Investor Day 2021 Maybank Group's Five-Year Strategy: M25

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Dis claimer: The con ten ts of this document/information remain the in tellectual property of M ayban k and n o part of this

is to be reproduced or transmitted in an y form or by an y means , in cludin g electronically, photocopyin g, recording or in

an y information storage and retrieval s ystem without the permission in writin g from Maybank. The con tents of this

documen t/information are confidential and its circulation and use are restricted.

Investor Day 2021

Maybank Group’s Five-Year Strategy: M25

9 April 2021

Humanising Financial Services

0

Who We Are

OUR CORE VALUES Teamwork Integrity Growth Excellence & Efficiency Relationship Building

OUR MISSION Humanising Financial Services

Serving our Over 42,000 Maybankers Our strong retail

OUR UNIQUE communities in ways who serve the mission, community

DIFFERENTIATORS that are simple, fair empowered by our franchise spanning

and human. TIGER Core Values. across ASEAN.

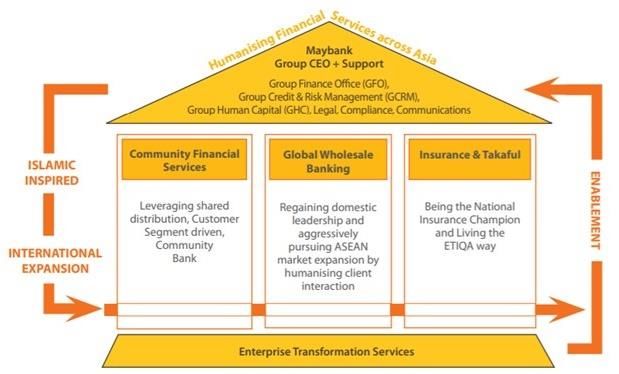

Our Three Business Pillars…

Group

Community Group Group

Financial Global Insurance &

OUR STRUCTURE Services Banking Takaful

Islamic Finance leverage model

… Enabled by Group Corporate Functions

1

Our Strategic Journey

The Top ASEAN Community Bank

The Leading ASEAN Wholesale Bank Linking Asia

The Leading ASEAN Insurer

The Global Leader in Islamic Finance

The Digital Bank of Choice 2021-2025

2016-2020 Sustainability agenda embedded in long-

term strategy to become Bank’s DNA.

2010-2015 Strengthen our position in ASEAN across Bettering customer experience and

all our key businesses. interface through enhanced digitalisation

and data analytics.

Creation of the “House of Maybank” Digital technology becomes a key theme.

Extracting growth from new value

Strengthen position in our three core Continue to build on capital and liquidity drivers.

markets of Malaysia, Singapore and strengths given evolving capital and

Indonesia. liquidity regulatory requirements.

Building on strategic acquisitions made in Drove sustainability-led initiatives as per

Indonesia (PT Bank Internasional five-year 20/20 Sustainability Plan

Indonesia in 2008) and investment established in 2015, premised on three

banking (Kim Eng Holdings Ltd in 2011). pillars (community and citizenship; our

Refocus growth agenda in target regions people; access to people and services)

and exited Papua New Guinea.

2

Our Regional Strategy Contributed to Our Earnings Growth

Net Operating Income PPOP Net Profit 2015-2020: 5-Year CAGR

Net Operating Income : 3.1% (3.9%) 2020-2025: 5-Year (f)

PPOP : 4.3% (4.7%) ROE : 13-15%

2010-2015: 5-Year CAGR Net Profit : -1.1% (4.6%) CIR : 4%, SG: principles with customers and the

SG: 3%-6%). 0.7%-4%, IND: 5%) and volatility in commodity community being at the foremost in

markets, we focused on building capital and liquidity everything we do.

• Strong upside in the commodity sectors given strengths as well as new fee income streams.

growing economies. • New value drivers focused on digital-play

• Focus on digitalisation in line with aspiration to (digital inclusion for SMEs, digitalising the

• Given robust operating environment growth and become The Digital Bank of Choice. Wholesale Banking customer experience,

Maybank’s repositioning of business segments, scaling up digital insurance business),

net profit expanded >1.5 times from RM4.45* • Re-balancing asset and liability portfolio strategies strengthening wealth proposition with

billion in FY2011 to RM6.84 billion in FY2015. to optimise risk/returns in line with evolving risk Universal Private Bank, expanding Islamic

management practices, enabling optimal Banking from credit to investment

shareholder returns (i.e.: better effective dividend intermediary to grow fee income

cash payout) and improved capital management. contributions, and tapping on cross border

opportunities of the various corridors.

*The RM4.45 billion Net Profit is based on 12-month ending 30 June 2011, while 2011 bar chart data is based on calendar year. The differing figures is due to fiscal period change in 2011.

3

Source: data.worldbank.org for GDP data

We Continue to Maintain Strong Capital & Liquidity Positions…

Capital Adequacy Ratio1 RWA Density1

21.50 CET1 (%) AT1 (%) Tier 2 (%) 62.2%

60.4%

18.90 18.68 18.40 17.90 52.2%

Maybank’s capital and 16.88 16.80 16.40 15.77 15.69 47.1%

49.4% 50.5%

risk-weight assets 13.70 41.2% 41.6% 41.8% 42.9%

density positions 28.7%

compare very favorably

relative to peers.

15.90

12.60

15.31

14.70

15.20

13.18

13.90

11.30

12.89

10.87

10.00

HSBC CBA Maybank UOB OCBC ICBC DBS ANZ SHINHAN BOC WOORI HSBC ANZ SHINHAN OCBC CBA Maybank DBS WOORI UOB ICBC BOC

Total Capital Ratio & CET1 Ratio Liquidity Risk Indicators

Total Capital Ratio CET 1 Ratio LDR LCR CASA Composition

Our past emphasis on

healthy liquidity and 151.9%

141.0% 142.0%

133.1% 132.4%

capital levels gave us an 19.29% 19.38% 19.02% 19.39%

18.68%

edge to enter this

pandemic from a

93.9% 93.4% 92.7% 92.4% 90.1%

position of strength.

15.73% 15.31%

14.77% 15.03% 42.8%

13.99% 36.0% 37.3% 35.9% 35.5%

FY2016 FY2017 FY2018 FY2019 FY2020 FY2016 FY2017 FY2018 FY2019 FY2020

Source: 1. Bloomberg data as at 31 March 2021. Note: Calculation of RWA density = RWA / Total Assets.

4

…Enabling Steady Shareholder Rewards & Better Cash Payouts up to FY19

Total dividend payout ratio consistently above 40-60% policy rate

Dividend (sen), Payout Ratio, Yield and Cash Component (%)

79.9% 78.5% 78.1% 78.5% 87.8% 91.2%

Dividend Payout 76.5% 74.9% 74.7% 71.9% 76.3% 77.3%

Ratio 100%

67% 53%

27% 20% 25% 19% 27% 34%

Cash Component 13% 11% 12%

of Total Dividend

7.3% 6.7% 7.1% 7.4%

Gross Dividend 6.2% 6.4% 6.3%

5.4% 5.6% 6.0% 6.1%

Yield

4.2%

65.0 64.0

60.0

57.0 55.0 57.0

55.0 53.5 54.0 52.0 52.0

#

Final 33 +

32 85.7%* 39

33 + 32

Interim 86.1%* 36.0 31 30 32

32 81.7%*

44 85.9%* 82.6%* 83.7%* 38.5

89.1%*

88.6%*

36 32 +

28 24 25

88.5%* 88.2%* 22.5 24 20 23 25

91.1%* 84.0%* 87.5%* 13.5

11 85.9%* 83.5%* 85.7%* 84.0%* 87.4%*

FY08 FY09 FY10

FY10 FY11

FY11 FP11

FP11 FY12

FY12 FY13

FY13 FY14

FY14 FY15

FY15 FY16

FY16 FY17

FY17 FY18 FY19 FY20

Effective Cash

Dividend Paid Out 60.4% 61.4% 26.2% 17.2% 17.0% 19.0% 22.0% 29.0% 23.2% 28.6% 57.2% 47.1% 87.8% 39.3%

from Net Profit

Note:

* Actual Reinvestment Rate for Dividend Reinvestment Plan. The r einvestment r ate for Final Dividend FY2020 is pending the execution of the 20th DRP.

+ The Final Dividend for FY2017, Inter im and Second Inter im Dividend (r eclassification fr om Final Dividend) for FY2019 wer e fully in cash.

# The Net Dividend is 28.5 sen of which 15 sen is single-tier dividend. Maybank adopted the single-tier dividend r egime with effect fr om FY2012.

• Effective Cash Dividend Paid Out for FY2020 is based on the actual r einvestment r ate for Inter im Dividend FY2020 and an 85% r einvestment r ate assumption for Final Dividend FY2020.

5

Maybank2020: Achievements in Key Strategic Objectives

The Top ASEAN Community Bank

To be a leading retail & commercial financial services provider in ASEAN,

leveraging our regional presence, banking expertise and growth opportunities in ASEAN.

Consumer adoption rate using Monetary transactions through Winner:

digital platforms: digital platforms (YoY growth): • Regional winner (Asia Pacific) for Best Website Design

2020: 66.1% 2020: 53.0% Award 2020 by Global Finance Magazine 2020.

2016: 36.3% 2016: 34.5% • Asia Trailblazer of the Year 2020 by Retail Banker

International Asia Trailblazer Awards 2020.

% of core product sales Regional Retail SME recorded • World’s Best Consumer Digital Bank Awards in Asia

generated through digital 8.4% five-year CAGR growth Pacific (Malaysia, Indonesia) by Global Finance Magazine

platforms: in loans: 2020.

2020: 78.6% 2020: RM32.7 billion • Best Digital Bank in Malaysia and Indonesia by Global

2016: 23.8% 2016: RM23.7 billion Retail Banking Innovation Awards 2020

Group Wealth Management recorded 8.3% CAGR growth in total Introduced many innovative and first-to-market digital solutions such as:

AUM over the last five years: • MAE by Maybank2u, a lifestyle app.

2020: RM244.0 billion • New and improved Maybank2u app with biometric and Secure2u features.

2016: RM177.7 billion • QRPay and Tap2Phone, affordable digital payment solutions for small

merchants.

• SME Digital Financing with 10-minute approval.

Leader in digital banking: • EzyQ, an online branch appointment system.

Largest market share in Malaysia with 60.7% in mobile • Fully digital real-time account opening for SMEs in Malaysia.

banking. • Video Know-Your-Customer (KYC) via Maybank2u, enabling fully digital

customer onboarding in Indonesia.

6

Maybank2020: Achievements in Key Strategic Objectives

The Leading ASEAN Wholesale Bank Linking Asia

To be the trusted ASEAN financial partner that links Asia

by leveraging our ASEAN leadership capabilities to deliver client solutions across Asia.

Bloomberg League Table

Leading Global Banking franchise in the country and region:

• Best Trade Finance Provider in Malaysia by Global Finance Trade & Supply Chain Finance MYR Islamic Sukuk

Awards 2020. 2020: 1

• Best Investment Bank in Malaysia by Euromoney, Global Finance, and Finance Asia. 2016: 1

• Best Broker in Southeast Asia by Alpha Southeast Asia

Malaysia Bonds

2020: 2

No. 1 Wholesale Bank in Malaysia by market share of Leading brokerage franchise in ASEAN and Top 5 in 2016: 2

loans, deposits and trade finance. Malaysia, Thailand and Indonesia.

Malaysia ECM

2020: 1

Maybank2E expanded ASEAN capabilities across the

ESG market leader in Malaysia: 2016: 1

region.

• Consistently ranked No. 1 on the

ESG League Table (Dealogic) since Global Sukuk

Group Asset Management’s AUM recorded five-year

2017 2020: 3

CAGR growth of 12.6% to RM32.6 billion in FY2020.

• Executed noteworthy ESG-driven 2016: 2

deals across the region such as

Net Promoter Score Total # of ASEAN DCM the LSS3 solar power projects ASEAN Local Currency Bonds

(NPS) in Malaysia: deals: financing, and Indonesia’s USD2.5 2020: 2

2020: 15 2020: 82 billion Sovereign Sukuk. 2016: 2

2016: 6.4 2016: 56

7

Maybank2020: Achievements in Key Strategic Objectives

The Leading ASEAN Insurer

To be a leading ASEAN insurer by

leveraging synergies between Maybank’s regional banking footprint and Etiqa’s expertise in Takaful & bancassurance

No. 1:

Expanded ASEAN footprint from Malaysia and Singapore NPS in Malaysia:

• General Takaful Provider in Malaysia.

to the Philippines (2014), Indonesia (2017) and Cambodia 2020: 24

• Online Insurer with over 66% market share

(2020). 2016: -7

in Malaysia.

Regular Premium/Contribution Bancassurance

Market Share in Malaysia:

2020: No. 1 (20.4%)

2016: No. 2 (17.3%)

Life/Family APE Bancassurance

Market Share in Malaysia:

2020: No. 1 (19.4%)

2016: No. 2 (16.0%) Implemented Insurance Introduced Etiqa’s

Advisor Model driving Smile App enabling

growth in customers to access the

Winner: bancassurance regular full extent of services

Highest ever revenue:

• Best Takaful Company 2019 (International Takaful premium, achieving No. including policy details,

RM11.27 billion in 2020

Awards) 1 position in Malaysia. service providers and

(in gross written

• Top Bancatakaful Producer 2020 (Malaysian Takaful claim submission.

premium).

Association)

8Maybank2020: Achievements in Key Strategic Objectives

The Global Leader In Islamic Finance

To continue delivering innovative client-centric universal financial solutions, building on our global leadership in Islamic Finance

NPS in Malaysia:

• Largest Islamic Finance Led the development of Islamic Finance in

2020: 33

Provider in Malaysia and Asia the region:

2016: -6

Pacific. • Joint lead arranger for one of the world’s

largest green Sustainable and Responsible

• Top 5 Islamic Bank globally by Investment (SRI) sukuk in 2019.

asset size Sukuk League Table

• Contributed and collaborated with

academic, educational and governmental MYR

bodies such as INCEIF, ISRA and IIUM to 2020: No. 1

develop Islamic Finance knowledge, learning 2016: No. 1

MGIB Contribution to Maybank Group and banking modules.

Assets Funding PBT Global

2020 :31.7% 2020: 35.7% 2020: 28.2% 2020: No. 3

2016: 26.9% 2016: 27.9% 2016: 21.2% 2016: No. 2

Winner:

• Global Islamic Bank of the Year (2014,

2015, 2020) – The Banker Awards

(Financial Times) Established Maybank’s

• Asia-Pacific Islamic Bank of the Year first branch in the

Introduced innovative products such as Investment (2016-2020) – The Asset Triple A Islamic Dubai-DIFC to drive

Account, HouzKEY and the first Shariah-compliant e- Finance Awards GCC-ASEAN flow.

wallet in Malaysia, MAE.

9Maybank2020: Achievements in Key Strategic Objectives

The Digital Bank of Choice

To be the digital bank of choice by

putting our customers’ preferences first and transforming to deliver next-generation customer experience.

Further enhanced customer experience by building partnerships, digital assets, platforms and capabilities such as:

Introduced various customer facing capabilities and innovations as Launched Maybank Sandbox as a regional collaboration platform for

mentioned across the four strategic objectives above, such as SME Digital FinTech developers to test out new ideas using real banking APIs.

Financing with 10-minute approval and MAE by Maybank2u lifestyle app.

Standardised and rolled out base applications and Straight-Through Introduced CARisMa (Capital Adequacy and Risk Management), an

Processing capabilities across the countries and geographies to serve our integrated system to better manage assets, liabilities and risks.

customers.

Established Maybank Labs to augment digital and analytical delivery for Built connections to partner ecosystems to allow seamless payments &

Maybank Group. customer experience, i.e. Grab, Lazada and Shopee.

Sealed strategic partnerships with Grab, SamsungPay, Alipay and Shopee. Rolled out FutureReady digital upskilling programmes for employees.

Increased in-house capabilities to manage and develop financial First local bank to introduce SWIFT gpi in 2019, enabling speedier,

applications and improve cyber defence capabilities. convenient and secure cross-border remittances.

Supporting community development, particularly during the pandemic:

• Launched Sama-Sama Lokal in 2020, a platform that enables small businesses to

operate online at no cost.

• Introduced MaybankHeart in 2016 – the first-of-its-kind digital social fundraising

platform for non-governmental organisations (NGOs).

10Maybank Is The Most Valuable Company in Malaysia

Company Market Cap Market Price No. of Shares PE Ratio

Rank

(Ranking as at 30 March 2021) (RM Bil) (RM) (in Bil) (times)

1 Malayan Banking Bhd 95.88 8.40 11.41 14.57

2 Public Bank Bhd 83.08 4.28 19.41 17.05

3 Petronas Chemicals Group Bhd 64.80 8.10 8.00 40.50

4 Tenaga Nasional Bhd 59.33 10.40 5.70 16.48

5 IHH Healthcare Bhd 47.67 5.43 8.78 240.27

6 CIMB Group Holdings Bhd 44.26 4.46 9.92 37.04

7 Press Metal Aluminium Holdings Bhd 40.87 10.12 4.04 89.40

8 Hong Leong Bank Bhd 40.75 18.80 2.17 15.37

9 Top Glove Corp Bhd 37.29 4.78 7.80 5.66

10 Maxis Bhd 36.38 4.65 7.82 26.12

Source: Bloomberg

11Leading Regional Financial Services Group

Largest Banking Network In Malaysia

Strong Financial & Leadership Positions within ASEAN

& Present in all 10 ASEAN Countries

2,626 51 Total Assets (USD bil)¹ Loans and Deposits (USD bil)¹

retail branches investment banking 286

DBS 492 DBS

worldwide branches worldwide 352

OCBC 395 UOB 213

246

UOB 327 OCBC 202

238

130

Maybank 213 No.4 Maybank 144 No.4

CIMB 150 CIMB 91

101

Bangkok Bank 127 Bangkok Bank 79

94

Kasikornbank 122 Public Bank 86

91

Public Bank 112 Krung Thai Bank 78

82

Krung Thai Bank 111 Siam Commercial 76

81

Siam Commercial 109 67 Loans Deposits

Bank Rakyat Indonesia 81

PATAMI (USD mil)¹ Market Capitalisation (USD bil) 2

DBS 3,448 DBS 55.0

OCBC 2,412 Bank Central Asia 54.2

Bank Central Asia 1,865 OCBC 39.4

UOB 1,682 Bank Rakyat Indonesia 38.2

UOB 32.2

Maybank 1,542 No.5 No.6

Maybank 23.1

Bank Rakyat Indonesia 1,280

Bank Mandiri 20.3

Bank Mandiri 1,176

Public Bank 20.0

Public Bank 1,160 Siam Commercial 12.2

BDO Unibank 1,005 Kasikornbank 11.1

Kasikornbank 917

Note :1 As at 31st December 2020. 2 As at 30th March 2021

Source: Bloomberg. Note: Except for Market Capitalisation, Maybank’s figures are computed based on internal exchange rate assumptions. The deposit balances for Maybank and CIMB are 12

inclusive of Investment Accounts.Over the Past Decade (Prior to COVID-19 Pandemic), Banks in Our Home Markets Have Seen ROEs Decline… …with Maybank’s ROE declining at a relatively slower gradient and remaining above its reducing cost of equity (

Operating Context Against these emerging macroeconomic and social trends, our next five year strategy was designed… Humanising Financial Services

Our Operating Context (1/2)

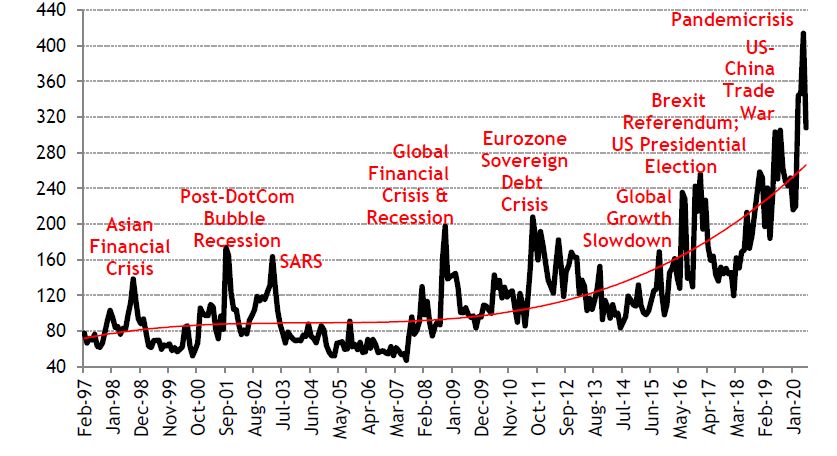

Global Economic Policy Uncertainty Index 1 Decreasing industry ROE trajectory 2

We have seen

30.00

heightened uncertainty

in the global economy in 25.00

the past five years, 20.00

impacting the banking

15.00

sector ROEs.

Exacerbating this 10.00

environment is the 5.00

recent pandemic- 0.00

induced uncertainties. 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 YTD

MY Banks SG Banks ID Banks

Global Average Interest Rates (% p.a.)3 ASEAN Central Banks Have Slashed Policy Rates Amid the Pandemic Crisis4

Given the volatility

globally and slowing

economic growth, we

have been experiencing

a prolonged low interest

rate environment since

the Global Financial

Crisis, with new interest

rate lows seen in 2020.

Source: 1) “ASEAN X Macro Global Economy Update: The Good, The Bad, The Uncertain” by MKE Research @ 7 Aug 2020 2) S&P Global Market Intelligence 3) “ASEAN Macro Year Ahead:

2021 Recovery & Reopening” by MKE Research @ 7 Dec 2020 4) “Year Ahead 2021: ASEAN – Herd Immunity & Escape Velocity” by MKE Research @ 7 Dec 2020 15Our Operating Context (2/2)

Tech Investment in ASEAN Stayed Resilient at USD5.6 bn Mobile Banking App Users Jumped the Most in

Investment trends in 1H20, more than Double the Amount in 2H19 1 Vietnam, Philippines & Indonesia 2

continue to show

increasing spend on

digitalisation efforts

across ASEAN, even

during the recent

pandemic, with more

users being on-boarded

on digital banking

platforms.

Per for mance of MSCI ESG index vs MSCI

Companies with high

Environmental, Social

and Governance (ESG)

performance relative to

Asia ex-Japan index

their sector peers have

done well and continue

to attract capital.

Yr

Source: 1) & 2) “ASEAN X MACRO The Post-Pandemic Normal” by MKE Research @ 13 Nov 2020 3) “Sustainability: New Directions, Expanding Opportunities” by MKE Research @ 20 Oct 2020

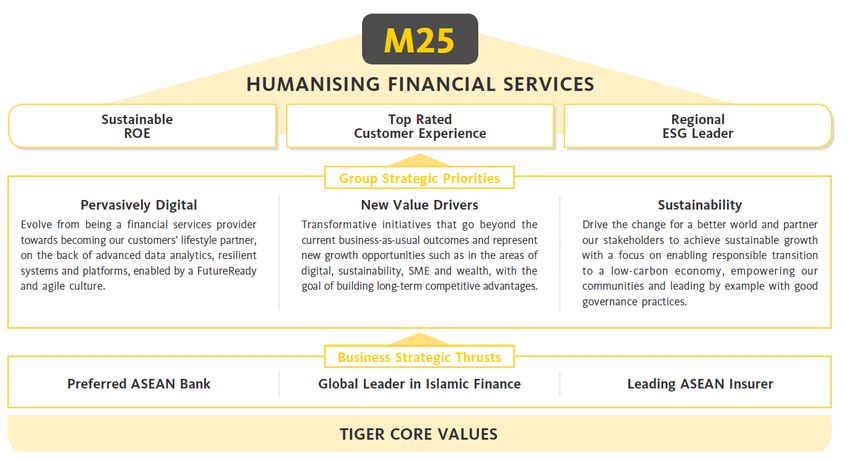

16M25 Refreshing our mission and anchoring our strategy on three priorities Humanising Financial Services

Humanising Financial Services

Our purpose has been refreshed to reflect long-term priorities and a new operating landscape

HUMANISING FINANCIAL SERVICES

Being at the heart of the community,

For our stakeholders: To create the following impact:

we will:

• Make financial services simple, Customers Employees

Empowering Everyone

intuitive and accessible • Best-in-class customer • Growth and capability building

to thrive and advance their ambitions

experience • Inclusiveness, diversity and

• Build trusted partnerships for a • Convenient access to well-being

sustainable future together financial services (digital & Poverty Eradication

physical) Regulators with financial inclusion & improved livelihoods

• Fair terms & pricing; • Standard-bearer for the

• Treat everyone with respect, dignity, advisory based on needs industry

fairness and integrity • Transition support to • Professionalism and business Reduced Inequalities

sustainable practices ethics across populations, geographies, gender, etc

Shareholders Communities

• Sustainable and responsible • Financial inclusion and Clean & Sustainable Environment

returns empowerment through low carbon economy, green

• Strong governance and • Commitment to low-carbon infrastructure

transparency economy

Stronger Institution

via responsible practices, future-proofing

resilience

18Maybank’s Next Five-year Strategy: M25

Anchored on our purpose of Humanising Financial Services

19Group Strategic Priorities

Pervasively Digital

• Pervasively Digital represents our digital efforts to strengthen and deliver more value to the stakeholders, guided by the Core

principles of Experience, Trust and Resilience.

The Core Principles guide.. .. Our Focus Areas… … which is enabled by:

• Workforce capabilities powered by new/digital

• Customer Engagement Platforms skills and rethinking models

• Digital Ecosystems • Systems, policies and processes that support

EXPERIENCE TRUST

mobile workforce and agility

• Data Monetisation Strategy

• Expansion of Robotic Process Automation

• Customer 360 view

CUSTOMERS • Strengthened core and auxiliary systems

• Deepened Engagements • Integrated data system

• Reforms in Distribution • Enhanced cash management flow

RESILIENCE • Partnership Ecosystem • Multi-cloud tech platforms for quicker server

• Exploration of New Opportunities provisioning and scale

• Micro-service platforms for speed and agility

• Our goal is to evolve from being a financial services provider to becoming our customers’ lifestyle partner and build wraparound

experiences within our services, products and platforms.

20Group Strategic Priorities

New Value Drivers

• New Value Drivers go beyond the current business-as-usual (BAU) and represent new business growth opportunities covering

SME, wealth, trade, ESG and digital. These are transformative initiatives meant to help us grow over the long-term and

sustainably build our competitive edge.

Group Community Financial Services Group Global Banking Group Islamic Banking Group Insurance & Takaful

• Driving financial inclusion for SMEs • Digitalising end-to-end Wholesale • Re-imagining the Islamic Banking • Scaling up digital insurance

through digital and data-led solutions Banking customer experience business by expanding from through strengthened digital

• Strengthening wealth proposition with credit to investment position, delivering best Auto

one-stop Universal Banking solutions intermediation digital solutions and becoming

the preferred digital banca

partner

• We aim to defend and grow our customer base, generate income more effectively & efficiently, provide beyond financial

services, and fortify our propositions in the different markets we serve.

21Group Strategic Priorities

Sustainability

• We aim to drive the change for a better world and partner clients to achieve sustainable growth.

• Our sustainability agenda is predicated on three key pillars: enabling responsible transition to a low carbon economy,

empowering our communities and leading by example with good governance practices.

Responsible Transition Enabling our Communities Our House is in Order &

1 2 3 We Walk the Talk

Enable transition to a low carbon economy Building community resilience across ASEAN, Leading by example with good management

balancing environmental and social imperatives undertake responsive action to promote practices and ensuring that Maybank’s ESG

with stakeholders’ expectation economic development and social well-being strategy is based upon a strong foundation

• Supporting the Transition to a Low-Carbon • Empowering Communities • Governance and Compliance

Economy • Financial Inclusion • Privacy

• Developing Sustainability Focused Products • Climate Resilience • Our Supply Chain

& Services • Transparency and Trust • Our Environmental Impact

• Systemic Risk Management • Diversity, Equity and Inclusion

• ESG integration in Financial Analysis

• Engaging our People in Sustainability

• Business Ethics

• Financing Commitments:

No Deforestation, No New Peat, and No Exploitation (NDPE) stance approved by the Board in January 2020 (which

applies to all relevant sectors including but not limited to palm oil, forestry and logging, construction and real estate).

The Group will not provide financing to black listed activities deemed not in line with the Group’s core values.

No financing of new coal activities (transitioning together with existing borrowers to achieve sustainable renewable

energy mix over medium- to long-term)

22Business Strategic Thrusts

Preferred ASEAN Bank – Group Community Financial Services

Group Community Financial Services aspires to be the “Most Preferred Community Bank” through:

AIM HOW? OUTCOME

Attain

• Strengthen our position in home markets; create a digital eco-system and marketplace – Grow ≥3x

Forefront Position improve SME commerce capabilities and enable connectivity between SMEs and end-consumers borrowing base in MY

in the SME Space

> 5.0x

• Enhance data analytics capabilities – shift towards advanced analytics to better drive customer Avg product holding

Data and Digital-led centricity solutioning and offerings

≥ 80.0%

Strategy • Continue to build and upscale our digital banking capabilities and propositions – enable

Digital sales contribution and

seamless product and service delivery across the region

digital customer penetration

rate

• Position ourselves to be the Universal Private Bank – gateway to full suite of financial offerings

Fortify Our ranging from retail to corporate solutions 2x growth in

Wealth Management

• Enable regional Private Wealth borderless customer experience – via consistent enhancement Private Wealth Customers

Propositions

of delivery of product and services across our markets

23Business Strategic Thrusts

Preferred ASEAN Bank – Group Global Banking

Group Global Banking aspires to be the “Valued ASEAN Banking Partner Globally’ through:

AIM KEY ENABLERS STRATEGIC INITIATIVES OUTCOME

BUSINESS MODEL SHIFTS • Client segment diversification for optimal risk-return profile >50% five-year

Effective Balance Sheet • Ramp-up flow business by driving GM-TB sales franchise CAGR from New

Undisputed No.1 In Management, Income • Investment Banking & Investment Management (IM) propositions Profit Drivers (NPD)

Malaysia Diversification & Structural for IB & AMG

• Building community resilience across ASEAN, undertake responsive action

Shifts to promote economic development and social well being. income

10% - 15%

CLIENT SERVICING MODEL VIA

• Platform to automate end-to-end on boarding and credit processing improve TAT

The Partner Of DIGITAL BREAKTHROUGH

Infrastructure building to

Choice For Our deliver superior client

>40% five-year

• Trade, treasury and cash platform optimisation to provide integrated flow CAGR from NPDs for

Clients Globally experience & improve solutions Trade, Treasury &

productivity

Cash Mgt income

Efficient, Value INTERNATIONAL • Reposition our focus in key international markets (SG, ID & Greater China)

through targeted segments, infrastructure building, cross-border solutions >50% five-year

GO-TO-MARKET STRATEGY

Generating and tapping into intra-ASEAN and ASEAN+ corridors CAGR from NPDs for

Focus on business with

Regional Banking income through

sustainable returns • Invest in capacities, infrastructure and capabilities in CLMV & the

Franchise cross-border flows

Philippines to complete our flow business proposition

24Business Strategic Thrusts

Global Leader in Islamic Finance

Group Islamic Banking aspires to be a Global Leader in Islamic Finance through Financial Resilience, Global Prominence and

Thought Leadership in Sustainable Finance, Product Innovation and Shariah through:

EXPANDED BUSINESS MODEL WHY? HOW? OUTCOME

Credit Intermediation • Embrace the risk-sharing model that is more • Introduction of multiple funds under Multi-Asset Investment RM2 billion

equitable in terms of risk-return Account (MAIA) Revenue

Investment Intermediation • Reduce reliance on balance sheet • Investment Account (IA) as Capital Raising Instrument (Over 5 Years)

• MAIA/ IA as Capital Raising Instrument

Fund-Based Income 30%

• Reduce reliance on balance sheet • Islamic Estate Planning (IEP) and Investment Solutions

Fee-Based

• Manage cost of capital more efficiently under Islamic Wealth Management (IWM)

Fee-Based Income Income Composition

• Amplifying trade financing solutions for Halal industry

• Reduce costs and widen the reach of our products

Traditional • Adoption of Group CFS Digital Ecosystem initiatives

and servicesBusiness Strategic Thrusts

Leading ASEAN Insurer

Etiqa aspires to be “A Leading ASEAN Insurer” in line with its purpose of “We Want To Make The World A Better Place” by putting the

interests of our customers & communities first and providing protection & wellness offerings to as many people as possible.

AIM OUTCOME

No.1 Digital Insurer Be the Grow our PBT Continue to be

Of Choice in ASEAN

#3 ASEAN with a CAGR of 12% Agile & have SCRUM

owned insurer over the next 5 years as a key enabler

More than Establish an Remain focused on being

All Things Auto Double our Topline Auto platform Fast & Easy to deal with

with a CAGR of 15% that goes beyond & giving the Best Advice

over the next 5 years Insurance to our customers

Banca Preferred Retained our #1 Bancassurance Expanded our #1 Digital Insurer

Partner position while securing a position across the Region while

broader base of Banca partners offering personalised services online

26M25 Targeted Outcomes

Drivers behind ROE uplift

To improve a BAU potential ROE of around ~11.5% by 2025, we have identified New Profit Drivers (NPD) that will bring us closer

towards achieving our aspirational ROE of between 13%-15% by 2025.

• Digital: Continuously enhance STP capabilities, drive customer engagement &

Group

stickiness.

Community

Aspirational ROE • Group Private Wealth: Leveraging regional platforms and targeting niche and

Financial

neglected segments.

Services

Etiqa • SME: Digitise sales in home markets (i.e.: RSME loans) and enabling lateral

(GCFS)

connectivity to SME customers across our home markets.

NPD

• IB & IM: Prime brokerage, investment and asset management ESG centric growth

MGIB’s NPDs are embedded

Group Global • Capture cross border flows from SG-MY and ASEAN+ corridors.

GGB

Banking • Automate end-to-end onboarding and credit processing.

across the 3 pillars

(GGB) • Optimise trade, treasury and cash platforms so flow business for GB & CFS clients

remain relevant

BAU ROE: • Expand role from an Islamic Bank to investment intermediation, to drive Islamic

~11.5% Group Islamic fee-based income contribution to Group.

Banking • Develop Wealth Management business in home markets through product innovation

GCFS (MGIB) and prioritising customer experience, as well as linking investors from Dubai and

Brunei to our home markets.

Group

• Digitising sales to become No. 1 Digital Insurer of Choice in ASEAN.

FY25 ROE: NPD Insurance &

• To become preferred banca partner leveraging digital tools.

BAU + NPD Breakdown Takaful

• Expand Auto digital service offerings.

(Etiqa)

27M25 Targeted Outcomes

Desired Long-Term Outcomes

Build top-notch experience for our • Mobilise RM50 billion in Sustainable

customers via digital and hybrid services Finance by 2025.

13-15% 100 sen 40-60%

Dividend • Achieve 1 million hours p.a. for

Earnings per Conversion

share

payout ratio sustainability and delivering 1

(net cash basis) Rate thousand significant UN-SDG related

outcomes by 2025.

28MALAYAN BANKING BERHAD 14th Floor, Menara Maybank 100, Jalan Tun Perak 50050 Kuala Lumpur, Malaysia Tel : (6)03-2070 8833 www.maybank.com Disc laimer: This presentation has been prepared by Malayan Banking Berhad (the “Company”) for information purposes only and does not purport to contain all the information that may be required to eva luate the Company or its financia l position. No representation or warranty, express or implied, is given by or on beha lf of the Compa ny as to the accuracy or completeness of the information or opinions contained in this presentation. The presentation does not constitute or form part of an offer, solicitation or invitation of any offer, to buy or subscribe for any securities, nor should it or any part of it for m the basis of, or be relied in any connection with, any contract, investment decision or commitment whatsoever. The Company does not accept any liability whatsoever for any loss howsoever arising from any use of this presentation or their contents or otherwise arising in connection therewith. Humanising Financial Services

You can also read