Market Presentation Israel - www.lloyds.com/marketpresentations www.lloyds.com/countryprofiles

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Market

Presentation

Israel

Sigal Schlimoff

Lloyd’s Representative in Israel

October 2013

> www.lloyds.com/marketpresentations

> www.lloyds.com/countryprofiles

The Market 1

Insurance Market Trends

Reinsurance Market Trends

Content

Regulatory Environment

Lloyd’s 2

Business Profile

Coverholders & Service Companies

Opportunities 3

Whom to target

What to target

Conclusions © Lloyd’s

1

The Market

Macro Themes

Insurance Themes

Market Size

Top Insurers

Distribution

A Market In Motion

Changes in Regulation

Outlook

© Lloyd’s

The Market >Macro Themes 1

Chart: GDP (Years & Indicator)

BUSINESS ENVIRONMENT in US$ (Billions)

HEADLINES

2013 ECONOMIC GROWTH: +3.4% 400 6%

(Q1+Q2 2013)

5.0% 5%

4.6% 4.5%

RANKED #4: most 4.4% 4.4%

4%

dynamic 3.4%

3.2%

OECD 200

2.8%

3%

growth

2%

UNEMPLOYMENT RATE: 6.1% 1.1% 1%

0 0%

2009 2010 2011 2012 2013 2014 2015 2016 2017

PRICE STABILITY: 2.2% Inflation

STRONG CURRENCY

1 Continued Resilience of economy

Large Natural Gas Extraction

SOLID BANKING SECTOR: NPL at 0.4% 2 expected to add 1%age point to

growth

Over the last 5 years Israel is one of the fastest-growing economies in the world and

is growing faster than its OECD peers

January 2013 – first election driven by social issues © Lloyd’s

Source: Market Intelligence calculation based on: Central Bureau of Statistics, Bank of Israel, www.bankisrael.gov.il; Global Insight (September 2013)

The Market >From “Start Up” to “Exit” Nation 1

Start

Start UpUp Buyer

Buyer Price

Price

US$ 966m

US$ 800m

US$ 800m

US$ 480m

US$ 475m

2012 - 50 exits in Israel, amounting to- US$ 5.5bn

This trend is set to continue throughout 2013

© Lloyd’s

Source: Soft Market Intelligence – Globes Magazine, The Marker Magazine, Calcalist Magazine

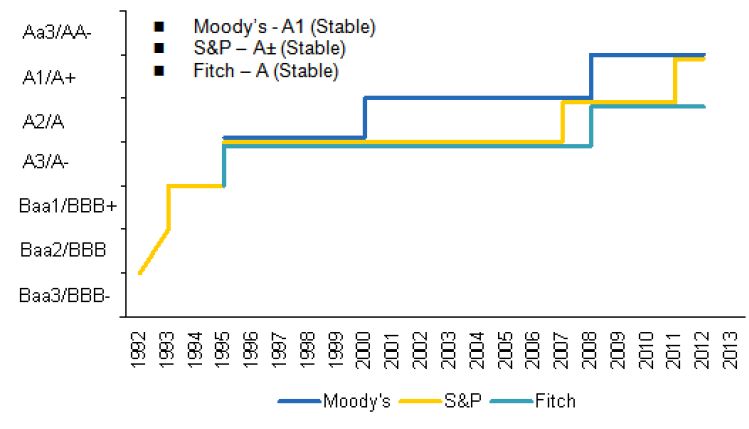

The Market >Israel’s Sovereign Ratings 1

Sovereign Ratings over time

HEADLINES

Moody’s – A1(stable)

S&P – A+ (Stable)

Fitch – A (stable)

Israel is amongst the few OECD countries which have recently been upgraded

Since the 2008 crisis, all agencies upgraded ratings

Steady rating improvement over the years

© Lloyd’s

Source: The Government Debt Management Unit http://ozar.mof.gov.il/debt/gen/mainpage.asp; S&P Israel: http://www.maalot.co.il/publications/CP20130807113430.pdf; MOF

The Market >Insurance Themes 1

INSURANCE ENVIRONMENT Chart: 2000-2012 Market HEADLINES

premiums

(non-life, in million NIS)

PREMIUM GROWTH: steady 30,000

25,000

Premium growth from 2011 to 2012

20,000

(non-life): +6.6% (in local currency)

15,000

Still a soft market 10,000

All insurance companies are composite 5,000

insurers – which contributes to their 0

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

stability

(non-life, in million US$)

Regulator takes active steps to encourage

8,000

competition 7,000

6,000

Tight regulation in private lines – recent 5,000

regulation in life and health insurance 4,000

3,000

More lenient regulatory environment in 2,000

respect of commercial insurances 1,000

0

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Favourable regulatory regime

Increasingly open to foreign investors / insurers

Advanced implementation of Solvency II regulation © Lloyd’s

Source: Market Intelligence calculation based on: Commissioner of Capital Markets, Insurance & Savings, http://ozar.mof.gov.il; soft intelligence based on Lloyd’s Representative, 2013

The Market >Market Size 1

Chart: 2000 – 2012 Non-Life Market Premiums by Class

in million NIS LEGEND

30,000

25,000

Miscellaneous

20,000

MAT

15,000 PA & Health

Liability

10,000

Property

5,000 Motor

0

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Most significant class of business growth in: Third Party Liability, Credit Insurance, Product

Liability, Employers’ Liability

Market is still driven by Motor insurance (c. 40%) and life.

2013 - 1st year of profit in Motor & Property insurance following many years of losses

© Lloyd’s

Source: Market Intelligence calculation based on: Commissioner of Capital Markets, Insurance & Savings, http://ozar.mof.gov.il; soft intelligence based on Lloyd’s Representative, 2012

The Market >Market Size 1

Chart: 2000 – 2012 Non-Life Market Premiums by Class

in million US$ LEGEND

8,000

7,000

6,000 Miscellaneous

5,000 MAT

4,000 PA & Health

3,000 Liability

2,000 Property

1,000 Motor

0

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Most significant class of business growth in: Third Party Liability, Credit Insurance, Product

Liability, Employers’ Liability

Market is still driven by Motor insurance (c. 40%) and life.

2013 - 1st year of profit in Motor & Property insurance following many years of losses

© Lloyd’s

Source: Market Intelligence calculation based on: Commissioner of Capital Markets, Insurance & Savings, http://ozar.mof.gov.il; soft intelligence based on Lloyd’s Representative, 2012

The Market >Top Insurers 1

Chart: 2012 Gross Written Premiums by top Market players

in million US$; non-life only

0 500 1000 1500 HEADLINES

Harel

The Phoenix

19 insurance companies

Clal

Menora Mivtachim Very High level of concentration

Migdal

Ayalon

- Top 6: 78%

IDI

ILD

Eliahu - Others: 22%

AIG

Other

Chart: 2012 Gross Written Premiums by top Market players

in million US$; including life insurance Local market depends on

0 500 1000 1500 2000 2500

international Reinsurance

capacity; no local Reinsurance

Migdal

capacity

Harel

Clal

Market entry of new players

The Phoenix

Menorah Movtachim

Ayalon

Premium income increase for most insurance companies (16 out of the 19) between

2011-2012

© Lloyd’s

Source: Market Intelligence calculation based on: Commissioner of Capital Markets, Insurance & Savings, http://ozar.mof.gov.il; soft intelligence based on Lloyd’s Representative, 2012The Market >Distribution 1

HIGHLIGHTS

No legal difference in Israel

Main distribution channel -

between broker & agent

insurance agents

Unique stakeholders -

Circa 12,000 insurance agents

insurance consultants in

operate within 1,150 insurance

commercial insurances

agencies- significant parts in

pension insurance

Increased trend in sale of direct

insurance – (IDI & AIG and also

other insurance companies). IDI Significant potential change -

celebrated a successful IPO. “Tied Agencies” – Commissioner

considers prohibiting insurance

agencies controlled by insurance

New advanced technological

companies from selling insurance

distribution solutions in pipeline products of other insurers,

(tablets, smartphones, online) specifically in private lines - many

large insurance agencies will be

sold or become “tied agencies”

© Lloyd’s

Source: Market Intelligence calculation based on: soft intelligence by Lloyd’s Legal RepresentativeThe Market >A Market In Motion 1

1 MIGDAL & CLAL

Migdal: Generali sold the controlling shares to Shlomo Eliyahu

(local player)

Clal: Sale of control to Chinese Group – JT Capital

2 PEOPLE CHANGES

New CEOs appointed in the major insurance companies – introducing

different business approach

3 REGULATION

New Commissioner of Insurance was appointed as a result of recent

elections. Most of the senior staff were replaced

Investment Houses are now allowed to sell life insurance - new players

© Lloyd’sThe Market > Changes in Regulation 1

1

Opening of the Israeli market to foreign insurers – under review by

Commissioner

2

Major regulation change in Executive Insurances, Life Insurance

and Pension Insurance

3

Implementation of new strict claims handling process in personal lines

Imposition of wording restrictions on policy wordings

© Lloyd’sThe Market >Outlook 1

1 FINANCIAL STABILITY AND GROWTH

Strong and diversified economy, proven resilience during financial crisis,

growing consistently faster than OECD peers

2 EVOLVING INSURANCE MARKET REMAINS VERY STABLE

Well regulated insurance market with enhanced capital requirements

Strong financial results

3 A VERY CONCENTRATED YET SOPHISTICATED MARKET

In 2012, the insurance market became more concentrated with fewer

insurance companies

The insurance market is very sophisticated with high levels of penetration

& insurance awareness

© Lloyd’s2

Lloyd’s

Background

Business Profile

Coverholders & OMCs

Reinsurance

Key Actions & Office Support

Events

Summary

15 © Lloyd’sLloyd’s >Background 2

WESTERN ASIA LLOYD’S PROFILE

Other

18% UAE

20%

Cyprus

2012

Israel is consistently a

6%

Western Asia major source of

Qatar Lloyd’s Premiums

7%

US$ 939m Israel

premiums for Lloyd’s

19%

Saudi Arabia

8%

in the region

Bahrain

9% Turkey

13%

SOURCE: Market Intelligence based on *Gross Signed premiums; Xchanging (2013); unaudited figures based on country of origin and processing by calendar year; see Appendix for details

DIRECT BUSINESS

Lloyd’s underwriters are allowed to transact business on a direct basis (no deposit requirement)

IN ISRAEL: Business is conducted through Lloyd’s Coverholders

or Open Market Correspondents (OMCs)

(who must obtain a licence from the Commissioner of Insurance)

IN LONDON: Business is conducted through Lloyd’s brokers

REINSURANCE BUSINESS

Lloyd’s underwriters are approved by all local insurance companies to reinsure all lines of business,

© Lloyd’s

facultative and treatyLloyd’s >Business Profile 2

2008 – 2012 Premiums by type (in million US$)

2012 GROSS SIGNED PREMIUMS*

200

Total US$ 180m

150

Reinsurance US$ 72.m

Direct US$ 106.9m

100

50 *COUNTRY OF ORIGIN PREMIUMS

Policyholders based or

headquartered in this territory;

0 Premiums may be written outside

this territory;

2008 2009 2010 2011 2012

X Not where risks are located.

Direct Reinsurance

SOURCE: Market Intelligence based on *Gross Signed premiums; Xchanging (2013); unaudited figures based on country of origin and processing by calendar year;

see Appendix for details

SUCCESS STORIES 2012 Premiums by Class* (in million US$)

1 COVERHOLDERS & OMCs UK Motor

23 Coverholders & OMCs Property Treaty

Property (D&F)

EXPANDED BUSINESS Overseas Motor

2 24 new applications for Marine

OMC/Coverholder status or Energy

expanded classes Casualty Treaty

Casualty

LEADER IN INNOVATIVE

3 PRODUCTS

Aviation

Accident & Health

Lloyd’s perceived as leader in

0 10 20 30 40 50 60

sophisticated & niche lines © Lloyd’sLloyd’s >Coverholders & OMCs 2

COVERHOLDERS & OMCs Coverholders & OMCs

6 Coverholders

17 Open Market Correspondents

11

9

Claims

5 Coverholders have claims handling

authority

1 Coverholder has delegated claims

handling authority to a Third Party

Administrator domiciled in Israel

Number of active binders by region > SEE: www.lloyds.com/directories

0 11

for further details

1 Be local

Lloyd’s Coverholders & OMCs operating from Tel Aviv and vicinity across the country

2 Coverholders / OMCs are active in complementary solutions which are not provided by the local

market

Source: Market Intelligence calculation based on Country Manager & Lloyd’s Delegated Authorities (October 2013)Lloyd’s >Reinsurance 2

2010 TOP REINSURERS Lloyd’s main reinsurance involvement ‐

OTHERS

31.5%

in facultative reinsurance

4%

4%

19%

Need for greater capacity in CAT risks

4.5%

5%

5%

12% Main potential for Lloyd’s in Israel ‐ in

7%

8% Reinsurance ‐ high growth potential

2012 Top Reinsurers of 5 biggest Insurers

Non-life, reinsurers exceeding 10% of premium in one or more insurer

Swiss Re

Munich Re

Generali

National Indemnity

Zurich

Lloyd’s

Source: Market Intelligence calculation based on The Israeli Insurance Market – main figures Dec. 2010, MOF - capital market insurance and savings divisions, Individual Financial Statements of 5 biggest Insurance

CompaniesLloyd’s >Key Actions and Office Support 2

2014 COUNTRY DEVELOPMENT PLAN OFFICE SUPPORT

1

1 2 3 4 5

KEY KEY BUSINESS INSURANCE LLOYD’S

FACTS STATISTICS ENVIRONMENT ENVIRONMENT BUSINESS

Create a facility to enable London

Lloyd’s Vision 2012

Positioning Lloyd’s as an unquestionable leader on non-life speciality insurance and reinsurance market in Poland. Lloyd’s is well understood by the top local intermediaries

contacting Market and bringing business there on a daily basis. The coverholder’s network is well established across the country and the local coverholders deliver the

substantial part of Lloyd’s country production.

Lloyd’s key Initiatives 2012

Build a network of at least 15 coverholders at the end of 2012.

The Lloyd’s Country Development Plan

Targeting 20 top insurers in the country and supporting them in developing business with Lloyd’s.

contains key Market Development

Promoting use of Lloyd’s Polska office in Warsaw.

Improving the visibility and understanding of Lloyd’s among the local stakeholders.

Promoting Lloyd’s in the country.

Events & Market Intelligence

INDUSTRY EVENTS

Annual Brokers Congress, May 2012.

LLOYD’S EVENTS

Polish Risk Managers Visit to London, 12 March 2012.

Reinsurance Rendezvous, Warsaw, 5 June 2012.

Regional event in Hungary, Budapest, 26 June 2012.

Meet the Market Event, Warsaw, 11 September 2012.

MARKET INTELLIGENCE

Country Profile

Market Presentation

Country Roundup

Activities and a clear Vision U/Ws & Brokers to meet local

stakeholders

© Lloyd’s

> www.lloyds.com/events > www.lloyds.com/marketintelligence

2 Contacts with Regulators

1. EXPLORE OPPORTUNITIES IN

CHANGING MARKET

New opportunities and challenges for Lloyd's 3 Support local insurance companies

in view of the significant changes in the market & brokers interested in working with

Lloyd’s

2. HIGHLIGHT REINSURANCE AND

SPECIALIST APPETITE

Lloyd's unique position as a leading insurer

FUTURE EVENTS

and reinsurer in special lines, should be

fortified

1 J Gross Memorial scholarship

3. PROMOTING LLOYD’S

Lloyd’s predominance as an international

London-based market should be introduced

2 Lloyd’s Market and COB event

and promoted

3 Coverholders' Dinner

© Lloyd’s

Source: Country Manager (October 2013)Lloyd’s >Summary 2

1 Main Role of Lloyd’s in Local Market - Specialty & Innovative Products

Lloyd’s is perceived as a leader mainly in specialist lines and an

important source when high capacity is required

2 Steady Growth of Lloyd’s Premium Income in Israel

From 2011 to 2012 – increase of 6.5% in total premium

From 2010 to 2011 – increase of 25% in total premium

3 Israel is a Major Market for Lloyd’s in the Region

A strong cooperation with local insurance companies and a solid network

of Coverholders & OMCs puts Israel among the top market for Lloyd’s in

the region

© Lloyd’s3 Opportunities Targets Summary 22 © Lloyd’s

Opportunities >Specialty Lines 3

1 CYBER INSURANCE

Israel Faces 100,000 cyber attacks each day, yet the damages are not

very high in view of tight secured systems.

There is a very high awareness of the risk but very few products in the

market

2 TERROR INSURANCE

Businesses seek cover from terror risks. In view of the existence of a

State’s Statutory Fund which compensate against property damage

caused by war and terrorism, the risk for insurers is only residual – for

whatever is not covered by the fund

(indirect damages, reinstatement value)

3 ENERGY INSURANCE

Significant natural gas discoveries have led to increased need for

insurance capacity

© Lloyd’s

Soft market intelligence : http://www.israelnationalnews.com; http://www.maglangroup.comOpportunities >Specialty Lines 3

1 HIGH TECH

Constantly evolving high tech market requires various types of cover,

from PI, PL, Cyber, Multimedia, VC Liability

2 MEDICAL TOURISM

Israel is quickly becoming an international attraction in the field of health

tourism.

Insurance opportunities include: Travel, Health and Med-mal insurances

3 REINSURANCE

Participation in treaties, fronting facilities & facultative in special lines:

e.g. Financial Institutions, Diamonds, Med-mal, Terror, D&O

© Lloyd’s

Soft market intelligence : http://www.israelnationalnews.com; http://www.maglangroup.comOpportunities >Targets- Who to target? 3

Increase appetite for reinsurance

Offer reinsurance in innovative products

Local Carriers Increase participation in treaty reinsurance

Utilise market need for fronting facilities

Work in cooperation with local and international

Local & Intl. Lloyd’s brokers

Support brokers who are or wish to become

Brokers coverholders /OMCs in areas where there is a need

for the market

Large companies

and specialty Who seeks direct or reinsurance at the Lloyd’s market

industries

© Lloyd’sOpportunities >Targets – What to Target? 3

1 OPPORTUNITIES FROM SECTORS WHERE LOCAL CARRIERS

LACK KNOW-HOW

2 OPTIONS FOR GROWTH IN NEW SEGMENTS AND SOPHISTICATED

CLASSES (AS PER OPPORTUNITIES)

3 POTENTIAL OPPORTUNITIES IN ISRAELI-ARAB SECTOR

© Lloyd’sOpportunities >Summary 3

1 CHANGE MAY CREATE OPPORTUNITIES

Changes in the Israeli insurance market create new opportunities for

Lloyd’s both in Direct and Reinsurance business

2 STEADY PREMIUM GROWTH FOR LLOYD’S

Lloyd’s gross premiums have exhibited steady growth in recent years

3 LLOYD’S FINANCIAL STRENGTH IS A MAJOR ADVANTAGE

Lloyd’s high rating is a major advantage in the reinsurance sector,

in view of tightening regulatory requirements

© Lloyd’sA Appendix About Market Intelligence 28 © Lloyd’s

> www.lloyds.com/marketintelligence

COMPARE COUNTRIES 1 COUNTRY PROFILES 2

Interactive Google Motion Chart Summary fact sheets on 54 territories

Heat map of key indicators overview of insurance market

Download Insurance Market Statistics Guide to Lloyd’s premiums & licence

MARKET PRESENTATIONS 3 CLASS REVIEW 4

Local perceptions & market statistics Class of Business Analysis by territory

Key opportunities & challenges Market share analysis

Lloyd’s activities Downloadable triangulations*

SUBSCRIBE AT: www.lloyds.com/misignup * Detailed performance stats for Managing Agents only

COUNTRY ROUNDUPS 5 QUESTIONS ?

Receive updates from Country Managers Visit our website

Digest of insurance & reinsurance news Contact us directly

Focus on local brokers, CH and MAs Subscribe at www.lloyds.com/misignup

SUBSCRIBE AT: www.lloyds.com/misignup

FREE DOWNLOAD AT www.lloyds.com/MARKETINTELLIGENCE

DOWNLOADMarket Intelligence – Team

Filip Wuebbeler, Senior Manager

Email: filip.wuebbeler@lloyds.com

Focus: Team Leader / Northern Europe / Product Development

Tom Grace, Asia Pacific Analyst (to start on 2 December 2013)

Email:

Focus: Asia Pacific / South Africa & Ireland / V25 Strategy

Chris Brown, Americas Analyst (to start on 30 September 2013)

Email:

Focus: Americas / Italy / Spain / Class Review / Engagement Strategy

Lara Green, Soft Intelligence Executive

Email: lara.green@lloyds.com

Focus: Country Roundups Development & Roll Out

Robert Shearman, MI Data Analyst (to start on 16 September 2013)

Email:

Focus: Better Market Intelligence Project Work, MI Portal

To book a personal surgery session with the MI team email marketintelligence@lloyds.com

© Lloyd’sAppendix > Data Limitations & Disclaimer

Lloyd’s Data Limitations

Please note the information contained in this document is based upon data collected from Xchanging and may be incomplete

for some classes of business; for instance a substantial figure, which is missing from the REG 258 data set is comprised of UK

Motor, which is not processed by Xchanging.

Gross Premiums: Original and additional inward premiums, plus any amount in respect of administration fees or policy

expenses remitted with a premium but before the deduction of outward reinsurance premiums.

Lloyd’s figures are based on gross written premiums based on figures processed by Xchanging by processing year and country

of origin.

Country of Origin: denotes the country from where demand for the insurance / reinsurance emanates; i.e. the coverholder or

policyholder, irrespective of the country to which the risk is classified for regulatory reporting purposes.

Processing Year: relates to the calendar year in which the premium, additional or return premium is processed by Xchanging,

irrespective of the actual underwriting year of account of the risks (which is determined by the inception date of each risk).

Example: A policy holder in the UK insuring a holiday home in France would be classified as a UK risk by Country Of Origin, but

French for regulatory reporting purposes. Similarly a risk incepting on 1st December 2007 would be classified at 2007

underwriting year of account but may not be processed by Xchanging until 2008 and so be allocated to the 2008 processing

year

Disclaimer

This document is intended for general information purposes only. Whilst all care has been taken to ensure the accuracy of the

information Lloyd's does not accept any responsibility for any errors or omissions. Lloyd's does not accept any responsibility or

liability for any loss to any person acting or refraining from action as a result of, but not limited to, any statement, fact, figure,

31 © Lloyd’s

expression of opinion or belief obtained in this document.32 © Lloyd’s

You can also read