Investor Presentation - August 2020 - Viper Energy Partners

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Investor Presentation August 2020

Forward Looking Statements

This presentation contains “forward-looking statements” within the meaning of the securities laws. All statements, other than statements of historical fact, included in this presentation that

address activities, events or developments that Viper Energy Partners LP (“Viper,” the “Partnership,” “VNOM”, “we” or “our”) expects, believes or anticipates will or may occur in the future are

forward-looking statements. The words “believe,” “expect,” “may,” “estimates,” “will,” “anticipate,” “plan,” “intend,” “foresee,” “should,” “would,” “could,” or other similar expressions are

intended to identify forward-looking statements, which are generally not historical in nature. However, the absence of these words does not mean that the statements are not forward-

looking.

Without limiting the generality of the foregoing, these statements discuss future expectations, contain projections of results of operations or of financial condition or state other forward-looking

information and include statements with respect to, among other things, Viper’s ability to make distributions on the common units and expectations of plans, strategies and objectives and

anticipated financial and operating results of Viper. These statements are based on certain assumptions made by Viper based on management’s expectations and perception of historical

trends, current conditions, anticipated future developments and other factors believed to be appropriate. Such statements are subject to a number of assumptions, risks and uncertainties,

many of which are beyond the control of Viper, which may cause actual results to differ materially from those implied or expressed by the forward-looking statements. These include the

factors discussed or referenced in the “Risk Factors” section of Viper’s Annual Report on Form 10-K, Quarterly Reports on Form 10-Q and Current Reports on Form 8-K and in Viper’s other filings

with the Securities and Exchange Commission (the “SEC”), risks relating to financial performance and results, current adverse industry and macroeconomic conditions and resulting capital

restraints, Viper’s future cash distribution policy, depressed commodity prices and demand for oil and natural gas and impact on proved reserves, borrowing base redeterminations and

possible impairments of oil and gas interests, availability of drilling equipment and personnel, availability of sufficient capital to execute our business plan and acquisition strategy, impact of

compliance with legislation and regulations, including any regulatory action that may impose production limits on Viper’s properties, the impact and duration of the ongoing COVID-19

pandemic, including logistical challenges and the supply chain disruptions, successful results from our operators’ identified drilling locations, our operators’ ability to efficiently develop and

exploit the current reserves on our properties, any delays, curtailments or interruptions of production on our mineral and royalty acreage, our ability to acquire additional mineral and royalty

interests, our pending, completed or future acquisitions of mineral and royalty interests and other important factors that could cause actual results to differ materially from those projected.

Any forward-looking statement speaks only as of the date on which such statement is made and Viper undertakes no obligation to correct or update any forward-looking statement, whether

as a result of new information, future events or otherwise, except as required by applicable law.

Non-GAAP Financial Measures

Adjusted EBITDA is a supplemental non-GAAP financial measure that is used by management and external users of our financial statements, such as industry analysts, investors, lenders and

rating agencies. Viper defines generally accepted accounting principles, or GAAP. Management believes Adjusted EBITDA is useful because it allows it to more effectively evaluate Viper’s

operating performance and compare the results of its operations from period to period without regard to its financing methods or capital structure. Adjusted EBITDA should not be considered

as an alternative to, or more meaningful than, net income as determined in accordance with GAAP or as an indicator of Viper’s operating performance or liquidity. Certain items excluded

from Adjusted EBITDA are significant components in understanding and assessing a company’s financial performance, such as a company’s cost of capital and tax structure, as well as the

historic costs of depreciable assets, none of which are components of Adjusted EBITDA. Viper defines cash available for distribution generally as an amount equal to its Adjusted EBITDA for the

applicable quarter less cash needed for debt service and other contractual obligations and fixed charges and reserves for future operating or capital needs that the board of directors of

Viper’s general partner may deem appropriate. Viper’s computations of Adjusted EBITDA and cash available for distribution may not be comparable to other similarly titled measures of other

companies or to such measure in its credit facility or any of its other contracts. For a reconciliation of Adjusted EBITDA to net income (loss), please refer to Viper’s filings with the SEC.

Oil and Gas Reserves

The SEC generally permits oil and gas companies, in filings made with the SEC, to disclose proved reserves, which are reserve estimates that geological and engineering data demonstrate

with reasonable certainty to be recoverable in future years from known reservoirs under existing economic and operating conditions, and certain probable and possible reserves that meet

the SEC’s definitions for such terms. Viper discloses only estimated proved reserves in its filings with the SEC. Viper’s estimated proved reserves as of December 31, 2019 contained in this

presentation were prepared by Ryder Scott Company, L.P., an independent engineering firm, and comply with definitions promulgated by the SEC. Additional information on Viper’s

estimated proved reserves is contained in Viper’s filings with the SEC.

In this communication, Viper may use the terms “resources,” “resource potential” or “potential resources,” which the SEC guidelines prohibit Viper from including in filings with the SEC.

“Resources,” “resource potential” or “potential resources” refer to Viper’s internal estimates of hydrocarbon quantities that may be potentially discovered through exploratory drilling or

recovered with additional drilling or recovery techniques. Such terms do not constitute reserves within the meaning of the Society of Petroleum Engineer’s Petroleum Resource Management

System or SEC rules and does not include any proved reserves. Actual quantities that may be ultimately recovered by the operators of Viper’s properties will differ substantially. Factors

affecting ultimate recovery include the scope of the operators’ ongoing drilling programs, which will be directly affected by the availability of capital, drilling and production costs, availability

of drilling services and equipment, drilling results, lease expirations, transportation constraints, regulatory approvals and other factors; and actual drilling results, including geological and

mechanical factors affecting recovery rates. Estimates of potential resources may change significantly as development of our properties by our operators provide additional data. In addition,

our production forecasts and expectations for future periods are dependent upon many assumptions, including estimates of production, decline rates from existing wells and the undertaking

and outcome of future drilling activity, which may be affected by significant commodity price declines or drilling cost increases.

2

Viper: Investment Highlights

2Q ‘20 cash available for distribution of $0.12/unit; Board approved distribution of $0.03 with remaining available

cash to be retained for balance sheet strength

Q2 2020 Review 2Q ‘20 average oil production of 14,453 Bo/d, up 9% year over year

134 total gross (2.4 net 100% royalty interest) horizontal wells with average lateral of 8,648’ turned to production

during 2Q ‘20

Q3 2020 / Q4 2020 average production guidance of 14,750 – 16,000 Bo/d (24,500 – 26,500 Boe/d), the midpoint of

which is up 6% from 2Q ‘20 average daily oil production

FY 2020 production guidance of 15,250 – 16,000 Bo/d (25,250 – 26,250 Boe/d)

Durable Free

Cash Flow Relationship with Diamondback and diversified exposure to other well-capitalized operators within the Permian Basin

Profile and Eagle Ford Shale support Viper’s production profile

High cash margins, no capital requirements and limited operational costs drive continuous free cash flow generation

Strong free cash flow generation and variable equity distribution model enables cash flow flexibility

24,714 net royalty acres positioned in the core of the Permian Basin and Eagle Ford Shale with 14 rigs currently

operating on Viper’s acreage

Unmatched Size

and Scale Proved reserves as of December 31, 2019 of 88.9 MMBoe (78% PDP, 54.4 MMBo), up 41% year over year

Strong liquidity position of $436 million with low G&A burden and limited interest expense as primary cash expenses

485 gross (8.1 net 100% royalty interest) horizontal wells in the process of active development

Undeveloped 440 line-of-sight wells with visibility to potential of future development in coming quarters, but which are not

Inventory currently in the process of active development, in which Viper expects to own an average 2.0% NRI (8.8 net

Supports Long- 100% royalty interest wells)

Term Growth Largely undeveloped, concentrated acreage throughout the core of the Permian under competent

operators, primarily Diamondback, provides long-term organic growth potential

Viper’s Mineral and Royalty Interests Provide Significant Exposure to Perpetual Ownership of High Margin,

Largely Undeveloped Assets with Zero Capital Requirements to Support its Sustainable Free Cash Flow (1)

Source: Partnership data and filings. Data as of 6/30/2020 unless otherwise noted.

(1) Approximately 87% of Viper’s royalty assets are perpetual; the remaining royalty assets are overriding royalty interests that are subject to lease expirations and not perpetual.

3

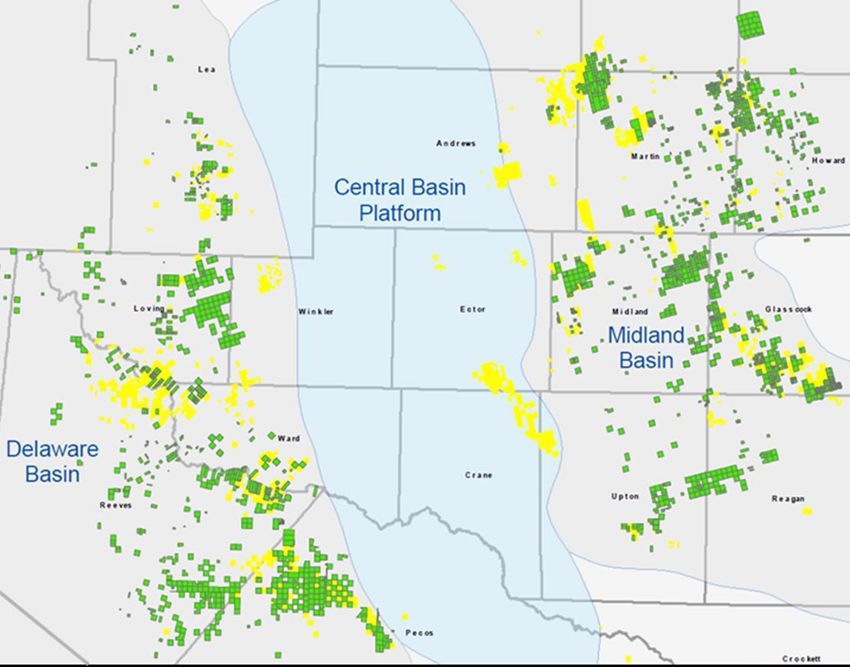

Viper Energy Partners Overview

Differentiated Investment Opportunity Viper Mineral and Royalty Assets

Unique Relationship with Primary Operator VNOM royalty acreage

Diamondback relationship and ownership reduces

uncertainty around pace of development

FANG acreage

Free Cash Flow Positive Through the Cycle

High margins, no capital requirements and limited

operating costs drive continuous free cash flow generation

Perpetual Ownership with Priority Claims(1)

Mineral interests have claim to first-dollar-out

At expiration of lease, all rights revert to mineral owner

Significant Undeveloped Resource

Permian assetFree Cash Flow Sensitivity

Due to its high return and high cash margin structure, Viper’s free cash flow is resilient to changes in

commodity prices; further upside to commodity prices in 2021 as hedges roll off

At $40 oil and production held flat relative to its 2H 2020 guidance levels, Viper is expected to

generate >$180 million in free cash flow on an annualized basis in the first half of 2021, or a greater

than 11% free cash flow yield

Illustrative 2H 2020E and 1H 2021E Annualized Free Cash Flow Based on 2H 2020 Production Guidance(1)

2H 2020 Annualized FCF 1H 2021 Annualized FCF

Assumptions

Annualized FCF Yield @ Guidance Midpoint $250

14.75 – 16.00 Mbo/d

Oil Production

Annualized Free Cash Flow ($MM)

24.50 – 26.50 Mboe/d $200

Total Production

$6.5 Million

Cash G&A $150

14.0%

$32 Million 12.9%

Interest Expense(2) 11.5%

9.8% $100

7% of Revenue 8.2%

11.4%

Prod. & Ad Valorem Taxes 10.5%

9.7%

8.9%

25% of WTI / $1.00/Mcf 7.7% $50

Realized NGL / Gas Prices

~95% $0

% of WTI Realized ($/Bbl)

$30.00 $35.00 $40.00 $45.00 $50.00

Source: Partnership data and filings. Financial data as of 6/30/2020. Yield based on unit closing price as of 7/31/2020.

(1) Free cash flow defined as operating cash flow before changes in working capital. Includes hedge gain/(loss).

(2) Roughly approximates total interest expense based on 5.375% fixed interest payments on $480 million Sr. Notes due 2027, 3.0% interest on $153mm drawn on the revolving credit facility and a

0.4% non-use fee on the undrawn capacity of the revolving credit facility. 5Portfolio Overview

134 gross (2.4 net) horizontal wells turned to production during Q2 2020

Near-term inventory of 8.1 net wells currently in the process of active development and an

additional 8.8 net line-of-sight wells not currently being developed

14 gross rigs currently operating on Viper’s acreage, 4 of which are operated by Diamondback

No acquisitions were completed during Q2 2020, leaving Viper’s footprint of mineral and royalty

interests at a total of 24,714 net royalty acres

Diamondback Operated Third Party Operated

Midland Delaware Midland Delaware Eagle Ford Total

Net Royalty Acres 7,384 5,231 5,194 6,224 681 24,714

2Q ‘20 Gross Hz Wells Turned to

Production (Net 100% NRI Wells)

10 (0.9) 4 (0.3) 47 (0.6) 37 (0.4) 36 (0.2) 134 (2.4)

Gross Producing Hz Locations

(Net 100% NRI Wells)

733 (65.8) 346 (18.6) 1,077 (28.6) 985 (15.6) 1,339 (7.6) 4,480 (136.2)

Gross Active Rigs

(Net 100% NRI Rigs)

4 (0.1) 0 (0.0) 7 (0.1) 3 (0.1) 0 (0.0) 14 (0.3)

Gross Work-in-Progress(1)

(Net 100% NRI Wells)

40 (4.2) 26 (1.0) 252 (1.4) 97 (1.2) 70 (0.3) 485 (8.1)

Gross (Net) Line-of-Sight(2) 53 (3.6) 21 (0.7) 179 (2.2) 146 (2.1) 41 (0.2) 440 (8.8)

Source: Partnership data and estimates and DrillingInfo. Acreage as of 6/30/2020; activity data as of 7/14/2020. Existing permits or active development of Viper’s royalty acreage does not ensure

that those wells will be turned to production given the current depressed oil prices.

(1) Work in progress wells represent those that have been spud and are expected to be turned to production within approximately the next six to eight months.

(2) Line-of-sight wells are those that are not currently in the process of active development, but for which Viper has reason to bel ieve that they will be turned to production within approximately

the next 15 to 18 months. The expected timing of these wells is based primarily on permitting by third party operators or Diamondback’s current expected completion schedule.

6Near-Term Inventory Summary and Forward Visibility

Diamondback has recently brought three completion crews back to work after taking an almost

three-month break from all completion activity in the second quarter of 2020

Diamondback expects to focus its completion activity on areas where Viper has significant royalty

interests, primarily in the Midland Basin

Visibility into third party operators’ anticipated activity levels has remained limited due to current

depressed commodity price environment, but has increased in recent months

100% NRI Work-in-Progress(1) 100% NRI Line-of-Sight(2) 100% NRI Near-Term Inventory

OTHER

15% OTHER OTHER

23% 24%

PXD 2%

COP 3%

EOG 3%

COP 2% FANG

XTO 5% 8.1 PE 3% 8.8 49%

COP 2%

XTO 4%

16.8 FANG

XTO 4% 56%

SM 8% FANG SM 4%

64%

CXO 8% CXO 4%

PXD 6%

PXD 11%

Diamondback and Other Well-Capitalized Operators Support Viper’s Production Profile

Source: Partnership data and estimates. Existing permits or active development of Viper’s royalty acreage does not ensure that those wells will be turned to production given the current depressed

oil prices.

(1) Work in progress wells represent those that have been spud and are expected to be turned to production within approximately the next six to eight months.

(2) Line-of-sight wells are those that are not currently in the process of active development, but for which Viper has reason to bel ieve that they will be turned to production within approximately

the next 15 to 18 months. The expected timing of these wells is based primarily on permitting by third party operators or Diamondback’s current expected completion schedule.

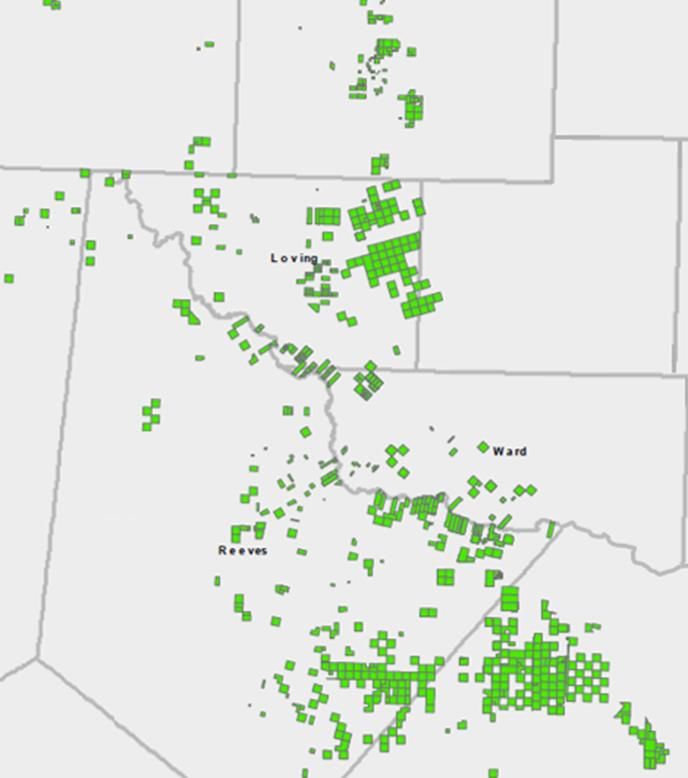

7Diamondback DUC Backlog Overview

Diamondback’s DUC Backlog on Viper’s Royalty Acreage as of 6/30/2020

VNOM royalty acreage

FANG acreage Andrews/Martin: 10-15 gross DUCs

Average NRI: 4.5%

Average Lateral: 9,200’

Howard: 20-25 gross DUCs

Average NRI: 2.0%

Average Lateral: 10,200’

Midland: 20-25 gross DUCs

Average NRI: 16.5%

Average Lateral: 11,100’

N. Delaware 0-5 gross DUCs

Average NRI: 0.5%

Average Lateral: 10,400’

Glasscock: 0-5 gross DUCs

Average NRI: 12.5%

Average Lateral: 7,500’

ReWard: 15-20 gross DUCs

Average NRI: 3.0%

Average Lateral: 10,100’

Pecos: 25-30 gross DUCs

Average NRI: 4.0%

Average Lateral: 10,200’

Viper Has Meaningful Exposure to Approximately 65% of Diamondback’s Total Gross DUCs

Source: Partnership data and estimates. DUC backlog as of 6/30/2020.

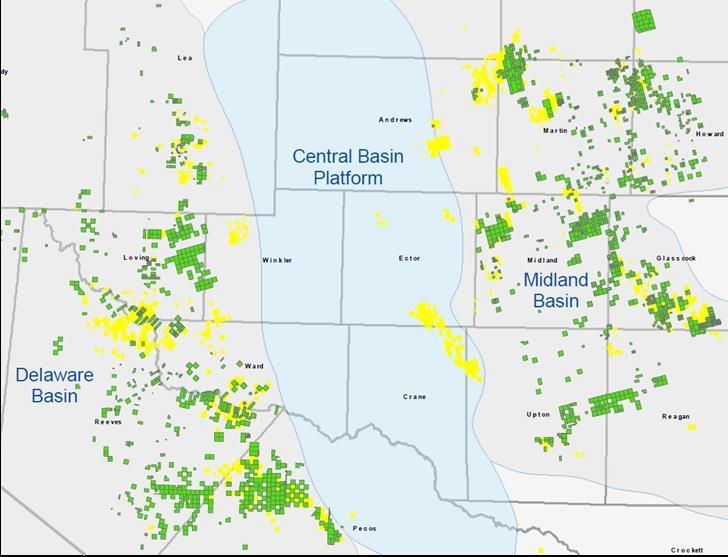

8Significant Undeveloped, Concentrated Resource

Highly Concentrated Acreage in Midland Basin Illustrative Remaining Midland Basin Resource

12,578 VNOM

Net Royalty Acres

Assumed 1.5

Assumed 25%

mile lateral

lease royalty

(240 NRA)

13.1 Net Drilling Spacing

Units (100% NRI)

28 wells

per 1.5

mile DSU

~365 illustrative net

Estimated 900

100% NRI VNOM

MBoe EUR/well

locations

~329 MMBoe

Total Resource

% Developed ~270 remaining

~95 producing

net locations

% Undeveloped net locations

(>70% undeveloped;

(Significant Undeveloped, Concentrated Resource

Highly Concentrated Acreage in Delaware Basin Illustrative Remaining Delaware Basin Resource

11,456 VNOM

Net Royalty Acres

Assumed 1.5

Assumed 25%

mile lateral

lease royalty

(240 NRA)

11.9 Net Drilling Spacing

Units (100% NRI)

20 wells

per 1.5

mile DSU

~240 illustrative net

Estimated 1,000

100% NRI VNOM

MBoe EUR/well

locations

~240 MMBoe

Total Resource

% Developed

~205 remaining

~35 producing

net locations

% Undeveloped net locations

(>85% undeveloped;

(Spectrum of Oil and Gas Interest Ownership

~87% of Viper’s Royalty Assets

Own rights in perpetuity; all development rights revert to mineral owner at

1 expiration of lease

Perpetual Mineral Revenue is received from E&P companies as lessor royalties from producing wells

Interest(1) located on leased lands

~13% of Viper’s Royalty Assets (55% of which operated by FANG)

Overriding Royalty

2 Royalty interests carved out of lessee’s leasehold interest

Interest (ORRI)

Burdens working interest and expires with underlying lease

Volumetric Production Structured investment that relates to a specific amount of

Payment

3 production for a pre-determined amount of time

Royalties paid based on the profitability of a defined area

Net Profit Interest

4 Royalty collector exposed to operating and capital costs,

typically excluding environmental liabilities

Acreage is leased from a mineral owner

Working Interest

5 Responsible for drilling wells (if they are the operator)

and associated capital and operating costs

Minerals Provide the Greatest Form of Protection Available in the Oil Industry Due Perpetual Ownership and

Priority Claims with Right to First-Dollar-Out

Source: Partnership data and filings. Acreage as of 6/30/2020.

(1) Includes non-participating royalty interests.

11Illustrative Delaware Basin Oil & Gas Lease Life Cycle

Sign New

Lease

2015: Minerals Leased 2018: Extension 2021: CDC Expires

• 25% royalty • No development by • Operator does not

• Lease bonus operator within drill any additional

• 3-year primary term primary term wells

• 180-day CDC(1) • Another lease bonus • Lease terminates for

• Lease requires 4 wells to mineral owner 1/1/2020 7/1/2020 any land/depths not

to hold 640 acres per • Maintain other Held-by-Production

zone requirements of lease

Operator drills Operator drills Extend

2 WCA(2) wells 1 2BS(4) well Lease

Pugh Clause

Security of Mineral Ownership

Mineral ownership remains safest asset in the oil

industry because it is a perpetual, real property

1 Mile

1 Mile

interest

Lease terms like “Continuous Development

Clause” and “Pugh Clause” allow for 1 Mile 1 Mile

development rights to revert to mineral owner if no 320 acres of 320 acres of

WCA HPB(3) WCA HPB

development by lessee &

160 acres of

Right to receive compensation in various forms 2BS HPB

and right to first-dollar-out with priority claims

(1) CDC: Continuous Development Clause.

(2) WCA: Wolfcamp A.

(3) HBP: Held by Production.

(4) 2BS: Second Bone Spring. 12How Viper Defines a “Net Royalty Acre”

Methodology for deriving “Net Royalty Viper’s Formula for Net Royalty Acreage

Acreage” differs widely across the industry

Many companies calculate assuming there

are eight royalty acres for every one net Net Lease Net

Royalty

mineral acre (NMA) Mineral Royalty

Acres and other

burdens Acres

Viper derives its total net royalty acreage

from net mineral ownership taking into Viper believes its methodology more accurately defines its

consideration the royalty interest AND all acreage for which it will receive revenue

other burdens

Acreage Definition Comparison NRA Example Assuming Standard ¼ Royalty

640

NMA 160 NRA

Viper Net Royalty Acres 24,714

Mineral Royalty

640-acre Acres Acres

section

Viper Net Royalty Acres

(Normalized to 1/8) 197,712

100%

Mineral 640 1,280

0 50,000 100,000 150,000 200,000 Interest NMA NRA

Mineral Royalty

Acres Acres

Source: Partnership data and filings. Acreage data as of 6/30/2020.

13Financial Overview

Financial Strategy Viper Capitalization

Maintain Financial Flexibility

($ in millions) 6/30/2020

♦ Borrowing base of $580 million with only $154 million

drawn as of 6/30/2020 Cash $10

♦ Maintain strong liquidity and optionality with cash flow Revolving Credit Facility 154

to strengthen balance sheet

Borrowing Base 580

Availability Under Revolver 426

Use of Cash Available for Distribution up to Board of

Directors’ Discretion Each Quarter Senior Notes 486

♦ Historically (through 2019) had paid substantially all Liquidity $436

cash available to unitholders through quarterly

Net Debt / LTM EBITDA 2.5x

distributions

♦ 75% of available cash from 1Q ‘20 and 2Q ‘20 retained Guidance Update

to strengthen balance sheet

Q3/Q4 2020 Net Oil Production – Mbo/d 14.75 – 16.00

Downside Protection Provided through Hedges

Q3/Q4 2020 Net Total Production – Mboe/d 24.50 – 26.50

♦ Majority of 2020 oil production hedged through collars

Full Year 2020 Net Oil Production - Mbo/d 15.25 – 16.00

♦ Downside protected in 2020 to $30 oil for large portion

of expected production Full Year 2020 Net Total Production – Mboe/d 25.25 – 26.25

Unit Costs ($/boe)

No Direct Operating or Capital Expenses

Cash G&A $0.60 - $0.80

♦ Focus on mineral and royalty interests preserves low-

cost structure Non-Cash Equity Based

$0.10 - $0.25

Compensation

♦ Expected production and ad valorem taxes of 7.0% of

royalty income Depletion $9.50 - $11.50

♦ Operators bear capital burden, allowing Viper to Production and Ad Valorem Taxes (% of

7% - 8%

generate continuous free cash flow Revenue)(1)

Interest Expense(2) $3.25 - $3.75

Source: Partnership data and filings.

(1) Includes production taxes of 4.6% for crude oil and 7.5% for natural gas and NGLs and ad valorem taxes.

(2) Assumes 1H 2020 actual interest expense plus interest expense for the remainder of 2020 assuming $480mm in principal of Sr. Notes and $155mm drawn on the revolver.

14Hedge Update

Crude Oil (Bbls/day, $/Bbl) Q3 2020 Q4 2020 FY 2021

1,000 1,000 -

Swaps - WTI

$27.45 $27.45 -

Costless Collars - WTI 14,000 14,000 10,000

Floor $28.86 $28.86 $30.00

Ceiling $32.33 $32.33 $43.05

Deferred Premium Call Options - WTI - 8,000 -

Premium - -$1.89 -

Strike - $45.00 -

4,000 4,000 -

Basis Swaps - WTI (Midland-Cushing)

-$2.60 -$2.60 -

Natural Gas (Mmbtu/day, $/Mmbtu) Q3 2020 Q4 2020 FY 2021

Natural Gas Basis Swaps - 25,000 25,000 -

Waha Hub -$2.07 -$2.07 -

Source: Partnership data as of 6/30/2020.

15Final Thoughts

Viper Energy Partners offers sustainable free cash flow, substantial

remaining inventory and upside to future strength in commodity prices

Mineral ownership provides surest form of security in the oil industry

Relationship with Diamondback provides visibility to production and

cash flow growth

Royalty assets offer organic growth without any capital costs or

operating expenses

Strong free cash flow generation with financial flexibility

Advantaged tax structure that enables non-taxable distributions

(1) Last eight quarterly quarterly distributions reasonably determined to not constitute dividends for U.S. federal income tax purposes; rather constitute non-taxable reductions to tax basis.

16Viper Energy Partners LP Kaes Van’t Hof, President

500 West Texas Ave., Suite 1200 (432) 221-7430

Midland, TX 79701 minerals@viperenergy.com

www.viperenergy.com

Adam Lawlis, Vice President, Investor Relations

(432) 221-7430

ir@viperenergy.com

17You can also read