KDP ASSET MANAGEMENT, INC - High Yield Bond and Senior Secured Bank Loan Outlook

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

KDP ASSET MANAGEMENT, INC.

High Yield Bond and Senior Secured Bank Loan Outlook

November 2021

KDP Asset Management, Inc.⬧ 24 Elm Street ⬧ Montpelier, Vermont ⬧ 802.223.0440 ⬧ HighYield@kdpam.com

High Yield Observations

Fundament

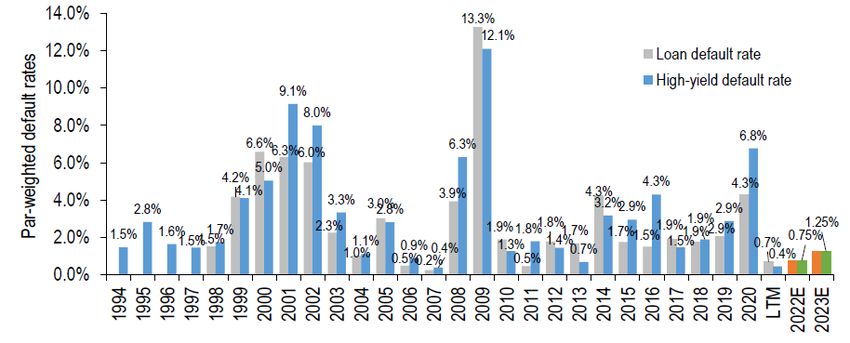

• The Moody’s global speculative grade issuer default rate fell to 2.3% in October down from 2.6% in September. The default rate has

declined for 10 consecutive months since its cyclical peak of 6.8% at year-end 2020. It is projected to stabilized at 1.7% by December

2022.

• Near-term maturities remain low given the magnitude of recent refinancings taking advantage of low interest rates and the technical tailwind

provided by the Fed's financial initiatives.

• EBITDA for most HY companies in 2020 fell precipitously due to Covid-19 but has rebounded significantly in 2021 on higher earnings.

• Leverage levels declining as EBITDA improves and companies start to retire borrowings used to shore up liquidity in 2020.

Technicals

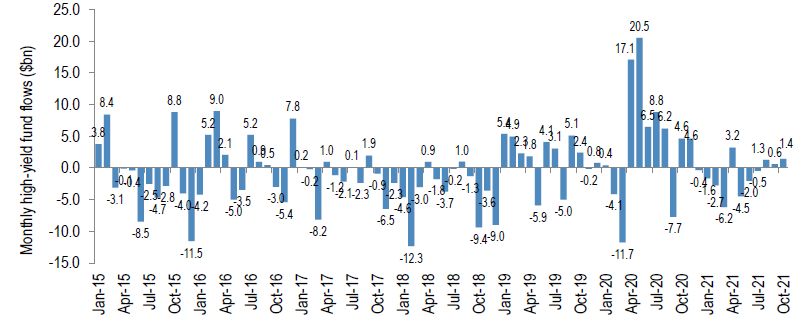

• HY weekly fund flows were positive for the 3rd month in a row in October at +1.4B, down from a robust +2.0B in September.

• The HY market posted a negative -0.18% return in October after a modest +0.03% return in September.

• October’s negative performance reflected a sharp rise in Treasury yields through the first three weeks of the month and despite positive

earnings, light issuance and solid retail flows.

• The best industry performers during October were Publishing with a +1.75% return, Airlines +0.49% and Energy +0.47%. Laggards were

Broadcasting -1.29% and Restaurants -1.01%.

• October’s performance by rating reflected some risk aversion. CCCs posted a -0.37% return, BBs -0.16% and Bs -0.15%.

• Primary market issuance dropped to $30.0B in October from $48.2B in September.

• Issuance proceeds since April 2020 have been primarily destined for enhancing liquidity and refinancing, though there has been a

significant uptick in M&A activity.

Valuations

• Credit quality has been improving reflecting positive impacts of stimulus programs and ongoing COVID vaccine rollout.

• HY spreads could be volatile given higher interest rate concerns due to increasing reflation as economy improves.

• Given still low Treasury yields, higher-quality carry remains at attractive relative levels on a risk/reward basis.

• Risk/reward for CCCs will continue to be volatile as yields tighten further.

Macro

• High yield returns will remain susceptible to an increasing interest rate outlook and success of COVID vaccine rollout.

• KDP believes that higher-quality credits will continue to offer attractive risk/return opportunities compared to other fixed income classes

given their:

• Significant spread advantages

• Relative shorter duration

• Lower correlation when interest rates rise

• KDP reiterates and maintains its up-in-quality preference.

2The Case for High Yield

Fundamentals: High Leverage Drops to 6-Year Lows on Technicals: HY Extends Modest Positive Flows for

Improving Earnings and Lower Need For Increased Liquidity 3rd Consecutive Month, Erasing Some of 2021 HY

Outflows

Source: Morgan Stanley, US Corporate Credit Strategy Chartbook, 11/1/2021 Source: J.P Morgan, High Yield Bond and Leveraged Loan Monitor, 11/1/2021

Macro: Default Rates Forecast to Remain Near Historical Lows Valuation: Higher Quality HY Spreads Remained

for Foreseeable Future Largely Constant in September as the 10-Year Treasury

Yield Rose +7bp

Source J.P.Morgan, Default Monitor, 11/1/2021 Source: Barclays, US High Yield Corporate Update, 11/1/2021

3Senior Secured Bank Loan Observations

Fundamentals

• The par weighted default rate for leveraged loans dropped again in October coming in at 0.51% compared with 0.71% in September with.

October’s loan default rate reflected a 25-month low.

• Loans have seen a reduction in distressed names lately given increased market liquidity and improving economic outlook, which is

indicative of a declining pace of defaults going forward.

• No near-term maturity concerns reflect recent record levels of refinancing/repricing.

• Overall, the leverage spike in 2020 that was due to the take down of debt as companies sought to raise cash to enhance liquidity and

maturity runways is declining.

• Interest coverage levels which fell reflecting extreme Covid economic pressures during 2020 have begun to rebound as earnings improve

Technicals

• Leveraged loans posted a +0.24% return in October down from +0.69% in September.

• October’s performance reflected solid retail inflows and record monthly CLO issuance outweighing a decade’s high monthly loan

issuance. While Leveraged Loans’ performance moderated from earlier months, Loans soundly outperformed HY Bonds that posted a

negative -0.18% monthly return.

• Lower-rated loans underperformed in October braking with recent trends. B-rated loans posted a +0.29% return, BBs +0.19%. And Split

B/CCCs -0.27%.

• During October, loans were led by Metals/Mining +0.92%, Utility +0.72% and Transportation +0.66%.

• Weekly loan retail fund flows were +$2.8B in October compared with +$2.9B in September.

• Gross loan issuance was +$77.2B in October up from $54.4B in September. Gross loan issuance YTD through October amounted to

$730.9B, up 106% year-over-year.

Valuations

• The average loan price was 98.71 at the end of October down -7bp from 98.78 at the end of September.

• The spread to the 3-year takeout tightened -5bp to 409bp.

• At the end of October, the yield to the 3-year takeout rose +26bp to 5.03% due to a spike in the forward curve.

• Typically, loan volatility tends to be significantly lower when compared to HY bonds as loans are higher in the cap structure, have higher

recovery levels, and float with LIBOR rates.

Macro

• Loans, due to their negative convexity and short duration, provide one of the most compelling asset classes in 2021.

• Highly liquid quality loans trading around par offer an attractive carry trade while providing upside when interest rates rise.

• High quality secured, floating-rate bank loans are compelling given the attractive risk/reward adjusted returns, and portfolio diversification

benefits.

• The floating-rate nature of bank loans traditionally provide a natural hedge to interest rates, low duration risk, and have low correlation to

other asset classes.

• Retail inflows are likely to remain strong in 2021 with interest rates expected to rise reflecting inflationary pressures due to supply

disruptions as well as labor tightness.

• CLOs should continue to be active going forward as CLO AAA spreads track IG spreads tighter, increasing technical tailwinds for

leveraged bank loans.

4The Case for Senior Secured Bank Loans

Fundamentals: Loan Continues to Decline Significantly in 3Q as Technicals: Loans Extend Monthly Inflows to 10

Economy/Earnings Improve and Need For Additional Liquidity Months Running

Diminishes

Source: Morgan Stanley, US Corporate Credit Strategy Chartbook, 11/1/2021 Source Credit Suisse, CS Credit Strategy Daily Comment, 11/3/2021

Macro: Default Rates Forecast to Remain Near Historical Lows Valuation: Higher Quality Spreads Stay Stable and

for Foreseeable Future Forecast to Remain So Remainder of 2021

Source J.P.Morgan, Default Monitor, 11/1/2021 Source: J.P Morgan, High Yield Bond and Leveraged Loan Monitor, 11/1/2021

5This is an analytical piece and the asset classes discussed herein, and any other materials provided to you, are intended only for

discussion purposes and are not intended as an offer or solicitation of an offer with respect to the purchase or sale of any

security and should not be relied upon by you in evaluating the merits of investing in any securities. These materials are not

intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use is contrary

to local law or regulation. Past performance is not indicative of future results. The asset classes discussed herein should not

be perceived as investment recommendations. It should not be assumed that investments in any asset class discussed was or

will prove profitable. The views expressed herein represent the opinions of KDP Asset Management, Inc. and its affiliates and

are not intended as a forecast or guarantee of future results. This material may not be reproduced or used in any form or

medium without express written permission. Additional information on KDP, including fee schedules can be found in Form ADV

Part II which is available upon request.

6You can also read