Valuer-General's 2018 - Property Market Movement Report

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

State Valuation Service

Valuer-General’s 2018

Property Market Movement Report

Cover photos

Gold Coast City. (Photo courtesy of Shutterstock)

Point Vernon in Hervey Bay, Fraser Coast Regional Council. (Photo courtesy of Shutterstock)

Emerald in Central Highlands Regional Council. (Photo courtesy of Central Highlands Development Corporation)

Cattle (Photo courtesy of S Barlow)

© State of Queensland, 2018.

The Queensland Government supports and encourages the dissemination and exchange of its information.

The copyright in this publication is licensed under a Creative Commons Attribution 3.0 Australia (CC BY) license.

Under this license you are free, without having to seek our permission, to use this publication in accordance with the

license terms.

You must keep intact the copyright notice and attribute the State of Queensland as the source of the publication.

Note: Some content in this publication may have different license terms as indicated.

For more information on this license, visit http://creativecommons.org/licenses/by/3.0/au/deed.en.

CS7909 03/18

Valuer-General’s 2018 Property Market Movement Report ii

Contents

Valuer-General’s foreword 1

Introduction 2

Property market movement 2

Overall market trends 3

Gold Coast 3

Greater South East 4

Wide Bay–Burnett 5

Darling Downs 5

Maranoa 6

Central Queensland 7

North Queensland 8

Western Queensland 9

Rural 10

Figures

Figure 1 Local government areas and the 2018 annual valuation program iv

Figure 2 Property land use by region, 2018 2

Figure 3 Overall percentage movement in total value since the previous annual 11

valuation for the whole state and all local government areas

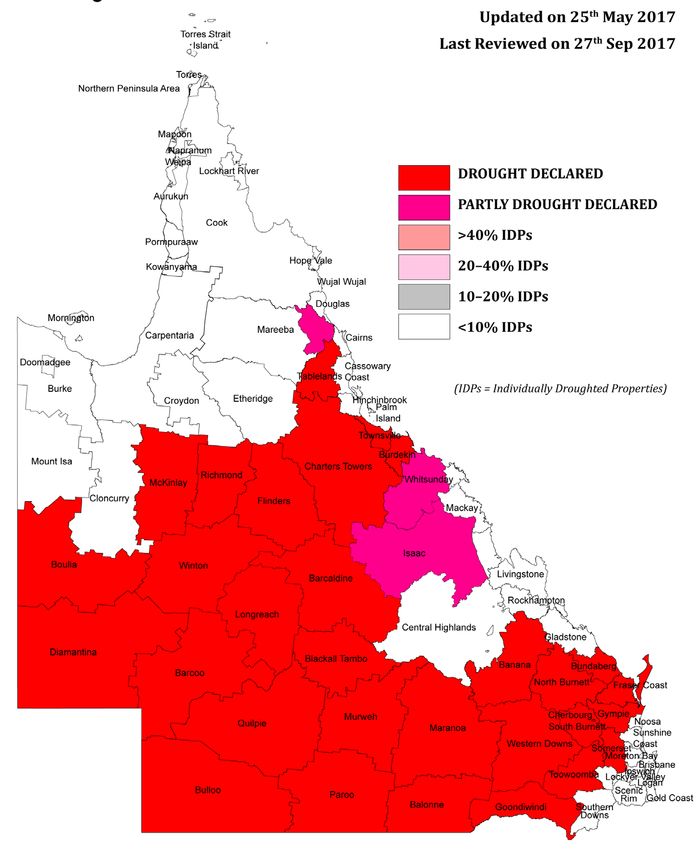

Figure 4 Queensland drought situation as at 27 September 2017 14

Figure 5 Queensland drought situation as at 11 January 2018 15

Tables

Table 1 New median value and percentage movement in median value for 12

residential and rural residential land since the previous annual valuation

in local government areas included in the 2018 annual valuation

Table 2 New total value and percentage movement in total value for commercial, 13

industrial, multi-unit and primary production land since the previous

annual valuation in local government areas included in the 2018

annual valuation

Valuer-General’s 2018 Property Market Movement Report iii

2018 Annual Valuation Program

Inset

TORRES SHIRE

FRASER COAST

REGIONAL

GYMPIE REGIONAL

WEIPA TOWN

NOOSA

SHIRE

SUNSHINE COAST

REGIONAL

SOMERSET

REGIONAL

MORETON BAY

COOK SHIRE REGIONAL

BRISBANE REDLAND

LOCKYER VALLEY CITY

DOUGLAS SHIRE IPSWICH CITY

REGIONAL

CITY LOGAN

CITY

CARPENTARIA MAREEBA SHIRE

SHIRE CAIRNS REGIONAL GOLD

SCENIC RIM COAST

REGIONAL CITY

CASSOWARY COAST

TABLELANDS

BURKE REGIONAL

CROYDON REGIONAL

SHIRE ETHERIDGE

SHIRE

SHIRE HINCHINBROOK SHIRE Included in Program

TOWNSVILLE CITY Not Valued (40)

BURDEKIN SHIRE

CHARTERS Valued (22)

TOWERS WHITSUNDAY

MOUNT ISA

REGIONAL REGIONAL

CITY MCKINLAY RICHMOND

SHIRE SHIRE

FLINDERS MACKAY REGIONAL

SHIRE

CLONCURRY

SHIRE

ISAAC REGIONAL

WINTON SHIRE

BOULIA SHIRE BARCALDINE LIVINGSTONE SHIRE

REGIONAL

LONGREACH ROCKHAMPTON

REGIONAL REGIONAL GLADSTONE

REGIONAL

CENTRAL HIGHLANDS

REGIONAL

DIAMANTINA SHIRE BLACKALL-TAMBO BANANA

BUNDABERG

REGIONAL SHIRE

BARCOO SHIRE REGIONAL

NORTH

BURNETT

REGIONAL

MURWEH SHIRE SOUTH

QUILPIE SHIRE BURNETT

WESTERN REGIONAL Inset

MARANOA REGIONAL DOWNS

REGIONAL

TOOWOOMBA

REGIONAL

BULLOO SHIRE PAROO SHIRE

GOONDIWINDI

SOUTHERN

BALONNE SHIRE REGIONAL

DOWNS

REGIONAL

Figure 1 Local government areas and the 2018 annual valuation program

CS7798 01/18

Valuer-General’s 2018 Property Market Movement Report iv

Valuer-General’s foreword

I am pleased to release this year’s property market ‘Conditions facing regionally important industries,

movement report, ahead of the issue of the 2018 annual including in the resource sector and tourism, have

statutory land valuations on Wednesday, 7 March 2018. continued to strengthen. For example, coal prices and

associated import demand from China have held up, better

Following a statewide market survey and consultation

winter rainfall has eased drought conditions in some areas

with local government and industry groups, 22 local

and tourism numbers continue to improve.’2

government areas have been valued in accordance with the

Land Valuation Act 2010. ‘A global trade recovery, strengthening commodity prices

and increased export volumes boosting Queensland

A market survey report prepared for each local government

export earnings. The value of Queensland goods exports

area details the sales of land in the area since the last

increased $22.3 billion to be $71.4 billion in the year

valuation was made and the probable impact of those

to October 2017, while education and tourism exports

sales on the value of land in an area. In addition, valuers

continue to grow, driven by demand from Asia.’3

also consider factors that impact on the value of the land

such as the state of the economy, commodity prices and Coinciding with the issue of annual valuations on

population trends. 7 March we are introducing a new online search feature

for landowners to find their land value information.

The 22 local government areas receiving new valuations

this year are: Banana, Barcoo, Boulia, Bulloo, The online search displays annual valuation information

Central Highlands, Charters Towers, Diamantina, from the existing online valuation roll, residential market

Douglas, Fraser Coast, Gladstone, Gold Coast, tables and mapping products into one easy-to-use online

Goondiwindi, Hinchinbrook, Isaac, Maranoa, Murweh, search accessible on desktop and mobile devices. The

Noosa, Paroo, Quilpie, Scenic Rim, Sunshine Coast and search tool also displays the movement in the residential

Toowoomba. median values of major residential localities and local

government area as a whole.

The rateable local government areas being valued this year

represent approximately 41 per cent of the total land area Queensland Globe continues to provide landowners with

of Queensland or 29 per cent of the properties on the state access to more detailed valuation information. Our online

valuation roll. resources, Queensland Globe and rural sales map can be

viewed at www.qld.gov.au/landvaluation and can help you

The new valuations will take effect on 30 June 2018 for local

better understand your land valuation and local property

government rating, state land tax and state land rental

market.

purposes (where applicable).

With many Queensland landowners now electing to receive

This report summarises the comprehensive analysis of

their notices electronically, I encourage all landowners

all property markets within the 2018 annual valuation

to have their future valuation notices and other valuation

program for Queensland by a team of regionally-based

information sent to them by email by visiting

registered valuers in the State Valuation Service of the

www.qld.gov.au/landvaluation and changing their contact

Department of Natural Resources, Mines and Energy.

details.

There are continued signs of strength in some areas

I hope you find this year’s property market movement

of Queensland’s property market. Generally, across

report informative.

Queensland there has been increased sales activity in

rural markets. This has resulted in an uplift in land values

within the majority of grazing, horticultural, small crop and

dryland farming industries.

Continued strengthened cattle prices within the beef

industry and continued low interest rates are driving this Neil Bray

confidence, even though the majority of the state remains Valuer-General

drought declared. State Valuation Service

Looking at other economic indicators, Queensland Treasury

advise ‘dwelling investment increased by a further 2.4 per

cent in 2016–17. However, dwelling approvals are now well

below their peak in early 2016, driven by significant falls in

approvals for medium-to-high density dwellings.’1

1 Queensland Budget 2017–18: Mid year fiscal and economic review, p8, Queensland Government

2 ibid. p11

3 ibid. p3

Valuer-General’s 2018 Property Market Movement Report 1

Introduction Property market movement

Two methodologies are used to undertake statutory land The volume of property lodgements recorded with the

valuations in Queensland—site value and unimproved Registrar of Titles decreased over the first half of the 2017–18

value. financial year with an average of 2926 daily lodgements,

down 6 per cent from the previous financial year.

Site value is used to value all non-rural land. It is the

amount for which non-rural land could be expected to Proper ty value changes, both up and down, can be

sell for, at the date of valuation, without any structural attributed to a number of factors:

improvements on the land (e.g. houses, buildings or

• supply and demand within the market place

fences). Site value includes site improvements made to the

land such as earthworks (e.g. levelling, filling, or drainage • consumer confidence

works). Excavations and drainage associated with a

• availability of finance

building are not included in site value.

• local, national and global economic factors

Unimproved value is used to value rural land. It is the

amount for which rural land could be expected to sell for, at • the effects of extreme weather events.

the date of valuation, without physical improvements such

as houses, fences, dams, levelling or earthworks. If your Table 1 (page 12) shows the new median value and

land has been valued on an unimproved basis, it is either percentage movement for residential and rural residential

zoned rural (or equivalent) or designated rural for statutory land in the local government area since the previous

valuation purposes. valuation. Table 2 (page 13) shows new total value and

percentage movement in total value for each land use

category since the last annual valuation was issued.

Single unit residential Figure 3 (page 11) shows the overall percentage movement

Rural residential INSET

Multi-unit residential in total value since the previous valuation for each local

Commercial NAMBOUR

Industrial government area and the whole state.

Primary production

Other

This year’s overall percentage movements in land values

BRISBANE for the 2018 annual valuation are summarised below:

IPSWICH • Nineteen local government areas recorded an overall

increase of between 1.6 per cent (Charters Towers) and

GOLD COAST 41.9 per cent (Maranoa).

NORTH

• Of the nineteen local government areas that increased,

CAIRNS

three increased by 0–5 per cent, four increased 5–10 per

cent and twelve recorded increases of more than 10 per

Local government cent.

areas valued

TOWNSVILLE

DNRME offices

with SVS staff

• Three local government areas recorded an overall

decrease in value between 5.1 per cent (Paroo) and

MACKAY

9.2 per cent (Hinchinbrook).

ROCKHAMPTON

CENTRAL EMERALD

BUNDABERG

NORTH

COAST MARYBOROUGH

ROMA

SEE

TOOWOOMBA

INSET

SOUTH WEST WARWICK

Figure 2 Property land use by region, 2018

Valuer-General’s 2018 Property Market Movement Report 2

Overall market trends Gold Coast

An increase in urban land values has generally occurred in Gold Coast City land values have generally increased

the Gold Coast, Scenic Rim, Toowoomba, Sunshine Coast, from the 2017 annual valuation. While the key contributor

Noosa and Douglas local government areas. In contrast, to the overall increase was in the residential sector,

some regional Queensland local government areas increases have been recorded across most market

experienced generally static to falling property values, in sectors. The market movement is consistent with general

particular those communities whose economies are closely economic indicators such as improving visitor numbers1,

linked to activity in the resources sector, such as Gladstone development and infrastructure spending in the lead up to

and Isaac regional councils. the 2018 Gold Coast Commonwealth Games2.

The market is still being influenced by: Most residential localities recorded minor increases in

value, the stronger increases being in coastal and near

• prevailing economic uncertainty and weak employment

coastal locations such as Mermaid Beach, Burleigh Waters,

growth in some regional centres

Burleigh Heads, Elanora, Currumbin Waters and Tugun.

• declining business investment reflecting the state of the Residential land values in Coombabah and Runaway Bay

resources sector have recorded only slight increases.

• drought – although better winter rainfall in some areas Gold Coast multi-unit development site values increased

saw a recovery in crop production and herd rebuilding. by a minor amount overall depending on location.

The diversity in values is reflective of the demand for

However, these drivers are offset by:

development sites in particular locations and markets.

• strong housing construction and growth in dwelling Southern coastal localities between Mermaid Beach and

investment Coolangatta generally increased by minor to moderate

• continued growth in international tourism and education amounts. Land values in central coastal and broadwater

due to the lower Australian dollar locations, such as in Southport, Surfers Paradise,

Broadbeach and Labrador, generally increased by only

• low borrowing costs and improving rental yields slight amounts, while values in non-coastal, lower density

• investment opportunities being taken up by interstate locations such as in Robina showed slight to minor

and overseas buyers. increases.

The market for Gold Coast commercial property has been

The mining and gas industries continue to influence characterised by improving yields and reducing vacancy

the property market as the gas sector moves from an rates. Commercial land value increased by a minor amount

exploration and construction phase towards a production overall varying by location. The overall movement was

phase, while the mining industry is impacted by volatile influenced by significant increases in southern coastal

resource prices. The fluctuating activity within the sector localities such as Palm Beach and Tugun. Land values in

is still impacting on centres including Gladstone, and the established commercial locations such as Southport

townships within the Isaac and Banana local government and Bundall increased slightly, while emerging locations

areas. such as Robina and Varsity Lakes experienced only minor

Increased confidence within rural markets has led to increases.

moderate increases across the state with some minor to

moderate increases in Greater South East Queensland.

Continued high commodity prices within the beef

industry and continued low interest rates are driving this

confidence, even though the majority of the State remains

drought declared.

Despite a drop in the sugar price and an increase in the

Australian dollar the demand for sugar cane land is still

evident, with the market still generally supporting static to

slightly increased land values.

Gold Coast City. (Photo courtesy of Shutterstock)

1 Travel by Australians: Results of the national visitor survey for year ending September 2017

2 Andrew Potts, Gold Coast Bulletin, June 11 2017

Valuer-General’s 2018 Property Market Movement Report 3

Steady demand for industrial sites across the Gold Coast Residential land values in the towns and villages increased

has resulted in a moderate overall increase in industrial moderately overall with significant increases in Tamborine

land values. Values in all major industrial locations, such Mountain and Canungra. The rural homesite market,

as in Yatala, Molendinar and Burleigh Heads, increased which is the main market driver in the area, also increased

at relatively consistent rates. More significant increases moderately overall. Diverse movement in this market

occurred in the Coomera Marine precinct. Nerang, Carrara reflected local sales evidence and demand resulting in a

and Currumbin industrial values increased by only minor range of increases from relatively minor in Tamborine to

amounts. significant on Tamborine Mountain. Kooralbyn, Canungra,

Peak Crossing, Beaudesert and Aratula rural residential

Rural residential home sites recorded a minor increase

values have increased moderately.

in value overall, with homesite lots closer to denser

residential areas in Helensvale and Nerang reporting The impact of emerging markets and infrastructure

marginally greater increases. resulted in a range of movements for commercial and

industrial land in Bromelton and Aratula that resulted

Gold Coast primary production land values, represented

in a moderate increase for each location. Otherwise the

by the horticulture, cane farming and beef cattle grazing

majority of commercial and industrial land value was

industries have generally remained unchanged.

static.

Greater South East Farming and grazing businesses in the area are a

significant component of the local economy. Farm and

Greater South East Queensland encompasses the valley grazing land values increased by a minor amount overall,

areas west of Greater Brisbane, coastal areas north to with more moderate increase recorded in locations such as

Noosa, and areas inland to Gympie Regional Council. Peak Crossing, Mount Walker and Beechmont.

These local government areas were valued in 2018: Noosa and Sunshine Coast local government areas were

last valued in 2016 and generally most market sectors and

• Scenic Rim Regional Council localities have increased in value since that time.

• Noosa Shire Council The Sunshine Coast region has experienced minor to

• Sunshine Coast Regional Council moderate growth in residential land values driven by a

number of factors including the significant infrastructure

Scenic Rim Regional Council area was last valued in 2015. construction, strong tourism activity and continued

Values in the area have been static until recently when demand for coastal living. Demand typically centres on

demand spreading from surrounding areas has lifted value. mid-priced coastal property as well as the smaller towns

Overall the increase in value was minor, however there has along the North Coast railway line such as Yandina,

been variability with significant increases in some markets Nambour and Landsborough that provide an affordable

and locations. option for buyers. Prestige property values have also

improved with minor increases in beachfront lands as

well as for canal frontage properties in Noosa and

Pelican Waters.

Improving multiple unit building activity and demand is

evident on the Sunshine Coast and has resulted in minor

growth in mulit-unit land values.

Commercial land values are generally steady with some

minor increases across the Sunshine Coast region, however

there is growth in most industrial values underpinned by

the strengthening building and development sector.

Rural residential home site values generally mirrored the

changes in the urban areas, with minor increases recorded

in value in Sunshine Coast and Noosa.

Farming activities such as cattle, small crops and tree

crops are significant enterprises in South East Queensland.

Rural land values in Sunshine Coast have had moderate

increases with market activity reflecting the demand for

hinterland properties.

Sunshine Beach, Noosa Shire Council. (Photo courtesy of

Shutterstock)

Valuer-General’s 2018 Property Market Movement Report 4

Wide Bay–Burnett These local government areas in the region were valued

in 2018:

Wide Bay–Burnett encompasses the region from

• Toowoomba Regional Council

Maryborough north to Bundaberg, and west to Kingaroy

and Monto. Within the region Fraser Coast Regional Council • Goondiwindi Regional Council

was valued in 2018.

The economy of Toowoomba and surrounds continues

Fraser Coast was last valued in 2016 and since that time

to be positive due to a number of completed, ongoing

market conditions have improved in some areas with land

and proposed infrastructure including the Brisbane

values rising in Hervey Bay and some coastal areas.

West Wellcamp Airport, Grand Central shopping centre

Hervey Bay is experiencing some activity in the residential development, the Second Range Crossing, Charlton

sector, with most areas showing a slight to minor rise in Industrial Estate development, the proposed Inland

values predominately in the lower to middle price range. Rail, and the proposed Toowoomba railway precinct and

The older established areas of Maryborough remained parkland development.

static, while values in the hinterland towns and villages

These projects have created confidence within

remained generally unchanged.

Toowoomba City. This is further supported by the effects

Multi-unit land values remained static in Maryborough, of the continued strengthening beef commodity prices,

however values have risen in some areas within Hervey Bay low interest rates and the general demand for rural land

in line with the rising residential land values. across the Darling Downs, resulting in moderate increases

in rural land values.

Industrial, retail and other commercial activity has been

largely subdued across the local government area as a Toowoomba Regional Council was last revalued in 2016.

reflection of local market conditions and as a result, land Since that time there has been minor to moderate growth

values are mostly unchanged. within the residential and rural residential markets

of Toowoomba and surrounding towns. The towns of

Rural residential values remained generally static with

Millmerran, Pittsworth, Oakey and Yarraman are the

demand typically focused on smaller sites around the

exception where the markets remained static, and minor

major centres.

reductions have been made in Clifton, Nobby, Cooyar and

Grazing, cane growing, and small and tree cropping are Greenmount.

significant land uses in the Fraser Coast area, however land

The multi-unit market in Toowoomba has now plateaued,

values were generally static on the back of limited sales

following a sustained period of significant development

evidence in the farming sector.

prior to the 2016 annual valuation.

Darling Downs Generally, the industrial market across Toowoomba

remained static, except for the Charlton Industrial Estate

The Darling Downs is a farming region on the western which has experienced significant increases in value,

slopes of the Great Dividing Range in southern related to the significant infrastructure projects in the

Queensland. The Downs are to the west of the Greater region.

South East and is generally applied to an area comprising There is considerable optimism within the commercial

Southern Downs, Western Downs, Toowoomba and market of Toowoomba City. The market for quality

Goondiwindi regional council local government areas. commercial investment properties has been robust.

Point Vernon in Hervey Bay, Fraser Coast Regional Council. (Photo courtesy of Shutterstock)

Valuer-General’s 2018 Property Market Movement Report 5

There is demand for smaller commercial premises or sites The continued effects of the strengthened beef

suitable for commercial use on a scale suitable for owner commodity prices and low interest rates has seen the

occupiers. There has been an increase in leasing activity general demand for rural land continue from the 2017

within the CBD and fringe for food and entertainment revaluation across the Goondiwindi Regional Council

venues including cafes, restaurants and bars. The local government area, resulting in continued significant

increased retail floor area brought on line by the Grand increases in value.

Central shopping centre redevelopment appears to have

increased overall vacancy levels within this locality.

Demand for office space within the CBD fringe also Maranoa

continues with the conversion of residential dwellings in The Maranoa region is located in south west Queensland

to professional offices. approximately 480 km west of Brisbane and adjoins the

Redevelopment is occurring within the city fringe Darling Downs.

commercial areas with the recently completed Bunnings The town of Roma, is the dominant urban centre and serves

store on the former foundry site at the corner of Ruthven as the region’s primary hub for commerce, education,

and Bridge streets. Inner city development continued with health, transport, government, retail and financial

a number of new developments and restaurants being services.

constructed, coupled with more apartments.

The urban markets throughout Maranoa Regional Council

Sales within this market support an overall minor have stabilised, since the gas industry has moved from

increase in the level of land value, with varying increases infrastructure development to the production phase.

in the fringe commercial and outlying suburban Within the last revaluation of 2017, all urban land values

commercial areas. were significantly reduced within the town of Roma.

Since the last revaluation of Goondiwindi Regional Rural land values have continued to rise significantly,

Council in 2017, the urban components remained following the increases contained in the last revaluation

generally static overall, except for significant increases in 2017. These increases are a result of the continued

in the industrial market and moderate to significant strengthening of the beef commodity prices and low

increases for rural residential properties in Goondiwindi, interest rates. Better quality and more sought after

including the riverfront properties along the lands have reflected larger increases in property values.

McIntyre River.

Aerial view of Toowoomba (Photo courtesy of Dan Proud Photography)

Valuer-General’s 2018 Property Market Movement Report 6Central Queensland The worst affected property markets are the lower-valued

properties in improved residential property markets and

Central Queensland encompasses Rockhampton, the residential rental markets. Reliable evidence of a

Gladstone and Mackay and extends south to Miriam Vale, decline in land values has taken time to filter through,

north to Bowen and west to the Queensland–Northern but there is now sufficient market evidence to indicate a

Territory border. downward movement.

These Central Queensland local government areas were The level of reduction varies from town to town, the extent

valued in the 2018 annual valuation: of reductions relates to a combination of the town’s

reliance on the mining industry, and the date at which the

• Banana Shire Council

town’s associated mines rationalised their workforce.

• Central Highlands Regional Council

Although there was considerable variation between mining

• Gladstone Regional Council towns, the trend throughout the local government areas

• Isaac Regional Council of Gladstone, Isaac and Banana was of moderate value

reductions for most urban land types. Urban lands were

Over the last year, Central Queensland experienced a more stable in Central Highlands Regional Council, after

mixed property market movement. Generally, urban some significant reductions in previous valuation periods.

property markets softened or remained static, and rural While property values have reduced in the mining towns

property markets have remained static or increased. such as Dysart, Moranbah, Clermont, Moura and Theodore,

Since the early 2000’s, regional urban markets have been the residential rental market in most towns has started to

influenced by the region’s resources industry. During 2017, firm at lower and more sustainable levels.

the region started to recover from the previous economic Gladstone property values also reduced in 2017 with small

downturn, caused, in part by the reduced viability of the lot residential and multi-unit values reduced in many areas.

Bowen Basin coal industry. This ongoing easing in the residential market demand

Reductions in coal prices since 2013 saw several in 2017 was mainly due to continued uncertainty in the

uneconomic mines closed during 2015–16, remaining LNG sector and excess supply created during the LNG

operational mines rationalised, and infrastructure infrastructure construction phase. There were some flow-

development projects postponed or abandoned. In mid- on reductions in property values in Gladstone’s industrial

to-late 2016 and throughout 2017, an increase in the and commercial sectors, although not all areas were

spot prices for coal saw stabilising in some markets and impacted.

renewed interest in new coal projects. The grazing markets throughout the region, after several

Support industries were also impacted by conditions in years of softening, have generally seen moderate to

the mining sector. The biggest impact occurring in the significant increases with the continued strengthened

mining and resource-based towns which traditionally cattle prices achieved in 2016–2017. Sales across the

accommodated workers in houses rather than in temporary region continued to trend upward. Grazing land values

accommodation. in all Central Queensland local government areas have

seen minor to moderate increases, except for in Gladstone

The effect on the property market was that demand for Regional Council where values remained unchanged.

urban lands remained soft in 2017 in most urban centres.

However, with continued strong coal prices, we are now

seeing stabilisation in these urban markets.

Emerald, Central Highlands Regional Council. (Photo courtesy of Central Highlands Development Corporation)

Valuer-General’s 2018 Property Market Movement Report 7North Queensland Demand for larger rural residential blocks has generally

flattened, however values have increased moderately for

North Queensland encompasses the Burdekin in the blocks located east of the Mingela Range.

south, and extends north to Cape York and west to the

The primary production sector within the local government

Queensland-Northern Territory border.

area, has been very active since the last annual valuation

These local government areas were valued in the 2018 in 2014. The market for grazing lands remains optimistic

annual valuation: but cautious. The property sales indicate some variability

depending on land quality and location. Whilst the broader

• Charters Towers Regional Council

trend is static to increasing, some of the values for the

• Douglas Shire Council poorer quality lands are still below levels set in the last

• Hinchinbrook Shire Council annual valuation.

Based on the available land sales, moderate increases in

Charters Towers Regional Council is centred on the town value have occurred for the better quality pastoral lands,

of Charters Towers, located 135 kilometres southwest of a minor to moderate reduction in the high-cost breeder

the major regional centre of Townsville. Charters Towers is lands, and a general stabilisation of values elsewhere.

largely a service centre for adjoining pastoral and mining

enterprises. Douglas Shire is located in Far North Queensland about 50

kilometres north of Cairns. The main administrative centre

Traditionally, the real estate market in the town of Charters is the town of Mossman, while the main urban centre is

Towers has been closely related to the state of the mining, Port Douglas.

pastoral and education sectors. The pastoral sector

continues to suffer from the prolonged drought, although The economy has advanced through the economic

confidence appears to be returning on the back of record downturn since 2008 with positive evidence in the tourism

high cattle prices and demand exists for quality land. industry. The property construction market has improved

Over recent years, there has been a reduction in mining steadily with development and renovation of resorts, units

opportunities for the town with slowed activity in both and houses evident in recent times. The local tourism

the Central Queensland coal mines and the local gold industry continues to lead the recovery with improvements

operations, impacting local employment. in the market evident from the 2016 period. This has

continued into 2017 with sound levels of holiday occupancy

These economic drivers have caused a slowing in the levels being maintained. The arable and intensive

volume of sales leading to a slight to minor softening of grazing market is resilient on the back of continued high

land values within the Charters Towers residential market, commodity prices for beef and a strong sugar industry.

and a general stabilisation of values within the immediate

rural residential homesite market. A full review was The residential market in Mossman has improved with

undertaken of all commercial and industrial lands within minor increases in values experienced across the board.

the town, resulting in a variation to values in most cases. The commercial and industrial markets have generally

remained the same.

Slight to moderate increases in values were experienced

in the smaller localities and villages within the local On the back of strong tourism, Port Douglas commercial

government area including in Homestead, Pentland and lands have generally experienced minor increases

Mingela. The exception is the town of Greenvale, where a to land values. The industrial locality of Craiglie has

significant decrease in values has occurred due to a lack of also experienced a slight to minor increase in values.

demand. Residential lands in Port Douglas have experienced minor

increases in values.

Variations to values have existed across localities within

the local government area. Minor increases have been

experienced in Wangetti, Newell and Daintree; minor to

moderate increases in values in Cooya Beach and Craiglie;

whilst there has been slight reduction in values at Wonga

Beach.

The rural homesite market generally has experienced a

minor increase in values north to the Daintree River, with a

stabilisation of values north of the river.

The arable and grazing market has generally experienced

minor to moderate increases in value, which also better

aligns to the levels of value in similar quality adjoining

areas in the Far North region.

Hinchinbrook Shire Council is centred on the sugar cane

community of Ingham and associated localities about 110

Port Douglas, Douglas Shire Counicl (Photo courtesy of

kilometres north of Townsville.

Shutterstock)

Valuer-General’s 2018 Property Market Movement Report 8The volume of sales transactions are generally down on Boulia Shire Council is situated about 300 kilometres

historic levels, with the exception of arable lands which south of the city of Mount Isa, adjacent to the Northern

are trending to be within normal parameters. Communities Territory border. The shire has a geographic area of 61 635

such as Forrest Beach are oversupplied with vacant land sq.kilometres with the town of Boulia as its administrative

stock, which has put a downward pressure on land values. centre.

Residential land values within Ingham have generally Landforms within Boulia Shire are diverse as they

experienced a softening of values with minor to moderate encompass parts of the North West Highlands, Mitchell

decreases. This trend is also occurring in the commercial Grass Downs and Channel Country biogeographical

and industrial markets. regions. Located within the semi-arid to arid zone where

rainfall varies considerably, Boulia Shire has been drought

The lack of demand for land in Forrest Beach has resulted

declared over successive years.

in minor to moderate reductions of land value. There is

limited stock available in the communities of Taylors Beach Despite the drought, a number of primary production

and due to this, land values have generally remained the transactions have occurred leading up to the date of

same. valuation demonstrating a moderate uplift in pastoral

values, generally consistent with an upward movement in

Other villages within the local government area including

values experienced in the south and east.

Toobanna, Trebonne, Abergowrie, Halifax and Cordelia

have generally experienced a minor softening in land Residential land values within the town of Boulia have

values. generally remained stable, while there has been significant

reductions to values in the town of Urandangi, albeit from

Similar to residential lands, there has been limited demand

a low base.

for rural residential lands throughout the local government

area. Minor to moderate reductions in value have generally In Barcoo and Diamantina shire council areas, urban land

been experienced across the board, including the Mount values have been maintained at previous levels. Many

Fox locality. of the smaller towns are feeling the impact of prolonged

drought conditions and subsequent population drift away,

Despite a drop in the sugar price and an increase in the

due to limited employment opportunities. While there has

Australian dollar the demand for sugar cane land is still

been a partial break in seasonal conditions, it may take

evident, with the market still generally supporting static

some time for the smaller towns to recover, as demand for

to slightly increased land values.

labour in the rural sector recovers as graziers re-stock. All

urban areas are generally static within the local authorities

Western Queensland of Bulloo and Quilpie, since the last revaluation in 2014.

For the purposes of this report, the Western Queensland In Paroo and Murweh shires last valued in 2015, the

region encompasses the pastoral zone local government towns of Charleville and Cunnamulla recorded significant

areas west to the Northern Territory border and south to reductions in value, while the towns of Morven and

the South Australia and New South Wales borders. Augathella in Murweh Shire recorded significant increases.

These local government areas were valued in the 2018 The increase in values within the rural property market

annual valuation: within the south west are being driven by the continued

strengthened beef commodity prices and low interest

• Barcoo Shire Council rates. Significant increases in value have occurred within

• Boulia Shire Council the mulga lands due to its affordability. The Warrego flood

plain market is generally static. Carbon credit affected

• Bulloo Shire Council

sales have been occurring within the mulga market. Sales

• Diamantina Shire Council between producers are being sold at generally similar

levels within this market. The impact on land values from

• Murweh Shire Council

the construction of wild dog exclusion fencing has yet to

• Paroo Shire Council be determined in the market place, with regard to those

properties that have fencing installed and those that don’t.

• Quilpie Shire Council

(Photo courtesy of S Barlow)

Valuer-General’s 2018 Property Market Movement Report 9Rural The Australian wool market closed in 2017 in record

territory, with the Eastern Market Indicator closing at

Continued optimism generally surrounded rural property 1760c/kg in December 2017.2 In early 2018 it has continued

markets this year, even though the majority of Queensland to rise to 1822c/kg compared to around 400c/kg less in

remained drought declared. This market confidence 2017,3 resulting in higher prices for re-stockers rebuilding

has generally been driven by high commodity prices their flock.

within the beef and sheep industries and continued low

The effect of continued strengthening of beef commodity

interest rates. This optimism in rural markets is also being

prices is particularly evidenced within the better quality

supported by investment in the construction of exclusion

property markets of Central Queensland, Maranoa and

fences to control wild dogs on many rural properties across

the Darling Downs. There has also been significant

Queensland.

interest within the mulga property market in south-west

Rural land values have continued to grow on the back of Queensland due to its affordability.

landowners’ expectations that conditions in agriculture

Generally, the bulk of market purchases are by existing

have improved and continue to do so. Potential

family business acquiring additional property.

purchasers however still remain cautious, until there is

an improvement in weather conditions. Queensland has Increased rural values are generally occurring throughout

not seen a reasonable season for some time, and many the majority of local authorities being revalued across

primary producers are still waiting for rains to start before Queensland, with sales across Maranoa, Goondiwindi,

re-stocking after the prolonged drought conditions. Sunshine Coast regional councils and Murweh and Douglas

shires generally showing significant increases.

Strong cattle market competition exists between re-

stockers, for limited availability. The Eastern Young Cattle Generally, moderate increases have occurred in the rural

Indicator reflects this situation. 1 October 2014: 365 cents/ areas of Boulia, Diamantina, Barcoo, Banana and Quilpie

kg/cwt (carcase weight), 4 October 2016: 719 cents/kg/ shires, and the regional councils of Isaac and Toowoomba.

cwt, 3 October 2017: 547.84 cents/kg/cwt and 30 January

Minor to slight increases generally occurred in Bulloo,

2018: 534.25 cents/kg/cwt. 1 This trend has been impacted

Paroo, Hinchinbrook shires and the regional councils of

by current weather conditions, and has impacted on

Central Highlands, Scenic Rim and Charters Towers, while

rebuilding efforts. Demand for high quality Australian beef

markets in Gladstone and Fraser Coast regional councils

remains strong.

remained static.

Full reviews of rural valuations are currently underway in

many locations across Queensland to improve uniformity

between valuations. The 2018 annual valuation included

a full review of Murweh Shire Council, the Taroom area

of Banana Shire and the eastern areas of Goondiwindi

Regional Council. The south west local government areas

were also analysed as common markets for the respective

country types. These market based reviews have resulted

in varied changes to valuations being issued.

Rural land purchased by resource companies for the

purpose of mining or other extractive industry are not

used to determine statutory land values of rural land. This

market activity has now slowed due to the state of the

resource sector, and respective markets are now being

influenced by rural landowners.

Despite a drop in the sugar price and an increase in the

Australian dollar, the demand for sugar cane land is still

evident with the market still generally supporting static to

slightly increased land values.

Cattle (Photo courtesy of S Barlow)

1 Source: Meat and Livestock Australia

2 Source Landmark Wool Report

3 Queensland Country Life

Valuer-General’s 2018 Property Market Movement Report 10HINCHINBROOK

-9.2

GLADSTONE

-9.0

PAROO

-5.1

CHARTERS TOWERS

1.6

ISAAC

2.8

BULLOO

3.8

FRASER COAST

5.5

Overall percentage change by local government area

CENTRAL HIGHLANDS

6.4

TOOWOOMBA

8.2

GOLD COAST

8.3

Local government area

2018 annual land valuation

STATEWIDE

8.8

10.4

SUNSHINE COAST

10.8

DOUGLAS

11.3

NOOSA

15.2

BANANA

17.3

SCENIC RIM

17.9

DIAMANTINA

18.1

MURWEH

18.5

BOULIA

19.7

BARCOO

21.8

QUILPIE

25.9

GOONDIWINDI

41.9

MARANOA

50

40

30

20

10

0

-10

-20

% change

Figure 3 Overall percentage movement in total value since the previous annual valuation for the whole state and all local

government areas valued in the 2018 annual valuation.

Valuer-General’s 2018 Property Market Movement Report 11Table 1 New median value and percentage movement in median value for residential and rural residential land since the

previous annual valuation in local government areas valued in the 2018 annual valuation.

Residential Rural residential

Local New Median New Median

government median value median value

area value change value change

($) (%) ($) (%)

Banana 65 000 -1.5 73 000 -7.6

Barcoo 10 000 0.0 21 500 0.0

Boulia 9 000 0.0 23 000 0.0

Bulloo 4 000 0.0 6 400 0.0

Central Highlands 58 000 0.0 124 000 0.0

Charters Towers 49 500 -4.8 110 000 0.0

Diamantina 19 000 0.0 50 000 0.0

Douglas 140 000 12.0 152 500 2.4

Fraser Coast 129 000 10.3 117 000 2.6

Gladstone 95 000 -15.9 118 000 -6.4

Gold Coast 345 000 9.5 390 000 5.4

Goondiwindi 75 000 0.0 130 000 12.1

Hinchinbrook 56 000 -22.2 95 000 -12.0

Isaac 37 000 -46.4 74 000 -17.8

Maranoa 58 000 0.0 158 750 5.8

Murweh 12 000 -57.9 28 000 -58.2

Noosa 270 000 13.7 202 500 8.0

Paroo 4 700 -52.5 16 000 -60.0

Quilpie 24 000 0.0 31 000 0.0

Scenic Rim 167 500 14.0 237 500 13.1

Sunshine Coast 247 500 8.8 275 000 10.0

Toowoomba 185 000 7.3 197 500 5.3

Valuer-General’s 2018 Property Market Movement Report 12Multi-unit Commercial Industrial Primary production

New Total New Total New Total New Total

Local government area total value total value total value total value

value change value change value change value change

($) (%) ($) (%) ($) (%) ($) (%)

Banana 3 712 000 -1.0 16 325 400 -11.3 37 749 834 -1.2 1 357 062 890 22.0

Barcoo 106 500 0.0 81 000 0.0 63 281 500 20.2

Boulia 186 610 -5.8 172 280 0.0 69 752 100 19.3

Bulloo 44 600 0.0 215 800 0.0 44 981 500 2.7

Central Highlands 24 651 100 -1.1 77 493 600 0.1 76 805 770 0.0 1 796 759 040 9.5

Charters Towers 2 388 500 -3.7 18 353 700 5.8 15 300 440 4.2 443 541 100 4.7

Diamantina 540 000 0.0 459 850 0.0 43 387 000 19.8

Douglas 272 360 000 8.6 161 691 500 7.2 39 500 200 6.9 101 681 100 47.0

Fraser Coast 276 281 000 5.2 397 063 200 0.5 162 024 800 0.5 230 532 000 0.0

Gladstone 130 164 000 -12.3 206 098 400 -5.8 266 744 050 -9.3 230 757 520 0.0

Gold Coast 17 175 645 400 6.6 4 095 568 700 8.5 3 692 649 500 15.4 125 046 800 0.2

Goondiwindi 6 457 000 19.9 39 822 250 2.9 55 772 500 13.5 778 768 900 38.0

Hinchinbrook 6 602 000 -18.9 39 127 000 -21.4 14 991 000 -10.2 318 293 600 4.8

Isaac 11 406 000 -27.3 25 917 000 -20.8 24 189 400 -23.8 1 814 735 610 18.8

Maranoa 5 765 400 -0.3 70 680 600 0.6 91 992 150 0.1 1 853 246 070 59.6

Murweh 4 635 800 -57.0 1 815 700 -56.7 257 778 290 52.9

Noosa 1 426 416 500 4.5 232 195 000 2.7 139 566 000 9.5 61 565 500 20.1

Paroo 1 085 800 -58.2 410 000 -59.7 93 385 200 3.5

Quilpie 770 450 0.0 1 198 800 0.0 54 704 800 26.3

Scenic Rim 53 894 500 13.0 163 732 500 1.1 80 284 800 4.7 1 121 213 320 11.0

since the previous annual valuation in local government areas valued in the 2018 annual valuation.

Sunshine Coast 3 418 594 200 12.8 1 710 894 400 5.6 759 604 500 7.2 382 303 100 30.4

Toowoomba 528 746 500 0.3 845 398 980 7.5 775 030 132 5.3 2 265 847 230 23.3

Valuer-General’s 2018 Property Market Movement Report

13

Table 2 New total value and percentage movement in total value for commercial, industrial, multi-unit and primary production landQueensland drought situation as at 27 September 2017

Figure 4: Queensland drought situation as at 27 September 2017 Source: www.longpaddock.qld.gov.au

Valuer-General’s 2018 Property Market Movement Report 14Queensland drought situation as at 11 January 2018

Figure 5: Queensland drought situation as at 11 January 2018 Source: www.longpaddock.qld.gov.au

Valuer-General’s 2018 Property Market Movement Report 15You can also read