

more effective more efficient human connection

Automation

Robotics Customer centred

Prescriptive AI

Simplification Relationship focussed

Digitisation

Ease of effort Proactive personalisation

Insight led

Faster Cheaper Valued

25. Trustpower Investor Day 17 July 2018…and aspirations

• Reduce staffed contacts from 53% to 40% enabling Forecast on-queue staffing & volumes

efficient service growth & focussing human

interactions on the moments that matter 158

KCE Migration

• Reduce on-queue FTE by increasing their productivity

132

by at least 10% (services/FTE)

• More than double the amount of automation in telco

provisioning

• Support 13,000 ex KCE customers (17,000 ICP) with

no back office FTE increase & on queue lift of 4 FTE

• Deliver back office initiatives delivering savings of

$600,000 + Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

2018 2018 2018 2018 2019 2019 2019 2019 2020 2020

Total Services Supplied Total Contacts

Staffed Contacts On Queue Staff

26. Trustpower Investor Day 17 July 2018Energy and Regulatory Risk Peter Calderwood – GM Strategy and Growth

Portfolio strategy

Key focus areas

Strategic regulatory Issues Energy risk management New opportunities

• Joined up thinking within Government • Making sure energy risk management • Potential M&A Opportunities

maximises EBITDA within acceptable

• Climate change and move to low • Divestment where other owners

volatility

emissions economy are better fit

• Continuing to improve generation

• Evolution of gas and telco regulatory • Continuous scanning of new

dispatch to maximise revenue

governance arrangements technology and products for

• Co-optimisation of: existing customers

• Water allocation and quality

– Energy

• Electricity Price Review – Avoided Cost of Transmission

• Tax Working Group – Reserves

• Ongoing TPM work – Demand Side Management

28. Trustpower Investor Day 17 July 2018Climate change and low emissions economy

Key focus areas

Trustpower’s Position Key Areas for Involvement Opportunities

• Trustpower supports the now bi- • Productivity Commission • New storage and

partisan view that New Zealand generation technologies –

• Climate Change Commission (Zero Carbon Bill)

should significantly reduce its both grid connected and

green house gas emissions. • Joined up thinking across Government behind the meter

organisations

• Decarbonisation of other sectors • Enhancement of existing

will lead to increase in electricity – Recognise the positive impact of existing assets to support new

gross demand. hydro generation on NZ’s Emissions footprint intermittent generation

– Linkage to Water Reform (incl. via tax

• The transition to a new normal • Participation in new

reform)

will be turbulent and needs markets

careful and deliberate policy and • Market structures for transition to new normal

regulatory governance to

minimise disruption, and protect

the interests of investors

29. Trustpower Investor Day 17 July 2018Electricity price review

Key focus areas

Trustpower’s Position Key Areas for Involvement Opportunities

• The current market functions well. • Contribute to the review to • Leverage from

assist the Government to Trustpower as a

• The review is a valuable opportunity to fine-tune

deliver more effective knowledgeable and

industry governance

outcomes particularly for long term retailer

• Trustpower continues to support competition as the vulnerable customers.

most effective way of delivering the best outcome to

consumers.

• Ideal opportunity for a review of governance

arrangements for a new future energy mix.

30. Trustpower Investor Day 17 July 2018Review of DGPPs (ACOT payments) Assessment of ongoing ACOT Current Trustpower estimate of future ACOT revenue (Avoided Cost of Transmission) payments ACOT revenue reduction over time (estimate), incl. Rotokawa and • Electricity Authority’s final decision announced 6 KCE Contribution December 2016 • Lower SI review complete • Lower NI proposed beneficiaries published and presently subject to consultation • Outcomes are in line with previous guidance. 31. Trustpower Investor Day 17 July 2018

Balanced exposure to wholesale risk

Overview of a typical year

Trustpower Generation Tilt FPVV PPAs FPVV PPAs (excl Tilt) FPFV Hedges incl ASX Spot passed through to C&I

Generation/Purchase

FPVV = Fixed Price

Overall long Customer

Variable Volume Direct pass

generation to reduce contracts

through with

FPFV = Fixed Price exposure to weather matched to

no market

Fixed Volume related hydro/wind hedge

exposure

variability contracts

Retail

Net Length MM Fixed Price C&I Fixed Price C&I on spot

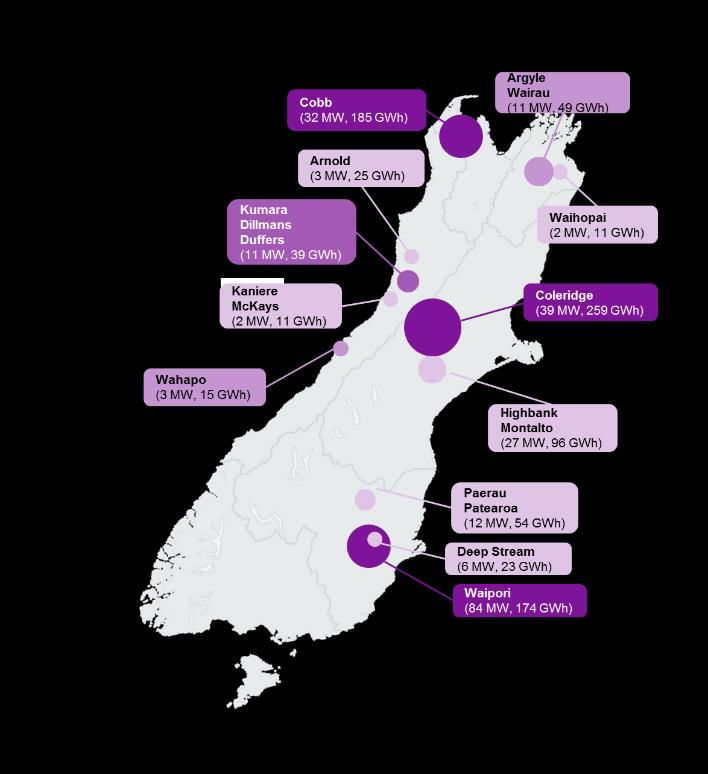

32. Trustpower Investor Day 17 July 2018Generation Overview Stephen Fraser – GM Generation

Generation portfolio – provides

efficient, flexible risk management

43 20%

hydro power shareholding in Rangitata Diversion

stations across Race Management Limited (New

Zealand’s largest irrigation scheme)

26

schemes 75% - 80%

of Trustpower’s EBITDAF

is provided by the NZ generation

75% business

shareholding in

King Country Energy

Flexible and low

marginal cost

496MW portfolio benefits from market firming

total NZ installed and able to optimise growth, hold or

generation capacity divest

34. Trustpower Investor Day 17 July 2018We will continue to drive portfolio profitability & manage risk

in the near term through a number of different focus areas

Key focus areas

Maximizing portfolio Our licence to operate Asset Identifying new

profitability and risk management efficiency generation opportunities

• Continuous improvement • Focus on health, safety • Targeted asset • Sharper focus on

and focus on revenue and the environment, management practices development: ‘brownfield’

growth with an eye on dam/civil safety – that focus on the enhancement and

cost efficiencies delivering our ‘licence to efficiency, reliability and ‘greenfield’ growth by

operate’ agenda availability of our highest keeping an eye out for the

• Improved

value assets right opportunities

project/programme

delivery and supply chain • Improving asset

optimisation management maturity –

more data and analytics,

predictive and

preventative focus

35. Trustpower Investor Day 17 July 2018Generation portfolio – outperforms market

• Strong output from NI schemes in FY18; our geographically diverse spread of generation stabilises our output against regional

hydrology.

• This enabled us to outperform market expectations of price for the majority of the financial year while our competitors

experienced difficult portfolio positions in the South Island.

– Our average monthly Generation Weighted Average Price (GWAP) was 3.4% higher than the national average price.

9%

$46.28

8%

% difference between GWAP and

$132.29

200 7% $127.37

national average price

6% $121.52

5%

GWh

$147.03

100 4% $67.89

3% $66.92

$56.74 $99.69

2% $85.30 $61.38

0 1%

Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar 0%

Northland Bay of Plenty Taranaki -1% $55.71

Marlborough/Tasman West Coast Canterbury

Otago KCE LT average (incl. KCE) Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar

36. Trustpower Investor Day 17 July 2018Matahina G1 refurbishment + enhancement – case study

• Refurbished second-hand 56 MVA Transformer Matahina – based on actual generation

replaced end-of-life single-phase transformers – total

installed cost of $1.5m versus $3-5m for a new 45

transformer 35

GWh

• Investigations initiated for a Low-flow Turbine to 25

increase total station GWh

15

5

Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar

1 in 5 1 in 20 Median: Monthly 1 in 20 1 in 5 Actual Generation

Matahina Station (In top 5 highest value in portfolio):

• Outage timed to minimise lost generation

Transformer lifted onto Installed in final • Concurrent major rotor refurbishment works

trailer for short journey location in

to switchyard switchyard • ‘Healthy’ outage concept with good H&S results

37. Trustpower Investor Day 17 July 2018Coleridge G2 & G3 generator replacement

• Condition assessment and Asset Management Plan identified Coleridge Generators G2 & G3 (12 MW each) as two of our six top-

earning machines, but being in very poor condition

• International tendering process to select preferred supplier and installer

• Optimal timing for generator replacement balanced the risk of failure (lost revenue) with the benefit of delay (project cost).

New G3 G3 stator

rotor being lifted

awaiting into station

installation

38. Trustpower Investor Day 17 July 2018People, Culture and Communication Mel Dyer – GM People & Culture

Building organisational capability

Key Capabilities

Driving action Delivering Building, Keeping our Fostering an

based on data, products, maintaining and workforce and open

analytics and propositions, leveraging contractors organisational

insight and service that strong, positive safe and well culture with a

meet our relationships collective

customers’ with our learning

needs. stakeholders. focus.

40. Trustpower Investor Day 17 July 2018People capability to execute on future opportunities Key Capabilities Future organisational capability • Targeted development to strengthen resiliency, leadership, and collaboration for better business outcomes – Over 50% of Leadership program spots taken by women in the last 4 years • Focus on cross functional teams to match our customers’ experience and to deal with increasing complexity • Fast business improvement skills development – Focusing on driving efficiency and a better outcome for our customers • Internal Facilitators trained to help groups work in different ways and break down barriers https://www.trustpower.co.nz/Getting-To-Know-Us/Working-For-Trustpower 41. Trustpower Investor Day 17 July 2018

Focus on diversity to build capability and drive success

Diversity for adaptability and flexibility Demographics

• Recent review of our remuneration has ensured we are competitive Gender balance

- but with no desire to be the highest payer in our markets

• Focus is on providing an environment where people can flourish

• analysis of the pay gap between males and females for the same

position shows no significant difference between genders

Male v female remuneration, 2018 Males

Female - 2018 Male - 2018

Females

Salary

Organisational Level

42. Trustpower Investor Day 17 July 2018Safety and wellbeing

Keeping our workforce safe and well

Injury frequency rates per 200,000 hours worked - 12 month rolling average Key focus areas

20 • Completed production of new Safety

Lost Time Management System

18

Lost Time and Medical Treatment

16

• New incident reporting system

Injury frequency rate

Lost Time, Medical Treatment and First Aid

14

implemented with better reporting for

12

root cause diagnosis

10

8 • Public Safety accreditation maintained

6

4 • Wellbeing initiatives in major projects

2 • New in car monitoring system

0

implemented

Jul-16

Jul-12

Apr-18

Apr-13

Jul-13

Oct-13

Apr-14

Jul-14

Apr-15

Jul-15

Apr-16

Apr-17

Jul-17

Oct-12

Oct-14

Oct-15

Oct-16

Oct-17

Jan-13

Jan-14

Jan-15

Jan-16

Jan-17

Jan-18

• Participation in industry StayLive forum

43. Trustpower Investor Day 17 July 2018Maintaining a strong community presence which

recognises the value of being a good corporate citizen

Sponsorship of the TECT

13 regional and 1 national Rescue Helicopter

Community Awards events

held annually to celebrate

the work of volunteers and

community groups Generation team

tree planting

44. Trustpower Investor Day 17 July 2018A range of efforts are helping build and maintain positive

relationships with our key stakeholder groups

This year Trustpower received an

Enhancement funds that Fisheries management – including environmental management

provide for local environmental, eel management programmes, trout accreditation from BRAID in

cultural and community projects release in some catchments, and recognition of the work undertaken

in the catchments Trustpower ongoing fish passage investigations on the Rakaia River to restore

operates and initiatives braided river bird habitat

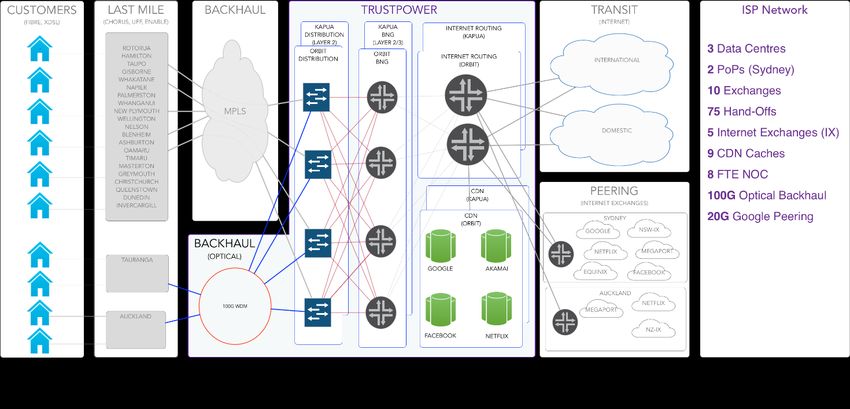

45. Trustpower Investor Day 17 July 2018Digital Platforms Simon Clarke – GM Business Solutions & Technology

Our responsive tech foundations will underpin our evolution

to a future ready digital business

Past Current

Multi-product &

CX/UX focus v4.02

Key focus areas

Stable & Resilient

Infrastructure

Speed & Scale

Modern

Collaborative

Workplace

Foundational Keep it Simple, Scalable Rock Solid IT Cloud & People Digital & Build & Leverage

Principles & Fit for Purpose & ISP Platforms Agility Data Lead People & IP

47. Trustpower Investor Day 17 July 2018We are transitioning to an agile delivery model focused on

value and user & customer experience (UX/CX)

Digitising operations Digitising UX/CX

Based on insight & focused on Based on market insight

automating processes and lowering and user and customer

costs across the business response

Examples Examples

Nine cross-functional Chorus B2B integration Customer App

teams working in sprints • enabling fibre install support • >12,000 downloads

with quarterly reviews • ~$160K cost for $500K pa • >5000 contacts mitigated

Work prioritised saving Webchat

by business owners based Baseband IP Migration • ~10,000 interactions/month

on value & impact with long

• ~27,000 telco customers AI Chatbot

term strategic goals in mind

•We have a scalable & modern ISP platform & capability

Optical backhaul gives us

more control & visibility in

key markets

Increasing caching &

Trans Tasman peering

capability provides better

customer experience &

reduces international

bandwidth and input costs

In-house ISP Network

Operations Team means

less reliance on upstream

vendors and closer

connection to customer

49. Trustpower Investor Day 17 July 2018TB No. Services

000’s

0

4

8

12

16

100

0

25

50

75

Oct-14

Dec-14 Oct-14

Feb-15 Dec-14

Apr-15 Feb-15 Total services

Total bandwidth

Jun-15 Apr-15

Aug-15 Jun-15

Oct-15 Aug-15

Dec-15 Oct-15

Feb-16 Dec-15

Feb-16

Apr-16

Apr-16

Jun-16

Jun-16

Aug-16

Aug-16

Oct-16

50. Trustpower Investor Day 17 July 2018

Oct-16

Dec-16

Dec-16

Feb-17 Feb-17

Apr-17 Apr-17

Jun-17 Jun-17

Aug-17 Aug-17

Oct-17 Oct-17

Dec-17 Dec-17

Feb-18 Feb-18

Apr-18 Apr-18

Jun-18 Jun-18

Our ISP network has supported

Mbps

significant growth & is NZ leading

3.0

3.5

4.0

Mar-16

Apr-16

May-16

Jun-16

Jul-16

Aug-16

Sep-16

Oct-16

Nov-16

CallPlus

Dec-16

MyRepublic

Jan-17

Vodafone NZ

Feb-17

Mar-17

Apr-17

May-17

https://ispspeedindex.netflix.com/country/ new-zealand

Jun-17

Spark

Jul-17

Aug-17

Trustpower

Sep-17

Oct-17

Nov-17

Dec-17

Jan-18

Feb-18

Bigpipe

Mar-18

2degrees

Apr-18

May-18We are last to the dance on smart meters - but best dressed

• Cost based business case (only now just making

sense)

• Partnership with Australasian metering technology

& service company L+G/intelliHub

• “Proof of Performance” over the last 12 months to

test technology & business processes - complete

• Internal development of fit for purpose & scalable

meter data management (MDM) platform -

complete

• 3 year deployment programme - commenced

51. Trustpower Investor Day 17 July 2018Finance Overview and Wrap up

Kevin Palmer– Chief Financial OfficerFY19 guidance remains unchanged

After normalising for the sale of our Australian (GSP) assets (~$27m) and abnormal hydrology during FY18 (~$20m), we retain

our current EBITDAF guidance of $205-$225m:

FY18 to FY19 Bridge – Difference (range) from FY18

12

10

8 8

7

6

5

4 4 3

$M

2

0

-2 -4 -3

-3 -3 -3

-4 -4 -5 -5

-6 -6

-8

ACOT Retail Retail Generation Generation Corporate Other

gross profit OPEX OPEX Other Revenue OPEX

53. Trustpower Investor Day 17 July 2018Debt position

Key comments

• Debt levels forecast to be ~2x Debt/EBITDA and are below industry peers. A capital distribution programme is being considered by

the Board to return Trustpower to 2.5x-2.8x debt/EBITDAF over time.

• The average tenor of debt is shorter than ideal but is not a real concern at these debt levels – while not seen as urgent Trustpower is

considering a debt capital market issuance.

Sources of debt ($m) Debt maturity ($m)

400

Bank Unutilised Bank

163 172 300

Sub Bonds

Senior Bonds

200 Senior Bonds

Sub Bonds Bank

114 100

Unutilised Bank

211

0

0-1 1-3 3-5 5-7 7+

54. Trustpower Investor Day 17 July 2018Summary of key messages

Our retail business is well positioned Our generation assets are well placed to

• Our differentiated bundled strategy is adding value with a significant growth opportunity capitalise on a renewable future

due to the fibre rollout • Geographical diversity and high levels of

• Being a value led rather than price lead competitor is a long term sustainable and availability

profitable position

We are facing a high level of regulation

• We have made significant progress in our digital strategy and are well positioned for the

both in energy and in telco

digital future

• It is yet to be seen if this will be a

We have developed a high level of capability that gives us the flexibility and agility to positive or negative for Trustpower.

perform well in a changing future However we are fully engaged and

believe we have the flexibility and

• A highly capable organisation that focuses on collective learning and fast decision making

capability to prosper whatever the

• A strong focus on the communities in which we operate and a commitment to be a outcome.

positive contributor

• Agile and flexible technology platforms that support our commitment to digital initiatives We are well positioned to grow both

organically and through acquisition

• We are extracting significant scale benefits from our telco platform

55. Trustpower Investor Day 17 July 2018Thank You

Non-GAAP Measures

• EBITDAF is a non GAAP financial measure but is commonly used within the electricity 2017 industry2018as a measure of performance as it shows the level of earnings

before impact

ProftofAfter

gearing levels and to

Tax Attributable non-cash charges

Shareholders such

of the as depreciation and92,545

Company amortisation.128,127

Market analysts use the measure as an input into company

valuation and

Fairvaluation metrics

value losses usedontofinancial

/ (gains) assess relative value and performance of companies

instruments (3,825) across the sector. The EBITDAF shown in the financial statements

2,675

excludes the Australian

Gain business

on sale of which is

the subsidiary a discontinued

after income tax operation. - (183)

• Reconciliation betweenofstatutory

Impairment assets measures of profit and EBITDAF, as well as EBITDAF per the financial

3,479 5,099statements and total EBITDAF, is given below:

Demerger related expenditure 23,959 -

Changes in income tax expense in relation to adjustments (687) (749)

Underlying Earnings After Tax 115,471

2017 134,969

2018

Operating Profit 141,883 191,068

Fair value losses / (gains) on financial instruments (3,825) 2,675

Impairment of assets 3,479 5,099

Depreciation and amortisation 44,742 44,242

Discount on acquisition - -

EBITDAF per financial statements 186,279 243,084

EBITDAF of Australian business 31,552 26,684

Reclassification of foreign currency translation reserve - (3,022)

Total EBITDAF 217,831 266,746

57. Trustpower Investor Day 17 July 2018Disclaimer While all reasonable care has been taken in the preparation of this presentation, Trustpower Limited and its related entities, directors, officers and employees (collectively "Trustpower") do not accept, and expressly disclaim, any liability whatsoever (including for negligence) for any loss howsoever arising from any use of this presentation or its contents. No representation or warranty, expressed or implied, is made as to the accuracy, completeness or thoroughness of the content of the information. All information included in this presentation is provided as at the date of this presentation. Except as required by law or NZX listing rules, Trustpower is not obliged to update this presentation after its release, even if things change materially. The reader should consult with its own legal, tax, investment or accounting advisers as to the accuracy and application of the information contained herein and should conduct its own due diligence and other enquiries in relation to such information. The information in this presentation has not been independently verified by Trustpower. Some of the information set out in the presentation relates to future matters, that are subject to a number of risks and uncertainties (many of which are beyond the control of Trustpower), which may cause the actual results, performance or achievements of Trustpower or the Trustpower Group to be materially different from the future results set out in the presentation. The inclusion of forward-looking information should not be regarded as a representation or warranty by Trustpower or any other person that those forward-looking statements will be achieved or that the assumptions underlying any forward-looking statements will in fact be correct. This presentation may contain a number of non-GAAP financial measures. Because they are not defined by GAAP or IFRS, they should not be considered in isolation from, or construed as an alternative to, other financial measures determined in accordance with GAAP. Although Trustpower believes they provide useful information in measuring the financial performance of the Trustpower Group, readers are cautioned not to place undue reliance on any non-GAAP financial measures. This presentation is for general information purposes only and does not constitute investment advice or an offer, inducement, invitation or recommendation in respect of Trustpower securities. The reader should note that, in providing this presentation, Trustpower has not considered the objectives, financial position or needs of the reader. The reader should obtain and rely on its own professional advice from its legal, tax, investment, accounting and other professional advisers in respect of the reader’s objectives, financial position or needs 58. Trustpower Investor Day 17 July 2018

You can also read