Doncaster Hill - Development Opportunities and Constraints

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Doncaster Hill – Development Opportunities and Constraints

Final Draft Report

DoncasterPREPARED

Hill –FOR Development

THE LOCAL GOVERNMENT ASSOCIATION OF

SOUTH AUSTRALIA

Opportunities and Constraints

Prepared for

Manningham City Council

MacroPlan Australia Pty Ltd

July 2010

FINAL REPORT

Prepared for Manningham City Council 1

MacroPlan Australia Pty Ltd

June 2010 MACROPLAN AUSTRALIA PTY LTD

SYDNEY | MELBOURNE | BRISBANE | PERTH

Doncaster Hill – Development Opportunities and Constraints

Final Draft Report

Project Manager

Wayne Gersbach

Manager

Development Facilitation & Strategy

CONTACT Signed*

MacroPlan Australia Pty Ltd

Level 4, 356 Collins Street,

Melbourne, Vic. 3000

t 03 9600 0500

f 03 9600 1477

info@macroplan.com.au …………………………………

* This document is for discussion purposes only unless signed

and dated by the persons identified.

www.macroplan.com.au

DATE: …………………….………2009

© MacroPlan Australia Pty Ltd

All Rights Reserved. No part of this document may be reproduced, transmitted, stored in a retrieval system, or translated

into any language in any form by any means without the written permission of MacroPlan Australia Pty Ltd.

All Rights Reserved. All methods, processes, commercial proposals and other contents described in this document are the

confidential intellectual property of MacroPlan Australia Pty Ltd and may not be used or disclosed to any party without the

written permission of MacroPlan Australia Pty Ltd

Prepared for Manningham City Council 2

MacroPlan AustraliaAUSTRALIA

MACROPLAN Pty Ltd PTY LTD

June 2010

SYDNEY | MELBOURNE | BRISBANE | PERTH

Doncaster Hill – Development Opportunities and Constraints

Final Draft Report

Contents

1 EXECUTIVE SUMMARY ................................................................................. 4

2 INTRODUCTION ............................................................................................ 5

2.1 PROJECT BACKGROUND AND CONTEXT .........................................................................5

3 THE PROPERTY MARKET............................................................................. 7

3.1 MELBOURNE AND MANNINGHAM – POPULATION GROWTH...............................................7

3.2 MELBOURNE AND MANNINGHAM – HOUSE PRICE GROWTH ...........................................11

3.3 WHERE IN THE CYCLE ARE WE? ...................................................................................13

3.4 THE MANNINGHAM MARKET........................................................................................14

4 FUTURE DONCASTER ................................................................................ 19

4.1 THE DONCASTER HILL PRECINCT UPDATE ....................................................................19

4.2 THE PROPERTY DEVELOPMENT EQUATION FOR DONCASTER..........................................21

4.3 FLOOR SPACE DEMAND AND REQUIREMENTS FOR DONCASTER HILL ...............................24

5 THE NEW DONCASTER HILL VALUE EQUATION ...................................... 26

5.1 THE OUTLOOK FOR DONCASTER HILL ..........................................................................26

5.2 NEW COMPETITIVE POSITION VIZ A VIZ OTHER LOCATIONS .............................................30

Prepared for Manningham City Council 3

MacroPlan Australia Pty Ltd

June 2010

Doncaster Hill – Development Opportunities and Constraints

Final Draft Report

1 Executive Summary

Doncaster Hill is uniquely positioned in the Melbourne property market. It is:

Approximately 15 kilometres from the Melbourne CBD;

Growing at faster rate than metropolitan Melbourne; and

Identified as a Principal Activity Centre with high levels of accessibility and amenity.

Several recent development projects have occurred in Doncaster, including:

A $650 million redevelopment of the Westfield shopping centre – establishing it as a

flagship centre in Australia and expanding its market catchment draw;

The current construction of 205 apartments, with another 1,206 proposed;

A five-star $45 million hotel development (Crowne Plaza); and

A $38 million Civic Precinct Community Centre building in addition to other retail and

restaurant facilities.

Recently a property developer paid just shy of $2,000/m² for an 8,400m² bulky goods complex at

602-630 Doncaster Road (presently occupied by Officeworks and Autobarn). The site is to be

rebuilt as a $100m mixed-use village of shops, offices and apartments. Other developments are

progressing on the basis of strong pre-commitments being obtained.

Notwithstanding, there remains significant development opportunity at Doncaster Hill.

MacroPlan estimates that over 50 % of the centre’s development potential is yet to be reached.

Doncaster Hill’s primary planning document, the Doncaster Strategy, adopted in 2002, envisages

a vibrant mixed use activity centre. The strategy, and property development generally, has been

affected by recent global events. These events drastically altered property lending conditions and

development yields. Such conditions have only just begun to revert to ‘normal’ with underlying

land values on the mend, with banks beginning to unfreeze their credit policies and as property

portfolios begin to regain some of the gloss lost to share markets.

In MacroPlan’s opinion there remains significant underlying demand for the type of high-density

mixed use development envisaged by the Doncaster Hill Strategy. This demand will continue to

grow with population changes and the return of more favourable property investment

conditions.

Having out-lasted the ill effects of the global financial crisis the Strategy for Doncaster is now well

placed to attract market interest. The property fundamentals of Manningham / Doncaster as an

investment location remain strong – it has a growing population, increasing underlying land

values, distinctive locational advantages and a solid critical development mass to build from.

With these credentials MacroPlan believes that Doncaster will, particularly over the next decade,

develop into the vibrant urban community envisaged by its Strategy.

Prepared for Manningham City Council 4

MacroPlan Australia Pty Ltd

June 2010

Doncaster Hill – Development Opportunities and Constraints

Final Draft Report

2 Introduction

MacroPlan has been commissioned by the Manningham City Council to provide a commentary

with respect to the opportunities and constraints for property development at Doncaster Hill.

Our report provides an up-to-date assessment of the changing socio-demographic profile of

Doncaster, current house price trends and other economic trends and drivers relevant to

Manningham and Doncaster.

Our report confirms the potential to create a ‘state of the art’, contemporary, sustainable, high

density mixed use village at Doncaster that enhances the social, environmental, economic and

cultural characteristics of the centre.

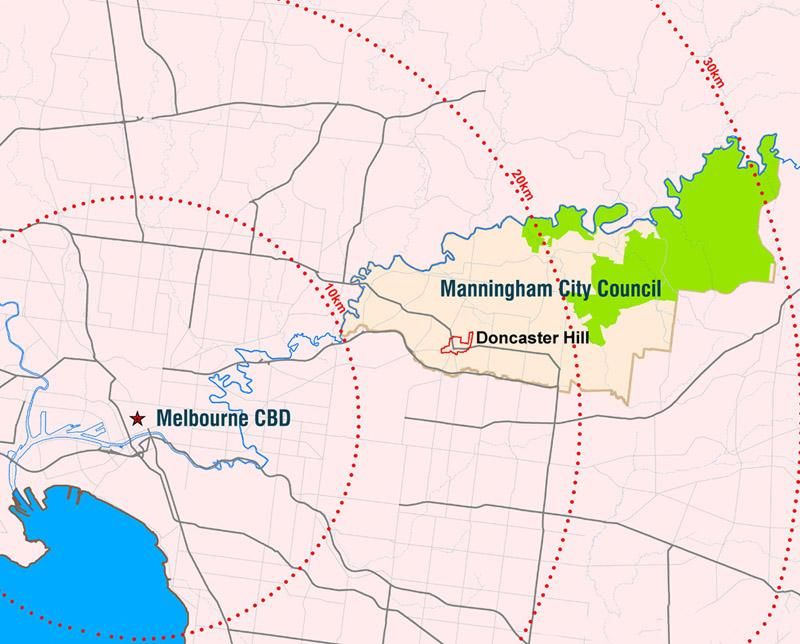

Figure 1. Doncaster – Location and Metropolitan Setting

Source: Manningham City Council (2010)

2.1 Project Background and Context

In 2004 Manningham City Council engaged MacroPlan to assess development opportunities and

potential constraints at Doncaster Hill, with particular reference to Council’s Doncaster Hill

Strategy.

Prepared for Manningham City Council 5

MacroPlan Australia Pty Ltd

June 2010

Doncaster Hill – Development Opportunities and Constraints

Final Draft Report

The document examined the state of the property market, the impact of building cost increases

and changing demographics and how these impacted upon the future development of the

precinct.

This report builds upon the previous 2004 work and presents information in a similar manner.

Prepared for Manningham City Council 6

MacroPlan Australia Pty Ltd

June 2010Doncaster Hill – Development Opportunities and Constraints

Final Draft Report

3 The Property Market

3.1 Melbourne and Manningham – Population Growth

Between 2001 and 2009 Victoria grew by 640,000 people to reach a total population of

approximately 5.4 million, with greater Melbourne reaching a population of approximately 4

million.

Figure 2. Population Growth in Victoria and Melbourne

8,000,000

7,000,000

6,000,000

5,000,000

4,000,000

3,000,000

2,000,000

1,000,000

0

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

Melbourne Rest of Victoria

Source: ABS Regional Population Growth (Cat. NO. 3218.0, 2010); Victoria in Future (2009); MacroPlan Australia

(2010).

Current population growth is summarised as:

Victoria’s population is presently 5,473,300 (Sept 2009 ERP), an increase of 30,000 (0.6%)

since the June quarter

Over the same quarter, Australia's ERP grew by 110,400 (0.5%)

In 12 months Victoria's ERP increased by 117,900 (2.2%)

Victoria’s 2008-09 growth rate of 2.2% was higher than the average growth rate of 1.8%

experienced for the five years to June 2009

Over 30 years to 2036 Victoria is predicted to grow by an additional 2.3m people, with

1.8m of these expected to live in Melbourne (and almost 50% of this growth expected to

be accommodated in established areas)

Prepared for Manningham City Council 7

MacroPlan Australia Pty Ltd

June 2010Doncaster Hill – Development Opportunities and Constraints

Final Draft Report

Melbourne’s rapid population growth has been driven largely by a substantial increase in net

overseas migration and an increase in natural births over deaths. Notably also, less people are

now leaving Victoria for interstate locations.

The following figure demonstrates these state-wide trends for the period 1996-2010.

Figure 3. Victorian Population Drivers, 1996 – 2010

40,000

35,000

30,000

25,000

20,000

15,000

10,000

5,000

0

Nov-1996

Nov-2001

Nov-2006

Dec-1998

Dec-2003

Dec-2008

Oct-1999

Oct-2004

Jan-2001

Jan-2006

May-1999

May-2004

May-2009

Apr-1997

Apr-2002

Apr-2007

Feb-1998

Aug-2000

Feb-2003

Aug-2005

Feb-2008

Mar-2000

Mar-2005

Jun-1996

Jun-2001

Jun-2006

Sep-1997

Sep-2002

Sep-2007

Jul-1998

Jul-2003

Jul-2008

-5,000

Natural Increase Net Overseas Migration Net Interstate Migration Change Over Previous Quarter

Source: ABS Regional Population Growth (Cat. NO. 3218.0, 2010); Victoria in Future (2009); & MacroPlan Australia

(2010).

Melbourne’s rate of population growth is also reflected at the Manningham LGA level, as

depicted in the following graph.

Prepared for Manningham City Council 8

MacroPlan Australia Pty Ltd

June 2010Doncaster Hill – Development Opportunities and Constraints

Final Draft Report

Figure 4. Population Growth in Manningham

135,000

Estimated Residentail Population Actual

130,000

Projected

125,000

120,000

115,000

110,000

105,000

100,000

1996

2000

2004

2008

2012

2016

2020

2022

2024

2026

1998

2002

2006

2010

2014

2018

Source: ABS 3218 Estimated Residential Population, Victoria in Future 2009 and MacroPlan Australia (2010)

The LGA’s growth rate since 2006 has been 2.9%, 0.5% faster than Melbourne as a whole over

the same period (2.4%).

Manningham’s population at the time of the 2006 Census was 108,843. Its current population is

118,544 persons (ERP June 2009).

The characteristics of the Manningham population are outlined in the following table.

Prepared for Manningham City Council 9

MacroPlan Australia Pty Ltd

June 2010Doncaster Hill – Development Opportunities and Constraints

Final Draft Report

Figure 5. Doncaster, Manningham and Melbourne – Population Characteristics

Source: ABS Census 2006 & MacroPlan Australia (2010)

Manningham’s population can most readily be categorised as affluent, mature and traditional.

It has a larger percentage of persons aged 55 and over (30%) than metropolitan Melbourne

(23%). Notably, Doncaster has a higher proportion of persons aged 55 and over than both

Manningham and Melbourne (at 35%).

Manningham and Doncaster also have a higher proportion of home owners and buyers than

metropolitan Melbourne (at 85%, 82% and 73% respectively). This level of home ownership and

population ageing suggests that there is a high potential for older home-owners in Manningham

and Doncaster to cash out the family home to downsize their accommodation type or to consider

retirement living.

Prepared for Manningham City Council 10

MacroPlan Australia Pty Ltd

June 2010Doncaster Hill – Development Opportunities and Constraints

Final Draft Report

3.2 Melbourne and Manningham – House Price Growth

The table below shows that Melbourne homes had the third highest price increases in real terms

over the last five years to March 2010 of any capital city, behind only Perth and Darwin.

Figure 6. National Median House Prices

Change

Mar-05 Mar-10 %

Sydney 95.5 115.7 21.2

Melbourne 102.0 174.1 70.7

Brisbane 104.8 155.1 48.0

Adelaide 107.0 160.8 50.3

Perth 116.3 208.8 79.5

Hobart 112.5 159.8 42.0

Darwin 120.1 226.3 88.4

Canberra 100.6 147.4 46.5

Australia 101.3 148.5 46.6

Source: ABS 6146.0 2010, MacroPlan 2010

This trend is further demonstrated in the figure below, which tracks actual house price values

from 2002 to 2010.

Figure 7. National Median House Prices

600.0

500.0

Sydney

400.0

$ Thousnands

Melbourne

300.0 Brisbane

Adelaide

200.0 Perth

Hobart

100.0

Darwin

0.0 Canberra

Sep-2002

Sep-2003

Sep-2004

Sep-2005

Sep-2006

Sep-2007

Sep-2008

Sep-2009

Mar-2002

Mar-2003

Mar-2004

Mar-2005

Mar-2006

Mar-2007

Mar-2008

Mar-2009

Source: ABS House Price Indexes (March 2010) and MacroPlan Australia (2010).

This price growth has occurred notwithstanding a comparatively healthy addition to dwelling

stock across Victoria and Melbourne. It has been buoyed by the immediate post-GFC low interest

Prepared for Manningham City Council 11

MacroPlan Australia Pty Ltd

June 2010Doncaster Hill – Development Opportunities and Constraints

Final Draft Report

rate environment and further aided by recent government assistance to first and other home

buyers.

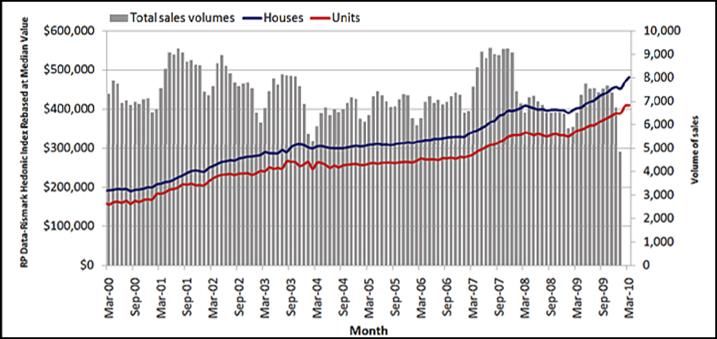

The following graphs track Melbourne’s sales volumes and dwelling prices as well as interest rate

movements.

Figure 8. Melbourne House and Unit Prices

Source: RP Data (2010)

Figure 9. Target Cash Rate – Reserve Bank of Australia

8.00%

7.00%

Cash Rate (%)

6.00%

5.00%

4.00%

3.00%

2.00%

1.00%

0.00%

May-01

May-03

May-05

May-07

May-09

Sep-06

Sep-00

Sep-02

Sep-04

Sep-08

Jan-00

Jan-02

Jan-04

Jan-06

Jan-08

Jan-10

Target Cash Rate

Source: Reserve Bank of Australia 2010; MacroPlan Australia 2010

Prepared for Manningham City Council 12

MacroPlan Australia Pty Ltd

June 2010Doncaster Hill – Development Opportunities and Constraints

Final Draft Report

3.3 Where in the Cycle are we?

An analysis of construction activity in Victoria over time shows that, generally, there are surges in

construction activity every three to five years and that the nature of building activity is often

sectoral.

At present residential activity in Victoria is strong, despite a level of residential under-building

across Australia.

Figure 10. Value of Building Work – Victoria 1985 – 2010

Source: ABS 8755.0; MacroPlan Australia 2010.

Prepared for Manningham City Council 13

MacroPlan Australia Pty Ltd

June 2010Doncaster Hill – Development Opportunities and Constraints

Final Draft Report

Figure 11. Trends in Australian Dwelling Approvals and Completions

200000

Approvals

Completions

180000 Compl.

long term

160000

140000

120000

100000

80000

Source: ABS 8731 & 8752; MacroPlan 2010

3.4 The Manningham Market

Since the early 2000s the value of the Manningham property market has increased substantially.

This increase has coincided with the release of the Doncaster Hill Strategy in 2002 and a number

of key developments in the area. In particular the Westfield shopping centre expansion has

cemented Doncaster Hill’s position as a key activity centre in metropolitan Melbourne. Westfield

Doncaster attracts over 7 million consumers a year.

Current House Prices

Median house prices at Manningham have risen by $330,000 from 2000 levels to average prices

in excess of $600,000.

Prepared for Manningham City Council 14

MacroPlan Australia Pty Ltd

June 2010Doncaster Hill – Development Opportunities and Constraints

Final Draft Report

Figure 12. Metropolitan Melbourne V Manningham Median House Prices

$700,000

Manningham

$600,000

Metropolitan Melbourne

$500,000

Median House Pirce

$400,000

$300,000

$200,000

$100,000

$0

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

Source: Valuer Generals (2009) and MacroPlan Australia (2010)

Doncaster has also experienced a substantial increase in housing values since 2000, particularly

over recent years.

The median house price as at the March quarter in 2010 at Doncaster was $804,500 compared to

$763,000 in the December quarter 2009.

Doncaster is not alone in its experience of meteoric house value increases. Doncaster

experienced a 37.4% annual increase in house prices to March 2010, whilst other neighbouring

suburbs within the Manningham LGA experienced growth in excess of 50%.

Importantly, this bullish market means that the construction of medium and high density

dwelling product at Doncaster and surrounding markets has become far more financially viable

than was previously the case when MacroPlan last assessed market conditions in 2004.

Figure 13. House Prices in Manningham

Upper Dec 09 Mar 09 Quarterly Annual

Lower Mar 10

Quartile Median Median Change Change

Suburb Quartile Median

Doncaster $751,500 $804,500 $839,888 $763,000 $585,500 5.40% 37.40%

Doncaster East $662,500 $738,000 $831,000 $687,500 $629,100 7.30% 17.30%

Donvale $683,750 $777,500 $966,250 $750,000 $575,000 3.70% 35.20%

Templestowe $774,225 $949,444 $1,227,750 $845,400 $677,550 12.30% 40.10%

Templestowe

Lower $690,000 $738,000 $840,000 $694,500 $541,500 6.30% 36.30%

Warrandyte $669,500 $853,750 $1,022,500 $775,000 $537,500 10.20% 58.80%

Source: Real Estate Institute of Victoria and MacroPlan Australia

Prepared for Manningham City Council 15

MacroPlan Australia Pty Ltd

June 2010Doncaster Hill – Development Opportunities and Constraints

Final Draft Report

Figure 14. Median House Price Trends – Manningham, March 2006-2010

Source: Real Estate Institute of Victoria

The Global Financial Crisis impacted on different suburbs in Manningham in different ways. At

Doncaster prices fell by $100,000 over a six month period, then recovered within a year and

subsequently increased to their current high levels.

Building Activity

As demonstrated by the below graph, residential building approvals in Manningham peaked in

2005.

The overall number of residential building approvals at Manningham declined steadily over the

three years from 2005 and then rose in 2009. The important point to note is that the decline

from 2006 to 2008 was mostly for separate houses and that the increase to 2009 was driven

mainly by higher density dwellings.

Notably, approvals of higher density dwellings have comprised about half of the dwelling

approvals over the past 5 years.

Prepared for Manningham City Council 16

MacroPlan Australia Pty Ltd

June 2010Doncaster Hill – Development Opportunities and Constraints

Final Draft Report

Figure 15. Building Approvals in Manningham

600

Separate Houses

Higher Density

500

Building Approvals - Manningham LGA

400

300

200

100

0

2004

2005

2006

2007

2008

2009

Source: ABS Building Approvals (2010) and MacroPlan Australia (2010).

The following figure tracks the value of building permits in residential and non-residential

markets from 2001.

Notably, the value of retail and commercial development has increased in Manningham over the

last five years. The strength of these sectors is encouraging and reinforces the context of

Manningham and the role of Doncaster (as the major centre in Manningham) in the Melbourne

metropolitan strategy – i.e. the LGA’s role as a key inner-urban location and Doncaster Hill’s role

as a major activity centre.

Although the total value of residential building permits issued in Manningham has declined,

MacroPlan’s investigations as to the current underlying value of residential projects suggests that

the 2003-2010 trend in building approvals may be reversed if current market conditions remain.

The recent flurry of commercial and retail development at Manningham demonstrates the

cyclical nature of activity in a mixed use market. The fact that this level of commercial and retail

development has occurred, however, has now made Doncaster a more attractive residential

investment proposition.

Further discussion on the current market appetite for retail, commercial and residential

development at Doncaster is provided in the following chapter.

Prepared for Manningham City Council 17

MacroPlan Australia Pty Ltd

June 2010Doncaster Hill – Development Opportunities and Constraints

Final Draft Report

Figure 16. Value Trends in Building Permits – Manningham

50

45

40

35

30 Retail

25

$m

Commercial

20

Residential

15

10

5

0

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Source: Building Activity Profile – Building Commission Victoria and MacroPlan Australia (2010)

Prepared for Manningham City Council 18

MacroPlan Australia Pty Ltd

June 2010Doncaster Hill – Development Opportunities and Constraints

Final Draft Report

4 Future Doncaster

‘Melbourne @ 5 million’ sets a target for an additional 600,000 dwellings by 2030, with at least

53% or 318,000 of these expected to be provided in the established urban areas. A good deal of

this population and dwelling growth is anticipated to occur in nominated redevelopment sites

(i.e. in Principal Activity Centres and Major Activity Centres). Doncaster Hill is identified as a

Principal Activity Centre.

4.1 The Doncaster Hill Precinct Update

It is anticipated that recent State Government initiatives such as the introduction of the new

Activity Centre Zone will act to encourage further development at the Doncaster Hill centre. It is

also noted that Doncaster Hill has been selected by Sustainability Victoria as a Smart Energy Zone

and has accordingly been awarded grants of up to $2 million from Federal and State

governments to assist in the implementation of energy generation and efficiency measures.

Recently developments at Doncaster Hill include:

A $650m redevelopment of the Westfield shopping centre – establishing it as a flagship

centre in Australia and expanding its market catchment draw;

205 residential apartments under construction, with another 1,206 proposed;

A five-star $45m hotel development (Crowne Plaza); and

A $38m Civic Precinct Community Centre building, in addition to other retail and

restaurant facilities.

Also, recently an Asia-based builder has paid $16.25m for an 8,400m² bulky goods complex at

602-630 Doncaster Road (presently occupied by Officeworks and Autobarn). The site is to be

rebuilt as a $100m mixed-use village of shops, offices and apartments.

Prepared for Manningham City Council 19

MacroPlan Australia Pty Ltd

June 2010Doncaster Hill - Development Opportunities and Constraints

Final Draft Report

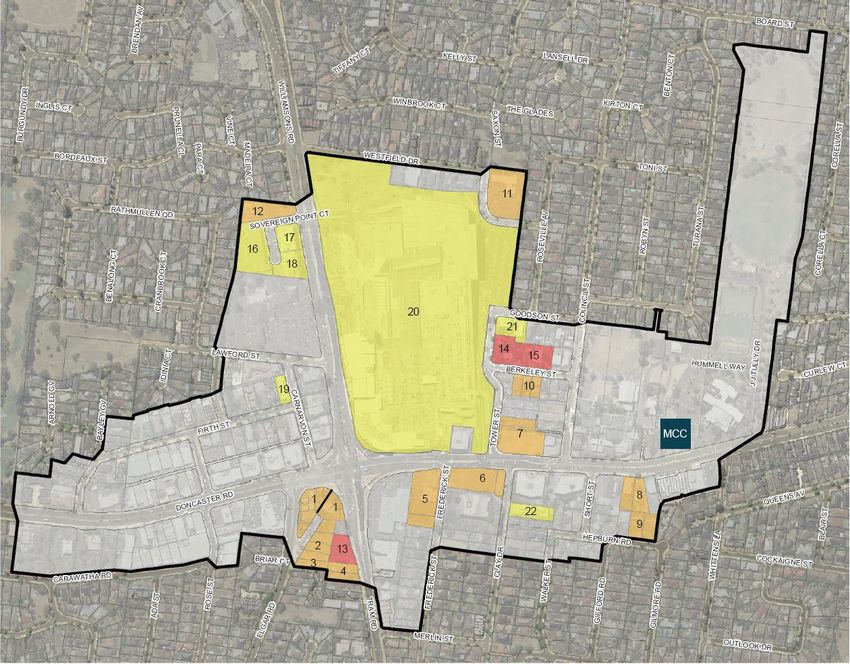

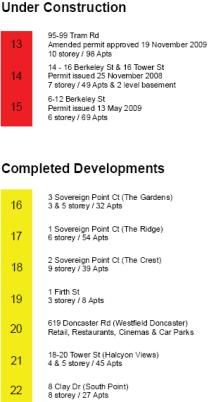

Figure 17. Recent Doncaster Hill Developments

Prepared for Manningham City Council 20

MacroPlan Australia Pty Ltd

June 2010Doncaster Hill – Development Opportunities and Constraints

Final Draft Report

4.2 The Property Development Equation for Doncaster

In order to test the relevance of the Doncaster Hill Strategy, MacroPlan has considered the

underlying value proposition for residential, commercial and mixed use (retail) development in

order to fathom the market’s potential appetite for development at the Hill.

For the purpose of this exercise MacroPlan has updated previous advice and property value

information provided in its 2004 report, i.e. it has used the same property characteristics but

updated its models based on current sales values for residential, retail and office uses.

The results of MacroPlan’s findings are summarised below:

Residential Development

Land at Doncaster is presently valued at around $50,000 per apartment.

Applying this rule of thumb value to a 200 unit development project we find that the market

could absorb a purchase price for the land of up to $10 million. In other words if the site was

purchased for $5 to $7 million, it would offer good value for high-density residential

development.

The feasible development of sites at Doncaster will obviously depend on other factors such as

trends in building costs and the cost of finance but the above rule of thumb is relevant for

comparison to other development opportunities.

Commercial and Retail Land

The equation for commercial and retail land is more complex as the feasibility of this form of

development depends not only on the price of ‘raw’ land, building costs and expected sale prices,

but also on the projected rental yield and take-up rates.

Whilst prices of up to $2,000 per square metre have been paid for ‘raw’ commercial land in the

Manningham/ Doncaster area, high construction costs (of up to $2,300 per m²), a low demand

base and a retail value of around $4,000 per m² for retail and $4,500 per m² for office space

means that commercial developments in their own right are difficult to stack up. This does not

mean, however, that commercial and retail development cannot be incorporated into mixed use

developments to support overall project viability.

Mixed Use Development Feasibility Case Study

In order to demonstrate the impact of project variables on overall feasibilities MacroPlan has

updated a demonstration case study of a hypothetical mixed use development project on a

5,000m² site on Doncaster Road. The case study compares construction and other costs and

overall potential profit levels in today’s market with the same development scenario from our

2004 report.

Prepared for Manningham City Council 21

MacroPlan Australia Pty Ltd

June 2010Doncaster Hill – Development Opportunities and Constraints

Final Draft Report

The following development approval and cost assumptions have been used:

Residential - 132 apartments @ at average size 100m² each = 13,200m²

Retail - 1,828m² including a restaurant

Office - 1,525m²

Car park - 285 spaces

Residential Construction Costs - $3,000/m²

Retail Construction Costs - $1,800/m²

Office Construction Costs - $2,300/m²

Interest Rate - 7.5%

LVR - 60%

The costs listed above represent average construction costs for suburban Melbourne and are

based on the industry-accepted Rawlinsons Australian Construction Handbook (2010). The costs

of construction for residential are 30% higher than 2004, while retail and office construction

costs have risen 10% and 7% respectively.

The development equation for each component of the development is depicted below:

Figure 18. The Residential Equation

Year 2004 Year 2010

RESIDENTIAL EQUATION - 13,200m² offer

Revenue from sales @ $6,000/m² $51,744,000 $77,616,000

Less developers 20% share of sales revenue -$10,348,800 -$15,523,200

Net sales revenue $41,395,200 $62,092,800

Construction Cost of Apartments @ $3,000/m² $30,360,000 $39,600,000

Construction Cost of Carparks @ $800/m² $6,076,000 $9,873,500

TOTAL CONSTUCTION COST -$36,436,000 -$49,473,500

Interest allowance on borrowed funds -$2,550,520 -$4,452,615

TOTAL PROJECT COST -$38,986,520 -$53,926,115

SUPER PROFIT / ADDITION TO LAND VALUE $2,408,680 $8,166,685

Prepared for Manningham City Council 22

MacroPlan Australia Pty Ltd

June 2010Doncaster Hill – Development Opportunities and Constraints

Final Draft Report

Figure 19. The Retail Equation

Year 2004 Year 2010

RETAIL EQUATION – 1,828m² offer

Revenue from sales @ $4,000/m² $5,374,320 $7,165,760

Less developers 20% share of sales revenue -$1,074,864 -$1,433,152

Net sales revenue $4,299,456 $5,732,608

Construction Cost of Retail @ $1,800/m² $2,997,920 $3,290,400

Construction Cost of Carparks @ $800/m² $1,120,000 $1,120,000

TOTAL CONSTUCTION COST -$4,117,920 -$4,410,400

Interest allowance on borrowed funds -$288,254 -$396,936

TOTAL PROJECT COST -$4,406,174 -$4,807,336

SUPER PROFIT / ADDITION TO LAND VALUE -$106,718 $925,272

Figure 20. The Office Equation

Year 2004 Year 2010

OFFICE EQUATION – 1,525m² offer

Revenue from sales @ $4,500/m² $5,230,750 $6,725,250

Less developers 20% share of sales revenue -$1,046,150 -$1,345,050

Net sales revenue $4,184,600 $5,380,200

Construction Cost of Office @ $2,300/m² $3,263,500 $3,507,500

Construction Cost of Carparks @ $800/m² $784,000 $784,000

TOTAL CONSTUCTION COST -$4,047,500 -$4,291,500

Interest allowance on borrowed funds -$283,325 -$386,235

TOTAL PROJECT COST -$4,330,825 -$4,677,735

SUPER PROFIT / ADDITION TO LAND VALUE -$146,225 $702,465

Prepared for Manningham City Council 23

MacroPlan Australia Pty Ltd

June 2010Doncaster Hill – Development Opportunities and Constraints

Final Draft Report

Overall the above analysis demonstrates that a mixed-use residential/office/retail development

providing the developer with a 20 per cent return on sales yields the following returns:

2004 2010

Total project sales revenue $49.9 million $73.2 million

(net of developers share)

Total project cost $47.72 million $58.2 million

Total addition to land value $2.155 million $9.8 million

The total addition to land value represents the profit margin above the developers’ return of 20%

on sales revenue. It can be used to assess whether the purchase price of land is feasible as part

of the overall project cost equation.

The above table reveals that the total addition to land value ($9.8 million) has increased almost

five-fold since 2004 levels.

Land at Doncaster Hill has recently sold for around $2,000/m². Using the hypothetical total

addition to land value for 2010 from the above case study of $9.8m for a 5,000m² site represents

a ‘raw’ value of $1,960. In this case, therefore, the development yield from the mixed use

development is sufficient to cover land and other costs. In 2004, under the same assumptions

but with different sales values, the hypothetical project was found to be unviable. The increase in

market values for residential, retail and commercial product has therefore helped to improve the

viability of development options at Doncaster since 2004.

Importantly, the most valuable development scenario from those tested is residential

development, with an end sale price of around $6,000 per m². This finding strongly supports the

underlying tenet of the Doncaster Hill Strategy to support and promote mixed use development

at the centre, i.e. the primary residential focus of the Doncaster Strategy is in keeping with

current market expectations and will provide a strong underpinning of mixed use developments

within the centre over the short-medium term.

MacroPlan’s development equation assessment suggests that the financial uncertainty that

dogged development projects over the last 5 years at Doncaster may have “turned a corner” as

demonstrated by current market values and the fact that the worst of the global financial crisis

has passed. As lending conditions ease and a renewed focus on property portfolios emerges, it is

likely that Doncaster’s development opportunities will be more eagerly sought in the immediate-

short term, barring any significant global relapse.

Our review has demonstrated the cyclical nature of property investment and the impact of

construction costs and retail costs, inter alia, on project viabilities. It is, accordingly, appropriate

for Council to revisit fundamental market conditions at regular intervals to test market

responsiveness or the relevance of planning and like controls at that time in the property cycle.

Commentary on these matters is provided in the following section.

4.3 Floor space demand and requirements for Doncaster Hill

In 2007 Manningham Council commissioned work by Tim Nott to consider the range of

compatible non-residential activity (e.g. local neighbourhood retailing, entertainment activities,

Prepared for Manningham City Council 24

MacroPlan Australia Pty Ltd

June 2010Doncaster Hill – Development Opportunities and Constraints

Final Draft Report

office development and community facilities) that could be supported by the predominant

residential development anticipated at Doncaster Hill.

The main findings of the ‘Neighbourhood Commercial Activities for Doncaster Hill (May 2007)’

report were:,

By 2021 new residents will create demand for 5,000-17,000 m2 of additional non-

residential uses that could be located outside of Westfield, such as local convenience

stores, newsagents, restaurants, cafes and video stores as well as community and

entertainment facilities.

If co-located with residential developments, non-residential uses would need to be

located on ground floors to capture passing trade and promote business

Planning strategies from other centres revealed that a mix of uses is essential for

successful centres, but that two different uses in the same building – office/retail,

residential/retail or residential/community – were more acceptable to the market than

three or more different uses

A further Review of Retail Floor Space (July 2008) by Tim Nott compares the implications of four

different retail floor space controls for Doncaster Hill and recommends that the existing ‘15% of

site area’ control be abandoned in favour of a ‘12.5% of building area’ control. The review

identifies that this control could deliver 46,000m² of retail space compared to an identified need

of 38,000m² by 2031..

The report notes that controls recommended by the State Government’s Priority Development

Panel (PDP), i.e. a ‘25% of building area’ control, would generate up to 97,000m² of retail space,

some 59,000m² in excess of estimated demand and potentially to the detriment of nearby

smaller local centres.

It is noted that the recent doubling in size of the Doncaster Westfield (from 51,000m² and 202

retail outlets to 111,000m2 and 400 outlets) to become the fifth largest shopping centre in

Australia has added an extra 60,000m2 of retail to the Doncaster Hill precinct, which is well above

the required 38,000m2 identified by Nott. In this context, a debate about the specific controls to

encourage more retail development in the present climate may be futile. Accordingly, the

approach recommended by Nott more realistically responds to a quantum of retail space that the

market may be prepared to deliver, although it is likely that the rate of that delivery may slow in

the immediate future.

MacroPlan’s above findings (Section 4.2) highlight the comparative attractiveness of residential

development at Doncaster Hill at this point in time of the property cycle. Council’s continued

focus on the residential potential of Doncaster is therefore supported by current market

conditions. Any undue increase in retail development capacity may serve to contradict this policy

emphasis and should therefore be avoided.

Prepared for Manningham City Council 25

MacroPlan Australia Pty Ltd

June 2010Doncaster Hill – Development Opportunities and Constraints

Final Draft Report

5 The New Doncaster Hill Value Equation

This chapter further examines what the future market opportunities at Doncaster might look like.

5.1 The Outlook for Doncaster Hill

Our outlook is influenced by the following factors:

The Manningham LGA currently has an employment self-containment level of 21.9%.

Approximately 16% of Manningham’s workforce travel to Melbourne CBD to work, while

a further 24% work in surrounding LGAs. Manningham’s self-sufficiency is about average

for similarly positioned LGAs in metropolitan Melbourne, although the strong

representation of people working in adjacent LGAs suggests that there is a capacity to

draw back some of these jobs to Manningham. Doncaster is expected to increasingly

become an employment destination of choice for the LGA’s workforce.

Elsewhere in Australia

5.0% Melbourne (C)

16.2%

Elsewhere in Victoria

32.8%

Manningham (C)

21.9%

Adjacent LGAs

24.1%

Source: ABS, Journey to Work Data, 2006

This suggests that more employment opportunities could be offered at Doncaster to

capture residents leaving the LGA for work. The strong regional availability of jobs also

suggests that Doncaster, with its strong public transport (bus) linkages, could perform

the role of an origin centre providing a residential base for resident workers travelling

elsewhere in the region for work.

New housing products will be required to meet expected demand generated from

Manningham’s continued population growth. Changing household structures, including

an increase in sole person households and an increasing proportion of residents born

overseas, will drive demand for a higher density accommodation offer.

Melbourne’s increasing remote and mobile workforce and the increased level of wealth

that this brings will also drive a demand for low-maintenance higher density dwellings.

Prepared for Manningham City Council 26

MacroPlan Australia Pty Ltd

June 2010Doncaster Hill – Development Opportunities and Constraints

Final Draft Report

This increased wealth is expected to drive a demand for high end products/premium

locations in the Manningham area and an increased demand for multiple dwelling

buildings as more people seek to take advantage of the LGA’s offerings.

Manningham’s and Doncaster’s attractiveness compared to other centres an equal

distance from Melbourne CBD is such that new development is likely to attract residents

from both neighbouring localities and localities further afield. Manningham is well

serviced by the M3 Eastern Freeway and orbital bus links and there is a genuine lack of

similar sized and similarly located centres with sufficient underlying land value to attract

investors and developers.

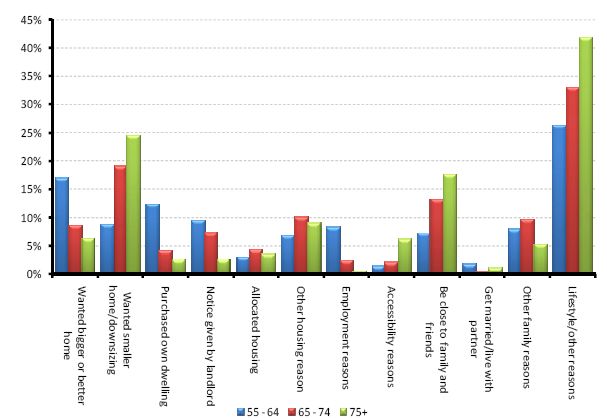

Manningham’s ageing population will further ensure a demand for higher density or

multiple dwelling accommodations as cashed-up retirees look to downsize their housing

type

Figure 21. Reasons for Moving Houses – 55 – 75 Age Brackets

Source: ABS & MacroPlan (2010)

Melbourne’s ageing population more generally is likely to result in a new wave of capital

city re-urbanisation, as the elderly seek to locate close to city facilities, particularly those

related to health services.

Manningham and Doncaster are well positioned to respond to this housing demand,

especially given its proximity to services such as the Box Hill Hospital and its attractive

green suburban hinterland within close proximity to Melbourne CBD. Also, as shown

earlier in this report, the underlying housing values in the LGA are such that the

downsizing of housing types for ageing residents is financially possible.

Prepared for Manningham City Council 27

MacroPlan Australia Pty Ltd

June 2010Doncaster Hill – Development Opportunities and Constraints

Final Draft Report

MacroPlan anticipates that the provision of vertical housing product to suit ageing

residents is a prime candidate for the Doncaster mixed use centre, offering a high quality

residential setting close to city services and modern retail facilities.

Figure 22. Victoria’s Ageing Population

2009 2026 Increase

55 - 74 year olds 986,731 1,401,524 414,793

Source: Projected Resident Population ABS

A strong feature of current metropolitan and local planning policies is the linking of

population densities to urban services, especially transport services. The consolidation

of Melbourne’s population is expected to accommodate almost 50% of Melbourne’s

population growth to 2030.

Improved public transport connections to and from Doncaster – the Red (Mordialloc to

Altona) and Green (Chelsea and Airport West) Orbital SmartBus services commenced in

April 2010. The SmartBus system offers more frequent services and greater reliability.

The Yellow orbital bus service is anticipated to commence operations in early 2011. Also,

the DART (Doncaster Arterial Rapid Transit) service is due to commence in early 2011,

which will increase the number, frequency and times available of bus services running

through Doncaster Hill.

Prepared for Manningham City Council 28

MacroPlan Australia Pty Ltd

June 2010Doncaster Hill – Development Opportunities and Constraints

Final Draft Report

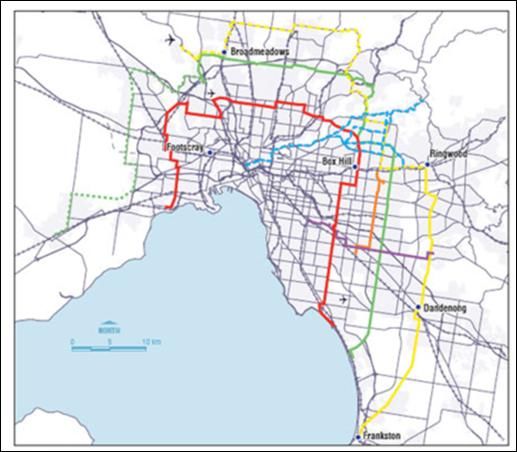

Figure 23. SmartBus Orbital Bus Routes

Source: Metlink, Victoria 2010

Doncaster is also well serviced by the M3 Eastern Freeway, providing good access to the

Melbourne CBD for both motorists and bus-commuters.

Apart from Box Hill, Doncaster is the only other activity centre identified within the

north-east sector of Melbourne. Doncaster is identified as a Major Activity Centre with

Box Hill identified as a Central Activity District under the Melbourne 2030 strategy. These

two centres will vie for development activity within the corridor. There are no other

centres within the corridor capable of meeting long term housing and employment

requirements. Eltham is ageing and Greensborough is not ready. Despite some locational

advantages of Box Hill over Doncaster (mainly its rail connection and its health and

tertiary education facilities) the surrounding catchments are sufficiently wealthy and

amenable to support both activity centres.

MacroPlan anticipates that future Transit Orientated Development (TOD) opportunities

at Doncaster will reinforce its role as the primary activity centre in the LGA and help to

develop the functioning of the centre as both a residential origin and as an employment

destination centre.

Whilst Melbourne’s great competitive strength at present is the ability to produce

housing at relatively affordable prices to other mainland capitals, its ability to continue to

Prepared for Manningham City Council 29

MacroPlan Australia Pty Ltd

June 2010Doncaster Hill – Development Opportunities and Constraints

Final Draft Report

expand the city is and will continue to be tested. Whilst Melbourne’s recent competitive

advantage has been in the delivery of inexpensive, quality suburban development this is

expected to shift over the course of the next decade to an emphasis on quality infill

development.

Both Manningham and Doncaster are well placed to reap of the benefits of this shift in

housing opportunities. Its green suburbs and strong transport linkages make Doncaster a

prime target for the new wave of green office buildings (in response to recent federal

laws requiring the disclosure of office building energy performances).

Doncaster is also well placed to attract the provision of new forms of affordable housing

as the market increasingly responds to government initiatives and incentives to increase

the supply of affordable housing stock. New trends in affordable housing provision for

seniors, modelled on the Dutch Humanitas approach (‘apartments for life’) are also

suited to the Doncaster centre. The ‘apartments for life’ approach is based on providing

a suitable form of accommodation for ageing Australians where the active elderly are

able to integrate with the broader community, both on a business and private level. The

program is gaining market recognition in New South Wales following a recent Court

approval at Bondi. It is being investigated for broader roll-out by Housing NSW. The

initiative is based on an apartment offer above a ground level retail or commercial

component and is therefore well suited to the mixed use rationale of the Doncaster

Strategy.

5.2 New Competitive Position viz a viz Other Locations

Based on MacroPlan’s findings with respect to the current development climate for residential,

commercial and mixed use projects at Doncaster and our understanding of future development

drivers, MacroPlan has identified the following gaps/opportunities for Doncaster:

Apartment Living – Doncaster is a high quality location and has a strong long term

investment potential for this development form, appealing to various household types –

empty nesters, sole persons, couple families without children and the aged (e.g. vertical

retirement). The broad range of market segments that this type of housing is suited to at

Doncaster underlies the importance of meeting the full variety of demand across a

variety of price points. Not all apartment products at Doncaster need to be targeted to

the premium end of the market.

Doncaster is under-employed and offers potential to grow its employment base. Given

its transport linkages and proximity to educational services (e.g. Box Hill TAFE) it is able

to be developed for business people – SME / proximity to airport

Transit Oriented Development opportunities focusing on mixed use developments with a

core residential component

Health-related services building on the ageing population characteristic and the potential

for value-add services to capture this emerging market

A developing night-time economy, catering for expected an increasing local population,

possibly including new ‘club of the future’ formats offering facilities for all ages and

strong community networks.

Prepared for Manningham City Council 30

MacroPlan Australia Pty Ltd

June 2010Doncaster Hill – Development Opportunities and Constraints

Final Draft Report

Importantly, in advancing the future development of the Doncaster Hill centre it is vital that the

broader community be engaged. The Westfield shopping centre is a ‘favourite’ location,

attracting over 7 million visitors per year. Westfield provides a critical mass around which to

develop other retail, office and residential uses. Its anchor role is expected to be shared by the

new Crowne Plaza hotel project. It will be important to consolidate the social networking

opportunities that these developments offer and to ensure that other new developments

address the need to incorporate appropriate ‘people space’. The new Council offices provide an

opportunity for such meeting places.

Public meeting places, either separately provided or incorporated into private developments, are

expected to take on an increased importance as Doncaster develops as a compact living

environment/mixed use centre. The provision of such space will help to dispel any public

misgivings about higher density forms of housing. As the centre matures this need will be

replaced, to some extent, by the commercial provision of meeting spaces – e.g. in the form of on-

street restaurants and cafes etc.

It is also important that Council embrace the current commercially-driven trend of ‘greenifying’

buildings. This should be done in concert with industry and with community expectations,

offering an opportunity to signify Doncaster’s commercial presence in a distinctive manner. This

will help to ensure that a suitable offering of A-Grade commercial stock is made available at

Doncaster, as is presently required by the market (including government uses). The strong desire

for high-rated environmentally performing building stock is partly driven by the onset of new

national regulation which requires the disclosure of energy usage by commercial tenancies.

In MacroPlan’s opinion Doncaster is unique. It is ‘green and suburban’ but closely linked

regionally and to the Melbourne CBD through excellent private and public transport services.

Whilst green areas are not typically associated with higher density built forms, Doncaster’s

location as the primary activity centre at the head of Melbourne’s north-eastern corridor means

that it is well positioned to take advantage of its activity centre status.

Having out-lasted the ill effects of the global financial crisis the strategy for Doncaster is now well

placed to attract market interest. The property fundamentals of Manningham / Doncaster as an

investment location remain strong – it has a growing population, increasing underlying land

values, distinctive locational advantages and a solid critical development mass to build from.

With these credentials MacroPlan believes that Doncaster will develop into the vibrant urban

community envisaged by the Doncaster Hill strategy.

Prepared for Manningham City Council 31

MacroPlan Australia Pty Ltd

June 2010You can also read