Introductory Presentation - Gresham House Strategic plc (GHS.LN) Strategic Public Equity Investment Strategy

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Introductory Presentation Gresham House Strategic plc (GHS.LN) Strategic Public Equity Investment Strategy Targeting superior long-term returns through a private equity approach to public markets June 2016 www.ghsplc.com

Important information

This presentation (the “Presentation”) is issued by Gresham House Asset any management fees, carried interest, taxes and allocable expenses of the kind

Management Ltd (“GHAM”), Investment Manager for Gresham House Strategic that will be borne by investors in a fund, which in the aggregate may be

plc (“GHS”) for information purposes only. This Presentation, its contents and substantial. Prospective investors are reminded that the actual performance

any information provided or discussed in connection with it are strictly private realised will depend on numerous factors and circumstances some of which will

and confidential and may not be reproduced, redistributed or passed on, directly be personal to the investor.

or indirectly, to any other person or published, in whole or in part, for any

Statements contained in this Presentation that are not historical facts are based

purpose, without the consent of GHAM (provided that you may disclose this

on current expectations, estimates, projections, opinions and beliefs of GHAM.

Presentation on a confidential basis to your legal, tax or investment advisers (if

Such statements involve known and unknown risks, uncertainties and other

any) for the purposes of obtaining advice). Acceptance of delivery of any part of

factors, and undue reliance should not be placed thereon. In addition, this

the Presentation by you constitutes unconditional acceptance of the terms and

Presentation contains “forward-looking statements.” Actual events or results or

conditions of this notice.

the actual performance of the Fund may differ materially from those reflected or

This Presentation does not itself constitute an offer to subscribe for or purchase contemplated in such forward-looking statements.

any interests or other securities. This Presentation is not intended to be relied

Certain economic and market information contained herein has been obtained

upon as the basis for an investment decision, and is not, and should not be

from published sources prepared by third parties and in certain cases has not

assumed to be, complete. It is provided for information purposes only. Any

been updated to the date hereof. While such sources are believed to be reliable,

investment is subject to various risks, none of which are outlined herein. All

neither GHAM, GHS nor any of its directors, partners, members, officers,

such risks should be carefully considered by prospective investors before they

employees, advisers or agents assumes any responsibility for the accuracy or

make any investment decision.

completeness of such information.

You are not entitled to rely on this Presentation and no responsibility is

No person, especially those who do not have professional experience in matters

accepted by GHAM, GHS or any of its directors, officers, partners, members,

relating to investments, must rely on the contents of this Presentation. If you

employees, agents or advisers or any other person for any action taken on the

are in any doubt as to the matters contained in this Presentation you should

basis of the content of this Presentation. Neither GHAM, GHS nor any other

seek independent advice where necessary. This Presentation has not been

person undertakes to provide the recipient with access to any additional

submitted to or approved by the securities regulatory authority of any state or

information or to update this Presentation or to correct any inaccuracies therein

jurisdiction.

which may become apparent.

For the Attention of United Kingdom Investors

No undertaking, representation, warranty or other assurance, express or

implied, is made or given by or on behalf of GHAM, GHS or any of its respective This Presentation is intended for distribution in the United Kingdom only to

directors, officers, partners, members, employees, agents or advisers or any persons who: (i) have professional experience in matters relating to

other person as to the accuracy or completeness of the information or opinions investments, (ii) who are investment professionals, high net worth companies,

contained in this Presentation and no responsibility or liability is accepted by high net worth unincorporated associations or partnerships or trustees of high

any of them for any such information or opinions. value trusts, and (iii) investment personnel of any of the foregoing (each within

the meaning of the Financial Services and Markets Act 2000 (Financial

Past performance is not indicative of future results. The value of investments

Promotion) Order 2005).

may fall as well as rise and investors may not get back the amount invested.

Changes in rates of foreign exchange may cause the value of investments to go For the Attention of Investors outside the United Kingdom

up or down. No representation is being made that any investment will or is

likely to achieve profits or losses similar to those achieved in the past, or that This Presentation relates to an Alternative Investment Fund within the meaning

significant losses will be avoided. of the Alternative Investment Fund Managers Directive and the availability of

this Presentation will be subject to registration in relevant jurisdictions as

Prospective investors should seek their own independent financial, tax, legal described in the documents relating thereto. Any dissemination or

and other advice before making a decision to invest. unauthorised use of this Presentation outside the United Kingdom by any

person or entity is strictly prohibited.

The internal rates of return or IRRs presented on a “gross” basis do not reflect

Contents

GRESHAM HOUSE O V E RV I E W – T H E O P P O RT U N I T Y 1

S T R AT E G I C P L C ( G H S . L N )

GRESHAM HOUSE

S T R AT E G I C P L C B A C K G R O U N D A N D D E TA I LS 2

S I G N I FI C A N T P O T E N T I A L U P S I D E FR O M E X I S T I N G P O RT FO LI O 3

I M I M O B I LE – I N V E S T M E N T O P P O RT U N I T Y 4

N E W I N V E S T M E N T O P P O RT U N I T I E S – W E LL D E V E LO P E D P I P E LI N E 5

S T R AT E G I C P U B L I C

EQUITY S P E A P P R O A C H – TA R G E T I N G S U P E R I O R LO N G - T E R M R E T U R N S 6

G H S P LC - S P E T R A C K R E C O R D 7

EXPERIENCED GHS INVESTMENT TEAM 8

SPE INVESTMENT PROCESS 9

CONCLUSION

C O N C LU S I O N 10

S U P P L E M E N TA RY

I N F O R M AT I O N 11 - 1 9

BRIDGING THE DIVIDE BETWEEN PUBLIC AND PRIVATE MARKETS

Gresham House Strategic plc

Overview

The opportunity - Gresham House Strategic plc (GHS.LN)

Strategic Public Equity mandate – Targeting net 15% IRR over the longer term1

Private equity approach to investing in public markets

Focus on inefficient areas of the market - UK smaller companies2

Significantly higher levels of engagement with investee company stakeholders

Focused portfolio – the majority of the portfolio will be invested in 10-15 companies

Attractive entry point trading at a 20% discount to NAV3

Investment appraisal has identified potential for significant upside within existing portfolio

Valuation opportunities presenting themselves as market bifurcates

Diligence and engagement with target companies

Proven investment team with a track record of strong long-term returns

Investment team aligned to performance through significant shareholding

1 Refer to Investing Policy section (p:10) of the GHS circular sent to shareholders 21st July 2015

2 The fund will invest primarily in UK equities but can also invest in smaller European companies

3 Mid price as of 27th May 2016 and applying announced NAV as at 27th May 2016

Page 1 BRIDGING THE DIVIDE BETWEEN PUBLIC AND PRIVATE MARKETSGresham House Strategic plc (GHS)

Background & details

Investing company traded on AIM - £36m NAV trading at a 20%1 discount

Investment Manager is Gresham House Asset Management Ltd (GHAM)

GHAM is a division of specialist asset manager Gresham House plc, founded in 1857

Gresham House plc and team own c.20% of GHS

New Strategic Public Equity Investment Mandate – Bridging the divide between public and private markets

Private equity approach - investment appraisal, due diligence and risk management

Disciplined investment process and use of Investment Committee and Advisory Group

Concentrated portfolio of 10-15 smaller, typically UK quoted companies2

Targeting companies that can benefit from strategic, operational or management initiatives

Investment Team – Strong long-term track records at SVG & PDFM (led by Tony Dalwood and Graham Bird)

Fees – 1.5% management charge with 15% performance fee over a 7% hurdle rate

GHAM to reinvest 50% of performance fee into Gresham House Strategic plc shares

1 Mid price as of 27th May 2016 and applying announced NAV as at 27th May 2016

2 Manager has the ability to invest up to 30% of the portfolio in unquoted securities

Page 2 BRIDGING THE DIVIDE BETWEEN PUBLIC AND PRIVATE MARKETSGresham House Strategic plc – Existing portfolio

Significant potential upside

IMImobile Poorly understood, lowly valued Earnings growth

£16.3m Cash generation

with strong growth prospects

Potential for re-rating - currently less than 7x EBITDA

Proven management team

Be Heard Group Buy & build, organic growth

Strong track record of value creation

£2.3m* plus strong cash generation Digital media consolidation via enhancing acquisitions

Niche market exposure

Quarto Group Organic and acquisition

£2.1m Grow earnings through enhancing acquisitions and operational efficiencies

growth at attractive valuations Highly cash generative; reducing debt

Northbridge De-leverage - strong cash generation and significant scope to reduce capex

Industrial Services Recovery and growth, investing

Profit growth as margins recover to long-term average

£1.8m alongside management Attractive entry point at a substantial 40% discount to realisable assets

AUM and earnings growth

Miton Group Significant operational gearing Cash generation and cost control

£1.3m

Strong balance sheet

Spaceandpeople Sales growth and recovery of EBIT margin

£1.1m Recovery, margins and growth Highly cash generative

Continued contract wins and renewals

Cash and other net assets

£12.0m

Attractively valued portfolio:

Tax losses

Excluding cash - portfolio trades on a weighted avg EV/EBITDAIMImobile – GHS c.18% shareholding

High growth business benefiting from mobile data growth

www.imimobile.com

Attractions

High recurring revenues and embedded solutions

Strong cash generation and balance sheet, high return on capital and successful acquisition track-record

High gross margins and significant operational gearing

Investment thesis

Significant discount to sector on 7.4x FY17 (March year-end) EV/EBITDA1, falling to 6.7x FY181 vs peer group average of c.13x1

Significant opportunity to simplify business and market messaging and positioning with investors

Strategic initiatives delivering with strong momentum; clear value creation plan

Catalysts – earnings growth; further improvement in quality of earnings; new markets (USA); potential for a PE or trade buyer

Potential risks / threats

Customer concentration - loss of a major contract could have a material short-term impact

Regulatory environment

Responsiveness (product development and deployment) to technological change and innovation

GHAM is engaged with management and shareholders

GHAM team actively engaged with executive management, Board and key teams (tech, finance)

Tom Teichman (GHS IC member) was an original VC backer of IMImobile with invaluable insight and relationships

Shareholder engagement and aligned interests – Tosca 27.6%, Liontrust 12.9%, management 21.2%

1 House broker, Investec Securities research, April 2016 and peer group analysis (Software sector).

Page 4 BRIDGING THE DIVIDE BETWEEN PUBLIC AND PRIVATE MARKETSNew investment opportunities

Well developed pipeline of new investment opportunities

Public Private

Private Equity houses

P2P opportunities typically uncomfortable

1478 – Stocks on FTSE All-share and

[1470 – Stocks

AIM All-Share Indexon with public markets

Profitable companies with

FTSE All-share and organic & acquisition

Pre-IPO

AIM

910 –All-Share Index]

Stocks with a Market

growth (not ready for

public markets yet)

Capitalisation below £250m Watchlist Preferred quasi Convertibles, mezzanine

equity positions Preferred instruments

412 – Stocks trading > 50% below

3yr price high Growth / Recovery Strategic &

Acquisition Capital Capital Opportunistic

44 – EV/ 36 – 34 – FCF Improvement

21 – ROCE

EBITDA Gearing > Yield >

> 10%

< 7x 75% 10%

Private: Pre-

Source: Bloomberg, 13th April 2016

M&A Asset Realisation IPO / P2P /

Catalyst quasi equity

Listed Private

Equity

Reject Portfolio

Page 5 BRIDGING THE DIVIDE BETWEEN PUBLIC AND PRIVATE MARKETSStrategic Public Equity

SPE approach

Targeting superior long-term returns

Value creation opportunities through a focus on inefficient areas of public markets

Valuation anomalies as a result of temporary market inefficiency

Limited advice / access to growth capital can result in small companies being strategically constrained

Poor research coverage of smaller companies – an average of one live broker recommendation per stock1

Philosophy – Value based approach, longer term holding period

Typically focus on cash generative companies, where ROCE and growth can be improved

Applying disciplined Private Equity techniques in public markets:

Influential, minority block stakes typically 5%-25% of equity

Significant engagement with stakeholders including; Management, shareholders, customers, suppliers and competitors

Support a clear equity value creation plan (Management, capital, strategic and operational support)

Targeting superior long-term investment returns - 15% net IRR over the long-term2

Private Equity - style approach including Investment Committee and extensive due diligence

Small company focus (GHS plc – SPE investment track record

Team and SPE performance track record

SVG Investment Managers / Strategic Equity Capital Investment Trust

Schroder Ventures Ltd (London)

5yr IRR 23%1, 11% IRR since 20071

Tony Dalwood established the

Strategic Public Equity Strategic Recovery Fund I (LP)

Over 130 years’ investment strategy at SVG and

experience of SPE launched two LPs the Strategic 46% net IRR2 (03 Vintage)

Track record of

investment & Recovery Fund I and II and the

strong relative Investment Trust (SEC plc), the Strategic Recovery Fund II (LP)

corporate advisory

returns at SVG and latter two with Graham Bird

within team and

PDFM 6% net IRR2 (06 Vintage).

Investment Graham left SVG in Feb 2009 Remaining equity investments transferred to limited

Committee partners in specie3

Tony left SVG in March 2011 Journey Group plc +67% since fund

realisation

E2V plc +75% since fund realisation

Lavendon Group plc -12% since fund

Breadth of skills: realisation

Investment UK Focus Fund (OEIC)

Corporate Advisory 78% total return 2003–2011, vs 14% for SMXX4

Banking

Private Equity Downing LLP Downing Active Management (OEIC)5

Tony chaired the Investment 98% 3yr total return (vs 90% SMXX)

Gresham House: Committee from July 2011 – 73% total return since inception (vs 55% SMXX)

Dec 2014

• Advisory Group broadens and deepens the appraisal process

and deal sourcing PDFM (UBS Asset Management) Managed UK equity Funds of £1.5bn.

UK Investment Committee member, top quartile

• Network bridges public & private markets Tony was a member of the UK (CAPS data)

Investment Committee Pension Fund of the year 2001 (Pooled Fund) –

• Range of skills and experience enhances due diligence process Team member

1 Gresham House Asset Management Ltd calculations excluding dividends, including period subsequent to the departures of Graham Bird (Feb 2009) and Tony Dalwood who left SVG in March

2011 having stepped down from the SEC plc Investment Committee, moving to non-executive Chairman of SVGIM on 30 Sept 2010.

2 GVQIM website.

3 Bloomberg data (total return since 30 Aug 2013 when SRFII wound up through to 5th Jan 2016) – SEC plc continues to follow an SPE style of investment and demonstrates the success of the

strategy over the investment cycle.

4 Bloomberg data – total return. Tony Dalwood left SVGIM in March 2011 therefore data tracked for UK Focus Fund from Aug 2003 (July inception) - 31 Dec 2010.

5 Tony Dalwood chaired Downing Active Management Fund Investment Committee from July 2011 – Dec 2014. Total return Performance data up to 26th Dec 2014.

Page 7 BRIDGING THE DIVIDE BETWEEN PUBLIC AND PRIVATE MARKETSExperienced GHS investment team

Fund Tony Dalwood* Graham Bird* Pardip Khroud

Management Fund Manager Fund Manager Investment Director

Chairman of Investment Committee, Previously Director of strategic Pardip has 13 years experience in

Established SVGIM and launched Strategic investments at SVGIM and a Director audit, private equity transactions

Equity Capital plc and the Strategic within the corporate finance and global tax restructuring at

Recovery Funds. Former CEO of SVG department at JP Morgan Cazenove. KPMG, Senior Manager at Lloyds

Advisers (Schroder Ventures London), Recently held senior positions at Banking Group and most recently

former chair of Downing Active Paypoint plc including strategic as an Investment Manager at

Management Investment Committee and a planning and corporate development Lloyds Development Capital (LDC)

member of the UK Investment Committee director and PayByPhone President & where she managed numerous

at PDFM. Currently NED of JP Morgan executive Chairman. Graham Bird is investments and was also

Private Equity Plc and an adviser to LDC Head of Strategic Investments at appointed to the Board of portfolio

through Gresham House. Tony is also Gresham House plc and a director of companies uSwitch and Bluestone.

Chairman of the Investment Committee GHAM.

and CEO of Gresham House plc

Investment Tom Teichman Rupert Robinson Bruce Carnegie Brown

Committee 30 years’ VC & banking experience. Over 25 years’ experience in Private Bruce is currently chairman of Aon

Founded Spark in 1995. Former Wealth and Asset Management. UK Ltd and of

Investment Committee member at Former CEO and CIO of Schroders Moneysupermarket.com Group plc.

Brandt’s, Credit Suisse, Bank of Montreal Private Bank and was instrumental in He is a non-executive director of

and Mitsubishi Finance London. Start-up driving organic growth in AUM which Santander UK plc. He was

investor/director of lastminute.com, doubled between 2008 and 2012 from previously a managing partner of 3i

mergermarket.com, Chairman of Kobalt £4.5 to more than £9bn. Prior to QPE plc, a managing director of JP

Music, notonthehighstreet.com, ARC, MAID, Schroders, Rupert was Head of UK Morgan and CEO of Marsh Ltd.

amongst others. Investor/director in Wealth Management at Rothschild Bruce is also a member of the

System C Healthcare, Argonaut Games, Asset Management. Rupert is the Gresham House plc Investment

World Telecom. Delivered various disposals Managing Director of GHAM. Committee.

to trade, P-E, and through IPO.

Strategic Advisory Group

Investment Jonathan Dighe

team Public markets and advisory background Gareth Current Chairman of Wolseley, William Hill and DS Smith. Former CEO of Imperial Tobacco

members focused on smaller companies Davis and Senior Executive at Hanson.

Laurence Hulse Alan Former Senior Partner and Head of Healthcare at 3i Group plc, appointed to the board in 1993.

Warwick University graduate. Interned at Mackay Currently Managing Partner at GHO Capital and former CEO of Hermes GPE.

Rothschild and Barclays Capital

Sir Roy Adviser to Credit Suisse, current Non-Executive Chairman of Serco, Senior Independent

Gardner Director of William Hill Plc and Non-Executive Director of Willis Group Holdings Plc. Former

Sanjeev Sarkar (Venture Partner)

Chairman of Compass Group, Manchester United and CEO of Centrica.

Private Equity background and experienced

principal investor

Page 8 BRIDGING THE DIVIDE BETWEEN PUBLIC AND PRIVATE MARKETS

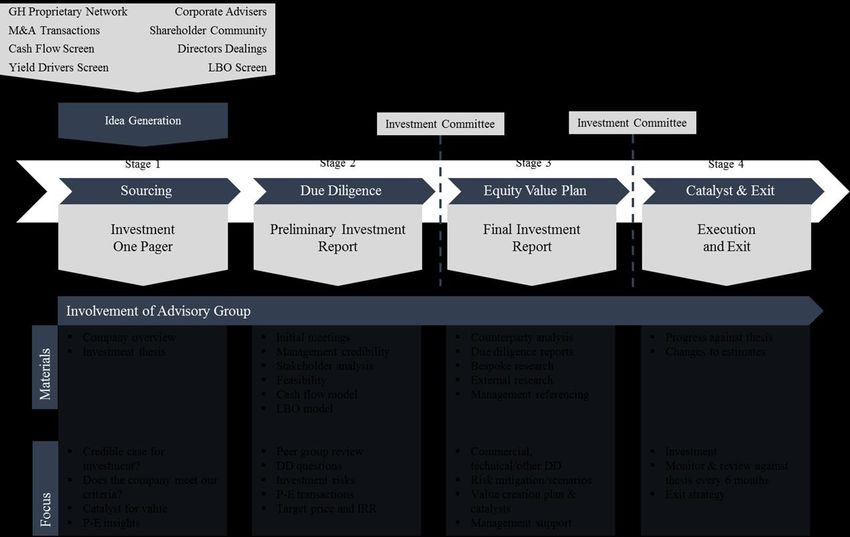

13SPE investment process

Source: Gresham House Asset Management Limited

Page 9 BRIDGING THE DIVIDE BETWEEN PUBLIC AND PRIVATE MARKETSConclusion

Attractive entry point - GHS plc is currently trading at a 20% discount to NAV1

Gresham House believes there is significant potential upside from existing strategic investments in the

portfolio over the medium term (valuations plus catalysts)

Attractive pipeline of investment opportunities – engaged with a number of opportunities

Investment team with a track record of delivering strong long-term absolute returns

Investing with a Strategic Public Equity (SPE) approach can deliver superior long-term returns

Investment team aligned to performance – plans to scale and continue to narrow discount to NAV

1 Mid price as of 27th May 2016 and applying announced NAV as at 27th May 2016

Page 10 BRIDGING THE DIVIDE BETWEEN PUBLIC AND PRIVATE MARKETSSupplementary Information - Contents

S U P P L E M E N TA RY NEW INVESTMENT CASE STUDIES ( 11 - 1 3 )

I N F O R M AT I O N

Q U A RTO G R O U P I N C 11

B E H E A R D G R O U P P LC 12

N O RT H B R I D G E I N D U S T R I A L S E RV I C E S P LC 13

S P E – U T I LI S I N G P R I VAT E E Q U I T Y LE V E R S FO R E Q U I T Y VA LU E C R E AT I O N 14

VA LU E I N V E S T M E N T P H I LO S O P H Y G E N E R AT E S LO N G - T E R M R E T U R N S 15

S U P E R I O R LO N G - T E R M R E T U R N S FR O M S P E S T Y LE S T R AT E G Y 16

S P E – LO N G - T E R M VA LU E C R E AT I O N FR O M A FO C U S E D P O RT FO LI O 17

AT T R A C T I O N S O F S M A LLE R C O M PA N Y U N I V E R S E 18

LI T T LE C O M P E T I T I O N FR O M O T H E R I N V E S TO R S 19

BRIDGING THE DIVIDE BETWEEN PUBLIC AND PRIVATE MARKETSQuarto Group – c.5% shareholding

“Secondary followed by potential primary growth capital” www.quartoknows.com

Date of investment: January 2016, increasing stake to 5% in March 2016

Deal Type: Secondary with plan for provision of growth capital in support of acquisitions complementing organic growth

Overview: Secondary – Supporting the new management teams organic growth strategy with the agreed potential to provide growth capital to facilitate acquisitions

The story Engagement

The Quarto Group (‘Quarto”) is a leading global illustrated book publishing and Restructuring Phase Growth Phase

distribution group. Quarto creates more than 1,500 adult and children's books a

year, sold into 35 countries and in 25 languages. Subjects range from Art 'How-

To', Graphic Design, and Home Improvement, to Cooking. Quarto specialises in Engagement and due diligence period

producing books that can be better explained with photographs or illustrations.

The business went through a restructure under the new management team and is

now well positioned to grow earnings organically and by acquisition.

260 MAR ‘16 – Increase stake to c.5%

Investment thesis MAR ‘16 – Collaboration with management

240 to provide advisory support on acquisition

Backing management to grow earnings and create value through a combination of: strategy and model

Organic earnings growth Operational improvement and increasing exposure to

higher margin niche publishing areas 220

De-leverage – Strong cash generation enabling debt reduction

MAR ‘16 -

Potential to provide primary growth capital to fund enhancing acquisitions DEC ‘15 – Buy

200 Presentation to

The strategy seeks to acquire smaller publishers for low multiples (4x-5x shares through management on

EBITDA) and integrate them with Quarto trading closer to 7.2x1 fwd secondary opportunities for

EV/EBITDA, driving operational synergies and enhancing group earnings. placing

Pipeline of identified acquisition opportunities exceeds $25m 180 divisional businesses

M&A Track record - IVY press was acquired in 2015 and the team had grown

EBITDA from c.£0.4m at time of acquisition and generated in excess of £1m

within first year of inclusion in the group 160

Trade / PE deal precedents at high relative valuations2

Jan 15 April 16

Source: Bloomberg share price data

1 Stockdale

Securities research note March 2016 140

2 Gresham House calculations using peer group as determined by GHAM

Page 11

BRIDGING THE DIVIDE BETWEEN PUBLIC AND PRIVATE MARKETSBe Heard – c.10% shareholding

“Primary growth capital, supporting buy & build strategy” www.beheardgroup.com

Date of investment: Initial investment November 2015, further investment in April 2016

Deal Type: Growth capital

Overview: Cornerstone capital raise & re-Admission to support a proven management team aiming to build a leading digital marketing network through acquisitive

and organic growth

The Story Engagement

Be Heard's strategy is to create a network of digital marketing businesses spanning

media planning and buying; design, build and UX; creative and content; and

High engagement with management team

5.5

strategy, innovation and data analytics

Growth will be achieved through acquiring smaller, niche complementary

businesses in the UK, US and Europe and organically developing capability. The 5 NOV ‘15 - placing raises £5.5m

strategy is to create a mid-size digital marketing network providing more flexibility for acquisition of Agenda21 + JAN - MAR ‘16 – Active

than holding groups and greater scale than digital specialists can achieve alone name change and re-Admission due diligence of

4.5 to AIM proposed acquisition

Investment thesis OCT ‘15 – Meeting

4 with CEO and FD

Backing a proven management team - Strong track record of value creation in the

sector and highly capable integrators of businesses

3.5

Support a buy and build growth and value creation strategy – Paid c.6x

EBITDA for the initial acquisition of Agenda21 with an earn-out up to 8x and c.5.5x NOV ‘15 –

for the second acquisition of MMT rising to a maximum of 8x MAR ‘16 - Announced proposed

3 Referencing of mgt acquisition of MMT and fund raise

Valuation arbitrage - Larger companies in the sector trade on a range of 9-11x and engage 3rd party

EBITDA1 expert adviser APRIL ‘16 –

2.5

NOV ‘15 – Invest DEC –

Market growth in digital media is evident with spending on internet advertising increase invest £1.6m in

£0.7m of growth

forecast to double 2014-201518 holding at firm placing at

2 capital in primary

Significant revenue and cost synergies available from the buy and build 2.97p 3.25p

issue at 3.25p

strategy

Sep 15 Apr 16

Strong cash flow generation from operations and earnings growth expectation Source: Bloomberg share price data

1 Gresham House calculations. GHAM determined peer group including much larger peers which in time as BHRD executes on its buy and build strategy should become appropriate

comparable companies.

2 Enders Analysis based on GroupM/ZenithOptimedia

Page 12

BRIDGING THE DIVIDE BETWEEN PUBLIC AND PRIVATE MARKETSNorthbridge Industrial Services – c.10%* shareholding

“Recovery and growth capital investing alongside

management” www.northbridgegroup.co.uk

Date of investment: April 2016

Deal Type: Recovery and growth capital

Overview: Cornerstone capital raise to reduce debt and support future growth, including underwriting Open Offer. Collaborative engagement with management with a

view to supporting the execution of the agreed future strategy

The Story Engagement

Northbridge manufactures specialist electrical industrial equipment for sale and

rental and is a leading global supplier of loadbanks. The company also supplies 600 8 months engagement and due diligence period

the oil & gas sector with drilling equipment for rent.

The business has consistently generated ROCE exceeding its cost of capital

backed by its solid loadbank business, which continues to perform strongly. 500

Once the oil and gas sector begins to recover we expect the business to NOV ‘15 – Site visit to Burton on MAR ‘16 – proposals to

strengthen in-line with our investment horizon.

400 Trent management on funding options

Having spent over six months engaging with the management team GHS is

supporting the next phase of the company’s growth plan FEB ‘16 – Engaged 3rd

300 party expert adviser

Investment thesis APR ‘16 - Injection of

SEPT ‘15 -

recovery & growth

De-leveraging – cash generation and significant reduction in capex 200 Meeting with

capital

advisers

Multiple expansion – Entry EV/EBITDA at 4.8x representing a 63% discount

100

to peers and a low point compared to the last 2 years’ trading range1 OCT ‘15 – Initial company

Margin recovery – Profit growth as margins recover to long-term average meeting MAR ‘16 – External independent

0

Free cash flow yield of 20%2 and Recovery P/E ratio of 5.9x3

research report

Liquidation value – Underpinned by realisable assets. Attractive entry point Mar ‘15 Apr ‘16

Source: Bloomberg share price data

at 60% of net asset value4

1 Bloomberg data 2 Free cashflow yield GH 2016 forecasts (operating cashflow after interest & tax, less maintenance capex. EV based on fully diluted number of shares at 75p and forecast net debt).

3 Gresham House forecast 2019 EPS, assuming turnover recovers to 2015 levels and margins return to c.12%, applying entry price of 75p.

4 Stockdale Securities forecasts - note 18 April 2016

Page 13

BRIDGING THE DIVIDE BETWEEN PUBLIC AND PRIVATE MARKETSStrategic Public Equity value creation

Utilising Private Equity levers for equity value creation

The experience of Private Equity demonstrates that it is factors under the influence of management and investors which drive the

majority of value creation

Equity value is delivered through three levers

Profit growth

De-gearing

Multiple expansion

Source: Centre for entrepreneurial and financial studies, technical university of Munich, Capital Dynamics. 241 mainly European enterprises backed

by Private Equity over 17 yr period 1989-2006. Average holding period 3.5yrs. Data published in FTfm October 2009.

Page 14 BRIDGING THE DIVIDE BETWEEN PUBLIC AND PRIVATE MARKETSValue investment philosophy generates long-term returns

Lower valuation at time of investment leads to higher returns

10yr Cyclically Adjusted PE & Future Average Real Compound Returns for 32 Countries (1980 – 2011)1

Avg CAPE % 1yr 3yr 5yr 7yr 10yr

by Bucket Occurrence Real CAGR Real CAGR Real CAGR Real CAGR Real CAGR

50 2.0% -4.5% -12.3% -6.4% -1.9% -3.1%

1 Cambria - CQR ISSUE 5 using global financial data, Morningstar.

Page 15 BRIDGING THE DIVIDE BETWEEN PUBLIC AND PRIVATE MARKETS

21Superior long-term returns from SPE style strategy

Year to 31 January

2008 2009 2010 2011 2012 2013 2014 2015

100%

80%

60%

40%

20%

0%

-20%

-40%

-60% SMXX NASCIT Strategic Equity Capital Crystal Amber

Source: Bloomberg data, Annual Report & Accounts. NAV growth vs FTSE small-cap (ex IT)

The SPE strategy delivered an average NAV CAGR of 7.4% vs 4.0% for the SMXX between Jan 2008 – Jan 20151

Gresham House has no relationship with Strategic Equity Capital plc, NASCIT and Crystal Amber. The purpose of this slide is to demonstrate the long-term

aggregate outperformance of the engaged strategic public equity style investment strategy.

1 Gresham House calculations. SPE strategy average NAV CAGR calculated by taking the average NAV growth of NASCIT, Strategic Equity Capital plc

and Crystal Amber over the period vs the CAGR in share price of the FTSE small-cap index excluding Investment Trusts (SMXX) .

Page 16 BRIDGING THE DIVIDE BETWEEN PUBLIC AND PRIVATE MARKETSSPE – Long term value creation from focused portfolio

SEC plc demonstrates the long-term investment cycle for SPE style investing

Strategic Equity Capital plc - Top 10 holdings as of 30/6 each yr - % of invested portfolio

2007 2008 2009 2010 2011 2012 2013 2014

Redstone 14.6 Redstone 14.6 Intec 16.4 SRF II 13.9 SRF II 16.6 SRF II 17.2 Tyman (Lupus) 13.1 E2V 12.2

Pinewood 8.4 Pinewood 8.8 RPC 11.5 RPC 9.8 E2V 11.8 Lupus Capital 12.2 E2V 12.7 Tyman 12.1

Melrose 6.7 Spirent 7.8 Spirent 9.1 KCOM 9.0 Lupus Capital 9.2 E2V 10.1 4imprint 10.0 Servelec 10.6

Evolution 5.5 Intec 6.9 StatPro Group 8.7 E2V 8.5 RPC 8.9 Lavendon 8.5 Lavendon 9.1 4imprint 8.6

Spirent 5.5 Thorntons 6.1 Pinewood 8.3 4imprint 7.9 KCOM 8.9 4imprint 8.4 KCOM 8.3 Wilmington 8.5

Cardpoint 5.3 4imprint 5.5 Thorntons 6.8 Lavendon 6.6 Lavendon 8.4 KCOM 7.8 CVC Group 6.1 EMIS 7.9

Mecom 5.3 RPC 5.0 4imprint 6.7 StatPro 5.4 Mecom 7.8 RPC 6.3 Allocate 5.9 Allocate 7.2

Gooch &

Renold 4.5 Renold 4.8 ORA Capital 5.2 Pinewood 5.2 4imprint 7.3 Allocate 5.7 Housego 5.6 Goals 7.1

Gooch &

Intec 4.4 Vintage 1 4.5 KCOM 4.2 Mecom 5.2 Allocate 4.3 Kewill 4.4 Wilmington 5.4 Housego 5.8

Journey

Thorntons 4.3 Mecom 4.5 Group 3.6 Allocate 5.0 Kewill 3.6 CVS Group 4.3 RPC 5.2 RPC 3.9

Top 10 as %

of portfolio 64.5 68.6 80.4 76.9 86.8 84.9 81.4 83.9

Private Equity 2010 or earlier investment

Highlighted stocks reflect initial investment decisions made in or prior to 2010

Engage, influence, value creation plan and then the market re-rates on execution /delivery (not a short-term strategy)

Unquoted – significant drivers of performance – SRF II (IRR 36.8%, 2.8x1), Vintage (46.0% IRR 5.7x1)

1 SEC plc Annual Report 30 June 2013, net of fees and since purchase in Aug 2009.

Page 17 BRIDGING THE DIVIDE BETWEEN PUBLIC AND PRIVATE MARKETSAttractions of smaller company universe

AIM valuation and growth forecasts

Many smaller companies suffer a valuation

discount compared with larger peers

Longer term investment can exploit the ‘illiquidity

discount’

Many of the smaller companies exhibit attractive

Source: Liberum; Bloomberg

value characteristics and growth potential,

providing a large pool from which to source ideas FTSE Allshare and AIM Allshare indices – 1461 Companies

Of these …

900 – companies with a market capitalisation below £250m

Of these …

490 – companies trading at a share price which is trading at 26 – have ROCE > 49 – deliver Free

EV/EBITDA below 7x 75% 10% Cashflow yield > 10%

Source: Bloomberg, as at 17 December 2015

Page 18 BRIDGING THE DIVIDE BETWEEN PUBLIC AND PRIVATE MARKETSLittle competition from other investors

Private equity is often unable / unwilling to access the

small quoted company opportunity AIM trading values

Restricted to public information

Private equity investors usually require certainty

of transaction and seldom go hostile

Pension deficits or other contingent liabilities may

prevent investment

Public market managers are often wary of private Source: Allenby Capital AIM market update Aug 2015 and LSE

equity and will not engage AIM market capitalisation range

Access to borrowing can be restricted

Trading liquidity on AIM has fallen, reducing the

attractions to public market institutions

There is a large universe of companies with smaller

Source: Bloomberg; data as at 8 January 2016; FTSE AIM All Share index constituents,

market capitalisations to choose from excluding companies suspended from trading and nil values

Page 19 BRIDGING THE DIVIDE BETWEEN PUBLIC AND PRIVATE MARKETSThe flagship listed Gresham House

Strategic Public Equity platform

Gresham House Asset Management Ltd www.ghsplc.com

107 Cheapside info@greshamhouse.com

London EC2V 6DN 020 3837 6270

26You can also read