FOLLOW US ON TWITTER @COMPETITIONLAWS AND JOIN THE CONVERSATION USING #GLOBALANTITRUSTECONOMICS - CONCURRENCES

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Follow us on Twitter @CompetitionLaws and join the conversation using #GlobalAntitrustEconomics

Follow us on Twitter @CompetitionLaws and join

the conversation using #GlobalAntitrustEconomics

08.45 WELCOME REMARKS

Luis CABRAL I Chair, Department of Economics, NYU Stern School of Business, New York

Lawrence WHITE I Professor, Department of Economics, NYU Stern School of Business, New York

Follow us on Twitter @CompetitionLaws and join

the conversation using #GlobalAntitrustEconomics

09.00 OPENING KEYNOTE SPEECH

Noah Joshua PHILLIPS I Commissioner, US Federal Trade Commission, Washington, DC

Follow us on Twitter @CompetitionLaws and join

the conversation using #GlobalAntitrustEconomics

09.30 ANTITRUST IN SPORTS

Roger NOLL I Professor of Economics, Emeritus, Stanford University, Stanford

Andrew ZIMBALIST I Professor of Economics, Smith College, Northampton

Brad HUMPHREYS I Professor of Economics, West Virginia University, Morgantown

Rodney FORT I Professor of Sport Management, University of Michigan, Ann Arbor

Michael HAUSFELD I Partner, Hausfeld, Washington, DC

James KEYTE I Director, Competition Law Institute, Fordham Law School, New York

Moderator: Lawrence WHITE | Professor, Department of Economics, NYU Stern School of Business, New York

10.45 Coffee Break

Follow us on Twitter @CompetitionLaws and join

the conversation using #GlobalAntitrustEconomics

11.00 TELECOM MERGERS

Gail LEVINE I Deputy Director, Bureau of Competition, US Federal Trade Commission, Washington, DC

Tim BRENNAN I Professor of Public Policy & Economics, University of Maryland, Baltimore

Gregory ROSSTON I Senior Fellow, Stanford Institute for Economic Policy Research, Stanford

Dennis CARLTON I Professor of Economics, University of Chicago Booth School of Business, Chicago

John HARKRIDER I Partner, Axinn, New York

Cristina CAFFARRA I Vice President, Head of European Competition, CRA, London/Brussels

Moderator: Katja SEIM I Associate Professor of Business Economics and Public Policy, The Wharton School,

University of Pennsylvania, Philadelphia

12.15 Lunch

Follow us on Twitter @CompetitionLaws and join

BT/ EE (2015)

the conversation using #GlobalAntitrustEconomics

TeliaSonera/

Telenor TeliaSonera/

O2/Three (2014) (2015X) Tele2 (2014)

T-Mobile-Tele2 Vodafone/

O2/Three (2015) (2018) KDG (2013)

e-plus/ O2

Ziggo/LGI (2014) (2014)

Mobile and mobile Vodafone/Ziggo (2016)

Cable and cable

Hybrid mobile and cable/fixed Telenet/ Base (2015)

Network and content LGI/De Vijver (2014, 2019) Vodafone/LGI (2019)

LGI/KBW (2013)

Numericable/

SFR (2014) Orange//H3G (2012)

Sunrise/UPC (2019)

Bouygues/

Orange Three/ Wind (2016)

(2016, abandoned)

Cabovisao /

PTT (2015)

Orange/Jazztel (2014)

Altice/Media Vodafone/ Wind Hellas

Capital (2017) TIM/Vivendi/Mediaset (2012 – abandoned)

(2017)

Optimus/ ZON Vodafone/Ono (2014)

(2013)

Cellcom/Golan

(2016)

Follow us on Twitter @CompetitionLaws and join

the conversation using #GlobalAntitrustEconomics

01.45 PRICING ISSUES IN PHARMA: PAY-FOR-DELAY, PRODUCT

HOPPING...

Paul CSISZÁR I Director, European Commission - DG COMP, Brussels

David GILO I Professor of Law, Tel Aviv University, Tel Aviv

George ROZANSKI I Partner, Bates White, Washington, DC

Ingrid VANDENBORRE I Partner, Skadden Arps, Brussels

Jack PACE I Partner, White & Case, New York

Moderator: Robert WILLIG I Professor of Economics and Public Affairs, Emeritus, Woodrow Wilson School

of Public and International Affairs, Princeton University

03.00 Coffee BreakFollow us on Twitter @CompetitionLaws and join

the conversation using #GlobalAntitrustEconomics

03.15 IN-HOUSE COUNSEL SESSION: PLATFORMS

Samantha KNOX I Associate General Counsel, Facebook, San Francisco

Martin D’HALLUIN I VP, Associate General Counsel, News Corp, New York

David HIGBEE I Partner, Shearman & Sterling, Washington, DC

Boris BERSHTEYN I Partner, Skadden Arps, New York

Moderator: Harry FIRST I Professor, NYU School of Law, New YorkFollow us on Twitter @CompetitionLaws and join

the conversation using #GlobalAntitrustEconomics

04.30 CLOSING KEYNOTE SPEECH

Hal VARIAN I Chief Economist, Google, San Francisco

05.00 DrinksThe Seven Deadly Sins of Tech?

Hal Varian

NYU

May 2019

The views in this presentation are those of the author and do

not represent the views of his employer or any other party.alleged!

The /Seven Deadly Sins of Tech?

Hal Varian

NYU

May 2019

The views in this presentation are those of the author and do

not represent the views of his employer or any other party.The alleged seven deadly sins of tech

● Concentration

● Competition

● Innovation

● Acquisitions

● Entry

● Lock-in

● Fixed costsConcentration

Concentration

● Autor, et. al. (2017) describe two interpretations of concentration

increase

○ “...super-star firms with higher productivity increasingly capture a

larger slice of the market,”

○ “...arise from anticompetitive forces whereby dominant firms are

able to prevent actual and potential rivals from entering and

expanding.”

● Their conclusion: industries that became more concentrated were those

in which productivity increased the most

● Related findings by Ganapati [2017], Bessen [2017], OECD, and others.Competition

Where’s the competition in search? Follow the money.

● General purpose search is a tough business: you can only sell

6% of what you produce.

○ Just ask AOL, Ask Jeeves, Yahoo, Inktomi, Excite, Lycos…

○ Why? Only 6% of clicks are commercial clicks (ads)

○ Competition is intense for commercial clicks: Amazon,

eBay, Yelp, Travelocity, Expedia, Orbitz, Trip Advisor, and

thousands of comparison and review sites

● By contrast no one cares about non-commercial search from

an antitrust perspective: book search, scholar search, patent

search, encyclopedia search, etc.Why is competition intense for commercial clicks?

● Companies want users to go directly to them, so they try to build

a strong brand, good reputation. For example, now 54% of

shopping journeys in the US start on Amazon.

● Companies advertise heavily now so they don’t have to advertise

so much in the future.

○ The widespread use of apps (Amazon, Yelp, Maps) reinforce

this trend. Yelp gets 35M visitors via its mobile app.

○ This competition for commercial clicks is great for users.

● If Google provides great answers for [ancient history], people will

use Google to provide great answers to [sushi near me].Competition Tech firms compete intensely against each other. That’s why prices are low, and innovation is high.

Innovation

Innovation Tech companies are leading spenders on R&D. Source: Bloomberg

Innovation Tech companies are leading spenders on R&D. Even more if you group GAFA + Tech Source: Bloomberg

Acquisitions

Acquisitions by Google ● Median number of hires per acquisition: 6 ● 25% had 3 or fewer employees ● 75% had 18 or fewer employees ● These were primarily acqui- hires.

There are 5 times as many exits via acquisitions than IPOs

Silicon Valley BankEntry

Kill zone: where is it? ● Kill zone: “areas not worth operating or investing in, since defeat is guaranteed.” ● Google, Apple, Amazon, Microsoft, Facebook, China, Europe, and many others have all announced major AI initiatives. ● Surely no startup would want to enter this “kill zone”

Kill zone: where is it?

● Kill zone: “areas not worth operating

or investing in, since defeat is

guaranteed.”

● Google, Apple, Amazon, Microsoft,

Facebook, China, Europe, and many

others have all announced major AI

initiatives.

● Surely no startup would want to enter

this “kill zone”

● Or would they?

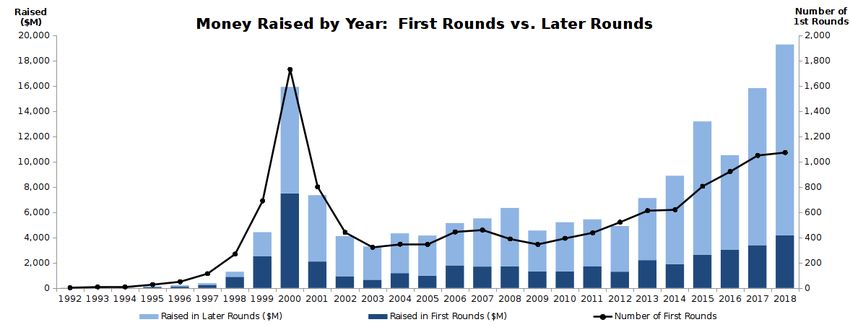

Source: AIindex.org 2018Entry: VC finance of US startups Source: Sand Hill Econometrics and VentureSource

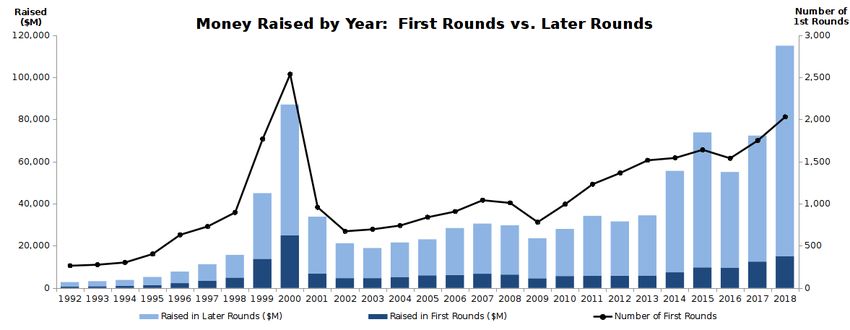

Entry: VC finance of European startups Source: Sand Hill Econometrics and VentureSource

Lock-in

Switching costs and data portability

● Google Takeout: June 2011

○ Download your data to

desktop, Gdrive,

OneDrive, Dropbox

● Data Transfer Project 2018

○ Transfer your data

between Google,

Facebook, Microsoft

Twitter… and others!

● Research

○ OpenImage (9.5M),

YouTube Video (8M),

and many othersFixed costs

Fixed costs 1999: data centers centers, hardware, software, networking. Much of the software was proprietary, internal to the data center operator, and needed to be re-developed for everyone who used the datacenter. Example: Map/Reduce, Hadoop, BigTable, BigQuery, etc. 2019: Tools are open sourced, standardized and available at data centers built by Google, Amazon, Microsoft, IBM, etc. Everyone has access to technology that only the richest companies could afford a decade ago. Image recognition, communications, coordination, etc. In fact, now anybody can offer a new search engine.

DuckDuckGo and Qwant ● DuckDuckGo uses 400 sources, and syndicates search results from Bing and Yahoo. It gets 45 million searches per month and has been profitable since 2014 ● Qwant does essentially the same thing, with 50 million unique queries per month, and is now the official search engine for the French government. ● Tech entrants no longer have fixed costs on the supply side. ● Fixed costs: that’s so 1990s, grandpa! ● But there is still a cost in attracting users: “Marketing fixed costs, though frequently overlooked, are often the more important of the two.” (Spence 1976.) ● Have to have a differentiator which in this case is privacy focus.

How to start up a startup

● Fund your project on Kickstarter ● Set up a Kaggle competition

● Hire employees using LinkedIn ● Use Nolo for legal documents

(company, patents, NDAs)

● Office space from WeWork ● Use QuickBooks for accounting.

● Cloud cloud computing and ● Use AdWords, Bing, Facebook for

network from Google, Amazon, marketing

Microsoft

● Use open source software like ● Use Salesforce for customer

Linux, Python, Tensorflow, etc relations

● Manage your software using ● Use ZenDesk for user support

GitHub

● Use Skype, Hangouts, Google Docs, ● Become a micro-multinational

for team communicationSeven sins or seven virtues? ● Concentration ● Competition ● Innovation ● Acquisitions ● Entry ● Lock-in ● Fixed costs

The End

Economic stats

● Most valuable stock

○ Amazon: currently less than 3% of the total value of all U.S. stocks

○ AT&T was 13% of total U.S. stock-market value back in 1932;

○ General Motors, 8% in 1928;

○ IBM, 7% in 1970.

● Revenue of top 4 companies

○ 1969: GM, Ford, GE and IBM totaled 5.4% of US GDP and 2.0% of global GDP.

○ 2019: Apple, Amazon, Google, and Facebook totals 2.9% of US GDP and 0.7 percent of GDP.

● Economic performance

○ “The tech/telecom/ecommerce sector has outperformed the rest of the non-health private sector

across a wide range of important economic measures since the tech boom started in 2007”

● What does tech provide?

○ Hi wages, low prices, rapid innovation

Source: WSJ, PPIFollow us on Twitter @CompetitionLaws and join

the conversation using #GlobalAntitrustEconomics

Thank you for coming!

Please give us your opinion about the conference

by answering the online survey.You can also read