Howard Weil Energy Conference - March 2015 - Criterion Research

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Howard Weil Energy Conference

March 2015

Important Note to Investors

This presentation contains certain forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995 regarding Dominion and

Dominion Midstream. The statements relate to, among other things, expectations, estimates and projections concerning the business and operations of Dominion

and Dominion Midstream. We have used the words "anticipate", "believe", "could", "estimate", "expect", "intend", "may", "plan", “outlook”, "predict", "project",

“should”, “strategy”, “target”, "will“, “potential” and similar terms and phrases to identify forward-looking statements in this presentation. As outlined in our SEC

filings, factors that could cause actual results to differ include, but are not limited to: unusual weather conditions and their effect on energy sales to customers and

energy commodity prices; extreme weather events and other natural disasters; federal, state and local legislative and regulatory developments; changes to federal,

state and local environmental laws and regulations, including proposed carbon regulations; cost of environmental compliance; capital market conditions, including

the availability of credit and the ability to obtain financing on reasonable terms; fluctuations in interest rates; changes in rating agency requirements or credit ratings

and their effect on availability and cost of capital; impacts of acquisitions, divestitures, transfers of assets by Dominion to joint ventures or to Dominion Midstream,

and retirements of assets based on asset portfolio reviews; receipt of approvals for, and timing of, closing dates for acquisitions; the execution of Dominion

Midstream’s growth strategy; changes in demand for Dominion’s services; additional competition in Dominion’s industries; changes to regulated rates collected by

Dominion; changes in operating, maintenance and construction costs; timing and receipt of regulatory approvals necessary for planned construction or expansion

projects and compliance with conditions associated with such regulatory approvals; the inability to complete planned construction projects within time frames

initially anticipated; and the ability of Dominion Midstream to negotiate and consummate acquisitions from Dominion and third-parties, and the impacts of such

acquisitions. Other risk factors are detailed from time to time in Dominion’s and Dominion Midstream’s filings with the Securities and Exchange Commission.

The information in this presentation was prepared as of February 3, 2015. Dominion and Dominion Midstream undertake no obligation to update any forward-

looking information statement to reflect developments after the statement is made. Projections or forecasts shown in this document are based on the assumptions

listed in this document and are subject to change at any time. In addition, certain information presented in this document incorporates planned capital expenditures

reviewed and endorsed by Dominion’s Board of Directors in late 2014. Dominion undertakes no obligation to update such planned expenditures to reflect plan or

project-specific developments, including regulatory developments, or other updates until the following annual update for the plans. Actual capital expenditures may

be subject to regulatory and/or Board of Directors’ approval and may vary from these estimates.

This presentation shall not constitute an offer to sell or the solicitation of an offer to buy securities. Any offers, solicitations or offers to buy, or any sales of securities

will be made in accordance with the requirements of the Securities Act of 1933, as amended.

This presentation has been prepared primarily for security analysts and investors in the hope that it will serve as a convenient and useful reference document. The

format of this document may change in the future as we continue to try to meet the needs of security analysts and investors. This document is not intended for use

in connection with any sale, offer to sell, or solicitation of any offer to buy securities.

This presentation includes various estimates of EBITDA which is a non-GAAP financial measure. Please see the Appendix for a discussion of EBITDA.

Please continue to regularly check Dominion’s website at www.dom.com/investors

and Dominion Midstream’s website at www.dommidstream.com/investors.

March 2015 Howard Weil Energy Conference 2

Dominion Midstream

Key Investment Highlights

• Strong and supportive sponsor

• Quality asset inventory

• Dropdown strategy provides 22% distribution growth

• Financial strength and flexibility

March 2015 Howard Weil Energy Conference 3

Dominion Profile

Strong and Supportive Sponsor

Leading provider of energy and energy services in

the Midwest and Eastern regions of the U.S.

24,600 MW of electric generation

6,455 miles of electric transmission

NY

12,400 miles of natural gas transmission,

gathering and storage pipeline CT RI

949 billion cubic feet of natural gas storage PA

operated

IN MD

Cove Point LNG Facility OH

2.5 million electric customers in VA and NC

WV

1.3 million natural gas customers in OH & WV

VA

1.3 million non-regulated retail customers in 12

states (not shown) NC

D owns 100% of DM General

SC

Partner and 69% of LP units

Please refer to page 2 for risks and uncertainties related to projections and forward looking statements.

March 2015 Howard Weil Energy Conference 4Total Dominion Capex

2015 – 2020 Growth Plan ($billions)

$19.2 billion

Growth $54.7

Capex $2.1 Net

$2.5 Plant1

$2.8

$3.2

$4.3

$4.3

$35.5 Average annual spend of

Net ~$3.2 billion per year

Plant

2014 2015 2016 2017 2018 2019 2020

1 Excludes 2015-2020 DD&A and Maintenance Capex

Please refer to page 2 for risks and uncertainties related to projections and forward looking statements.

March 2015 Howard Weil Energy Conference 5Dominion EPS Growth

Long-term Projections

6-7% CAGR for 2015 - 2020

Transformational

Investments + MLP

accelerate EPS

growth post-2017

$3.48*

2014 2015 2016 2017 2018 2019 2020

Foundation Transformational Investments & Financial Initiatives

*Note: Represents weather-adjusted 2014 Operating EPS

Please refer to page 2 for risks and uncertainties related to projections and forward looking statements.

March 2015 Howard Weil Energy Conference 6Dominion Dividend Growth

Long-term Projections

8%

Board increased Annual

payout ratio to Growth

70-75% starting

in 2015

5-6%

Annual

$2.59 Growth

$2.40

Note: Annual

dividend rates

subject to Board

2014 2015 2016 2017 2018 2019 2020 approval

Please refer to page 2 for risks and uncertainties related to projections and forward looking statements.

March 2015 Howard Weil Energy Conference 7Quality Asset Inventory

• Cove Point LNG

• Dominion-Carolina Gas Transmission

• Dominion’s interest in Atlantic Coast Pipeline

• Dominion’s interest in Blue Racer

• Other retained Dominion assets

March 2015 Howard Weil Energy Conference 8Dominion Midstream

Initial Asset Overview

– Existing Operations: Cove Point

• LNG import and storage services

• Domestic natural gas and regasified

LNG transportation services

– Long-term contracts with firm

reservation payments with

creditworthy counterparties

– Preferred Equity Interest

• Perpetual, non-convertible preferred

equity interest entitled to the first

$50 million of annual cash

distributions from Cove Point

Please refer to page 2 for risks and uncertainties related to projections and forward looking statements.

March 2015 Howard Weil Energy Conference 9Cove Point LNG Export

Cove Point Export construction is

on-time and on-budget

Expected in-service late 2017

– Engineering is ~77% complete

– Procurement of major

equipment on schedule

• Engineered equipment packages are

~84% awarded

– Total estimated project cost

$3.4 - $3.8 billion* Total 2015-2020 Capex

• ~$1 billion* spent through 2014 of $2.4 - $2.8 billion*

*Excludes financing costs

Please refer to page 2 for risks and uncertainties related to projections and forward looking statements.

March 2015 Howard Weil Energy Conference 10Dominion – Carolina Gas Transmission

Dominion acquisition of CGT for ~$493

CGT System

million closed on January 31, 2015

– 1,500 miles of FERC-regulated pipeline in

SC and GA

• ~0.70 Bcf/d capacity expanding to ~0.82

Bcf/d by 2018 SC

Growth projects are fully contracted

– Expected to be dropped into DM in 1H15

– Financial highlights:

• 2015 annualized EBITDA of ~$38 million*

Expected to grow to ~$50 million by 2018

Acquisition

• 2015 annualized DCF of ~$22 million*

accretive for both

Expected to grow to ~$30 million by 2018 D and DM

*Excludes non-recurring transaction costs

Please refer to page 2 for risks and uncertainties related to projections and forward looking statements.

March 2015 Howard Weil Energy Conference 11Atlantic Coast Pipeline

OWNERSHIP STRUCTURE:

Dominion Resources* 45%

Duke Energy 40%

Piedmont Natural Gas 10%

AGL Resources 5%

– 550 miles of 42” pipe

– 1.5 Bcf per day capacity

• Subscribed through ACP partners and

other LDCs

• Expandable to >2 Bcf per day

ACP

– Est. cost $4.5 – $5.0 billion** DTI Pipeline

Storage

• >55% of total procurement complete Cove Point

– 20-year binding contracts with Utica

Shale

electric and gas utilities

Marcellus

– Expected In-service November 2018 Shale

* Dominion will construct, operate and manage the pipeline

** Excludes financing costs

Please refer to page 2 for risks and uncertainties related to projections and forward looking statements.

March 2015 Howard Weil Energy Conference 12Blue Racer Midstream JV

Overview

Growth-oriented midstream platform located

in the rich and lean areas of Utica & Marcellus

– High-quality assets Lean Utica

• ~750 miles of gas, NGL and condensate pipelines Rich Utica

• 600 MMcf/d of processing capacity Utica Volatile Oil

• 47,000 Bbl/d of fractionation capacity

– Largely fee-based contracts Lewis

• ~90% of expected 2015 revenues

Rich Marcellus

• New contracts expected to increase fee-based %

post-2015

– Favorable well results driving significant

Natrium

producer activity in the southern Utica

• Blue Racer uniquely positioned to capture Berne

significant growth

Please refer to page 2 for risks and uncertainties related to projections and forward looking statements.

March 2015 Howard Weil Energy Conference 13Blue Racer Midstream JV

Key Projects Through 2015

– Processing

• Natrium I & II

1 Bcf/day

• Berne I

processing capacity

• Berne II - 1H2015 by the end of 2015

• Lewis I - 2H2015

– Fractionation

• Natrium 123,000 bbls/day

• Natrium Expansion - 1H2015 by the end of 2015

– Gathering / NGL Projects funded at Blue Racer & do not

• Multiple growth projects require cash outlays from Dominion

Please refer to page 2 for risks and uncertainties related to projections and forward looking statements.

March 2015 Howard Weil Energy Conference 14Blue Racer Midstream JV

Updated Long-term Forecast*

Current business plan shows

significant long-term growth

$265 - $275

$245 - $255

$220 - $230

$185 - $195

$140 - $150

$85 - $95

2015 2016 2017 2018 2019 2020

* Dominion’s pro-rata share of EBITDA (less partnership level cash interest expense) from joint venture

Please refer to page 2 for risks and uncertainties related to projections and forward looking statements.

March 2015 Howard Weil Energy Conference 15Dominion Additional Retained Assets

Dominion Gas Holdings

– Dominion Transmission

• 7,775 miles of pipeline in six states*

• 778 Bcf of underground natural gas storage

• 9.3 Bcf/d gas peak sendout capability

• 270,000 mcf/d of natural gas processing capacity

– Interest in Iroquois Pipeline

• 416 miles of mile interstate natural gas pipeline system

• 24.72% ownership interest

– Dominion East Ohio

• 171 Bcf of underground natural gas storage 10,900 miles of natural gas transmission, gathering

and storage pipeline

• 1.2 million natural gas customers

949 billion cubic feet of natural gas storage

• 360 Bcf of natural gas throughput in 2014 operated

• 21,700 miles of natural gas distribution pipeline 1.2 million natural gas customers in OH

* Excludes 3,125 miles of gas transmission at DEO and Hope.

Please refer to page 2 for risks and uncertainties related to projections and forward looking statements.

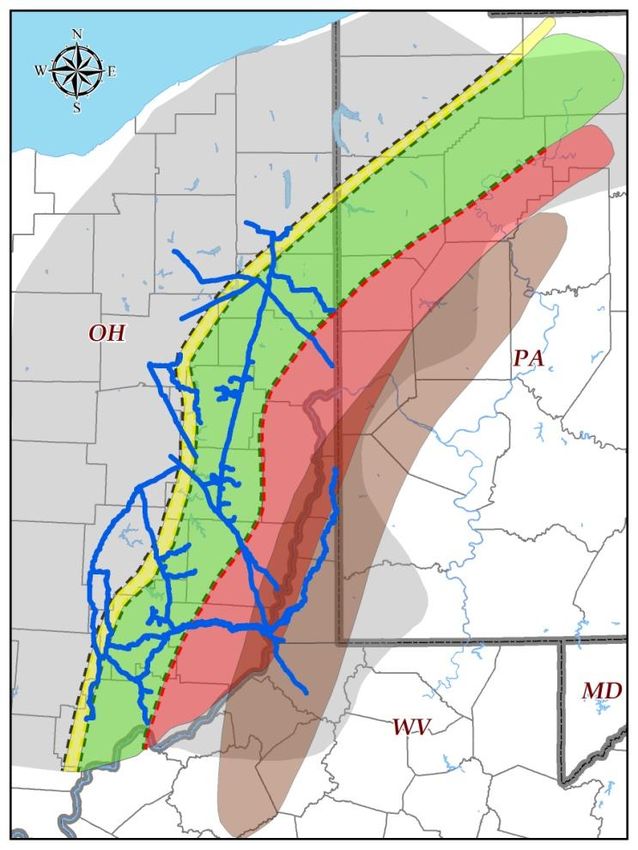

March 2015 Howard Weil Energy Conference 16Marcellus and Utica Shale

Fall 2014 Natural Gas Production Forecast

40 2025 Production – Takeaway

Capacity Gap (Bcf/day)

14.4

35 Utica production*

10.7

30 9.4

Bcf Per Day

25 Fall Spring Fall

2013 2014 2014

20 24.2 Bcf/d of incremental firm pipeline

take away capacity**

15

10

5 Marcellus production*

0

*Wood Mackenzie – Fall 2014 natural gas long term view

** Projects under construction or fully subscribed

Please refer to page 2 for risks and uncertainties related to projections and forward looking statements.

March 2015 Howard Weil Energy Conference 17Dominion Energy

2015 – 2020 Growth Plan ($billions)

*Total excludes Cove Point, ACP & Blue Racer

$3.3 billion

Growth $11.9

$0.5

Capex* Net

$0.5 Plant1

$0.7

$0.6

$0.6

Avg. annual spend of ~$0.6 billion

$8.6 $0.5

Drivers:

• DTI Supply Header

Net • Producer Outlet Projects

Plant • Market Access Projects

• DEO Pipeline Infrastructure Replacement

2014 2015 2016 2017 2018 2019 2020

1 Excludes 2015-2020 DD&A and Maintenance Capex

Please refer to page 2 for risks and uncertainties related to projections and forward looking statements.

March 2015 Howard Weil Energy Conference 18Producer Outlet Projects

Producer Outlet Projects optimize current

transmission system to address changing

dynamics of Northeast gas flows

– 5 projects totaling ~1 Bcf/d have

been placed into service

– 4 additional projects expected to

enter service before end of 2016

• Additional 1 Bcf/d

• ~$400 million of capex

– Expect an incremental $500

million or more of projects ~$900 million Total Capex

through the end of the decade

Please refer to page 2 for risks and uncertainties related to projections and forward looking statements.

March 2015 Howard Weil Energy Conference 19Market Access Projects

Market Access projects are demand-

driven projects that move gas off the

system to end use customers NY

CPV Power

Generation

New Market

Project

OH PA

Keys Power

Generation

MD

~$440 million

Leidy total Capex

South WV

Please refer to page 2 for risks and uncertainties related to projections and forward looking statements.

March 2015 Howard Weil Energy Conference 20DTI Supply Header

Project will increase access to diverse

Marcellus and Utica gas supplies for ACP

customers and other producers

– Capacity of 1.5 Bcf/day

• Subscribed through ACP partners and

other LDCs

– Expected Project Milestones

• Open Season completed Fall 2014

• FERC Pre-filing submitted Fall 2014 ACP

DTI Pipeline

• Receive FERC certificate Summer 2016 Storage

Cove Point

• In-Service November 2018

Supply Header Utica

Shale

~$500 million receipt points Marcellus

total Capex

Shale

Please refer to page 2 for risks and uncertainties related to projections and forward looking statements.

March 2015 Howard Weil Energy Conference 21Dominion Energy

Farmout Opportunities

Farmout opportunities provide incremental earnings

streams from mineral rights leasing, royalty revenues and

takeaway & processing agreements

– Announced and completed multiple

Marcellus farmout agreements

covering over 125,000 acres

• ~$270 million expected pre-tax

earnings contribution 2015-2020

– Additional farmout potential of

~180,000 acres of Utica mineral rights

~$450 - $500

• ~$180 - $230 million of million of potential

DTI Pipeline

Storage

incremental pre-tax earnings total pre-tax Cove Point

contribution 2015-2020 earnings 2015-2020 Utica

Shale

Marcellus

Shale

Please refer to page 2 for risks and uncertainties related to projections and forward looking statements.

March 2015 Howard Weil Energy Conference 22Dropdown Strategy March 2015 Howard Weil Energy Conference 23

Dominion Midstream Partners

Dropdown Strategy to Support Best-in-Class Growth ($ millions)

$1.7 billion+ of projected Dominion

MLP-eligible EBITDA provides robust $349

inventory of post-2020 growth

$175

Annual EBITDA Contribution to MLP

On-Going MLP EBITDA* $81 $525

$61 $329

$36 $228

$39

$93

$139

$50 $50

IPO 2015 2016 2017 2018 2019 2020

Cove Preferred + CGT

Blue Racer

Cove Equity / ACP

Third-Party M&A** / Organic Growth

* EBITDA figures annualized based on year end

** Opportunistic third-party M&A not included; M&A would supplement existing dropdown strategy

Please refer to page 2 for risks and uncertainties related to projections and forward looking statements.

March 2015 Howard Weil Energy Conference 24Dominion Midstream Partners

Targeted LP Distribution Growth Rate Per Unit

Dropdown strategy supports “best-in-class” growth rate

~$2.30

$0.85

$0.70

2014 2015 2016 2017 2018 2019 2020

Note: Distributions reflect year end run-rate

Please refer to page 2 for risks and uncertainties related to projections and forward looking statements.

March 2015 Howard Weil Energy Conference 25Dominion Midstream Partners

Total Projected Cash Flow to Dominion ($ billions)*

Total cash flows of ~$7 billion 2015-2020 will be used to: $2.9

• Support strong dividend growth at D

• Buyback D shares

• Pay down DRI debt

• Fund new growth projects

$1.7

$0.9

$0.7

$0.4

$0.1

2015 2016 2017 2018 2019 2020

Drop Down Proceeds LP Distributions GP Distributions

*Pre-tax

Please refer to page 2 for risks and uncertainties related to projections and forward looking statements.

March 2015 Howard Weil Energy Conference 26Dominion Midstream Partners

Projected LP and GP Distributions to Dominion ($ millions)*

Distributions to Dominion grow rapidly over time

Total LP & GP distributions of

~$1 billion 2015-2020

$241

~48% of EBITDA dropped through 2020

flows back to D in the form of LP and GP

distributions

$129

$61

$26 $181

$6 $112

$64 $81

$39 $52

2015 2016 2017 2018 2019 2020

LP Distributions GP Distributions

*Pre-tax

Please refer to page 2 for risks and uncertainties related to projections and forward looking statements.

March 2015 Howard Weil Energy Conference 27Dominion Midstream Partners

Projected Dominion Ownership

Dominion will retain 100% of the GP and a large

portion of the LP units through 2020

Total LP Units (millions)

190M

143M

105M

91M

82M

64M 71M

81M

60M 43%

44M 49M 50M 50M 52M

69%

At IPO 2015 2016 2017 2018 2019 2020

D Ownership Public Ownership

Please refer to page 2 for risks and uncertainties related to projections and forward looking statements.

March 2015 Howard Weil Energy Conference 28Appendix March 2015 Howard Weil Energy Conference 29

Reconciliation of Operating Earnings to Reported Earnings

2014 Earnings (Twelve months ending December 31, 2014)

– The net effects of the following items, all shown (millions, except per share amounts) 1Q14 2Q14 3Q14 4Q14 YTD 2014 2

on an after-tax basis, are included in 2014 Operating earnings $607 $361 $545 $490 $2,003

reported earnings, but are excluded from Items excluded from operating earnings (after-tax):

operating earnings: North Anna and offshore wind facilities (191) (28) (29) (248)

Producer Services repositioning (193) (193)

• $248 million charge associated with Virginia Charges associated with liability management exercise (2) (172) (174)

legislation enacted in April that permits Virginia Future ash pond closure costs (74) (74)

Power to recover 70% of the costs previously Goodwill write-off at unregulated electric retail (31) (31)

deferred or capitalized through Dec. 31, 2013 Other items (4) (11) 14 28 27

relating to the development of a third nuclear 1 (228) (202) (16) (247) (693)

Total items excluded from operating earnings (after-tax)

unit located at North Anna and offshore wind Reported net income $379 $159 $529 $243 $1,310

facilities as part of the 2013 and 2014 base rates. Common shares outstanding (average, diluted) 582.9 583.9 584.6 586.5 584.5

• $193 million net charge related to the Operating earnings per share $1.04 $0.62 $0.93 $0.84 $3.43

repositioning of our Producer Services business, Items excluded from operating earnings (after-tax) (0.39) (0.35) (0.03) (0.42) (1.19)

reflecting the termination of natural gas trading Reported earnings per share $0.65 $0.27 $0.90 $0.42 $2.24

and certain energy marketing activities.

• $174 million charge associated with our liability 1) Pre-tax amounts for items excluded from operating earnings are reflected in the following table:

management exercise, mainly reflecting the call Items excluded from operating earnings: 1Q14 2Q14 3Q14 4Q14 YTD 2014

premiums on our early debt redemptions in the

fourth quarter. North Anna and offshore wind facilities (287) (43) (44) (374)

Producer Services repositioning (319) (319)

• $74 million charge related to a settlement offer

Charges associated with liability management exercise (3) (281) (284)

to incur future ash pond closure costs at certain

Future ash pond closure costs (121) (121)

utility generation facilities.

Goodwill write-off at unregulated electric retail (31) (31)

• $31 million goodwill write-off associated with the Other items (2) (15) (8) (12) (37)

company exiting the unregulated electric retail

Total items excluded from operating earnings ($352) ($302) ($54) ($458) ($1,166)

energy marketing business.

• $27 net benefit related to other items. 2) YTD EPS may not equal sum of quarters due to share count differences.

Please refer to page 2 for risks and uncertainties related to projections and forward looking statements.

March 2015 Howard Weil Energy Conference 302015 Earnings Expectations

– Reconciliation of measures prepared in accordance with Generally Accepted Accounting Principles (GAAP) versus non-GAAP

measures:

• 1Q 2015 Operating Earnings (estimate): $0.85 - $1.00

• FY 2015 Operating Earnings (estimate): $3.50 - $3.85

• 1Q 2015 Reported Earnings (estimate): See Note 1 below

• FY 2015 Reported Earnings (estimate): See Note 1 below

Note 1: In providing its first-quarter and full-year 2015 operating earnings guidance , Dominion notes that there could be differences between expected reported (GAAP) earnings

and estimated operating earnings for matters such as, but not limited to, divestitures or changes in accounting principles. At this time, Dominion management is currently not

able to estimate the aggregate impact, if any, of these items on reported earnings. Accordingly, Dominion is not able to provide a corresponding GAAP equivalent for its operating

earnings guidance.

– Dominion uses operating earnings as the primary performance measurement of its earnings guidance and results for public communications with analysts and investors.

Dominion also uses operating earnings internally for budgeting, for reporting to the board of directors, for the company’s incentive compensation plans and for its targeted

dividend payouts and other purposes. Dominion management believes operating earnings provide a more meaningful representation of the company’s fundamental earnings

power.

– Dominion’s estimates of first-quarter and full-year 2015 earnings are subject to various risks and uncertainties. Factors that could cause actual results to differ materially from

management's projections, forecasts, estimates and expectations may include factors that are beyond the company's ability to control or estimate precisely, including fluctuations

in energy-related commodity prices, estimates of future market conditions, additional competition in our industries, changes in the demand for Dominion’s services, access to and

costs of capital, fluctuations in the value of our pension assets and assets held in our decommissioning trusts, impacts of acquisitions, divestitures, transfers of assets to joint

ventures or Dominion Midstream and retirements of assets based on asset portfolio reviews, the receipt of regulatory approvals for, and timing of, planned projects, acquisitions

and divestitures, the timing and execution of Dominion Midstream’s growth strategy, and the ability to complete planned construction or expansion projects at all or within the

terms and timeframes initially anticipated. Other factors include, but are not limited to, weather conditions and other events, including the effects of hurricanes, earthquakes,

high winds, major storms and changes in water temperatures on operations, the risk associated with the operation of nuclear facilities, unplanned outages at facilities in which

Dominion has an ownership interest, the impact of operational hazards and catastrophic events, state and federal legislative and regulatory developments, including changes in

federal and state tax laws and changes to environmental and other laws and regulations, including those related to climate change, greenhouse gases and other emissions to

which we are subject, political and economic conditions, industrial, commercial and residential growth or decline in Dominion’s service area, risks of operating businesses in

regulated industries that are subject to changing regulatory structures, changes to regulated gas and electric rates collected by Dominion, changes to rating agency requirements

and ratings, changing financial accounting standards, fluctuations in interest rates, employee workforce factors, including collective bargaining, counter-party credit and

performance risks, adverse outcomes in litigation matters or regulatory proceedings, the risk of hostile cyber intrusions and other uncertainties. Other risk factors are detailed

from time to time in Dominion’s quarterly reports on Form 10-Q or most recent annual report on Form 10-K filed with the Securities and Exchange Commission.

Please refer to page 2 for risks and uncertainties related to projections and forward looking statements.

March 2015 Howard Weil Energy Conference 31Non-GAAP Measures

• EBITDA represents net income before interest and related charges, income tax and

depreciation and amortization. Distributable cash flow (DCF) is defined as EBITDA adjusted

for known timing differences between cash and income, less capital expenditures.

• The GAAP measure most directly comparable to EBITDA is net income. EBITDA and DCF

should not be considered alternatives to net income, operating income, cash flow from

operating activities or any other measure of financial performance or liquidity presented in

accordance with GAAP. EBITDA and DCF exclude some, but not all, items that affect net

income and operating income, and these measures may vary among other companies.

Therefore, EBITDA and DCF as presented may not be comparable to similarly titled

measures of other companies.

• EBITDA forecasts for Blue Racer Midstream and Dominion Midstream were derived on an

EBITDA-only basis. At this time, elements of net income including tax and depreciation

information are not available. Accordingly, Dominion and Dominion Midstream are not able

to provide a corresponding GAAP equivalent for EBITDA forecasts.

Please refer to page 2 for risks and uncertainties related to projections and forward looking statements.

March 2015 Howard Weil Energy Conference 32Non-GAAP Reconciliation

Dominion - Carolina Gas Transmission

2015E 2018E

Net income $ 18.2 $ 24.6

Add back:

Depreciation 8.6 10.7

Fixed Charges - -

Income Tax 11.2 15.1

EBITDA 38.0 50.4

Non-cash Adjustments, net (0.4) (0.6)

Maintenance Capex (15.6) (19.8)

Distributable Cash Flow $ 22.0 $ 30.0

($ in millions)

Please refer to page 2 for risks and uncertainties related to projections and forward looking statements.

March 2015 Howard Weil Energy Conference 33March 2015 Howard Weil Energy Conference 34

You can also read