FRANCE FOOD RETAIL COUNTRY REPORT - Kantar Retail IQ

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

FRANCE FOOD RETAIL COUNTRY REPORT

KantarRetail.com

KantarRetailIQ.eu

Table of Contents

FRANCE’S FOOD RETAIL LANDSCAPE: 2014–2018 OUTLOOK ................................................................2

KEY THEMES ......................................................................................................................................2

CONSOLIDATION............................................................................................................................................ 2

PRICE COMPETITIVENESS ................................................................................................................................ 2

MULTI-CHANNEL DEVELOPMENT...................................................................................................................... 3

CHANNEL BLURRING ...................................................................................................................................... 3

THE ECONOMY & ITS IMPACT ON SHOPPERS ......................................................................................4

THE ECONOMY.............................................................................................................................................. 4

HAVES & HAVE NOTS..................................................................................................................................... 4

Implications for Retailers in a Have & Have-Not Society ...................................................................... 5

CHANNEL TRENDS ..............................................................................................................................6

HYPERMARKETS ............................................................................................................................................ 6

SUPERMARKETS............................................................................................................................................. 7

CONVENIENCE & FOOD PROXIMITY .................................................................................................................. 8

DISCOUNTERS ............................................................................................................................................... 9

Discounter Reinvention in France........................................................................................................ 10

Lidl .................................................................................................................................................................................... 10

Aldi Nord .......................................................................................................................................................................... 11

Dia/ED .............................................................................................................................................................................. 11

The Future of French Discounters ....................................................................................................... 11

CASH & CARRY............................................................................................................................................ 11

ONLINE GROCERY (INCL. DRIVE)..................................................................................................................... 12

KEY RETAILERS ................................................................................................................................. 13

CARREFOUR ................................................................................................................................................ 13

LECLERC ..................................................................................................................................................... 15

INTERMARCHÉ............................................................................................................................................. 16

AUCHAN .................................................................................................................................................... 16

SYSTÈME U................................................................................................................................................. 17

CASINO ...................................................................................................................................................... 18

OUTLOOK/CONCLUSIONS ................................................................................................................. 19

1

KantarRetail.com

KantarRetailIQ.eu

France’s Food Retail Landscape: 2014–2018 Outlook

France’s food retail market is one of the strongest in the world—supporting best practice development

among a wide range of retailers and allowing for the most successful retailers to expand and lead retail

in other markets around the globe.

France’s leading retailers are influenced by domestic consumers but often times inspired by global

shopping trends making food retail in France an interesting mélange of global and local.

Key Themes

Consolidation

France’s retail landscape is characterized by high concentration in all channels. The channels

spearheading additional market concentration are convenience and drives, while hypermarkets,

supermarkets, and discounters are going through an ongoing reinvention phase in their attempts to

regain relevancy in front of a more convenient French shopper.

The top 5 grocery retailers account for approximately 70% of the market* and are gradually expected to

grow to up to 75% by 2018 (Figure 1). The key levers employed for this feat consist of gradually taking

over smaller retailers (usually cooperatives) and attracting more of the already small traditional retail

base.

Figure 1. Top 10 Grocery Retailers in France

Source: KRiQ.eu

Sales (EUR million)* Grocery Market Share** CAGR

Retailer 2008 2013 2018 2008 2013 2018 08-13 13-18

1 Carrefour*** 37,882 34,879 37,676 22.8% 19.7% 18.5% -1.6% 1.6%

2 Leclerc 23,499 30,975 38,474 14.1% 17.5% 18.9% 5.7% 4.4%

3 Intermarché 25,180 23,898 29,892 15.2% 13.5% 14.7% -1.0% 4.6%

4 Auchan 21,012 22,168 24,954 12.6% 12.5% 12.2% 1.1% 2.4%

5 Système U 13,224 18,223 22,684 8.0% 10.3% 11.1% 6.6% 4.5%

6 Casino 19,169 17,914 19,641 11.5% 10.1% 9.6% -1.3% 1.9%

7 Schwarz G. 6,323 7,534 8,384 3.8% 4.3% 4.1% 3.6% 2.2%

8 Louis Delhaize 7,103 6,706 7,164 4.3% 3.8% 3.5% -1.1% 1.3%

9 Metro Group 3,947 4,112 4,842 2.4% 2.3% 2.4% 0.8% 3.3%

10 Aldi Nord 2,861 3,240 3,598 1.7% 1.8% 1.8% 2.5% 2.1%

Other 5,921 7,080 6,465 3.6% 4.0% 3.2% 3.6% -1.8%

TOTAL 166,121 176,730 203,773 100.0% 100.0% 100.0% 1.2% 2.9%

* Sales exclude sales generated by Retailers through non-food formats (home, consumer electronics, etc.).

** Grocery Market Share = Share of Kantar Retail Formal Grocery Retail Sales.

*** Carrefour Sales and Market Share do not reflect the recent Dia acquisition as the network’s channel outlook under

Carrefour is not yet confirmed.

Price Competitiveness

During 2013, price ranking experienced significant changes in all channels. The hypermarket price

leader, Leclerc, continued to be referenced and challenged by its main competitors (Casino, Carrefour)

2

KantarRetail.com

KantarRetailIQ.eu

through price comparison campaigns aimed at undermining its position. Casino even managed to catch

up on Leclerc in early 2014, but at the cost of overall sales falling. In early 2014, Auchan renewed its

commitment to improve its hypermarket price perception after incurring disappointing results in 2013.

In the discount channel, the leading retailers have both improved the quality and price of their ranges

(Lidl) contributing to the phenomenon of channel blurring, as well as further decreasing their prices

while adjusting their product mix in an attempt to regain fleeing shoppers.

Multi-channel Development

What started as a race for space in both physical stores as well as online has increasingly turned into a

key and complex strategic direction for most of the grocery retailers in France (Figure 2). The market is

the global leader in developing the drive format, which was perfected during 2013 as retailers further

adjusted their assortment, decreased order fulfillment times, and further diversified the model by

introducing it to smaller formats.

Multi-channel strategies are accompanied by the subsequent reshaping of organizational structures,

which become increasingly flatter and place more emphasis on adding new staff (Intermarché,

Carrefour, Auchan).

Figure 2. Grocery Channel Trends in France

Source: KRiQ.eu

Sales (EUR million) Grocery Market Share CAGR

Channel 2008 2013 2018 2008 2013 2018 08-13 13-18

1 Hypermarket 82,323 78,860 87,505 49.6% 44.6% 42.9% -0.9% 2.1%

2 Supermarket 54,332 61,203 68,263 32.7% 34.6% 33.5% 2.4% 2.2%

3 Discounter 16,324 17,156 17,501 9.8% 9.7% 8.6% 1.0% 0.4%

4 Convenience 7,659 9,408 12,143 4.6% 5.3% 6.0% 4.2% 5.2%

5 Non Store Retail 445 5,247 13,199 0.3% 3.0% 6.5% 63.8% 20.3%

6 Cash and Carry 5,037 4,857 5,162 3.0% 2.7% 2.5% -0.7% 1.2%

Grand Total* 166,121 176,730 203,773 100.0% 100.0% 100.0% 1.2% 2.9%

* Channel Sales and Market Share do not reflect the recent Dia acquisition as the network’s channel outlook under Carrefour is

not yet confirmed.

Channel Blurring

As a result of increased competition, we are witnessing increased channel blurring in France, as retailers

mix strategies across channels: discounters increase the share of their high-quality private label ranges

(Lidl – Deluxe), hypermarkets realign their low price private label propositions (Carrefour – Petit Prix),

while all channels increase their focus on fresh and ready-to-eat ranges. The assortment adjustments

also include an increased share of regionally sourced products and brands aimed at catering to the

shopper’s increased demand for local taste and sustainable sourcing (Carrefour – Quality and Origin;

Casino – The best of here).

3KantarRetail.com

KantarRetailIQ.eu

The Economy & Its Impact on Shoppers

The Economy

France’s economic woes have made life difficult for its biggest retailers. The three economic drivers of

consumer growth—job growth, labor productivity, and competitive advantage (measured in export

demand)—have all underperformed when compared to both the European and global averages over the

past 15 years.

France’s policymakers all see this and understand it; yet, political deadlock within France and the EU

threatens more stagnation and potentially a return to recession. Keep in mind that France has a 57%

public spending to GDP ratio—the highest in the EU—and that its labor policy is one of the most

complicated in the EU.

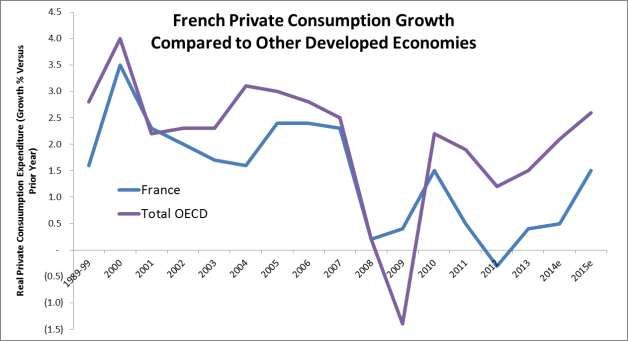

Despite this, the country is growing and its consumers are growing more diverse. Kantar Retail’s outlook

for retail in France is for moderate growth with an acceleration of positive conditions after 2016 (Figure

3). France is a very large, multi-cultural, multi-industry country that can and should see economic

improvement in the near future.

Figure 3. France's Private Consumption Growth Has Stagnated 2010–2015

Source: OECD, INSEE

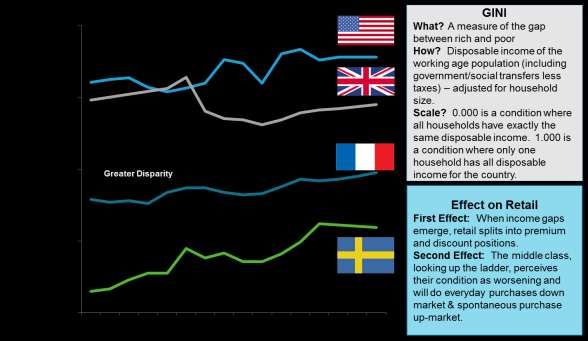

Haves & Have Nots

Economic stagnation and higher joblessness have created a wider divide between Haves and Have Nots,

not unlike other developed economies around the world (Figure 4). The key difference in France is the

level of geographic concentration as compared to other economies. In France, the Have Nots are

generally concentrated in very large public housing conglomerations in the suburbs of major cities.

4KantarRetail.com

KantarRetailIQ.eu

Increasingly, the aging population in France’s rural areas could also be classified as shopping with a

“Have-Not” attitude, as they rely largely on public pension payments that are fixed and limited, creating

a “watch my total food budget” shopping mentality.

Figure 4. France's Growing Divide Between Haves and Have Nots

Source: OECD

Implications for Retailers in a Have & Have-Not Society

Stagnating economic growth produces well-documented behavior among consumers best described as

“save now, spend later.” Purchase patterns become more frequent but on very small, essential

baskets—often times on highly discounted items. Likewise, big celebration periods such as religious

feasts/festivals, birthdays, and other lifetime events become “big spending occasions.” In short, retail

becomes more seasonal in nature, consumers move from one purchasing extreme to another, and

retailers must develop fewer mainstream positions and more focused/differentiated solutions. Retail

formats move to extremes—deep discount on one side and high premium on another.

In summary, five main trends emerge:

Price Messaging. Retailers become very good at price messaging both in marketing and in-store

(Figure 5). Retailers that promote an unclear price/value message generally suffer.

Format Differentiation. Retailers must localize stores. Decentralization of decision making is

essential, and store managers must play a stronger role in listing items and finding the right

prices for products.

5KantarRetail.com

KantarRetailIQ.eu

Focus on Efficiency. Retailers must become lean in their operations—reducing inventory levels,

rationalizing categories, and keeping staff levels at lower levels than normal.

Promotional Excellence. Retailers, especially those that depend on Have Nots, must develop

strong communication platforms.

Private Label Sophistication. Retailers will develop a new generation of private label focused on

higher quality and differentiated product as compared to their closest competitors. It is notable

in France that brands have responded positively and now have clawed back share from retailer

brands, yet investment in stronger private brand lines continue. (Note: According to Kantar

Worldpanel (KWP), private label share in France was approximately 38% in 2013, down from

39% in 2012—still among the highest in the world and growing sharply over the 10-year period.)

Figure 5. Typical In-Store Communication on "Lowest Prices"

Source: Kantar Retail store visit, April 2014

Channel Trends

Hypermarkets

Although hypermarkets are by far and away the largest grocery channel in France, they have been under

structural and economic pressure over the last five years. Issues facing the channel have included:

Weak demand for non-food items due to weak consumer sentiment;

Competition in non-food categories from online retailers and non-food specialist chains;

Competition and cannibalisation arising from the rapid growth of online and drive grocery

services;

6KantarRetail.com

KantarRetailIQ.eu

The expansion of, and shopper enthusiasm for, proximity retailing; and

Socioeconomic trends, such as growth in the number of smaller households, which have

impacted the number of hypermarket trips.

Carrefour used to be the clear leader in the hypermarket channel, although limited physical expansion

from Carrefour and new space and market share growth from Leclerc have seen the two retailers

converge, and the race for channel leadership is now extremely close (Figure 6). Auchan has grown

consistently over the last few years and is now a strong number three in the hypermarket channel.

Smaller players such as Intermarché, Casino, Louis Delhaize, and Système U also have a credible

presence in the hypermarket channel, although hypermarket expansion has not been a huge priority for

some of these operators. Système U is a slight exception, as the retailer is looking to acquire more

partners and expand its hypermarket network.

Figure 6. Top 10 Hypermarket Operators in France

Source: KRiQ.eu

Sales (EUR million) ChannelShare* CAGR

Retailer 2008 2013 2018 2008 2013 2018 08-13 13-18

1 Leclerc 20,640 25,580 30,962 25.1% 32.4% 35.4% 4.4% 3.9%

2 Carrefour 22,277 18,820 18,782 27.1% 23.9% 21.5% -3.3% 0.0%

3 Auchan 16,193 16,887 18,166 19.7% 21.4% 20.8% 0.8% 1.5%

4 L. Delhaize 5,649 4,899 4,501 6.9% 6.2% 5.1% -2.8% -1.7%

5 Casino 6,185 4,843 4,724 7.5% 6.1% 5.4% -4.8% -0.5%

6 Intermarché 8,216 4,223 6,254 10.0% 5.4% 7.1% -12.5% 8.2%

7 Système U 2,256 3,419 4,085 2.7% 4.3% 4.7% 8.7% 3.6%

8 C. Normandie 145 153 - 0.2% 0.2% 0.0% 1.1% -

9 Migros 80 36 32 0.1% 0.0% 0.0% -14.9% -2.0%

10 Coop Alsace 458 - - 0.6% 0.0% 0.0% - -

Other 223 - - 0.3% 0.0% 0.0% -

TOTAL 82,323 78,860 87,505 100.0% 100.0% 100.0% -0.9% 2.1%

*Channel Share = Share of Kantar Retail Formal Channel Grocery Retail Sales

Faced with the previously mentioned challenges, many retailers are seeking to enhance their

hypermarket networks through improving ranges and merchandising in categories such as fresh, health

& beauty, baby, books & music, and consumer electronics. With the long-term structural shifts

underway in non-food categories, players in the channel are unlikely to open more of the giant stores of

yesteryear; instead, the focus will shift toward compact hypermarkets, expansion in convenience, and

ongoing growth of multi-channel retailing.

Supermarkets

Despite losing market share in recent years, supermarkets remain the second-largest channel in the

French grocery market. Factors that have impacted the channel include:

7KantarRetail.com

KantarRetailIQ.eu

The success of retailers like Intermarché and Système U in recruiting and retaining independent

retailers within their supermarket networks;

The growing importance of supermarkets within the drive networks being developed by major

players in the sector; and

An increasing emphasis on fresh, food-to-go, and foodservice as supermarkets—particularly in

urban areas—seeking to tap into evolving shopper missions.

The major player in the channel is Intermarché, which has long dominated the supermarket scene

through its network of independent members (Figure 7). Carrefour has seen its performance in the

channel slightly held back through a protracted period of integration and store conversions (following

the acquisition of the Champion network) although progress is set to be stronger as the Carrefour

Market and C Market concepts gather pace. Système U is set to continue its credible track record in the

supermarket space—it has successfully expanded store numbers and has unveiled some interesting new

concepts in urban store formats recently.

Figure 7. Top 10 Supermarket Operators in France

Source: KRiQ.eu

Sales (EUR million) Channel Share CAGR

Retailer 2008 2013 2018 2008 2013 2018 08-13 13-18

1 Intermarché 14,284 16,177 18,016 26.3% 26.4% 26.4% 2.5% 2.2%

2 Système U 10,351 12,658 14,470 19.1% 20.7% 21.2% 4.1% 2.7%

3 Carrefour* 9,432 11,669 12,617 17.4% 19.1% 18.5% 4.3% 1.6%

4 Casino 8,756 8,457 8,789 16.1% 13.8% 12.9% -0.7% 0.8%

5 Auchan 4,652 4,304 4,830 8.6% 7.0% 7.1% -1.5% 2.3%

6 Leclerc 2,855 3,925 5,041 5.3% 6.4% 7.4% 6.6% 5.1%

7 L. Delhaize 1,375 1,337 1,402 2.5% 2.2% 2.1% -0.6% 1.0%

8 Picard 1,040 1,325 1,646 1.9% 2.2% 2.4% 5.0% 4.4%

9 Biocoop 391 573 772 0.7% 0.9% 1.1% 8.0% 6.2%

10 Colruyt 199 266 298 0.4% 0.4% 0.4% 6.0% 2.2%

Other 998 510 382 1.8% 0.8% 0.6% -12.6% -5.6%

TOTAL* 54,332 61,203 68,263 100.0% 100.0% 100.0% 2.4% 2.2%

* Although it is likely that Carrefour’s acquisition of Dia will impact the supermarket channel, it is not yet reflected in our data

as the network’s outlook is not yet confirmed.

Convenience & Food Proximity

Convenience retailing in France is gaining momentum, and there is an increased focus from all retailers

to develop the format in high-density urban areas (Figure 8). The convenience channel’s evolution has

materialized as a result of several key enablers:

Growing through Franchises. In a race for space, the market witnessed additional concentration

with small chains and traditional trade being absorbed in various franchise schemes (Carrefour

integrated Coop Alsace, Casino integrated Le Mutant). All major retailers made franchising a key

strategic initiative in France. Similarly, retailers that have yet to develop a convenience

proposition have rolled out new franchise concepts (Auchan – A 2 Pas).

8KantarRetail.com

KantarRetailIQ.eu

Increasing Assortment Relevancy. While the format’s original expansion was fueled by a race

for space, the recent rise of convenience has been a result of changing shopper habits. During

this period, convenience stores have become increasingly focused on addressing the needs of

the local time-constrained shopper. French retailers have made continuous efforts to improve

their fresh and food-to-go assortments in an attempt to cater to more shopper missions.

Redefining the Urban Supply Chain. As the format continues to penetrate high-density urban

areas, challenges have arisen in the supply chain system. The limited in-store storage space and

high-frequency shopping times (lunch) mean retailers have to optimize their operations. This

includes creating dedicated fresh warehouses and intensifying their logistics partnerships to

help speed up deliveries.

Figure 8. Top 10 Convenience Operators in France

Source: KRiQ.eu

Sales (EUR million) Channel Share CAGR

Retailer 2008 2013 2018 2008 2013 2018 08-13 13-18

1 Carrefour 2,830 3,333 4,555 36.9% 35.4% 37.5% 3.3% 6.4%

2 Système U 602 1,722 2,030 7.9% 18.3% 16.7% 23.4% 3.3%

3 Casino 1,671 1,704 1,943 21.8% 18.1% 16.0% 0.4% 2.7%

4 Intermarché 1,538 1,614 2,445 20.1% 17.2% 20.1% 1.0% 8.7%

5 TotalFina Elf 509 476 522 6.6% 5.1% 4.3% -1.3% 1.9%

6 Schiever 316 322 339 4.1% 3.4% 2.8% 0.4% 1.0%

7 Colruyt 48 98 148 0.6% 1.0% 1.2% 15.4% 8.6%

8 C. Normandie 75 60 55 1.0% 0.6% 0.5% -4.3% -1.8%

9 ExxonMobil 70 44 37 0.9% 0.5% 0.3% -8.8% -3.3%

10 Auchan - 30 61 0.0% 0.3% 0.5% - 15.2%

Other - 5 8 0.0% 0.1% 0.1% - 9.4%

TOTAL 7,659 9,408 12,143 100.0% 100.0% 100.0% 4.2% 5.2%

Discounters

While discounters continue to build on their momentum with strong sales growth across Europe,

discounters have struggled in France (Figure 9). According to KWP, the market share of discounters has

steadily declined to 12.6% over the past year. This decline is a result of its two competitive advantages

being relentlessly attacked—price and convenience.

Lowest Item Price Message. Discounters leverage price as their key competitor advantage

through extensive private label and an OPP positioning (Opening Price Point merchandising).

This proposition has continuously been attacked by out-of-channel competition in most

European markets. However, discounters are now facing unprecedented price competition from

hypermarkets and supermarkets in France. Auchan, alone, plans to invest EUR200 million in

pricing by 2016. This is contributing to an already intense price war in France, with discounters

reacting by lowering prices. Intermarché-operated Netto has responded most strongly, with a

new pricing strategy, reducing prices on more than 1,000 SKUs. This has been accompanied by

increased promotional activity declaring, “Over 1,000 products at the lowest price in the hard

9KantarRetail.com

KantarRetailIQ.eu

discount.” Lastly, the discounter will also refund the difference if a product is cheaper in another

discounter store within five kilometers.

Opening Price Point Convenience. Convenience is inherent in the overall discounter channel

concept. Discounters are often conveniently located, but more importantly, they are convenient

to shop, with a limited/edited assortment being the overriding factor in creating an easy,

convenient trip for the shopper. This convenience has been attacked by the soaring popularity

of the drive format, with shoppers and retailers alike embracing the format. The drive

proposition primarily focuses on a quick and convenient shopping trip. As big-box retailers

continue to develop the popular drive format as well as invest heavily in price, discounters are

being forced to reinvent themselves.

Figure 9. Top 5 Discount Operators in France

Source: KRiQ.eu

Sales (EUR million) Channel Share CAGR

Retailer 2008 2013 2018 2008 2013 2018 08-13 13-18

1 Schwarz Group 6,323 7,534 8,384 38.7% 43.9% 47.9% 3.6% 2.2%

2 Aldi Nord 2,861 3,240 3,598 17.5% 18.9% 20.5% 2.5% 2.1%

3 Casino 2,556 2,613 2,981 15.6% 15.2% 17.0% - 2.7%

4 Dia* - 2,177 1,262 0.0% 12.7% 7.2% - -10.3%

5 Intermarché 1,142 1,162 1,143 7.0% 6.8% 6.5% 0.4% -0.3%

Other 3,455 444 143 21.1% 2.6% 0.8% -33.7% -20.3%

TOTAL 16,337 17,171 17,511 100.0% 100.0% 100.0% 1.0% 0.4%

* Carrefour’s acquisition of Dia is not reflected as the network’s channel outlook under Carrefour is not yet confirmed.

Discounter Reinvention in France

While discounter market share has declined on the whole, German discounters Lidl and Aldi Nord have

managed to maintain their own share. This has been a result of investment in adapting their

proposition.

Lidl

Lidl has considerably softened its hard discounter image in France and is looking to position itself as a

middle-market proximity retailer, with Managing Director Friedrich Fuchs declaring, “Our concept is to

leave hard discount without becoming a traditional supermarket.” This transition involves three main

shifts:

Brands. Not only is Lidl adding more national brands to the assortment, it is actively marketing

them in-store with new and bolder POS messaging. The number of products on offer as a whole

will also be extended, including both private labels and brands.

Store layout. Lidl continues to redesign store layouts and experiment with the new arrangement

of categories, such as breakfast items instead of beverages located at the store entrance.

Fresh. Lidl will continue to put a renewed focus on its fresh offer, adding new categories such as

fresh fish, improving its fruit & vegetable offer, and rolling out in-store bakeries.

10KantarRetail.com

KantarRetailIQ.eu

Aldi Nord

The most noticeable shift for Aldi Nord is advertising listed brands in its promotional leaflets and online.

In recent leaflets, the discounter features logos of “preferred brands.” This is a significant move away

from its strict private label proposition and helps grow shopper acceptance, especially among the

younger generations.

Store modernization has also helped Aldi Nord reinforce a convenient weekly shopping trip. It has

pressed ahead with the modernisation of all its stores in France. The retailer’s focus is on rearranging its

product categories, improving lighting, and enhancing the overall shopper experience. While these

refurbishments have seen double-digit growth in many stores in its home market of Germany, stores in

France are only reporting slight increases.

Dia/ED

While Lidl and Aldi Nord have had a certain degree of success sustaining market share, Dia has

continued to lose share, culminating in reports of the discounter divesting its operations in France.

While Dia has the best price image in four of its markets (Spain, Portugal, Argentina, and Brazil), it has

struggled in France primarily due to the ongoing price war. However, unlike Lidl and Aldi Nord, which

have added more brands and grown assortments to include fresh, Dia has failed to adapt.

Dia’s recent trial of the popular click & collect service in Paris is not and cannot be part of any long-term

recovery strategy for the discounter. Ultimately, Dia’s priorities have shifted to its emerging market

operations and Iberia. Indeed its CAPEX outlay highlights this shift: In 2011, CAPEX in France amounted

to EUR139 million. In 2014, that number will be as low as EUR20 million. A turnaround in French

fortunes is unlikely with little investment and with high returns coming from the business in Argentina

and Brazil; the divestment of its 865 stores in France is a real possibility.

The Future of French Discounters

The future of discounters in France is dependent on how well they adapt. Lidl will continue to

experiment with its overall proposition and has the financial backing and acumen to adapt in the

market. Aldi Nord’s heavy investment in refurbishing its stores, highlight its commitment to battling

stagnating sales. Netto’s investment in price may only be a short-term solution and investment in top

management and its overall proposition to drive and grow the sales and profitability of the business will

be just as important. Without any significant investment, Dia cannot succeed in the market.

Cash & Carry

The French cash & carry (C&C) market continues to be dominated by Metro Group with nearly 70%

market share through its Metro C&C banner (Figure 10). Carrefour and its Promocash banner have 20%

of the French C&C market and have aligned themselves to Metro’s strategy. The only key difference

between the two is that Promocash is a franchised operation and is no longer directly owned by

Carrefour.

The French retail market has seen the C&C market also embrace the drive phenomenon. Customers of

both Metro and Promocash have adopted similar shopping habits, and over 10% of Metro sales are

11KantarRetail.com

KantarRetailIQ.eu

made through drive-only stores. Online orders and delivery have also become prevalent across nearly all

of Metro’s and Promocash’s stores, which is not the case in practically any European C&C market.

Metro’s large non-business customer base has also adopted its online approach, which is the most

advanced in its online portfolio. Flash sales, where electronic goods like TVs are offered at a large

discount for a limited period and with limited stock, have also become prevalent across Metro France.

Figure 10. Top Cash and Carry Operators in France

Source: KRiQ.eu

Sales (EUR million) Channel Share CAGR

Retailer 2008 2013 2018 2008 2013 2018 08-13 13-18

1 Metro Group 3,947 3,708 3,814 78.4% 76.3% 73.9% -1.2% 0.6%

2 Carrefour 520 556 533 10.3% 11.4% 10.3% 1.3% -0.8%

3 Rewe Group 509 535 562 10.1% 11.0% 10.9% 1.0% 1.0%

4 Colruyt 61 58 69 1.2% 1.2% 1.3% -0.9% 3.4%

5 Costco - - 183 0.0% 0.0% 3.6% - -

TOTAL 5,037 4,857 5,162 100.0% 100.0% 100.0% -0.7% 1.2%

Ultimately, Metro and Promocash have built on their excellent infrastructure by offering a more

personalised shopping experience to their customers through providing them the opportunity to speak

directly to depot managers to align their ranges to meet their requirements. Additional services like

printing bespoke takeaway packaging and menus are also becoming popular. The C&C market in France

is the most advanced in Europe, if not the world.

It will continue to become one to watch as the world of C&Cs evolve, and it has the potential to grow if

the successful hybrid C&C model like Supeco and its peers in Brazil, Spain, and Morocco help to take up

some of the excess space in France’s hypermarket portfolio.

Online Grocery (incl. Drive)

Even though Auchan launched the Auchan Drive format in 2000, more than 2,500 drive locations (a total

of 2,900 locations to date) have been built in France during the last three to four years. In 2013, the

format recorded sales of EUR4.28 billion and is forecast to continue to grow by an CAGR of20% until

2018. According to KWP, 92% of online grocery sales in France are made through drives, and the

concept reaches 25% of French households (approximately 3 million consumers).

By 2015, KWP expects 6-8% of France’s total grocery market sales to be made through the drive format.

Auchan started with its Chronodrive stand-alone drive format, which like all standalones, have a more

limited range of 10,000 SKUs in order to gain sales from competitors’ large format hypermarkets

without the land and investment required. The economics of the situation have, however, changed in

recent years, with same store sales of a hypermarket and a drive increasing by 1.3%, versus -1.7%

without a drive bringing in extra footfall.

12KantarRetail.com

KantarRetailIQ.eu

Leclerc has stamped its authority on the format with the highest average sales per store, and we

anticipate it will continue to be ahead of the rest of the French online grocery market for the next few

years due to its ability to utilize new ideas like bespoke drive-only packaging (Figure 11). Drives are

thoroughly embedded within the loyalty card landscape, as shoppers continue to shop stores and drives

depending on their needs, thus making their proposition acceptable to the public.

Ultimately, cost has been at the forefront of the drive phenomenon, which has become the largest in

Europe. Consumers have been educated by retailers to collect their own shopping for a nominal fee of

EUR3 rather than paying nearly double for a home delivery proposition. However, the race to build the

most drives has been a way for grocery retailers to gain the most market share with minimal

investment.

Figure 11. Top Online Grocery Operators in France

Source: KRiQ.eu

Sales (EUR million)* Channel Share CAGR

Retailer 2008 2013 2018 2008 2013 2018 08-13 13-18

1 Leclerc 4 1,470 2,471 1.0% 28.0% 18.7% 221.7% 10.9%

2 Auchan 163 939 1,889 36.6% 17.9% 14.3% 42.0% 15.0%

3 Intermarché - 721 2,033 0.0% 13.8% 15.4% - 23.0%

4 Carrefour 108 500 1,188 24.4% 9.5% 9.0% 35.7% 18.9%

5 Louis Delhaize 80 466 1,254 18.0% 8.9% 9.5% 42.2% 21.9%

6 Système U 15 425 2,099 3.3% 8.1% 15.9% 95.8% 37.7%

7 Metro Group - 404 1,028 0.0% 7.7% 7.8% - 20.5%

8 Casino - 297 1,204 0.0% 5.7% 9.1% - 32.4%

Other 75 26 33 16.8% 0.5% 0.3% -19.4% 5.4%

TOTAL 445 5,247 13,199 100.0% 100.0% 100.0% 63.8% 20.3%

* Sales comprise all online grocery formats: drive, home delivery.

We anticipate that the drive format will continue to be popular with French consumers. Some retailers

like Intermarché that have been unable to join the drive bandwagon have focused on click & collect

instead. Intermarché alone now has over 1,000 click & collect locations, with Auchan opening click &

collect points in Metro stations. As with other markets, home delivery may become more common as

retailers make them more economical as well as offering an even more convenient proposition to

consumers. However, retailers will have to redesign their websites and phone applications to be more

customer friendly and more suited to helping brands build more complex promotional and education

activities to stay ahead.

Key Retailers

Carrefour

Carrefour is the largest grocery retailer in France with sales of EUR35 billion from over 4,500 locations.

Its main format remains hypermarkets, which account for 54.0% of sales (Figure 12). However, as

13KantarRetail.com

KantarRetailIQ.eu

hypermarket sales decline, Carrefour is putting further emphasis on its two growth drivers: convenience

(9.6% of total sales) and online (1.4% of total sales).

Under the guidance of CEO George Plassat, the retailer has refocused its efforts on reviving sales in its

home market as its market share continues to be attacked by Leclerc. To do this, Carrefour has

identified four key initiatives:

Implementing successful aspects of it’s up-market banner, Carrefour Planet, into its standard

hypermarkets;

Focusing on building an extensive store network of “attached” drive locations;

Enhancing its price perception by improving clarity, consistency, and trust among shoppers; and

Developing its franchise network.

After developing an unsuccessful up-market banner called Carrefour Planet in 2010, Carrefour has

begun implementing successful aspects of the format into its standard hypermarkets, namely a new

layout to improve navigation and high-quality fixtures and fittings to drive shopper engagement.

Carrefour has invested in an extensive store network of the popular drive format, focusing on an

“attached” drive model. Recently, the retailer has shifted its drive strategy toward the more profitable,

but more expensive, stand-alone drive model. As shoppers continue to embrace the format in France,

Carrefour’s drive format will continue to be the key growth driver of sales.

Figure 12. Carrefour’s Channel Trends in France

Source: KRiQ.eu

Sales (EUR million) Share* CAGR

Channel 2008 2013 2018 2008 2013 2018 08-13 13-18

1 Hypermarket 22,277 18,820 18,782 58.8% 54.0% 49.9% -3.3% 0.0%

2 Supermarket 9,432 11,669 12,617 24.9% 33.5% 33.5% 4.3% 1.6%

3 Convenience 2,830 3,333 4,555 7.5% 9.6% 12.1% 3.3% 6.4%

4 Cash and Carry 520 556 533 1.4% 1.6% 1.4% 1.3% -0.8%

5 Online Grocery 108 500 1,188 0.3% 1.4% 3.2% 35.7% 18.9%

6 Discount 2,714 - - 7.2% 0.0% 0.0%

Grand Total** 37,882 34,879 37,676 100.0% 100.0% 100.0% -1.6% 1.6%

* Share = Share of Kantar Retail Retailer Grocery Sales

** Carrefour Sales and Market Share do not include the recently acquired Dia acquisition as the network’s channel outlook

under Carrefour is not yet confirmed.

As price wars grip France, Carrefour is striving to improve its price perception by improving clarity,

consistency, and trust among local shoppers. This is being done through maintaining an everyday low

price (EDLP) proposition, rolling out new initiatives such price guarantees, and offering local

comparative pricing to stores in specific catchment areas.

Finally, Carrefour is also developing its franchise network to attract local shop owners under the

umbrella of its small-format banners—Express, City, Contact, Proxi, 8 a Huit, and Shopi—targeting 300

14KantarRetail.com

KantarRetailIQ.eu

new stores annually. The channel’s growth was fueled during 2013 by Carrefour’s takeover of 120 Coop

Alsace stores in Northern France. This emphasis on franchises allows a more hands-on management of

the business and means its store base can better cater to the needs of local shoppers.

Leclerc

Leclerc is the second-largest grocery retailer in France with grocery sales of EUR31 billion in 2013 (Figure

13). In total, it operates approximately 700 affiliated stores, of which 520 are hypermarkets and 175 are

supermarkets. Additionally, the retailer has developed an extensive drive network in recent years,

operating 450 units at the end of 2013, with 100 more to be opened over the next three years.

Figure 13. Leclerc’s Channel Trends in France

Source: KRiQ.eu

Sales (EUR million) Share CAGR

2008 2013 2018 2008 2013 2018 08-13 13-18

1 Hypermarket 20,640 25,580 30,962 87.8% 82.6% 80.5% 4.4% 3.9%

2 Supermarket 2,855 3,925 5,041 12.1% 12.7% 13.1% 6.6% 5.1%

3 Online Grocery 4 1,470 2,471 0.0% 4.7% 6.4% 221.7% 10.9%

Grand Total 23,499 30,975 38,474 100.0% 100.0% 100.0% 5.7% 4.4%

Leclerc has been the big winner in France over the last five years. Its success has been a result of its low

price proposition (in-store and online) and a high percentage of quality private label products. By

continuing to be aggressive on price and making significant investments in drive expansion, Leclerc has

gained considerable ground on market leader Carrefour.

Leclerc’s price leadership continues to be attacked and is often a site of comparison for other retailers.

Therefore, the retailer has significantly boosted its marketing on price, putting more pressure on its

already thin operating margins.

Similar to Carrefour, Leclerc has identified the drive format as a key growth driver of the business.

However, Leclerc has looked to grow the more expensive stand-alone drive locations. Among other

drive initiatives, Leclerc is employing what is known as a “star” system, where a hub location delivers

grocery orders to remote locations, thereby extending its reach.

The retailer’s national strategies are implemented at local level by the store owners; this translates into

a highly customized offer catering to the needs of local shoppers, ultimately leading to a high level of

loyalty. Leclerc’s momentum in France will be sustained by steady store refurbishments, the

development of new format launches (urban hypermarkets), and by an increased emphasis on

improving the non-food ranges (books, drug, and opticians) to maximize the appeal of its store

locations.

15KantarRetail.com

KantarRetailIQ.eu

Intermarché

Intermarché is the third-largest grocery retailer in France with sales of EUR24 billion in 2013 and 14.2%

market share, an increase of 0.3 % y-o-y (Figure 14). The retailer operates a network of 1,800 stores in

France, which includes hypermarkets, supermarkets, convenience stores, drives, and discounters.

The retailer has laid down ambitious expansion plans to grow the business in France. These plans

include growing its convenience format, Intermarché Express, by quadrupling the number of stores by

2018, thereby operating 200 stores in total. The retailer also announced plans to expand its latest

compact hypermarkets concept, Mag3.E, to 200 stores (currently 83). These stores have a smaller selling

area of 3,500 square meters and look to offer a more compelling shopper experience that is closer to

the shopper in terms of location and offer. This format is expected to drive like-for-like sales growth and

increase hypermarket share in total sales.

Figure 14. Intermarché’s Channel Trends in France

Source: KRiQ.eu

Sales (EUR million) Share CAGR

Channel 2008 2013 2018 2008 2013 2018 08-13 13-18

1 Supermarket 14,284 16,177 18,016 56.7% 67.7% 60.3% 2.5% 2.2%

2 Hypermarket 8,216 4,223 6,254 32.6% 17.7% 20.9% -12.5% 8.2%

3 Convenience 1,538 1,614 2,445 6.1% 6.8% 8.2% 1.0% 8.7%

4 Discount 1,142 1,162 1,143 4.5% 4.9% 3.8% 0.4% -0.3%

5 Online Grocery - 721 2,033 0.0% 3.0% 6.8% 23.0%

Grand Total 25,180 23,898 29,892 100.0% 100.0% 100.0% -1.0% 4.6%

The retailer is also investing heavily in the refurbishment of its supermarkets, with a focus on rolling out

an extended range of services for customers, including self-scanning, ticket machines, electronic labels,

and attached drives.

Auchan

Auchan achieved sales of EUR22 billion in 2013 and operates 550 stores in total (Figure 15). The

retailer’s multi-channel strategy consists of 140 hypermarkets, with the remainder split between

supermarkets (Simply Market, Atac) and a relatively new convenience format (A 2 Pas, aka, 2 steps

away). Like its competitors, Auchan continues to develop an extensive network of drive locations (200;

Chronodrive – standalone, AuchanDrive – attached), which generated approximately EUR1 billion in net

sales alone during 2013.

16KantarRetail.com

KantarRetailIQ.eu

Figure 15. Auchan’s Channel Trends in France

Source: KRiQ.eu

Sales (EUR million) Share CAGR

Channel 2008 2013 2018 2008 2013 2018 08-13 13-18

1 Hypermarket 16,193 16,887 18,166 77.1% 76.2% 72.8% 0.8% 1.5%

2 Supermarket 4,652 4,304 4,830 22.1% 19.4% 19.4% -1.5% 2.3%

3 Online Grocery 163 939 1,889 0.8% 4.2% 7.6% 42.0% 15.0%

4 Convenience - 30 61 0.0% 0.1% 0.2% 15.2%

5 Discount 3 8 8 0.0% 0.0% 0.0% 19.0% 0.9%

Grand Total 21,012 22,168 24,954 100.0% 100.0% 100.0% 1.1% 2.4%

Coming out of a positive 2012, when sales in France grew 2.2%, and despite the progress of its drives,

Auchan’s 2013 sales dipped 1.1% in 2013, mostly due to the disappointing performance of its

hypermarkets. The results have attracted radical measures at the beginning of 2014, with its top and

middle management structure being reshuffled completely and the retailer engaging in additional price

campaigns on thousands of products to compete with the increased market price pressure. Auchan will

invest EUR200 million in improving price perception between 2014 and 2016.

Auchan’s s strategy has also historically hinged on developing large retail parks outside urban clusters,

where it deploys retail businesses to create and build shopper traffic. The hypermarkets that

accompanied these retail parks have traditionally been large (more than 9,000 square meters of selling

area) and accommodated a wide variety of goods in a low-cost setting.

The retailer has maintained its traditional and relatively unchanged strategy throughout the years but

has also managed to stay at the forefront of retail innovation—one of the most eloquent examples

being the creation of the drive format back in 2000. Only in recent years, along with the gradual decline

of hypermarkets, has Auchan opened up smaller proximity-focused formats, as a means of fueling

growth.

Système U

Système U reported 2013 sales up 3.5% y-o-y to EUR18.2 billion (Figure 16). After breaching the 10%

market share at the end of 2012, it now aims to reach 12% in 2018 by maintaining the steady market

share gain it has displayed since 2003.

While the 2012 sales were boosted by the affiliation of Coop Atlantique, in 2013 Système U continued to

grow its footprint by attracting additional partners and by joining forces with O’marche frais to enter

Paris.

The retailer is focusing on drive development (mainly standalone, linked to a star distribution model)

and expansion of the click & collect service to the entire network.

17KantarRetail.com

KantarRetailIQ.eu

Figure 16. Système U’s Channel Trends in France

Source: KRiQ.eu

Sales (EUR million) Share CAGR

Channel 2008 2013 2018 2008 2013 2018 08-13 13-18

1 Supermarket 10,351 12,658 14,470 78.3% 69.5% 63.8% 4.1% 2.7%

2 Hypermarket 2,256 3,419 4,085 17.1% 18.8% 18.0% 8.7% 3.6%

3 Convenience 602 1,722 2,030 4.6% 9.4% 8.9% 23.4% 3.3%

4 Online Grocery 15 425 2,099 0.1% 2.3% 9.3% 95.8% 37.7%

Grand Total 13,224 18,223 22,684 100.0% 100.0% 100.0% 6.6% 4.5%

Système U increased its emphasis on sourcing its products from small and medium producers to both

offer smaller prices as well as an assortment with an increased regional characteristic (U De Loire

Atlantique).

Casino

Casino achieved sales of EUR18 billion with a total store network of more than 10,000 stores in 2013

(Figure 17). Casino’s multi-channel strategy aims to cater to all shoppers in France. This consists of

hypermarkets (Geant), supermarkets (Casino, Monoprix), discounters (Leader Price, Franprix),

convenience (Petit Casino, Vival, Monop’), and online grocery (Casinodrive.fr).

Recently, Casino has consolidated its position in France by initiating several major takeovers. Following

the majority stake takeover of Monoprix, it has further developed the network catering to high-density

urban areas. The retailer has also seized the opportunity of boosting its Leader Price discount chain by

taking over competitor chains Norma (South-East France) and Le Mutant (North-West France). Although

Casino operates on multiple fronts, it employs several common strategies throughout its entire store

base.

Casino lowered prices during 2013 in its Geant hypermarkets and managed to achieve leader Leclerc’s

price index in early 2014. The move was accompanied by a low price guarantee on 3,000 products. The

same strategy was deployed in the Leader Price discount chain and was accompanied by an adjustment

of the assortment to counteract a general decrease of the format’s appeal to French consumers. Price

adjustments were complemented by an increased offer of regional products in response to shopper

demand for sustainable sourcing and local taste. Casino’s Monoprix format has undergone a thorough

makeover, focusing on improved store navigation. Similarly, Leader Price’s expansion has gone hand-in-

hand with adjustments to the format’s assortment and layout.

18KantarRetail.com

KantarRetailIQ.eu

Figure 17. Casino’s Channel Trends in France

Source: KRiQ.eu

Sales (EUR million) Share CAGR

Channel 2008 2013 2018 2008 2013 2018 08-13 13-18

1 Supermarket 8,756 8,457 8,789 45.7% 47.2% 44.7% -0.7% 0.8%

2 Hypermarket 6,185 4,843 4,724 32.3% 27.0% 24.1% -4.8% -0.5%

3 Discount 2,556 2,613 2,981 13.3% 14.6% 15.2% 0.4% 2.7%

4 Convenience 1,671 1,704 1,943 8.7% 9.5% 9.9% 0.4% 2.7%

5 Online Grocery - 297 1,204 0.0% 1.7% 6.1% 32.4%

Grand Total 19,169 17,914 19,641 100.0% 100.0% 100.0% -1.3% 1.9%

Casino has increased its emphasis on developing online capabilities to complement its physical stores.

The retailer has further expanded its online proposition for Monoprix while continuing to develop and

improve Geant’s drive offer.

Although Casino’s formats lie across the whole spectrum of prices, the retailer added consistency to its

promotional proposition during 2013 by deploying the same multi-buy campaign across all formats.

Outlook/Conclusions

The French food retail industry is home to some of the world’s best retailers who ply their trade both at

home and abroad. For this reason, the industry is fast changing and quickly adopts best practices.

Kantar Retail sees the French retail market as becoming a best practice environment for several new

trends in retail, including:

Managing Haves & Have Nots. French retailers, using more sophisticated shopper data and POS

analysis, will cater their stores to a more differentiated consumer that lives in a digital age.

Advanced Fulfilment. Drive has become the format of choice for many consumers—helping

them fulfil their shopping in a speedier manner—yet this space will evolve, and France’s

retailers will propel innovation in the ways that shoppers are able to receive the goods they

purchase.

Advanced Merchandising. French retailers will manage channel blurring by creating better

point-of-purchase materials—both digital and traditional—and will create better connections

across the path to purchase, whether it originates online or in-store.

New Forms of Urban Proximity. French retailers are investing heavily in urban proximity—with

new stores and more sophisticated pickup points including lockers, depots, and by post. Drones

may be next. The city of Paris may become a very interesting test arena for the latest and

greatest in retail fulfilment.

19KantarRetail.com

KantarRetailIQ.eu

Despite all these advancements, French retailers will still struggle in an environment where consumers

are feeling defensive and competition among retailers is aggressive. Kantar Retail expects the retailers

that win to have both a “save money” and a “save time” message that they consistently fulfil. Retailers

looking to improve on these two promises will perform strongest. Mergers, acquisitions, and portfolio

expansion will continue among France’s most sophisticated chains.

20KantarRetail.com

KantarRetailIQ.eu

ABOUT KANTAR RETAIL

Kantar Retail (www.kantarretail.com) is the world’s leading shopper and retail insights and consulting business and

is part of the Kantar Group of WPP. The company works with leading branded manufacturers and retailers to help

them transform the purchase behavior of consumers, shoppers and retailers through the use of retail insights,

consulting, analytics and organisational development services. Kantar Retail tracks and forecasts over 1000

retailers globally, has purchase data on over 200m shoppers and among its market-leading reports are the annual

PoweRanking survey (USA and China), and Industry Shopper Study Across Retailers. Kantar Retail works with over

400 clients and has 20 offices in 15 markets around the globe.

INFORMATION AND INSIGHTS

Kantar Retail provides robust, data-driven insight that looks across markets, shopper and customer trends,

presenting the most accurate view of the top Global retailers and markets. By transforming this intelligence into

insights, Kantar Retail helps clients to understand the trends of today and prepare for the realities of tomorrow.

Kantar Retail Market Insights studies over 1200 of the world’s leading retailers providing invaluable data and

insights for the industry and for our clients. Clients access Kantar Retail’s Market Insights through its online

platform KRIQ, attending workshops or conferences, through webinars or by having the retail subject matter

experts visit client offices.

KantarRetailIQ.com

KantarRetailIQ.eu

KantarRetailIQ.cn

FOR MORE INFORMATION

Contact Ray Gaul

Vice President - Research

+44 (0) 207 450 2609

Ray.Gaul@kantarretail.com

Tudor Popa

Analyst

+44 (0) 207 450 2609

Tudor.Popa@kantarretail.com

21You can also read