LOSING THE INFLATION ANCHOR - LSE Ricardo Reis

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

LOSING THE INFLATIO ANCHOR Ricardo Rei LSE 9th of September, 202 Brookings Papers on Economic Activit Fall conference, virtual 1 s 1 y N

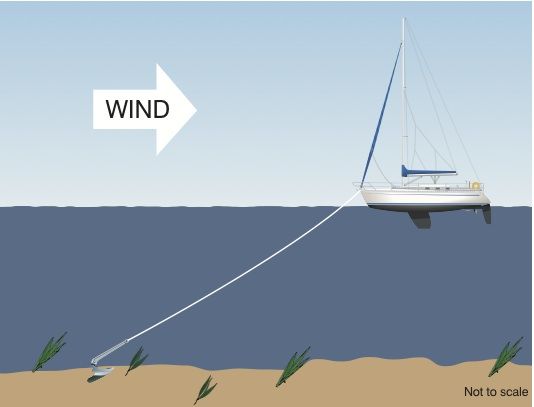

Is in ation out of control? Central bank can control the sails that guide the boa Inflation 2 fl t

Is in ation out of control? Central bank can control the sails that guide the boa But the winds from the recovery, Inflation the global shortages, and scal policy make the in ation boat oat, sometimes straying far from target. Is the boat lost 3 fl ? fl t fi fl

Is in ation out of control? Central bank can control the sails that guide the boa Inflation But the winds from the recovery, the global shortages, and scal policy make the in ation boat oat, sometimes straying far from target. Is the boat lost Inflation expectations Look underwater for the anchor. Is it anchored? 4 fl ? fl t fi fl

Most famous case: the Great In ation 1965-68: signs or no signs Martin had no use for models, pressured to prioritize Anchor In Seabed A Drifting Anchor First Oil Shock Unanchored Inflation unemployment. Sensitive to investor expectations, measured with bond rates. As in ation kept rising, 12% increasingly relied on “in ationary psychology CPI Inflation CPI Core Inflation GDP Deflator Inflation 1968-71: anchor driftin 8% As in ation accelerated, Martin, July 1969, “in ationary USD Off Gold psychology remained the main economic problem” Shocks temporary because eeting beliefs. Models of shifts in Phillips curve, in ation bias 4% 1971-74: anchor adrif Burns on wage and price controls “In this new 0% psychological environment, our trade unions may not push quite so hard for a large increase in wage rates, 1960 1961 1962 1963 1964 1965 1966 1967 1968 1969 1970 1971 1972 1973 1974 1975 1976 1977 1978 1979 1980 1981 since they would no longer be anticipating a higher in ation rate. And in this new psychological environment, our business people would not agree to large wage increases quite so quickly” No measurement, expectations as an add-on factor 5 fl fl fl fl t g fl ? fl . ” fl fl

The data they looked at: professionals Both Fed’s staff and 6% Livingston median expected inflation SPF median expected inflation Greenbook inflation forecast professional forecasters caught up sluggishl 4% 2% (And the Fed’s staff was particularly bullish on view 1965 1966 1967 1968 1969 1970 1971 1972 1973 1974 1975 that all was temporary Greenbook Livingston 8% 12 months ahead 12 months ahead median 9−12 months ahead 6 months ahead median 3 months ahead 6% 6−12 months ahead 6% 4% Behind the curve 4% 2% 2% 1967 1968 1969 1970 1971 1972 1973 1974 1975 1966 1967 1968 1969 1970 1971 1972 1973 1974 1975 6 y )

The data they rarely mentioned: households Since 1946, Michigan Survey of 12% Consumer Attitudes asked Michigan quantitative survey mean Mankiw−Reis−Wolfers qualitative survey mean whether expected prices to rise 10% or fall. MRW (2004) index 8% But also, between 1966Q2 and 5% 1976Q4, follow up question: “How large a price increase do you expect? Of course, nobody 2% can know for sure, but would you say that a year from now prices 0% will be about 1% or 2% higher, or 1966 1967 1968 1969 1970 1971 1972 1973 1974 1975 5% higher, or closer to 10% higher than now or what?” 7 .

Can look deeper: disagreement 0.75 5% 1967 0.10 1970 1974 0.50 Standard deviation (right axis) Skewness (left axis) 4% 0.25 0.05 0.00 3% 0.00 1967 1968 1969 1970 1971 1972 1973 1974 1975 1.5 3.5 5.0 7.5 12.0 1967-70: Thickening right tail, hollowing of left tail, standard deviation rising, positive skew fallin 1970-73: Median shifted slowly, right tail quickly, standard deviation rose, the skew rst up then down 8 fi g

Markets and the media 5% 15% Market: expected inflation Central bank % mentions in NYT (left axis) Inflation % mentions in NYT (left axis) Concern about inflation − about unemployment Gallup (right axis) 4% 60% 10% 3% 40% 2% 5% 20% 1% 0% 0% 0% 1965 1966 1967 1968 1969 1970 1971 1972 1965 1966 1967 1968 1969 1970 1971 1972 1973 1974 1975 New data from the Zurich market for gold forwards (alternative to London and Gold pool): very responsive, perhaps too much In media see some upticks 9 .

A model to combine them into fundamental RE Households: biased from experiences, h ⇤ h h e ⇤ sluggish average, over-react individuall AAAERXicdVNZbxMxEN5uOEq4UnjkZUREldAm2lQVRSCkCgjHA1Akekh1EnkdJ7G6V21vIFrtX+HXIPEE7/wI3lBfYbxHWqDx7mrHc3wz83nsRp5Q2nF+LNmVCxcvXV6+Ur167fqNm7WVW3sqjCXjuyz0QnngUsU9EfBdLbTHDyLJqe96fN89embs+1MulQiDD3oW8Z5Px4EYCUY1qgYr9ta0PxloWH0CJBL9+yiuActUa0D0hGuKYoOXGvThKLVK5yYQUl0F8tg8GMA/6eSj0JO0VOVYRAkfug3iYWVDRGyuZ3bIcQlWqOfYme/bhrNupLFP+xvoD+fkYTJUqqU4M61QD4ZIlxRubLZ5fpieZn9h+ihyZFXje1x0PpKUJUBEoGE20KdeY9xgXD9pddIGCX0+NrU3YbRADzAs20iTDO58hMUA83hIFzD7aE5tGZf397RBXDytglljLvnM2D0u/V6eJQEMC92+W/DQLTiaR037SZ7Z50NBgzQd6HUD1YRBre60Nxyz4H+h087+Tt0q1s6gdkKGIYt9HmjmUaUOO06kewmVWjCPp1USKx5RdkTH/BDFgPpc9ZJswlO4h5ohjEKJH7Kaac9GJNRXaua76OlTPVH/2ozyPNthrEcPe4kIoljzgOWJRrEHOgRzXXCmJM6XN0OBMimwVmATiuOi8VJVyXOOvUj+BnHfRVxSHcqEdPHsTSbXTbrIWK1esgGLhb2NdudBe/P9Zn37dUHZsnXHums1rI61ZW1br6wda9di9mf7i/3N/l75WvlZ+VU5yV3tpSLmtvXXqvz+A9uLWeI= vt = ⇡t + ct + ✓t (et + ⇡t ⇡t ) h h e 2 with ct ⇠ E( t ), et |⇡t ⇠ N (0, t ) Markets: more information, sensitive h e to news, lled with nois cross-sectional distribution vt ⇠ Ft (⇡t ) Professionals: median is misleading, not e R 1 1 e marginal traders yt (⇡t )gt (Ft (!t ))ft (Ft (!t ))d⇡t qt = R 1 1 gt (Ft (!t )ft (Ft (!t ))d⇡te Data inputs: three moments from e e household survey distribution, one with: !t ⇠ B( ), ⇡t |qt ⇠ G(⇡t ) market price, median professiona Model outputs: reaction, dispersion b median Et = Et (⇡t |vt , qt ) and bias ( , , ), market noise ( ), fundamental expected in ation ( e) 10 fi . e fl l y

Estimates of the expected in ation anchor 2 The drifting ancho 1.5 4.5 1 0.5 % 4 At rst, markets 0 seen as maybe -0.5 3.5 re ecting nois -1 1968 1969 1970 1971 3.1 But, disagreement 3 3 2.9 across households % 2.8 2.7 % 2.5 showed the fund. 2.6 2.5 expectation shiftin 2.4 2.3 2 2.2 1968 1969 1970 1971 6 Year 1.5 Later, sluggish 5 response of medians 4 of professionals 3 1 2 1967 1968 1969 1970 1971 con rms it 1 Year 0 1968 1969 1970 1971 Year 11 fl fi fi e g r fl

Beyond one episode: Brazil 2011-16? Figure 11: Brazil’s drifting expected inflation anchor: 2011-16 (a) Actual inflation and its target (b) Markets and survey first-order moments Loose monetary, scal 18.0% Consumer Price Inflation Consumer price inflation − admin prices Market−price implied Survey of Professionals dominance, belief all transitory, rising in ation Consumer price inflation − free prices 10.0% Survey of Households Inflation Target Inflation Target Upper Bound Upper Bound 14.0% 6.5% 10.0% 6.5% 4.5% Price controls over administrative prices 4.5% 2.5% 2.5% 0.0% 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 0.0% 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 kept it pent-up 2011-15 (c) Cross-sectional disagreement of households (d) Cross-sectional distribution of households Markets, professionals Cross−sectional survey skewness (lhs) Cross−sectional survey standard deviation (rhs) 8.0% 30 2011 weak signal 2014 6 2016 6.0% 20 4 4.0% But again household 2 10 disagreement revealed it 2.0% 0 0.0% 0 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 0% 5% 10% 15% 20% 25% 12 s fi fl . .

Third episode: Turkey 2018-… Figure 12: Turkey’s drifting expected inflation anchor: 2018-... (a) Actual inflation, markets and survey first- (b) Cross-sectional survey distribution order moments 30% 2017 2019 Actual inflation 20% 2020 Cross−sectional median of professionals... survey 25% Market−price implied expectation Weighted mean of firms... survey Target 15% 20% 15% 10% 10% 5% 5% 0% 0% 2% 4% 6% 7% 9% 10%12%13%15%16%18%19% 2% 4% 6% 7% 9% 10%12%13%15%16%18%19% 2% 4% 6% 7% 9% 10%12%13%15%16%18%19% 2015 2016 2017 2018 2019 2020 2021 Even in real time, cross-sectional survey expectations distributions give signa Subject to all these caveats, already by the end of 2017, the standard deviation almost If anchor is notwhile quadrupled, rm inthe theskewness seabed, shifts wentare from large and fastnegative at -1% to positive at 0.25%. being Panel (b) of Figure 12 shows the distributions 13 in December of 2017, January of 2019 and fi l

False positives: South Africa 2010-16? Figure 13: South Africa’s unlucky run: 2010-16 (a) Actual inflation, markets and survey first- (b) Cross-sectional survey distributions order moments 2014 2015 2016 0.2 6.0% 4.5% Inflation (CPI Headline) 0.1 Inflation (CPI Core) Analysts' forecast Businesses' forecast Trade unions' forecasts Upper bound Lower bound 3.0% 0.0 −1% 0% 1% 2% 3% 4% 5% 6% 7% 8% 9% 10% 11% 12% 13% 14% 15% 2012 2013 2014 2015 2016 2017 2018 2019 missed the fall in inflation in 2015 and were slow to catch up to the lower inflation Survey data stayed steady in light of unlucky run of shocks, price controls temporary effec from 2017 onwards. No drifting Theanchor, bottom nopanel false reproduces positive instead the cross-sectional distribution among house- holds at three successive months of October 14 between 2014 and 2016, calculated by Du t

What aboutFigure in 14: other direction? Dropping US the anchor: the US 1980s1980s (a) Actual and survey first-order moments (b) Survey disagreement 15.0% 4.0 20% Standard deviation (right axis) Skewness (left axis) 3.5 10.0% 3.0 15% 2.5 SPF median 2.0 10% 5.0% Michigan median Inflation (CPI) Inflation (Core CPI) 1.5 1978 1979 1980 1981 1982 1983 1984 1985 1979 1980 1981 1982 1983 1984 1985 is the loss of an inflation anchor, this Households ahead of professionals, agai episode corresponds to dropping of a new anchor, which persists in place until today. It adds a reversal situation and again tries to measure Disagreement pattern showed the dropping and rming of the anchor the anchor. 15 n fi

Looking ahead: US today? Figure 15: The expected inflation anchor through the pandemic (a) Actual inflation (b) Markets and survey first-order moments Tough test for beliefs 6% CPI Urban Core • salient price CPI Urban All Goods Trimmed Mean PCE 5% 5% Inflation Target People: Michigan 1 Year • recent dat 4% People: Michigan 5 Years 4% Traders: SPF 1 Year Market: 10 year Breakeven Inflation Rate 3% 2% 3% • over-reactio 1% 2% 0% 2018 2019 2020 2021 1% 2018 2019 2020 2021 See in the data the increase in disagreement (c) Cross-sectional disagreement of households (d) Cross-sectional distribution of households that points to an anchor 0.15 that is drifting up 5 Standard deviation (right axis) Skewness (left axis) 2020 January 2020 September But, jury is still out, and 1.0 4 0.10 2021 June much depends on luck 3 and policy over the next 0.05 0.5 2 1 0.00 12 months. 2018 2019 2020 2021 0.0 1.5 3.5 5.0 7.5 12.0 16 a s n . :

Conclusion • Expected in ation is not • …a mystical psychological variable for policymakers, an add-on factor, for data tters, a perfect mirror of actual in ation that can be ignored, too sluggish and biased in surveys to be usefu • Can measure the expected in ation anchor • …combine survey medians with markets and with disagreement in cross-sectional survey distribution • The roots of the Great In ation were in 1967-73, before oil shocks • …bad theory (of expectations), bad measurement (expectations), bad luck (salience • Five episodes in which expectations measurement would have been usefu • …and arguably useful now to see the anchor slightly drifting, but still in time to put it back in the seabed. 17 fl fl … fl fl … fi l ) … l s

You can also read