INVESTOR INFORMATION Q1 2019

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

INVESTOR INFORMATION Q1 2019 Published May 1, 2019

2

Canada’s leading integrated energy company

$85B ~940 mbpd ~600 mbpd 28+ years ~460 mbpd ~1750

Enterprise value1 Oil production Heavy upgrading 2P Reserve life Refining nameplate

Retail sites4

As at March 31, 2019 nameplate capacity2 nameplate capacity2 index3 capacity2

1, 2, 3, 4 See Slide Notes and Advisories

3

Suncor – A resilient business focused on shareholder returns

Cash flow growth Cash generation

Strong potential FFO1 increase largely independent of market conditions Significant upside FFO1 sensitivity to WTI, based on TTM5 actuals

US$62.80 WTI, 0.76 C$/US$, US$18.00 NYH 3-2-1 crack spread

~5% CAGR2 (C$ billion)

$16

(Based on 2019 price guidance)

TTM average production 750 mbbls/d

$14

$12

Debottlenecks, $10

cost reductions $8

Fort Hills, and margin

Syncrude, improvements $6

and Hebron $5.5B Sustaining capital6 + dividend

$4

$2 $2.8B Sustaining capital6

$0

1

2018 FFO Production Free funds flow 2023E FFO1 $60 $63 $70 $75 $80

TTM

growth 3 growth 4 WTI ($USD)

Shareholder returns Resilience

Commitment to reliable returns through the commodity cycles Managing the balance sheet as a strategic asset

Dividend per share7 Liquidity

Buyback per share7,8,9

Anticipated buyback per share7,9

Dividend + buyback yield

7% $5 3B . $1.9B cash and $3.4B in available lines of credit

As at March 31, 2019

—

5% 5%

A low Credit rating

Investment grade

1.14 3% 3%

0.85 1.88

Baa1 DBRS (A Low) Stable, S&P(A-) stable, Moody’s (Baa1) Stable

WTI FFO Break-Even10 (USD)

1.02 1.14 1.16 1.28 1.44 1.68 ~$45 Sustaining capital6 + dividend

2019

2014 2015 2016 2017 2018 2019E

1, 2, 3, 4, 5, 6, 7, 8, 9, 10 See Slide Notes and Advisories.

4

Multi-year focus on structural free funds flow growth1,2

Production

growth5 Growth

Free funds In situ replication

flow growth

projects1,5 Opportunistic

Production share buybacks

Debottlenecks, cost

growth reductions & margin

Fort Hills, Syncrude improvements

and Hebron ~4% anticipated Sustain the business &

~5% anticipated production CAGR

continually grow the

~10% anticipated FFO CAGR (Refer to slide 9) dividend

production growth

per share4 (Refer to slide 8) 2023/2024 forward2

2020 – 2023 Structural FFO3 growth

2019 – 2020 & balance sheet strength

(Refer to slide 7)

1, 2, 3, 4, 5 See Slide Notes and Advisories.

5

The Suncor business advantage

Long life, low decline Unique business Financial strength

and low cost integration through market cycles

~800 mbpd 2019 production guidance midpoint5

~1000 mbpd of conversion capacity6

Resilient free funds flow8

~31yrs ~600 mbpd of heavy upgrading capacity7

~$93

~$65

Oil Sands 2P ~$49 ~$51

~$43

Reserve Life Index1

Oil

E&P Sands ~$10.2B

Resources ~$9.0B ~$9.1B

~$6.8B

Minimal Suncor’s ~560mbpd ~$6.0B

turnaround year

Fort McMurray

Major planned

upgrading

decline

forest fires

McMurray

~1% anticipated near term oil

Fort

sands decline rate2

2014 2015 2016 2017 2018

Dividends Sustaining Capital

Suncor’s 8

~460mbpd Discretionary Free Funds Flow WTI Average Price

refining

network

~$30 Capital discipline

2018 Oil Sands operations

sustaining capex + cash cost 1.6x Net debt to FFO9

USD / bbl3 1.5x under the previous leasing standard10

Global Global Target < 3x

markets markets

30% Total debt to capitalization

28% under the previous leasing standard10

Target 20-35%

~$45 Suncor and 3rd party

global markets $5.3B Liquidity

2019 break-even4 WTI (USD) Cash & cash equivalents ($1.9B) plus

sustaining capital + dividend Available credit facilities ($3.4B)11

1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 11 See Slide Notes and Advisories.

6

The foundation of our business

Operational excellence

Reliability

Continuously improve the reliability of our business

Personal and process safety

Journey to Zero – goal to eliminate all workplace incidents

Cost management

Continuous focus on structural cost reduction initiatives

Environmental excellence and sustainability

Aiming to improve environmental performance, go beyond compliance in key areas Autonomous Haul Systems can reduce costs by ~$1/bbl1 and

improve safety, productivity, reliability, and environmental

performance

Capital discipline

Flexible allocation plan

Significant portfolio of high quality assets across the business

Balance sheet strength

17 years of dividend increases2

% Q1 2019 dividend increase

Opportunistic share buybacks

Liquidity and strong investment-grade credit rating through the commodity cycle

80 $100

Shareholder returns 60 $80

$60

Competitive & sustainable dividends, opportunistic share buybacks 40

$40

20 $20

Profitable growth 0

2013 2014 2015 2016 2017 2018

$0

Strategic acquisitions & divestments; high-quality organic growth potential

Shares WTI

1, 2 See Slide Notes and Advisories.

7

Capital discipline – flexible capital allocation plan1

$10/bbl increase in Brent price would generate approximately $2.4 billion of additional FFO2

Capital commitment Discretionary capital

Balance

Sustained Production

sheet

price growth to

leverage Sustaining Buyback4

outlook* 20203 Dividend4 Growth Capital1

metrics Capital1,6 target

Invest

8

Medium-term investment proposition1 – free funds flow2 growth

Free funds flow2 improvement potential for years 2020 - 2023 inclusive3 Examples of anticipated high return investment opportunities3

Excluding commodity price changes & largely independent of production growth

Suncor – Syncrude pipeline Tailings management

investment savings

$2.0B ~$200M at >25% IRR ~$4 per bbl

Potential to

deliver Conservative return based on Average go forward expected sustaining

incremental planned outages capital, reclamation & opex savings for

free funds base plant mined bitumen versus

flow2 of

~$500M/yr

Further potential value upside 2018 spend

including mitigation of unplanned

outages and product sharing during Tailings placement in pit - less land use

normal operations Less tailings transport & handling

Growth Margin Opex savings Sustaining Total value add (slide 21 for further details) Accelerated dewatering of ponds

improvements capital savings (slide 23 for further details)

Examples of short lead time & high quality initiatives independent of commodity market conditions

Growth Margin improvements Opex and sustaining capital savings

Asset synergies

E&P Coke fired boiler replacement Coordinated maintenance strategy, timing, materials, critical trades, etc.

Value developments & Cogeneration with lower cost, high efficiency

asset extensions steam and power revenue upside AHS4 deployment

Base mine & Fort Hills implementation

Suncor - Syncrude pipeline

Optimizing Syncrude assets & Suncor’s sour

Supply chain optimization

Debottlenecks Equipment standardization and inventory consolidation/reduction

Fort Hills, MacKay River & SCO margins

Firebag processing facilities

Supply & trading Tailings management

Value chain optimization Implementation of PASS5

Digital technology adoption

Wireless employee badges (worker safety & optimization), Advanced process analytics (operational optimization), Robotic process automation (cost reduction), etc.

1, 2, 3, 4, 5 See Slide Notes and Advisories.

9

Longer term organic growth – Replication1

Targeting less than $50 WTI (USD) cost of capital breakeven1

Planned phases of 40 mbpd next

~10 generation in situ facilities (replication)

Phases submitted for regulatory approval

7 2 approved and 5 pending approval

2023/24 Potential first oil from first phase 3

Months expected between first oil

12 to 15 from successive phases

360+ Mbpd production growth plans2

Potential replication production growth profile

400

Replication facilities approved by

300 the regulator

Replication facility application

mbpd

submitted

200

100

0

2023 2025 2027 2029 2031 2033

1, 2, 3 See Slide Notes and Advisories.

10

Disciplined cost management

History of structural cost reductions Medium-term cash operating

Consistent reduction in Oil Sands operations cash operating costs (C$/bbl)

(Fort Hills and Syncrude cash operating costs are not included)

cost targets4 (C$/bbl)

$40 Oil Sands1 Oil Sands ≤ $20/bbl

$37.00

Fort Hills ≤ $20/bbl

Reflects a heavy Syncrude ≤ $30/bbl

maintenance year

Mining2

$27.55 Enterprise-wide

$25.55

cost reduction initiatives

$25.25 Operational

Improved reliability across assets

$20 through sharing technology and

In situ3 procedures, coordinated maintenance

$16.50 planning and asset connectivity

Technology

Technology applications such as

robotic process automation, advanced

analytics, Autonomous Haul Trucks

$8.45 and Artificial Intelligence

Supply chain & business processes

Improved cost and efficiency across assets

$0 through contractor and parts

2013 2014 2015 2016 2017 2018 standardization, bulk procurement and

streamlined processes

1, 2, 3, 4 See Slide Notes and Advisories.11

Generating discretionary free funds flow1

FFO2 consistently exceeds sustaining capital, associated capitalized interest and dividends (C$ billions)

$12

$10

$10.2

$8 $9.1

$6

$6.8

$6.0 $2.3

$4 $2.1

$1.6 $1.9

$2 $3.9

$2.7 $3.0

$2.3

$0

2015 2016 2017 2018 2019E

WTI US$3 $48.75 $43.35 $50.95 $64.80 $58.00

NYH 3-2-1 US$4 $19.70 $14.05 $17.70 $18.00 $17.00

Sustaining capital Dividend FFO2 Illustrative 2019 FFO2,5 2019 Estimated sustaining capital6 + dividends7

1, 2, 3, 4, 5, 6, 7 See Slide Notes and Advisories.12

Returning value to shareholders

17 consecutive years of dividend increases1 & opportunistic share buybacks with increased share repurchase program2

17% $0.42 ~$5 billion ~$514 million $2 billion

Share repurchases Share repurchase

Q1 2019 dividend Q1 2019 dividend per NCIB programs executed3

completed program commenced

increase share (May 2017 - Dec 2018)

(Jan 2019 - Mar 2019) March 20194

$100 Expected buyback in 20192 $3.50

Buyback per share (Actual)2,5,6,7

Buyback per share (Expected)2,5,7

$3.00

Dividend per share5

$80

WTI US$

Dividends $2.50

expected to

$60 grow in line

with $2.00

C$/share

US$/bbl

sustainable

FFO8

$1.50

$40 increases7

$1.00

$20

$0.50

$0 $0.00

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

1, 2, 3, 4, 5, 6, 7, 8 See Slide Notes and Advisories.13

Strong balance sheet

1.6x Net debt to FFO1

Net debt to FFO1 1.5x under the previous leasing standard2

Has remained within target range throughout all price cycles Target < 3x

30% Total debt to capitalization

97.95 28% under the previous leasing standard2

94.20 93.00 Target 20-35%

WTI $5.3B Liquidity

($US/bbl) Cash & cash equivalents ($1.9B) plus available credit

facilities ($3.4B)1 as at March 31, 2019

64.80

54.90 A Investment grade credit rating

48.75 50.95 DBRS Rating Limited (A Low) Stable

low

Standard and Poor’s Rating Services (A-) Stable

43.35 Baa1 Moody’s Corp (Baa1) Stable

3x

2.4 Manageable debt maturity profile3

(C$ billion)

Increase due to new

leasing standard2

1.7

Target range

2019-2020 $0.2

1.6

1.4 1.5

2021-2024 $2.7

0.9 2025-2029 $1.5

0.7 0.7

2030-2034 $1.7

Net debt to FFO1 2035-2039 $5.1

0x 2040-2047 $1.5

2012 2013 2014 2015 2016 2017 2018 2019 Q1

1, 2, 3 See Slide Notes and Advisories.14

Generating industry-leading FFO1 per barrel and shareholder returns

Delivering leading FFO1 per barrel2 and shareholder returns despite Canadian oil differential headwinds,

demonstrating the value of our integrated business model and global competitiveness

Quality cash flow Shareholder returns

Reliable quality cash flow from Suncor’s unique Growing dividends and executing opportunistic

integrated business share repurchases with sustainable discretionary

free funds flow

FFO1/boe WTI Total cash yield

($US/boe) ($US/bbl) (dividend + buyback)

$60 120 10%

9%

$50 100

8%

7%

$40 80

6%

$30 60 5%

4%

$20 40

3%

2%

$10 20

1%

$- 0%

2012 2013 2014 2015 2016 2017 2018 2012 2013 2014 2015 2016 2017 2018

Suncor WTI Oil Sands peer range3 Supermajor peer range3 Suncor dividend yield4 Suncor buyback yield5

1, 2, 3, 4, 5 See Slide Notes and Advisories.15

Return on capital employed1 past the inflection point

Suncor's spending on major capital projects Fort Hills and Hebron completed

The 50-year, long-life, low-decline production profile of Fort Hills has begun

Focusing on near-term low capital intensity and high value added projects2

Debottleneck existing assets, product margin improvements and further cost reductions

ROCE1 compared to supermajors

20% $100

$80

15%

$60

10%

$40

5%

$20

0%

2013 2014 2015 2016 2017 2018 $0

-5% -$20

Supermajor peer range 3 Suncor WTI (US$/bbl)

1, 2, 3 See Slide Notes and Advisories.16

The value of Suncor’s integrated business

Benefiting from our crude and product strategy through all market cycles

Exposure to high value product pricing provides significant cash flow upside potential

BRENT E&P production attracts Brent based pricing

PRICING ~110 mbpd Offshore production with access to tidewater

SYNTHETIC Bitumen conversion to a higher value synthetic oil1

PRICING ~600 mbpd Heavy upgrading capacity1

GLOBAL

Oil sands bitumen with direct access to global markets

HEAVY

PRICING

~100 mbpd Logistical flexibility for non-upgraded bitumen

GLOBAL Suncor’s refined products capacity1 sold for global pricing

PRODUCT

PRICING

~460 mbpd ~260 mbpd of oil sands synthetic and heavy feedstock capability2

Remaining light oil feedstock purchased in the market

Integration between upstream, midstream & downstream businesses

minimizes downside risks from differential volatility

Heavy differential sensitivity Synthetic differential sensitivity

Up to $25M FFO3 impact anticipated (CAD) per $1 annual Between $20M to $40M FFO3 impact anticipated (CAD) per $1

change (USD) in a normalized Western Canadian L/H4 annual change (USD) in a normalized synthetic to WTI benchmark5

1, 2, 3, 4, 5 See Slide Notes and Advisories.17

IMO1 2020 – Positive FFO2 impact expected for Suncor

Expect IMO1 regulatory change will enhance demand for middle distillates used in new marine fuel

Projected impacts Suncor advantages

Decreasing global demand for bunker fuel3 Minimal exposure to bunker fuel

Sales from Suncor refineries (~1%)

Widening global L/H4 differentials Minimal impact of widening L/H4 spread18

Regional synergy opportunities1 for existing assets

Crude logistics

Upgrader feedstock optionality from multiple oil sands assets

Crude feedstock optionality for Edmonton refinery

Supply chain

Sparing, warehousing and supply chain management

Consolidation of regional contracts (lodging, busing, flights, etc.)

Operational optimizations

Unplanned outage impact mitigations

Turnaround planning optimization

Process and technology sharing

100% WI

Joint ownership

Base mine upgrader and terminal

Assets and resource developments U Syncrude upgrader

Lease development and asset utilization optimization C In situ central processing facility

P Fort Hills primary/secondary extraction

Pipelines

Proposed bi-directional pipelines1

1 See Slide Notes and Advisories.19

Market access for Suncor’s oil sands production

Suncor has made strategic investments in refineries and current/proposed logistics infrastructure

to mitigate Alberta egress limitations and market disconnects

Fort McMurray ~750 Alberta

egress bottleneck

does not impact

the ability to move

Suncor barrels1

142 Edmonton

Hardisty Enbridge Line 3

Potential Markets

Regina Central & Eastern

Vancouver Cromer Canada, US Midwest

& Gulf Coast

137

Montreal

TMEP Potential Superior

Markets

Asia & California 85

Sarnia

Steele City Chicago

98

Denver

Patoka

San Francisco Suncor refinery capacity

mbpd

Cushing Industry approximate rail

Pipelines Los Angeles

KXL Potential mbpd loading capacity in

(current and forecasted gross capacity2) Markets AB/SK

Feeder lines

Heavy oil refineries

Trans Mountain Pipeline, TMPL (300 mbpd)2 along the Gulf Coast

Trans Mountain Expansion , TMEP – Proposed3 (+590 mbpd)2

Express, Platte and Rocky Mountain (280 mbpd)2 Houston/Texas City

TransCanada Keystone (590 mbpd)2

TransCanada Keystone XL – Proposed3 (+830 mbpd) 2

Enbridge Mainline (2,600 mbpd)2

Enbridge Line 3 – Proposed3 (+370 mbpd) 2

Enbridge Line 9 (300 mbpd)2

Flanagan South Pipeline (585 mbpd)2

Marine opportunities

1, 2, 3 See Slide Notes and Advisories.20

Fort Hills – Leading deployment of mining technologies

Higher quality, fungible product Enhanced reliability & efficiency

Secondary extraction – Paraffinic Froth Treatment Autonomous Haul Systems

Bitumen froth mixed with solvents to remove water and minerals Heavy haulers are AHS ready, full deployment expected by 2021

Greater reliability & productivity

Designed to run 24/7 with no “breaks”

Shipped Lower costs

~$1/bbl opex savings1

>75% bitumen directly to

market Safer operations

~10% asphaltenes

Minimizes human interface in the mine, obstacle detection

2% water & sediment

back into Improved tailings technology

mine pit

Use of thickener process and PASS

Partially upgraded In process rapid dewatering coupled with in pit tailings storage

Higher value due to reduced asphaltenes content

Reduced energy intensity & operating costs

Lower GHG emissions Flocculant2 added in process to aid in dewatering tailings

In line with the average crude refined in the U.S.

Warm water from rapid dewatering is reused in the plant

Less diluent required Resulting lower energy demand reduces costs and GHG emissions

~20% diluent mix vs. ~30% for in situ barrel transportation

Faster reclamation

Fungible product Partially dewatered tailings feed into PASS process (slide 23)

Meets pipeline, refinery specifications, no further upgrading

1, 2 See Slide Notes and Advisories.21

Syncrude – Following Suncor’s proven reliability journey

Suncor base plant upgrader reliability 91% 91%

Multi-year journey to reach >90% reliability 90%1

Reliability step-change after 4 years

83% Not a gradual profile

81%

interconnect pipeline

80%

Firebag to basemine

79%

fully operational

Suncor began focusing on upgrader reliability initiatives in 2011

Culture – Operational excellence mindset

Process – Integrated maintenance strategy/approach

Infrastructure – Asset integration between Firebag and base plant

2011 2012 2013 2014 2015 2016 2017

Syncrude plant reliability

A similar multi year journey targeting >90% reliability2

2016 2017 2018 2019 2020/21 (Target >90% reliability &22

ESG leadership

Environment

Regulatory & policy leadership GHG & water performance Technology & innovation

Operate under one of the most stringent, >60% reduction in Oil Sands Base GHG emissions $635M in technology investments in 20184

transparent and compliance-focused regulatory intensity since 1990

Significant new technology deployment

frameworks1 Goal to reduce corporate GHG intensity by 30% PFT, AHS, PASS, NCG co-injection5

Participation in government-led initiatives to by 20302

External collaboration

advance leadership in Canada’s O&G sector Estimated carbon cost for upstream production is up to

Canada’s Oil Sands Innovation Alliance (COSIA)

(e.g. 2018 co-chair Resources of the Future) $0.60/bbl3 over the period 2018-2027

Clean Resource Innovation Network

A strong voice for practical, effective policy and ~30% reduction in water use intensity at Oil Sands NRG COSIA Carbon XPRIZE

regulation development and design Base vs. the prior 4-year average EVOK Innovations

(e.g. Bill C-69 amendments)

Social Governance

Advancing Aboriginal partnerships 2018 economic contribution Governance leadership

$503M agreement with Fort McKay and Mikisew $5.3 billion capital spend Chief Sustainability Officer reports to CEO

Cree First Nations for 49% of ETF6

$2.3 billion government royalties & taxes Climate risk is overseen by the Board

Spent $700M with Aboriginal businesses in 2018

$5 billion since 1999 Close to 5,000 vendors across Canada and Diverse and experienced Board of Directors8

1,300 in the US 8 out of 9 are independent

30 Petro-Canada branded retail sites owned or Aboriginal representation

leased by First Nations ~12,500 Suncor employees

33% are women

Working with multiple Aboriginal communities on

Executive compensation linked to financial,

DPL7 to support PASS5

operational and ESG factors

1, 2, 3, 4, 5, 6, 7, 8 See Slide Notes and Advisories.23

Suncor’s tailings reclamation – PASS

PASS technology aims to rapidly dewater and treat tailings to accelerate reclamation and

lower our environmental footprint at a lower cost

Advancing execution, with regulatory approval received October 2017

Suncor pioneered TRO in 2010

(Tailings Reduction Operations)

Removal of MFT1 from tailings pond

Rapid dewatering of MFT1 with addition of flocculant2

Atmospheric drying of MFT1 Reclamation timeframe is extended

Placement of MFT1 in thin layers for atmospheric drying takes time and is area limited due to drying process

Building on TRO with PASS

(Permanent Aquatic Storage Structure)

Addition of coagulant3 to improve water quality

Placement of tailings below grade, suitable for lake bottom

PASS does not result in new

Reclamation timeframe is reduced

Capping with aquatic cover (E.g. Demonstration Pit Lake) disturbed area

Anticipated benefits of PASS4

Faster reclamation Lower cost Community engagement Demonstrated results

In 2018, PASS doubled tailings treatment capacity to 165% of total annual tailings production

1, 2, 3, 4 See Slide Notes and Advisories24 Appendix

25

2019 Capital and production guidance1

2019 Capital2 Economic Investment3 Production4

$ millions percent boepd

Oil Sands 3,050 – 3,400 17% 410,000 – 440,000 Oil Sands operations

E&P 1,000 – 1,200 97% 85,000 – 95,000 Fort Hills

Downstream 700 – 775 23% 160,000 – 180,000 Syncrude

Corporate 150 – 225 53% 105,000 – 115,000 E&P

430,000 – 450,000 Refinery throughput

Total $4,900 – $5,600 37% 780,000 – 820,000 Upstream production

2019 Planned maintenance for Suncor operated assets and Syncrude5,6

Upstream Timing Impact on quarter Downstream Timing Impact on quarter

Firebag Q2 ~30 mbpd Edmonton Q2 ~10 mbpd

U1 Q2 ~25 mbpd* Commerce City Q2 ~20 mbpd

Fort Hills Q2/Q4 ~15/10 mbpd Montreal Q2 ~30 mbpd

U2 Q3/Q4 ~25/15 mbpd* Sarnia Q2 ~15 mbpd

Syncrude6 Q3/Q4 ~20/20 mbpd

* A portion of the SCO volume impact will be supplemented by increasing bitumen sales

2019 Sensitivities7 +1$/bbl Brent +$1/bbl NYH 3-2-1 +$0.01 FX +$1/GJ AECO +$1L/H Diff +$1L/L Diff

(US$) (US$) (US$/C$) (C$) (US$) (US$)

FFO (C$ MM) ~240 ~150 ~(205) ~(240) ~(25) ~(20 – 40)

1, 2, 3, 4, 5, 6, 7 See Slide Notes and Advisories.26

High quality mining, in situ and upgrading portfolio1

In Situ Mining

Firebag Base Plant

203,000 bpd capacity 350,000 bpd capacity

Suncor working interest 100% Suncor working interest 100%

2,553 mmbbls 2P reserves1 1,418 mmbbls 2P reserves1

MacKay River Syncrude

38,000 bpd capacity Syncrude operated

Suncor working interest 100% 205,600 bpd coking capacity (SU WI)

508 mmbbls 2P reserves1 Suncor working interest 58.74%

1,272 mmbbls 2P reserves1 (SU WI)

Future opportunities Fort Hills

Lewis (SU WI 100%) Suncor operated

Meadow Creek (SU WI 75%) 105,000 bpd capacity (SU WI)

Suncor working interest 54.11%

1,438 mmbbls 2P reserves1 (SU WI)

First oil achieved in January 2018

1 See Slide Notes and Advisories.27

Focused on long life, low decline reserves base

Typical attributes1 of North American oil plays

Initial Decline Sustaining Operating Reservoir Recovery

Illustrative annual FFO2 profiles3 capital rate costs cost risk factor

Mining High Very low Low Medium Very low Very high

~85% of Suncor’s 2019

guidance production

In Situ Medium Low Low Low Low High

Offshore

High Medium Medium Very low Medium Medium

~15% of Suncor’s 2019

guidance production

Tight oil Low Very high High Medium High Low

50 Years

Beneficial attribute Challenging attribute

1, 2, 3 See Slide Notes.28

Canada’s largest Refining & Marketing business

Edmonton refinery Sarnia refinery

142,000 bpd capacity 85,000 bpd capacity

100% oil sands feedstock1 ~75% oil sands feedstock1

Commerce City refinery Montreal refinery

98,000 bpd capacity 137,000 bpd capacity

~20% oil sands feedstock1 ~30% oil sands feedstock1

Marketing Other

Over 500,000 bpd in product sales 4 wind farms3 (111 MW)

1766 North American retail sites St. Clair Ethanol plant (400 ML/yr)

(~50% Suncor owned). 51% interest in Parachem

Petro-Canada remained as the brand Global sulphur and petroleum coke

with largest urban share of market in marketing

Canada for 20182

300+ wholesale sites

1, 2, 3 See Slide Notes and Advisories.29

Refining & Marketing – Demonstrating cash flow resilience

R&M Funds from operations1 WTI – WCS ($US/bbl) Refinery utilization vs. US average Suncor

Capturing the value of widening differentials FFO ($CAD billions) Percent of refining capacity

US Average2

26.30

Full turnaround

5

25.50 30

100% at the Edmonton

21.05 19.40

20

refinery Q2 2018

4

13.50 13.85 11.95

3.8 10

3.2

3

2.9 2.8 0

2.7 2.6 90%

2

2.3

-10

1

US$/Cdn$ FX > $0.90

(2012 – 2014)

-20

0 -30

80%

2012 2013 2014 2015 2016 2017 2018 2012 2013 2014 2015 2016 2017 2018 Q1 2019

Price realizations & refinery crude costs3 Realized GM6/bbl vs. NYH 3-2-1 benchmark

All Suncor refineries Q1 2019, 40% equity feedstock4 All Suncor refineries Q1 2019

36.35

$120

$100 28.65

Brent C$84.255

$80 20.75

15.55 NYH

$60

3-2-1

107 NYH C$

$40 3-2-1

62 60 US$

$20

Benchmark Benchmark Crude Product mix Yield/ Realized FIFO impact Realized

7

$0 crack crack differential & location feedstock/ GM (LIFO) 7 GM (FIFO)

OS realization Feedstock cost R&M realization differential other

1, 2, 3, 4, 5, 6, 7 See Slide Notes and Advisories.30

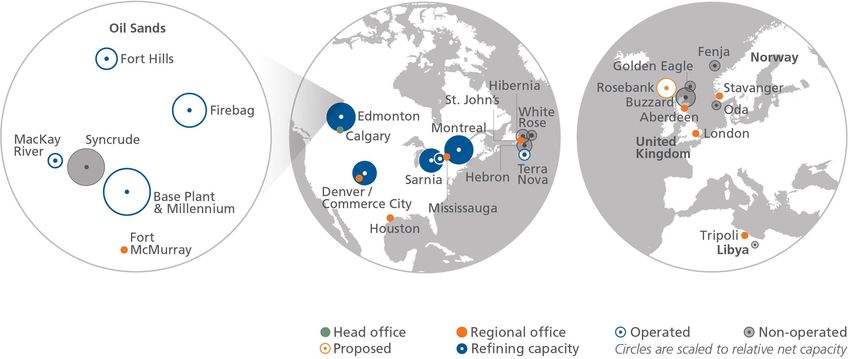

Offshore with >390 million barrels of 2P reserves1

East Coast Canada North Sea

Hibernia

ExxonMobil operated Buzzard

Suncor working interest 20% CNOOC Petroleum Europe Limited operated

63 mmboe 2P reserves1 (Suncor WI) Suncor working interest 29.89%

57 mmboe 2P reserves1 (Suncor WI)

Hebron

ExxonMobil operated

Suncor working interest 21.034%

31.6 mboepd planned net capacity

Golden Eagle

147 mmboe 2P reserves1 (Suncor WI)

CNOOC Petroleum Europe Limited operated

First oil achieved in November 2017

Suncor working interest 26.69%

13 mmboe 2P reserves1 (Suncor WI)

Terra Nova

Suncor Energy operated

Suncor working interest 37.675%

32 mmboe 2P reserves1 (Suncor WI)

Oda

Spirit Energy operated3

Suncor working interest 30%

11 mboepd planned net capacity

White Rose 8 mmboe 2P reserves1 (Suncor WI)

Husky Energy operated

Suncor working interest 27.5%2

54 mmboe 2P reserves1 (Suncor WI)

1, 2, 3 See Slide Notes and Advisories.31

E&P – Investing in high value, low risk projects

Recent performance Sanctioned projects1

mboe/d

Fenja (Norway)

120

• 17.5% working interest

• 6 mbbls/d anticipated net peak production

100

Hebron • First oil expected 2021

80 White Rose

60 Hibernia

Terra Nova

40 Buzzard Phase 2 (UK)

Golden Eagle

20 • 29.89% working interest

Buzzard

0

• Production anticipated to offset natural declines

2012 2013 2014 2015 2016 2017 2018 • First oil expected 2021

111.70 108.75

98.85

West White Rose Project (ECC4)

$billions

2.5 Brent

• ~26% working interest

71.05

54.25

($US/bbl) • 20 mbbls/d anticipated net peak production

52.40

2.0 • First oil expected 2022

43.75

1.5

FFO2

Free funds flow3

Future opportunities

1.0

Capital spend

• Rosebank-UK (40% Suncor WI)

0.5

• Near field developments including subsea

- tie-backs, field extensions and infill drilling

2012 2013 2014 2015 2016 2017 2018

1, 2, 3, 4 See Slide Notes and Advisories.32

Track record of counter-cyclical acquisitions and divestments

Non-core UK offshore 10% Fort Hills WI

$100 WTI US$/bbl 1

Total E&P Canada

$80 $

2 37% Syncrude WI

Canadian Oil Sands

$60 7

Petro -Canada 6

1 5

2 3

4

3 Rosebank

$40 30% WI

$20

4 5% Syncrude WI

Murphy Oil

$40

NYH 3-2-1 US$/bbl

Pioneer retail network 5

3.31% Fort Hills WI

$30 Total E&P Canada

$

$20 5% Syncrude WI4

Conoco Commerce Valero Commerce City 6 Mocal Energy

City refinery refinery

$10

17.5% Fenja WI5

Petro -Canada Faroe Petroleum

$0

7 Rosebank

$8 Colorado, Canadian & 10% WI6

AECO US$/gj Trinidad & Tobago

$6 gas assets

$ Canadian gas assets

$4

$

$2 Petro -Canada

$0

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Other divestments: East Tank Farm1, Lubricants2, wind facilities3 Acquisition

$ Divestment

1, 2, 3, 4, 5, 6 See Slide Notes and Advisories.33 Notes

34 Notes

35 Advisories Forward-Looking Statements – This presentation contains certain in costs; the ability to access external sources of debt and equity capital employed (ROCE) and last in, first out (LIFO) – are not “forward-looking statements” within the meaning of the United States capital; the timing and the costs of well and pipeline construction; prescribed by GAAP. All non-GAAP measures presented herein do Private Securities Litigation Reform Act of 1995 and “forward-looking Suncor’s dependence on pipeline capacity and other logistical not have any standardized meaning and therefore are unlikely to be information” within the meaning of applicable Canadian securities constraints, which may affect the company’s ability to distribute comparable to similar measures presented by other companies. legislation (collectively, “forward-looking statements”), including products to market; mandatory production curtailments being greater Therefore, these non-GAAP measures should not be considered in statements about: Suncor’s strategy and business plans; expected or imposed for longer than anticipated; the timely receipt of isolation or as a substitute for measures of performance prepared in compound annual growth rates, capital expenditures, shareholder regulatory and other approvals; the timing of sanction decisions and accordance with GAAP. All non-GAAP measures are included return growth, WTI break-even, balance sheet leverage metrics, Oil Board of Directors’ approval; the availability and cost of labour, because management uses the information to analyze business Sands decline rate, cost reductions, and operating and financial services, and infrastructure; the satisfaction by third parties of their performance, leverage and liquidity and therefore may be results; reserves estimates and reserve life indices; expected obligations to Suncor; the impact of royalty, tax, environmental and considered useful information by investors. See the “Non-GAAP utilization of assets; expectations for dividends, share repurchases, other laws or regulations or the interpretations of such laws or Financial Measures Advisory” section of the Q1 MD&A. production growth, funds from operations, free funds flow growth, regulations; applicable political and economic conditions; risks and ROCE; anticipated impact of changes in crude oil price associated with existing and potential future lawsuits and regulatory Funds from operations (previously referred to as cash flow from differentials; anticipated impact of IMO regulatory changes; potential actions; improvements in performance of assets; and the timing and operations) is defined in the Q1 MD&A, for the three months ended future free funds flow growth projects, including the timing and impact of technology development. March 31, 2019 is reconciled to the GAAP measure in the Q1 impact thereof, and free funds flow improvement and cash flow MD&A, for 2012 to 2018 is reconciled to GAAP measures in upside potential; illustrative funds from operations and discretionary Although Suncor believes that the expectations represented by such Suncor’s annual management’s discussion and analysis (MD&A) for free funds flow; target break-even cost of capital; plans around in forward-looking statements are reasonable, there can be no the respective year; annual E&P and R&M funds from operations for situ growth; cash operating costs targets; Suncor’s GHG intensity assurance that such expectations will prove to be correct. Suncor’s 2012 to 2017 are reconciled to GAAP measures in Suncor’s annual reduction goal; estimated average carbon cost for upstream Management’s Discussion and Analysis for the first quarter ended MD&A for the respective year; Oil Sands operations cash operating production; expectations, targets and potential opportunities with March 31, 2019 and dated May 1, 2019 (the Q1 MD&A), Annual costs (previously referred to as Oil Sands cash operating costs) is respect to Syncrude; expected IRR for Syncrude interconnecting Report for the year ended December 31, 2018 (the 2018 Annual defined in the Q1 MD&A, for the year ended December 31, 2018 is pipeline and tailings management savings; Oil Sands regional Report) and its most recently filed Annual Information Form/Form reconciled to the GAAP measure in the 2018 Annual Report, and for synergy opportunities; expectations for and potential benefits of 40-F and other documents it files from time to time with securities 2013 is reconciled to the GAAP measure in Suncor’s 2013 annual autonomous haul trucks, and PASS, expectations about Fort Hills; regulatory authorities describe the risks, uncertainties, material MD&A; discretionary free funds flow (previously referred to as capital and production guidance; expected peak production and first assumptions and other factors that could influence actual results discretionary free cash flow) is defined in the Q1 MD&A, for 2015 to oil dates for sanctioned E&P projects; goals with respect to and such factors are incorporated herein by reference. Copies of 2018 is reconciled to the GAAP measure in Suncor’s 2018 annual reliability, safety, cost management and sustainability; and potential these documents are available without charge from Suncor at 150 MD&A, and for 2014 is reconciled to the GAAP measure in Suncor’s future pipelines and market access expectations that are based on 6th Avenue S.W., Calgary, Alberta T2P 3E3, by calling 1-800-558- 2016 annual MD&A; the estimated impact of the LIFO method for Suncor’s current expectations, estimates, projections and 9071, or by email request to invest@suncor.com or by referring to the three months ended March 31, 2019 is defined and reconciled in assumptions that were made by Suncor in light of its experience and the company’s profile on SEDAR at www.sedar.com or EDGAR at the Q1 MD&A; and Fort Hills cash operating costs and Syncrude its perception of historical trends. Some of the forward-looking www.sec.gov. Except as required by applicable securities laws, cash operating costs are defined and reconciled to the GAAP statements may be identified by words such as “planned”, Suncor disclaims any intention or obligation to publicly update or measures in the Q1 MD&A. “estimated”, “target”, “goal”, “illustrative”, “strategy”, “expected”, revise any forward-looking statements, whether as a result of new “focused”, “opportunities”, “may”, “will”, “outlook”, “anticipated”, information, future events or otherwise. Suncor’s actual results may Reserves– Unless noted otherwise, reserves information presented “potential”, “guidance”, “predicts”, “aims”, “proposed”, “seeking” and differ materially from those expressed or implied by its forward- herein for Suncor is presented as Suncor’s working interest similar expressions. Forward-looking statements are not guarantees looking statements, so readers are cautioned not to place undue (operating and non-operating) before deduction of royalties, and of future performance and involve a number of risks and reliance on them. without including any royalty interests of Suncor, and is at December uncertainties, some that are similar to other oil and gas companies 31, 2018. For more information on Suncor’s reserves, including and some that are unique to Suncor. Users of this information are Suncor’s corporate guidance includes a planned production range, definitions of proved and probable reserves, Suncor’s interest, cautioned that actual results may differ materially as a result of, planned maintenance, capital expenditures and other information, location of the reserves and the product types reasonably expected among other things, assumptions regarding: commodity prices; based on our current expectations, estimates, projections and please see Suncor’s most recent Annual Information Form/Form 40- timing of commissioning and start-up, cost, characteristics, and assumptions (collectively, the “Factors”), including those outlined in F dated February 28th, 2019 available at www.sedar.com and capacity of capital projects; assumptions contained in or relevant to our 2019 Corporate Guidance available on www.sec.gov. Reserves data is based upon evaluations conducted Suncor’s 2019 Corporate Guidance; fluctuations in foreign exchange www.suncor.com/guidance, which Factors are incorporated herein by independent qualified reserves evaluators as defined in NI 51- and interest rates; product supply and demand; market competition; by reference. Suncor includes forward-looking statements to assist 101. future production rates; assets and facilities not performing as readers in understanding the company’s future plans and anticipated; expected debottlenecks, cost reductions and margin expectations and the use of such information for other purposes BOE (Barrels of oil equivalent) – Certain natural gas volumes improvements not being achieved to the extent anticipated; may not be appropriate. have been converted to barrels of oil on the basis of six thousand dividends declared and share repurchases below expected levels; cubic feet to one boe. This industry convention is not indicative of the sufficiency of budgeted capital expenditures in carrying out Non-GAAP Measures – Certain financial measures in this relative market values, and thus may be misleading. planned activities; risks inherent in marketing operations (including presentation – namely funds from operations, free funds flow, Oil credit risks); imprecision of reserves estimates and estimates of Sands operations cash operating costs, discretionary free funds recoverable quantities of oil, natural gas and liquids from Suncor’s flow, Syncrude cash operating costs, Fort Hills cash operating costs, properties; expected synergies and the ability to sustain reductions In Situ cash operating costs, mining cash operating costs, return on

36

Slide Notes

Slide 2------------------------------------------------------------- All dividends are at the discretion of Suncor’s Board of Directors. Slide 5---------------------------------------------------------------

(1) Market capitalization + debt - cash and cash equivalents. See Forward-Looking Statements in the Advisories. (1) As at December 31, 2018 and assumes that approximately 7.19

(2) Nameplate capacities as at March 31, 2019. Nameplate capacities (8) Figure does not include the $43 million worth of shares repurchased billion barrels of oil equivalent (boe) of proved and probable

may not be reflective of actual utilization rates. See Forward- in the twelve months ended December 31, 2015 ($0.03/share reserves (2P) are produced at a rate of 628.6 mboe/d, Oil Sands’

Looking Statements in the Advisories. repurchased in 2015). average daily production rate in 2018. Reserves are working interest

(3) As at December 31, 2018 and assumes that approximately 7.58 (9) 2017 buyback per share reflects $1.4 billion of actual spend under before royalties. See Reserves in the Advisories.

billion barrels of oil equivalent (boe) of proved and probable the normal course issuer bid (NCIB). 2018 buyback per share (2) Reflects Oil Sands’ anticipated compounded annual decrease in

reserves (2P) are produced at a rate of 732.0 mboe/d, Suncor’s reflects $3.1 billion of actual spend under Suncor’s NCIBs. 2019 production for 2019-2023 and is calculated on a production-

average daily production rate in 2018. Reserves are working buyback per share assumes the repurchase of approximately $2.0 weighted basis using planned production for those years, and

interest before royalties. See Reserves in the Advisories. billion in 2019. Suncor’s Board of Directors has approved the assumes no economic capital spend, no acquisitions and no

(4) 1527 retail sites are operated under the Petro-Canada brand. repurchase of up to $2.0 billion worth of the company’s common divestments during that period.

Slide 3-------------------------------------------------------------- shares beginning March 1, 2019. Suncor’s share repurchases are (3) Refers to Oil Sands operations sustaining capital per barrel, which is

(1) Funds from operations (FFO) is a non-GAAP financial measure. opportunistic. The actual number of shares that will be repurchased calculated by dividing Oil Sands operations sustaining capital by Oil

See Non-GAAP Measures in the Advisories. Funds from operations and the timing of any such purchases will be determined by Suncor Sands operations production, plus Oil Sands operations cash

is calculated as cash flow provided by operating activities excluding and will depend on market conditions, funds flow and other factors, operating costs per barrel, all as indicated in the Q1 MD&A. Oil

changes in non-cash working capital. FFO indicated for 2019 to and could differ materially from this assumption. See Forward- Sands operations cash operating costs is a non-GAAP financial

2023 is illustrative and is not intended to be a forecast of Suncor’s Looking Statements in the Advisories. measure. See Non-GAAP Measures in the Advisories.

FFO. It is indicative of FFO based on the 2019 pricing guidance (10) Refers to estimated average WTI crude oil price for 2019 in US (4) Refers to estimated average WTI crude oil price for 2019 in US

released on May 1, 2019, as well as the production and free funds dollars required for funds from operations for 2019 to equal dollars required for funds from operations for 2019 to equal

flow growth assumptions outlined below. Actual results may differ estimated 2019 sustaining capital expenditures inclusive of estimated 2019 sustaining capital expenditures inclusive of

materially. See Forward-Looking Statements in the Advisories. associated capitalized interest and dividends. Sustaining capital associated capitalized interest and dividends. Sustaining capital

(2) Compound annual growth rate (CAGR) is calculated for the years represents anticipated asset sustainment and maintenance capital represents anticipated asset sustainment and maintenance capital

2018 to 2023 using Suncor’s business plan. Actual results may vary expenditures plus well pad spend (inclusive of associated expenditures plus well pad spend (inclusive of associated

materially. See Forward-Looking Statements in the Advisories. capitalized interest) based on the company’s current business capitalized interest) based on the company’s current business

(3) Production growth assumes ~10% CAGR per share from 2018 to plans. Assumes production, sustaining capital and business plans. Assumes production, sustaining capital and business

2020 and is calculated using the midpoint of 2019 guidance as well environment at the midpoint of 2019 guidance released on May 1, environment at the midpoint of 2019 guidance released on May 1,

as Suncor’s production growth business plan for 2020. Actual 2019 and a $0.42/share dividend for each quarter in 2019. All 2019 and a $0.42/share dividend for each quarter in 2019. All

production may vary materially. See Forward-Looking Statements in dividends are at the discretion of Suncor’s Board of Directors. dividends are at the discretion of Suncor’s Board of Directors. Actual

the Advisories. Actual results may differ materially. See Forward-Looking results may differ materially. See Forward-Looking Statements in

(4) Free funds flow, previously referred to as free cash flow, is Statements in the Advisories. the Advisories.

calculated by taking funds from operations (FFO) and subtracting Slide 4--------------------------------------------------------------- (5) Full guidance is available at suncor.com/guidance. See Forward-

capital expenditures, including capitalized interest. Free funds flow (1) Free funds flow, previously referred to as free cash flow, is Looking Statements in the Advisories.

is a non-GAAP measure. See Non-GAAP Measures in the calculated by taking funds from operations (FFO) and subtracting (6) Conversion capacity as at March 31, 2019 and reflects Suncor’s

Advisories. Illustrative free funds flow growth potential shown capital expenditures, including capitalized interest. Free funds flow upgrading and refining capacity. Conversion capacity may not be

includes possible future opportunities currently being evaluated and is a non-GAAP measure. See Non-GAAP Measures in the reflective of actual utilization rates. See Forward-Looking

which may be subject to Board of Directors’, counterparty and Advisories. Statements in the Advisories.

regulatory approval. There can be no assurance these opportunities (2) Based on the company’s current business plans and business (7) Nameplate capacities as at March 31, 2019. Nameplate capacities

will be pursued or if pursued that they will result in the expected environment expectations, which are subject to change. Actual may not be reflective of actual utilization rates. See Forward-

benefits. See Forward-Looking Statements in the Advisories. results may differ materially. See Forward-Looking Statements in Looking Statements in the Advisories.

(5) Refers to Trailing Twelve Month average value as at March 31, the Advisories. (8) Free funds flow and discretionary free funds flow are non-GAAP

2019. (3) Funds from operations (FFO) is a non-GAAP financial measure. measures. See Non-GAAP Measures in the Advisories.

(6) The classification of the company’s capital expenditures has been See Non-GAAP Measures in the Advisories. Funds from operations (9) Funds from operations (FFO) is a non-GAAP financial measure.

updated to “‘asset sustainment and maintenance’’ and ‘‘economic is calculated as cash flow provided by operating activities excluding See Non-GAAP Measures in the Advisories. Funds from operations

investment’’ to better reflect the types of capital investments being changes in non-cash working capital. is calculated as cash flow provided by operating activities excluding

made by the company. Sustaining capital represents asset (4) Anticipated production growth per share is calculated using the changes in non-cash working capital.

sustainment and maintenance capital expenditures (inclusive of midpoint of 2019 guidance as well as Suncor’s business plan for (10) New metrics include the impact for IFRS 16 which came into effect

associated capitalized interest), which have been restated for April 2020. Actual results may vary materially. See Forward-Looking on January 1, 2019.

1, 2018 to December 31, 2018 to reflect the change in classification. Statements in the Advisories. (11) All figures are in billions of CAD. U.S dollar facilities converted at a

For a description of asset sustainment and maintenance capital (5) Includes possible future opportunities currently being evaluated and USD/CAD rate of $0.75, the exchange rate as at March 31, 2019.

expenditures see the Capital Investment Update section of the Q1 which may be subject to Board of Directors’, counterparty and

MD&A. regulatory approval. Assumes the completion of incremental continued …

(7) Based on the weighted average number of shares outstanding in pipeline capacity out of the Alberta market. There can be no

each year for 2014 to 2018 and the weighted average number of assurance these opportunities will be pursued or if pursued that they

shares outstanding for the three months ending March 31, 2019 for will result in the expected benefits. See Forward-Looking

2019. 2019 dividend amount assumes $0.42/share for each quarter. Statements in the Advisories.37

Slide Notes (continued)

Slide 6--------------------------------------------------------------- Slide 9------------------------------------------------------------- respective year. The WTI pricing for 2019 is based on Corporate

(1) Expected opex savings are upon full implementation and are (1) Based on current business plans and business environment Guidance issued May 1, 2019.

based on current plans and business environment expectations, expectations including completion of incremental pipeline capacity (4) The NYH 3-2-1 benchmark numbers for 2015-2018 are actual

which are subject to change. See Forward-Looking Statements in out of the Alberta market. Includes projects subject to Board of averages for each respective year. The 2019 price is based on

the Advisories. Directors’, counterparty and regulatory approval. Actual results Corporate Guidance issued May 1, 2019.

(2) Annualized dividend increases for 17 years assumes $0.42/share and breakeven cost of capital may differ materially from this (5) Illustrative FFO is not intended to be a forecast of Suncor’s FFO.

dividend for each quarter in 2019. All dividends are at the target. See Forward-Looking Statements in the Advisories. It is indicative of FFO based on the midpoint of 2019 guidance

discretion of Suncor’s Board of Directors. See Forward-Looking (2) Gross project volume including CNOOC International's 25% released on May 1, 2019. Also based on continued industry

Statements in the Advisories. interest in Meadow Creek. growth fundamentals. Actual results may differ materially. See

Slide 7-------------------------------------------------------------- (3) Refers to Other Six Lease Operators (OSLO). Forward-Looking Statements in the Advisories.

(1) Based on current business plans, which are subject to change. Slide 10-------------------------------------------------------------- (6) 2019 sustaining capital represents anticipated asset sustainment

See Forward-Looking Statements in the Advisories. (1) Refers to Oil Sands operations cash operating costs per barrel, and estimated maintenance capital expenditures (inclusive of

(2) Baseline funds from operations (FFO) has been derived from which is a non-GAAP measure. See Non-GAAP Measures in the associated capitalized interest) based on the company’s current

midpoint of 2019 guidance and the associated business Advisories. business plans. Actual sustaining capital expenditures and

environment. Sensitivities are based on changing a single factor (2) Refers to Mining cash operating costs per barrel, which is a non- associated capitalized interest along with the company’s business

by its indicated range while holding the rest constant. FFO is a GAAP measure, and is calculated by taking the sum of OS&G plans may differ materially from those anticipated and are subject

non-GAAP financial measure and is calculated as cash flow expenses (a GAAP measure) for Oil Sands, subtracting costs that to Board of Directors’ approval. For a description of asset

provided by operating activities excluding changes in non-cash are not directly attributed to Oil Sands operations Mining bitumen sustainment and maintenance capital expenditures see the

working capital. See Non-GAAP Measures in the Advisories. production, and dividing the resulting figure by Oil Sands Capital Investment Update section of the Q1 MD&A. See

(3) Based on 2018 full year production and planned volumes for operations Mining bitumen production, as indicated for the Forward-Looking Statements in the Advisories.

2020. Actual production may vary materially. See Forward- applicable year in the Supplemental Financial and Operating (7) Assumes 2019 quarterly dividend of $0.42/share. All dividends

Looking Statements in the Advisories. Information in the 2018 Annual Report and Suncor’s Annual are at the discretion of Suncor’s Board of Directors. See Forward-

(4) Dividends and future buybacks (NCIBs) are at the discretion of Report for the year ended December 31, 2017 (the 2017 Annual Looking Statements in the Advisories.

Suncor’s Board of Directors. NCIBs are subject to maximum limits Report). See Non-GAAP Measures in the Advisories. Slide 12-------------------------------------------------------------

permitted by law and stock exchange rules. See Forward-Looking (3) Refers to In situ cash operating costs per barrel, which is a non- (1) Annualized dividend increases for 17 years assumes $0.42/share

Statements in the Advisories. GAAP measure, and is calculated by taking the sum of OS&G dividend for each quarter in 2019. All dividends are at the

(5) Funds from operations (FFO) is a non-GAAP financial measure expenses (a GAAP measure) for Oil Sands, subtracting costs that discretion of Suncor’s Board of Directors. See Forward-Looking

and is calculated as cash flow provided by operating activities are not directly attributed to Oil Sands operations In situ bitumen Statements in the Advisories.

excluding changes in non-cash working capital. See Non-GAAP production, and dividing the resulting figure by Oil Sands (2) 2019 buyback per share assumes $2.0 billion of share

Measures in the Advisories. operations In situ bitumen production, as indicated for the repurchases in 2019. Suncor’s Board of Directors has approved

(6) Sustaining capital represents anticipated asset sustainment and applicable year in the Supplemental Financial and Operating the repurchase of up to $2.0 billion worth of its common shares

maintenance capital expenditures (inclusive of associated Information in the 2018 Annual Report. See Non-GAAP Measures beginning March 1, 2019. Suncor’s share repurchases are

capitalized interest) based on the company’s current business in the Advisories. opportunistic. The actual number of shares that will be

plans. See Non-GAAP Measures in the Advisories. (4) Refers to Oil Sands operations cash operating costs, Fort Hills repurchased and the timing of any such purchases will be

Slide 8--------------------------------------------------------------- cash operating costs and Syncrude cash operating costs, which determined by Suncor and will depend on market conditions,

(1) Based on possible future opportunities, including examples shown are non-GAAP measures. See Non-GAAP Measures in the funds flow and other factors, and could differ materially from this

on the slide, currently being evaluated and which may be subject Advisories. Targets based on current business plans and assumption. See Forward-Looking Statements in the Advisories.

to Board of Directors’, counterparty and regulatory approval. business environment expectations. Actual results may differ (3) Refers to approximately $5 billion of shares repurchased under

There can be no assurance these opportunities will be pursued or materially from these targets. See Forward-Looking Statements in Suncor’s normal course issuer bid (NCIB) programs from May 2,

if pursued that they will result in the expected benefits. See the Advisories. 2017 to December 31, 2018.

Forward-Looking Statements in the Advisories. Slide 11-------------------------------------------------------------- (4) Refers to Suncor’s announced share repurchase program of $2.0

(2) Free funds flow, previously referred to as free cash flow, is (1) Discretionary free funds flow, previously referred to as billion, effective March 1, 2019. Suncor’s share repurchases are

calculated by taking funds from operations (FFO) and subtracting discretionary free cash flow, is calculated by taking funds from opportunistic. The actual number of shares that will be

capital expenditures, including capitalized interest. Free funds flow operations (FFO) and subtracting sustaining capital, inclusive of repurchased and the timing of any such purchases will be

is a non-GAAP measure. See Non-GAAP Measures in the associated capitalized interest, and dividends. Discretionary free determined by Suncor and will depend on market conditions,

Advisories. funds flow is a non-GAAP measure. See Non-GAAP Measures in funds flow and other factors, and could differ materially from this

(3) Based on company’s current business plans and the current the Advisories. amount. See Forward-Looking Statements in the Advisories.

business environment, which are subject to change. Actual results (2) Funds from operations (FFO) is defined as cash flow provided by

may differ materially. See Forward-Looking Statements in the operating activities excluding changes in non-cash working continued …

Advisories. capital. Funds from operations is a non-GAAP financial measure.

(4) Refers to Autonomous Haulage Systems (AHS). See Non-GAAP Measures in the Advisories.

(5) Refers to Permanent Aquatic Storage Structure (PASS). (3) WTI pricing for 2015-2018 are actual averages for eachYou can also read