ELECTRIC CARS AN OVERVIEW OF THE ELECTRIC CAR INDUSTRY AND ASSOCIATED TECHNOLOGY - Innovation Origins

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

ELECTRIC CARS

AN OVERVIEW OF THE ELECTRIC CAR

INDUSTRY AND ASSOCIATED TECHNOLOGY

Table of contents

Technology: The road to greater range and faster charging Adoption: The drivers behind demand

▪ Batteries ▪ Sales growth

▪ Range ▪ Penetration rate

▪ Charging infrastructure ▪ Sales potential

Investment: The ideas leading to innovation Revenue: The segments and regions of growth

▪ Auto industry R&D ▪ Market growth

▪ EV investments ▪ Electric vehicle market size

▪ Patents ▪ EV battery market size

Production: The leading regions, companies, and models Sustainability: The issues that need to be tackled

▪ Assembly ▪ Transportation-related emissions

▪ Manufacturers ▪ Renewable sources in power generation

▪ Models ▪ Materials used in batteries

2

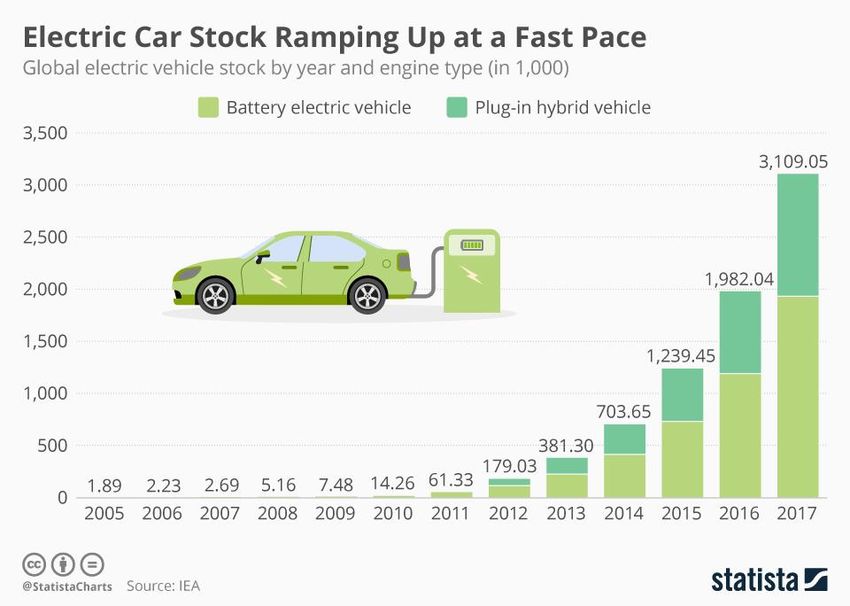

Executive Summary The history of motor vehicle manufacturing can be compared to a long and winding road which began in the second half of the 19th century. Although the early 20th century saw the electric car accounting for about one third of road vehicles in operation in the United States and Europe, this type of vehicle quickly became marginalized by diesel and gasoline-powered automobiles, including Ford’s Model T. The so-called Tin Lizzy was built at such an exceptionally low cost that it became hard for electric vehicles (EVs) to compete. The superior driving range of the internal combustion engine (ICE) used in gasoline and diesel-powered cars, coupled with a growing number of gas stations which made refueling quick and easy, added further to the decline in the electric car’s popularity. However, the love for diesel and gasoline-powered vehicles among customers in Europe and North America still took some unexpected turns between 1973 and 2011. During these four decades, several instances of fossil fuel shortages roiled the world’s leading economies and affected the prices of petroleum products. Additionally, some countries began to introduce higher taxes on fuel to incentivize ecological sustainability. Since the first United Nations Framework Convention on Climate Change (UNFCCC) Conference of the Parties was held in 1995, the rise of greenhouse gas (GHG) emissions has raised concerns among the United Nations member states that greenhouse gases will increase surface temperature levels and thus lead to the destruction of the earth’s ecosystem. Considering that the transportation sector is one of the leading producers of greenhouse gases, cutting GHG emissions from car travel has emerged as an effective way to curb emission growth. In light of these efforts to tackle GHG emissions, passenger electric vehicles have made a comeback: If electricity from renewable energy sources is used to fuel them, EVs have the potential to play a vital role in the reduction of carbon dioxide and nitrogen oxide emissions. This is an even more important undertaking today, as the light vehicle market has increased tremendously over the past two decades, approaching the 100 million vehicle sales mark. Batteries remain the electric car’s greatest vulnerability. Recharging will have to become easier, and range will have to improve. In the end, EVs can only be environmentally benign if the industries providing the commodities used in electric vehicle batteries are able to reduce their impact on the planet. 3

Electric vehicle timeline

1832 Robert Anderson creates the first crude electric carriage

1900 Ferdinand Porsche develops the world’s first hybrid

1935 Gasoline-powered cars force EVs out of the market

1996 General Motors launches the EV1

1997 Toyota releases the Prius - the first mass-produced hybrid car

2008 Tesla Motors launches its Roadster, an all-electric luxury sports car

BYD releases the F3DM - the world’s first plug-in hybrid compact sedan

2010 General Motors introduces the Chevy Volt - the first mass-produced plug-in hybrid;

Nissan releases the all-electric Leaf

2014 Nissan Leaf sales surpass the 100,000 unit mark

2018 The Model 3 becomes Tesla’s best-selling model

4

01 Technology: The road to greater range

and faster charging

▪ Batteries

▪ Range

▪ Charging infrastructure

Improved battery technology is the key to competitiveness

While Toyota is betting big on fuel cell electric vehicles (FCEVs), many other carmakers are focusing on battery technology. There are

two major categories of batteries holding the potential to power EVs: solid-state batteries and liquid electrolyte batteries. While solid-

state batteries for EVs have not yet reached market commercialization, the latter have been used in EVs for many decades.

In 2016, the lithium-ion batteries in some Samsung Galaxy Note 7 devices caught fire and exploded. This incident shows how difficult it

is to manufacture lithium-ion batteries that are both efficient and stable. When the EV battery industry began to add nickel to their

battery cells to increase the range of electric vehicles, the inclusion of cobalt and manganese was required to prevent the battery from

losing stability by controlling how nickel and lithium ions move between the battery cell’s anode and cathode.

▪ Research into electric vehicle battery technology aims to achieve the following:

› low costs

› high capacity and stability

› quick and easy recharging

▪ 50 percent of BEV manufacturing costs are powertrain-related

▪ Declining battery costs are expected to push electric vehicle sales

▪ Finding the right material mix will be key to winning the EV battery race

▪ Consumers demand higher range, lower costs, and easier access to charging infrastructure

▪ Electric vehicle energy charging demand will push electricity use in the United States – and probably across all other markets too

6

50 percent of BEV manufacturing costs are powertrain-related As of 2018, the costs

unrelated to the electric

powertrain in a battery

electric vehicle (BEV) only

account for about 50

Share of BEV manufacturing costs in 2018 percent of the overall

0 10 20 30 40 50 60 manufacturing costs.

Battery cells currently

Battery cell 25 account for around 25

percent of costs attributed

to the manufacturing of all-

electric vehicles, and thus

Electric motor and power electronics 15

hold the greatest potential

for cost reduction.

Battery integration 10

Costs unrelated to the powertrain 50

Note: Worldwide

Source(s): JPMorgan Chase; BCG

7

Lithium-ion battery pack costs are set to reach a record low in 2019 This year, lithium-ion

battery pack costs are

expected to drop to 158

U.S. dollars per kilowatt

hour.

1200

Estimated cost in 2018 in U.S. dollars per battery pack Battery pack costs are

0 500 1000 1500 2000

Costs between 2010 and 2019 in U.S. dollars per kilowatt hour

driven by size, production

1,000

1000 volumes, and costs

Cobalt 1,764 attributable to the

commodities used in the

800 manufacturing process.

Electric vehicles may be

Nickel 1,433

599 less vulnerable to fossil

600

fuel prices, but they

continue to be susceptible

400

to a volatile commodity

Lithium carbonate 1,005 market. As a result of

273

cobalt’s contribution to EV

200 158 battery pack costs in 2018,

automotive manufacturers

Graphite 536 and suppliers are now

0 seeking alternatives to this

2010 2013 2016 2019*

commodity and other

expensive materials.

Note: Worldwide

Source(s): Bloomberg New Energy Finance; Bloomberg; PwC; Strategy&; Various sources

8

Battery chemistry trends diverge between China and the rest of the world By 2020, natrium-

manganese-nickel (NMC)

battery cathodes are

LMO LFP NCA NMC-622 NMC-811 expected to include more

120.0% nickel than today’s

batteries and the cobalt

content in the more novel

100.0%

NMC-622 and NMC-811

types is projected to be

15%

significantly lower than in

32% the NMC-111 batteries that

Projected market share in 2020

80.0%

are used most commonly

today. Taking into

consideration that cobalt

60.0% prices rose fourfold

between 2016 and 2018,

40% 73% the trend towards lower

40.0% cobalt levels may make

EV batteries more cost-

effective in the long run.

20.0% Concurrently, the level of

26% nickel in the NMC-811 and

2%

the nickel-cobalt-aluminum

10%

0.0%

2% (NCA) variants is set to

Worldwide (excluding China) China exceed the 80 percent

mark, leading to enhanced

battery capacity.

Note: Worldwide

Source(s): McKinsey

9

Battery chemistry composition is expected to drive mild increases in battery capacity levels

Plug-in hybrid electric vehicles Battery electric vehicles

50

45

45 43

41

40

Estimated battery capacity in kilowatt hours

35

30

25

20

15

10.2 10.6 11

10

5

0

2017 2021 2025

Note: Worldwide

Source(s): Various sources; BMO Capital Markets

10Consumers are expected to welcome the converging range gap between electric and ICE cars

EV range in kilometers Share of respondents surveyed in 2018 who will not consider buying

500 EV

0.0% 10.0% 20.0% 30.0% 40.0%

450 440

Price/cost 35%

400 380

350

Charging 24%

300

300

Range 18%

250

200 Cost reductions,

Uncertainty about future

12%

tech developments better charging

150 infrastructure,

and longer

100 Suitability for daily use 11% ranges will help

convince those

50 who said they

Image 1% would not switch

0 to an electric car

2020 2025 2030 in 2018.

Note: Worldwide; 18 years and older; 2,028 Respondents;

Source(s): Oliver Wyman; VDA; Merrill Lynch; KPMG

11Electric vehicle public charging infrastructure growth is waning globally

80.0%

71%

69%

70.0%

EV public charging infrastructure percent growth

60.0%

50.0%

40.0%

33%

30.0%

20.0%

10.0%

0.0%

2015 2016 2017

Note: Worldwide

Source(s): AlixPartners

12Range anxiety remains a

common concern among

those consumers who are

hesitant to purchase an

electric car.

In addition to this,

consumers are concerned

that the electric car

charging infrastructure in

place today is not yet

sufficient for widespread,

carefree recharging.

No matter how much the

number of charging outlets

has grown over the past

decade, consumers want

to be able to recharge

whenever their battery is

low – and they want to do

it fast.

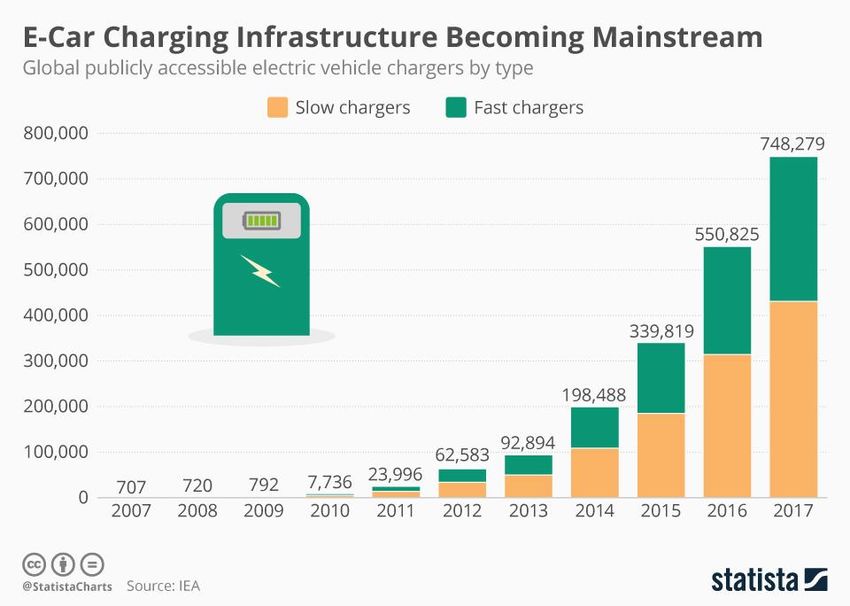

13Slow Fast Number of chargers

was not equally

Number of EV chargers in 2017

0 50000 100000 150000 200000 250000 distributed across

China

markets in 2017

Consumers cannot yet

United States expect to find a charging

outlet whenever they need

Netherlands

it although the number of

Japan

electric vehicle supply

equipment (EVSE)

Others chargers grew a

thousandfold between

Germany 2007 and 2017.

France

Moreover, there is a

distinction between slow

United Kingdom and fast chargers, different

socket standards, and

Norway payment methods, making

it even more difficult for

Canada

consumers to find the

charging point they need.

Korea

Sweden

Note: Worldwide

Source(s): IEA; EAFO

14Despite being the second

largest sales market for

electric vehicles, the

United States trailed most

countries in terms of

electric vehicle charging

density in 2017.

In addition to this, the

charging outlets that do

exist are provided by a

number of charging

networks using varying

standards in terms of plug

size and power limits.

15Electric vehicle charging infrastructure fragmentation left consumers confused in 2018

Number of charging outlets as of July 18, 2018 by network

0 5000 10000 15000 20000 25000 30000

ChargePoint 23,992

Tesla 7,758

Blink 3,494

SemaConnect 2,657

EVgo 2,372

Greenlots 992

Note: United States

Source(s): Alternative Fuels Data Center; Automotive News

16Energy demand for electric vehicle charging is expected to be highest in North America by 2030

Projected demand in 2030 in megawatt hours

0 50 100 150 200 250

North America 78.74

China 68.32

Europe 34.16

Japan 10.17

Worldwide 207.99

Note: Worldwide

Source(s): Wood Mackenzie; Bloomberg

17Electric vehicle energy charging demand will push electricity use in the United States

EV charging demand in billion kilowatt hours Electricity use in billion kilowatt hours

60 6000

53

5,193

4,932

50 5000

4,712

4,509

4,352

4,203

4,039

40 4000 3,853

30 3000

23

20 2000

10 1000

6

0 0

2020 2025 2030 2017 2020 2025 2030 2035 2040 2045 2050

Note: United States

Source(s): McKinsey; EIA

1802 Investment: The ideas leading to

innovation

▪ Auto industry R&D

▪ EV investments

▪ PatentsInvestments are the foundation on which the industry stands Investments need to be made not only in the field of electric vehicle-related battery technology, but also with regards to the sufficient provision of charging outlets. Providing the infrastructure for all the various types of electric vehicles proves to be a difficult task, after an entire industry had focused on diesel and gasoline-propelled motor vehicles for almost a century. The tightening of environmental regulation puts pressure on carmakers and suppliers alike to invest in emerging electric vehicle technologies. The shift away from internal combustion engines may not come without risks, but the introduction of new technologies offers additional opportunities for automotive suppliers and manufacturers. While some original equipment manufacturers (OEMs) in the motor vehicle manufacturing and parts industry started shifting their attention towards the connected driving and mobility services realms, others have made it paramount to invest in green vehicles: • Globally operating traditional automakers invest most heavily in R&D activities • Tesla has the highest R&D intensity in the industry • France is the leading European nation in terms of electric vehicle-related technology 20

“I hope you will still recognize us as being the inventor of

„

the car, but we should be defined by our future, not by our

past.”

– Dieter Zetsche,

Chairman of Daimler AG and Head of Mercedes-Benz Cars

21Traditional OEMs invest most heavily in R&D activities Traditional automotive

OEMs were the ones

investing most heavily in

R&D spending in FY 2018 in billion U.S. dollars research and development

0 2 4 6 8 10 12 14 16 18 (R&D) activities during the

2018 fiscal year.

Volkswagen* 15.53 That said, the highest ratio

of R&D spending to

revenue was yielded by a

firm with a comparatively

Daimler* 10.36 small sales base: Tesla.

Toyota** 9.58

Ford 8.2

General Motors 7.8

Note: Worldwide

Source(s): Statista; Volkswagen; Daimler; Toyota; Ford; General Motors

* VW: the value refers to R&D costs in the automotive division; VW & Daimler: These figures have been converted at the following rate, correct

as of March 1, 2019: 1 euro = 1. 13835 U.S. dollars; ** this figure has been converted at the following rate, correct as of March 1, 2019: 1,000

Japanese yen = 9. 00558 U.S. dollars; the figure is for FY ended March 31, 2018.

22R&D intensity by carmaker as of June 2018

Tesla outperformed its larger

0.0% 2.0% 4.0% 6.0% 8.0% 10.0% 12.0% 14.0% competitors in terms of R&D to

sales ratio in 2018

Tesla 11.7%

The following list includes a selection of

investments and partnerships:

Volkswagen Group 5.7%

▪ Daimler: invests in ChargePoint,

collaborates with BYD, is part of IONITY

Honda 5.4%

▪ BMW: invests in ChargePoint, is part of

IONITY, collaborates with Umicore,

Ford 5.1% Northvolt

▪ VW: invests in ChargePoint , is part of

Isuzu Motors Limited 5%

IONITY

▪ Ford: is part of IONITY

BMW 5% ▪ GM: invests in Evgo

▪ Hyundai: collaborates with Hawtai

General Motors 5% ▪ Delphi: is owner of NuTonomy

▪ Shell: is owner of NewMotion, invests in

Renault 4.4% Sonnen

▪ BP: invests in PowerShare, FreeWire,

Suzuki Motors 4.4% StoreDot, Chargemaster

▪ Total SA: is owner of G2mobility, Saft SA,

Note: Worldwide

collaborates with Nexans

Source(s): PwC; Strategy&; Various sources

According to the source, all sales and R&D expenditure values in foreign currencies were converted into U.S. dollars at an average of the exchange rate over the relevant period;

all figures are for the last fiscal year, as of June 30, 2018.

23Daimler and Tesla dedicated ~ 90 percent of patents to green vehicles between 2012 and 2016

0 10 20 30 40 50 60 70 80 90 100

Daimler 90.4

Tesla 90.4

VW 84.2

Audi 77

BMW 76.3

GM 35

Note: Worldwide

Source(s): Oliver Wyman; WIPO

24Globally operating carmakers are projected to account for almost two thirds of investments in 2023

Projected R&D funding in 2023 by investor in billion U.S. dollars

0 50 100 150 200 250 300

Globally operating OEMs 184

Chinese OEMs 32

Globally operating suppliers 21

Chinese suppliers 10

EV niche OEMs 9

Total 255

Note: Worldwide

Source(s): AlixPartners

25Qualcomm has filed one of the most valuable patents in the field of EVs Qualcomm’s 2017 R&D

costs-to-revenue ratio was

comparatively high with

around 25 percent. The

company filed some 2,163

4500 4,024 patents in 2017.

Number of applications in

4000

3500 2,965 In 2018, an EV wireless

3000 2,637 2,521

2500 2,163 1,945 charging patent application

2017

1,818 1,757

2000

1500

was submitted on behalf of

1000 Qualcomm and approved

500

0

by the USPTO.

Huawei ZTE Corp. Intel Corp. Mitsubishi Qualcomm Inc. LG Electronics BOE Samsung

Technologies Electric Technological Electronics It was considered a

Group scientific breakthrough and

acquired by WiTricity in

2019.

30.0%

25% 25%

Qualcomm’s research and

development costs as a

25.0% 22%

share of revenue

20.0%

15.0%

10.0%

5.0%

0.0%

2016 2017 2018

Note: Worldwide

Source(s): WIPO; Qualcomm

269000 Moderate

8,500

growth in

8000 EV-related

7,500 patent

filings

7000

can be

anticipated

6000

Number of EV-related patents filed

Most electric

vehicle-

5000 related

patents were

granted in the

4000 electric

propulsion

and

3000

secondary cell

manufacturing

2000 segments,

with most of

the activity

1000 occurring in

China and the

0

United States.

2018 2020

Note: Worldwide

Source(s): Power Electronics World (powerelectronicsworld.net)

27Technology Industry Market France seemed better equipped in

terms of technology than other

Index score

0 2 4 6 8 10 12 European markets in 2018

Not only is France home to some of the

China 0.9 5 5 world’s leading automotive manufacturing

groups, such as Groupe Renault and

Groupe PSA, but the country is also the

U.S. 1.8 4.6 4.5

domestic market of Total SA-owned Saft

Groupe SA, one of the few battery

manufacturers in Europe with an

international presence.

Japan 1.8 4.3 4.2

France’s carmakers offer a range of electric

vehicles in the non-premium segment,

including Europe’s second-best-selling all-

Germany 2.2 3 5

electric car, the Renault Zoe.

France 2.9 1.5 5

South Korea 2.1 3.8 3.1

Note: Worldwide

Source(s): Roland Berger; fka

The indicators are defined by the source as follows:

Technology: Current status of electric vehicle-related technology developments made by domestic OEMs, and national subsidy program support

Industry: National vehicle, system and component production industry added value

28 Market: National electric vehicle market size based on current customer demand03 Production: The leading regions,

companies, and models

▪ Production volume

▪ Models

▪ OEMs„

“ “The first step is to establish that something is possible;

then probability will occur.”

– Elon Musk,

CEO of Tesla, Inc. and SpaceX

30Production volumes are beginning to pick up after a slow start Policymakers saw the opportunity to replace ICE cars with electric vehicles as soon as the effects of road transportation on air quality became apparent. However, the CEOs of traditional carmakers, such as Volkswagen or General Motors, seemed to lack the imagination to believe in the electric vehicle’s success for the best part of two decades. Some 16 years after Tesla’s founding, traditional automotive manufacturers have likely turned a corner, and, along with new entrants from the Chinese mainland - including BYD, Chery, and Hawtai - they are now hot on Tesla’s heels. It is expected that over 30 million hybrid cars and plug-in electric vehicles will be produced by 2025, with battery electric vehicles accounting for almost 50 percent of total production. ▪ Worldwide production volume of all-electric vehicles is expected to grow fourfold ▪ Growth is expected to be highest in the plug-in electric vehicle segments, but hybrid production will continue to rise ▪ China is predicted to remain the largest market in terms of electric vehicle production by country ▪ Additional model launches are expected to trigger consumer demand 31

Battery and plug-in hybrid vehicles are projected to experience the highest growth

16 12

14.8

10.5

14

10

12

8

PHEV production in millions

BEV production in millions

10

8 6

6

4

3

4 3.5

2

2

0.5 0.2

0 0

2015 2020 2025 2015 2020 2025

Note: Worldwide

Source(s): McKinsey

326 Hybrid production

will continue despite

5.4

smaller output levels

5 The production of hybrid

electric vehicles is

projected to grow to about

5.4 million units globally by

4 2025.

Hybrid EV production in millions

This volume is significantly

lower than the anticipated

10.5 million units in the

3 2.9

plug-in hybrid electric

vehicle segment and the

14.8 million units in the

battery electric vehicle

2

segment but the market is

still likely to grow.

1.2

1

0

2015 2020 2025

Note: Worldwide

Source(s): McKinsey

33Asia will remain the leading producer of electric vehicles throughout 2030

Expected xEV production volume by 2030 in million units

0 5 10 15 20 25 30 35 40

Asia* 37.6

Europe 16.5

North America 4.4

South America 0.8

Middle East and Africa 0.4

Note: Worldwide

Source(s): IHS Markit

* The figures for India, China, Japan, South Korea, and the ASEAN region have been added up.

The term xEV refers to battery and plug-in hybrid vehicles.

34EV* production in 2021 in thousand units

China will continue to lead on a

0 1000 2000 3000 4000 5000 6000 7000 8000 country-by-country level through ‘21

The following list presents a selection of

China 6,843 announcements on EVs made by OEMs:

▪ Toyota is expected to release 10 EV

models by 2020

United States 3,058 ▪ VW is committed to launch more than 50

BEV models by 2025

▪ Renault-Nissan wants EVs to account for

20 percent of sales by 2023

Germany 2,247

▪ GM will launch two EV models in 2019

Country

▪ PSA is to launch 27 EV models by 2023

Japan 1,023 ▪ Ford plans to release 40 EV models by

2022

▪ By 2022, Daimler plans to release 10 EV

models

France 763

▪ BMW is expected to launch the Mini E, the

i5, and the X3 i between 2019 and 2021

▪ BAIC intends to add 10 EV models to its

South Korea 632 portfolio by 2025

▪ Geely plans to launch two more models

under its Polestar brand by 2025

Note: Worldwide

Source(s): Forschungsgesellschaft Kraftfahrwesen Aachen; Roland Berger

* Numbers refer to battery-powered and plug-in hybrid vehicles.

35Global number of battery electric vehicle model launches between 2015 and 2020

80

73

70

59

60

55

Number of new BEV model launches

50

44

40

30

20 17

14

10

0

2015 2016 2017 2018 2019 2020

Note: Worldwide

Source(s): LMC Automotive; Citigroup

36Global number of plug-in hybrid electric vehicle model launches between 2015 and 2020

70

64

60

Number of new PHEV model launches

50

45

42

40

30

20

20

16

10

7

0

2015 2016 2017 2018 2019 2020

Note: Worldwide

Source(s): LMC Automotive; Citigroup

3704 Adoption: The drivers behind

demand

▪ Sales

▪ Penetration rate

▪ ForecastsDemand is affected by cost competitiveness and mobility trends Ten years from now, plug-in electric vehicles are expected to account for close to half of all vehicle sales. It is also projected that electric vehicle adoption will be driven by growing access to public charging infrastructure in tandem with increased vehicle model availability. Furthermore, electric vehicles are projected to pique consumers’ interest, once the cost of ownership reaches parity with ICE vehicles; this is predicted to happen over the course of the next two to four years. Innovative trends in the field of mobility services such as car-sharing, ride-sharing, and ride-hailing are forecast to raise consumer awareness and help users familiarize themselves with EV technologies. ▪ The share of ICE cars in overall light vehicle sales is forecast to fall to almost 50 percent by 2030 ▪ As adoption levels pick up, the electric vehicle market is projected to gain traction ▪ Mobility service fleets are set to fuel electric vehicle demand ▪ Tesla has emerged as the market leader in battery electric vehicle sales ▪ The Model 3 has become Tesla’s best-selling model 39

Key drivers of electric vehicle adoption It is predicted that EV

buyers want the total cost

of ownership in tandem

with potential government

Supply side factors Demand side factors

subsidies to be within the

range of what they would

Electricity/ oil

normally have to pay for a

prices comparable ICE car.

Efficiency New mobility trends are

Availability of projected to help

vehicles

Manufacturing consumers familiarize

costs

themselves with EV

Variety of Cost is driven

OEM competition increases

models competitiveness by National technologies.

subsidies

As soon as consumers are

Political EV

Maintenance satisfied with the

triggers costs

frameset adoption availability of suitable

Availability of are

chargers

Consumer attitudes

affected by models and a sufficient

Implementation

Range anxiety charging infrastructure,

increases

of infrastructure

adoption levels can be

Awareness expected to pick up speed.

Speed of Adoption of new are

charging mobility trends affected by

Availability of

Mobility services

Availability of

Autonomous cars

Note: Worldwide

Source(s): Statista; Nytimes.com; ICCT; Consumer Affairs; Renew Economy; L.E.K.

40The cost of refueling ICE cars is often higher than the running costs of electric vehicles

8

6.89

Assuming that

Gasoline prices as of Q4 2018

6.6 6.48

7 6.12 6.09 5.95 5.83 an average

in U.S. dollars per gallon

6

5

4.85 4.7

4.22

ICE sedan

3.95 3.95 3.94 3.88

4 has a fuel

2.6 2.48

3 2.06 economy of

2

0.54 30 mpg, and

1

0 thus a

consumption

level of about

3.3 gallons

per 100 miles,

U.S. Norway France Germany low power

12 rates may

Costs* in 2018 in U.S. dollars

10

9.57 9.68 help convince

8.07 8.25

consumers to

per 100 miles

8

5.69 5.69 5.75 5.76 switch to an

6 4.79 4.8 4.9 4.91

3.58 3.61

electric car,

4 3.01 3.08

especially in

2 markets

0 where gas

Hyundai IONIQ Tesla Model 3 Nissan Leaf II Renault Zoe

prices are

Note: Worldwide high.

Source(s): Bloomberg; IMF; UN; World Bank; CleanTechnica; nextmove.de; Eurostat; chooseenergy.com

* The results are based on estimated consumption rates by model and average residential electricity prices by country. The values have been converted from euros to U.S. dollars

at an average annual rate of 1 euro = 1.18 U.S. dollars, as retrieved from the ECB.

41The sales share of ICE vehicles continues to decline globally

Gasoline Diesel Mild hybrid electric vehicle (MHEV) Hybrid electric vehicle (HEV) Battery electric vehicle (BEV) Plug-in hybrid electric vehicle (PHEV)

120.0%

100.0%

1% 6%

1%

19% 2% 14%

80.0% 1%

13%

Share of car sales

60.0% 15%

5%

40.0%

76%

47%

20.0%

0.0%

2017 2030

Note: Worldwide

Source(s): BCG

42Projected size of the global electric vehicle fleet between 2020 and 2030

140

127

120

100

87

Vehicles in fleet in millions

80

60

60

40

40

25

20

13

0

2020 2022 2024 2026 2028 2030

Note: Worldwide

Source(s): Business Insider

43„

“ “We are convinced that the future of carsharing is electric.”

– Olivier Reppert,

CEO of Share Now

44Fleet size in 2025 in million units

Mobility fleet electrification is set to

0 5 10 15 20 25 30 35 40 45 50 spark EV adoption

Electrification will be key to other mobility

areas due to growing environmental

Carpooling 44.98 commitments and lower maintenance costs

associated with the parts in battery electric

vehicle motors.

Some firms have begun to unlock the value

of mobility services:

Ridehailing 35.93 ▪ Daimler: is owner of Share Now, ViaVan

▪ BMW: is owner of Share Now, Moovit

› Share Now has 3,200 BEVs in fleet1

▪ VW: is owner of Moia

Car rental & sharing 7.26 › Moia has 100 BEVs in fleet2

▪ GM: is owner of Maven, BOOK, invests in

Lyft

› Maven has 20 BEVs in fleet3

▪ Hyundai-Kia: invests in Grab

Carsharing (fleet-based and P2P) 1.42

▪ Avis: is owner of Zipcar

▪ Uber: collaborates with Daimler, Toyota,

VW

▪ Didi: collaborates with VW

Note: Worldwide

Source(s): Bank of America; Merrill Lynch

45Battery electric vehicles Plug-in hybrid electric vehicles Hybrids China

12000 holds the

potential to

extend its

10000

lead with

636 regards to

EV sales

Projected 2030 vehicle sales in thousand units

throughout

8000

2030

3,863

It is expected

that sales to

6000 customers in

China will

592

continue to be

436

crucial for EV

4000

1,976 manufacturers

1,638

throughout

5,507 2030. This is

2000

true for the

hybrid and

2,864

2,293 plug-in

electric

0 vehicle

U.S. Europe China segments.

Note: Worldwide

46 Source(s): Citigroup47

Estimated electric vehicles in use in selected countries as of 2017

PHEV BEV

Number of electric vehicles in thousands

0 200 400 600 800 1000 1200 1400

China

U.S.

Japan

Norway

Germany

Note: Worldwide

Source(s): IEA

48China’s electric vehicle registration share is expected to grow While historical light

vehicle registration data

shows that Norway might

reach an electric vehicle

sales share of 50 percent

Plug-in hybrid electric vehicle sales in China EVs as a share of light vehicle registrations in 2017 soon, several experts’

Battery electric vehicle sales in China 0.0% 10.0% 20.0% 30.0% 40.0% 50.0% outlook figures show that

900000

Norway 39.2%

China has the potential to

~ 770,000 PEV

sales in 2017

become the undisputed

800000 Sweden 6.3% leading market in terms of

125,000

700000 Netherlands 2.7%

EV sales by 2030.

652,000 Finland

The country has great

600000 2.6%

potential with combined

Number of units

500000

China 2.2% battery and plug-in electric

98,000

UK 1.7%

vehicle sales of around

400000 770,000 units and a

409,000

France 1.7% registration share of 2.2

300000 83,610 percent in 2017.

Germany 1.6%

200000 247,482

United States 1.2%

100000 New Zealand 1.1%

0 Canada 1.1%

2015 2016 2017

Note: Selected countries

Source(s): CAAM; IEA

49Battery-electric vehicle sales worldwide in the 1st quarter 2018, by brand

Sales in Q1 2018 in units

0 5000 10000 15000 20000 25000 30000

Tesla 27,529

BAIC 26,409

Nissan 22,666

JAC 11,597

Renault 10,482

Chery 8,193

VW 6,779

Zotye 5,640

Hyundai 5,494

Chevrolet 5,159

Note: Worldwide

Source(s): JATO

50Worldwide plug-in electric vehicle sales in 2018, by model

Sales in thousand units

0 20 40 60 80 100 120 140 160

Tesla Model 3 145.85

BAIC EC-Series 90.64

Nissan Leaf 87.15

Tesla Model S 50.05

Tesla Model X 49.35

BYD Qin PHEV 47.45

JAC iEV E/S 46.59

BYD e5 46.25

Toyota Prius PHEV 45.69

Mitsubishi Outlander PHEV 41.89

Renault Zoe 40.31

BMW 530e 40.26

Chery eQ EV 39.73

Note: Worldwide

Source(s): EV Sales; insideevs.com

51After production and

Tesla has ramped up its Model 3 deliveries after a slow start delivery volume targets

were missed in late 2017

and early 2018, the Model

3 has turned into Tesla’s

Model S Model X Model 3

best-selling model during

100000

the fourth quarter of 2018.

90000 As of February 2019, the

Model 3 is Tesla’s most

80000 recent model addition, as

the first units rolled off the

70000 assembly line in 2017. It

Number of vehicle deliveries

comes at a price tag of

60000 63,150 35,000 U.S. dollars (and

50000

up), thus targeting broader

customer segments than

40000 the Model S and Model X,

both of which are aimed

30000 1,550 towards the high-end

market segments. Tesla’s

13,120 14,050

20000 new Model Y was unveiled

in March 2019; production

10000

15,200 13,500 is expected to start in

0

2020.

Q4 2017 Q4 2018

5205 Revenue: The segments and regions of

growth

▪ Market growth

▪ Electric vehicle market size

▪ EV battery market sizeThe electric vehicle market is beginning to gain momentum The fact that electric car sales accounted for about two to three percent of overall light vehicle sales leaves great opportunities for growth for carmakers and automotive suppliers alike. Charging equipment manufacturers emerge as a third group of beneficiaries who can expect a golden age of electrified transportation. ▪ The United States and China are market leaders in terms of market growth, while Europe lags behind ▪ The electric vehicle battery market has enormous potential ▪ Wireless electric vehicle charging is set to revolutionize the sector 54

China’s rising affluence correlates with electric vehicle market growth The electric vehicle market

in the Asia-Pacific region is

expected to expand its

volume at a compound

annual growth rate of

Market volume CAGR between 2016 and 2026

40000

0.0% 5.0% 10.0% 15.0% 20.0% 25.0% 30.0% 35.0%

almost 30 percent

36,396.20 between 2016 and 2026.

35000

This comes as no surprise

Per capita income of urban households in China

31,194.80

Asia-Pacific 29.5%

considering the vast

30000

number of potential buyers

26,467.00

in this populous region,

25000 coupled with the rising

21,809.78

affluence of its growing

in yuan

20000 middle class.

17,174.65 North America 28.5%

15000

10000

Europe 23.2%

5000

0

2009 2011 2013 2015 2017

Note: Selected countries or regions

Source(s): National Bureau of Statistics of China; BIS Research

55Size of the global market for electric vehicles in 2017 and 2025

600

567.3

500

Revenue in billion U.S. dollars

400

300

200

118.86

100

0

2017 2025

Note: Worldwide

Source(s): Allied Market Research; PR Newswire

56Projected global wireless EV charging market size in 2020 and 2025 Wireless charging

infrastructure is

450 slated to be a game

changer

407

400 The wireless technology is

set to facilitate the

charging process, and

350

customers are expected to

welcome the

Market size in million U.S. dollars

300 seamlessness that will

accompany wireless

250

charging.

Evatran and WiTricity are

200

the leading providers in

this field.

150

100

50

8

0

2020 2025

Note: Worldwide

Source(s): MarketsandMarkets

5758

Market cap of lithium-ion battery component manufacturers worldwide as of September 2017

Market cap as of September 4, 2017 in million U.S. dollars

0 2000 4000 6000 8000 10000 12000 14000 16000 18000

Asahi Kasei 16,597

Toray 15,328

Mitsubishi Chemical 14,042

Sumitomo Metal Mining 9,946

Umicore 8,406

Mitsui Chemical 6,020

Hitachi Chemical 5,610

Ube Industries 3,016

Mitsui Mining & Smelting 2,982

Central Glass 922

W-scope 641

Nippon Carbon 436

Note: Worldwide

Source(s): Goldman Sachs; Various sources

59Global market share of lithium ion battery makers in the 1st quarter of 2018

Market share

0.0% 5.0% 10.0% 15.0% 20.0% 25.0%

Panasonic Sanyo 21.1%

CATL 14.41%

BYD 10.99%

LG Chem 10.59%

Samsung 5.57%

Note: Worldwide

Source(s): electrive.com

6006 Sustainability: The issues that need to

be tackled

▪ Transportation-related emissions

▪ Renewable sources in power generation

▪ Materials used in batteriesToday’s electric vehicles fall short of sustainability goals

While EVs clearly have the potential to outperform ICE cars in terms of fuel-related emissions, it is not easy to ascertain if electric

vehicles are environmentally sustainable, or not. There is no denying in the fact that all motor vehicles have an impact on the

environment, though.

▪ Questions about EVs financial sustainability aside, the key factors in gauging the sustainability of EVs include the following:

› type of energy used as a source of power

› battery material types

▪ Although electric cars have a smaller carbon footprint than gasoline or diesel-powered automobiles, a shift away from coal power will

be necessary to soften the transportation sector’s carbon footprint

▪ To date, battery supply chain sustainability has not been achieved due to the continued unsustainable mining of key materials,

including cobalt, lithium, and nickel

▪ The growing demand for those commodities that are used in the manufacture of electric vehicle batteries is likely to have an impact

on spot prices

62„

“ “(…) [E]lectromobility alone is not effective climate

protection. We need an energy transition alongside the

transport transition to truly improve our carbon footprint”

– Herbert Diess,

CEO of Volkswagen Group

63Rise in anthropogenic CO2 emission levels requires mitigation Since the second half of the 20th century,

the combustion of fossil fuels has led to the

release of unfettered volumes of carbon

dioxide (CO2) emissions into the

atmosphere. The resulting concentration of

41,396.8

Emissions in 2016 in kilograms per capita CO2 in the atmosphere continues to

0 1000 2000 3000 4000 5000

exacerbate what has been dubbed the

36,396.8 Total emissions 4,350 greenhouse effect: The earth’s surface

temperature rises because solar heat is

31,396.8 Electricity and

heat generation 1,805 absorbed by molecules of carbon dioxide

Emissions in million metric tons

26,396.8

and other greenhouse gases, including

Transportation* 1,059 nitrous oxide, methane, and water vapor.

21,396.8

Manufacturing industries

822

Higher surface temperatures have been

and construction

16,396.8

linked to rises in sea levels, stronger

Residential 254 hurricanes, and changes in precipitation

11,396.8 patterns.

Other energy

214

6,396.8

industries own use** The transportation sector contributes some

Commercial and eight gigatons of carbon dioxide

113

1,396.8 public services equivalents worth of emissions globally4.

Under the auspices of the UN, 197 ratifiers

-3,603.2

have thus agreed to mitigate vehicle-

related fuel combustion CO2 emissions by

replacing ICE vehicles with EVs.

Note: Worldwide

Source(s): IEA, Global Carbon Project

* Includes international bunkers in transport sector. ** Includes emissions from own use in petroleum refining, the manufacture of solid fuels, coal

64 mining, oil and gas extraction and other energy-producing industries.Conventional sources represent ~ 90 percent of the power mix About 40 percent of electricity generation

worldwide comes from the combustion of

coal. In order to be environmentally benign,

EVs need to make use of as little coal

power as possible because of the severe

14.0%

11%

12.1% health effects caused by its combustion. If

Share of renewables

12.0% 10%

8.6% 9.2% renewable sources are used as the primary

10.0% 8%

8.0% 5.9% 6.1%

6.9% source of power though, the widespread

5.2% 5.3%

6.0% adoption of electric cars is predicted to

4.0% reduce GHG emission levels in a significant

2.0%

manner.

0.0%

2007 2009 2011 2013 2015 2017 Although the share of renewable power in

electricity generation has more than

doubled over the past decade, electricity

generated from coal, oil, gas, nuclear, and

5.39 conventional hydro sources still accounts

in metric tons of carbon

GHG emissions in2017

4.76 for almost 90 percent of power generation.

Transportation sector

dioxide per capita

4.04 4.03

Therefore, the current power mix is unlikely

2.04

to lessen the carbon footprint associated

1.99 1.85

with emissions from the transportation

sector.

U.S. Canada Australia Saudi Arabia South Korea Germany France The transportation sector in the United

States produced the highest volume of

GHG emissions per capita in 2017, when

the U.S. car parc comprised almost 270

Note: Worldwide million vehicles.

Source(s): Enerdata; Climate Transparency; UNEP; Bloomberg New Energy Finance; FS-UNEP Collaborating Centre

Large hydro is not considered a renewable energy source in this data set.

65Power mix continues to affect the carbon footprint of EVs The increased use of electricity from

renewable sources softens EVs’ carbon

footprint, but electric car owners need to

make an active choice to recharge where

2017 share of coal power 2017 share of electric

generation worldwide vehicle stock worldwide coal is not used as the primary energy

China 44.8% 39.5% source. However, this choice is not an easy

United States 13.5% 24.5%

one to make, considering the complex

Japan 3.5% 6.6%

nature of the energy market with all its

regional regulations. Ultimately, it is the

Germany 2.5% 3.5%

share of coal power in a country’s

Netherlands 0.3% 3.8%

electricity mix that determines the carbon

UK 0.2% 4.3%

footprint of its EV fleet unless motorists

France* 0.1% 3.8%

select charging stations with low coal levels

Norway** - 5.7%

in the power mix.

China has the largest EV fleet, but also the

CO2 emissions in g/mile highest share of coal in its energy mix.

0 50 100 150 200 250 300

Norway’s EV fleet has shown impressive

EVs in China 188.5 growth and the country’s coal use is

EVs in the U.S. 147.5 nonexistent, but Norway’s overall car

EVs in Japan 142.7 market is small: Norway saw passenger car

EVs in Germany 140.4 sales of under 150,000 units in 20185.

EVs in the UK 76.2

France seems to be well prepared, but its

EVs in France 2.7

dependence on nuclear power has led

Gasoline vehicles 248.5

some experts to question the sustainable

viability of the French EV market.

Note: Worldwide

Source(s): IEA; BP; Statista; Bloomberg New Energy Finance; World Economic Forum

Coal power: * The value for France (10.52 TWh) is for 2016; was taken from IEA's website, as this country was not listed.

** The figure for Norway (146 GWh) is for 2016; it's based on information on IEA's website, as this country was not listed.

66Cobalt share of materials as of 2018

Cobalt remains a critical ingredient

0 5 10 15 20 25 30 35 40 45 in most battery types

A growing electric vehicle industry is

LCO 39 expected to spur the demand for several

materials, most notably cobalt, lithium, and

nickel.

NMC-111 13 The composition of these commodities

varies among the different types of lithium-

ion batteries that are used in electric cars,

NMC-433 11 most notably nickel manganese cobalt

(NMC) batteries.

Currently, most electric vehicles are

NMC-532 8 equipped with NMC-111 batteries. In 2018,

cobalt accounted for around 13 percent of

materials used in NMC-111 batteries, while

NMC-622 7 lithium cobalt oxide (LCO) batteries

reached the highest level of cobalt with

about 40 percent.

NCA 6

NMC-811 4

Note: Worldwide

Source(s): Bloomberg New Energy Finance; Bloomberg

NMC: nickel manganese cobalt; LCO: lithium cobalt oxide; NCA: nickel cobalt aluminum

67Africa and the Middle East Americas Asia-Pacific Europe Regional breakdown

1600 of battery electric

vehicle sales shows

Asia-Pacific’s

1400

dominance

The tremendous growth in

1200 electric vehicle sales that

has already occurred

globally is slated to trigger

Vehicle sales in thousand units

1000

worldwide demand for the

various commodities used

in electric vehicle

800

batteries, too.

600

400

200

0

2012 2018

68Lithium-ion batteries will likely drive lithium consumption

Battery consumption Other

600 160000

509

Consumption in metric tons lithium carbonate

140000 134,897

500

118,505

120000 111,585

Demand in kilotons of LCE

400 100,942

100000

96,668

equivalent

24.7%

CAGR 77,821

300 80000

64,398

60000

200

39,463

40000

29,058

100

87 20,026

20000

0 0

2017 2025 2008 2010 2012 2014 2016

Note: Worldwide

Source(s): McKinsey; Roskill

69Battery-related demand for cobalt drives Congolese cobalt production The batteries segment

within the global cobalt

market is expected to see

a compound annual

Share of global production in 2017 growth rate of just over 15

0.0% 10.0% 20.0% 30.0% 40.0% 50.0% 60.0% 70.0%

percent.

140

DR Congo 58.8%

Cobalt is often extracted in

Russia 5.14% regions where safe

Battery-related cobalt demand in kilotons of refined metal

120 117

Australia 4.59% working conditions are not

Canada 3.95%

always guaranteed,

100 including the Democratic

Cuba 3.86%

Republic of the Congo. An

80

Philippines 3.67% estimated 20 percent of

Madagascar 3.49%

Congolese cobalt comes

from the country’s artisanal

60 Papua New Guinea 2.94%

mining sector, where

Zambia 2.66% workers lack basic

38

40 New Caledonia 2.57% protective equipment,

exposing them to toxic,

South Africa 2.3%

20

metal-containing dust6.

United States 0.6%

Other countries 5.42%

0

2017 2025

Note: Worldwide.

Source(s): US Geological Survey; McKinsey

70Low-level battery-related nickel demand is forecast to grow Nickel is expected to be the EV battery

commodity yielding the highest compound

annual growth rate between 2018 and 2025

Primary nickel consumption in 2017 in thousand metric tons with 41 percent.

0 200 400 600 800 1000 1200 1400 1600 1800

However, the toxicity of this metal has

Stainless steel and special steels 1,562.2 sparked concerns about the negative

Alloys 171.2

impact of nickel mining on the environment

and production workers7.

Electroplating 149.8

While the metal manufacturing industry

Special steels 149.8 mainly uses low-grade nickel ores, the

more stable nickel sulfate is required for

Batteries 107 the manufacture of batteries. This might be

Other 21.4

the reason why batteries only accounted

for about five percent of primary nickel

consumption worldwide in 2017.

700 665

Consumption in thousand metric

600

500

400

tons

300

200

100 60

0

2018 2025

Note: Worldwide

Source(s): Norilsk Nickel; Various sources (Company data); UBS; Metal Bulletin

71Glossary BEV - Battery electric vehicles run only on electricity, using power from a battery. CO2 - Carbon dioxide is a greenhouse gas. EV - BEVs, FCEVs, PHEVs, and hybrid electric vehicles. EVSE - Electric vehicle supply equipment, or chargers, provide EVs with electricity. FCEV - Fuel cell electric vehicles run only on electricity, using power from a fuel cell. GHG - Greenhouse gases comprise methane, nitrous oxide, water vapor and carbon dioxide. GHG molecules absorb solar heat and thus lead to an increase in the earth’s temperature. Hybrid vehicles - Hybrid vehicles run mainly on gasoline or diesel, but have an electric motor as well. ICE - Internal combustion engines create energy from burning fossil fuels such as diesel and gasoline. MPG - Miles per gallon measure the number of miles a motorist can drive in a vehicle using one gallon. NMC batteries - Nickel manganese cobalt batteries, also abbreviated NCM PEV - Plug-in electric vehicles comprise PHEVs and BEVs, can be plugged in to charge from an off-board electric power source. PHEV - Plug-in hybrid electric vehicles run mainly on electricity, but have an ICE as well. Rechargeable batteries - In batteries, electricity is produced through the movement of electrons between anode and cathode. Rechargeable batteries function according to the same principle, but also have the ability to be recharged. xEV - BEVs and PHEVs 72

Footnotes 1 Share Now (2019): “Your Car is Always There”, retrieved from https://www.your-now.com/our-solutions/share-now 2Moia (2019): “Premiere am Rathaus: MOIA startet Testbetrieb”, retrieved from https://www.moia.io/de-DE/blog/premiere-am-rathaus- moia-startet-testbetrieb-in-hamburg/ 3 General Motors (2018): “Maven Joins City of Austin, Texas in Deploying All-Electric Shared Use Fleet of Chevrolet Bolt EVs”, retrieved from https://media.gm.com/media/us/en/maven/pressroom.detail.html/content/Pages/news/us/en/2018/mar/0302-maven-austin.html 4 IEA (2019): “CO2 Emissions Statistics”, retrieved from https://www.iea.org/statistics/co2emissions/ 5 Opplysningsrådet for Veitrafikken AS (2019): “Registreringsstatistikk”, retrieved from https://ofv.no/registreringsstatistikk?selectedDistribution=Fylkesfordelt&selectedMonth=12&selectedVehicleCategory=Personbiler&selec tedYear=2018 6 O‘Driscoll, Dylan; University of Manchester (2017): “Overview of child labour in the artisanal and small-scale mining sector in Asia and Africa “, retrieved from https://assets.publishing.service.gov.uk/media/5a5f34feed915d7dfb57d02f/209-213-Child-labour-in-mining.pdf 7 CDC (2018): “Workplace Safety and Health Topics: Nickel“, retrieved from https://www.cdc.gov/niosh/topics/nickel/default.html 73

Sources Alix Partners Electrive.com MarketsandMarkets Tesla Allied Market Research Enerdata Metal Bulletin Toyota Alternative Fuels Data Center Eurostat Merrrill Lynch UBS Automotive News EPA Moia UN Bank of America fka National Bureau of Statistics of China UNEP BCG Ford Nextmove.de US Department of Energy BIS Research FS-UNEP New York Times US Geological Survey Bloomberg General Motors Norilsk Nickel VDA Bloomberg New Energy Finance Global Carbon Project O‘Driscoll, Dylan Volkswagen BMO Capital Markets GlobeNewswire Oliver Wyman WIPO BP Goldman Sachs Opplysningsrådet for Veitrafikken AS World Bank Business Insider ICCT Power Electronics World Wood Mackenzie CAAM IEA PR Newswire World Economic Forum CDC IHS Markit PwC Chooseenergy.com IMF Qualcomm Citigroup Insideevs.com Renew Economy Climate Transparency JATO Roland Berger Consumer Affairs JP Morgan Chase Roskill Daimler KPMG Samsung EAFO McKinsey Share Now ECB L.E.K. Statista EIA LMC Automotive Strategy& 74

Recommendations Dossiers Electric vehicles worldwide Electric vehicles in the U.S. Electric vehicles in Italy Electric vehicle industry in the Netherlands Tesla Top lists Top 200 Companies: Electric Motors, Generators and Transformers Mobility Market Outlook Tesla (Passenger Cars) In-depth: eMobility Digital Market Outlook Ride Hailing 75

Authors, Imprint, and Disclaimer

Isabel Wagner

Senior Researcher

Isabel Wagner is the Statista

specialist for research on

transportation, metals, and

electronics in the U.S. She is

an expert for mobility-related

trend topics such as electric

and autonomous vehicles.

E-M ail: isabel.wagner@statista.com

Released: March 2019

Imprint

Statista, Inc. ▪ 55 Broad Street, 30th floor ▪ New York, NY 10004 ▪ +1 (212) 433 2270 ▪ www.statista.com

Disclaimer

Statista, Inc. shall not be liable for any loss, injury, claim, liability, or damage of any kind resulting in any way from (a) any errors in or omissions from the Statista, Inc. industry report(s) or

any Materials available or not included therein, (b) the unavailability or interruption of the Statista, Inc. industry report(s) or any features thereof or any Materials, (c) An Authorized User or

Member's use of the Statista, Inc. industry report(s), Online Services, or Materials, (d) the loss or corruption of any data or equipment in connection with the Statista, Inc. industry report(s), (e)

the content, accuracy, or completeness of Materials, all regardless of whether you received assistance in the use of the Statista, Inc. industry report(s) from a Covered Party, (f) any delay or

failure in performance beyond the reasonable control of a Covered Party, or (g) any content retrieved from the Internet even if retrieved or linked to from within the Statista, Inc. industry

report(s).

76You can also read