Energy Savings Performance Agreement - Tim Stoate, Vice President, Impact Investing - Share

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Energy Savings Performance Agreement

Tim Stoate, Vice President, Impact Investing

February 2014

About TAF Toronto City Council created the Toronto Atmospheric Fund (TAF) in 1991 First municipal climate agency in the world $23 million endowment for grants & mandate-related investments Independent (arm’s length)

Mandate Support local initiatives that significantly reduce greenhouse gas and air pollution Toronto’s GHG reduction targets are 30% reduction by 2020 and 80% by 2050

Why is TAF investing in energy efficiency? Almost 60% of GHG emissions are from buildings. TAF seeks to accelerate energy efficiency in the high-rise residential market by reducing financial regulatory and other barriers. More than 6500 buildings in GTA

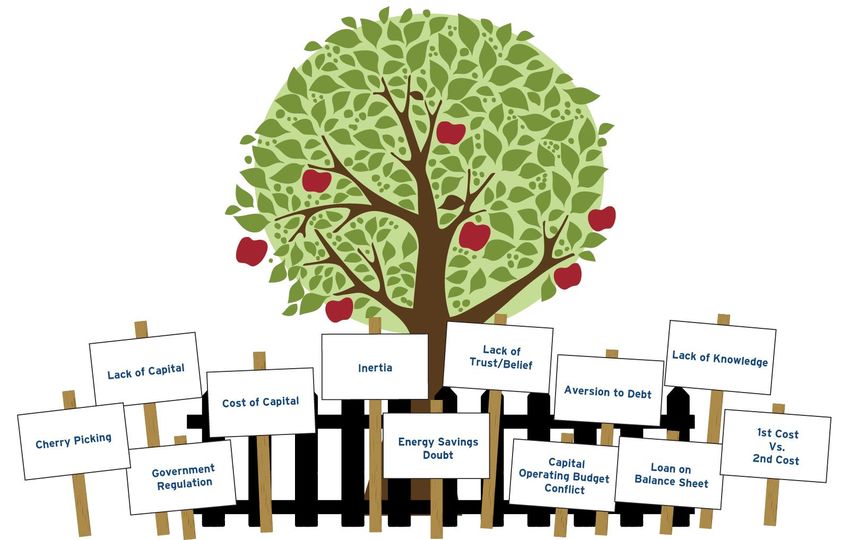

The low hanging fruit myth

Energy efficiency barriers

“What is the main barriers to pursuing

energy efficiency at your organization?”

• Lack of funding to pay for

improvements (37%)

• Insufficient Payback ROI (21%)

• Uncertainty regarding

savings/performance (11%)

6

Energy Savings Performance Agreement The ESPA is a new financing structure Essentially a service agreement It’s not a loan TAF will pay directly for a suite of energy efficiency measures Energy savings shared and insured Transaction minimum $250,000

ESPA vs. Loan ESPA Loan TAF pays up to 100% - building’s capital Building’s ability to attract capital protected reduced Non-debt and no lien on property Liability on balance sheet Transfers much of the risk of Responsible for technology changes ownership, technology changes and and equipment performance performance to TAF Building never pays more than savings Building can pay more than savings ROI to building virtually unlimited ROI could be lower but can’t be higher Borrowing by-law not required Borrowing by-law required Option to pre-pay after 3 years Pre-payment not always an option

Features and benefits Quality. Retrofit plan optimized for savings by TAF and insurer Commissioning and re-commissioning required to ensure that new equipment is installed and operating correctly Aligns stakeholders (building owners, investors, insurer, engineers)

Return from savings

Savings used to Pay Building Owner

Pre- Project

Energy Costs

Savings used to Pay TAF

Energy Costs ($)

Post-Project Energy Costs

Financing Term

Time

10Too good to be true? Energy audit is the responsibility of building owner - incentives pay for a portion (up to 50%) TAF earns a return! Pre-payment has “make-whole clause” – TAF has to make a minimum return

Harbourfront Centre $117,000 in financing 9 energy efficiency measures $54,000 annual energy savings 80% to TAF, 20% to Harbourfront 200 tonnes/yr of CO2 reduced

Robert Cooke Co-Operatives Homes $485,000 in financing 7 energy efficiency measures $70,000 annual energy savings 90% to TAF, 10% to Building 170 tonnes/yr of CO2 reduced

Thank You

Tim Stoate

Vice President, Impact Investing

tstoate@tafund.org 416-393-6368

Toronto.ca/TAFLooking for Honey in Other

Pots

Financing social economy projects,

the Québec

Experience

Regeneration forum, Toronto, Feb 11th 2014

15Le Chantier de l’économie sociale

Chantier de l’économie sociale: networks of collective

enterprises, local and regional development

organisations and social movements to promote and

develop the social economy

Recognition by Quebec government as a participant in

economic and social development

16Challenges

Many institutional barriers

Acces to capital

Undestanding of social economy

Commercialization strategies

Image of the social economy

17A first answer

Réseau d’investissement social du Québec:

A 12M$ fund

Contribution from:

Québec governement

Private entrprises:

Alcan

Groupe Jean-Coutu

Imasco

Caisse Desjardins

Banque Nationale, de Montréal et Royal

18A quick snapshot

Réseau d’investissement social du Québec:

• Technical assistance and capitalization components

484 projects

$11 million investment

Creation and maintenance of more than 6,000 jobs

Recreation and tourism, services, recovery-recycling,

solidarity commerce, culture, etc.

19Fiducie de Chantier de l’économie sociale

CES Trust

Contribution from:

Development Agency of Canada for the Regions of

Quebec : 22.8 M$

Fonds de solidarité FTQ: 12,0 M$

Fondaction CSN: 8,0 M$

Québec governement: 10,0 M$

Total : 52,8 M$

20Fiducie de Chantier de l’économie sociale

Operations Patient Capital

Real Estate Patient Capital:

21Fiducie de Chantier de l’économie sociale

Patient capital

Repayment in a single instalment after 15

years

Monthly paymnet of interst and fees

No security or any other guarantee

Real estate patient capital

Mortgage financing with a financial

institution

Guatentee by real estate mortgage

subordinated

22Fiducie de Chantier de l’économie sociale

Patient capital

32% in operating patient capital

39% Real estate patient capital

29% mix of both

23Housing Challenges

Need for community Housing

Response against « social bonds »

Response to the diminution of gouvernement

program

Beeing a actor in financing

24A limited partnership fund

With the actors of community Housing

In adition to governement program

Pilot of 1 200 units :

2013: 200 unités

2014: 500 unités

2015: 500 unités

31,5M$

25A limited partnership fund

Guarentee from the governement of Québec

Investments from union fund

Fonds de solidarité de la Fédération des

travailleurs du Québec (FTQ)

Fondaction, Confédération des syndicats nationaux

(CSN)

26A limited partnership fund

Integrated in the developpement program

AccèsLogis

Patient capital 15 years

Mortgage from a partner institution (SSQ a mutual

insurance group)

27 3 funds:

Réseau de l’investissement social du Québec (RISQ)

Fiducie du Chantier de l’économie social

Fond d’habitation – Capital patient

3 structures:

Non-profit organisation

Trust

Limited partnership

28 Many types of loans

Risk capital

Patient capital

Operating capital

Many investors

Governements

Private sector

Unions

2930

Looking for honey in other pots Presentation to HSC Regeneration Forum Derek Ballantyne 613-366-1169 info@communityforwardfund.ca 251 Bank Street, 2nd Floor, Ottawa, ON K2P 1X3 www.communityforwardfund.ca

Community Forward Fund

• A loan and financing fund for

Canadian nonprofits and charities

• Targets gap in access to patient

capital, working capital, bridge

financing and growth capital for the

sector

• Builds financial capacity through

financial reviews and coaching

services

• Works in partnership with regional

funds, foundations and other

community partnersCFF Organization Structure

Accredited Investors

Investment Assets Annual Return

Mgmt Fee

Community Forward Fund

Community Forward Fund

Assistance Corporation

(Concentra Trust)

(Registered Fund Manager)

Advise

Interest Payment

Loan Principal Principal Repayment

Loan RecipientsCommunity Forward Fund

• Operating since July 2012

• Registered for investors in 5 provinces

Lending Financial Capacity Building

• $7.8 million subscriptions • Introductory workshops

• $2.0 million commitments alternative financing

• $6.8 million loans approved • Site analysis

– 70 % drawn

• In depth financial reviews /

• 2012 return to investors 3.2%

clinicLoan portfolio • Detailed loan review process • Two-stage credit approval process • Provide secured and unsecured lending • Lending rates 5% - 8% • Average loan $270,000 • Average term 30 months

Housing loans • $ 2,500,000 – Project development funding – Participation in take-out lending – 80% secured on assets – Balance secured on cash flow or GSA • Significant demand – Complement to conventional lenders – Prepared to assess risk differently – Can lend when security on asset not possible

Investors

• Community Foundations / Private foundations

– Impact investors

• Local impact

• Social impact

– Return equal or above disbursement requirements

– Third party due diligence and loan managementSources of alternative financing • Community loan funds – Relatively small, close to capacity • Foundations – Challenge of diligence, loan monitoring – Limits related to concentration of investment class • Community bonds – Primarily retail investment, RRSP drive – Challenge of placement mechanisms • Structured investment / debt product

Why are good ideas not funded • Investor needs not always met – Ability to manage / cost of due diligence – Viable business plan – Quantum of risk exposure to asset class – Liquidity of investment • Limited number of intermediaries – Sufficient capitalization for housing – Can diversity investor risk – Provide investor liquidity – Generate on-going returns

You can also read