ECONOMIC MISSION OF CT. VAUD IN TURKEY 2015 - Mehmet Yildirimli, Head of SBH Turkey, 27th October 2014

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Mehmet Yildirimli, Head of SBH Turkey, 27th October 2014 ECONOMIC MISSION OF CT. VAUD IN TURKEY 2015

Swiss Business Hub Turkey Agenda / Content • Turkey at Glance o Doing business in Turkey • Bilateral Trade & Opportunities • Q&A 2

TURKEY AT GLANCE

Swiss Business Hub Turkey

CH - TR

Indicators (2013) Switzerland Turkey Comparison

Surface 41‘285km2 783’562km2 1 x 20

Population 8.2 Mio 76.7 Mio 1 x 9.5

Direct Investment

Population TR in CH 100‘000 3‘700 30 x 1

/ CH in TR

GDP per capita 45‘300 USD 10‘782USD 4x1 FDI from TR to 0.55 bn

CH CHF

GDP 623 bn USD 822 bn USD 1 x 1.3

GDP growth ~1 % ~4.4 % 1x4

Unemployment 3% 9% 1 x 3.5 FDI from CH to 2.6 bn

TR CHF

Import Export

CH with World ~195 bln USD ~220 bln USD

TR with World ~251 bln USD ~153 bln USD

CH with TR ~1.2 bln CHF ~1.96 bln CHF

Source: CIA world factbook 2014

Swiss Business Hub Turkey

Management Summary

• 2013 was a turbulent year for Turkey unexpected protests

US-FED’s signal for a possible cut down

on liquidity

17th December; graft allegation probe

against some ministers and their sons

• Despite the unrest of protests as well as the other happenings in Q4 2013,

Turkey’s large and dynamic domestic market (~80 Mio people and 50% young

population) is still a very significant factor diferentiating the country from its

neighbour countries, mainly in Central and Eastern Europe.

• Turkey’s economic performance in 2013 was bettter in certain terms compared

to the previous year despite months of polical turmoil in the country.

• Turkey’s economy will grow slowly than expected because of higher borrowing

costs, instable exchange rates and a sharp fall in private consumption and the

«instable» political situation ~4-4.5%

6

Swiss Business Hub Turkey

• 17th largest economy in the world and 6th when compared to the EU Countries

in 2013 (IMF)

• Turkey is the 6th most visited holiday destination in the world (2013) after F, US,

ES, Ch, I 39.2Mio visitor in 2013

• Turkey is the 8th largest steel producer in the world and 2nd compared with

the EU countries (worldsteel 2013)

• Turkey is the 17th largest automotive producer in the world (OICA 2013)

• The largest youth population when compared to the EU countries

• 32,6 million broadband internet subscribers (2013)

• 57 million credit card users (2013)

• 69.6 million GSM users (2013)

7

Swiss Business Hub Turkey

• The 61th government program foresees that Turkey will be among the 10

biggest global economies in 2023. It aims to reach 500 billion USD in

exports volume with an average of 12% increase in exports annually. GDP 2

trillion USD, GDP per Capita 25K USD, 5-6% unemployment

• Turkey’s tomorrow is to invest strongly into research & development, into

infrastructure, into the country positioning and into the way of working.

• i.e brand

new old

Not to forget is that Turkey has not only access to one market but

multiple markets 1,6 billion people; $26 trillion GDP; $8 trillion trade

8

Swiss Business Hub Turkey

Macroeconomic Indicators & Trends

Overall Economic

Forecast 2015

OP.

9

DOING BUSINESS IN TURKEY

Swiss Business Hub Turkey

Mustafa Kemal Atatürk – Father of the Turks

• Military Commander 1st WW

• Destruction Greek forces in Asia Minor (1919–1922)

• 1923 founding of Republic of Turkey (Treaty of

Lausanne peace treaty signed in Lausanne, ended

the state of war with allied British Empire, French Rpublic, Kingdom of

Italy, Empire of Japan, Kingdom of Greece…)

• First reforms based on western ideologies (latine

alphabet, metrical system, gregorian calendar,

surnames, separation of powers of the state

legislative power executive power and judicial

power, equality of gender, women voting rights, etc.)

• Introduction of the civil code based on the Swiss

civil code)

Secular, modern nation stateSwiss Business Hub Turkey

Characteristics; Pride and Nationalism

Proud of

history

culture

country

modernity (westernization)

family

Turks see themselves as Europeans!Swiss Business Hub Turkey

Turkey – two faces

Cosmopolite and western oriented Cities i.e.

Ankara, Istanbul, Izmir

Rural areaSwiss Business Hub Turkey Historicals, good to know about Turkey Two of the Seven Wonders of the World are located in Turkey THE MAUSOLEUM AT HALICARNASSUS TEMPLE OF ARTEMIS (TOMB OF MAUSOLUS) Near Izmir In today’s Bodrum 14

Swiss Business Hub Turkey JULIUS CAESAR – VENI VIDI VICI CLEOPATRA Julius Caesar spoke these famous words after Marcus Antonius gave Cleopatra one part of the defeating Pharnaces II, the King of Pontus (at the southwestern coast of Turkey as a wedding gift. northeastern province of Anatolia on the southern coast of the Back Sea) in 47 AD. 15

Swiss Business Hub Turkey

Santa Claus was born in Demre, a

settlement at the Mediterranean coast

of Turkey.

The city of Troy – the district of the

ancient Trojan wars – lies in the west of

Turkey.

16Swiss Business Hub Turkey Good to know about Turkey Nutrition 70 % of the worldwide hazelnut production comes Coffee was brought to Europe by the Turkish from Turkey Turkey is also the largest producer and exporter of apricots, cherries and dried fruit Turkey is the second largest pasta producer in Europe behind Italy 17

Swiss Business Hub Turkey Good to know about Turkey Other TURKISH AIRLINES INTERNET AUTOMOTIVE And hundreds of other Turkish Airlines is the Turkey is ranked 7th in PRODUCTION reasons to invest in fourth largest Airline in Europe (27th worldwide) Ranked 17th worldwide Turkey… Europe and it won the in terms of Internet and 7th in Europe «Best European Airline usage Award» in 2011 18

Swiss Business Hub Turkey Family “Ich traue keinem Manager, Rechtsanwalt etc. – ich traue nur meiner Familie.” (Hakan Yakin, NZZ, 2.9.2005)

Swiss Business Hub Turkey

Trust

To show respect & interest for country, people,

culture, rules

To prove reliability

To be a member of the family

To have personal contact / regularly visits TR-

CH

To know some Turkish words

To do dinners/lunches

To congratulate to celebrations (Bayram)Swiss Business Hub Turkey

Loosing Face

“loosing face”

No direct critics

Not being pushy

Indirect communication

Challenges: Evaluation of partner’s know

how

To ask in a diplomatic waySwiss Business Hub Turkey

Hierarchy

Hierarchy is important (age and sex not imp., except in

the family)

Important is protocol: sittings, rules, etc.

Top-down system (very westernized and modern

comp. bottom-up

Challenge: “Decision Makers” to identify and meet

SBH Turkey can operate as “Door opener”Swiss Business Hub Turkey

First meeting

Business casual /business dress code

Start with “Merhaba” (good day) oder “Nasilsiniz” (how are you?) / Small

Talk (family, football, weather…)

Attention: don’t start with politics!

Tea or Coffee

Slow negotiations don’t push

Trust and Friendship takes time

Presents

You Naming by man: -bey

Naming by woman -hanImSwiss Business Hub Turkey

Communication / Negotiation

Indirect communciation (oral/written)

Dynamic and intensive

Challenging partners to negotiate

Very price sensitive

Everything can happen: between anger and

hugging

To be patient, flexible, strategic and also hardSwiss Business Hub Turkey Ease of Doing Business Ranking Source: Doing Business , The Worldbank 2013

BILATERAL TRADE &OPPORTUNITIES

Swiss Business Hub Turkey

CH-TR Bilateral Relations; Legal Framework of the Economic Relations

Year Agreement

1930 Trade Agreement

1942 Agreement on the Organization of Commercial Exchange and Payments

1988 Agreement on the Reciprocal Promotion and Protection of Investment

1991 Free Trade Agreement EFTA-TURKEY

2001 Memorandum of Understanding (MoU) of Joint Economic Commission

2002 MoU on High Level Commercial and Economical Consultation

2009 MoU in Energy Cooperation

2011 EFTA Protocol E (Mutual Recognition of Conformity Assessment of Products)

2013 Avoidance of Double Taxation Agreement

27Swiss Business Hub Turkey

3.1 Export Figures & Market Potential

Export 2013 2014 (estimate) Outlook Industry Sectors

Total Imports from CH

2015

1,992 2,151

Bn CHF Product of chemicals,

pharmaceuticals

Machines, appliances,

Most Important Industry

% Mio. CHF

electronics

Sectors (2013)

Prod. Of chemicals, Precision instruments

pharmaceuticals or allied 44.0 0,876

industries Metal

Machines, appliances,

28.0 0,557

electronics Luxury goods

OP.

Precision instruments,

clocks, watches and

jewelry

13.0 0,259 Med-bio Tech

Metals 4.0 0,08 Product of chemicals,

pharmaceuticals

28Swiss Business Hub Turkey

Bilateral Trade by Sectors

Swiss Exports to Turkey by Industrial Sector 2013

4 Products of chemicals, pharmaceuticals or allied industries

11

13 Machines, appliances, electronics

44

Precision instruments, clocks and watches and jewellery

28 Metals

Various

Swiss Imports from Turkey by Industrial Sector 2013

Textiles, clothing, shoes

22.5

Vehicles 39

11

Forestry and agricultural products, fisheries

12,5

Metals 15

Various

Source: Fed. Customs AdministrationSwiss Business Hub Turkey

Trends & Opportunities

CONSTRUCTION

LIFE SCIENCE

CLEANTECH

INFRASTRUCTURESwiss Business Hub Turkey Trends & Opportunities

Swiss Business Hub Turkey

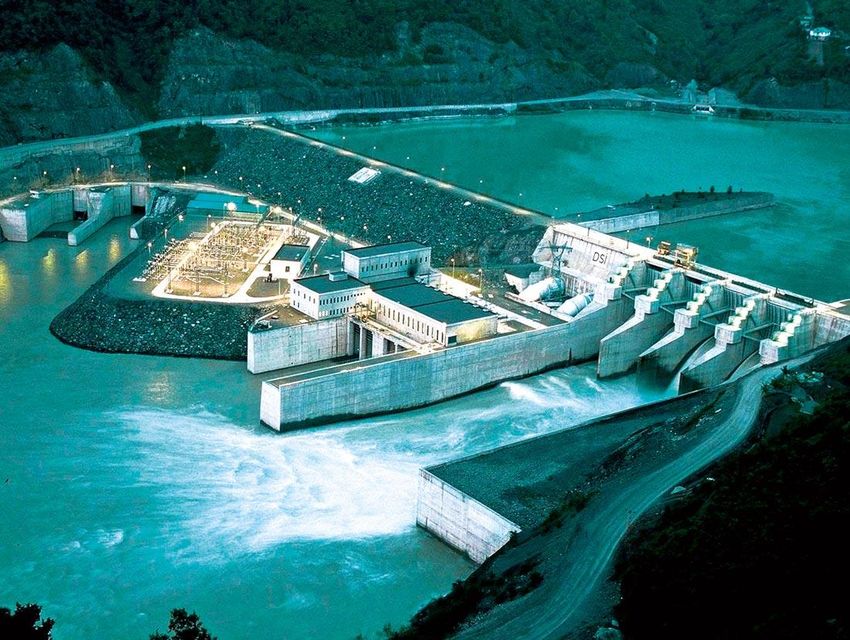

ENERGY

Strategic location for energy terminal and corridor

In the last decade energy demand and electric consumption have increased by 4% and 8% per year

Turkey needs to make over $200 billion investment in electricity production in the next twenty years

Privatization of energy generation assets and electricity distribution networks

The framework agreement (2009) b/w Switzerland and Turkey aims to encourage business and

technical cooperation in various fields (e.g. Renewable, energy efficiency, nuclear safety etc.)

Increasing/developing of renewable Energy resources

wind-, solar- and geothermal power plants

Improving of Energy Efficiency

Building Nuclear CapacitySwiss Business Hub Turkey ENVIRONMENT Total Investment required (2007-2023): € 59 billion Waste and waste management; waste water and water management

Swiss Business Hub Turkey

TRANSPORTATION

Railways: Turkey plans to increase 11’000 km current network of rails to 25’000 km within ten years;

5’500 light vehicles (metro) is projected in twenty years

Highways: construction of highways/bridges connecting major economic zones ($10 billion)

Airports: rehabilitation and/or expansion of existing airports and construction of new airports (150mio

passengers, consturction cost 10 bn EUR)

Privatization of some existing networks

General: 2013-23 > 350 bn USD will be invested

Intensity of highway, motorway and railwaySwiss Business Hub Turkey

Projects of the century

TURKEY’S BIGGEST TECHNOPARK THIRD BOSPORUS BRIDGE

On the Asian side of Istanbul At the northern end of the Bosporus

750 000 m² 1 875 m

Costs: USD 4 bn Costs: USD 2 bn

- IZMIT GULF TRANSIT

- ISTANBUL-IZMIR HIGHWAY

- HIGH SPEED TRAIN TRHOUGH ANKARA-

THE WORLD’S BIGGEST AIRPORT BURSA-ISTANBUL

Capacity for 150 Mio passengers per year - ……

Area of 90 mio m2

Costs: EUR 10 bnSwiss Business Hub Turkey HEALTH The Turkish health-care system has been undergoing a reform process. The government aims to increase the quality, efficiency and accessibility More than 40 new state hospitals are planned to open in 29 provinces ($750 million) Over 100 new private hospitals in addition to existing 500 private hospitals to be opened The size of the pharma sector is expected to reach more than $15 billion in 2014

Swiss Business Hub Turkey INFORMATION AND COMMUNICATION TECHNOLOGIES (ICT) Fastest growing IT companies in the region are from Turkey, 27 of the 500 fastest growing tech companies in EMEA are Turkish Cell phone penetration rate is over 90%. Internet penetration is 45% (more than doubled in last 5 years) Market size is around >$30 billion (2013) and huge potential for further growth E-commerce is expected to exceed $13 billion in 2014 (16 times bigger compared with 2005) Increasing budget allocation by government for public IT investments

Swiss Business Hub Turkey RETAIL BUSINESS Market size is expected to exceed $300 billion in 2013 Food, home appliances, textile, technology products and luxury products are the major categories

Swiss Business Hub Turkey AGRIBUSINESS Turkey has the capacity to be the main food hub in the region Organic farming: increasing with 2-digits growth rate

Swiss Business Hub Turkey

Foreign direct investments, from and to Switzerland

Notable Swiss firms investing in Turkey: Notable Turkish firms investing in Switzerland:

OP.

ABB, Adecco, Blaser Swisslaube, Bühler AG, Credit Suisse, Glencore, Kofisa SA (Koc Group), Dilko SA (TR Peugeot

Mövenpick Hotel, Nestlé, Glencore, Novartis Oerlikon, Phonak, Roche, Supplier), Baytur SA (Cukurova Group), Kibar Inl.

Sandoz, Schinder, Sika, Swiss, Syngenta, UBS, Viatrans, Barry (Kibar Group), City Trade SA (Altinbas Group), Europe

Callebaut, Ammann-Technomak, Pfiffner, BR Scneider-Ammann, Credit Bank (FIBA), Is Bank Gmbh, Bank Commerce

Swatch Group, Swissotel Deplacement (Yapi Kredi), Rixos Hotel, Dogus

Holding, various advocate offices

40Swiss Business Hub Turkey

Sum up

SWOT: Year Analysis 2014

Strengths Weaknesses

• Large, dynamic market • Current account deficit continues to be a source of

• It has an ideal strategic geographical location for vulnerability

trading • Weakness and relapse in education

• Strengthened investor protections through a new • Strong dependence on imports of energy sources

commercial code • Signs of anti-democratic statecraft

• Steady regulatory improvements are making it • Lumbering bureaucracy

easier to set up and run a business in Turkey • Increase on Minimum Capital for new businesses

• Reduced time for dealing with construction

permits

Opportunities Threats

• Growing suburbs & sub-regions • Education system is not delivering enough of the

• Young and skilled labor force Growth of know- skills needed by an innovative and dynamic

how (returnees) and R&D (government) entrepreneurial business sector

• Potential role as an energy –gas hub • Threat of energy shortage

OP.

•

•

•

Manufacturing (hub) of high quality products

Strategically located between key markets in

Europe, the Middle East, Russia and Central Asia

Growing interest in renewable energy and energy

•

•

•

Currency risk

High inflation

Instability at the borders such as the disturbance

caused by ISIL and PKK

efficiency • Excessive increase in immigration from neighbour

• There are many industrial locations and resources countries

untouched

41Partner

VARIOUS LOCAL EXPERTS AND

OTHER CHAMBERS AND INSTITUTIONS

42Contact

MEHMET YILDIRIMLI ALBERTO SILINI

Director of Swiss Business Hub Turkey Head of Consulting, Responsible for Turkey

c/o Consulate General of Switzerland Switzerland Global Enterprise

Esentepe Mah. Büyükdere Cad. 173 Stampfenbachstrasse 85

1. Levent Plaza A Blok Kat:3 8006 Zürich

TR-34394 Levent - Sisli - Istanbul

Tel. +41 (44) 365 53 15

Tel. +90 (0) 212 / 283 12 82 (ext. 234) Mobile +41 (79) 239 69 03

Mobile +90 (0) 530 230 12 20

Fax. +90 (0) 212 / 283 12 98 E-Mail alberto.silini@s-ge.com

Web www.s-ge.com

E-mail mehmet.yildirimli@eda.admin.ch

Web www.eda.admin.ch/istanbul

43QUESTIONS?

MERCI!

TEŞEKKÜRLER!

44Swiss Business Hub Turkey BACK UP SLIDES 45 30.10.2014 | © SWITZERLAND GLOBAL ENTERPRISE

CT. VAUD – TURKEY DRAFT PROGRAM 2015

Program Istanbul & Ankara May 4-9, 2015

Swiss Business Hub Turkey

TURKEY SWITZERLAND

Facilitating / change of laws Science, technology, innovations

Economic strength & growing young Skilled and multilingual staff

population High education system (high number of

Middle class, energy, construction, waste Nobel Prize per capita)

management, railway, Medtech, etc. World-leading research environment (HQ

Growing suburbs & sub-regions of multinational companies)

Growth of know-how (returnees) and R&D Ideal destination for administration and

(government) distribution, tourism and financial services

Geopolitical location

BOTH COUNTRIES NOT IN EU BUT KEY PLAYERS IN THE WORLD

48Swiss Business Hub Turkey OTHER Upcoming public tenders is anticipated to reach $20 billion level (Ministry of Industry) Financing is provided by the state, the private sector, the EU and international agencies The World Bank will be providing $6.5 billion for Turkey’s investment plans in energy, health, public services and education. EBRD’s portfolio built up to more than 2 billion Euros since 2009 in about 50 operations ranging from agribusiness to renewable energy projects. The Bank’s investments will continue to focus on renewable energy, promoting of mid-size companies in underdeveloped regions and supporting privatization efforts The new incentive scheme and the new Commercial Code provide better investment environment Swiss companies can take part through their subsidiaries, local agents or consortium partners (local and EU companies) by supplying goods (systems, sub-systems, parts and components) providing engineering and consultation services 49

Swiss Business Hub Turkey

Trends & Opportunities

Automotive Target to produce over 2 million vehicles within 5 years

Transportation Highway capacity planned to be tripled up until 2023 with 12 different

project

Real Estate Third most attractive real estate investment destination in 2012

(AFIRE); Istanbul is the most attractive real estate investment market

in 2012 (PwC, ULI); more than $27 billion FDI over past decade.

Finance Resilient to the global financial crisis with strong regulatory and

supervisory framework, the most attractive sector with $39 billion FDI

in the past decade; more opportunities with Istanbul Finance Center

Energy Strategic location for energy terminal and corridor; rapidly growing

demand: over $100 billion investment is needed to meet the demand

till 2023; privatization and diversification opportunities.

ICT Fastest growing IT companies in the region are from Turkey, 27 of the

500 fastest growing tech companies in EMEA are Turkish. 2011 winner:

Logic Bilişim (5-year revenue growth of 28,617% with 412% CAGR).MARKTEINTRITTS- STRATEGIEN TÜRKEI

Markteintrittsstrategien TÜRKEI

Türkei – und man denkt an… 53 Corporate Design PowerPoint | 30.10.2014 | © SWITZERLAND GLOBAL ENTERPRISE

Markteintrittsstrategien

1. Markteintritt ohne Direktinvestitionen

a) Direktvertrieb

b) Zusammenarbeit mit einer Agentur oder einem Importeur

c) Vertrieb über einen Handelsvertreter

d) Gründung eines Verbindungbüros

2. Markteintritt mit Direktinvestitionen

a) Gründung einer Niederlassung

b) Neugründung eines Unternehmens

c) Beteiligung an einer Gesellschaft

d) Übernahme eines Unternehmens

e) Joint Venture

Art des Markteintritts hängt von zahlreichen Faktoren ab

(Wettbewerbssituation, Investitions- und Risikobereitschaft, Know-how etc.)

54 Corporate Design PowerPoint | 30.10.2014 | © SWITZERLAND GLOBAL ENTERPRISEGrundlagen zur Entwicklung einer Markteintrittsstrategie

- Rahmenbedingungen müssen bekannt sein (oft Fehleinschätzungen)

- Marktgewohnheiten

- Rechtliche Rahmenbedingungen

- Marktzutritt

- Zölle

- Zertifizierungen

- Marktumfeld

- Internationale und lokale Wettbewerber

- Stellung und Strategien der Wettbewerber

- Marktpotenzial / Entwicklung

- Regionale Verteilung der Kunden

- Vertriebsstrukturen

- Preise

- Markenimage

55 Corporate Design PowerPoint | 30.10.2014 | © SWITZERLAND GLOBAL ENTERPRISEMarkteintritt OHNE Direktinvestitionen

Direktvertrieb

Direktvertrieb aus dem Ausland ohne lokalen Partner nur wenn:

- Anzahl Kunden nicht gross ist

- Kunden grössere Unternehmungen sind, welche gewöhnt sind, direkt aus

dem Ausland zu importieren

- Produkt erklärungsbedürftig und kundenspezifisch ist

- Keine Vertretung das nötige Know-how hat

Vorteile Direktvertrieb Nachteile Direktvertrieb

Direkter Kundenkontakt Bei grösserer Anzahl Kunden sehr

aufwändig

Bessere Marge / weniger Kleinere türkische Unternehmungen

Preisaufschläge für Provisionen beschaffen lieber lokal (einfacher,

Vertrauen etc.)

56 Corporate Design PowerPoint | 30.10.2014 | © SWITZERLAND GLOBAL ENTERPRISEVertrieb über Agenten oder Importeur Agent: - Auch Handelsvertreter genannt (türk. acente) - Vermittler von Aufträgen - Vergütung durch Provisionierung - Rechnungsstellung und Lieferung erfolgen direkt aus dem Ausland in die Türkei - Können natürliche oder juristische Personen sein - Handelsvertreter bedürfen einer entsprechenden offiziellen Urkunde Importeure: - Kaufen und verkaufen Produkt auf eigene Rechnung an türkische Kunden - Preisaufschlag (Marge) durch Importeur Generell: - Mischformen sind möglich (Grosskunden durch Agenten / Kleine durch Importeure) - Unter 1 Mio. Umsatz lohnt sich i.d.R. keine eigene Vertriebsstruktur 57 Corporate Design PowerPoint | 30.10.2014 | © SWITZERLAND GLOBAL ENTERPRISE

Vertrieb über Agenten oder Importeur (EXKURS) Die Wahl des Vertriebspartners ist ausschlaggebend für den Geschäftserfolg! Viele KMU unterschätzen Risiken Vielmals werden an Messen Kontakte geknüpft und sofort Vertriebspartnerschaften eingegangen «Wir verfügen über wertvolle Kontakte, sind in der Branche bestens bekannt, beliefern sowohl General Electric und die türkische Regierung! Zudem haben wir persönliche Kontakte bis auf Regierungsebene!» sind nicht selten gehörte Aussagen von potenziellen Partnern. V O R S I C H T ! Lassen Sie die Partner durch S-GE verifizieren oder fragen Sie S-GE für eine qualifizierte Vertriebspartnersuche 58 Corporate Design PowerPoint | 30.10.2014 | © SWITZERLAND GLOBAL ENTERPRISE

Qualifizierte Suche von Vertriebspartnern durch S-GE

• Erstellung Partnerprofil mit CH-Firma

• Suche durch Swiss Business Hub (Datenbanken, eigene Quellen, Verbände, Netzwerk etc.)

Longlist • Check der Longlist und Verifizierung Ansprechpartner

• Selektion der zu kontaktierenden Firmen (Kunde / S-GE)

• Aufbereitung personalisiertes Mailing durch SBH in lokaler Sprache

Shortlist

• Versand Mailing / telefonisches Follow-up durch lokalen Partner

• Einholen von Interessensbekundungen

Search • Interviews

• Validierung der Interessensbekundungen

• Überprüfung der Kandidaten nach festgelegten Kriterien

Qualifizierung • Präsentation Findings an Schweizer KMU

59 Corporate Design PowerPoint | 30.10.2014 | © SWITZERLAND GLOBAL ENTERPRISEQualifizierte Suche von Vertriebspartnern durch S-GE

• Wahl der potenziellen Kandidaten

Selection

• Organisation von Meetings (vor Ort) mit Schweizer KMU

• Begleitung durch lokalen Mitarbeiter des Swiss Business

Fact Finding Hubs an Meetings

• Entscheid: Vertriebspartner / Strategie und Identifizierung

von allfälligen weiteren Massnahmen

ENTSCHEID

60 Corporate Design PowerPoint | 30.10.2014 | © SWITZERLAND GLOBAL ENTERPRISEProblemfelder bei der Auswahl und Zusammenarbeit Exklusivität: - Wenn Produkte in mehreren Zielsegmenten / -branchen abgesetzt werden, ist Vorsicht geboten - Mindestabsatzmengen festlegen - Verschiedene Partner für verschiedene Branchen ist OK Portfolio des Vertriebspartners: «Traditionell» ist kein Qualitätsmerkmal Auf Langfristigkeit setzen Filterung von Informationen vermeiden Sich mit Mentalität auseinander setzen: «Ich habe alles meinem Partner erklärt, jetzt möchte ich sehen, wie selbständig er daraus was macht» – NO GO! 61 Corporate Design PowerPoint | 30.10.2014 | © SWITZERLAND GLOBAL ENTERPRISE

Vor- und Nachteile bei der Zusammenarbeit mit DISTRIBUTOREN

Vorteile Nachteile

Günstige Kostensituation Oft kurzfristiges Denken der

Partner

Schneller Marktzugang Schwierige Steuerung

Geringe Fixkosten Keine direkte Bestimmung der

Strategie

Nutzung vorhandener Ressourcen Gefilterte Marktinformationen

Weniger Vertrauen bei Kunden im

Vergleich zur eigenen

Repräsentanz

62 Corporate Design PowerPoint | 30.10.2014 | © SWITZERLAND GLOBAL ENTERPRISEVertrieb über ein VERBINDUNGSBÜRO / REPRÄSENTANZ Allgemein: - Stellt keine türkische juristische Person dar - das Verbindungsbüro darf selbst keine Rechnungen stellen, bzw. Umsatz generieren (reines Ausgabenbüro) - definitionsgemäss ein Kontaktbüro zur Marketing- oder Einkaufsunterstützung - die Kosten werden von der Muttergesellschaft im Ausland beglichen - das Verbindungsbüro muss daher in der Türkei keine vollständige Buchhaltung führen, nur begrenzt Steuererklärungen abgeben und keine Körperschaftssteuer zahlen. - die Kosten werden beim Mutterhaus im Ausland komplett in den Aufwand eingebucht. - als Anreiz des türkischen Staates die Mitarbeiter von der Einkommenssteuer befreit. 63 Corporate Design PowerPoint | 30.10.2014 | © SWITZERLAND GLOBAL ENTERPRISE

Vertrieb über ein VERBINDUNGSBÜRO / REPRÄSENTANZ

Gründung:

- ein Verbindungsbüroleiter mit umfangreichen Vollmachten

- Antrag auf Gründungserlaubnis an das Staatssekretariat für Schatzwesen

beim Generaldirektorat für ausländische Investitionen in Ankara gestellt. Das

Genehmigungsschreiben des Generaldirektorats gilt als Legitimation des

Büros vor Ort.

Vorteile Nachteile

Steuerung der Strategie über Keine Möglichkeit, lokale

eigene Mitarbeiter Rechnungen zu stellen

Keine Einkommenssteuer für die Keine Import- oder

Mitarbeiter Lagerhaltungsmöglichkeit

Repräsentanz mit Adresse und Vorsteuer nicht abzugsfähig

Telefonnummer in der Türkei

Einfache Ausgabenbuchhaltung

Vertrauen der Kunden

64 Corporate Design PowerPoint | 30.10.2014 | © SWITZERLAND GLOBAL ENTERPRISEDIREKTINVESTITIONEN

Allgemein:

- Sehr liberales Investitionsklima

Vorteile Nachteile

Erleichterter Marktzugang Hohe Investitionskosten (Fix)

Kundennähe und –vertrauen Längere Amortisationsdauer

Umgehung von Handelsbarrieren Hohe Transaktionskosten

Günstige Kostensituation

Wettbewerbsvorteile

65 Corporate Design PowerPoint | 30.10.2014 | © SWITZERLAND GLOBAL ENTERPRISEYou can also read