Investor Presentation - Advanced Info Service Plc. June 2018 Ticker: ADVANC (SET) - Advanced Info Services Public ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Investor Presentation

Advanced Info Service Plc.

June 2018

Ticker: ADVANC (SET)

AVIFY (ADR)

Add AIS IR LINE@

AIS: Digital Life Service Provider

Lead and digitally transform in Grow stronger in Partner to offer differentiated

“Mobile” “Fixed broadband” “Digital service”

Mobile revenue market share Subscriber market share Focused on FOUR key areas

(approx.8.4mn)

27%

48%

33%

1Q18 21%

1Q18

25%

7% Mobile

39% Video

money

1Q18 breakdown

prepaid postpaid

Bt31bn Enterprise

IoT Business

19% 4th year of operation in 2018

60% Mobile 43%

data

81% covering 50 key cities out of

40% Voice 57% 77 provinces

Mobile revenue subs % to mobile expect to cover 6mn homepass*

40.1mn revenue out of total 21.5m households

Digital life service provider with convergence products

Mark leadership in mobile data Aim to be a significant player in Pursue long-term growth with

• Nationwide 4G/3G/2G coverage 2020 integrated services

with focus on network quality • Leverage existing nationwide fibre • Emphasize partnership &

• Focus on scale to maintain cost infrastructure ecosystem

advantage • Defensive value to core mobile • Leverage the large sub base and

business telecom infrastructure

*Homepass is defined as a number of households within AIS fibre service area. This includes the homes that require additional investment i.e.

port, last miles to be able to get connected.

2

AIS’ digital transformation toward 2020

Next Generation Next Generation Next Generation Next Generation

Network Economy Xperience Team

Network Function Contents and Full Service

Customer Value Organization

Virtualization & Enterprise Digitization

Management Transformation

Cloudification Segments

• > 90%

Target 2020

• Expand revenue • Move to ARPH • Provide shops & • Data-driven

cloudification contribution of • Improve revenue services that organization &

• Network enterprise business assurance and never sleep culture

virtualization ready from 9% to 25% add valued users

for 5G

• 5G future-proof New opportunities: Data-driven • Digitize all • Organization

Strategy toward 2020

networks • IoT analysis based on customer readiness for

• SME & R-SME customer insights: journeys digital disruption

• IT legacy • Managed

transformed to Security Bundle mobile, • AI/Chatbots • Leverage

Cloud-friendly • Mobile Digital fibre & content via embedded into capabilities and

network Marketing FMC all self-service create synergies

architecture channels in value chain

Maximize value of

supporting digital

contents in

• AI for network • Deployment of business

customer retention

operation OMNI channels objectives

and branding

3

1Q18 Quarterly Summary

Service revenue improved in all segments Strategic executions

(Bt mn)

Service ▲6.5% YoY Expand into enterprise market

revenue

34,565 ▲2.5% QoQ

• Paid Bt3.4bn for 81.47% of CSL’s shares

▲3.1% YoY

Mobile 31,172 ▲0.5% QoQ • Fully consolidated since Feb-18

• Incurred goodwill of Bt2.8bn

▲85% YoY • Final tender offer until 6-Jul at Bt7.80/share

FBB 1,013

▲6% QoQ • 7.6GB/sub of mobile

▲63% YoY

data consumption

Others 962 • 51k of FBB net addition Widen e-service/mobile payment to

▲51% QoQ

• CSL revenue Thai users

IC & IC & ▲31% YoY

Equipment 1,418 consolidation

equipment rental ▲28% QoQ

rental • Paid Bt788mn to buy 1/3 JV stake with

Rabbit and LINE

• Utilize each party’s strength in subscriber

Cost controlled resulted in profit expansion base, distribution channel, and brand

EBITDA (Bt mn) NPAT (Bt mn) Officially signed 2100MHz contract

▲9% YoY ▲4.5% YoY

▲2.4% QoQ • Improved service • Agreements effective since 1-Mar

▲4.4% QoQ

20,000 10,000

revenue • Equipment rental agreement

15,000 8,000

10,000

6,000

• Lower regulatory • Roaming agreement

5,000

4,000

fee, network OPEX, • Net financial impact remains relatively the

18,905 2,000 8,037

- - and controlled same at a net cost of Bt3.9bn/year

1Q18 1Q18 handset subsidies

4

FY18 Guidance (maintained)

Item FY18 Guidance

• 2% of which comes from CSL

Service revenue • Increasing data usage on 4G and fixed broadband

+7-8% YoY subscriber base

(ex. IC) • Moderate growth in enterprise business with synergy from

CSL

Decline and make

Sale revenue • More targeted marketing campaigns

near-zero margin

EBITDA margin 45-47% • Improving revenue and continuing cost management

• Strengthen 4G capacity to support mobile data growth

Cash CAPEX Bt35-38bn using advanced technology

• Expand fixed-broadband coverage and last miles

Minimum 70% payout of

Dividend policy • Preserve financial health and flexibility for future growth

NPAT

5

Mobile: Drive 4G users through valued offerings

Business direction in 2018 4G adoption continued uptrend

Key driver

• Increasing 4G penetration and 4G handset penetration

data usage 3G handset penetration

Mobile data revenue (% to mobile revenue)

• Continue to improve network and 56% 53% 50% 60%

49% 46%

brand perception 50%

Strategy

39% 42%

35% 46% 40%

• Target uplifted offerings through 43%

30%

customer value management

20%

program 53% 55% 58% 59% 60%

10%

• Convergence of mobile, FBB, and 0%

video content targeting revenue per

1Q17 2Q17 3Q17 4Q17 1Q18

household and brand value

Focus on postpaid and maintain competitiveness in prepaid

• Postpaid segment grew Prepaid statistics in 1Q18 Postpaid statistics in 1Q18

robustly following

popularity of video -5%

streaming on mobile YoY

flat

-5%

+14% YoY +14% +61% 3.6%

• Prepaid segment YoY YoY +2% +100%

YoY

YoY YoY 1.4%

softened due to

32 7.6 17 13 184 578 7 9.2

prepaid-to-postpaid

conversion and Subscriber Revenue ARPU VOU Churn rate

competition (mn) (Bt bn) (Bt/month) (GB/month) (/month)

6

Mobile: Build end-to-end customer satisfaction

Reinforce OMNI channel and privilege

End-to-end customer

engagement

Increase brand perception in both online & teen segment

Strong

branding Partner with CH3

Zeed SIM for

to co-market teenagers

“Love Destiny”

Product Focus on valued-product proposition

differentiation

Increase Maintain level Targeted

FMC revenue per of profitable offerings

household subsidies

Great network Ensure proper investment and strong spectrum position

quality

55 Low- and Advanced solutions

MHz high-band with pre-5G network

spectrum planning

7

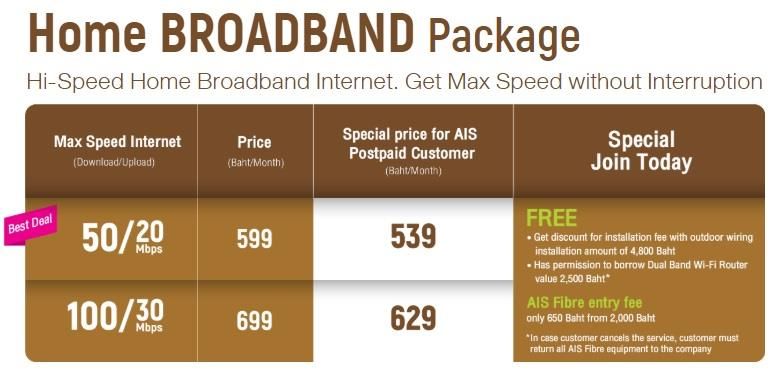

FBB: Industry expanding into fibre-to-the-home

Thai fixed broadband market FBB subscriber market share Industry ARPU

39% market penetration with majority using xDSL Total est.8.4mn users Maintained at around

Bt600/month

Broadband users (mn)

33% ARPU (Bt/month)

% household peneration 637

21% 635

38% 39%

29% 34% 1Q18

26% 600

7%

541

39% 510

6.2 7.2 8.2 8.4

5.4

4Q16 1Q17 2Q17 3Q17 4Q17

FY14 FY15 FY16 FY17 1Q18

Competitive fibre pricing with higher speed at same price

ARPU (Bt/month)

1000

Current fibre plans

800

100Mbps packages are recently affordable

at below Bt1,000

600

400

Typical package for new fixed broadband

customers remained at Bt600, targeting new

and ADSL users

200

0 20 40 60 80 100 120

Download speed (Mbps)

8

AIS Fibre continues to focus on quality customers

with improved acquisition rate

AIS Fibre performance

FBB subscriber (‘000) FBB net additions (‘000)

Focus on existing

ARPU (Baht/month)

50 cities,covering

637 635 618 6mn homepass

1,200 600 650

1,000

541

100

800

482 521 572 550 72 72

600 374 446 51

50 36 40

400 450

200

- 350

- Synergy with CSL in

1Q17 2Q17 3Q17 4Q17 1Q18 1Q17 2Q17 3Q17 4Q17 1Q18 condo segment

• Acquire quality subscribers through

convergence services of “Power4” and

“Family Extra” packages

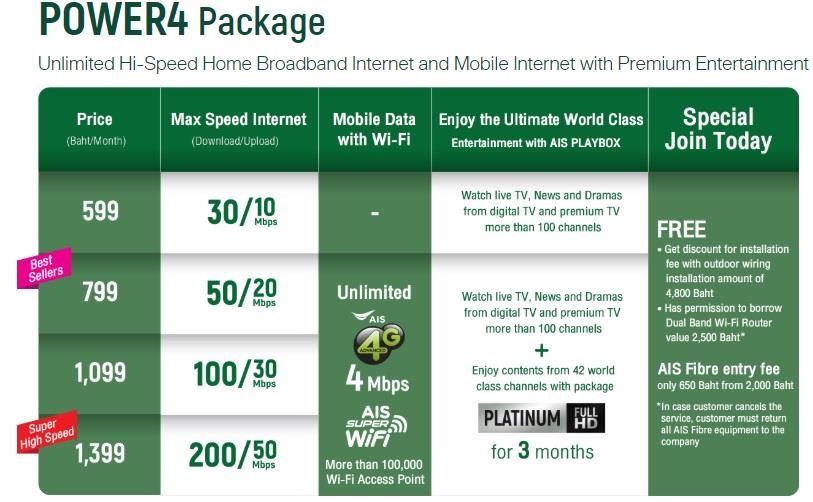

Join AIS Fibre + up to 4 AIS mobile numbers, get extra privileges for a family

Free 2GB Free call

Mobile data to 1 AIS number Pure fixed

broadband 14% Convergence

Get privileges for 86%

Serenade Emerald

HBO movies & series on mobile and extra meals & movies

+ World class cartoons at home privileges AIS Fibre customers by segment

9

Digital services: add on variety of contents &

expand further into digital money segment

Digital contents AIS Rabbit LINE-Pay

Digital contents

2 new channels including CNN and Cartoon Network,

available on AIS PLAY and PLAYBOX • On 5th March 2018 ,AIS, through mPAY, has

entered into 33.33% stake (Bt788mn) in a joint

venture with Rabbit LINE Pay, an e-Money

platform that connect with Bangkok Mass

Transits and is embedded in Line chat

application.

on the go at home • Strengthen AIS’ digital life service provider

position by leveraging customer bases,

available on both AIS PLAY and AIS PLAYBOX platform, channels of AIS and partners to

enhance mobile money for both AIS and non-

AIS customers

Continued to add value and

create differentiation through digital contents

On top packages: Mao Mao Entertain

Free internet in

ViU, Hook, Karaoke apps

Bt19/day

Korean series

512Kbps*

+ or

Hollywood movies

Bt34/day for

UL 4Mbps +8.5mn users

+2.6mn users +45mn users

Karaoke

*FUP: speed drop to 64kbps after 300MB 10Enterprise: CS LOXINFO Business Integration

Enterprise revenue market share

18%

Bt56bn 23%

ICT & Mobile enterprise 5%

market in 2017

Before M&A After M&A

Strengthen position in

enterprise market

Lower inter. bandwidth cost COST SYNERGY

Asset light models

Own fiber infrastructure ✓ Operate CSL’s services with lower OPEX

Data center outside BKK REVENUE SYNERGY Data center in inner BKK

✓ Cross sell & upsell potential from larger customer

Large size corporate customers Mid-size corporate customers

base and complementary product portfolio

Sizable corporate mobile base ✓ Widen Data Center propositions and target Well-known brand with good

segments service quality

Economies of scale OPERATIONAL EFFICIENCY Strong and experienced sales

✓ Sales & Marketing alignment and technical support in ICT

✓ Leverage sale and technical expertise

✓ Align product roadmap

Expected to realize synergy in 1-2 years

11APPENDIX

121Q18 Financial Highlights

FY18

Bt mn 1Q17 4Q17 1Q18 %YoY %QoQ

Guidance

Mobile revenue 30,226 31,016 31,172 ▲3.1% ▲0.5%

Fixed broadband revenue 549 956 1,013 ▲85% ▲6.0%

Other revenues* 589 639 962 ▲63% ▲51%

Service revenue ex. IC & equipment

31,364 32,611 33,147 ▲5.7% ▲1.6% +7-8% YoY

rental

IC and equipment rental 1,087 1,107 1,418 ▲31% ▲28%

Service revenue 32,451 33,717 34,565 ▲6.5% ▲2.5%

SIM and device sales 6,407 7,488 6,368 ▼0.6% ▼15% decline

Total revenue 38,858 41,205 40,933 ▲5.3% ▼0.7%

Cost of service (16,256) (17,018) (17,281) ▲6.3% ▲1.5%

SG&A (5,439) (6,338) (6,336) ▲17% stable

EBITDA 17,347 18,454 18,905 ▲9.0% ▲2.4%

EBIT 10,430 10,290 10,826 ▲3.8% ▲5.2%

NPAT 7,693 7,701 8,037 ▲4.5% ▲4.4%

Capex (11,509) (7,286) (6,467) ▼44% ▼11% Bt35-38bn

Sales margin -6.7% -0.6% -1.1% ▲560bps ▼50bps near-zero

EBITDA margin 44.6% 44.8% 46.2% ▲160bps ▲140bps 45-47%

EBIT margin 26.8% 25.0% 26.4% ▼40bps ▲140bps

NPAT margin 19.8% 18.7% 19.6% ▼20bps ▲90bps

*Other revenues include enterprise data services, including CSL and other revenues

13Improved EBITDA from better revenue growth

and well-managed costs

1Q18 EBITDA (YoY) (Bt mn)

+9.0% YoY

2,115 (232) 359 (868)

340 (156) 18,905

17,347

1Q17 Service Service cost Reg fee Net sales SG&A Others 1Q18

revenue

1Q18 EBITDA (QoQ) (Bt mn)

+2.4% QoQ

848 (192) 21

(174) (23) (29) 18,905

18,454

4Q17 Service Service cost Reg fee Net sales SG&A Others 1Q18

revenue

14Net profit rose from strong EBTIDA despite 4G and

fixed broadband investment

EBITDA & margin Net profit & margin

EBITDA (Bt bn)

EBITDA margin, excluding TOT equipment rental (%)

Net profit (Bt bn) Net profit margin (%)

46.9%

44.6% 44.8%

24.0 45.0%

12.0 19.8% 18.7% 19.6%

22.0 11.0

40.0%

20.0 18.5 18.9 10.0

17.3 35.0% 9.0

7.7 7.7 8.0

18.0 +9.0% YoY 8.0

30.0% +4.5% YoY

16.0 +2.4% QoQ 7.0

14.0 25.0% 6.0 +4.4% QoQ

20.0% 5.0

12.0

4.0

10.0 15.0% 3.0

1Q17 4Q17 1Q18 1Q17 4Q17 1Q18

• 1Q18 EBITDA rose YoY and QoQ, 1Q18 net profit grew YoY and QoQ from

underpinned by decent revenue momentum improved EBITDA despite increased D&A

and ongoing cost optimization program. from 4G investment.

• Excluding impact from TOT equipment rental,

EBITDA margin improved to 46.9% and

aligned with the full year guidance of 45-47%.

15Maintained financial flexibility for future growth

1Q18 Balance Sheet 1Q18 Cash flow

(Bt bn) (Bt bn) Cash increase Cash decrease

others A/P

spectrum license Operating Investing Financing Net cash

spectrum 21 34 payable 18.1

license

106 74

Assets Liabilities goodwill

3 9.3

6.5

239 4.2

B/S

287 2.2

1Q18 interest- 0.4 0.3 0.4

101 bearing

CAPEX

Income

tax paid

Finance cost

cash flow

decreased

Cash

Operating

acquisition

JV & Business

Repayment of

Others

borrowings

debt

134 Equity

48

PPE 27

22 others

18 26

A/R 8

retained earnings

cash others CAPEX continued to decline to Bt6.5bn or 19% to

service revenue after completing nationwide 4G at

end of 2016

1.2X 2.1X

Operating cash flow remained strong to support

Net debt to EBITDA Interest bearing debt

to Equity future investment

Average finance costs = 3.2% p.a.

• Maintaining investment grade credit ratings

0.5X 65% • Fitch: national rating AA+ (THA), outlook stable

Current ratio Return on Equity • S&P: BBB+, outlook negative

16Mobile: 40.1m subs with expanding postpaid segment

Subscribers (mn) postpaid prepaid ARPU (Bt/sub/month) postpaid prepaid blended

34.0 33.5 33.0 32.7 32.4 579 593 590 581 578

244 251 254 256 257

6.7 7.0 7.2 7.4 7.6 181 182 182 183 184

Net addition (‘000) VOU (GB/data sub/month)

232 330 235 227

163

7.6

5.7 4.0 6.7 7.5 5.4 5.9 8.3 6.2 6.7 9.2 7.0

3.5 4.7

-233 4.1

-294

-615 -504 -523

1Q17 2Q17 3Q17 4Q17 1Q18 1Q17 2Q17 3Q17 4Q17 1Q18

• Mobile subscribers was at 40.1mn, a slight drop of • Blended ARPU improved Bt1 QoQ, reaching Bt257

5.5k QoQ from lower prepaid users. from larger postpaid mix.

• Postpaid subscribers grew 227k QoQ from bundled • Blended VOU increased to 7.6GB from increasing

package offerings and migration from prepaid. 4G adoption and popularity of video streaming.

• Prepaid subscribers decreased 233k QoQ due to

migration to postpaid and market competition.

17Mobile price plans: Target better ARPU and build

differentiation on postpaid

Unlimited data usage with capped-speed packages Full 4G speed packages

• Offer unlimited data usage at different • Attract new data users and encourage higher ARPU

speeds for diverse needs e.g. chat, social subscriptions through premium VDO contents e.g. AIS

networks, music, HD video streaming PLAY, Premier package, HOOQ, and Netflix

• Encourage customers to move from prepaid • 4G speed with FUP, reduced speed after reaching the data

to postpaid subscription with worry-free plan usage limit

• Serve high-end heavy data users with real unlimited max

speed experience

Buffet Net Plus 4G MAX SPEED

4G/3G FUP after Call all

Monthly Call within Enjoy Monthly Total

Unlimited internet reach data networks Enjoy Free

Fee (Bt) AIS (mins) Free Fee (Bt)

max speed at usage limit (mins)

5 numbers 299 1GB 100

299 1Mbps

24 hr. 1 month 1 month

399 3GB 150

450 2Mbps 128kbps

499 7GB 200

550 4Mbps Unlimited

5am – 5pm 599 10GB 250

600 6Mbps 3 months

799 15GB 350 3 months

*AIS WIFI is included in all packages.

384kbps

999 20GB 450

1,099 650

1,299 Unlimited 850

at max -

1,499 speed 1,200

3 months

1,899 2,000

*AIS WIFI is included in all packages.

18

Updated: May-18Mobile market share by subscribers

Total subscriber (mn)

92 96 90 90

75 83 83

25% 25%

25% 23% 27% 30%

25% Operator 3

30% 29% 27%

32% 31% 25%

31% Operator 2

45% 46% 46% 46% 45% AIS

44% 43%

2011 2012 2013 2014 2015

* 2016 2017

Postpaid subscriber (mn) Prepaid subscriber (mn)

81 83

74 68 73 70

68 24%

20 24%

25% 25%

18 25% 21% 29%

14 35% 29%

7.4 9.1 11 13 34% 32%

30%

31% 27%

33% 31% 24%

31% 28%

23% 29% 29%

29% 31% 30%

31% 32% 45% 47% 48% 48% 47%

32% 37% 44% 43%

39% 39% 38% 37%

45% 41%

2011 2012 2013 2014 2015 2016 2017 2011 2012 2013 2014 2015 * 2016 2017

* In 2015, sub base of the industry was affected by the adjustment of prepaid sub reporting to reflect only active ones. The decrease in sub base also

caused by NBTC’s announcement requiring prepaid sub to register their SIMs. The SIMs that failed to register by the deadline were terminated.

19AIS Fibre: Competitive price plans with differentiation

Bt599/month Bt399/month Bt299/month Bt199/month

20

Updated: May-18Historical profitability and CAPEX trend

Industry AIS

EBITDA margin

45% 42% 42% 44% 46% 40% 45%

36% 32% 32% 33% 33% 32% 36%

2011 2012 2013 2014 2015 2016 2017

Industry AIS

NPAT margin

24% 24% 24% 25% 20%

14%18% 14% 19%

13% 9% 13% 9% 8%

2011 2012 2013 2014 2015 2016 2017

AIS’ CAPEX to service revenue ex. IC AIS’ CAPEX (Bt bn)

41% 32%

24% 28% 27%

CAPEX

6% 9%

48

41

10 28 33 32

6

2011 2012 2013 2014 2015 2016 2017

Source: company data

21Debt payment and License payment schedule

Spectrum license payment schedule* Debt repayment Schedule

900x10MHz license payment (Bt bn) Debenture (Bt bn) Loan (Bt bn)

1800x15MHz license payment (Bt bn)

59.6

Total payment of

Bt78bn toward 2020

24.8

13.9 13.3 14.2

14.3 2.8 11.2

6.4 6.6 7.2 9.0

4.0 3.4 12.1

4.0

10.2 7.8 7.8 0.0

1.8

2018 2019 2020 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027

Note: 1800x15MHz license: the total payment is Bt40,986m for the use of 18 years, expiring in 2033

900x10MHz license: the total payment is Bt75,654m for the use of 15 years, expiring in 2031

22Distribution Channel

expanding touch points to +400k

AIS Branded Shop Exclusive branded shop by AIS Buddy

partner (Telewiz)

100+ shops 450+ shops 1,000+ shops

Electronic Distribution Channels Modern Trade Outlets

400k+ points 10k+ shops

(refill-on–mobile Auto top-up

agent ) KIOSK

23Digital content: More varieties and exclusivities

Introduced new content packages to attract customers with different preferences e.g. sports,

family, movies at more affordable prices on both AIS PLAY and AIS PLAYBOX.

NEW NEW

Mobile

Ultimate Ultimate Movies and Exclusive sport

entertainment entertainment series from entertainment

+ Unlimited Bt299month HBO Bt199month

internet Bt199month

Bt499/month

Fixed broadband

NEW NEW NEW

Ultimate Ultimate World class Thrilling

entertainment movies & series cartoons sports matches

in all forms Bt399month Bt299month Bt199month

Bt599/month

24

Updated: May-18Contact us IR website: http://investor.ais.co.th Email: investor@ais.co.th Tel: +662 029 5014 Disclaimers Some statements made in this material are forward-looking statements with the relevant assumptions, which are subject to various risks and uncertainties. These include statements with respect to our corporate plans, strategies and beliefs and other statements that are not historical facts. These statements can be identified by the use of forward-looking terminology such as “may”, “will”, “expect”, “anticipate”, “intend”, “estimate”, “continue” “plan” or other similar words. The statements are based on our management’s assumptions and beliefs in light of the information currently available to us. These assumptions involve risks and uncertainties which may cause the actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements. Please note that the company and executives/staff do not control and cannot guarantee the relevance, timeliness, or accuracy of these statements.

You can also read