INVESTOR PRESENTATION - 2018RESULTS-April 2019 - 2018 RESULTS-April 2019

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

I N V E S T O R P R E S E N TAT I O N

2 0 1 8 R E S U LT S - A p r i l 2 0 1 9

DISCLAIMER

This document has been prepared by La Banque Postale and La Banque Postale Home Loan SFH solely for use in investor meetings. This document is confidential and is not to be reproduced by any person, nor be distributed to

any person other than its original recipient. La Banque Postale and La Banque Postale Home Loan SFH take no responsibility for the use of these materials by any person.

This presentation does not constitute a prospectus or other offering document in whole or in part. Recipients should not subscribe for any securities issued pursuant to the Offering except on the basis of information in the

prospectus in final form (including the documents incorporated by reference therein) to be issued by the Company in connection with the Offering.

Information contained in this presentation is a summary only, and is qualified in its entirety by reference to the prospectus. The prospectus will include a description of risk factors relevant to an investment in the securities to be

issued by the Company and any recipients should review in particular the risk factors before making a decision to invest.

This presentation does not constitute or form part of any offer or invitation to sell or issue or any solicitation of any offer to buy or subscribe for any security nor shall it (or any part of it) form the basis of (or be relied on in connection

with) any contract or investment decision in relation thereto. Recipients should conduct their own investigation, evaluation and analysis of the information set out in this document and should rely solely on their own judgment,

investigation, evaluation and analysis in evaluating the Company, its business and affairs.

No representation or warranty, express or implied, is given by or on behalf of the Company, the Joint Lead Managers, or any of their respective directors, officers, employees, advisers, agents, affiliates or any other person as to (a)

the accuracy, fairness or completeness of the information or (b) the opinions contained in this document, and, save in the case of fraud, no liability whatsoever is accepted for any such information or opinions.

The information and opinions contained in this presentation are provided as at the date of this document and are subject to change without notice although neither the Company nor any other person assumes any responsibility

or obligation to provide the recipients with access to any additional information or update or revise any such statements, regardless of whether those statements are affected by the results of new information, future events or

otherwise. All liability (including, without limitation, liability for indirect, economic or consequential loss) is hereby excluded to the fullest extent permissible by law.

Certain statements included in this presentation are “forward-looking”. Such forward-looking statements speak only at the date of this document, involve substantial uncertainties and actual results and developments may differ

materially from future results expressed or implied by such forward-looking statements. Neither the Company nor any other person undertakes any obligation to update or revise any forward-looking statements.

All written, oral and electronic forward-looking statements attributable to the Company, or the Joint Lead Managers, or persons acting on their behalf are expressly qualified in their entirety by this cautionary statement.

This document and the investment activity to which it relates may only be communicated to, and are only directed at (i) persons in the United Kingdom having professional experience in matters relating to investments, being

investment professionals within the meaning of Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005, as amended (the FPO); (ii) qualified investors (investisseurs qualifiés) as defined in Articles

L411-2 of the French Monetary and Financial Code and (iii) persons to whom the communication may otherwise lawfully be made (together Relevant Persons). Any investment or investment activity to which this document relates

is available only to Relevant Persons and will be engaged in only with Relevant Persons. This document must not be acted or relied on by any persons who are not Relevant Persons.

NOT FOR PUBLICATION OR DISTRIBUTION IN THE UNITED STATES - Nothing in this presentation shall constitute an offer of securities for sale in the United States. The securities referred to in this presentation (if any) have not been

registered under the U.S. Securities Act of 1933, as amended (the Securities Act) or under the securities laws of any state of the United States , and may not be offered or sold in the United States absent registration or an exemption

from registration under the Securities Act and applicable state securities laws.

This document may contain a number of forecasts and comments relating to the targets and strategies of the La Banque Postale Group. These forecasts are based on a series of assumptions, both general and specific, notably –

unless specified otherwise - the application of accounting principles and methods in accordance with IFRS (International Financial Reporting Standards) as adopted in the European Union, as well as the application of existing

prudential regulations. This information was developed from scenarios based on a number of economic assumptions for a given competitive and regulatory environment.

The Group may be unable:

to anticipate all the risks, uncertainties or other factors likely to affect its business and to appraise their potential consequences;

to evaluate precisely the extent to which the occurrence of a risk or a combination of risks could cause actual results to differ materially from those provided in this presentation.

There is a risk that these projections will not be met. Investors are advised to take into account factors of uncertainty and risk likely to impact the operations of the Group when basing their investment decisions on information

provided in this document. Unless otherwise specified, the sources for the rankings are internal.

2018 RESULTS – April 2019 INVESTOR PRESENTATION La Banque Postale - 2

Table of contents 1 Overview and business model …………………………….........4

2 Strong credit and extra-financial ratings ………….…….........10

3 A challenging economic environment ……….………….........14

4 2018 Results : resilient results and a solid balance sheet …....18

5 2019 Outlook ………………………………….………………......26

6 Sound risk management ………….……………………………..28

7 Liquidity and Funding .…………..……………..………………...31

8 Capital and MREL requirements ………..…………………......37

9 LBP Home Loan SFH ………………………………………........43

10 Appendix ………………..……………………………………........51

2018 RESULTS – April 2019 INVESTOR PRESENTATION La Banque Postale - 3OVERVIEW AND BUSINESS MODEL

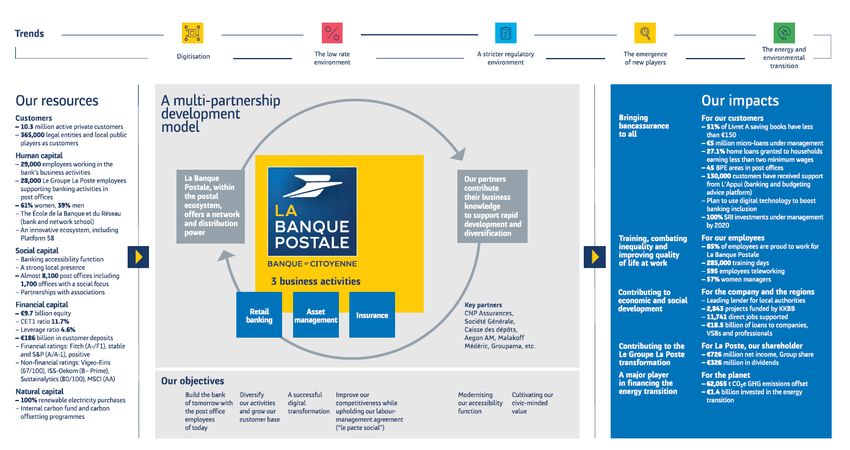

La Banque Postale: a strategic subsidiary of La Poste Group

La Banque Postale, a subsidiary of La Poste The backbone of La Banque Postale

La Banque Postale is fully-owned by La Poste, the French Postal Service

La Poste is structured around 4 business units and fulfill 4 public missions: (1)

73.68%

Universal postal service

Contribution to regional planning

Press distribution

26.32%

Banking accessibility

La Banque Postale is a strategic subsidiary of La Poste: 100% 40.87%

La Poste is hold by law a majority stake in La Banque Postale (Law of

postal activities regulation, 2005)

La Banque Postale is a key contributor to La Poste income

La Banque Postale uses the distribution network La Poste 20.15%(2)

(1) Caisse des Dépôts and its subsidiaries constitute a State-owned group at the service of the public interest and of the

country’s economic development. The said group fulfils public interest functions in support of the policies pursued by the

State and local authorities, and may engage in competitive activities. (Article L. 518-2 of the French Monetary Financial Code)

(2) 18.14% with Sopassure and 2.01% in call option

2018 RESULTS – April 2019 INVESTOR PRESENTATION La Banque Postale - 4OVERVIEW AND BUSINESS MODEL

La Poste: a major French services Group

Multi-business model(1)(2) Growing 2018 revenues

La Banque Postale

La Banque 2018 Net Banking Income: +0.7%(3)

Postale Balance sheet: €245.2 billion

22.1% Service-Mail- 22% of La Poste revenues and 49% of operating income in 2018(4)

Parcels

Service-Mail-Parcels

45.9% 2018 Revenues: +1.3%

2018 Revenues 2018 Parcels volume: 335 million

€24.7bn

(+2.4% vs 2017)

Geopost / DPD

2018 Revenues: +8.2%

2018 Parcels volume: 1,310 million

Geopost / DPD

29.2%

Digital Services

Digital Services 2018 Revenues: +6.6%

2.8% Number of Digiposte+ customers: 3 million

(1) Breakdown of 2018 La Poste revenues excluding Network, other sectors and intercompany (3) Restating 2017 from the General Interest Mission compensation paid in 2017 in respect of 2016 excluding

home savings provision

(2) La Banque Postale’s revenue corresponds to its net banking income (4) Breakdown of 2018 La Poste revenues and operating income excluding Network, other sectors and intercompany

2018 RESULTS – April 2019 INVESTOR PRESENTATION La Banque Postale - 5OVERVIEW AND BUSINESS MODEL

La Banque Postale: a sustainable business model

2018 RESULTS – April 2019 INVESTOR PRESENTATION La Banque Postale - 6OVERVIEW AND BUSINESS MODEL

La Banque Postale : a bank with a full range of services

Since 2006, LBP has gradually expand its range of services through partnerships and acquisitions.

CIB Banking License for

creation Ma French Bank

Acquisition of

La Banque EasyBourse, an online Ecole de la Banque KissKissBankBank Goodeed

Postale brokerage platform et du Réseau acquisition acquisition

Tocqueville

2006 2008 Finance BPE 2014 2017 2018

acquisition acquisition

2007 2009 2010 2011 2012 2013 2015

30 August 2018

La Banque Consumer Property Corporate Public Partnerships Announcement of a

Housing

Postale loan and lending Sector with Aegon AM and merger project

loan

Prévoyance casualty financing Malakoff-Médéric between La Banque

insurance Postale and

Development of insurance activities CNP Assurances

Development of lending activities

Before 2006, La Poste’s financial services business was mainly focused on savings. Since then, LBP has developed its product range to become a bank with a full range of services :

With diversified lending activities, enhancing LBP’s role in financing the French economy.

Committed to serve all clients, all over the country.

2018 RESULTS – April 2019 INVESTOR PRESENTATION La Banque Postale - 7OVERVIEW AND BUSINESS MODEL

La Banque Postale : growth through efficient partnerships

Retail Banking Insurance Asset Management

Retail banking

Private banking / discretionary portfolio Life insurance

management Asset management for individuals

P&C Asset management for companies

Consumer finance

Health insurance

Real estate

Public sector lending

Contingency insurance

Non-profit organizations & Corporate banking

Partnership in Partnership in

Consumer finance Life Insurance P&C Partnerships in Asset Management

FINANCEMENT ASSURANCES IARD

ASSET MANAGEMENT

35% 65%

100% 20.15% 25% 5%

Partnership in Public sector lending Partnership in

Health Insurance 70%

75% 5%

20%

ASSURANCE SANTE

100% 60% 40%

35% 14%

51%

2018 RESULTS – April 2019 INVESTOR PRESENTATION La Banque Postale - 8Table of contents 1 Overview and business model …………………………….........4

2 Strong credit and extra-financial ratings ………….…….........10

3 A challenging economic environment ……….………….........14

4 2018 Results : resilient earnings and a solid balance sheet ...18

5 2019 Outlook ………………………………….………………......26

6 Sound risk management ………….……………………………..28

7 Liquidity and Funding .…………..……………..………………...31

8 Capital and MREL requirements ………..…………………......37

9 LBP Home Loan SFH ………………………………………........43

10 Appendix ………………..……………………………………........51

2018 RESULTS – April 2019 INVESTOR PRESENTATION La Banque Postale - 9STRONG CREDIT AND EXTRA-FINANCIAL RATINGS

Credit ratings aligned with market standards

S&P Global Ratings Fitch Ratings

LBP: LT / ST: A / A-1, outlook: Positive LT / ST: A- / F1, outlook: Stable

LBP Home Loan SFH: AAA, outlook: Stable

Last rating action on 2018/10/30: Last rating action on 2019/02/06:

LT/ST ratings affirmed LT/ST ratings affirmed

Outlook upgraded to Positive Stable outlook unchanged

Rating by debt: Rating by debt:

Senior Preferred: A Senior Preferred: A-

Senior Non Preferred: BBB Senior Non Preferred: A-

Tier 2: BBB-

Rating comments: Rating comments:

« The positive outlook on LBP mirrors that on La Poste. We expect the La Poste « LBP’s ratings reflect its established franchise in deposit collection and housing loans

group will maintain a strong, lasting interest in LBP in the next two years. LBP is part in France, fairly conservative risk appetite, good asset quality, modest profitability and

of the group’s overall strategy, and we see it as strongly integrated within the group. sound capitalisation, taking into account potential ordinary support from its parent La

Because we equalize the ratings on LBP with those on La Poste, an upgrade of La Poste (A+/Stable), France’s state-owned post office. »

Poste would trigger an upgrade of LBP. »

S&P Global Ratings methodology: Fitch Ratings methodology:

LBP’s rating is equalized to the rating of its parent company, La Poste LBP has a Support Rating Floor (SRF) rated ‘A-’.

Group.

LT credit ratings for French peers: LT credit ratings for French peers:

A A+ A A A+ A A- A+ A+ A A+ A+

2018 RESULTS – April 2019 INVESTOR PRESENTATION La Banque Postale - 10STRONG CREDIT AND EXTRA-FINANCIAL RATINGS

A strong and stable shareholding structure

S&P Global Ratings Fitch Ratings

LT / ST: AA / A-1+, outlook: Stable LT / ST: AA / F1+, outlook: Stable

France Last rating action on 2018/10/05: Last rating action on 2018/07/20:

LT/ST ratings affirmed LT/ST ratings affirmed

Stable outlook unchanged Stable outlook unchanged

LT / ST: AA / A-1+, outlook: Stable LT / ST: AA / F1+, outlook: Stable

Caisse des Dépôts

Last rating action on 2018/04/16: Last rating action on 2018/11/30:

et Consignations LT/ST ratings affirmed LT/ST ratings affirmed

Stable outlook unchanged Stable outlook unchanged

LT / ST: A / A-1, outlook: Positive LT / ST: A+ / F1, outlook: Stable

La Poste Last rating action on 2018/10/30: Last rating action on 2018/09/11:

LT/ST ratings affirmed LT/ST ratings affirmed

Outlook upgraded to Positive Stable outlook unchanged

2018 RESULTS – April 2019 INVESTOR PRESENTATION La Banque Postale - 11STRONG CREDIT AND EXTRA-FINANCIAL RATINGS

Outstanding extra-financial ratings

May 2018 May 2017

1st bank in France 1st bank among 231 international banks

2nd bank among 339 international banks Rating: 67/100 (+ 4pts)

Second international bank to obtain the B- rating

“Prime” Status(1)

June 2017 2017

First active rating for La Banque Postale in 2017 Rating: AA

Rating: 73/100 (+ 14pts)

(1) Awarded to companies that meet specific minimum requirements in Corporate Ratings and achieve the best ESG

scores among their sector peers

2018 RESULTS – April 2019 INVESTOR PRESENTATION La Banque Postale - 12Table of contents 1 Overview and business model …………………………….........4

2 Strong credit and extra-financial ratings ………….…….........10

3 A challenging economic environment ……….………….........14

4 2018 Results : resilient results and a solid balance sheet …...18

5 2019 Outlook ………………………………….………………......26

6 Sound risk management ………….……………………………..28

7 Liquidity and Funding .…………..……………..………………...31

8 Capital and MREL requirements ………..…………………......37

9 LBP Home Loan SFH ………………………………………........43

10 Appendix ………………..……………………………………........51

2018 RESULTS – April 2019 INVESTOR PRESENTATION La Banque Postale - 13A CHALLENGING ECONOMIC ENVIRONMENT

Low interest rates and adverse market conditions

Eonia – Annual average level, %

0,50

0,25

0,00

EONIA still negative,

-0,25 -0.35% -0.36%

around -0.4% per year

-0,50

2013 2014 2015 2016 2017 2018

Low interest rates Source : IHS, LBP

10-year OAT – Annual average level, %

2,5

2,0

1,5 10-year OAT still at

0.82%

1,0 0.75% a very low level

0,5

0,0

2013 2014 2015 2016 2017 2018

Source : IHS, LBP

CAC 40 – Year-end level

5500 5313

5250

5000 4731 Declining European

Adverse market 4750

4500 stock indexes, among

4250

conditions 4000

3750

which CAC-40

3500

2013 2014 2015 2016 2017 2018

Source : IHS, LBP

2018 RESULTS – April 2019 INVESTOR PRESENTATION La Banque Postale - 14A CHALLENGING ECONOMIC ENVIRONMENT

The French housing market: encouraging trends

The French housing market is well positioned in Europe A resilient French housing market

A comparatively low home ownership rate (64%(1)) In 2018, production of home loans has increased by 5%(4) compared to

Prudent credit market underwriting practices with a cautious loan 2017 and reached €168bn(4). This growth reflects a good dynamic in

approval policy based on borrowers’ solvability analysis rather than on a very low-rate environment.

the value of underlying assets. In 2018, the share of credit renegotiation has reached 17%(4)

Stability of revenues and debt ratio are key issues : In France, the compared to 41%(4) in 2017. At December 2018, the share reached

affordability ratio is stable at 30%(2) in 2018. 14.6%, the lowest level since 2014. The market is now normalized.

Average maturity at inception: 18 years(3) at December 2017

(almost stable compared to December 2016) France : home loans production (in €bn)

273

European Home Ownership % (2017) 252

213 203

Germany 51% 160 168

121 137

France 64%

UK 65%

Eurozone 66%

Netherlands 69%

Italy 72%

2015 2016 2017 2018

Spain 77%

Total production Production out of renegotiations

Source : Eurostat data

Source : Banque de France data (December 2018), LBP internal results

(1) Eurostat data (4) Internal figures based on Banque de France data (December 2018)

(2) CA Economic – Real Estate (February 2019)

(3) EMF – Hypostat 2018 (September 2018)

2018 RESULTS – April 2019 INVESTOR PRESENTATION La Banque Postale - 15A CHALLENGING ECONOMIC ENVIRONMENT

2018 loan growth driven by corporate and public sector financing

2018 loan

Home loans : €10.3bn

New consumer loans: €2.5bn (+6.4%)

Corporate loans and public sector financing: €26.3bn (+27%)

Credit portfolio

Home loans (1) (in €bn) Consumer loans (in €bn)

+3.4% 2018 outstanding loans

€93bn (+9.5%) +1.9%

55.8 58.4 60.4

53.4 54.1 4.8 4.9

4.5 4.7

4.0

65%

2014 2015 2016 2017 2018

5%

2014 2015 2016 2017 2018

(1) excluding Dutch home loan portfolio

Public sector financing (in €bn)

Corporate loans (in €bn)

+40.5%

+7.2%

18.5

4.5

7.1 8.1 8.7

20% 7.8

13.2

3.6 5.3

2.9

2014 2015 2016 2017 2018

10% 2014 2015 2016 2017 2018

2018 RESULTS – April 2019 INVESTOR PRESENTATION La Banque Postale - 16Table of contents 1 Overview and business model …………………………….........4

2 Strong credit and extra-financial ratings ………….…….........10

3 A challenging economic environment ……….………….........14

4 2018 Results : resilient results and a solid balance sheet …...18

5 2019 Outlook ………………………………….………………......26

6 Sound risk management ………….……………………………..28

7 Liquidity and Funding .…………..……………..………………...31

8 Capital and MREL requirements ………..…………………......37

9 LBP Home Loan SFH ………………………………………........43

10 Appendix ………………..……………………………………........51

2018 RESULTS – April 2019 INVESTOR PRESENTATION La Banque Postale - 172018 RESULTS : RESILIENT RESULTS AND A SOLID BALANCE SHEET

Resilient 2018 results

CONSOLIDATED RESULTS 2017 %

(in € millions)

2017 2018

proforma(1) proforma(1)

Net Banking Income 5,687 5,557 5,570 + 0.2 % NBI up 0.7% despite challenging environment

Net Banking Income excluding the PEL/CEL effect 5,619 5,489 5,528 + 0.7 %

(low interest rates) +0.7%

Operating expenses (4,619) (4,619) (4,615) - 0.1 % Operating expenses slightly down 0.1% yoy

-0.1%

Gross Operating Income 1,068 938 955 +1.8 %

Cost of risk(2) (192) (192) (133) - 30.6 % Cost of risk down 30.6% in Retail Banking

14 bps(2)

Cost of the ACPR penalty 0 - (50) -

Operating Income 876 746 772 + 3.4 %

Share of profits of equity associates 263 263 268 + 1.9 %

Pre-tax Income 1,138 1,008 1,039 + 3.1 %

Income tax (340) (283) (274) - 3.3 %

Non-controlling interests (34) (34) (40) + 16.0 %

Net Income, Group Share 764 691 726 + 5.1 %

Cost-Income ratio 81.8 % 83.7 % 83.4 % - 0.3 point Cost-income ratio slightly down -0.3 point

(1) Restating 2017 from the General Interest Mission compensation paid in 2017 in respect of 2016

(2) Annualized cost of risk after application of IFRS 9 as from 1 January 2018

2018 RESULTS – April 2019 INVESTOR PRESENTATION La Banque Postale - 182018 RESULTS : RESILIENT RESULTS AND A SOLID BALANCE SHEET

Resilient revenues across all businesses

Performance trends across businesses (NBI excl. PEL/CEL effect) Retail Banking NBI (excl. PEL/CEL effect)

in € millions in € millions

% of 46%

5,528 Commissions 45%

5,461 5,489 +0.7% and others 43%

+0.5%

153 +5.2%

Asset 145 NBI 5,100 5,122 5,114

163 +0.4% -0.1%

Management

Commissions

and others

2,213 2,309 2,366

222 261 +17.6%

Insurance 198

NIM

Retail Banking 5,100 5,122 5,114 -0.1% (Net Interest 2,887 2,813 2,748

Margin)

2016 proforma 2017(1) 2018 2016 proforma 2017(1) 2018

(1) Restating 2017 from the General Interest Mission compensation paid in 2017 in respect of 2016 (1) Restating 2017 from the General Interest Mission compensation paid in 2017 in respect of 2016

2018 RESULTS – April 2019 INVESTOR PRESENTATION La Banque Postale - 192018 RESULTS : RESILIENT RESULTS AND A SOLID BALANCE SHEET

Efficient cost control and a lower cost-income ratio

Breakdown of operating expenses(1) Cost-Income Ratio

in € millions in percent (%)

4,587 + 0.7% 4,619 - 0.1% 4,615

488 522

83.7

Employee benefit expenses 566 + 1.3 pt 83.4

Taxes and duties 11 60 104 - 0.3 pt

82.4

External services and other expenses(2) 3,913 3,857 3,749

Amortisation and provision 176 181 197

2016 2017 2018 2016 proforma 2017(3) 2018

(1) General operating expenses + net depreciation, amortisation and impairments of tangible and (3) Restating 2017 from the General Interest Mission compensation paid in 2017 in respect of 2016

intangible assets

(2) Customer advisors & salesforce, Back office & IT, Counter & ATM transaction and operating costs

2018 RESULTS – April 2019 INVESTOR PRESENTATION La Banque Postale - 202018 RESULTS : RESILIENT RESULTS AND A SOLID BALANCE SHEET

2018 Strong results

Operating income Pre-tax income

in € millions in € millions

834(2) 1,023 1,008 + 3.1 % 1,039

Asset

70 746 772 - 1.4 %

Management + 3.4 %

Insurance 92 - 10.5 % 60

59 59

113 132

113

2016 Proforma 2017(1) 2018

Net income, Group share

Retail Banking 672 574 579 in € millions

726

694 691

574 + 5.1 %

- 0.5 %

2016 Proforma 2017(1) 2018

2016 Proforma 2017(1) 2018

(1) Restating 2017 from the General Interest Mission

(2) Scope effect linked to Ciloger cession in 2016 (€15.8 million impact on operating income)

2018 RESULTS – April 2019 INVESTOR PRESENTATION La Banque Postale - 212018 RESULTS : RESILIENT RESULTS AND A SOLID BALANCE SHEET

Retail Banking : continuous growth in loan outstandings

Resilient financial performances Loan production

Consolidated results 2017 % in € billions

2017 2018

(in € millions) proforma(1) proforma(1)

Net Banking Income 5,320 5,190 5,156 -0.7% 39.1

36.7 +6.5 %

+27.0 %

10.3

Operating expenses (4,424) (4,424) (4,395) -0.7% 28.9

13.5

2.5

Gross Operating Income 896 766 762 -0.7% Home loans 11.2 2.4

Cost of risk (192) (192) (133) -30.6%

Consumer loans 2.4

26.3

Loans to 20.8

Cost of the ACPR penalty 0 0 (50) - corporations 15.3

and public sector

Operating Income 704 574 579 +0.9% 2016 2017 2018

(1) Restating 2017 from the General Interest Mission

2018 Financial results Saving outstandings(2)

NBI excluding non-recurring items is near stable at €5,114 million, or -0.15% compared to 2017. The restated in € billions

Net Interest Margin (NIM) fell by 2% at €2,748.1 million while commissions were up slightly by 0.6% over the 315 315

period thanks to increased sales.

310 -0.1 %

+1.5 %

Demand deposits 59 63 66

Balance sheet

Retail bank operating expenses remained under control, down slightly by 0.7% over the period at €4,395

savings

million.

Ordinary savings 80 81 82

The cost of risk decreased significantly by 30.6% at €133 million. This is 14 basis points in terms of loan

outstandings. Housing savings 32 32 32

Retail Banking operating income was €579 million. It was up by 0.9% over the period compared to the 2017

proforma.

Financial

savings

Life insurance 126 126 124

The decision of the ACPR published on 24 December 2018 regarding La Banque Postale’s AML/CFT system

was recorded in operating income in the amount of €50 million. Restated for the ACPR penalty and the UCITS 12 12 10

General Interest Mission, operating income increased by 9.5%. 2016 2017 2018

(2) End-of-period

2018 RESULTS – April 2019 INVESTOR PRESENTATION La Banque Postale - 222018 RESULTS : RESILIENT RESULTS AND A SOLID BALANCE SHEET

A strong contribution from the Insurance business

Strong financial results Insurance : a 17.6% increase in NBI

Consolidated results

2017 2018 %

(in € millions)

4,613

Net Banking Income 222 261 +17.6%

Insurance contracts 4,568

(in thousands)

Operating expenses (109) (128) +17.7%

4,452

261

Gross Operating Income 113 133 +17.6%

+ 17.6 % 14

Cost of risk 0 (1) ns 222

NBI 49

(in € millions) 198 + 12.1 % 11

Operating Income 113 132 +17.1%

Health 10

47

2018 Financial results Insurance

50 64

Advisory

The non-life insurance business continued to grow with the portfolio now at nearly 4.6 million contracts

(+1%). In particular: 52

The portfolio of Property and Casualty insurance contracts (37.3% of total volume) increased by P&C 46

3.6% over the period to reach 1.7 million contracts, boosted by a solid sales dynamic;

La Banque Postale Prévoyance provident savings portfolio (58.6% of the total portfolio) was virtually

stable over the period at about 2.7 million contracts;

The Health care insurance contract portfolio (4.1% of the portfolio by volume) decreased by 3.8% at 135

0.2 million contracts. 110

The Insurance unit's NBI increased by 17.6% to €261 million over the period, driven by the strong Providence 91

performance of Prévoyance (51.7% of the insurance unit's NBI, +22.7%) and Property and Casualty (24.5% of

the insurance unit's NBI, +23.1%).

The operating expenses of the insurance subsidiaries reached €128 million (+17.7%) due to development

costs. 2016 2017 2018

Lastly, the insurance unit's operating income came in at €132 million for the period, up significantly by 17.1%.

2018 RESULTS – April 2019 INVESTOR PRESENTATION La Banque Postale - 232018 RESULTS : RESILIENT RESULTS AND A SOLID BALANCE SHEET

Growth in Asset Management Business

Increasing financial results Asset Management : a 5.2% increase in NBI

Consolidated results

2017 2018 %

(in € millions)

Net Banking Income 145 153 +5.2% Assets

under management 222 218

Operating expenses (86) (93) +7.1% (in € billions)

181

Gross Operating Income 59 60 +2.5%

NBI

Cost of risk 0 0 - (in € millions)

163 - 10.6 %

+ 5.2 % 153

Operating Income 59 60 +2.5% Ciloger(1) 26 145

18

Tocqueville 17

15

Finance SA

2018 Financial results

Assets under management of La Banque Postale Asset Management group amount to €218 billion, down by 2%

over the period. LBP 128 135

The total assets of La Banque Postale Asset Management decreased by 1.9% over the period to €216.3 billion Asset Management 122

due to adverse stock markets. However, distribution remained positive thanks to the retail network.

The Asset Management NBI rose by 5.2% over the period to €153 million.

LBPAM continues investing to support its development and increasing therefore the operating expenses by 7.1%

to €93 million.

Operating income increased by 2.5% compared to 2017 to reach €60 million.

2016 2017 2018

(1) In equity associate since 2017

2018 RESULTS – April 2019 INVESTOR PRESENTATION La Banque Postale - 24Table of contents 1 Overview and business model …………………………….........4

2 Strong credit and extra-financial ratings ………….…….........10

3 A challenging economic environment ……….………….........14

4 2018 Results : resilient results and a solid balance sheet ......18

5 2019 Outlook ………………………………….………………......26

6 Sound risk management ………….……………………………..28

7 Liquidity and Funding .…………..……………..………………...31

8 Capital and MREL requirements ………..…………………......37

9 LBP Home Loan SFH ………………………………………........43

10 Appendix ………………..……………………………………........51

2018 RESULTS – April 2019 INVESTOR PRESENTATION La Banque Postale - 252019 OUTLOOK

2019 Outlook

A stronger balance sheet A merger project with CNP Assurances

In order to support the growth of La Banque A key year for the project

Postale and subjected to the approval of its

governance, La Poste Group plans in the first half of

2019 a capital increase by converting €800 million

of AT1 into equity(1).

A boost in Digital A reinforced citizen commitment

Launch of Ma French Bank this summer

in 2,000 post offices Caps on incident fees (€25 monthly) for its

1.6 million financially vulnerable customers

Development of Platform58 startup

Incubator (1 February 2019) Freeze on bank fees for all of its customers

(1) In accordance with Article 26 of (EU) no. 575/2013, the recognition in capital of the securities issued for this

transaction is subject to the approval of the European Central Bank.

2018 RESULTS – April 2019 INVESTOR PRESENTATION La Banque Postale - 26Table of contents 1 Overview and business model …………………………….........4

2 Strong credit and extra-financial ratings ………….…….........10

3 A challenging economic environment ……….………….........14

4 2018 Results : resilient results and a solid balance sheet ......18

5 2019 Outlook ………………………………….………………......26

6 Sound risk management ………….……………………………..28

7 Liquidity and Funding .…………..……………..………………...31

8 Capital and MREL requirements ………..…………………......37

9 LBP Home Loan SFH ………………………………………........43

10 Appendix ………………..……………………………………........51

2018 RESULTS – April 2019 INVESTOR PRESENTATION La Banque Postale - 27SOUND RISK MANAGEMENT

A lower cost of risk reflecting prudent risk policies

Retail banking cost of risk (in € millions) NPL and coverage ratios

-30.6%

Coverage ratio 39.3%(2) 76% 54% 75% 85%

181 181 192 NPL ratio 3.6%

133 2.6% 2.8%

2.4%

0.9%

La Banque BNP Paribas Société Générale BPCE Crédit Agricole

2015 2016 2017 2018 Postale Group

(2) Depreciations (Bucket 3) at 31/12/18, divided by impaired outstandings (Bucket 3) Source: 2018 Investor Presentations

Retail banking cost of risk (in bps(1)) Retail banking cost of risk – French market (in bps(1))

yoy

-8 bps -5 bps -4 bps stable stable -3 bps -1 bp

-8 bps evolution

26 23

23 23 22

16 17

14 15

14

10

La Banque BNP Société Banque Caisse Caisses LCL

2015 2016 2017 2018 Postale Paribas Générale Populaire d’Epargne Régionales CA

(1) Annualized cost of risk (1) Annualized cost of risk Source: 2018 Investor Presentations

2018 RESULTS – April 2019 INVESTOR PRESENTATION La Banque Postale - 28SOUND RISK MANAGEMENT

A strong asset quality

High quality of assets at 2018 High quality of retail lending portfolios

A conservative RWA calculation approach following standard method

Balance sheet at 31 December 2018: €245bn, +€14bn vs 01.01.2018 A progressive and controlled diversification of lending businesses

o/w €93bn loan outstandings A conservative financing approach, focusing on stringent management

Credit risk still accounting for most of total RWAs High quality securities portfolios (HTC and HTCS YE 2018)

(in € billions) Breakdown by sector Breakdown by country Breakdown by rating

65.2

69.9 9% 6 2% 7%

52.7 54.2

59.6 2.0

1.1

18% Credit %

institutions Europe

Outside 25% A

2.1 Businesses Europe Other

Market RWA 1.3 1.2

43.8 48.2 53.9 59.4

Credit RWA 42.5

Operational RWA 8.9 9.2 9.3 9.3 9.4

2014 2015 2016 2017 2018

Basel 3 / CRR 73 % 92% 68%

Sovereign France AAA and AA

2018 RESULTS – April 2019 INVESTOR PRESENTATION La Banque Postale - 29Table of contents 1 Overview and business model …………………………….........4

2 Strong credit and extra-financial ratings ………….…….........10

3 A challenging economic environment ……….………….........14

4 2018 Results : resilient results and a solid balance sheet ......18

5 2019 Outlook ………………………………….………………......26

6 Sound risk management ………….……………………………..28

7 Liquidity and Funding .…………..……………..………………...31

8 Capital and MREL requirements ………..…………………......37

9 LBP Home Loan SFH ………………………………………........43

10 Appendix ………………..……………………………………........51

2018 RESULTS – April 2019 INVESTOR PRESENTATION La Banque Postale - 30LIQUIDITY AND FUNDING

Balance sheet breakdown

Key points LBP balance sheet at 31 December 2018 (€bn)

245 245

Balance sheet at 31 December 2018: €245bn, +€14bn vs 01.01.2018

Large customers’ deposits base : €182bn

Centralised regulated savings 69 76 Regulated savings

LBP “centralises” at the CDC most of all the funds deposited on Livret A,

LDDS and LEP regulated savings accounts and since H1 2016, only half of LEP

regulated savings accounts

Customer

Remaining part of the deposit base (not centralised to CDC) amounting to deposits/

Retail

€112bn: 63 savings

home loans(1)

€182bn

is used to fund customer lending and mainly home loan activity.

Corporations Customer deposits/savings

106

Assets out of home loans 7 excluding regulated savings

is invested in a portfolio mostly classified in Amortised Costs regulated

savings

Other loans

25

(dating back to before LBP was created and mainly consisting in centralised to customer

HQLA bonds) and a credit spread portfolio. at CDC

Amortised costs

€176bn

portfolio 24

Since January 2018, LBP is no longer allowed to overcentralise its Livret A FVOCI portfolio 14 22 Debt securities

deposits, but will benefit from a 10-year phase-in period to absorb the liquidity

it will receive back. Short term assets 19 Repo

and central bank

30

9 Other Liabilities and Provisions

Others 13 14 Own funds and hybrids

Assets Liabilities

(1) Including Dutch mortgage loan portfolio (€2.7bn)

2018 RESULTS – April 2019 INVESTOR PRESENTATION La Banque Postale - 31LIQUIDITY AND FUNDING

A strong and stable liquidity position

Loan to Deposit ratio Group’s LCR ratio and HQLA liquidity buffer

in percent (%) LCR ratio HQLA

in percent (%) in € billions

76%

24.6

Level 2 1.6

1,3

86.4%

81.3% 157.4% 145.3%

74.4% Level 1

21.8 23.0

2016 2017 2018 2017 2018 2018

Sound financing structure with a loan to deposit ratio at 86.4% LCR ratio: 145.3% at 31 December 2018

at 31 December 2018 (+5.1 pts vs 2017)

A strong liquidity buffer with 94% of level 1 assets

2018 RESULTS – April 2019 INVESTOR PRESENTATION La Banque Postale - 32LIQUIDITY AND FUNDING

2018 Funding mix

Liability breakdown at 31 December 2018

€245bn

In addition to a large customers deposit base, LBP has diversified wholesale

Provisions and other liabilities(1)

funding sources: Bond borrowings

Short-term debts

Short Term: 4% 4%

Interbank funding: €20bn Neu CP programme 5%

Repo: Large valuable portfolio of high quality securities Own funds and hybrids

5%

ECP program of €20bn

Repo 8% 43% Customer deposits

Medium to Long Term:

Covered bond programme through LBP Home Loan SFH

EMTN and Neu MTN programme

Agreement with SFIL/CAFFIL to refinance French local

authorities loan production

Access to EIB (European Investment bank) long term funding

Long term Repo 31%

Regulated savings

(1) Accruals (2.1%), Provisions (1.2%), Revaluation differences (0.3%), Derivatives (0.1%) and Tax liabilities (0.1%)

2018 RESULTS – April 2019 INVESTOR PRESENTATION La Banque Postale - 33LIQUIDITY AND FUNDING

Diversifying funding instruments to support lending growth

2019 Funding plan Wholesale funding sources at 31 December 2018

in percent (%)

Refinance its growing loan portfolio and further diversify its investor base trough:

Covered bonds: besides €1bn already issues in Q1 in primary

€12.37bn

markets, further benchmark and private placements would be

considered

Senior Non-Preferred: further issuance with at least one

6% 6%

benchmark transaction and private placement Senior Preferred

Repo LT

Senior Preferred: although issuance will be driven by private

placements issuance in Euros and Dollars, La Banque Postale could

consider to issue a benchmark transaction for the first time

10%

A green and social Bond Framework

54% Senior Non

Covered Bonds Preferred

24%

Tier 2

2018 RESULTS – April 2019 INVESTOR PRESENTATION La Banque Postale - 34LIQUIDITY AND FUNDING

Debt maturity schedule

Debt maturity schedule (benchmarks)

in € millions

1200

1000

800

600

400

200

0

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

Tier 2 SNP Covered

2018 RESULTS – April 2019 INVESTOR PRESENTATION La Banque Postale - 35Table of contents 1 Overview and business model …………………………….........4

2 Strong credit and extra-financial ratings ………….…….........10

3 A challenging economic environment ……….………….........14

4 2018 Results : resilient results and a solid balance sheet ......18

5 2019 Outlook ………………………………….………………......26

6 Sound risk management ………….……………………………..28

7 Liquidity and Funding .…………..……………..………………...31

8 Capital and MREL requirements ………..…………………......37

9 LBP Home Loan SFH ………………………………………........43

10 Appendix ………………..……………………………………........51

2018 RESULTS – April 2019 INVESTOR PRESENTATION La Banque Postale - 36CAPITAL AND MREL REQUIREMENTS

CET1 Evolution in 2018

CET1 Evolution

in € millions

-4.3%

327

726 140

8,522

626

8,155

CET1 31/12/2017 Profit Dividend FTA IFRS9 Others CET1 31/12/2018

La Banque Postale’s fully loaded CET1 ratio is 11.7%, down 1.7 point compared to the end of December 2017.

The decrease in La Banque Postale’s common Equity Tier 1 capital is mainly due to:

the impact of the IFRS 9 standard first application (€140 million),

unrealised capital losses generated by the volatility of markets conditions, which have a full impact on La Banque Postale’s own funds since 1 January 2018(1).

(1) In application of Articles 467 and 468 of regulation (EU) no. 575/2013, the deductibility of unrealised gains and losses on regulatory capital could be handled via temporary measures until 31/12/2017.

2018 RESULTS – April 2019 INVESTOR PRESENTATION La Banque Postale - 37CAPITAL AND MREL REQUIREMENTS

2019 Supervisory Review and Evalution Process (SREP)

CET1 Ratio

Margin

Following the Supervisory Review and Evaluation Process (SREP) carried out by the ECB, the 9.0% +2.7 pts

latter notified La Banque Postale of its consolidated CET1 own funds requirements(1) applicable O-SIIs 0.25%

CCB 2.50%

as of 1 March 2019. It was 9.0% and included:

4.50% of CET1 P2R 1.75%

11.7%

a 1.75% requirements in additional own funds for Pillar 2 (Pillar 2 Requirements)

Pillar 1 4.50%

2.50% for a capital conservation buffer (CCB)

and 0.25% for a buffer for Other Systemically Important Institutions (O-SIIs). Minimum requirement of CET1 ratio as at 31/12/18

CET1 Ratio (fully loaded) (fully loaded)

Total Capital Ratio

12.5% Margin

+3.7 pts

Following the Supervisory Review and Evaluation Process (SREP) carried out by the ECB, the O-SIIs 0.25%

latter notified La Banque Postale of its consolidated Total Capital own funds requirements(1) CCB 2.50%

P2R 1.75%

applicable as of 1 March 2019. It was 12.5% and included:

16.2%

9.00% of CET1 SREP requirements applicable as of 1 March 2019

Pillar 1 8.00%

1.50% of Additional Tier 1 (ATI)

2.00% of Tier 2 (Tier 2)

Minimum requirement of Total Total Capital ratio as at

Capital Ratio (fully loaded) 31/12/18 (fully loaded)

(1) These requirements do not take into account the countercyclical buffer, applicable as of 1 July 2019, which is 0.25% for exposures in France.

2018 RESULTS – April 2019 INVESTOR PRESENTATION La Banque Postale - 38CAPITAL AND MREL REQUIREMENTS

Regulatory capital and MREL eligible ressources

MREL eligible ressources at 31/12/18

in € millions in % of RWAs

14,012 20.0%

TLAC and MREL considerations 724 1.0% Other instruments(1)

As an “O-SIB” and as of today, La Banque Postale is not subject to 718 1.0% Other senior debt

1,250 1.8% SNP debt

TLAC such as defined by the FSB

On 15/02/19, the European Council and European Parliament agreed 2,365 3.4% T2

on a legislative package which introduces TLAC in European law and

800 1.1% AT1

amends MREL

This package should be adopted by European Parliament in April 2019

MREL eligible ressources at 31/12/18 8,155 11.7% CET1

A total amount of €14,012m

Including a Total Capital amount of €11,320m at 31/12/18

Representing 20.0% of RWAs

31/12/18

(1) Mainly representing the part of 2010 Tier 2 issuance not qualified as Tier 2 anymore

2018 RESULTS – April 2019 INVESTOR PRESENTATION La Banque Postale - 39CAPITAL AND MREL REQUIREMENTS

An ability to generate capital to support future growth

Capital management philosophy

LBP and Group LP are committed to manage adequate solvency levels to LBP Tier 1 ratios and La Poste Group support

support LBP’s strategy as evidenced by several capital actions.

First capital Capital increase of AT1

increase €228m and AT1 Capital increase Core Tier 1

issue of €800m of €633m

Maintening a prudent approach on capital… of €860m

15.5% 15.7%

14.6%

Consistently above 10% CET1 ratio since LBP creation 12.7% 13.2% 12.8%

11.4% 14.0% 14.3% 113.4% 11.7%

… under conservative solvency calculations

Assessing Pillar 1 risk under standard approach

2011 2013 2014 2016 2017 2018

… AT1 conversion on H1 2019 Basel 2 / 2.5 Basel 3 / CRR

La Poste Group plans in the first half of 2019 a capital increase by converting

€800 million of AT1 into equity(1) (1) In accordance with Article 26 of (EU) no. 575/2013, the recognition in capital of the securities issued for this

transaction is subject to the approval of the European Central Bank.

2018 RESULTS – April 2019 INVESTOR PRESENTATION La Banque Postale - 40CAPITAL AND MREL REQUIREMENTS

Balance sheet - Regulatory indicators

Regulatory indicators well above requirements

CAPITAL LEVERAGE LIQUIDITY

CET 1 Total Capital Leverage ratio LCR NSFR

2018 requirements (1) 8.3% 11.8% N.A. >100% >100%

End-2018 ratios 11.7% 16.2% 4.6% (2) 145% >100%

2019 requirements (1) 9.0% (3) 12.5% N.A. >100% >100%

(1)

(2)

Excl. P2G

3.4% at 31/12/2018 including centralized savings

p p p p p

(3) 9.25% from 01/07/2019, including a contra cyclical buffer at 0.25%

2018 RESULTS – April 2019 INVESTOR PRESENTATION La Banque Postale - 41Table of contents 1 Overview and business model …………………………….........4

2 Strong credit and extra-financial ratings ………….…….........10

3 A challenging economic environment ……….………….........14

4 2018 Results : resilient results and a solid balance sheet ......18

5 2019 Outlook ………………………………….………………......26

6 Sound risk management ………….……………………………..28

7 Liquidity and Funding .…………..……………..………………...31

8 Capital and MREL requirements ………..…………………......37

9 LBP Home Loan SFH ………………………………………........43

10 Appendix ………………..……………………………………........51

2018 RESULTS – April 2019 INVESTOR PRESENTATION La Banque Postale - 42LBP HOME LOAN SFH

La Banque Postale Home Loan strategy

La Banque Postale home loan business Split by guarantee (2018 production)

In percent (%)

Low risk profile customers : 3% 4%

Owner occupied home (84%) Others Other credit

institutions

Tenor at inception (19.9 years)

36% 57%

Fixed rate loans (99.6%) Collateral security

(mortgage) Crédit Logement

55% of loans were guaranteed by Crédit Logement on 31 December 2018

Source LBP

Loan purpose (2018 production) Doubtful home loans

In percent (%)

In percent (%)

7% 1,8

1,6

8% Other 1,4

1,2

French market

LBP(1)

Repurchase 1

0,8

17% 0,6 Crédit Logement

New Home 68% 0,4

0,2

Existing home 0

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Source LBP Source: Banque de France, ACPR, LBP, Crédit Logement ; (1) LBP out of BPE and Sofiap

2018 RESULTS – April 2019 INVESTOR PRESENTATION La Banque Postale - 43LBP HOME LOAN SFH

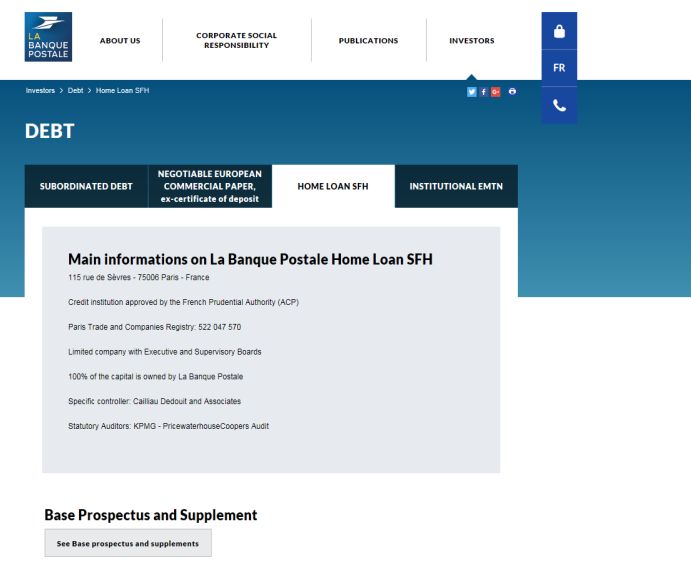

La Banque Postale Home Loan SFH : legal framework

A strong legal framework and advantageous treatment for Investors

Investor informations : a dedicated website

La Banque Postale Home Loan SFH is a French credit institution, 100% owned by LBP, licensed

by the French financial regulator (Autorité de Contrôle Prudentiel et de Résolution – ACPR).

Minimum contractual over-collateralization (OC) of 8.1% over the 5% legally required, using

the same weightings

Under CRD IV / CRR (article 129) and LCR delegated act, AA- or better rated covered bonds

with minimum size of €500m are eligible to level 1B for LCR and benefit from a 10% RW

treatment

Segregation of cover pool assets and legal preferential claim for covered bonds investors

Absolute seniority of payments over all creditors, no early redemption or acceleration

Regulated covered bonds are exempted from bail-in (BRRD)

https://www.labanquepostale.com/en/investors/debt.hlsfh.html#

ECBC Label to ensure full

transparency on the cover pool

2018 RESULTS – April 2019 INVESTOR PRESENTATION La Banque Postale - 44LBP HOME LOAN SFH

La Banque Postale Home Loan SFH : legal framework

Structure overview Namens-schuldverschreibungen Documentation

La Banque Postale

(Borrower)

Cover Pool

(French Home Loans)

In June 2014, La Banque Postale has established a program for the issuance

Collateral Collateralized Principal and of German registered covered bonds, named as :

Security Loans Interest

Namensschuldverschreibungen or “N-bonds”.

La Banque Postale Home Loan SFH

(Covered Bonds Issuer) Investors in the N-bonds benefit from a strong protection with absolute

seniority over the SFH's assets (including the coverpool), by law. They are

Collateralized loans Public Issuances

ranked pari passu with the other SFH's bondholders.

Private Issuances

The N-bonds are registered covered bonds governed by German law.

Covered Bonds Covered Bonds

(OH) Proceeds

Investors

2018 RESULTS – April 2019 INVESTOR PRESENTATION La Banque Postale - 45LBP HOME LOAN SFH

La Banque Postale Home Loan SFH : a resilient and granular cover pool

Program Terms

Program size € 20bn

Rating AAA by S&P

Currency €

Listing Euronext Paris

Governing law French Law, Ability to issue German law governed Namens-schuldverschreibungen

Amount issued €9,236 bn (14/03/2019)

Maturity type Hard/Soft bullet

Registrar and paying agent for NSV LBBW

Cover Pool (ECBC template : reporting date 02/25/2019 – cut-off date 01/31/2019)

Total outstandings € 12,850 bn

Number of loans 192,589

Average loan balance € 66,723

Seasoning 55.9 months

WA LTV 67.6%

Indexed WA LTV 65.9%

Owner occupancy 87.2%

Interest rates 100% fixed rates

2018 RESULTS – April 2019 INVESTOR PRESENTATION La Banque Postale - 46You can also read