Digital Transformation Outlook - Technology - Retail June 2020 BI Theme Book - Bloomberg LP

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

BI Theme Book Digital Transformation Outlook Technology - Retail June 2020

About Bloomberg Intelligence. Bloomberg Intelligence (BI) research delivers an independent perspective providing interactive data and investment research on companies, industries and global markets. Our team of 350 research professionals helps our clients make informed decisions in the rapidly moving investment landscape. Bloomberg Intelligence is available to Bloomberg Terminal® subscribers and can be accessed at BI . To learn more, go to bloomberg.com/intelligence. Access deeper data. E-Commerce Online Sales by IT Spending Point of Sale Venmo Volume Sales Retailer Breakdown Trends Data BI ASFT > BI APPMG > BI ISFT > BI APPRN > BI CARDN > Industry > Industry > Internet Industry SpendTrend Analyzer > PayPal E-Commerce

Covid-19’s Strong Push to Digital

Products Unlikely to Reverse

The drive to digital is reaching hyper speed and Covid-19 may be the spark

that makes the trend irreversible, with online sales in the U.S. potentially

surging 25% in 2020 while the use of e-wallets could hit $1.4 trillion by 2023.

The virus is forcing corporations and consumers to adopt new technology

faster. After this year's growth spurt, digital retail in the U.S. may expand by

midteens through 2024, according to Bloomberg Intelligence analysis, led by

grocery, home and athleisure segments. Digital payments could grow by 27% a

year.

Digital media, cloud, security software and hardware can see steady demand

as they provide the IT infrastructure for this change. Companies enabling

video-streaming services also benefit, while businesses such as traditional

advertising and cinemas could struggle for years to come.

Key Investment Topics

04 U.S. Retal Digital Sales May Double by 2024

10 E-Wallet Use to Increase 2.5x Post Pandemic

15 Expect Much Faster Shift to Cloud in 2021

22 Remote Work Tailwind for Security Software

27 Traditional Media Recovery Could Take Years

33 IT Upgrades to Aid Networking, Hardware Spend

3

The New Normal: Digital Disruption

to Accelerate

U.S. Retail Digital Sales Penetration Could Double by 2024

The advance of e-commerce sales in the U.S. may double to 22% in 2024 from

2019, our analysis shows, as coronavirus-related store closings that pushed

consumers online amid more integrated shopping via mobile apps and social

networks takes root. The rate could rise when brick-and-mortar retailers' share

is included.

Topic Takeaways

• Amazon, Walmart, Target Lead E-Commerce

• Digital Surge Accelerates, With Grocery Leading

• Online Grocery Could Reach $160 Billion in Sales by 2024

• Mobile to Lead E-Commerce Gains

• Store Closings Accelerate as Digital Grows

4

Amazon, Walmart, Target Lead E-Commerce

Double-digit e-commerce sales gains should continue even if trends moderate

from peak pandemic levels, in our view. We expect grocery, home and

athleisure to outperform this year, providing firm footing for a doubling of

overall digital sales penetration by 2024, based on our estimate for a 25%

jump in 2020 and mid-teens growth through 2024. Amazon.com, Walmart,

Target, Wayfair, Lowe's, Williams-Sonoma and Kohl's digital efforts stand out.

Walmart's e-commerce sales during the initial peak of Covid-19 reached 74%,

while Target's rose 141%. Apparel retailers' digital sales surged, even as stores

start reopening. Wayfair cited a 90% gain in 2Q-to-date sales through May 5.

In 1Q, Lowe's digital sales rose 80% and William's Sonoma delivered a low-

single-digit same-store sales gain, despite being closed for most of the

quarter.

Digital Leaders Across Retail Sectors

Source: Bloomberg Intelligence

5

Digital Surge Accelerates, With Grocery Leading

Retail e-commerce sales could see a 25% increase in 2020, led largely by the

forced shift to digital, given store closings from the pandemic. Forced behavior

changes likely fostered new habits that we think could double e-commerce

penetration by 2024. In April and May, at the height of the Covid-19 pandemic

and the number of states under shelter-in-place mandates was at its peak, e-

commerce sales already made up for 22% of total U.S. retail sales, based on

Mastercard SpendingPulse data, which exclude brick-and-mortar retailers'

share of digital. We expect double-digit gains across all subcategories in 2020,

with grocery in the lead.

Mastercard's May consumer survey found the shift to online should have a

lasting effect, with 47% of consumers indicating they'd shop less in stores post-

virus.

Retail E-Commerce Growth Projection

Source: 2015-2019 eMarketer, 2019 -2024 Bloomberg Intelligence

6

Online Grocery Could Reach $160 Billion in Sales by 2024

Food and beverage e-commerce sales could rise to $60 billion, or 5% of total

retail e-commerce sales, by 2024. Factoring in online orders that are filled by

stores -- which aren't included in Census Bureau e-commerce data -- sales

could reach as high as $160 billion in online grocery, in our view. This reflects

the growing availability of click-and-collect services and consumers who are

leaning away from home delivery, particularly outside of city centers. The rapid

rise in e-grocery is supported by accelerated long-term adoption, stemming

from consumer trial and use during the Covid-19 pandemic.

Walmart, Kroger, Albertsons and Ahold Delhaize are among retailers with the

strongest grocery digital platforms. Costco and Target have a more limited

food assortment and less robust click-and-collect grocery options.

E-Grocery Estimated Growth Through 2024 ($ Bln)

Source: 2015-2019 eMarketer, 2019 -2024 Bloomberg Intelligence

7

Mobile to Lead E-Commerce Gains

Mobile-commerce sales could make up almost 60% of total e-commerce sales

and more than 10% of overall retail sales by 2024, BI analysis shows. This

compares with 41% and 4.7% in 2019. We expect mobile sales to increase 35%

this year as shoppers spend more time on their devices amid stay-at-home

mandates. While the growth could moderate in 2021, a more than 20% gain is

still possible through 2024. Larger screen sizes, better retailer app

implementations, coupled with the rise of social, image and video shopping,

are factors contributing to the expansion. More mobile-payment use by

consumers, along with integration of that technology, will help propel growth.

Amazon.com, Walmart.com and ebay.com were the most popular mobile-

commerce apps in 2019, based on Statista data.

M-Commerce Penetration to More Than Double

Source: 2015-2019 eMarketer, 2019 -2024 Bloomberg Intelligence

8

Store Closings Accelerate as Digital Grows

An accelerated pace of store closings and bankruptcies, amid heightened

digital disruption, will transform the U.S. retail store landscape in 2020, in our

view. Many retailers can still reduce their physical footprint by 30-50 stores. In

1H, more than 15 consumer companies filed for bankruptcy including J.C.

Penney, Pier 1, Modell's Sporting Goods, Hertz and Neiman Marcus. Amid

coronavirus-driven store closings -- as long as three months in some cases --

we expect many retailers won't reopen as they seek to exit existing leases. Gap

and L Brands are actively reducing their store fleet amid the acceleration of

secular weakness.

Counterpoint: We see store expansion at off-price apparel and discount

retailers where digital is small and demand for in-store treasure-hunt shopping

is high.

Store Closings to Surge From 2019

Source: Statista, Bloomberg Intelligence

9

Digital Transformation in Payments

Digital Payments Adoption to Push E-Wallet Activity Up 2.5x

By 2023, the wallet most people will reach for to make payments will be digital,

accounting for $1.4 trillion in payments, a 27% annual increase, we calculate. A

confluence of events, including social distancing, adoption of contactless

solutions and rising smartphone penetration is accelerating the shift away from

cash to digital-payment methods.

Topic Takeaways

• Advantages Vary, But Are Strongest for Card Brands

• Demand Catalysts, Infrastructure Readiness Form Sweet Spot

• Wallets Grow as Applications Address Post-Covid Needs

• Growth Can Stick as New Functionality Is Added; Watch PayPal

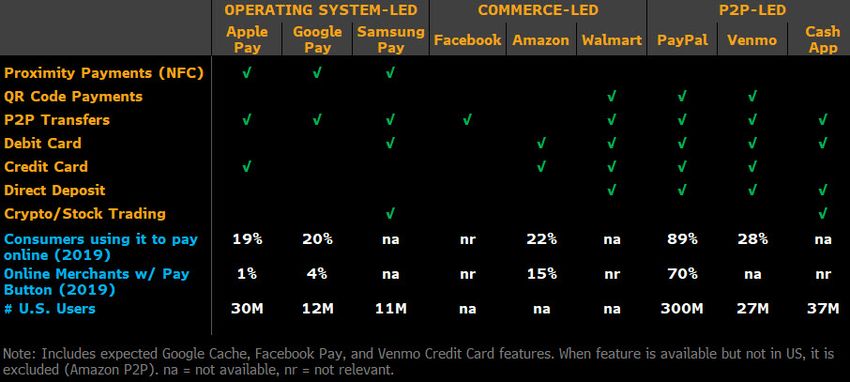

10Advantages Vary, But Are Strongest for Card Brands

Digital--wallet providers were originally dedicated to one of three applications,

but are now blurring the lines between functionality with differing goals in

mind. No matter which wallet vendors win, Visa and Mastercard will benefit

since their branded cards fund a majority of payments.

For digital payments in-store, smartphone makers embedded their own wallets

- ApplePay, Google Pay and Samsung Pay. Their goal is less about revenue, and

more to drive handset stickiness and utility. P2P apps PayPal, Venmo and

CashApp are popular mobile wallets for (mostly free) peer-to-peer payments,

but are shifting focus to related functionality that can be monetized. Finally, e-

commerce wallets from marketplaces and retailers are evolving from a

checkout convenience to sales drivers via incentives based on better customer

data.

Major Wallet Providers by Application

Source: Bloomberg Intelligence

11Demand Catalysts, Infrastructure Readiness Form Sweet Spot

There are four drivers of accelerating payment volume and adoption of digital

wallets. First is the surge in demand for e-commerce following store closures

and social distancing. BI expects e-commerce to double to 22% of total U.S.

retail by 2024, bringing e-payments with it. And digital payments are replacing

cash, which is less-sanitary amid the pandemic. Some merchants have stopped

accepting it, and ATM withdrawals are falling. Cash use has been eroding 1-3

percentage points annually, and could decline even faster from 30% globally

today.

Digital-payments infrastructure has reached critical mass. In-store, 62% of

worldwide merchant terminals are NFC-enabled for contactless cards and

smartphone wallets. And the proliferation of smartphones puts wallets in the

hands of 38% of the world's population, 72% in the U.S.

Covid-19 Drives Demand that NFC, Phones Support

Source: eMarketer, Berg Insight, Worldpay, Bloomberg Intelligence

12Wallets Grow as Applications Address Post-Covid Needs

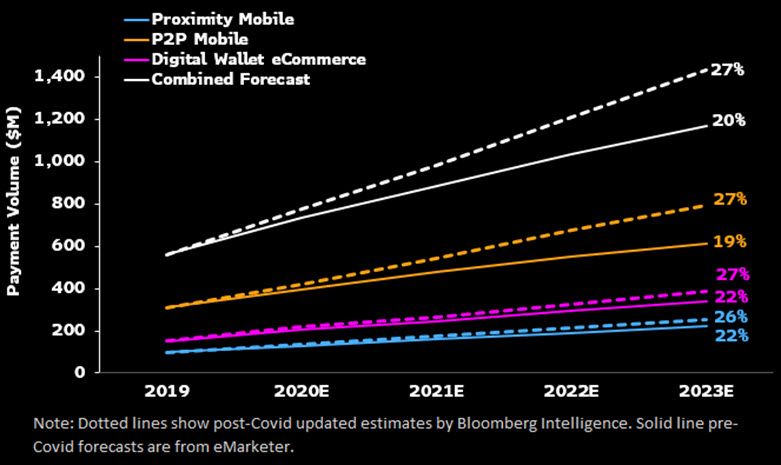

Three killer applications can increase digital-wallet payment volume 27%

compounded annually, from pre-Covid-19 industry forecasts of 19%. First, P2P

apps have evolved quickly from tools used to share expenses with friends, to a

substitute for cash when paying individuals and a social media outlet for

fundraising. As these apps add functionality, growth could reach 27% a year.

Next, E/M-commerce is growing given store closures and social distancing,

and digital wallets offer a faster, easier, more secure and rewarding way to pay

online. Greater use could expand annual payment volume by 27%. Lastly,

proximity payments via mobile phone wallets are an alternative to touching

cash or card readers. Later this year, upgrades to 5G will speed smartphone

payment-transaction time, driving annual gains to 26%

Digital Wallet Sources and Estimates of Growth

Source: eMarketer, Bloomberg Intelligence

13Growth Can Stick as New Functionality Is Added; Watch PayPal

Paying by digital wallet is a behavior that will stick post-pandemic, in our view,

as providers add new services that increase utility. P2P app vendors lead in

new product roll-outs, led by Square's CashApp. Handset makers and retailers

can catch up with their deep pockets and large user bases. Samsung Pay

announced some banking services this Spring, and Walmart has vast financial

offerings for its own ecosystem. Valuable new capabilities allow users to

send/invest/shop with stored balances; receive direct deposits and earn loyalty

benefits, giving them reasons to engage regularly, generating revenue.

PayPal stands out as a pure play in digital wallets, with its greater user

awareness, merchant site presence, suite of offerings, large user base in e-

commerce and P2P, and recent entry into proximity point-of-sale payments.

Product Portfolios of Leading Digital Wallets

Source: eMarketer, SensorTower, Bloomberg Intelligence

14Expect Much Faster Shift to Cloud in

2021

Cloud Applications, Infrastructure Get Massive Boost Post-Virus

Cloud is the cornerstone to any digital transformation and could see a

significant boost as enterprises invest more aggressively when the coronavirus

pandemic subsides. While collaboration and communication applications are

seeing strong growth, the next phase will likely be led by sales productivity and

customer service, in our view.

Topic Takeaways

• Microsoft, Salesforce, Shopify Key DX Beneficiaries

• Collaboration, Communications Near-Term Winners

• Commerce, Customer Service, Sales Could be Next

• ERP, Human Resources Pick-Up Likely to Start in 2021

• Free Trials to Prolong Revenue Recognition

• Cloud Infrastructure Shift Likely Another 2021 Story

15Microsoft, Salesforce, Shopify Key DX Beneficiaries

Pure-play cloud providers such as Salesforce.com, Workday, Shopify, Slack and

Zoom should keep seeing steady sales growth as enterprises accelerate

digital-transformation efforts. Among larger technology companies, Microsoft,

Amazon.com, Google, Oracle, VMware, IBM, SAP and Cisco may see increased

demand for their hybrid and public cloud products. The hybrid products

bridge the gap between older on-premise products with new public cloud

software that can speed the pace of their digital shift.

Digital Transformation for Top Software Players

Source: Bloomberg Intelligence

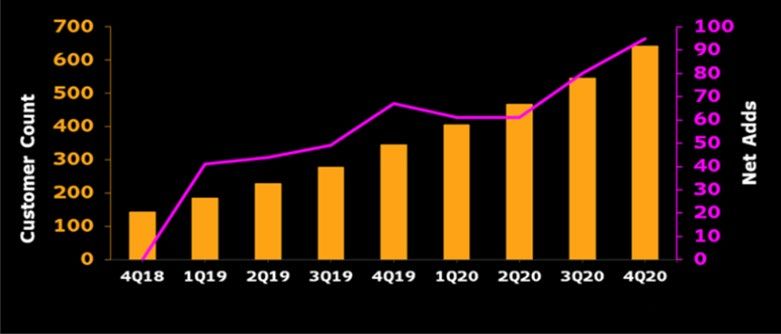

16Collaboration, Communications Near-Term Winners

The near-term beneficiaries of the disruptions caused by Covid-19 are software

products that help improve productivity and collaboration as more people

work from home. The most obvious applications seeing a demand boost are

Zoom, Microsoft Teams, Slack, Cisco Webex, Adobe, RingCentral, Twilio,

DocuSign and Citrix. It's highly likely that people will keep using these

products after the pandemic subsides and employees go back to work. Most

of these products are cloud-based and far superior than their on-premise

counterparts.

Zoom Net Additions of Customers Spending Over $100,000

Source: Company Filings, Bloomberg Intelligence

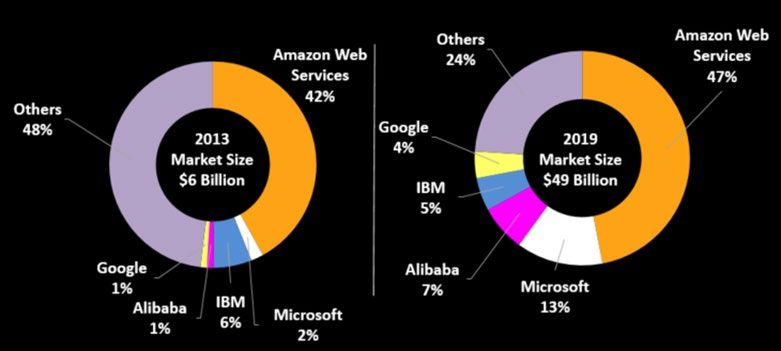

17Commerce, Customer Service, Sales Could be Next

Cloud-based commerce software is another category experiencing strong

demand, which we expect will continue, driving sales for companies such as

Shopify, Salesforce.com (Demandware) and SAP (Hybris). Sales productivity

and customer service could be the next big category that may see a strong

revival, perhaps as early as 2H, as enterprises upgrade to cloud-based

applications. These front-office applications are critical for increasing sales or

retaining clients and should see funding before back-office functions.

Cloud CRM-Market Breakdown

Source: IDC, Bloomberg Intelligence

18ERP, Human Resources Pick-Up Likely to Start in 2021

Back-office functions such as finance, which is part of the broader enterprise

resource-planning (ERP) category and human resources could take longer than

commerce or customer service, in our view. The cloud penetration rate of

broader ERP is far lower than areas such as customer service and HR and the

pandemic is making finance professionals realize the importance of cloud-

based software, especially as it relates to planning and budgeting.

Given the critical nature of this function and tight IT budgets, we believe that

the big push for this market may come in 2021. Oracle, Workday and SAP

would be the primary beneficiaries of such investment.

Cloud ERP, HR Spending Forecast

Source: IDC, Bloomberg Intelligence

19Free Trials to Prolong Revenue Recognition

While Covid-19 is likely to accelerate the need for applications, we don't expect

a boost in sales until 4Q and a recovery in 2021. The economic uncertainty led

to greater adoption of free trials, or freemium models, across many software

industries from Zoom to GoDaddy. Though this can elevate new user

registration, revenue recognition will likely be delayed into a later quarter until

these free trials convert to paid subscriptions.

Cloud-based software providers are likely to outperform legacy peers such as

SAP and Oracle in this environment since they can easily adopt newer services,

such as security enhancements or curb-side pickup, more quickly.

Wix Exemplifies Conversion Lag With Freemium Model

Source: Company Filings, Bloomberg Intelligence

20Cloud Infrastructure Shift Likely Another 2021 Story

IT infrastructure should be another major growth catalyst for the software

industry, most likely in 2021, as companies move more workloads to the public

cloud and invest in upgrading their internal systems at the same time.

Companies exposed to this faster adoption of the hybrid cloud include

Microsoft, Amazon.com, VMware, IBM (Red Hat) and Oracle. This faster shift to

public cloud could lead to enterprises closing more internal data centers,

which hurts the traditional IT-outsourcing business for companies such as IBM

and DXC Technology.

Infrastructure-as-a-Service Market Share

Source: Company Filings, Bloomberg Intelligence

21Remote Work, Digital Growth

Tailwind for Security

Remote Work, Digital Growth Spur Boost in Cybersecurity Spending

The secular shift to the cloud, an increase in remote work and higher incidence

of sophisticated breaches will aid the growth of cloud-based security

providers. Segments such as software-defined wide-area networks (SD-WAN),

endpoint detection and response (EDR), identity and access management

(IAM) and cloud gateway are poised to benefit as enterprises embrace

multicloud environments.

Topic Takeaways

• CrowdStrike, Okta, Zscaler Leaders in Cloud Security

• Increased Breaches Drive Security Spending

• Cloud Shift Poised to Accelerate

• M&A to Focus on Analytics, SD-WAN

22CrowdStrike, Okta, Zscaler Leaders in Cloud Security

While digital-transformation initiatives are likely to aid overall security-software

spending, we believe new leaders will emerge in this sector as workloads

move to the cloud from on-premise data centers. Pure-play cloud companies

such as CrowdStrike (corporate endpoint security), Okta (identity management)

and Zscaler (cloud-security gateway) will likely benefit from the trend of remote

work and will continue to grow at least 3-4x faster than the overall security

market.

The shift to behavior-based AI and machine-learning security products from

signature-based antivirus ones will hurt the prospects of NortonLifeLock

(Broadcom bought Symantec's enterprise business), McAfee and Trend Micro.

Among network-security providers, Palo Alto and Fortinet will grow much faster

than peers such as Check Point and Juniper.

On-Premise, Hybrid, Pure Cloud Security Vendors

Source: Bloomberg Intelligence

23Increased Breaches Drive Security Spending

Spending should increase for major security segments including network,

endpoints and identity management as the amount of data grows with digital-

transformation initiatives, while legacy security products prove inadequate to

handle the spike in sophisticated breaches. The upcoming U.S. elections and a

continued increase in the number of endpoint devices due to remote work

should also provide near-term boosts to overall security spending.

Security is likely to be among the fastest-growing segments of the $220 billion

infrastructure software market. While network-security companies have used

M&A to expand their cloud capabilities, an expanding perimeter for enterprise

data and applications will likely result in an accelerated share shift to cloud

companies from legacy ones in endpoint security and identity management.

Security Incidents vs. Breaches

Source: Verizon, Bloomberg Intelligence

24Cloud Shift Poised to Accelerate

The shift to the cloud is poised to accelerate in the cybersecurity market, as

companies see the benefit of cloud security amid workplace disruptions due to

Covid-19. Cloud-security gateway, or CASB, offerings should see increased

adoption with the accelerated migration of IT infrastructure and workloads to

the cloud due to more remote work. Growing preference for using cloud-

based IAM platforms for various business-to-business and business-to-

consumer applications bodes well for adoption of Okta's cloud product vs.

incumbents such as Dell, IBM and CA (Broadcom).

The secular shift to behavior-based techniques built around AI and machine

learning and away from signatures will help CrowdStrike, which continues to

take share from legacy endpoint peers such as Symantec, McAfee and Trend

Micro.

Cloud % of Security Segments

Source: IDC, Bloomberg Intelligence

25M&A to Focus on Analytics, SD-WAN

More consolidation is likely in security as both large, appliance-based firewall

companies and other infrastructure providers make deals to add capabilities in

cloud, EDR, SD-WAN, SIEM and container security. This trend was evident in

VMware's purchase of Carbon Black and Palo Alto's multiple acquisitions,

including CloudGenix, RedLock, Evident.io, Cyber Secdo, PureSec, Twistlock,

Demisto and Zingbox.

Companies such as Splunk, Tenable, Qualys and Rapid7 could be possible

targets, as both network-firewall peers including Cisco, Palo Alto Networks,

Check Point and Fortinet and endpoint-security leaders such as CrowdStrike

look to expand their analytics capabilities. SD-WAN is another high-growth

area in security that could see more consolidation after Palo Alto's recent

purchase of CloudGenix.

Recent Cybersecurity Deals

Source: Company Filings, Bloomberg Intelligence

26Media Won't Recover From Covid-19

for Years

It Will Take Years for Media to Recover From Covid-19 Clobbering

Covid-19 battered the media industry by closing theaters and theme parks,

derailing live sports and blunting ad spending, and we believe a recovery will

span years, with some semblance of normalcy in 2022. A speedier shift to

digital will weaken traditional-TV and ad-agency models and darken the

outlook for cinemas and others in the experience economy.

Topic Takeaways

• Netflix, Facebook Lead Digital Charge

• Video Streaming Clicks Deep-Six Traditional TV

• Digital Audio Set to Gain Ground

• Ad Agencies: From Mad Men to Sad Men

• Theme-Park Roller Coaster, Live Experiences Shunned

27Netflix, Facebook Lead Digital Charge

The digital revolution in media will likely continue to accelerate in the next few

years. Legacy media owners' hesitation to diversify away from traditional

businesses made them late to the game, and digital players capitalized on that

by capturing significant market share. Netflix's subscriber base reached 60

million domestically, while cord-cutting trends caused the pay-TV ecosystem to

lose more than 20% of its base.

In advertising, digital revenue topped traditional for the first time in 2018, as

large players such as Facebook and Google captured ad dollars from legacy

platforms.

Digital Transformation for Top Media Players

Source: Bloomberg Intelligence

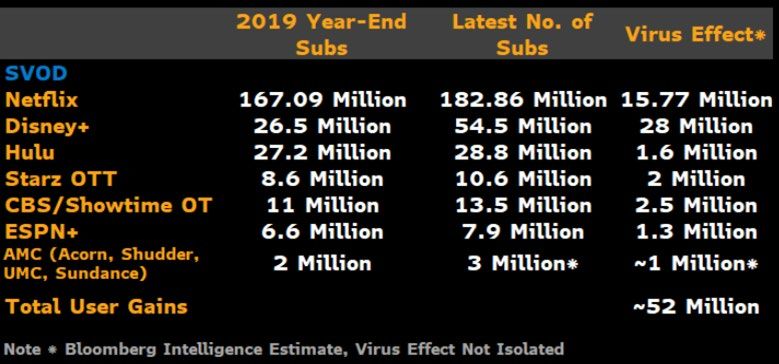

28Video Streaming Clicks Deep-Six Traditional TV

The pandemic and its economic repercussions will expand the potential

market for streaming, accelerating the shift of viewers from traditional-TV

services to cheaper streaming options, in our view. Major streaming services

have added at least 50 million subscribers since Jan. 1, as stay-at-home viewers

have been starved for entertainment. Netflix was the biggest beneficiary in 1Q,

adding almost 16 million customers. Traditional pay-TV operators lost about 2

million subscribers in 1Q. They're on track for a 9-10% decline in the 2020

subscriber base

Stay-at-home has been a boon for streaming, leading to what we believe are

lasting changes in consumer behavior. Nielsen data show time spent on

streaming more than doubled from a year ago. Netflix makes up 33% of all U.S.

streaming minutes.

Streaming Gets Covid-19 Boost

Source: Company Filings, Bloomberg Intelligence

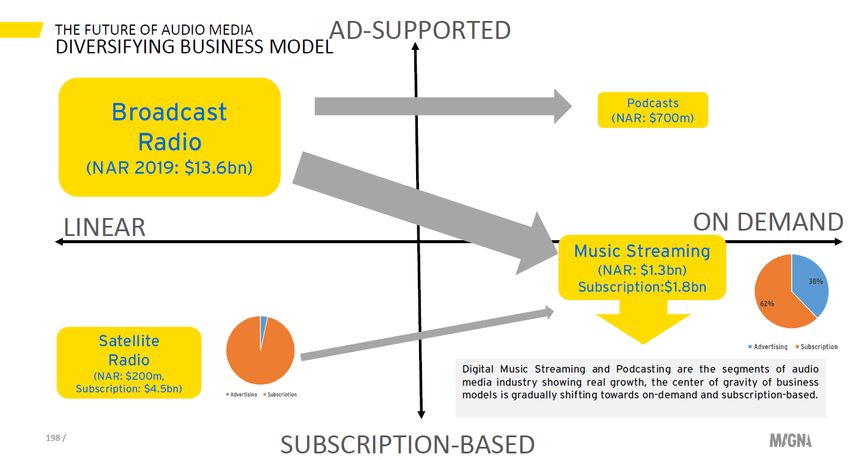

29Digital Audio Set to Gain Ground

The traditional audio business will likely be increasingly pressured by digital

players that are gaining ground because of the variety of content available

across multiple platforms. That's also due to the surge in mobile usage,

especially as new cars come with preinstalled Bluetooth technology and USB

cords. In addition, digital audio has benefited from rising demand for podcasts,

as Spotify and other competitors invest heavily in the medium. Podcasts could

accelerate the shift to on-demand platforms from traditional audio.

Spotify snagged three podcast companies -- Parcast, Gimlet Media and Anchor

FM -- for about $400 million. It bought The Ringer for about $200 million in

February, and announced a multiyear licensing deal for "The Joe Rogan

Experience" in May.

Future of Audio Media

Source: Magna Global

30Ad Agencies: From Mad Men to Sad Men

Covid-19 created a perfect storm for ad agencies, and we believe their

recovery will be a lot more difficult than after the 2008-09 recession, when they

didn't face such strong headwinds and had more leeway in cutting costs. The

industry has been upended with campaigns pulled, and the pandemic will

amplify the negative narrative because companies are shifting budgets in-

house and competition from consultancies already has squeezed fees. Organic

revenue growth, which slowed to about 1% in 2019, could slump by a mid-teens

percentage in 2020.

The long-term picture doesn't look rosy, either, as many chief marketing

officers plan long-term budget cuts. Media-buying firms and creative agencies

are likely the most vulnerable.

Organic Growth Was Challenged Even Before Virus

Source: Bloomberg Intelligence

31Theme-Park Roller Coaster, Live Experiences Shunned

Theme parks have gone from the biggest profit driver to the biggest drag for

media conglomerates such as Comcast and Disney. Social-distancing

guidelines will limit theme-park capacity significantly, and attendance is

unlikely to fully rebound until after a vaccine is widely available and the

economy improves. With the impact on travel much more severe than in prior

downturns, a multiyear slowdown is inevitable. We expect Disney's global

theme-park attendance to slip 50% in fiscal 2020 and 2021. In 2019, Disney had

more than 155 million global visits. The entire experiential sector, including live

events, will face sustained pressure over an extended period of time.

Meanwhile, Covid-19 has accelerated the shift away from traditional gyms,

creating a huge tailwind for Peloton, an at-home fitness company.

500 Million Yearly Visitors at Major Theme Parks

Source: TEA

32Enterprise Hardware in Post-Covid

World

Corporate Hardware Transformation Needs Accelerated by Covid-19

Corporations worldwide are under mounting pressure to quickly evaluate and

invest in next-generation IT, like automation, artificial intelligence and

disaggregation of software from hardware, in our view. The urgent need to

transform enterprise IT network and hardware architectures was starkly

illuminated by the sharp rise in working from home during this year's sweeping

pandemic-driven office shutdowns.

Topic Takeaways

• Cisco, Arista, Dell Could Gain From IT Architecture Changes

• Increased Automation Coming to Networks

• Virus Likely Amplifies ODM Directs' Gains

• Open Compute Project Standards Driving Growth

• Wireless-Equipment Sales Get Boost on Digital Transformation, 5G

33Cisco, Arista, Dell Could Gain From IT Architecture Changes

Investment in and evaluation of next-generation enterprise IT projects may

accelerate, as the closings of corporate offices and the sudden and dramatic

workplace changes put a spotlight on gaps and areas of under-investment in

enterprise IT architectures. The pandemic-driven operational disruptions may

accelerate the implementation of scale out and automation technologies for

on- and off- premises cloud data centers and corporate IT architectures.

Traditional hardware vendors have moved down the digital transformation

path by incorporating more software. Cisco, Arista and Extreme Juniper are

among networking vendors aiming to bring more automation to the

enterprise. Nutanix’s hyper-convergence leadership could extend gains, while

Dell and Hewlett Packard aim to keep their server footing with enterprise

customers.

Hardware Digital Transformation Enablers

Source: Bloomberg Intelligence

34Increased Automation Coming to Networks

The pandemic disruptions have revealed the operational limitations of

traditional corporate networks. Relative to public cloud providers, enterprises

have been slow to adopt automation and monitoring technologies in their own

data centers and corporate networks. Networking vendors, like Cisco, Arista,

Juniper Networks and Extreme Networks, have moved to add more

automation, artificial intelligence and monitoring functions. Data-center

switching and routing have made greater progress, as leading gear makers

have introduced or supported network automation applications and

virtualization technologies.

Automation of corporate campus networks are in the early stages, as gear

makers software-enable their campus switching and routing equipment.

Uptake may not be immediate given there’s been heightened investment in

data centers.

Data Center Networks Market Forecast

Source: IDC

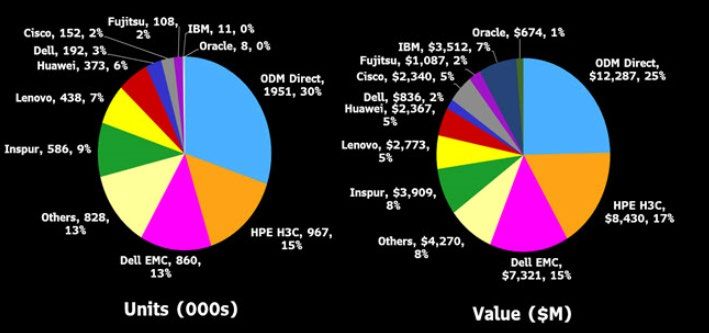

35Virus Likely Amplifies ODM Directs' Gains

Original design manufacturer (ODM) direct providers remain dominant among

server makers as the shift to the public cloud continues, and this is likely to

intensify in 2020 across both compute-intensive and storage-heavy platforms.

OEMs such as HPE and Dell are likely to keep losing unit and revenue share as

they have the past few years. The OEM category made up 70% of server units

as of 4Q19 but ODMs will steadily take away their market share and potentilly

even accelerate amid continued work-from-home growth after Covid-19. The

customer base is also extremely concentrated, with the top seven cloud-service

providers now accounting for 89% of ODM server shipments, most of which

are in the U.S.

Total Server Share (2H19)

Source: IDC

36Open Compute Project Standards Driving Growth

OEM server makers such as HPE and Dell could benefit from standards derived

from the Open Compute Project (OCP) first championed by Facebook. OCP-

inspired hardware standards have gained wide adoption and many smaller

member companies, for a variety of reasons, may prefer OCP-branded servers

and storage solutions. IDC suggests that this branded segment, while 30% of

total OCP (compute and storage) market revenue, could see a 21% CAGR from

2019-24 -- above that of the 14% of the ODM direct providers that mostly

service the hyperscale cloud buyers. Hyperscale customers account for 78% of

OCP's total revenue.

Alibaba, Amazon, Apple, Baidu, Facebook, Google, Microsoft and Tencent are

the top server customers. The OCP may account for only a portion of the

overall server and storage market, and even less of ODMs' revenue.

OCP (Compute and Storage) Infrastructure Revenue

Source: IDC

37Wireless-Equipment Sales Get Boost on Digital Transformation, 5G

An acceleration in the pace of digital transformation across industries should

provide a lift to wireless-equipment providers' sales as carriers increase

network capacity by upgrading their networks to 5G. A proliferation in devices

that require internet connectivity as a result of the shift is boosting growth in

wireless-data traffic, helping to drive a move to 5G from 4G and boosting

wireless-equipment sales. Carrier spending on 5G gear is forecast to rise to

$24.1 billion in 2023 from $7.6 billion in 2019, according to IHS.

5G Equipment Sales (Billions)

$30

$25 $23.3 $24.1

$20 $19.0

$15

$10.6

$10 $7.6

$5

$0

2019 2020 2021 2022 2023

SourceL IHS

38Analyst Team Jennifer Bartashus Boyoung Kim Senior Analyst, Food Retail, Packaged Goods Associate, Telecom Amine Bensaid Matthew Martino Analyst, Entertainment Associate, Technology John Butler Gili Naftalovich Senior Analyst, Telecom Associate, Software Julie Chariell Anurag Rana Senior Analyst, Fintech Senior Analyst, Software Abigail Gilmartin Geetha Ranganathan Associate, Consumer Senior Analyst, Media Marina Girgis Mandeep Singh Associate, Technology Senior Analyst, Internet Services Poonam Goyal Anand Srinivasan Senior Analyst, Consumer Retail Senior Analyst, Computer Hardware Woo Jin Ho Meryl Thomas Senior Analyst, Electrical Components, IT Associate, Specialty Finance Research Management David Dwyer Aude Gerspacher Research Director, Global Director of Research, AMER Drew Jones Deputy Research Director, Global Milo Sjardin Content Promotion & Marketing, Global

Take the next step. Beijing Hong Kong New York Singapore

+86 10 6649 7500 +852 2977 6000 +1 212 318 2000 +65 6212 1000

For additional information, Dubai London San Francisco Sydney

press the key twice +971 4 364 1000 +44 20 7330 7500 +1 415 912 2960 +61 2 9777 8600

on the Bloomberg Terminal®. Frankfurt Mumbai São Paulo Tokyo

+49 69 9204 1210 +91 22 6120 3600 +55 11 2395 9000 +81 3 3201 8900

bloomberg.com/intelligence

The data included in these materials are for illustrative purposes only. The BLOOMBERG TERMINAL service and Bloomberg data products (the “Services”) are

owned and distributed by Bloomberg Finance L.P. (“BFLP”) except (i) in Argentina, Australia and certain jurisdictions in the Pacific islands, Bermuda, China,

India, Japan, Korea and New Zealand, where Bloomberg L.P. and its subsidiaries (“BLP”) distribute these products, and (ii) in Singapore and the jurisdictions

serviced by Bloomberg’s Singapore office, where a subsidiary of BFLP distributes these products. BLP provides BFLP and its subsidiaries with global marketing

and operational support and service. Certain features, functions, products and services are available only to sophisticated investors and only where permitted.

BFLP, BLP and their affiliates do not guarantee the accuracy of prices or other information in the Services. Nothing in the Services shall constitute or be

construed as an offering of financial instruments by BFLP, BLP or their affiliates, or as investment advice or recommendations by BFLP, BLP or their affiliates of

an investment strategy or whether or not to “buy”, “sell” or “hold” an investment. Information available via the Services should not be considered as

information sufficient upon which to base an investment decision. The following are trademarks and service marks of BFLP, a Delaware limited partnership, or

its subsidiaries: BLOOMBERG, BLOOMBERG ANYWHERE, BLOOMBERG MARKETS, BLOOMBERG NEWS, BLOOMBERG PROFESSIONAL, BLOOMBERG

TERMINAL and BLOOMBERG.COM. Absence of any trademark or service mark from this list does not waive Bloomberg’s intellectual property rights in that

name, mark or logo. All rights reserved. © 2020 Bloomberg.

Bloomberg Intelligence is a service provided by Bloomberg Finance L.P. and its affiliates. Bloomberg Intelligence shall not constitute, nor be construed as,

investment advice or investment recommendations (i.e., recommendations as to whether or not to “buy”, “sell”, “hold”, or to enter or not to enter into any other

transaction involving any specific interest) or a recommendation as to an investment or other strategy. No aspect of the Bloomberg Intelligence function is

based on the consideration of a customer's individual circumstances. Bloomberg Intelligence should not be considered as information sufficient upon which

to base an investment decision. You should determine on your own whether you agree with Bloomberg Intelligence.

Bloomberg Intelligence Credit and Company research is offered only in certain jurisdictions. Bloomberg Intelligence should not be construed as tax or

accounting advice or as a service designed to facilitate any Bloomberg Intelligence subscriber's compliance with its tax, accounting, or other legal obligations.

Employees involved in Bloomberg Intelligence may hold positions in the securities analyzed or discussed on Bloomberg Intelligence.You can also read