Full year results presentation Year ended 30 September 2017 - C

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Full year results presentation Year ended 30 September 2017 C

Disclaimer

For the purposes of this notice, "presentation" means this document, its contents or any part of it, any oral presentation, any question or answer session and any

written or oral material discussed or distributed during the presentation.

This presentation does not constitute or form part of any offer or invitation to sell or issue, or any solicitation of any offer to purchase or subscribe for, any securities in

the Company, nor shall any part of it nor the fact of its distribution form part of or be relied on in connection with any contract or investment decision relating thereto,

nor does it constitute a recommendation regarding the securities of the Company.

The information and opinions contained in this presentation are provided as at the date of this presentation and are subject to change without notice. In furnishing this

presentation, the Company does not undertake or agree to any obligation to provide you with access to any additional information or to update this presentation or to

correct any inaccuracies in, or omissions from, this presentation that may become apparent. You should make your own independent evaluation of the Company and

should make such other investigations as you deem necessary.

No representation or warranty, express or implied, is given by or on behalf of the Company its directors, officers or employees or any other person as to the accuracy

or completeness of the information or opinions contained in this presentation and no liability whatsoever is accepted by the Company or any of its members, directors,

officers or employees nor any other person for any loss howsoever arising, directly or indirectly, from any use of such information or opinions or otherwise arising in

connection therewith.

Certain statements, beliefs and opinions in this presentation are "forward-looking statements". These statements reflect the Company's, or as appropriate, the

Company's directors' current expectations and projections about future events. Such forward-looking statements involve risks, uncertainties and other important

factors beyond the Group’s control that could cause the actual results, performance or achievements of the Group to be materially different from future results,

performance or achievements expressed or implied by such forward-looking statements. Such forward-looking statements are based on numerous assumptions

regarding the Group’s present and future business strategies and the environment in which the Group will operate in the future. Forward-looking statements contained

in this presentation regarding past trends or activities should not be taken as a representation that such trends or activities will continue in the future. These forward-

looking statements speak only as of their date and the Group and its directors, officers, employees, agents, affiliates and advisers expressly disclaims any obligation or

undertaking to supplement, amend, update or revise any of the forward-looking statements contained in this presentation to reflect any change in the Group’s

expectations with regard thereto or any change in events, conditions or circumstances on which any such statements are based, except where it would be required to

do so under applicable law. As a result of these factors, you are cautioned not to place undue reliance on such forward-looking statements.

1

Highlights

• 35% increase in global pets on plan to 188,000 (2016: 139,000)

• 36% increase in Group continuing revenues to £2.53m (2016: £1.87m)

• 50% increase in contracted clinics now totalling 1,084 in UK, Europe and US

• 29% increase in the number of pets on plan in the UK to 156,000 (2016: 121,000)

• £5.9m net cash proceeds after transaction costs from sale of the Premier Buying Group

• £3.2m of cash at 30 September 2017 (2016: net cash of £0.4m)

• US challenges being addressed

Post Balance sheet highlight

• £1.5m committed funding facility agreed - provides security of funding and flexibility to consider alternative sources of

funding.

2

Business Fundamentals

• Sticky and diverse customer base

• Recurring revenue stream with compound growth

• Bespoke scalable IT platform underpinning international operations

• No bad debt exposure

• Growth opportunity underpinned by cooperation agreements (Mid- West, Zoetis, MVS, VPI, PSI, TVC, MSD France)

3

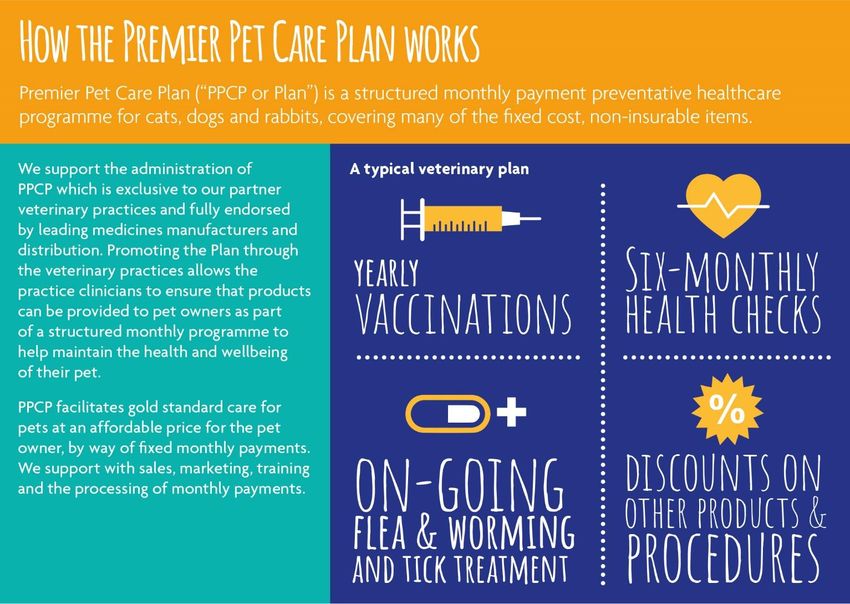

Premier Pet Care Plan

4

What are Preventative Health Plans?

Revenue streams come from:

• transaction fee per pet per month (Direct Debit,

SEPA, Credit card), plus

• set up fee per new pet plus

• practice set up fee plus

• manufacturer support fees

• Our service includes:

• Plan pricing

• Plan design

• Training and process integration

• Marketing

• Ongoing support and training

• Global IT platform and transaction processing

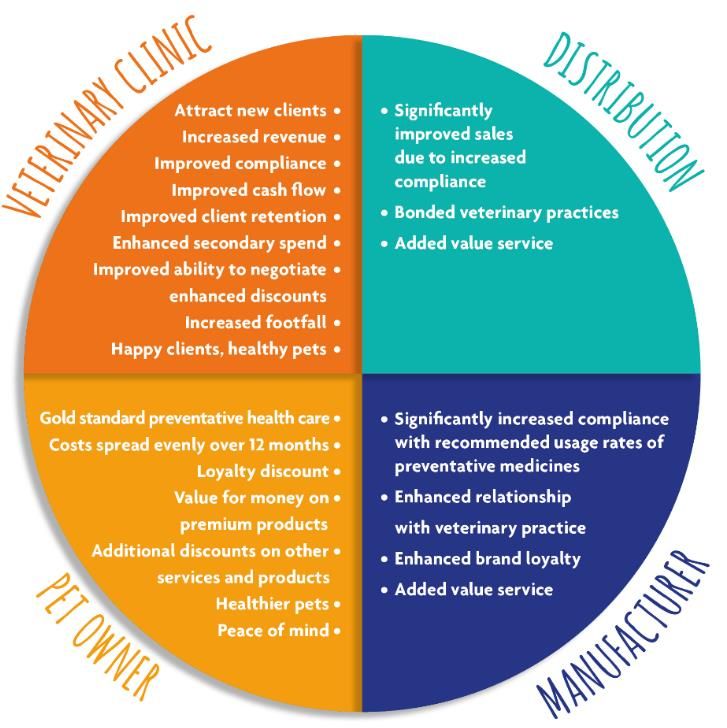

5Benefits of the Plan

All parties stand to benefit:

• Veterinary Clinics

• Distribution

• Pet Owners

• Manufacturers

6Strategy

7Global IT Platform

• Continued investment in Global IT

platform - £196k capex in FY 2017

Customer interface &

Data capture Global PCP Web Portal

• FY 2017 achievements:

• Rollout of portal throughout UK

and Europe improving customer

experience

WorldPay Finastra • Additional functionality to

GoToBilling support US

Credit Card BACS

Gateway Active

• Ongoing investment

• Ongoing improvements in

Payment Processing Systems resilience and security

• Enhanced collection methods

Citizen NETS SEPA BACS • Client reporting

Bank Clearing Clearing Clearing

8UK

UK Market Share/Opportunity

• UK market continues to present opportunities

for growth

Independent PVA Pet

Care Plan Clinics

8% • 29% annual increase in pets on plan to

Current PVA Medivet

PPCP - Market 156,000 at September 2017

PPCP Opportunity

3%

57%

• 18% growth in clinics operating PPCP

Vetpartners

4%

• PPCP serves both independent and corporate

Vets4Pets customers

9%

Linnaeus

1% CVS

9% IVC

9%

Total small animal clinics in UK – c4,800

Source: independent market research, company investor

presentations

9Europe - Netherlands

Rayons • 190 contracted clinics at 30 September 2017

aantal EGG's

North (46)

• Represents approximately 19% market

Middle (37)

South (46)

share

Netherlands Market

Share/Opportunity

• 46% annual growth in pets on plan to 24,000

at September 2017

19%

• Acquired customer base of competitor in

Netherlands

• Customer base being transitioned over

81%

coming months

PVA Pet Care Plan • Expected to become profitable during

Market Opportunity FY2018

Estimated small animal clinics

– c1,000

Source: KNMvD: Koninklijke Nederlandse

Maatschappijvoor Diergeneeskunde (Royal

Veterinary Association of the Netherlands)

10Europe - France

• 50 clinics signed up to PPCP during this

year (see map)

France Market Opportunity

• 33 clinics launched at 30 September 2017

1%

• Over 1,000 pets on plan

17%

• Initial sign up rates are encouraging

82% • Cooperation agreement with MSD Animal

Health producing leads

Pet Care Plan primary targets

• Cooperation agreement with Clubvet, one

Remaining market opportunity

of France’s largest buying groups

Contracted clinics

Estimated small animal clinics

• Territory showing early promise

Location of contracted clinics

– c6,000

Source: l’Ordre national des veterinaires” (

National Register of Veterinarians)

11USA

• Registered in 22 states (highlighted)

• Business focussed in South-Eastern and Mid-West States

• Recent cooperation agreements signed with:

• Purchases Services Holdings (“PSI”) – Group purchasing

organisation with over 4,000 members

• The Veterinary Cooperative (“TVC”) – Group purchasing

organisation with over 3,000 members

• 198 clinics signed contracts to launch PPCP at 30 September 2017

• 92 clinics launched at 30 September 2017

• 4,000 pets on plan

• US challenges being addressed. Focussed on:

• Improving sign up rates

Total small animal

clinics – c26,500

• Reducing cancellations

(UK c4,800) • Increasing average clinic size

• Leveraging partnership agreements

12Key Performance Indicators

13Global quarterly collection statistics

• 553,000 transactions in Q3 2017

(equivalent to 2.2m annual

transactions) – 38% increase on same

quarter last year

• Customer spend of £8.25m in Q3

2017 (equivalent to £33.0m

annualised spend)

• Generates sticky revenues for PVG

• 35% increase in pets on plan in last

twelve months

• 188,000 fee generating pets in

September 2017 with growth in all

regions

# fee generating pets on plan

000's Sep - 16 Dec - 16 Mar - 17 Jun - 17 Sep - 17

UK 121 132 137 145 156

Europe 18 21 22 25 28

US - 1 2 3 4

Total 139 154 161 173 188

14Global clinic relationships

Global Clinic Relationships at 30 September 2017

UK USA EU

• In total PVG now has 1,084 clinics

1200

contracted to PPCP

1,084

1000 • Important influence when

311 negotiating with pharmaceutical

manufacturers and

800 wholesalers/distributors

NO. OF CLINICS

198

600

1000

400

750

575

200 440 432 438

0

P VG I VC (UK ) CVS (UK ) P ETS AT HO ME ( UK ) B ANF I ELD ( US ) VCA (US)

15Diverse Customer Base

• Total of 455 contracts with

practices throughout UK, EU

& US.

• Only Medivet, the group’s

largest customer practice has

over 10,000 pets on plan.

• 95% of practices have less

than 1,000 pets on plan.

16Financials

17Profit and Loss - revenues

Year ended 30 September 2017 Revenues • 36% increase in global revenues

£000s 2017 2016 % change

• 17% UK revenue growth in line with plans.

PPCP – UK 1,873 1,606 17%

• Ongoing opportunities for revenue growth from

PPCP – Europe 493 263 87% existing customers and new opportunities

PPCP – US 168 - N/A

• 87% European revenue growth

Total - continuing operations 2,534 1,869 36%

• Netherlands the key source of growth in FY 2017

• France in early stage of development

• US revenue growth behind expectations due to

reductions in the rate of pet sign ups and higher

cancellation rates than expected

• US remains the largest single opportunity for

additional growth

18Profit and Loss – profits and EBITDA

Year ended 30 September2017 Profits

• Significant people and operating cost investment in both

%

Europe and US resulting in an increased operating loss

£000s 2017 2016 change

PPCP – UK 622 442 41% • Operating expense investment in IT development and

PPCP - Europe (983) (809) (21)% finance team in UK to support expansion and

development requirements

PPCP – US (1,895) (635) (198)%

EBITDA from PPCP (2,256) (1,002) • No executive bonus reducing central unallocated costs

Central unallocated costs (1,546) (1,908)

• One-off items incurred mobilising US investment and on

EBITDA from continuing operations (3,802) (2,910) legal costs to acquire customer base in Netherlands

One-off items (172) -

Depreciation and amortisation (134) (77) • Finance expense reduced following repayment of debt

after veterinary practices business disposal

Operating profit (4,108) (2,987)

Finance expense (161) (208) • Profit on discontinued operation in 2017 represents

Loss before and after tax from continuing operations (4,269) (3,195) trading profit of Buying Group up to date of disposal and

gain on disposal

Profit on discontinued operations 5,890 5,019

Profit attributable to equity holders 1,621 1,824

19Balance sheet

As at 30 September • Trade and other receivables reduced following receipt of

£000s 2017 2016 escrow money from sales of veterinary practices

business

Non-current assets 495 446

Trade and other receivables 705 1,719 • Sale of Buying Group enhanced net asset position

Trade and other payables (977) (871)

• Part of Buying Group proceeds used to repay loan notes

Net working capital (272) 848

Cash 3,218 1,254 • Deferred tax liability increase due to rollover relief being

Debt - (900) claimed on Buying Group disposal

Net cash/(debt) 3,218 354

Deferred tax (134) (10)

Net assets 3,307 1,638

20Cash flow

Year ended 30 September 2017

• Significant investment in international expansion

£000s 2017 2016

impacting EBITDA

£'000 £'000

EBITDA after central costs and non-recurring items (3,802) (2,910)

• Ongoing capital investment in IT around £250k per

Non-recurring items (172)

annum

Net working capital movement (74) (136)

Investment in IT and equipment (276) (210)

• Net disposal proceeds in 2016 relate to veterinary

Interest on loans and finance leases (161) (208)

practices business

Free cash flow (4,485) (3,464)

Net disposal proceeds 6,963 5,047

• Net disposal proceeds in 2017 include £1m escrow

Discontinued activities 338 881

release from disposal of veterinary practices and

Issue of share capital 48 97 balance relating to sale of Buying Group

Movement in net cash/(debt) 2,864 2,561

• Post balance entered into a committed facility with

Opening net debt 354 (2,207) Bybrook Finance Solutions Limited (“BFSL”) for up to

Closing net cash/(debt) 3,218 354 £1.5m in unsecured loan notes for drawdown in three

equal tranches from 1 June 2018 to 31 May 2019.

Net debt made up of; • Arrangement provides security of funding whilst

Cash 3,218 1,254 being sufficiently flexible to continue to consider

Debt - (900) alternative sources of funding.

3,218 354

21Business Fundamentals

• Sticky and diverse customer base

• Recurring revenue stream with compound growth

• Bespoke scalable IT platform underpinning international operations

• No bad debt exposure

• Growth opportunity underpinned by cooperation agreements (Mid- West, Zoetis, MVS, VPI, PSI, TVC, MSD France)

22Appendix

23Market opportunities

Market data UK Neth Germany France USA

Population 64m 17m 81m 66m 319m

Households 26m 7.4m 41m 26m 123m

Dog population 8.5m 1.6m 5.3m 7.4m 70m

Dog ownership households 24% 19% 13% 21% 36%

Cat population 8.5m 2.6m 8.2m 11.4m 74m

Cat owner households 19% 26% 16% 27% 30%

24Thank you for your time

25You can also read