LNG Market Fundamentals - October 2019

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

LNG Market Fundamentals October 2019

Cautionary statements

Forward-looking statements

The information in this presentation includes “forward-looking statements” within the meaning of The forward-looking statements made in or in connection with this presentation speak only as of the

Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange date hereof. Although we may from time to time voluntarily update our prior forward-looking

Act of 1934, as amended. All statements other than statements of historical fact are forward-looking statements, we disclaim any commitment to do so except as required by securities laws.

statements. The words “anticipate,” “assume,” “believe,” “budget,” “estimate,” “expect,”

“forecast,” “initial,” “intend,” “may,” “plan,” “potential,” “project,” “should,” “will,” “would,” and

similar expressions are intended to identify forward-looking statements. The forward-looking

statements in this presentation relate to, among other things, gas resources, production and costs,

infrastructure needs and costs, LNG export and pipeline capacity, LNG bunkering, LNG prices, future

demand and supply affecting LNG, and general energy markets and other aspects of our business

Reserves and resources

and our prospects and those of other industry participants. Estimates of non-proved reserves and resources are based on more limited information, and are

Our forward-looking statements are based on assumptions and analyses made by us in light of our subject to significantly greater risk of not being produced, than are estimates of proved reserves.

experience and our perception of historical trends, current conditions, expected future

developments, and other factors that we believe are appropriate under the circumstances. These

statements are subject to numerous known and unknown risks and uncertainties, which may cause

actual results to be materially different from any future results or performance expressed or implied

by the forward-looking statements. These risks and uncertainties include those described in the “Risk

Factors” section of our Annual Report on Form 10-K for the fiscal year ended December 31, 2018 and

our other filings with the Securities and Exchange Commission, which are incorporated by reference

in this presentation. Many of the forward-looking statements in this presentation relate to events or

developments anticipated to occur numerous years in the future, which increases the likelihood that

actual results will differ materially from those indicated in such forward-looking statements.

Disclaimer

Global LNG capacity call: ~100-250 mtpa

mtpa

800 Capacity required(1)

9.3% p.a. growth rate 9.3%(2)

700

~250 mtpa

600

5.0%(3)

500 ~100 mtpa

400

300 Possible FID projects(6)

Likely FID projects(5)

200

Under construction(4)

100

In operation

-

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Sources: Wood Mackenzie, Bernstein, Morgan Stanley and Tellurian Research. Freeport T1-3, PetronasFLNG 2, Portovaya, Prelude, Sengkang, Tangguh, Vysotsk and LNG Canada.

Notes: (1) Assumes 86.5% utilization rate. (5) Assumes ~40 mtpa of likely FID projects, including: Artic LNG T1-3, Mozambique Area 4 and new Qatar T1-3.

(2) Assuming sustained 2015-2018 demand growth rate of ~9.3% p.a. post-2019. (6) Assumes ~25 mtpa of possible FID projects, including: Cameron T4-T5, Freeport T4, PNG T3, Corpus Christi LNG Stage 3 and

(3) Assumes 5.0% p.a. demand growth rate post-2019. Papua LNG T1-T2.

(4) Assumes ~80 mtpa of projects under construction, including: Cameron T1-3, Calcasieu Pass, Elba Island T1-10,

3

Global LNG demand pull

Key drivers

800 Capacity required(1)

China

9.3%(2)

700

~250 mtpa

9.3% p.a. growth rate

600

5%(3)

India 500

Under construction ~100 mtpa

400

In operation

300

Europe

200

100

New

markets 0

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Sources: Wood Mackenzie, Tellurian Research.

Notes: (1) Assumes 86.5% utilization rate.

(2) Assuming sustained 2015-2018 demand growth rate of ~9.3% p.a. post-2019.

(3) Assumes estimate of 5.0% p.a. demand growth rate post-2020.

4

Emerging consumption: China and India

Population and economic growth imply significant upside to gas consumption in China and India

Size indicates relative Natural gas’ share of 2018 energy mix

GDP/capita

volume of gas

$80,000

consumed per capita in

2018 (mcf/capita)

$70,000

United States

$60,000 87 mcf/capita

$50,000

$40,000 European Union

38 mcf/capita 49%

$30,000

China 31%

$20,000

7 mcf/capita 23%

Argentina

$10,000 38 mcf/capita

India 6% 7%

2 mmcf/capita

$-

- 500 1,000 1,500 2,000 India China EU U.S. Argentina

Population (millions)

Sources: IHS Markit, SIA Energy, EIA, CIA World Factbook, BP Energy Outlook.

5

Growing demand in China

Economic growth and emerging environmental policy drives demand growth

Chinese gas demand

billion cubic meters per year

510

438

120 LNG 4.5% CAGR

(2018-2030)

108

277

74 Domestic

391 production 6.1% CAGR

(2018-2030)

330 & pipeline

203

imports

2018 2025 2030

Source: SIA.

6

India gas demand requires significant LNG imports

India natural gas demand – primary sources

mtpa

100 95

Domestic production

88

Contracted LNG

79

80 Uncontracted LNG

70

41

15 28 61

60

48

41 7 23 15 12

40

8

19 3

14

20

32 36 35 31

19 21

-

2018 2020E 2025E 2030E 2035E 2040E

Source: Wood Mackenzie.

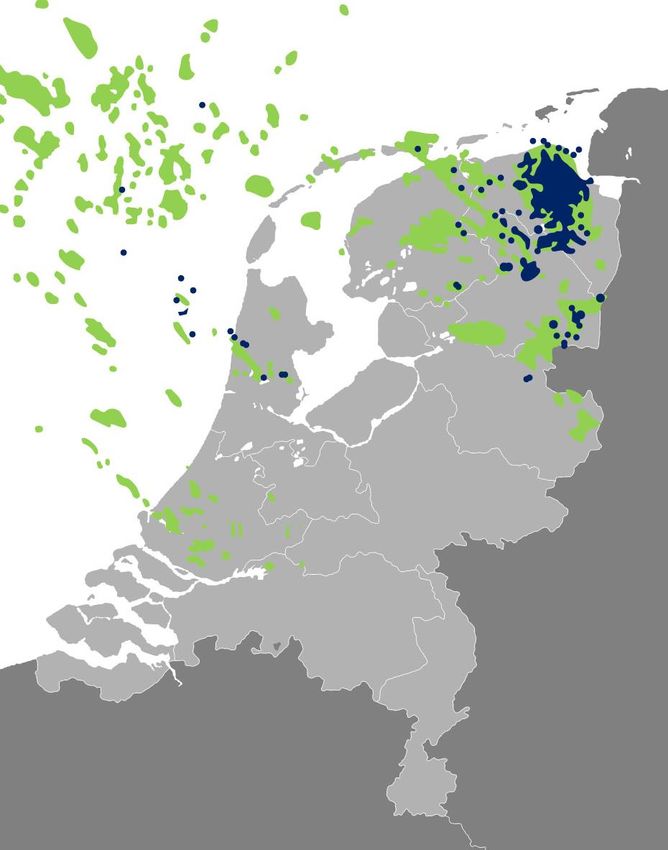

7LNG required to offset Groningen declines

Netherlands capping production from the Groningen field requires ~10 mtpa of LNG

bcm

Groningen yearly production

54

Forecast

Netherlands

42 Mandated

production cap

28 28

24

22

15

12 12 12

8

4 3

Gas fields

2024

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2025

Earthquakes

Source: NAM, Energy Aspects.

8 Global LNGGrowing number of importers accessing LNG

The number of LNG importing nations has grown by ~60% in the last 7 years

33 total floating storage

and regasification units

(FSRUs) represent ~130

42

mtpa of global 40

regasification capacity as 39

of May 2019

34

30

29 868

Number of 850

830

importing

26 777

countries 751

721

Global regas

capacity 668

(mtpa)

2012 2013 2014 2015 2016 2017 2018

Source: GIIGNL, IGU (2019), IHS Markit.

Notes: Includes Lampung, Nusantara, and Tanjung Benoa (all in Indonesia) and Northeast Gateway (United States).

9U.S. emerges as the world’s largest LNG exporter

Based on firm capacity

30.6

Triangle of low-

cost supply

102

77.8

88.8

Current capacity (mtpa)

(producing and under

construction)

Source: Wood Mackenzie, Tellurian Research.

Notes: Includes existing and under construction projects.

10Plentiful, low-cost U.S. natural gas

Production growth and resource base from selected U.S. unconventional basins Resource

size, Tcf

Basin

Wellhead cost, $/mmBtu

411

Total U.S. lower-48 dry natural gas production

36.0

Bcf/d

29.2 135 53 RBN(1)

7.4

3.6 23

2018 2025

Anadarko 17 EIA

74 $0-$1.00 2018 2025

16.9

Marcellus-Utica

9.6

112 < $1.00

99

2018 2025 52 82

8.6 9.4

Permian 7.9

< $1.00 4.9

2018 2025

2018 2025 2018 2025 Production

Eagle Ford Haynesville

growth

$0 - $1.50 < $1.50

Source: EIA 2019 Annual Energy Outlook, DrillingInfo, RBN, Tellurian analysis.

Note: (1) RBN high case – extrapolated from 2024 to 2025 by Tellurian.

11Looming challenge of U.S. gas oversupply

U.S. natural gas must be exported

Legend 2018-2025:

Operating/under construction LNG +7

Future infrastructure required +22 Bcf/d total gas supply growth(1)

+X Incremental gas supply by 2025 (bcf/d)

+12 Bcf/d excess gas supply(2)

+4

+100 mtpa LNG capacity required(3)

+1

+7

~$150 - $225 billion(4) of investment

+3 required to build 100-150 mtpa of LNG

and supportive pipeline infrastructure

to export excess U.S. gas supply

Sources: DrillingInfo, EIA, Tellurian analysis.

Note: (1) Assumes $70/bbl oil price and $3/mmBtu Henry Hub price; incremental supply comes from Permian, Scoop/Stack, Haynesville, Eagle Ford, and Appalachia.

(2) Assumes U.S. natural gas demand grows 0.6% p.a. and that the 7.4 bcf/d of LNG terminals under construction produce at a 90% utilization rate.

(3) Assumes new LNG terminals produce at a 90% utilization rate.

(4) Assumes new liquefaction capacity costs $1,000 per tonne plus an additional $70 billion of pipeline infrastructure to transport gas supply to the terminal.

12U.S. must export ~30 bcf/d of LNG by 2025

…including an additional ~20 bcf/d of LNG export capacity over firm capacity

U.S. natural gas export requirements

29 bcf/d

~20 bcf/d

additional U.S. LNG export capacity required(1)

$150 billion

investment required for >150 mtpa of additional LNG capacity(2)

Firm LNG

4 bcf/d export

capacity(3)

2018 2025E

Source: RBN, Tellurian analysis. (3) Includes 86 mtpa (11.5 bcf/d) of operational and under construction liquefaction export capacity.

Notes: (1) Assumes U.S. domestic gas demand grows at 0.6% p.a. and liquefaction capacity utilization rate of 90%.

(2) Assumes $1,000 per tonne for liquefaction capacity.

13Thank you

You can also read