Economics Goldilocks and the three bears - Capital Nomura Securities Public Company Limited - NOMURA DIRECT

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Connecting Markets East & West Economics Goldilocks and the three bears Capital Nomura Securities Public Company Limited Investment Research and Investor Services Nuchjarin Panarode (+66 2638 5776) Nuchjarin.panarode@th.nomura.com February 2020 © Nomura

Executive Summary

Global: Goldilocks and the three bears

US: Holding pattern

Euro area: ECB on hold

Japan: Still many clouds ahead

Asia: Glass is half full and half empty

Thailand : A severe fiscal drag

Capital Nomura Securities Public Company Limited

Economics - 1

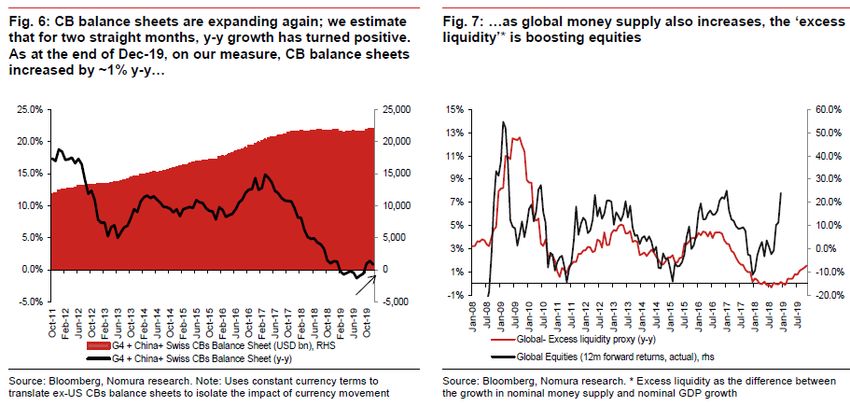

Global : Green shoots of recovery

Source : Nomura ,” Anchor Report: Asia Pacific Strategy : 2020 Outlook: The show will go on (10 January 2020)”

Capital Nomura Securities Public Company Limited

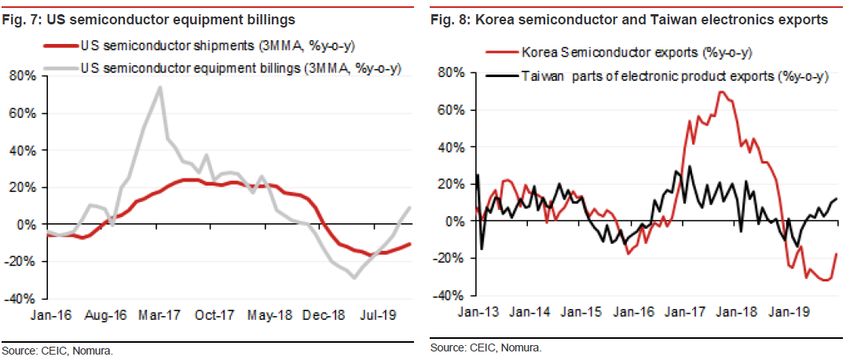

Economics - 2Global : Improving semiconductor/electronics cycle

Source : Nomura ,” Anchor Report: Asia Pacific Strategy : 2020 Outlook: The show will go on (10 January 2020)”

Capital Nomura Securities Public Company Limited

Economics - 3Global : Dovish monetary stance

Source : Nomura ,” Anchor Report: Asia Pacific Strategy : 2020 Outlook: The show will go on (10 January 2020)”

Capital Nomura Securities Public Company Limited

Economics - 4Nomura : FX valuation update ( Sep 19)

30 Sep 19 30 Sep 19

DXY = 99.38 USDTHB= 30.58

Overvalued by 11%

Overvalued by 4%

Source : Nomura , “FX Insights; Global FX valuation update (22 October 2019)

Capital Nomura Securities Public Company Limited

Economics - 5Nomura : FX valuation update ( Dec-19)

31 Dec 19 31 Dec 19

DXY = 96.39 USDTHB = 29.7

Overvalued by 10.1%

Overvalued by 2.5%

Source : Nomura ,” FX Insights: Global FX valuation update (23 January 2020)

Capital Nomura Securities Public Company Limited

Economics - 6Global : Goldilocks and the three bears

Source : Nomura ,” Global Economic Outlook Monthly ( 14 January 2020)” ; Note : EEMEA = Czech Republic, Hungary, Poland, Romania, South Africa, Turkey, Russia and Israel ; Bold = actual J Ja

Capital Nomura Securities Public Company Limited

Economics - 7Global risk : Debt stress, US-China rivalry and geopolitics

Source : Nomura ,” Global 2020 Economic Outlook (10 December 2019)”

Capital Nomura Securities Public Company Limited

Economics - 8Global risk : Coronavirus

Direct and total contribution of travel and tourism to the global economy

10.4% of global

GDP

Global Tourists 2018 = 1,323 mn

Chinese tourists = 149.72 mn

(11.3% share)

3.2% of global

GDP’18

(USD84.8trn

Source: https://www.statista.com/statistics/233223/travel-and-tourism--total-economic-contribution-worldwide/ ; https://www.travelchinaguide.com/tourism/

IMF, CNS (IRIS)

The direct travel & tourism contribution includes the commodities accommodation, transportation, entertainment and attractions of these industries: Accommodation services, food & beverage services,

retail trade, transportation services and cultural, sports & recreational services. The figures for total impact also include indirect and induced contributions.

Capital Nomura Securities Public Company Limited

Economics - 9US : De-escalation of US-China trade tensions.

Source : Nomura , “US Monthly Inflation Monitor ( 10 October 2019)” Source : “US Economic Weekly (10 January 2020)”

Capital Nomura Securities Public Company Limited

Economics - 10US : Holding pattern

Growth has slowed to potential but we expect a modest acceleration starting in H2 2020 as uncertainty wanes.

Recession risk has dissipated as consumer fundamentals help sustain the expansion

Core inflation should pick up as higher tariffs pass through to consumer prices and labor markets remain tight.

After cutting rates three times in 2019, we expect the Fed to remain on hold over the forecast horizon.

Risks include aggressive trade policy, elevated levels of corporate debt and a sudden tightening of financial conditions

Source : Nomura , “US Economic Weekly ( 24 January 2020 )”

Capital Nomura Securities Public Company Limited

Economics - 11Euro area : Green shoots of recovery

Source : Nomura , Europe Economic Weekly (17 Janurary 2020; 24 January 2020)

Capital Nomura Securities Public Company Limited

Economics - 12Euro area : ECB on hold

We expect growth to stay weak but to slowly recover in 2020. Manufacturing recession risks spilling over into

services/jobs.

We see euro area core inflation rising gradually over time, but remaining well below the ECB’s inflation aim.

We expect the ECB to remain on hold as survey data improve and underlying measures of inflation grind higher.

Source : Nomura , “Europe Economic Weekly ( 10 January 2020 )”

Capital Nomura Securities Public Company Limited

Economics - 13Asia ex-Japan : Glass is half full and half empty

Glass half empty: Despite recent green shoots, we expect GDP growth to slow further in Q4 with a prolonged bottoming

process into Q1 2020 due to a slowing China, weak consumption and elevated inventories.

Glass half full: We expect only the first signs of a recovery in Q2 2020, as Asia benefits from an upturn in the tech cycle

and easier financial conditions. The U-shaped growth profile will be led by exporters, while consumers lag.

Despite the Fed leaving rates unchanged, we forecast more policy rate cuts in China, India, Indonesia, Malaysia and

Thailand.

In the case of a deeper slowdown, fiscal easing will likely be stepped up.

Source : Nomura , “Global 2020 Economic Outlook ( 10 December 2019 )”

Capital Nomura Securities Public Company Limited

Economics - 14Asia ex-Japan : Growth cycle upturn will likely disappoint

Source : Nomura , “Global 2020 Economic Outlook ( 10 December 2019 )”

Capital Nomura Securities Public Company Limited

Economics - 15Asia ex-Japan : Sensitivity to China growth

Source : Nomura , “Global 2020 Economic Outlook ( 10 December 2019 )”

Capital Nomura Securities Public Company Limited

Economics - 16Asia ex-Japan : Easier financial conditions

Source : Nomura , “Global 2020 Economic Outlook ( 10 December 2019 )”

Capital Nomura Securities Public Company Limited

Economics - 17Thailand : Domestic-led growth

Source : NESDC ( 18 November 2019)

Capital Nomura Securities Public Company Limited

Economics - 18Thailand : Weaker domestic strength

Source : Nomura , “Global 2020 Economic Outlook ( 10 December 2019 )”

Capital Nomura Securities Public Company Limited

Economics - 19Thailand: Green shoots of recovery in industrial sector

Source : The Bank of Thailand (31 January 2020)

Capital Nomura Securities Public Company Limited

Economics - 20Thailand : A severe fiscal drag

We forecast 2020 GDP growth to remain well below potential at 2.7% (and below Consensus’ 3%). The large fiscal

drag from the delayed budget in the near term is likely under-estimated by market participants due to the government

announcing a slew of fiscal stimulus measures, which we think will prove ineffective.

In response, we expect the BOT to cut again by 25bp to 1% in Q1 ( Likely Feb-5)

In the near term, we expect H1 2020 GDP growth to average 2.3% y-o-y, from 2.4% in H2 2019, weighed on by the

fiscal drag due to delays in the budget bill being passed, before picking up to 3.1% in H2, helped by back-loaded

government spending.

Source : Nomura , “Global Economic Outlook Monthly (14 January D2019 )”

Capital Nomura Securities Public Company Limited

Economics - 21Risks: Coronavirus

Capital Nomura Securities Public Company Limited

Economics - 22Risks: Budget FY2020 delay

Source : Fiscal Policy Office

Capital Nomura Securities Public Company Limited

Economics - 23ANALYST CERTIFICATION FOR REGULATION

I, Nuchjarin Panarode , a research analyst employed by Capital Nomura Securities, hereby certify that all of the views expressed in this research report accurately reflect my personal views about any and

all of the subject securities or issuers discussed herein.

In addition, I hereby certify that no part of my compensation was, is, or will be, directly or indirectly related to the specific recommendations or views that I have expressed in this research report, nor is it

tied to any specific investment banking transactions performed by Nomura Securities International, Inc., Nomura International plc or by any other Nomura Group company or affiliate thereof.

Explanation of CNS rating system for Thailand companies under coverage published from 2 March 2009:

Stocks:

Stock recommendations are based on absolute valuation upside (downside), which is defined as (Fair Value - Current Price) / Current Price, subject to limited management discretion. In most cases, the

Fair Value will equal the analyst’s assessment of the current intrinsic fair value of the stock using an appropriate valuation methodology such as Discounted Cash Flow or Multiple analysis etc. However, if

the analyst doesn’t think the market will revalue the stock over the specified time horizon due to a lack of events or catalysts, then the fair value may differ from the intrinsic fair value. In most cases,

therefore, our recommendation is an assessment of the difference between current market price and our estimate of current intrinsic fair value. Recommendations are set with a 6-12 month horizon unless

specified otherwise. Accordingly, within this horizon, price volatility may cause the actual upside or downside based on the prevailing market price to differ from the upside or downside implied by the

recommendation.

• A "Buy” recommendation indicates that potential upside is 15% or more.

• A "Neutral" recommendation indicates that potential upside is less than 15% or downside is less than 5%.

• A "Reduce" recommendation indicates that potential downside is 5% or more.

Sectors:

A "Bullish" rating means most stocks in the sector have (or the weighted average recommendation of the stocks under coverage is) a positive absolute recommendation.

A "Neutral" rating means most stocks in the sector have (or the weighted average recommendation of the stocks under coverage is) a neutral absolute recommendation.

A "Bearish" rating means most stocks in the sector have (or the weighted average recommendation of the stocks under coverage is) a negative absolute recommendation.

DISCLAIMERS:

This publication contains material that has been prepared by Capital Nomura Securities Public Co., Ltd., Bangkok, Thailand. This material is (i) for your private information, and we are not soliciting any

action based upon it; (ii) not to be construed as an offer to sell or a solicitation of an offer to buy any security in any jurisdiction where such an offer or solicitation would be illegal; and (iii) is based upon

information that we consider reliable, but we do not represent that it is accurate or complete, and it should not be relied upon as such. Opinions expressed are current opinions as of the date appearing on

this material only and the information, including the opinions contained herein are subject to change without notice. We, or other affiliates and/or subsidiaries of Nomura Holdings, Inc. (collectively referred

to as the “Nomura Group”) may from time to time perform investment banking or other services (including acting as advisor, manager or lender) for, or solicit investment banking or other business from,

companies mentioned herein. We, the Nomura Group, our or any of their officers, directors and employees, including persons involved in the preparation or issuance of this material may, from time to time,

have long or short positions in, and buy or sell (or make a market in), the securities, or derivatives (including options) thereof, of companies mentioned herein. We, or a member of the Nomura Group, our

or any of their officers, directors and employees may, to the extent it is permitted by applicable law, have acted upon or used this material, prior to or immediately following its publication. The securities

described herein may not have been registered under the U.S. Securities Act of 1933, and, in such case, may not be offered or sold in the United States or to U.S. persons unless they have been

registered under such Act, or except in compliance with an exemption from the registration requirements of such Act. Unless governing law permits otherwise, you must contact a Nomura Group entity in

your home jurisdiction if you want to use our services in effecting a transaction in the securities mentioned in this material. This publication is intended for investors who are not private or expert investors

within the meaning of the Rules of the Securities and Futures Authority Limited, and should not, therefore, be redistributed to private or expert investors. No part of this material may be (i) copied,

photocopied, or duplicated in any form, by any means, or (ii) redistributed without CNS’ prior written consent. Further information on any of the securities mentioned herein may be obtained upon request. If

this publication has been distributed by electronic transmission, such as e-mail, then such transmission cannot be guaranteed to be secure or error-free as information could be intercepted, corrupted, lost,

destroyed, arrive late or incomplete, or contain viruses. The sender therefore does not accept liability for any errors or omissions in the contents of this publication, which may arise as a result of electronic

transmission. If verification is required, please request a hard-copy version.

Capital Nomura Securities Public Company Limited

Economics - 24You can also read