FRENCH OUTLET CENTRE MARKET - February 2019 Outlets that stand out - Cushman & Wakefield Events

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

FRENCH OUTLET CENTRE MARKET Outlets that stand out February 2019

CONTENTS Key figures 2 Introduction 3 The European market 4 Existing stock 5 Projects 7 Performances 8 Challenges 9 Investment 10 Definitions 12 Cushman & Wakefield – French outlet centres - February 2019 1

KEY FIGURES FOR OUTLET CENTRES

26

Organised centres

(1 operator or more)

70% of which in the regions

480,000 sq m

French stock

2.5% of shopping centre stock

€153

Average basket in Europe

€310 for customers with high

purchasing power

6.3 sq m per

1,000 pop.

60% Density in France 2019

Share of boutiques selling 9.9 sq m in the

personal goods United Kingdom

15% Medium spaces

Sources: Cushman & Wakefield / Ecostra / Coniq

Cushman & Wakefield – French outlet centres - February 2019 2

INTRODUCTION

Brief history

Outlet centres first started to appear in France during the

1980s. Originally inspired by factory outlet stores that aimed

to sell part of their unsold production directly to the public,

outlet centres have gradually entered the market offering

products selling excess stock (old lines, seconds) at lower

prices than those found in traditional retail stores. These

centres have gradually evolved since their inception.

The first factory outlet centres appeared in traditionally

industrial areas with a high proportion of clothing

manufacturers, such as Troyes and Roubaix. The anarchic

development of these first-generation centres met with

mixed results and they were quickly replaced in the 1990s by

the first designer outlet centres or second-generation factory

outlet centres (“Marques Avenue” and “McArthur Glen” in

Troyes). These architecture and marketing of these concepts

improved and developers became more involved in site

management and promotion.

The third generation centres, inspired by the UK market,

appeared in the 2000s in new areas close to key areas for

tourism. The concept changed once again, adopting a more

playful architecture with the emergence of outlet villages –

one of the front-runners was “La Vallée Village” in Marne-la-

Vallée in 2000. The notions of “shopping for pleasure” and

“customer experience” were naturally incorporated into these

new centres. Merchandising was brought in alongside these

changes and centres were positioned at the high-end of the

market by promoting the quality of supply and the brands

available on site.

This trend grew in popularity over the 2010s with the arrival

of fourth-generation centres (outlet villages) that are

resolutely focused on labels and brands and build on

previous concepts by incorporating restaurant and leisure

areas as well as a range of services. The best examples of

these are recent openings in France and in Europe which

give this asset class a more upmarket image by focussing on

the premium/luxury end of the market.

With the sluggish economy affecting almost all distribution

formats, the “outlet centre” phenomenon stands out for its

vigour in terms of footfall, performance and investment

projects carried out by the main European operators.

Cushman & Wakefield – French outlet centres - February 2019 3

FRENCH OUTLET CENTRE MARKET

THE EUROPEAN MARKET

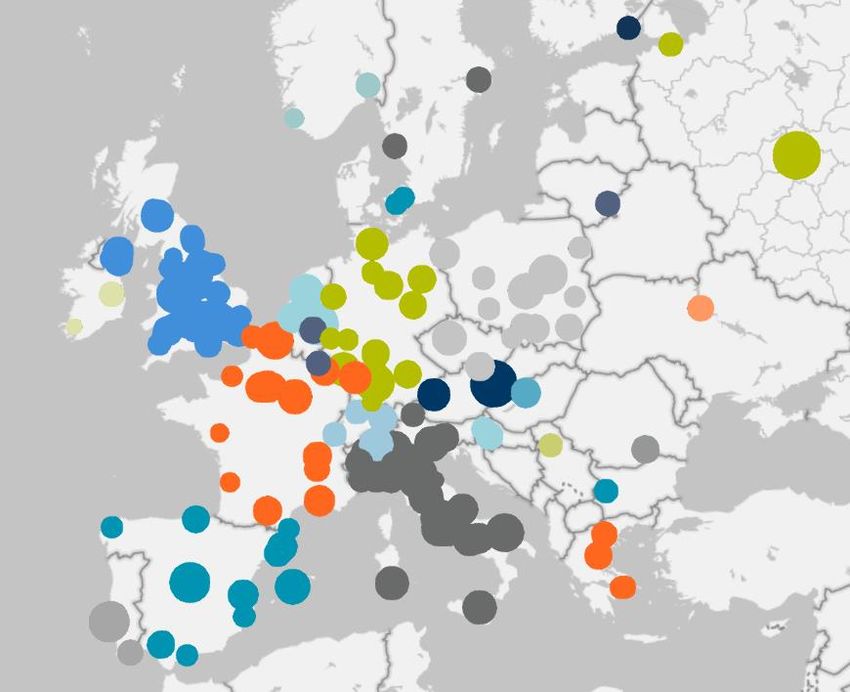

Continued growth in European stock Main outlet centre density in sq m per 1,000 inhabitants

The European outlet centre market was relatively active with in Europe, 2019

over 3.7 million sq m of GLA by the end of 2018, over more than

180 operational sites. Since 2016, the level of stock has risen

by +12% by volume ad +8% by number of sites. France is

ranked in third place in terms of the volume of space as well as

the number of centres - behind the United Kingdom and Italy

and just ahead of Spain and Germany. In terms of density,

France is in the lower end of the ranking with 6.3 sq m per

1,000 population and is far behind Portugal (13.9), Italy and the

United Kingdom. This performance is partially due to the

sector’s maturity, historical changes in industry and retail in

France, as well as a strict regulatory framework (AEC retail

authorisations that require an impact report, types of goods to

be sold). France’s position in this ranking is similar to its ranking Sources : Cushman & Wakefield, Ecostra, Oxford Economics

for shopping centres. The average floor space at French sites

stands at 18,000 sq m; this is in line with the median value for Main outlet centre polarities in Europe, 2018

Europe, but is below the average (21,000 sq m).

Good operator representation

The European outlet centre operator market has been largely

dominated by MCARTHURGLEN since 1995 with 23 centres

across Europe including 3 in France (Troyes, Roubaix and

Miramas). NEINVER comes in second place with 16 outlet

centres including “Roppenheim The Style Outlet” in France.

This Spanish operator has 6 centres on the Iberian peninsula

and also has centres across Europe, particularly in Poland

where it has 4 sites. NEINVER recently disposed of its logistics

assets to a fund managed by BLACKSTONE and is seeking a

purchaser for the rest of the group. This operator is planning

several openings in Europe, particularly the “Alpes The Style

Outlet” in 2020 in Châtillon-en-Michaille on the French-Swiss

border.

Source : Ecostra

Of the top-10 European operators, 5 have sites in France

including 2 that are exclusive to France: CONCEPTS ET

DISTRIBUTION-GROUPE MARQUES AVENUE, owners of the Main European outlet centres operators, 2018

historical brands Marques Avenue and Quai des Marques.

Open in France since 1993 (Troyes), the group currently runs 9

sites.

ADVANTAIL: One of the most recent operators (established in

2008), opened Nailloux Outlet Village in 2011. This group now

has 6 centres in France.

LA COMPAGNIE DE PHALSBOURG jointly with FREEPORT

have also entered the French market with the opening of “The

Village” in Villefontaine, near Lyon. FIMINCO and JMP

EXPANSION are expected to enter the market over the next

few years.

Source : Cushman & Wakefield, Ecostra

Cushman & Wakefield – French outlet centres - February 2019 4

FRENCH OUTLET CENTRE MARKET

EXISTING STOCK

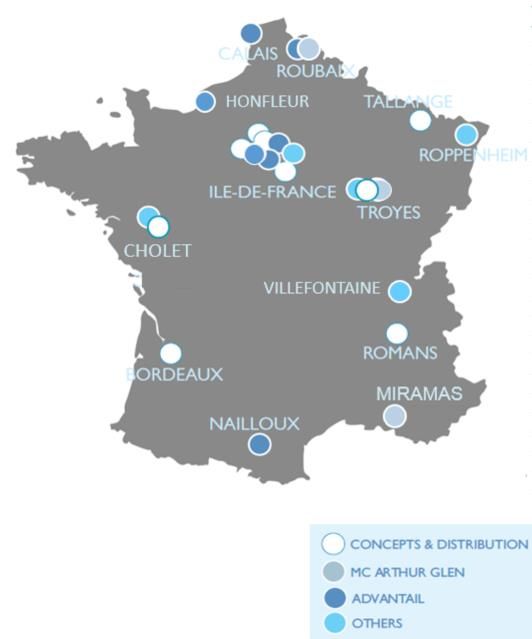

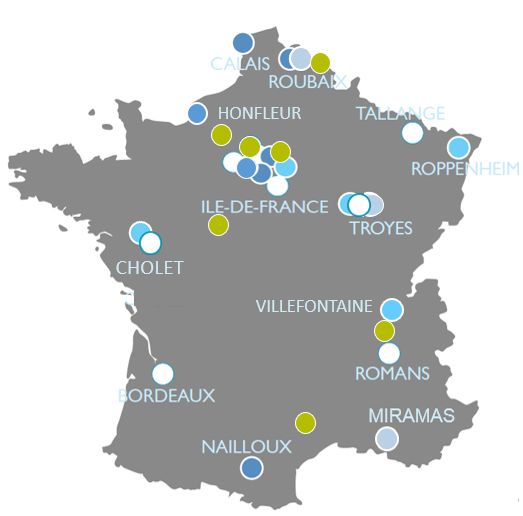

Locations of main existing French outlet centres

National coverage

• High concentration of sites in the Greater Paris Region,

around 1/3 of organised centres by floor area and by

number.

• French market dominated by Marques Avenue / Quai des

Marques (9 sites).

• Historic and developed centres run by several operators:

“Marques Avenue”, “McArthurGlen”, “Marques City” in

Troyes, “Circuit des Marques” and “Marques Avenue” in La

Séguinière.

• 22,000 sq m at “The Village” in Villefontaine which opened

in spring 2018. This was LA COMPAGNIE DE

PHALSBOURG’s first outlet site and particular attention

was paid to the site’s architectural concept - a key

characteristic of these 4th generation centres. This centre

will eventually attract 4 to 5 million visitors with a high

purchasing power, placing it in 2nd place among the most-

visited centres in France after “La Vallée Village”.

• The average vacancy rate varies by centre from 15% to

25%. For some sites, vacancy forms part of the retailer

renewal strategy and can vary significantly from one year to

the next with a high rotation of brands.

Source: Cushman & Wakefield / Magdus

Main outlet centres in France as at Q1 2019 (areas >10,000 sq m GLA)

Opening

Dpt City Name GLA Units Investor Operator / Developer

date

10 Saint-Julien-les-villas Marques Avenue Mode et Maison 31 000 140 1993 CIC/ AEW Concepts et Distribution/Marques Avenue

31 Nailloux Nailloux Outlet Village 30 950 136 2011 Klépierre Advantail

10 Pont-Sainte-Marie McArthur Glen 28 800 108 1995 Savills Investment Management Mc Arthur Glen

67 Roppenheim The Style Outlets 27 000 125 2012 Neinver / TH Real Estate Neinver

13 Miramas McArthur Glen 25 000 120 2017 Mc Arthur Glen Group Mc Arthur Glen

78 Les Clayes-sous-Bois One Nation 24 000 112 2013 Catinvest Catinvest

38 Villefontaine The Village 22 000 82 2018 Compagnie de Phalsbourg Compagnie de Phalsbourg, Freeport Retail

57 Talange Marques Avenue 21 735 79 1987 CNP Assurances (AEW Europe SGP) Concepts et Distribution/Marques Avenue

77 Serris La Vallée Village 21 400 112 2000 Value retail Value retail

78 Vélizy-Villacoublay Usine Mode et Maison 20 600 140 1986 Unibail Rodamco Westfield Advantail

91 Corbeil-Essonnes Marque Avenue A6 (ex-Art de Vivre) 20 100 111 2008 CNP Assurances (AEW Europe SGP) Concepts et Distribution/Marques Avenue

78 Aubergenville Marques Avenue A13 20 000 61 2015 Altarea Cogedim Concepts et Distribution/Marques Avenue

59 Roubaix L'Usine 18 550 74 1984 Primonial Reim Advantail

59 Roubaix McArthur Glen 17 000 60 1999 Savills Investment Management Mc Arthur Glen

95 Gonesse Usines Center Paris Nord 2 16 500 110 1985 CNP Assurances / AEW Europe SGP Advantail

10 Pont-Sainte-Marie Marques City 15 000 20 1990 nc nc

95 Franconville Quai des Marques A15 14 915 95 1989 CNP Assurances (AEW Europe SGP) Concepts et Distribution/Marques Avenue

26 Romans-sur-Isère Marques Avenue 14 800 70 1999 AEW Europe SGP (Nami Investment) Concepts et Distribution/Marques Avenue

93 Ile-Saint-Denis (L') Marques Avenue 14 500 70 1985 CNP Assurances (AEW Europe SGP) Concepts et Distribution/Marques Avenue

49 Séguinière (La) Circuit des marques 14 267 51 1989 indépendants indépendants

62 Coquelles L'Usine Channel Outlet 13 850 57 2003 Primonial Reim Advantail

14 Honfleur Honfleur Normandy Outlets 12 000 70 2017 Resolution Property Advantail

33 Bordeaux Quai des Marques 12 000 44 2004 Affine Concepts et Distribution/Marques Avenue

49 Séguinière (La) Marques Avenue 11 800 62 2005 Klépierre Concepts et Distribution/Marques Avenue

Sources : Cushman & Wakefield / Ecostra / Magdus / Codata

Cushman & Wakefield – French outlet centres - February 2019 5

FRENCH OUTLET CENTRE MARKET

EXISTING STOCK

Retail activities Mix-merchandising in outlet centres, % by activity

Most of the activity represented in outlet centres is traditionally

concentrated in personal goods sector (clothing, shoes, leather

goods, sportswear) as well as household goods (tableware,

linen, small electrical). Since 2014 and driven by American

outlets, department stores have started to appear in the outlet

market with the opening of a GALERIES LAFAYETTE Outlet in

the Paris region (“One Nation”) then outside Paris with

“Marques Avenue” La Séguinière and “Nailloux Outlet”. This

retailer now has stores in 10 sales outlets and should continue

to develop its network in French outlet centres. LE

PRINTEMPS Outlet followed with an opening at

“McArthurGlen”, Miramas in 2017. In just a few years, these

sites have taken the proportion of medium-sized units from 6%

to 10% just as few years ago, to the current 15% to 20% of the Source: Cushman & Wakefield

overall floor space. These are primarily dedicated to personal

goods (ready-to-wear clothing, shoes, sportswear). Following Change in outlet centre stock, in 000 sq m (excluding

the same trend seen for traditional shopping centres, the food- renovations)

and-beverage sector has gradually made its way into outlet

centres. Originally, it was introduced to meet the needs of

customers that can sometimes live up to 150km away and who

wish to spend all day on site. The proportion allocated to this

sector has therefore grown alongside the development of 4th

generation centres and now accounts for 5% to 10% of the

overall floor space in outlet centres. Leading supermarket,

CARREFOUR EXPRESS made its first appearance at “One

Nation” in 2018 over 150 sq m.

Changes in stock

The outlet centre market has seen progressive and relatively

linear growth since its origins in the 1980s. As at the end of

Source: Cushman & Wakefield

2018, the overall volume of floor space in France stood at

480,000 sq m across 20 sites which equates to just under 2.5%

of shopping centre stock. This is therefore a highly specific Changes in annual openings by type, in 000 sq m

market due to the restricted and exclusive network. By 2025, an

additional 200,000 sq m is expected to be completed, taking the

overall volume to around 670,000 sq m. As for any retail

project, it is likely that some of this space will be postponed or

even cancelled. As this is a relatively recent concept, the most

openings were new space creations (average of 90% in 2017).

Some centres have expanded since the 2000s, driven by

turnover growth and changes in the retail landscape. These

extensions have been for fairly limited spaces with an average

of around 2,900 sq m per site.

Source: Cushman & Wakefield

Cushman & Wakefield – French outlet centres - February 2019 6FRENCH OUTLET CENTRE MARKET

PROJECTS

Main projects

Outlet centres - main projects due in 2019 / 2021

Opening

Dpt City Name GLA Units Type of scheme Operator / Developer

date

93 Romainville Paddock 20 000 90 2019 Création Fiminco

12 La Cavalerie Viaduc Village 7 500 45 2019 Création Faubourg du Commerce

1 Châtillon en Michaille Alpes The Style Outlets 19 000 93 2020 Création Neinver

59 Hautmont Escale 19 950 nc 2021 Création JMP expansion

27 Douains Mac Arthur Glen 20 000 100 2021 Création Mc Arthur Glen

78 Aubergenville Marques Avenue A13 10 000 42 2021 Restructuration Altarea Cogedim

Sources : Cushman & Wakefield / Ecostra / Magdus

Location of the main outlet centres, existing and Projects of outlet centre openings over the medium

projects term, in 000 sq m

Source : Cushman & Wakefield

Sources : Cushman & Wakefield / Magdus

National network continues to expand

• Increase in supply in Normandy (Douains) and the Centre region by 2021 (Sorigny).

• Improved coverage in the border areas of the North and the East which will also attract customers from Benelux, Germany

and Switzerland (Châtillon-en-Michaille).

• New project to the North/East of the Greater Paris Region in Romainville on the Zac de l’Horloge: “Paddock”, 20,000 sq m

(2019).

• Downward revision of extension and refurbishment projects, with around 16,000 sq m of additional space over the next 3

years (Honfleur, Aubergenville)

• This sector is not growing as quickly as in the past and the rate of openings is set to slow: annual growth is estimated at +6%

from 2015 to 2025 compared with +10% from 1990 to 2015.

• 2 new project creations in 2019: “Paddock” in Romainville and “Viaduc Village” in Cavalerie (7,500 sq m).

• Longer term, further projects have been announced for areas that currently have no coverage: Brittany (Dinard) and in the

centre of the country (Clermont-Ferrand).

Cushman & Wakefield – French outlet centres - February 2019 7FRENCH OUTLET CENTRE MARKET

PERFORMANCE

Sales turnover Rental values

According to Ecostra’s 2018 outlet centre report, the top 3 Rents are generally made up of a fixed rent and an

centres in terms of performance in France were “La Vallée additional variable rent which is calculated as a % of the

Village” in Marne-la-Vallée (joint 8th place in the European turnover generated - either from the 1st €1, or when a

ranking), “Marques Avenue” in Romans-sur-Isère (13th certain threshold is reached. The 1st year’s turnover

place) and “Roppenheim The Style Outlet” (27th place). For normally acts as a guide for setting the fixed rent for the

the 1st time in 10 years, German centre “Outletcity following year.

Metzingen” seized the top spot, overtaking “McArthurGlen

Rents (excluding key money and charges) range from €180

Roermond” (Netherlands) which had been number one

to €320 per sq m per year) depending on the sector

since 2015.

(excluding extreme values).

There are some wide disparities in turnover between sites.

Apart from medium-sized units, the highest rents are

However, from the available references, the best sales

generated by boutiques in sectors that are still poorly

performances (>4,000 sq m sales area) are normally seen

represented in terms of floor space: health and beauty has

for sites in the Paris region and established regional sites

the highest rents and food and beverage the lowest. The

with a loyal customer base. The average sales performance

traditional sectors for outlet centres fall in the mid-range for

for outlet centres has remained stable for several years at

this sample and at a similar level: personal goods,

around €3,800 per sq m. By sector, there is some

household goods and sports and leisure. The average rent

considerable variation in terms of values from €2,500 per sq

for these sectors stands at around €280 per sq m.

m to €5,500 per sq m (excluding extremes). In the top spot,

medium-sized units (>500 sq m) which are mainly allocated This means that the average effort rates range from 8% to

to personal goods, can reach over €7,000 per sq m. This 15%, all sectors combined. Rates are lower for medium

analysis, based on a sample of around twelve centres, spaces which are normally under 10%. On top of rents,

excludes the “non-standard” results recorded at “La Vallée rental charges are far from negligible for these types of

Village” where the average performance is significantly units (particularly marketing costs), even though

higher. negotiations do often lead to landlords agreeing to take on

some of these costs themselves.

Top 5 European outlet centres according to retailers, Ratio between average rents and turnovers, €/sq m/year,

2018 2018

Source : Ecostra Source : Cushman & Wakefield

Cushman & Wakefield – French outlet centres - February 2019 8FRENCH OUTLET CENTRE MARKET

CHALLENGES

From outlet centres to villages …

Broad and fairly young customer base, Crucial role of digital

in search of good bargains Originally used by customers for price

(data: Magdus - Xerfi / Opinion Way report for Neinver / Coniq)

comparison, the internet has become a

genuine income-generating marketplace.

• The consumer profile for outlet centres is mainly the 30 to 55 age

bracket with a high proportion of women (65%). Outlet centre brands have strengthened

their on-line presence and improved the

• 52% of the French population, or 26 million people, claim to be user experience on their websites:

familiar with the outlet shopping concept, particularly women and

those living in the Greater Paris Region. • Marques Avenue has created an

e-magazine which is regularly updated

• Visitor frequency is three to four visits per year, mainly at with special offers and TV adverts

weekends, on public holidays and during sales periods.

• “thevillageoutlet.com” has been launched

• 10 million French consumers (20%) currently plan to visit an outlet with instant discounts for on-line

centre for recreation and 9 out of 10 shop while on holiday. purchases; customers may also use the

personal shopper service.

• Bargain hunting was the main motivation for customers visiting

outlet centres. A social media presence is now a necessity:

Instagram and Facebook play a major role in

• 38% of clothing is purchased during sales or promotions; this brand communications.

proportion is rising.

As in traditional retail, the physical

• 34% of European outlet centre turnover is generated by customers introduction of digital technology into stores

with a high level of purchasing power whose average basket is becoming widespread, particularly for

stands at €310, compared with an average centre basket of €153. cash-free and card-free payments (Alipay in

La Vallée Village).

• Chinese customers account for 60% of the tourist turnover

generated by European outlet centres.

Customer experience and shopping for pleasure

• Improvements to the architectural and environmental quality of sites as well as the consideration of ecological criteria

and sustainable development: “Marques Avenue A13”, a leading French retail complex, has a timber construction

and is certified as “Excellent” under BREEAM International 2013; “Roppenheim The Style Outlet” is also certified as

“Outstanding” under BREEAM for its rainwater-recovery system and finally “The Village” in Villefontaine which is HQE

certified and won the international “Best Outlet Center” award in 2018.

• Creation of themed, fun events, makeovers, photo shoots, … Partnership development with tour and transport

operators (airlines, bus companies, car hire, specialist media), cultural patronage.

• Stronger leisure and restaurant offering to prolong dwell time and improve the attractiveness of sites, particularly for

tourists.

• Development of stores and brands offering goods traditionally located in other types of centres: jewellery, sports

equipment, food (e.g. La Comtesse du Barry at Marques Avenue), perfumes and cosmetics (Nail bars, Clarins,

Rituals, …), convenience stores (Carrefour Express).

• Change in positioning to be more upmarket with an improved premium and luxury offering to compete with traditional

centres that focus on a mass-market clientele.

• Development of services: welcome desks, tax-free shopping, loyalty cards, concierge services, valet service, repairs,

personal shopper, transport (car sharing, public transport), ...

Cushman & Wakefield – French outlet centres - February 2019 9FRENCH OUTLET CENTRE MARKET

INVESTMENT

Volume in line with the scale of stock Invested volume in outlet centres in Europe and share

of France in the European market, € million

As this is a limited sector, the investment market for outlet

centres is a micro-market compared with retail real estate. In

2017, it accounted for 1.9% of the overall European retail real

estate investment market; this is just over the average

recorded for the last 10 years (1.1%). With over €900 million

in investments since 2009, France plays an important role in

the European market and French transactions accounted for

17% of the overall transaction volume for the outlet centre

segment in Europe.

Given the stock limitations (volume and number of sites), the

rate of transactions is erratic and varies in line with the

availability of market opportunities. This inconsistency

differentiates this niche market from traditional retail Source : Cushman & Wakefield, RCA

(shopping centres, retail parks) where supply is more

important. In France in 2018 SAVILLS INVESTMENT Share of outlet centre in retail investment (excluding

city centre), € million

MANAGEMENT carried out 2 acquisitions for “McArthurGlen”

centre in Roubaix and Troyes for about €300 million. This

volume broke the 2016 record which was set by the same

assets, although for a lower amount. This volume represents

a substantial proportion of the transactions recorded in

Europe in 2018 (62%).

For the last 10 years, the proportion of outlet centres in the

retail investment volume (excluding city centres) has also

followed an erratic path ranging from 0% to above-average

(3.8%) levels in 2010, 2013, 2016 and 2018.

Restricted investor panel

Several outlet centres have changed hands over the last 2

Source : Cushman & Wakefield

years. Firstly, “Usine Channel” in Coquelles and “L’Usine” in

Roubaix which were acquired by PRIMONIAL REIM in 2017 Main owners of outlet centres in France in 2019

from UNIBAIL-RODAMCO and, more recently, the

“McArthurGlen” centres in Troyes and Roubaix by SAVILLS

INVESTMENT MANAGEMENT. These transactions have led

to the arrival of new entrants as well as to the withdrawal of

others in the European rankings of investors for this asset

class. In terms of the number of centres, AEW EUROPE

SGP (and the funds it represents) clearly stand out as the

most-active investors in the French market.

Source: Cushman & Wakefield

Cushman & Wakefield – French outlet centres - February 2019 10FRENCH OUTLET CENTRE MARKET

INVESTMENT

Steady yield convergence Yield evolution in outlet centre market in Europe, in %

Yields for the European outlet centre segment have

followed the same pattern of compression seen for

traditional shopping centres. After having been close to 7%

in 2008, levels are now under 5%. This is however a more

gradual and linear change that indicates resilience to

market fluctuations, which are often more extreme than for

shopping centres. The gap with the best yields for

shopping centres has fallen by 50 bps and has stabilised at

1.25% since 2016 meaning that the best assets in the

French market are now at the same level as prime Italian

shopping centres.

The introduction of changes in merchandising mix and

architectural concepts to the latest-generation outlet

centres should further support yield convergence with

Source : Cushman & Wakefield

traditional shopping centres.

In summary

Although the development of outlet centres has been relatively erratic, this is a niche sector

that benefits form specific characteristics that offers several advantages, particularly for

investors:

• Very wide catchment areas (over 1 hour 30 journey time by car)

• Mainly occasional customers with a fairly high average purchase value

• Concept based on reduced prices, more resilient to changes in the economic climate

and consumption

• Attractiveness just as powerful as sales in physical stores or on-line offers.

• Generally low running costs, close to those seen for retail parks

• Rents more directly correlated to retailer performance than in shopping centres.

• A distribution and stock-depletion outlet for manufacturers that enables high sales

volumes

• Source of attractiveness and tourism for the regions and municipalities concerned.

• Very good returns for investors.

Cushman & Wakefield – French outlet centres - February 2019 11DEFINITIONS

Shopping centre: Defined as a grouping of at least 20 shops Floor space: has replaced SHON (or net floor area) since 1

and services with a minimum GLA of 5,000 sq m, conceived, March 2012. Total enclosed and covered floorspace with a

built and managed as one entity. ceiling height of over 1.80 metres. This is calculated based

on the bare interior of the facades.

Super-regional shopping centres: Shopping centres with a

GLA over 80,000 sq m and/or at least 150 shops and Prime yield: Expressed in %, a ratio of rents exclusive of

services. charges and the AEM acquisition price of the asset (New or

refurbished building, on long lease terms). The lowest level

Regional shopping centres: Shopping centres with a GLA

of profitability seen over a given period, after eliminating

over 40,000 sq m and/or at least 80 shops and services.

abnormal values (less than two occurrences).

Factory outlets / Outlet centres: originally shops attached

CNCC : The Conseil National des Centres Commerciaux

to manufacturing sites that offered discount pricing, end-of-

(National Council of Shopping Centres), the professional

line products, old lines or over supply.

body grouping those involved in the promotion or

development of shopping centres: developers, landlords, Factory outlets are precisely defined under Article L310-4 of

centre managers, retailers, service providers and the retail code: “The designation of shop or factory outlet

shopkeeper groups. can only be used by manufacturers selling part of their

unsold production from the distribution network or returns

Large shopping centres: Shopping centres with a GLA over directly to the public. To justify reduced pricing, these direct

20,000 sq m and/or at least 40 shops and services. sales are exclusively for products from the previous sales

season”.

Shopping centre footfall index: To measure shopping Specialist shopping centres tend to forgo the factory outlet

centre footfall, the CNCC has monitored a panel of 102 name in favour of designer outlet centre or outlet village, a

shopping centres equipped with a counting system since retail definition that has no legal standing, thereby

October 2006. This panel is made up of regional shopping assimilating the latter into traditional retail.

centres (4%), large shopping centres (53%) and small

shopping centres (23%). Out-of-town retail: Group of stores sited in suburban

locations. These may be shopping centres, themed centres,

Shopping centre performance index: Monthly analysis of retail parks, specialised stand-alone medium spaces or

shopping centre turnover conducted by the CNCC by type of medium-sized food stores. Out-of-town retail competes

shopping centre and by sector. The panel, updated every with city-centre retail.

year, currently includes 180 centres and covers 10,000

shops.

Small shopping centres: Shopping centres with a GLA of

over 5,000 sq m and/or at least 20 shops and services

Retail park : An open-air grouping of retail units that were

built and are managed as a whole. A park is over 3,000 sq m

SHON (built area) and consists of a minimum of five rental

units.

GLA: Total space leased to shopkeepers including the whole

of the space (sales + storeroom) with no deduction for

shafts or pillars and calculated from measured from the

centre of joint partitions to outside wall surfaces (Usage for

shopping centres).

Cushman & Wakefield – French outlet centres - February 2019 12AUTEURS Typhaine Gaillard Magali Marton Chargée d’Etudes Senior Directrice des Etudes +33 (0)1 86 46 10 94 +33 (0)1 86 46 10 95 typhaine.gailllard@cushwake.com magali.marton@cushwake.com CONTACTS Antoine Derville Christian Dubois Président Head of Retail Services France +33 (0)1 53 76 92 91 +33 (0)1 53 76 92 96 antoine.derville@cushwake.com christian.dubois@cushwake.com Jean-Philippe Carmarans Nils Vinck Vanessa Zouzowsky Head of Valuation & Advisory France Head of French Capital Markets Head of Retail - French Capital Markets +33 (0)1 41 02 71 11 +33 (0)1 86 46 10 19 +33 (0)1 86 45 11 05 jean-philippe.carmarans@cushwake.com nils.vinck@cushwake.com vanessa.zouzowsky@cushwake.com Disclaimer This report has been produced by Cushman & Wakefield LLP for use by those with an interest in commercial property solely for information purposes. It is not intended to be a complete description of the markets or developments to which it refers. The report uses information obtained from public sources which Cushman & Wakefield LLP believe to be reliable, but we have not verified such information and cannot guarantee that it is accurate and complete. No warranty or representation, express or implied, is made asto the accuracy or completeness of any of the information contained herein and Cushman & Wakefield LLP shall not be liable to any reader of this report or any third party in any way whatsoever. All expressions of opinion are subject to change. Our prior written consent is required before this report can be reproduced in whole or in part. ©2019 Cushman & Wakefield LLP. All rights reserve

You can also read