Unusually-failed to dent discretionary retail sales - Coresight Research

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

July 4, 2018

Our 2018 Midyear Wrap-Up condenses our coverage of major retail events and

developments from the first half of 2018.

1) US retail sales are up by a solid 4.5% year over year. Higher gas prices have—

unusually—failed to dent discretionary retail sales.

2) Store closures by major US retailers have reached 4,136 to date. We estimate that

2018 will end with 8,000–10,000 US store closures, exceeding the 7,066 closures

that we recorded for 2017.

3) In the UK, store closure numbers have surged. So far, we have recorded 934

announced closures, compared to the 1,005 closures we recorded for 2017 as a

whole. This suggests that the number of UK store closures for the full year could

almost double.

4) Target will invest $3.5 billion this year to remodel stores, open new-format stores

and expand digital fulfillment.

5) Zalando remains on course to double sales by 2020.

Deborah Weinswig, CEO and Founder, Coresight Research

6) JD.com opened a new supermarket format and plans to put convenience stores in

many

deborahweinswig@fung1937.com US: 917.655.6790 HK: 852.6119.1779 Chinese villages.

CN: 86.186.1420.3016

1

Copyright © 2018 Coresight Research. All rights reserved.

July 4, 2018

Table of Contents

Introduction ........................................................................................................................................................................................................... 3

1. Events................................................................................................................................................................................................................. 5

US Gas Prices Jumped—But Retail Growth Did Not Take a Hit................................................................................................................................ 5

US Retail Is On Track for Around 10,000 Store Closures This Year ........................................................................................................................... 7

The UK Is Seeing a Raft of Store Closures, Too ........................................................................................................................................................ 9

The US-China Tariff War Kicks Off Again ................................................................................................................................................................11

2. Companies.........................................................................................................................................................................................................14

Reviewing Partnerships and Investments ..............................................................................................................................................................14

Hearing About Target’s Plans for 2018 and 2019 ...................................................................................................................................................16

In Europe, Zalando Is “On Track” to Double Sales by 2020.....................................................................................................................................19

UK Department Store Retailers Plan a Slew of Closures.........................................................................................................................................20

Sainsbury’s-Asda Merger Could Create the UK’s “Amazon Crusher” ......................................................................................................................23

Management Arrivals and Departures ...................................................................................................................................................................25

3. Conferences.......................................................................................................................................................................................................27

Hearing About New Retail at World Retail Congress 2018 .....................................................................................................................................27

Our Notes from Shoptalk 2018 ..............................................................................................................................................................................28

What We Heard at ICSC Recon...............................................................................................................................................................................30

Fashion Industry Takeaways from WWDMAGIC 2018............................................................................................................................................32

Looking Ahead to the Second Half of the Year .......................................................................................................................................................35

Deborah Weinswig, CEO and Founder, Coresight Research

deborahweinswig@fung1937.com US: 917.655.6790 HK: 852.6119.1779 CN: 86.186.1420.3016

2

Copyright © 2018 Coresight Research. All rights reserved.

July 4, 2018

Introduction

Our 2018 Midyear Wrap-Up brings together our coverage of retail events, company developments and our conference

coverage from the first half of 2018. Our team has had a busy first half, attending conferences and investor days in the

US, Europe and Asia, and covering a raft of news events and company updates.

We divide our coverage into three themes:

• Events: Coverage of macro events and retail sector changes.

• Companies: A review of major company announcements and our notes from the various investor days.

• Conferences: Our takeaways from industry conferences that we attended worldwide.

The report concludes with a look ahead to key events coming up in the second half of the year. We hope you find our

coverage of the first half of 2018 informative and interesting. Our coverage of retail and technology continues every

day.

Deborah Weinswig, CEO and Founder, Coresight Research

deborahweinswig@fung1937.com US: 917.655.6790 HK: 852.6119.1779 CN: 86.186.1420.3016

3

Copyright © 2018 Coresight Research. All rights reserved.

July 4, 2018

Deborah Weinswig, CEO and Founder, Coresight Research

deborahweinswig@fung1937.com US: 917.655.6790 HK: 852.6119.1779 CN: 86.186.1420.3016

4

Copyright © 2018 Coresight Research. All rights reserved.

July 4, 2018

1. Events

US Gas Prices Jumped—But Retail Growth Did Not Take a Hit

Traditionally, higher gas prices We have seen something highly unusual in US retail: gas prices have increased at double-digit rates, yet retail sales of

have dented growth in discretionary goods have continued growing solidly. This breaks a longstanding trend of high gas prices denting growth

discretionary retail sales. in discretionary retail sales. In the graph below, we chart the year-over-year percentage increase in gasoline prices

However, so far this year, we versus that for apparel and general merchandise retail sales, with the latter inverted to more clearly show any

have seen a break in this correlation.

correlation.

• As gas-price deflation eased and inflation returned between early 2015 and early 2017, apparel and general

merchandise retail sales growth softened and then turned negative. This negative growth in discretionary

categories lasted until April 2017.

• Unusually, 2018 has seen a divergence from this trend: apparel and general merchandise sales growth has

strengthened, even in months when gas-price inflation has deepened.

Gas prices jumped in September and November 2017, yet growth in retail sales of apparel and general merchandise

spiked, too. The sharp decline recorded for apparel and general merchandise sales in April was driven by Easter falling

earlier in 2018 than in 2017, pulling some discretionary spending forward into March.

Figure 1. Gas Prices (Left Axis) vs. Apparel and General Merchandise Retail Sales (Inverted; Right Axis): YoY % Change

Gas Prices Apparel and General Merchandise Retail Sales (Inverted)

40.0 (4.0)

30.0

(2.0)

20.0

0.0

10.0

0.0 2.0

(10.0)

4.0

(20.0)

6.0

(30.0)

(40.0) 8.0

2014 2015 2016 2017 2018

Apparel and General Merchandise data refer to sales through general merchandise stores, clothing and footwear retailers, furniture stores, electronics

and appliance retailers, sports and leisure goods stores, and office supplies stores.

Source: US Bureau of Labor Statistics/US Census Bureau/Coresight Research

Deborah Weinswig, CEO and Founder, Coresight Research

deborahweinswig@fung1937.com US: 917.655.6790 HK: 852.6119.1779 CN: 86.186.1420.3016

5

Copyright © 2018 Coresight Research. All rights reserved.

July 4, 2018

Higher gas prices are likely to take billions of dollars from US consumers’ wallets this year:

• US consumers spent $274.8 billion on gasoline in 2017, up 11.8% year over year, per the US Bureau of Economic

Analysis.

If we assume a 12.0% increase in • If we assume a 12.0% increase in spending on gas this year, that adds a further $33.0 billion to Americans’ gas bills

spending on gas this year, that for 2018.

adds a further $33.0 billion to

Americans’ gas bills for 2018. • Those extra costs are likely to pressure discretionary spending among some cash-strapped consumers, although

the total remains minor relative to overall consumer spending.

• We estimate that total US consumer spending will reach $14.0 trillion this year, of which $1.4 trillion will be spent

on discretionary goods categories.

We remain bullish on the prospects for US retail in 2018. We estimate that total retail sales excluding automobiles and

gasoline will reach $3.6 trillion this year, up by around 4.4% year over year. Income tax changes, higher wages resulting

from corporate tax changes and solid economic growth are supporting retail spending.

In the first five months of 2018, US retail sales excluding automobiles and gasoline are up by a solid 4.5% year over year.

Figure 2. Total US Retail Sales (ex Automobile Retailers and Gasoline Stations): YoY % Change

7.0

6.5

6.0

5.5 5.3%

5.0

4.5

4.0

3.5

3.0

2.5 Early Easter

2.0

18

7

17

17

8

17

17

18

17

17

18

18

7

t1

r1

v1

c

l

n

ar

ay

p

b

ay

n

g

Ju

Oc

Ap

De

No

Au

Ju

Se

Fe

Ja

M

M

M

Data are not seasonally adjusted.

Source: US Census Bureau/Coresight Research

Deborah Weinswig, CEO and Founder, Coresight Research

deborahweinswig@fung1937.com US: 917.655.6790 HK: 852.6119.1779 CN: 86.186.1420.3016

6

Copyright © 2018 Coresight Research. All rights reserved.

July 4, 2018

US Retail Is On Track for Around 10,000 Store Closures This Year

After last year’s round of store closures, US retail looks on course to be scarred by a second year of nearly

unprecedented closure numbers. As of June 29, we recorded 4,136 announced store closures from major US retailers.

This compares to the 5,341 closures we recorded for the same period in 2017. We have recorded 1,985 announced US

openings store far this year, compared to the 3,267 announced by the same date in 2017.

We estimate that 2018 will We estimate that 2018 will end with 8,000–10,000 US store closures, exceeding the 7,066 we recorded for 2017. Last

end with 8,000–10,000 US year, store closure numbers slowed substantially in the second half of the year.

store closures, exceeding the

7,066 we recorded for 2017. Among the more high-profile events in the first half of 2018 were:

• Canadian retail group Hudson’s Bay Company (HBC) announced plans to close up to 10 Lord & Taylor stores

through 2019. The closures announced on June 5 include the iconic Lord & Taylor flagship store on Fifth Avenue in

Manhattan.

• Toys“R”Us liquidated, resulting in the closure of 881 stores.

• Bon-Ton Stores went bankrupt, impacting 260 stores.

Below, we break down the closures so far in 2018 by sector.

Figure 3. US: Announced Store Closures by Sector, as of June 29, 2018

Grocery, 108

Jewelers, 200 Other,

313

Electronics Stores, 250 Apparel Specialty

Stores, 918

Department Stores and

Toys, 881

Mass Merchandisers, 632

Health and

Beauty, 834

Source: Company reports/Coresight Research

Deborah Weinswig, CEO and Founder, Coresight Research

deborahweinswig@fung1937.com US: 917.655.6790 HK: 852.6119.1779 CN: 86.186.1420.3016

7

Copyright © 2018 Coresight Research. All rights reserved.

July 4, 2018

Figure 4. US: Year-to-Date 2018 Major Store Closure Announcements, as of June 29

Toys“R”Us 881

Walgreens 600

Sears and Kmart [Add latest closures chart; break down by sector]

274

Ascena Retail 267

Bon-Ton 260

Best Buy 250

Signet Jewelers 200

Mattress Firm 200

4,136

GNC 200

Claire’s 132

Foot Locker 110

Total:

The Children’s Place 100 announced store

Southeastern Grocers 94

closures

Aaron Brothers 94

Nine West 71

Gap 70

Walmart 63

Abercrombie & Fitch 60

A’gaci 49

Shoe Carnival 25

Kiko USA 24

Vera Bradley 17

Camping World 13

J.Crew 13

Target 12

Macy’s 11

Vitamin Shoppe 10

JCPenney 8

Land of Nod 6

Kroger 6

Island Pacific 6

Charlotte Olympia 4

Lord & Taylor 3

Safeway 2

Nordstrom 1

0 100 200 300 400 500 600 700 800 900 1,000

Coresight Research has calendarized store openings/closures to attribute them to the year in which they fell or are expected to fall. This involves an estimation for some retailers. These include:

Ascena, Gap, Lord & Taylor, The Children’s Place and Vera Bradley.

Source: Company reports/Coresight Research

Deborah Weinswig, CEO and Founder, Coresight Research

deborahweinswig@fung1937.com US: 917.655.6790 HK: 852.6119.1779 CN: 86.186.1420.3016

8

Copyright © 2018 Coresight Research. All rights reserved.July 4, 2018

The UK Is Seeing a Raft of Store Closures, Too

In the US, the acceleration in store closures began in earnest in 2017. In the UK, closures have taken hold this year. As of

We have recorded 934 June 29, we have recorded 934 announced closures in our week-by-week tracking of UK store closings by major

announced closures in our retailers. This midyear total is already comparable to the 1,005 closures we recorded for 2017 as a whole, suggesting

week-by-week tracking of UK that we could see around double the rate of closures for the full year.

store closings by major

retailers. • Department-store chains Marks & Spencer (M&S), Debenhams and House of Fraser have announced store closures

(or as in the case of M&S, an acceleration of previously stated closure plans); we discuss these department stores

and their strategies in more detail later in this report.

• Bankruptcies at electronics chain Maplin and Toys“R”Us have fueled closures this year.

• However, it is company voluntary arrangements (CVA), which allow retailers to exit selected stores if their

creditors agree, that have stoked the closures total for the year so far. Carpetright, New Look and Mothercare are

among those to have taken the CVA route—as well as the abovementioned House of Fraser.

Figure 5. UK: Year-to-Date 2018 Major Store Closure Announcements, as of June 29

Maplin 219

Poundworld 117

Toys“R”Us 100

Carpetright 92

Dixons Carphone 92

New Look 60

Mothercare 50

East

Original Factory Shop

House of Fraser

34

32

31

Total: 934

Monsoon Accessorize 28 announced store closures

M&S Clothing and Home 20

N Brown 20

Argos 13

French Connection 6

Dunnes Stores 5

Waitrose 5

Tesco 4

Sainsbury’s 3

Debenhams 2

B&M 2

0 50 100 150 200 250

Coresight Research has calendarized store openings/closures to attribute them to the year in which they fell or are expected to fall. This involves an

estimation for some retailers. These include: Argos, B&M, M&S, Monsoon Accessorize, Sainsbury’s and Tesco.

Source: Company reports/Coresight Research

Deborah Weinswig, CEO and Founder, Coresight Research

deborahweinswig@fung1937.com US: 917.655.6790 HK: 852.6119.1779 CN: 86.186.1420.3016

9

Copyright © 2018 Coresight Research. All rights reserved.July 4, 2018

As we noted at the start of this year, these closures are more a mark of undifferentiated—and in a number of cases,

heavily indebted—retailers, rather than underlying weakness in retail.

The popular narrative is that these retailers’ woes are indicative of “bleak” times for an “embattled” retail sector, driven

UK retail sales continue to

by shoppers cutting their spending, but the truth is that UK retail sales continue to grow above inflation and many

grow above inflation and

many retailers are flourishing.

retailers are flourishing. We chart UK retail sales growth below.

Large-store generalists that have traded on unique selling points (USPs) of choice, convenience and proximity have had

those advantages eliminated by e-commerce. Meanwhile, the sizable growth of more targeted retailers—both online

and offline—has attracted customers looking for products and brands that cater to their individual tastes and demands.

The abundance of choice that consumers now enjoy looks set to further fragment spending and suppress margins.

Figure 6. Total UK Retail Sales (ex Automotive Fuel): YoY % Change

7.0

Value Volume

6.0 6.3%

5.0

4.4%

4.0

3.0

2.0

1.0

0.0

(1.0) Early Easter

(2.0)

18

7

17

17

8

17

17

18

17

17

18

18

7

t1

r1

v1

c

l

n

ar

ay

p

b

ay

n

g

Ju

Oc

Ap

De

No

Au

Ju

Se

Fe

Ja

M

M

M

Data are not seasonally adjusted.

Source: Office for National Statistics/Coresight Research

Deborah Weinswig, CEO and Founder, Coresight Research

deborahweinswig@fung1937.com US: 917.655.6790 HK: 852.6119.1779 CN: 86.186.1420.3016

10

Copyright © 2018 Coresight Research. All rights reserved.July 4, 2018

The US-China Tariff War Kicks Off Again

In March, the US-China tariff war kicked off. In June, the dispute escalated, when the US announced new tariffs of 25%

The latest tariffs will take

on $34 billion worth of imports from China. The latest tariffs will take effect on July 6 and will impact 818 product

effect on July 6 and will

impact 818 product categories including industrial machinery, parts of electronic devices, and trains, planes, helicopters and automobiles. In

categories. May, US President Donald Trump specified that new tariffs should apply to $50 billion worth of imports from China that

contain “industrially significant technologies.”

Most consumer products, including apparel and many consumer electronics products, are not on the US Trade

Representative’s list of items subject to new tariffs. The biggest import category facing new tariffs is automobiles.

Some 515 items have been removed from an initial list of 1,333 items under consideration for new tariffs that was

published in early April. A second list of 284 categories comprising $16 billion worth of imports will go out for public

consultation before the US decides whether it will introduce tariffs on those items at a later date. Adding tariffs on that

second list of items would bring the total up to the requested $50 billion in imports subjected to new tariffs.

Following the US’s announcement on June 15, China’s Ministry of Finance responded later in the day by stating that it

would impose tariffs of 25% on 545 categories of imported US products worth $34 billion beginning on July 6. China also

threatened to introduce tariffs on a further $16 billion of US imports. In April, China had indicated that categories of US

imports including soybeans, whiskey and beef would face tariffs.

The First Phase

In early March, President Trump announced tariffs of 25% on steel and 10% on aluminum imported into the US from

China and other countries. In early April, China responded with tariffs of up to 25% across 128 US product categories,

including fruit, pork, steel pipes and ethanol. The US then revealed plans to apply 25% tariffs to 1,333 product

categories imported from China for sale in the US. These included industrial machinery and parts thereof, electronic

components, specialist electronic equipment and medical devices. This plan will be open to a public consultation.

China subsequently announced that it plans to impose tariffs of 25% on $50 billion worth of US exports across 106

categories that include chemicals, cars and soybeans. President Trump said that he had instructed the US Trade

Representative to consider whether additional tariffs on $100 billion worth of imports would be appropriate, and to

identify products on which it could impose those tariffs.

On May 29, President Trump stated that the US Trade Representative would announce by June 15 the imposition of an

additional 25% duty on approximately $50 billion worth of Chinese imports.

Apparel Again Not Directly Impacted

In the US, automobile imports look set to take the greatest hit from the new tariffs, but the bulk of the products to

which the new import charges apply are not the types of goods that consumers typically buy. Clothing and footwear

have again escaped from tariffs, to the benefit of US retailers and consumers. Should apparel be pulled into the trade

Deborah Weinswig, CEO and Founder, Coresight Research

deborahweinswig@fung1937.com US: 917.655.6790 HK: 852.6119.1779 CN: 86.186.1420.3016

11

Copyright © 2018 Coresight Research. All rights reserved.July 4, 2018

war, the impact on consumers would be substantially bigger than what we expect to see from the tariffs that will be

applied to cars.

In 2017, the US imported almost $39 billion of apparel and textiles from China, plus some $14 billion of footwear. In

aggregate, these categories would be bigger than all of those to which tariffs will be applied on July 6.

Figure 7. US: Imports of Apparel and Textiles and Footwear from China

2016 2017

Apparel and Textiles

Value (USD Mil.) $38,517 $38,741

China as % of All Imports 37% 37%

Footwear

Value (USD Mil.) $14,652 $14,020

China as % of All Imports 58% 56%

Source: US Department of Commerce International Trade Administration

Deborah Weinswig, CEO and Founder, Coresight Research

deborahweinswig@fung1937.com US: 917.655.6790 HK: 852.6119.1779 CN: 86.186.1420.3016

12

Copyright © 2018 Coresight Research. All rights reserved.July 4, 2018

Deborah Weinswig, CEO and Founder, Coresight Research

deborahweinswig@fung1937.com US: 917.655.6790 HK: 852.6119.1779 CN: 86.186.1420.3016

13

Copyright © 2018 Coresight Research. All rights reserved.July 4, 2018

2. Companies

Reviewing Partnerships and Investments

So far this year, we have seen Retail-tech partnerships are becoming one of the major themes in retailing in 2018, particularly in North America and

a flurry of tie-ups and Europe. So far this year, we have seen a flurry of tie-ups and investments involving long-standing retailers and tech firms

investments involving long- or platforms. For example, Kroger sealed a deal with Ocado for the latter to build robotic fulfillment centers, Walmart

standing retailers and tech announced it was buying a majority stake in Indian e-commerce marketplace Flipkart and Carrefour announced a deal

firms or platforms. that will let Google Home users buy Carrefour groceries through the device.

Future-Proofing Department Stores

Macy’s + B8ta: In June, Macy’s announced that it had acquired a minority stake in tech retailer B8ta and will partner

with the company to expand the department store’s pop-up concept, The Market @ Macy’s. B8ta operates stores

offering shoppers the opportunity to discover, trial and buy tech products.

Macy’s + STORY: In May, Macy’s announced that it had acquired STORY, a 2,000-square-foot concept store whose

theme changes—from design to merchandise—every 4–8 weeks, with the goal of bringing light to a new theme, trend

or issue. Past STORY themes have included “Work/Space,” “Love,” “Home for the Holidays,” “Beauty,” “Style.Tech” and

“Color.” (Our report.)

Kohl’s + Aldi: In March, US department store retailer Kohl’s announced that it would be slimming down 12 of its stores

and that, as part of a pilot program, 5–10 of those stores would carve out space to house Aldi discount supermarkets.

(Our coverage.)

Online to Offline, and Offline to Online

Carrefour + Google: In June, Carrefour announced a partnership with Google in France to allow consumers to buy from

Carrefour via the Google Home voice assistant and Google’s French shopping site.

Kroger + Ocado: In May, Kroger announced a deal with UK grocery and technology company Ocado to build up to 20

high-tech online grocery fulfillment centers in the US. So far this year, Ocado has announced similar partnerships with

Sobeys in Canada and ICA in Sweden, too.

Walmart + Flipkart: In May, Walmart announced the signing of a definitive agreement to invest $16 billion for a 77%

stake in Flipkart, a leading e-commerce player in India. The company said it supported Flipkart’s ambition to become a

publicly listed subsidiary in the future. (Our flash report.)

Walmart + JD.com: In April, Walmart China extended its supply-chain integration with JD.com to groceries, allowing

consumers within a three-kilometer radius of a new Walmart store in Shenzhen to buy grocery items on JD.com and

have them delivered within 30 minutes.

Deborah Weinswig, CEO and Founder, Coresight Research

deborahweinswig@fung1937.com US: 917.655.6790 HK: 852.6119.1779 CN: 86.186.1420.3016

14

Copyright © 2018 Coresight Research. All rights reserved.July 4, 2018

Walmart + Spatialand: In February, Walmart’s Store No. 8 technology incubator in the US announced that it had

acquired virtual reality (VR) startup Spatialand, with the goal of building and discovering new products and uses of VR to

provide an immersive shopping experience across Walmart’s different websites and stores.

Groupe Casino + Amazon: In March, France’s Groupe Casino announced that its Monoprix banner would make products

available on a dedicated store within the Amazon Prime Now service, in the Paris area.

JD.com + Fung Retailing: In February, JD.com, China’s leading online retailer, announced a partnership with Fung

Retailing, the retail business arm of Hong Kong conglomerate the Fung Group, which has a network of over 3,000 stores.

The two companies will cooperate in using AI to transform the retail lands in areas such as AI platform development and

the application of AI to smart retail. (More.)

Tapping Demand for Healthcare Alternatives

Albertsons + Rite Aid: In February, Albertsons, one of the nation’s largest grocery retailers, and Rite Aid, one of the

nation’s leading drugstore chains, announced a definitive merger agreement under which privately-held Albertsons will

merge with publicly-traded Rite Aid. Current Rite Aid Chairman and CEO John Standley will become CEO of the

combined company, with current Albertsons Chairman and CEO Bob Miller serving as Chairman. (More.)

Amazon + Berkshire Hathaway + JPMorgan Chase: In January, Amazon, Berkshire Hathaway and JPMorgan Chase

announced plans to form a partnership to find ways to address healthcare for their US employees. The goal is to

improve employee satisfaction and reduce costs. The three companies will bring their scale and complementary

expertise to this long-term effort and will pursue their objective through an independent company free of profitmaking

incentives and constraints. (Our flash coverage.)

Looking Ahead

We expect collaborations to We expect to see more collaborations between retailers and technology firms in 2018 and into 2019. And we expect

be sustained by certain tech these to be sustained by certain tech firms’ status as gatekeepers that hold the keys to valuable channels or markets.

firms’ status as gatekeepers

that hold the keys to valuable • Voice commerce: In the emerging voice commerce channel, tech giants Amazon and Google control many of the

channels or markets. devices and channels through which shoppers engage with retailers. That means that retailers wanting to offer

shoppers the opportunity to buy through Amazon Echo or Google Home devices are forced into partnering with

these tech firms, which may be competitors in other contexts.

• E-commerce in high-growth markets: The dominance of certain e-commerce platforms in high-growth markets

such as India and China will continue to prompt Western retailers to collaborate with those firms in pursuit of

growth in those markets. We expect firms such as Alibaba and JD.com in China and Flipkart, Snapdeal and

Bigbasket in India to remain gatekeepers of the retail markets in those countries.

Deborah Weinswig, CEO and Founder, Coresight Research

deborahweinswig@fung1937.com US: 917.655.6790 HK: 852.6119.1779 CN: 86.186.1420.3016

15

Copyright © 2018 Coresight Research. All rights reserved.July 4, 2018

Hearing About Target’s Plans for 2018 and 2019

In March, the Coresight Research team attended the 2018 Target Financial Community Meeting in Minneapolis.

Takeaways distilled from remarks by CEO Brian Cornell, COO John Mulligan and CFO Cathy Smith follow.

A $7 Billion-Plus Investment Program to Drive Growth

This investment aims to:

• Blend physical and digital stores.

• Reimagine Target stores.

• Open more new, small-format stores.

• Create digital capabilities.

• Launch great brands.

A Focus on Newness and Innovation to Improve the Digital Experience

In improving the digital experience, Target noted the following achievements:

• It fulfilled two-thirds of digital orders in its stores this past holiday season.

• It offers an order pickup/returns/exchanges desk.

• The retailer combined its Cartwheel and Target apps.

• It introduced a Target Wallet to expedite payment.

Target is enhancing the • It is enhancing the experience by adding a 360-degree visualization function, investing in AR, elevating storytelling

experience by adding a 360- and extending its assortment.

degree visualization function,

investing in augmented reality Investing in Its Team Through Training, Tools, Advancement Opportunities and Pay Raises

(AR), elevating storytelling Target is offering advancement opportunities and improved training to its sales associates, and providing them with

and extending its assortment. better tools, such as handheld devices for use on the store floor. In addition, the company raised the starting wage to

$12 per hour for certain employees this spring, after having raised the rate to $11 per hour in October 2017, and with

the goal of reaching $15 per hour in 2020. Target is also staffing its stores with subject-matter experts rather than with

generalists.

Plans to Renovate and Open more than 1,000 Stores by 2020

In reimagining its stores, Target is aiming for ease and inspiration, style and essentials, and mass and specialty. Target

refurbished 110 stores in 2017 and plans to refurbish 325 stores in 2018, with a goal of renovating and opening more

than 1,000 stores by 2020. In addition, Target plans to open 30 new-format stores in 2018.

Deborah Weinswig, CEO and Founder, Coresight Research

deborahweinswig@fung1937.com US: 917.655.6790 HK: 852.6119.1779 CN: 86.186.1420.3016

16

Copyright © 2018 Coresight Research. All rights reserved.July 4, 2018

Offers a Variety of Pickup and Delivery Options, Including Grand Junction, Drive Up and Shipt

Grand Junction: Grand Junction offers a software platform that retailers, distributors and third-party logistics providers

can use to manage local deliveries through a network of more than 700 carriers. The company offers same-day delivery

in Boston, Chicago, San Francisco and Washington, DC. The company has expanded delivery to all five boroughs of

Manhattan.

Drive Up: Target is expanding its Drive Up collection service to nearly 1,000 locations in the continental US.

Target aims to offer same-day Shipt: Target aims to offer same-day shipping in every major market by the holidays this year.

shipping in every major

market by the holidays this An Updating of Its Private-Label Brands in Apparel

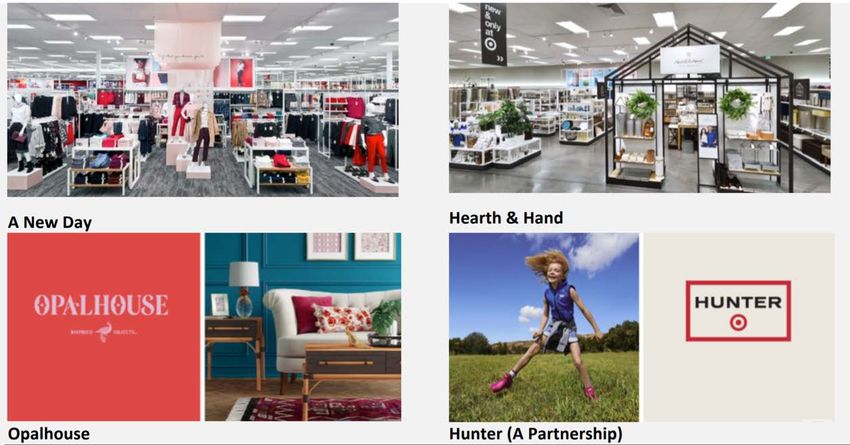

year. In 2017, Target committed to launching 12 new brands in 18 months. Below is a selection of the new logos.

Source: Company reports

Deborah Weinswig, CEO and Founder, Coresight Research

deborahweinswig@fung1937.com US: 917.655.6790 HK: 852.6119.1779 CN: 86.186.1420.3016

17

Copyright © 2018 Coresight Research. All rights reserved.July 4, 2018

Capital Expenditures Plans of $3.5 Billion in 2018

To drive long-term profitable growth in 2019 and beyond, Target is investing $3.5 billion as follows:

• Tripling the number of store remodels.

• Opening 30 more small-format stores.

• Expanding digital fulfillment options.

• Shipping more orders from stores.

• Investing in its supply chain.

• Introducing more new brands.

• Balancing everyday prices and promotions.

Deborah Weinswig, CEO and Founder, Coresight Research

deborahweinswig@fung1937.com US: 917.655.6790 HK: 852.6119.1779 CN: 86.186.1420.3016

18

Copyright © 2018 Coresight Research. All rights reserved.July 4, 2018

In Europe, Zalando Is “On Track” to Double Sales by 2020

In June, the Coresight Research team attended Zalando’s Capital Markets Day 2018 in Berlin. The day was bookended by

management presentations that reviewed the outlook for Zalando. In his introductory presentation, Co-CEO Rubin Ritter

noted the following prospects for Zalando:

• Doubling revenues: Ritter underscored Zalando’s ambitions to double sales, as measured by gross merchandise

volume (GMV), between 2017 and 2020. “The message of today is that we are on track and want to reiterate our

trajectory,” he said. Ritter does not see the retailer “hitting the ceiling anytime soon.” The company needs to add

€1.5 billion ($1.75 billion) in sales each year to achieve this goal, and will continue to invest for growth, meaning

that margins will not expand in a meaningful way in the next few years.

Localized merchandising, better • Convenience levers: Localized merchandising, better digital experiences and greater convenience will support

digital experiences and greater Zalando’s growth, Ritter said. Speaking about the company’s digital operations, he noted that mobile devices now

convenience will support account for 80% of the site’s traffic and 60% of transactions. When discussing convenience, he pointed to

Zalando’s growth. Zalando’s ambitions to be able to reach 25% of the European population with same-day delivery, 80% with next-

day delivery and 95% with two-day delivery by 2020.

• Gaining share of wallet: Zalando’s average active customer spends 25% of his or her fashion budget at Zalando.

This high share is primarily driven by frequency, and Ritter noted that active shoppers are placing more orders

than they used to. He also said that newer cohorts of consumers—those who have started shopping on the site

more recently—contribute disproportionately to revenues.

Birgit Haderer, SVP of Finance and Indirect Procurement, concluded the day by outlining the company’s financial

perspective:

• Revenue growth: Zalando continues to aim for 20%–25% top-line growth through 2020. It is currently the fifth-

biggest fashion player in Europe and could become the third biggest, after Inditex and H&M, in the next three

years, Haderer said, noting that Zalando is already the biggest multibrand fashion retailer in Europe.

• Little margin expansion: Haderer noted that the company had analyzed the margin development of tech

companies after they had gone public and found that those firms generally went from high revenue growth at a

lower margin, to strong growth and solid profitability, to slower revenue growth at a stronger margin. Zalando is in

the second of those three phases, Haderer remarked: the company expects to see strong growth and solid

profitability in the coming years.

• Gross margins: Haderer noted that positive gross-margin drivers include increased negotiating leverage with

brands, pricing algorithms and the company’s Partner Program, which is its marketplace operation for brands.

Factors that negatively impact gross margin include lower price points (Zalando has built out its offering in lower-

price fashion, including fast fashion); discounting, as Zalando “wants to be in line with the market” on price; and

growth in revenues from the lower-margin Rest of Europe region.

Read more takeaways from the Capital Markets Day in our flash report.

Deborah Weinswig, CEO and Founder, Coresight Research

deborahweinswig@fung1937.com US: 917.655.6790 HK: 852.6119.1779 CN: 86.186.1420.3016

19

Copyright © 2018 Coresight Research. All rights reserved.July 4, 2018

UK Department Store Retailers Plan a Slew of Closures

The UK department-store sector has seen a raft of store-closure announcements as embattled mid-market players look

to reduce their store counts in the face of underlying sales declines.

• M&S: On May 22, M&S announced plans to accelerate its closure program, which involves shuttering more than

100 of its Clothing and Home stores by 2022. This includes 21 that have already closed and 14 earmarked for

closure in the current fiscal year.

On June 6, privately-owned • House of Fraser: On June 6, privately-owned House of Fraser announced plans for a CVA that proposes 31 store

House of Fraser announced closures—more than half of its current 59 stores in the UK and Ireland.

plans for a company voluntary

arrangement (CVA) that • Debenhams: The retailer closed two stores in January and is reviewing a further eight for closure. At its interim

proposes 31 store closures. results in March, the company stated that these 10 stores “could become unprofitable over time.” Debenhams

opened one new UK store in January, and plans one UK opening in early FY19, which ends in August 2019.

• Debenhams also plans to rightsize a number of its stores, and at its latest results, stated that it is in discussion with

landlords and sees opportunities for at least 30 stores to be slimmed down.

Figure 8. Selected UK Department Stores: Planned Store Closures

Retailer Planned Store Closures

M&S Clothing and Home More than 100

House of Fraser 31

Debenhams Up to 10

Source: Company reports

Dwindling comparable sales is a hallmark of each of these three retailers. On June 19, Debenhams issued its third profit

warning of 2018, as comparable sales slid a further 1.7% in the 15 weeks ended June 16.

The reasons for the declining demand are the same in the UK as in other markets such as the US:

• Consumers have more choice of retailers than ever before and they are increasingly opting for specialized retailers

that resonate with their lifestyle or identity.

• E-commerce has stolen department stores’ competitive advantage of choice and convenience.

Deborah Weinswig, CEO and Founder, Coresight Research

deborahweinswig@fung1937.com US: 917.655.6790 HK: 852.6119.1779 CN: 86.186.1420.3016

20

Copyright © 2018 Coresight Research. All rights reserved.July 4, 2018

New Strategies

M&S

In November 2017, M&S announced a new five-year transformation plan designed to “make M&S special again.” This

includes focusing on becoming “the UK’s essential clothing retailer,” accelerating the company’s UK Clothing and Home

space rationalization plan, repositioning its food business and becoming a digital-first business.

Debenhams

Debenhams’ strategy, announced in April 2017, includes becoming a destination for “social shopping,” being digital-

driven and taking a new approach to its own brands.

House of Fraser

Store closures form the bulk of House of Fraser’s plan to turnaround its fortunes, although the company’s CVA

presentation notes three prongs to its strategy:

• Create a smaller, higher-quality and more-focused store estate: It plans to close 31 of its 59 stores.

• Refocus towards concessions and own-bought brands to reaffirm its premium position: “We are and will be the

house of brands,” said CEO Alex Williamson. This implies a move away from private labels, reversing recent

attempts to grow private label’s share of sales.

• Become an e-commerce-led retailer offering a seamless multichannel proposition.

The proposed transformation plan will see Chinese firm C.banner, the owner of toy retailer Hamley’s, become a 51%

shareholder, taking majority ownership from Chinese peer Sanpower. Management has pledged that £70 million ($92

million) of new money will be made available to fund the transformation plan, working capital and general corporate

purposes, and the company states that the cash flow benefit from the CVA will fully fund the business during the

transformation period.

As presented thus far, we feel As presented thus far, we feel that House of Fraser’s plan continues to lack a convincing, overarching strategy to

that House of Fraser’s plan transform the offering of the kind being implemented at M&S and Debenhams. While we believe that management is

continues to lack a convincing, right to reaffirm the retailer’s position at the top end of the mid-market and pull back from a focus on private label that

overarching strategy to was unsuited to its proposition, we think the new plan does not answer a key question: in a world of e-commerce, what

transform the offering of the happens to retailers who simply focus on selling other companies’ brands?

kind being implemented at

M&S and Debenhams.

Deborah Weinswig, CEO and Founder, Coresight Research

deborahweinswig@fung1937.com US: 917.655.6790 HK: 852.6119.1779 CN: 86.186.1420.3016

21

Copyright © 2018 Coresight Research. All rights reserved.July 4, 2018

Figure 9. House of Fraser’s Planned Evolution

Source: Company reports

Deborah Weinswig, CEO and Founder, Coresight Research

deborahweinswig@fung1937.com US: 917.655.6790 HK: 852.6119.1779 CN: 86.186.1420.3016

22

Copyright © 2018 Coresight Research. All rights reserved.July 4, 2018

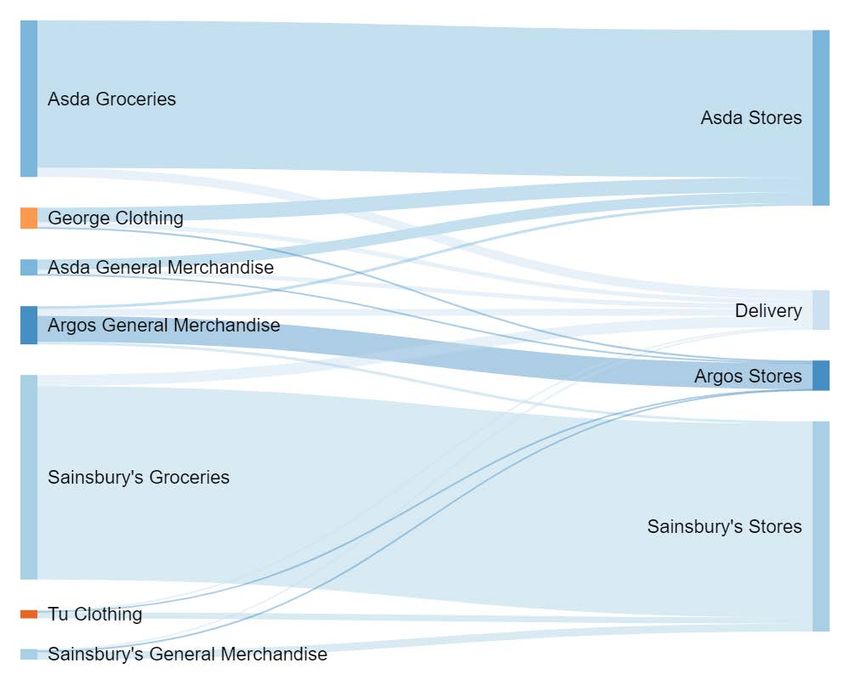

Sainsbury’s-Asda Merger Could Create the UK’s “Amazon Crusher”

In April, two of the UK’s biggest grocery retailers, Sainsbury’s and Walmart-owned Asda, announced plans to merge. The

The combination of combination will create the UK’s biggest grocery retailer, with total revenues of £51.0 billion ($67.3 billion). We think

Sainsbury’s and Asda will

that it will also create the UK’s biggest retailer of nonfood categories.

create the UK’s biggest

grocery retailer. We think that The new company will span online and offline grocery, two strong clothing brands and a large general merchandise

it will also create the UK’s operation. It will offer fulfillment across a number of banners and store formats, as well as home delivery that includes

biggest retailer of nonfood traditional delivery options and rapid delivery in grocery and general merchandise. In short, it will be the closest thing to

categories. an “Amazon crusher” that we are likely to see in UK retail—and it could serve as a template for retailers in other

countries as they battle Amazon for market share.

Figure 10. The Potential Sainsbury’s-Asda Network of Brands and Fulfillment

Source: Coresight Research

Deborah Weinswig, CEO and Founder, Coresight Research

deborahweinswig@fung1937.com US: 917.655.6790 HK: 852.6119.1779 CN: 86.186.1420.3016

23

Copyright © 2018 Coresight Research. All rights reserved.July 4, 2018

Creating the UK’s Top Nonfood Retailer and, Potentially, Its Biggest Apparel Retailer

The merger could make Sainsbury’s-Asda the UK’s top apparel retailer. We estimate that the new company would have

annual apparel and footwear sales of over £3 billion ($4 billion), setting up a rivalry with M&S for the title of the UK’s

leading clothing and footwear retailer. M&S saw apparel-only sales of around £3.2 billion ($4.2 billion) last year, we

We estimate that the new estimate, and those sales are declining.

combined entity would see

total sales of around £9–£10 We estimate that the new combined entity would see total sales of around £9–£10 billion ($12–$13 billion) across

billion across apparel and apparel and general merchandise, making it the UK’s biggest nonfood retailer. That would put it ahead of Amazon UK,

general merchandise, making which booked revenues of £8.8 billion ($11.6 billion) last year, although its GMV including marketplace sales will have

it the UK’s biggest nonfood been greater than this.

retailer.

In nonfood categories, the Sainsbury’s-Asda combination will bring together the following:

• The variety store Argos, which was acquired by Sainsbury’s in 2016, and which sells around £4.1 billion ($5.4

billion) of general merchandise per year.

• Asda’s highly successful George apparel brand, which is believed to generate sales of above £2 billion ($2.6 billion)

per year (we estimate that George sales totaled about £2.2 billion, equivalent to $2.9 billion, in 2017).

• Sainsbury’s newer but high-growth Tu clothing brand, which we estimate saw net sales of around £840 million

($1.1 billion) last year.

• Asda’s and Sainsbury’s own general merchandise sales, which we think are likely to total approximately £2–£3

billion ($3–$4 billion) per year.

An Omnichannel Leader

The new company will lead in its range of fulfillment options, too. Argos has been an omnichannel leader for many

years, having pioneered the concept of reserve online, pick up in store in the UK, and having rolled out same-day

delivery in 2015. Sainsbury’s and Asda each have mature online grocery operations, and Sainsbury’s also has a nascent

one-hour delivery service called Chop Chop. In addition, Sainsbury’s has a large network of convenience stores that it

could use as local collection points.

Sainsbury’s has already installed Argos shops-in-shops and collection points in its stores; management noted that there

is an opportunity to bring Argos into Asda stores, too. We think that the breadth and depth of the combined company’s

offering will make it the market leader in terms of “anytime, anywhere” shopping.

At the companies’ press conference, Walmart International CEO Judith McKenna said that Walmart is considering

deploying Argos in the US and elsewhere, further suggesting that this mix of offerings could be one way for retailers in

many markets to fight the growth of Amazon.

Deborah Weinswig, CEO and Founder, Coresight Research

deborahweinswig@fung1937.com US: 917.655.6790 HK: 852.6119.1779 CN: 86.186.1420.3016

24

Copyright © 2018 Coresight Research. All rights reserved.July 4, 2018

Management Arrivals and Departures

US

Macy’s: On May 23, Macy’s announced the appointment of Paula A. Price as CFO, effective July 9. Price will be

responsible for leading the company’s finance, accounting, investor relations and internal audit functions. Price will

succeed Karen Hoguet who had previously announced plans to retire at the end of the 2018 fiscal year.

On May 22, JCPenney JCPenney: On May 22, JCPenney announced the resignation of its Chairman and CEO Marvin R. Ellison, who moved to

announced the resignation of home-improvement retailer Lowe’s to take on the role of President and CEO, effective July 2. JCPenney has created an

its Chairman and CEO Marvin Office of the CEO that will take responsibility for the company’s day-to-day operations until a new CEO is appointed.

R. Ellison.

Jet.com: On March 26, Walmart-owned Jet.com announced that it had appointed Simon Belsham as President. He

succeeded Liza Landsman, who had previously announced plans to leave Jet.com. Belsham was CEO of British Internet

pure-play NotOnTheHighStreet.com from 2015 to 2017. Prior to that, he was Managing Director of Grocery Online at UK

grocery market leader Tesco for two years.

Gap: On February 20, Gap announced that Jeff Kirwan, President and CEO of the Gap brand, would leave the company.

In the interim, Brent Hyder, current EVP of Global Talent and Sustainability for Gap Inc., will oversee the brand. Hyder

previously served as COO of the Gap brand and as VP and General Manager of Gap Japan, leading all aspects of the

business in Japan. Kirwan had served as President and CEO of the Gap brand since December 2014. He joined the

company in April 2007 and previously held various roles at Gap China, Old Navy and Old Navy Canada.

Deborah Weinswig, CEO and Founder, Coresight Research

deborahweinswig@fung1937.com US: 917.655.6790 HK: 852.6119.1779 CN: 86.186.1420.3016

25

Copyright © 2018 Coresight Research. All rights reserved.July 4, 2018

Deborah Weinswig, CEO and Founder, Coresight Research

deborahweinswig@fung1937.com US: 917.655.6790 HK: 852.6119.1779 CN: 86.186.1420.3016

26

Copyright © 2018 Coresight Research. All rights reserved.July 4, 2018

3. Conferences

Hearing About New Retail at World Retail Congress 2018

In April, the Coresight Research team attended World Retail Congress 2018 in Madrid. Among those talking about New

Retail were senior management from Chinese e-commerce giants JD.com and Alibaba Group.

JD.com has opened a new JD.com: Richard Liu, Founder, Chairman and CEO of JD.com, observed that European retail tends to change more slowly

supermarket format and plans than Chinese retail. Liu noted that JD.com is trying brick-and-mortar formats. The company has opened a new

to put convenience stores in supermarket format and plans to put convenience stores in many Chinese villages. Despite this push into “old” retail

many Chinese villages. formats, Liu predicted that, sooner or later, the retail industry will be operated by AI and robots, rather than by humans.

Alibaba: Jet Jing, President of Alibaba Group’s Tmall, highlighted the appeal of Tmall and its sister site Tmall Global for

Western brands and retailers seeking to capture a share of the high-growth Chinese market. Jing refers to Tmall as the

“gateway to China” and believes that Western retailers do not have to put up with just surviving with Amazon, because

they can thrive with Tmall. Some 18,000 international brands have sold on Tmall in the past few years. However, Jing

pointed to the need for brands to adapt to Chinese demands, and especially the need for them to undertake rapid

product innovation; brands that do not innovate in China will die, he said. He noted that consumer packaged goods

(CPG) giant Procter & Gamble used big data analytics to identify consumer trends in China and then rapidly tested

dozens of new products by listing them on Tmall.

Third-Generation Retail

The “intergeneration rotation” in retail is creating a third generation characterized by “retail as a service,” according to

Dan O’Connor, Founder and CEO of RetailNet Group and Fellow at the Advanced Leadership Initiative at Harvard

University, who spoke on the third day of World Retail Congress 2018.

O’Connor noted that third-generation retail is characterized by the prominence of marketplace and intermediary firms

such as Alibaba, Amazon, WeChat, Facebook, Snapchat, Delivery Hero and Google, as well as by social media

influencers. This new structure of retail is changing the supply chain by shifting where consumers go for information and

how they connect with products and recommendations.

Other takeaways from O’Connor’s presentation include:

• Firms such as Alibaba are driving the unification of the third-generation retail landscape, as they consolidate

various types of retail and retail-adjacent services.

• This unification is also seen in mobile apps from firms such as Tencent, which is replacing stand-alone apps with

Mini Programs embedded in its WeChat app.

• Retail is moving from store-based retailers with technology to tech firms with some stores.

• We are seeing the emergence of retail as a service, spanning automation, platform services and intermediary

service providers. Tech giants such as Alibaba are driving this by collaborating with brick-and-mortar store brands.

Readers can find reports on day one, day two and day three of World Retail Congress 2018 on our website.

Deborah Weinswig, CEO and Founder, Coresight Research

deborahweinswig@fung1937.com US: 917.655.6790 HK: 852.6119.1779 CN: 86.186.1420.3016

27

Copyright © 2018 Coresight Research. All rights reserved.July 4, 2018

Our Notes from Shoptalk 2018

In March, the Coresight Research team attended and participated in the Shoptalk 2018 conference in Las Vegas. The

event is described as the world’s largest conference devoted to retail and e-commerce innovation. Below, we

summarize our top takeaways.

Retailers Are Providing New Automated Checkout Services that Enable Self-Scanning and Payment by Mobile App or

Facial Recognition

Many retailers are now The ubiquity of mobile devices is driving significant change in how consumers pay for products and services, and many

providing automated, retailers are now providing automated, cashierless checkout services that allow self-scanning and payment by mobile

cashierless checkout services app or facial recognition.

that allow self-scanning and

payment by mobile app or Macy’s: CEO Jeff Gennette announced that Macy’s will roll out mobile checkout in full-line stores by the end of 2018.

facial recognition. The checkout platform will allow shoppers to scan bar codes on items with their phones as they add merchandise to

their baskets.

AR, VR and Product Visualization Are Set to Transform Fashion and Retail

AR is moving into the mainstream, with apparel, beauty, home décor and furniture brands increasingly using the

technology to provide immersive experiences. Meanwhile, VR use cases are quickly materializing in retail, and many

involve retail store simulation for internal planning purposes rather than immersive experiences for consumers. Digital

product visualization technology is also advancing, enabling shoppers to see 3D images of products from different angles

and with various features.

Macy’s: Macy’s revealed plans to offer VR experiences in the furniture departments of 50 stores by this summer.

Target, Amazon and Walmart Are Innovating in Fulfillment and Logistics

Executives from Target and Walmart discussed a variety of fulfillment services designed to speed up the delivery cycle,

ranging from delivery by employees to discount-driven in-store pickup.

Target: CEO Brian Cornell announced that Target plans to become the first traditional retailer to offer same-day delivery

nationwide.

Walmart: Walmart plans to add 500 FedEx Office outlets in selected Walmart stores over the next two years. Consumers

will have the option of having packages shipped to a Walmart-based FedEx Office, where they will be held for five

business days.

Deborah Weinswig, CEO and Founder, Coresight Research

deborahweinswig@fung1937.com US: 917.655.6790 HK: 852.6119.1779 CN: 86.186.1420.3016

28

Copyright © 2018 Coresight Research. All rights reserved.July 4, 2018

Shoppers Are Embracing Products and Brands that Reflect Their Unique Preferences and Values, Contributing to the

Growth of DTC and Niche Brands

Today’s shoppers are embracing products and brands that reflect their unique preferences and values. Traditional

retailers have taken notice of this trend, and many are partnering with or acquiring direct-to-consumer (DTC) and niche

brands in response.

Allbirds: Joey Zwillinger, Cofounder and Co-CEO of shoemaker Allbirds, discussed how the company has established

itself by appealing to shoppers’ desire for products that are made sustainably and are therefore better for the

environment.

Glossier: Emily Weiss, Founder and CEO of beauty company Glossier, argued that, for a digitally native brand, just being

a part of the conversation is not enough: creating a platform for connections is key. Glossier allows customers to

connect to share recommendations, dislikes and skincare routines, all while building a community and the brand’s

image.

Walmart: Marc Lore, President and CEO of Walmart eCommerce US, said that Walmart will continue to consider brand

acquisitions in order to differentiate its online offering and attract millennial shoppers.

Data Is the New Currency

Data was central to nearly all Data was central to nearly all discussions at Shoptalk, whether the session topic was focused on personalization,

discussions at Shoptalk, partnerships, omnichannel retail or loyalty.

whether the session topic was

focused on personalization,

Google: “Data is the backbone of retail,” said Daniel Alegre, Google’s President of Retail and Shopping. Alegre

partnerships, omnichannel announced a new feature, Shopping Actions, which allows users to purchase items directly from search results and

retail or loyalty. across Google platforms. According to Alegre, Google started the new program after observing that although mobile

searches asking where to buy products had risen by 85% over the past two years, most shoppers still ended up buying

on Amazon.

New Retail from China Is Putting the Fun Back in Retail and Represents the Next Generation of Consumer Experiences

In a Shoptalk session titled “Overview of Retail and E-Commerce Innovation in China,” Coresight Research CEO and

Founder Deborah Weinswig noted that China is leading the world in terms of retail comp sales. She also discussed how

Alibaba’s New Retail model, in which acquisitions play a key role, is being embraced by US retailers, many of which are

making their own acquisitions or expanding from online-only operations into offline operations. Personalization and

customization will continue to trend in China, Weinswig said, with key opinion leaders (KOLs) and influencers leading the

market via livestreaming. New inspirations for retail include the deployment of AI, VR, facial recognition and automated

stores such as BingoBox and Tao Cafe in China.

Readers can find reports on day one, day two, day three and day four of Shoptalk 2018 on our website.

Deborah Weinswig, CEO and Founder, Coresight Research

deborahweinswig@fung1937.com US: 917.655.6790 HK: 852.6119.1779 CN: 86.186.1420.3016

29

Copyright © 2018 Coresight Research. All rights reserved.You can also read