Grab 'n Go: Session 8 Two-speed IT: It-organisering i en eksponentiel verden - juni 2016 #deloittegng

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Grab ‘n Go: Session 8 Two-speed IT: It-organisering i en eksponentiel verden 7. juni 2016 #deloittegng

Who are we?

• • •

• •

•

•

•

•

Technology Strategy & Architecture, 3000+ practitioners globally

Enterprise &

Tech-Enabled Technology IT Business Cloud & IT Mergers &

Solution IT Sourcing

Innovation Strategy Management Infrastructure Acquisitions

Architecture

Technology practitioners in total 37.000+

© 2015 Deloitte 2

IT is an integrated part of the business and the product – running

at multiple speeds

Business Business

Product Product

Product-enabling technology

Multi-modal Tech

Enterprise IT Functions

© 2016 Deloitte 3

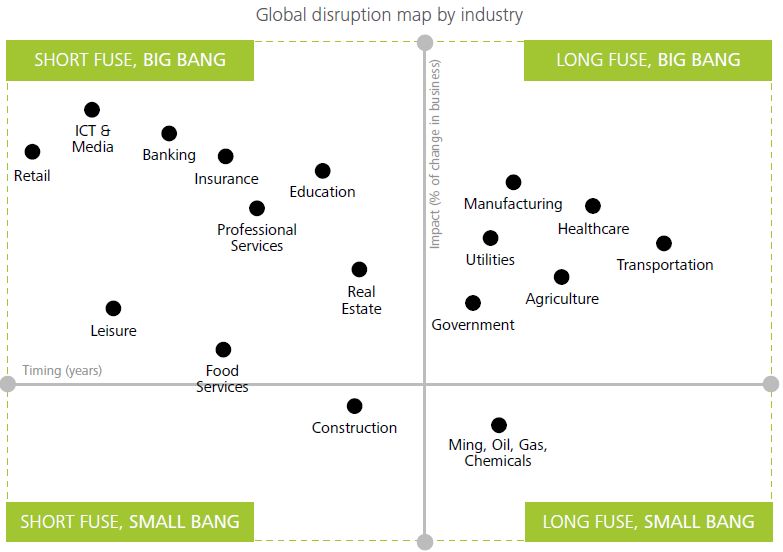

Some industries have been ahead of the game but others will quickly follow © 2016 Deloitte 4

…this results in a new set of challenges for the IT organisations

An increasingly disruptive digital world which requires speed, innovation and …creates a complex agenda

collaboration… for CIOs

...but also a need to keep it safe, scalable, sustainable…

© 2016 Deloitte 5

Agility and multi modes are emerging…but maturity is low

Lower cost to serve DELIVER INCREASING

Standardisation

BUSINESS DEMAND

Effectiveness in delivery

£ DO IT BETTER FOR LESS Enable differentiation

Speed to market

Exploit new technology

breakthroughs

Increased agility delivered; but often

• At too high cost

• Everything on-shore

• Decoupled from operations

• Agile for everything

© 2016 Deloitte 6A good design is vital to ensure the right balance

How do you design your future IT

organisation?

What is the best suited development

model?

Design

considerations

What role should IT play?

How can cloud computing be

leveraged appropriately?

How do you adapt your sourcing

model to new development models

and cloud?

© 2016 Deloitte 7IT delivery models © 2016 Deloitte 8

Designing for speed requires a comprehensive approach…

A complex agenda…

Right speed IT

© 2016 Deloitte 9…the first step is to define the delivery models that are right for

you…

A complex agenda…

Delivery models

© 2016 Deloitte 10Working styles, complexity and the nature of the applications drive

the delivery modes…

Agile, Scrum, Build modes Examples

Kanban • Customer apps, e.g. Mobile Pay

Innovation & • End-user apps, e.g. Expense

Prototyping management

• Solutions with no clear goal

• …

• Robotics

Business • Analytics

Cohabitation of

embedded • Intelligent processes

working modes - • Workflows

Right speeds • …

• CRM Salesforce

Cloud • HR WorkDay/Success factors

configuration • …

• SAP, Oracle ERP template roll-outs

ERP & • Core system replacements

Waterfall Enterprise • Customer core applications

© 2016 Deloitte

….Big programmes would combine several modes… 11…and must be fully integrated across your operational processes

and interactions…

ERP & Cloud Business Innovation &

Enterprise configuration embedded Prototyping

How will the users interact with the service desk?

Who will take care of functional support?

How will the solutions be maintained?

How will the solution be operated?

© 2016 Deloitte 12…with a clear understanding of how demand and change are

received and handled

Demand Change Operation

Third level support Second level support First level support

Application development Application maintenance Support Service desk management

Monitoring

Applications

Innovation & Prototyping

Business embedded

Cloud configuration Cloud configuration

Strategic programmes

Incidents

ERP & Enterprise ERP & Enterprise

New requirements

Problems

Small programmes

Small changes Events

Key Build Modes Support types Types of demand Embedded business capabilities

© 2016 Deloitte 13The new speed of IT is rapidly increasing and governance and

capabilities must mature…

Innovation &

Prototyping

Adapted

Architecture

Delivery Business

and solution

models Embedded

shaping

Portfolio and Sourcing and Cloud

financial contract Configuration

management management

Traditional

ERP &

Enterprise

© 2016 Deloitte 14…the right control requires IT to position itself in the context of the

chief digital officer (CDO)

CIO domain CDO domain

Traditional governance Adapted governance Stand alone

CIO CDO

EA and

PMO

strategy

New New New

Change Operations

modes modes modes

Fast IT #1 Fast IT #2 Fast IT #3

(Not fast enough) (Better option) (More shadow IT)

© 2016 Deloitte 15Cloud adoption © 2016 Deloitte 16

Cloud is a right-speed enabler giving users on-demand access to

large scale, elastic and shared computing capabilities

A complex agenda…

Cloud

© 2016 Deloitte 17Cloud is offered in many forms, shapes and sizes

Cloud services Cloud delivery models Cloud characteristics

Application + Applications Software Scalable and elastic based

Software

supporting (SaaS)

technology

on demand

stack

Public cloud

Paid for based on

consumption

Platform

EXAMPLES

(PaaS)

Platform

Salesforce.com

Software-defined and

Big Machines

rapidly configurable

Microsoft Office 360 Private cloud

EXAMPLES

SAP Business

Force.com

ByDesign

Google App Engine A managed set of

Infrastructure

Infrastructure Microsoft Azure shared services

(IaaS)

Heroku

EXAMPLES

Amazon Web Servies Hybrid cloud An enabler for agile IT

RackSpace Cloud delivery

© 2016 Deloitte 18Cloud is a key accelerator for the new development modes…

Software Platform Infrastruc.

(SaaS) (PaaS) (IaaS) Public Private

Innovation &

Prototyping

Key features

Agility, enhanced control,

Build Modes

Business compliance and

embedded

operational efficiency

Coherent connectivity

Cloud between private and

configuration public

ERP &

Enterprise

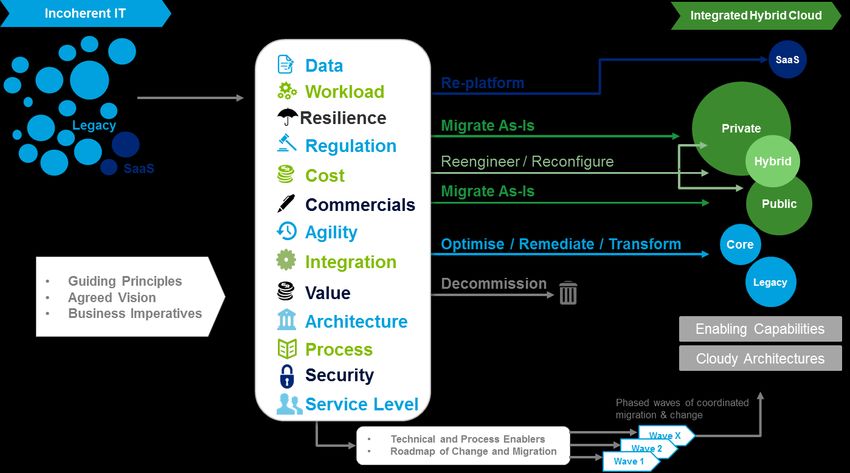

© 2016 Deloitte 19‘One-size-fits-all’ will not work for most enterprises

Incoherent IT Integrated hybrid cloud

SaaS

Legacy

SaaS ? Private

Hybrid

Public

Core

Legacy

© 2016 Deloitte 20A holistic approach will drive the best outcomes – evaluate your IT

portefolio against these 13 themes

Data

Incoherent IT Integrated hybrid cloud

Workload

Resilience SaaS

Regulation

Cost

Legacy Commercials Private

Agility Hybrid

SaaS

Integration

Public

Value

Architecture

Core

Process

Security Legacy

Service Level

© 2016 Deloitte 21Balance is needed to reach the right destination © 2016 Deloitte 22

Smoothing your path to hybrid cloud – the common themes

Start with an understanding Understand the Develop a clearly

of applications and data to differentiating capabilities prioritised strategy

clarify cloudy capabilities that create value for your and road map

that deliver most value business/customer

Drive out integration and Map cloudy requirements to

governance requirements to better public/private capabilities to

understand likely costs to validate understand delivery and

rationale and business case service options

© 2016 Deloitte 23Four capabilities you need to build in your organisation

Investment in developing Flexibility in the IT cost

advanced integration model to cater for both

and data management traditional on-premises

capabilities to support a service charge back and

cloud-to-cloud-to-core consumption-based cloud

mode service charge back

Security architecture

IT operations team with and cloud identity/

deep understanding of access management

cloud technologies and skills are critical as the

with DevOps and agile cloud portfolio within the

expertise enterprise grows

© 2016 Deloitte 24Right sourcing © 2016 Deloitte 25

Generating value and flexibility through new sourcing models is

key to unpinning speed and maintaining cost control

A complex agenda…

Sourcing

© 2016 Deloitte 26Evolution of outsourcing is moving towards 3.0….

Outsourcing 1.0 Outsourcing 2.0 Outsourcing 3.0

Past – The mega deal Present – Strategic sourcing Future – Convergence

1990’s to Post

Emerging

2005 2005

Smart sourcing focus

• Sole source • Multi-vendor • Integrated vendor models

• “1000 pager” • Improved contractual basis • Focus on service integration

• Focus on “The Deal” • Vendor management • Embrace the Cloud or die!

• Labour arbitrage • Enhanced capabilities • Everything “as a service”

• Niche advisory • Functional advisory • Automate using robotics etc.

• Obligation to innovate

• More agile and flexible contracts

• Transformation enabled

• Embrace multiple speed delivery models

© 2016 Deloitte 27…driven by a multitude of trends across the sourcing landscape

Supplier market shifts

• Increased Tier 1 competition

• Indian pure-plays dominate Infra

• Eco-system and niche partners emerging

Fine-grained operating models

• Unbundling and re-bundling Transformation wave

• From SIAM to Orchestration

• Limited insourcing • Ops tooling proliferation

• Greater tool-process-enablement • CyberSecurity

• Role of CIO debate • Application Rationalization

• New capability requirements emerging • Infrastructure footprint reduction

• Cloud readiness drives

• Consumerization in EUC

• Indian vendor R&D focus

• RPA pilots

New Sourcing models

“3rd generation” control and contract models • “Vertical slice” sourcing

• Emergence of Alliances, JVs and

• Ownership of process, tools and IP Utilities

• Exit rights and approaches • Evolution of ‘Ecosystem’ models

• Short Term and favourable terms • Convergence of ITO, BPO and SS

• Transparency and granularity Renewed risk focus • GBS, captive, co-source and mixed

• Regulatory and industry focus on third models

party risk • Industry solutions

• Increased vendor management spend

© 2015 Deloitte

• Data privacy regulation 28Moving to right-speed IT increases requirements to outsourcing

delivery models

Traditional +Right speed

• Multiple implementation modes

• Competitive pricing

• Increase use of onshore/landed resources

Application development • Fixed price/shared risk

• Time to market reduced by near shore teams

• Better access to skills and talent

• Distributed and duplicated SCRUM teams

• Low cost delivery • Convergence of AD and AM for selected areas

Application maintenance

• Managed services • Otherwise still low cost as much as possible

• Cloud orchestration is essential

Data centre • Different pricing models in cloud must be

• Low cost delivery

services defined

• Low cost still important

Infrastructure

Network and

• Specialist skills directly available • No major changes

telephony

• Low cost service desk

• Service Desk and Service Integration moving to

• Service integration

EUC independent 3’rd party or application provider

• Low cost delivery for software packaging and

• Mobile device management

distribution

© 2016 Deloitte 29…and aligning delivery modes to achieve value and speed is key

Requirements Near/Offshore potential Sourcing model Commercial

• Industry knowledge AD: 40% • Duplicated SCRUM teams Team- and value-based

Innovation & • Business insights AM: 40% across AD & AM pricing model of end-to-end

Prototyping • Innovation eco-system service teams

• End-to-end service teams

• Business insights AD: 0-10% • Onsite SCRUM team • Team-based pricing model

Business • Process/analytical skills AM: 50% working with super users

embedded • Possibility for AM split • Value-based, time and

Build Modes

when stabile material

• Functional and application- AD: 50-60% • Development through Fixed price, risk sharing,

Cloud specific knowledge AM: 90% Duplicated or distributed managed services

SCRUM teams

configuration

• Possibility for AM split

when stabile

• Application and process AD: 65-75% • More traditional AD and Fixed price, risk sharing,

ERP & knowledge AM: 90% AM split of team managed services

• Use of CoE for testing and

Enterprise assurance

© 2016 Deloitte 30…however, the current supplier landscape is struggling to keep up

Delivering Cloud

Service Maturity in new

as flexible as

integration is delivery models

promised seems

NOT working is low

difficult

• Suppliers are struggling to deliver • Many suppliers describe how • Waterfall and AD and AM split

successful service integration cloud services can be provisioned dominant

automatically – but struggle to

• Limited ability to work “outside” • New speeds at a high premium

deliver

own domains • Only basic pricing models in place

• Few suppliers have models that

• Customers are introducing cloud

really embraces public cloud • Innovation capabilities relatively

services without respecting the

models (amazon, google, azure low

service integration role of the SP

etc)

• Suppliers not organised to deliver

• Pricing models are often not

SI from AM

designed to handle cloud

• Customers are introducing cloud

infrastructure components without

defining responsibility for

managing them

© 2016 Deloitte 31What's next? © 2016 Deloitte 32

Good design is vital; successful deployment even more so

How do you design your future IT How do we embed the new model?

organisation? And instil different ways of working?

What is the best suited development How do we change behaviours?

model? How do we get people to do things

Deployment differently?

considerations

Design

considerations How do we build the requisite skills

What role should IT play? and competencies to operate in the

new world?

How can cloud computing be How do we transition to the new

leveraged appropriately? model without degrading live

service and project delivery?

How do you adapt your sourcing How do we educate and re-direct

model to new development models existing vendors and partners to

and cloud? the new model?

© 2016 Deloitte 33Enjoy the rest of the day and please consider:

Do you have clearly defined development models that enable right-speed? And are they well-

aligned to operations and interactions across your organisation?

Do you have a clear strategy for where to use cloud and how to ensure connectivity across

your landscape?

Does your current sourcing model differentiate between your different development models?

And do they seamlessly embed cloud in terms of pricing and service management?

© 2016 Deloitte 34Kristian Skotte, Thomas Andersen, Jesper Kamstrup- Holm 7. juni 2016

You can also read