MYTHS & REALITIES of RETAIL MARKETS - European Electricity - EEMG ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

MYTHS & REALITIES of

European Electricity

RETAIL MARKETS

WH Y I S TH ERE A NEED TO RE V EA L THE RE TAI L

MY T HS A ND REA L I TI E S?

A number of myths tend to hijack the European debate on retail electricity markets. Common

misconceptions include claims that energy bills increase due to rising company profits, or that

energy suppliers intentionally make it difficult for consumers to compare offers. These myths

need to be addressed and the realities properly clarified and explained.

The record must be set straight to allow the debate to focus on the real issues preventing

retail electricity markets from functioning properly. In this respect, it is crucial to fully and

constructively engage consumers.

To challenge these enduring retail myths, we consider the following elements: the nature of

the myth; the reality; and supporting evidence with quotes from authoritative sources such

as European and national regulatory authorities or the European Commission.

In a limited number of markets, where the situation is more complex, it can be harder to

debunk some of the myths. Where this is the case, we focus on further clarifying the intricacies

to give a more accurate picture of the reality.

Reality Evidence Quote

EU RE LE C TRI C in brief

The Union of the Electricity Industry – EURELECTRIC – is the sector association

representing the common interests of the electricity industry at pan-European level.

Our work covers all major issues affecting our sector, from electricity generation

and markets to distribution networks and customer issues. Our current members

represent the electricity industry in over 30 European countries, including all EU

Member States. We have also affiliates and associates on several other continents.

Our structure of expertise ensures that input to our policy positions, statements and

in-depth reports comes from several hundred active experts working for power

generators, suppl y c ompanies and distributi on network operators.

We have a permanent Secretariat based in Brussels, which is responsible for the

o v e r a l l o r g a n i s a t i o n a n d c o o r d i n a t i o n o f E U R E L E C T R I C ’s a c t i v i t i e s .

Dépôt légal: D/2016/12.105/14

Let’s debunk the retail electricity myths and focus on the

real issues preventing customer empowerment.

ENERGY BILLS INCREASE DUE TO

RISING COMPANY PROFITS

Many co nsu m ers bel iev e th at elect ri ci t y com pany profit s m ake u p a l arge par t of th ei r energy

b i ll. I n th e U K m arket f or i nst ance, a 2014 SSE/Yo u gov stu dy showed t hat 30% of the su rveyed

consu mer s t h oug ht th at energy suppl ier profit s represent t h e l argest par t of t heir energy bill 1.

Risi ng retail e lec tri city prices are la rge l y a result of gove r nmen t add-ons, no t o f su ppliers’

ma rg ins . Th ro u gho u t Eu ro pe , a strong an d stead y rise of taxes and charges aim ed at f inancing

Reality govern men tal policies fo r re ne wable e nerg y, ene rg y eff icien c y and social suppor t can clearl y be

obs er ved .

Over the past years, due to the liberalisation of elec tr icity mar kets an d the increase in

co mpet iti on , wh olesale pri ces ha ve decreased and suppliers’ oper atio ns have becom e mo re an d

mo re eff icie nt, dri ving costs down . To day, the e ne rg y compo ne n t o nl y represen ts a b ou t a thi rd

of t he ave ra ge re tail e le c tri cit y bill in Europe.

Su ppl i ers’ margins are - l i ke in any o ther market - l in ked to a n u mbe r of var iables an d the y var y

d epen d ing on the le ve l o f se r vi ce, the type of contract, the pro f ile of cons u mers, e tc . Howeve r,

in th e EU , margins ge n erally re prese n t a ve r y s mall par t of cons um ers’ en erg y bills 2.

Evolution of Household Price Components % of total price paid by Households

Evidence

€cent/kWh 100%

8.5 90%

8.0 80% 40% 36.8%

45%

8.1 7.5 -7%

7.5 7.7 70%

Energy & Supply 7.5

7.0 +47% 60%

Network

6.5 50% 26.7%

6.7 26%

Taxes & Levies

6.0 40% 26%

5.5 30%

5.1

5.0

5.4 +18% 20%

34% 36.5% Energy

5.1 29%

10% Network

4.5 4.6

0% Tax & Levy

4.0

2008 2009 2010 2011 2012 2013 2014 2008 2009 2010 2011 2012 2013 2014

Average EU figures – Source EURELECTRIC 2016

“ Loo king a t t re nds in e ne rgy p rices si nce 2008, the following main conc lus ions can be d rawn:

elec tric it y p rices, but eve n m o re i m p o rta ntly, cost s, continued t o rise overall f or bot h hou se hold s

Quote and ind ustry, desp i te falling o r stable level s of consumpt io n. (…) This rise in p rices is driven

m ainly by inc reases in taxes/ lev ies a nd n e twor k cost s. ”

(Co mmu nication from t he Eu ro pean Co mm i ssi o n o n “ Energy prices and cost s in Europe“,2 014, p.1 3)

“ The result s of t he a nalys is ( ...) su pp ort the conc lu sio ns (. ..) t ha t the energy comp onent of

elec tric it y a nd ga s re ta il p rices has dec lined. RES cha rges, which rep resent a sign ifica nt sha re

of the no n-co ntesta ble cha rges, h ave of f-set t he be n ef it s f rom t he falling energy comp onent in

several ca pital c it ies.”

(2015 ACE R/CE E R Mar ket Monito ring Repo rt , p. 31 )

1“Putting the customer first – How can we drive real consumer engagement with energy “, SSE and Yougov report, 2014: http://sse.com/media/268325/SSE_YouGov-Report.pdf

2 Based on informal discussions with our members, suppliers’ margins are estimated to make up less than 5% of consumers’ bills in most EU member states.

CONSUMERS DON’T SEE THE BENEFIT OF DECREASING

WHOLESALE ELECTRICITY PRICES IN THEIR BILLS

I t i s oft en aarguedrgued tthhat at decreasi

d ecreasing ng whwholesale

olesale prices

prices are

arenot

notpassed

passedt hro

ontuogh consu

t o t he

m ers

cust. Ret

o m ail

er.

elec

R et ait ri

l celect

i ty pri

ri cces

i t y pwou

ri ces

l d wo

al way

u l d salriways

se fast

rise

e r faster

t han t hey

t hanfall

t hey

when

fall co

commpared

pared t o wholesale prices.

Th i s i s oftaccomen acco

p an iedm p an

byied accusat

by accusat

i o ns aga

i onsinst

against

suppliesuppliers

rs f or not

f orbeing

not being

t ransparent

t ransparenten o uen

gho u

and

gh

“and

ri p p“iring

ppoff”

i ng off”

t h ei rt hcust

ei r ocust

m e rosm

. er s

Th ere is a dist in c tio n to b e made b e twe en the total retail price and the en erg y compon en t of the

to ta l re ta il price . T h e fo rm e r in cl udes all cost compon en t s, i.e. en erg y, n etwork , taxes and

Reality cha rges. T he latte r o nl y re f le c ts the costs to sou rce, trade, hedge and su pply electricity from th e

w h olesa le ma rke t i n d i f fe re n t ti m e f ram es (for ward, spot, etc.) , incl u ding balancing costs, as well

as suppl ier o p e ra ti ng cost s (e .g . ma rke ting, customer acquisition , customer care, billing, etc.)

an d su ppl ie r margin .

W h ilst t he deg re e o f co n n e c tio n b e twe en wholesale electricity prices and the en erg y compon e nt

o f re ta il prices d if fe rs b e twe e n co un tries, b oth elemen ts are strongly correlated in competitive

E U re ta il ma rke ts. In additi o n , ma rk-u ps are n ot equivalen t to suppliers’ prof it . Suppliers must

i ndeed cove r t he o p e rati ng costs m e n tion ed above.

Relationship between the wholesale price and the energy component of the retail price and the

Evidence

evolution of the mark-up

120 120

100 100

80 80

euros/MWh

euros/MWh

60 60

40 40

20 20

0 0

2008 2009 2010 2011 2012 2013 2014 2008 2009 2010 2011 2012 2013 2014

Finland Netherlands

120 120

100

100

80

euros/MWh

euros/MWh

80

60

60

40

40

20

20

0

0 -20

2008 2009 2010 2011 2012 2013 2014 2008 2009 2010 2011 2012 2013 2014

Norway Sweden

Mark-up Wholesale Retail

Source: 2015 ACER/CEER Market Monitoring Report

Relationship between the wholesale price and the energy component of

the retail price and the evolution of the mark-up

120 120

100 100

80 80

euros/MWh

euros/MWh

60 60

40 40

20 20

0 0

-20 -20

2008 2009 2010 2011 2012 2013 2014 2008 2009 2010 2011 2012 2013 2014

Belgium Denmark

120 120

100 100

euros/MWh

euros/MWh

80 80

60 60

40 40

20 20

0 0

2008 2009 2010 2011 2012 2013 2014 2008 2009 2010 2011 2012 2013 2014

Italy Portugal

Mark-up Wholesale Retail

Source: 2015 ACER/CEER Market Monitoring Report

“ Cl early, m ark-ups a re no t t h e sa me as p rofit s a s su ppliers have to p ay a ddi tion al op erat io nal

cost s ( e .g. m arke ting , sales, c usto m e r services, overhea ds e tc .) in bri nging a produ ct t o ma rket.”

Quote

(2 015 AC E R / CEER Ma rket Mo ni t o ri ng R epo rt , p.71)

“ As indi ca ted, m ark-u p di f f ere nces ca n be p a rt ially ex pla ined by di ff eren ces i n sup plie rs’

ope rating cost s and/ o r e xpe nditu res i nc urred i n a cquiring a nd reta ining cons um ers (i.e . ma rk-up

is no t f ixed a nd can vary f o r the sa m e supplier dur ing ca mp aigns a nd o ther times). These cost s

may be highe r in count ries ( …) whe re switching rates are re l atively high a nd where sup pliers face

si gni f ica nt co m p e t it io n a nd t h e re fo re have highe r sales, ma rket ing a nd c u st ome r serv ices cost s. ”

(2 015 AC E R / CEER Ma rket Mo ni t o ri ng R epo rt , p.72)REGULATED PRICES ARE A GOOD THING:

THEY PROTECT CONSUMERS

Regul a ted pri ces are often pe rceiv ed as a sh ield agai nst th e m arket . Th ey wo u ld protect

co nsu me r s f rom m arket p ri ces, wh i ch a re t ho u ght t o be inevit ably in creasing.

Regulated e n d- use r prices may prote ct consu mers from increases in en erg y costs in the sho r t

term , bu t th is is o f te n at the ex p ense of n on - regulated customers ( e .g. busin esses) , el ec tri city

Reality com pan ies an d pu bl i c finan ces whe re elec tr icit y tarif f def i cits are in cu rre d. In th e medi u m to

l ong run , regula te d p ri ces – espe cially w hen set b elow marke t costs – are n ot sustai nable an d

harm t h e in te rest s o f a ll co nsum e rs.

Re tail pri ce regulat ion is also a se rious obsta cle to compe titi o n among elec tricit y su ppl y

com pan ies. I t re d uces the in ce n tive on compan ies to b ecome m ore ef f icien t and may stif le the

devel opmen t o f val u e -adde d se r vices such as d ynam i c pricing. In additi on, regulated prices

i mpede co nsu m e rs f rom realising the t rue va l u e of the en erg y they consu me, the refo re

undermin i ng the pote n tial o f d e man d respo nse .

So met im es, reg ulate d pri ces a re de vised to protect the f inanciall y vul n erable. H owever, doing

s o is o f te n co un te rpro d u c tive : it do es not take peo ple o ut of b roader pove r t y; the pricing

met hodol og y lacks transpare n c y ; an d it may in crease en e rg y costs for vul n e rable and

no n-vul n erable co nsum e rs al ike . Othe r more sustainable an d targeted measu res (e.g. via gen eral

taxatio n o r th ro u gh e n e rg y e f ficie n c y fi nan cing schem es) sho uld th erefore b e expl ore d to h el p

Mem ber S tates phase regulate d p rices ou t . In any case , acco rding to the Eu ropean Cour t of

J ust ice, regulate d prices can o nly b e appli ed in exce pt io nal circu mstan ces an d n ot as a main rule

fo r price se tting .

F ina lly, it is im po r tan t to spe cif y that p hasing- ou t regulated pri ces does n ot im ply the end of f lat

tarif fs o r f ixe d pay m e n ts, which su ppliers can still pro pose to th eir custome rs.

I n Bulgaria: capped pr ices fo r ho useh olds are su bsidised by n on - ho usehold custome rs. “The

e ne rgy co mp one nt f or bu si ness c u st o m ers is mu ch h ighe r and co mp e nsates t he losses fro m the

Evidence sale o f e ne rgy t o t he hou se h ol ds.” ( Sou rce: Ene rgy Man agem ent Institu te, Bu lga ri a )

Weighted average electricity prices for regulated market since 1 Nov 2015, eur/MWh

80

75 45%77 76

purchase price 59 eur/MWh from 73

70

the public provider NEK

65

60

55 58

55

50 53

45

40

35

30

households non-households

CEZ EVN Energo-Pro

Source: Energy Management Institute, BulgariaIn Fra nce: pr ices for ho use h olds are still full y regulated and sin ce 2012 the gover n me nt

syste matically has se t re tail pri ces to a dif ferent leve l than the o ne recomm en ded by the natio nal

reg ulato r y au tho ri ty ( NRA) , leadi ng to tarif f def icit s, cou r t rul ings, red tape, additio na l costs and

consu mer co nfusio n .

2013 2014 2015

Recommend on ↗ 11.3% ↗ 1.6% ↘ 0.9%

by NRA

Decision by ↗ 5% as a sh ield against ↗ 2.5%

R egu l ated pri ces are often pe rceived the m arket . Th ey ↗w 2.5%

o u ld prot ect

government

co nsu mers f ro m m arket p ri ces, wh i ch a re perceiv ed as inev it ably go ing u p.

Source: EURELECTRIC table based on figures from Commission Régulation Energie (CRE), France

E xam ples of co un tries w he re su ppl i e rs are n ot a ll owed to cover the ir costs:

Relationship between the wholesale price and the energy component of

the retail price and the evolution of the mark-up

120

120

100 45%

100

euros/MWh

euros/MWh

80

80

60

60

40

40 20

20 0

0 -20

-40

-20 2008 2009 2010 2011 2012 2013 2014

2008 2009 2010 2011 2012 2013 2014

Lithuania Romania

Mark-up Wholesale Retail

Source: 2015 ACER/CEER Market Monitoring Report

“A rt if i c ially low reg u l a ted p rices ( eve n w it h ou t pushing t hem below cost s) l imit m arket entry a nd

in nova tion , p ro m pt co nsum e rs t o dise ngage f rom t he switching process a nd consequently hinder

Quote co m pe titio n in re ta i l ma rke t s. In a ddi ti on, they may inc rease investor uncertainty a nd i mp ac t t he

lo ng-ter m secu rit y o f su p ply. Furt h e rm ore, regu lated pr ices (even when set above cost s) can act

a s a pr icing f ocal p oint whi ch co m p e t ing suppliers a re able to c luster a round a nd at least in

ma rke t s featuring stro ng co ns um e r ine rtia can al so consi de ra bly dilute co mp etit ion. ”

(2015 ACE R/ CEER Market Moni t oring Rep or t , p.87 )

“We n ote t ha t a pr ice cap m ay reduce the in centives tha t ene rgy suppliers have t o inn ovate, for

example in te rm s of t im e-of-u se ta rif f s , as t hey are una ble to cha rge a p rem ium f or new/innova t ive

pro duc t s. Mo reove r, we co nsid e red tha t a pri ce control cou ld de ter e nt ry and growt h by po tential

co m pe tito rs as t h e re wo u ld be li kely t o be insu ffic ient hea droom wit hin the regula ted price level

t o allow t hem t o invest in adve rt i sing and ot her cost s ass oc ia ted wi th c ustom er a cqu isit ion. ”

(UK Compet itio n & Ma rke t s Au t ho rity, Energy m arket investigation, N o tice o f p ossible rem edies, 20 15, p.46 )ELECTRICITY GENERATION AND SUPPLY IN THE

SAME HANDS CAN ONLY HARM COMPETITION

So me st akeh ol der s ex press co ncerns a b out v er t ical i ntegra t io n of generat io n and supply in t he

elec t ri c i ty sect or. Th ey argue t h at su ppliers whi ch are pa r t of a com pany ow ni ng genera t ion

have n o i n cent iv e to off er co nsum er s energy efficien cy se rvices or fle x ible pro du ct s (e.g.

pro d u c t s wi t h h o urly sett lement) si n ce t h ey have an int erest in high wholesale pri ces.

I t is wo r th re calli ng that i n m ost EU co un tries:

Reality Th e n u m b e r o f su ppl i e rs wit h n o gen erat ion asset s is g rowing

I n tegrate d co m pan ies wi th ge n eratio n an d su ppl y ac tivit ies are organ isa ti onall y di vid ed

in to t wo o r m ore com pan ies

I f a co nsu m e r in te reste d i n a spe cific pro d u ct ca n n ot get it f rom it s suppl ier, h e /she

can swi tch to an o t he r supplier

Th e i m pac t of ve r tica l in tegra ti o n o f ge nerati o n an d suppl y on compe titi on was on e of th e issu es

care fully l o o ke d at by th e UK Com pe t iti on & Marke ts A u tho rity (CMA) in it s en erg y mar ke t

invest iga tion 1. T he CMA co ncl u de d that ver ti cal in tegra t ion in the UK does no t ha rm compe titi on

sin ce the re is n o evi de n ce that:

I n de p e n d e n t ge n era tors a re harmed b ecause of ver tically in tegrated su ppliers refusing

to buy fro m them , or buying o n worse te rms

Ve r tically in tegrate d ge n era tors refuse to supply in depen de n t ( n on-ver ticall y in tegrated)

suppl i e rs , o r suppl y the m o n worse terms

Ve r ticall y i ntegrate d supplie rs rais e barri ers to entr y and grow th by ne w su ppl iers by

p re ve n ting t he m to se cu re suf f icie n t wh olesale en erg y

OVERVIEW OF THE ENERGY SECTOR IN INDIVIDUAL EU MEMBER STATES

Evidence

COUNTRY NUMBER OF MAIN POWER GENERATION UTILITIES NUMBER OF ELECTRICITY RETAILERS

Austria 4 152

Belgium 2 33

Bulgaria 5 24

Czech Republic 1 360

Croatia 2 9

Cyprus 1 1

Denmark 2 55

Estonia 1 42

Finland 4 70

France 1 183

Germany 4 >1000

Greece 1 11

Source: European Commission, Country Reports, 2014

1 Energy market investigation, Provisional findings report, CMA, July 2015OVERVIEW OF THE ENERGY SECTOR IN INDIVIDUAL EU MEMBER STATES

Evidence

COUNTRY NUMBER OF MAIN POWER GENERATION UTILITIES NUMBER OF ELECTRICITY RETAILERS

Hungary 4 43

Italy 3 412

Ireland 5 6

Latvia 1 6

Lithuania 6 27

Luxembourg 2 11

Netherlands 4 35

Poland 6 82

Portugal 4 10

Romania 5 54

Slovakia 1 71

Slovenia 2 13

Spain 5 225

Sweden 3 120

UK 7 32

Source: European Commission, Country Reports, 2014

“ We have conside red t h e va riou s m ea ns by whi ch Verti cal Integra t ion (VI) could potentially ha rm

co m pe tition and ca u se ha rm t o co nsu mers. (…) O ur p rovisi on al view is that V I does not h ave a

Quote de trim ental i m p a ct on co m p e t it i o n f o r independent su ppliers a nd ge nera t ors.”

(U K Compe t iti on & Ma rke t s Au t hori t y, Ene rgy mar ket invest igati o n, Notice o f p ossi bl e remedies, 2 015, p.2 31-23 2)LOW SWITCHNIG RATES PROVIDE PROOF

THAT COMPETITION IS NOT WORKING

Sw i tch i ng is often co nsi d ered as th e key i ndicat or of well-fu nct io n ing ret ail m arket s. By

exerc i si ng t h eir ri ght t o swit ch , co nsu mer s pl ace co m pet it ive pressu re o n su pplie rs t o del iver

b est ser v ices at t h e best pri ces. Low swit ching rates are th us seen as a si gn t hat co nsu mers

a re n ot engag ed and th at co mpet i t i on do es n ot work eff ect iv ely.

While switching rates do say something about the level of competiti on in a market, they should

not be considered as the sole ind icator of market functioning. Indeed, consumers may decide not

Reality to switch for a variety of reaso ns, e.g. the y are satisfie d with the contract and qual ity of ser vice

provided by the ir current supplier; their supplier offers a variety of additi onal ser vices that

competitors do not offer; the y perceive the potential gains as too small compared to the ir current

contract; etc.

In addition, consumers some times switch offers or tariffs with the same supplier, which is usually

not counted as switchi ng. Switching may even go down in highly competiti ve markets since it

might no longer offer sufficien t finan cial benefits.

Crucially, whilst real savings are one of the key drivers for switching, it is impor tant to remember

that, on average across Europe, abou t two thirds of the bill are fixed an d devoted to collecting

taxes, policy support costs and network charges. Competition therefore occurs on a small part of

the bill.

Factors preventing electricity and gas consumers from switching – 2014

Evidence

10

9

8

7

6

5

4

3

2

1

Too

0 much

Insufficient Lack of Perceived Too much Satisfaction Loyalty to Lack of Regulated Electricity/gas choice

monetary trust in complex 'hassle' with existing awareness price are not

gain new supplier switching to bother current supplier/brand of choice interesting for

process supplier consumers

1 – not at all important Electricity Gas

10 – very important

Source: 2015 ACER/CEER Market Monitoring ReportWhat factors would motivate you to switch to a new electricity provider?

Better payment options

Base: Respondents in deregulated markets only.

Source: Actionable Insights for the New Energy Consumer, Accenture, 2012, www.accenture.com

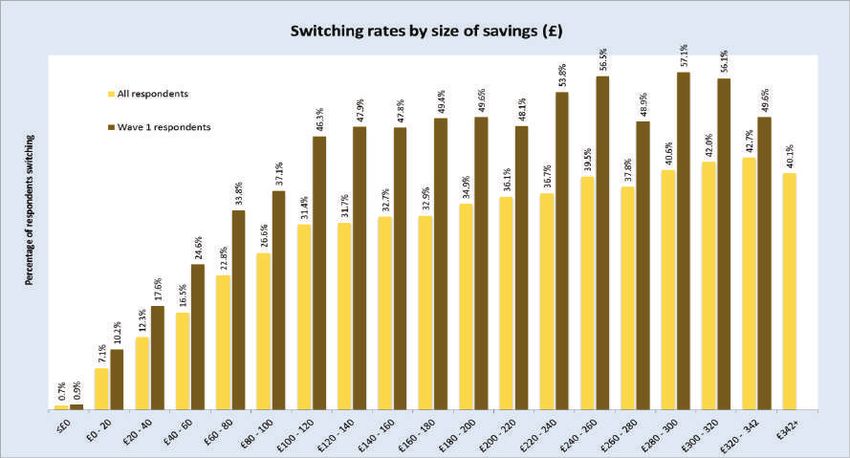

In the UK gains drive switching, but many don’t switch despite large gains

Switching rates by size of saving (£)

57.1%

56.1%

56.5%

53.8%

49.6%

49.6%

49.4%

48.9%

48.1%

47.9%

47.8%

All respondents

46.3%

Wave 1 respondents

42.7%

42.0%

40.6%

Percentage of respondents switching

40.1%

39.5%

37.8%

37.1%

36.7%

36.1%

34.9%

33.8%

32.9%

32.7%

31.7%

31.4%

26.6%

24.6%

22.8%

17.6%

16.5%

12.3%

10.2%

7.1%

0.9%

0.7%

00

20

+

60

40

60

80

40

80

20

42

20

00

0

0

0

00

42

0

0

-3

-6

-3

-4

≤£

-1

-2

-2

-2

-2

-8

-1

-1

-2

-3

-1

-2

-1

£3

80

0

00

0

40

20

40

60

£0

0

20

60

00

20

00

80

£4

£2

0

£6

£2

£3

£8

£1

£2

£2

£2

£1

£1

£2

£3

£1

£1

Source: UK Center for Competition Policy

“ W h ile h i g he r switching ra tes are indi ca t ive o f more comp e titive ma rket s, they s ho u ld be

conside red in co nj u nc t ion wit h ot he r co mp et it io n i ndica t or s. Swi tching ra tes a re, for exa mple ,

Quote so m etimes h igh( er ) du r ing t h e ea rly stages of ma rket o p ening, wh en consum ers first exerc ise

their choice, bu t m ay t h e n stab ili se as a m a rke t ma tures. On the ot her ha nd, i f consumers are

sa tisfied w it h their c urre nt suppl ie r s, t hey may have no rea so n to cha nge su pplier (e.g. t heir

cu rrent su p plie r d elive rs co m p etit ively priced p rodu c t s and g o od quality ser vice) a nd, the ref ore,

sw itching ra tes m ay be l ow eve n in a ve ry co mp et it ive ma rket . ”

(2015 AC E R/ CEE R Ma rket Monito ri ng Repo rt , p.5 7)

“ ( … ) A low switch ing ra te do es no t necessarily imply t hat consum er inv olve me nt is low. The sha re

of co nsum ers re nego t ia t i ng cont ra ct s must al so be taken int o cons ide ra t ion, as well a s t he sh a re

o f consu me rs wh o search fo r be tte r deal s, but su bsequ ently make the in for med dec isi on not to

switch . ( …) Anot he r i mp o rta nt se t o f in forma t ion is t he nu mber of su ccessf ul re negotia t io ns,

whe reby th e cu rre nt su pplie r o f f e r s co m p etit ive p rices and qu alit y ser vi ces t o t he sat isfa c t ion of

bo th e x isti ng a nd new cu st o me rs . ”

( CEE R Pa per o n Well-func tio ni ng reta il m ar ket s, 20 15, p. 24 )TOO MANY OFFERS MAKE THE MARKETPLACE UNNECESSARILY

COMPLEX. ALL THAT CONSUMERS WANT IS ENERGY

Consumers are often por t rayed as b ei ng a like- m inded m o nolit h ic grou p all want ing t he same

pro d uc t . Th eref ore, rest ri c t ing t h e n u mber of off er s is seen a s benefi cial as it w o ul d sim pl ify

t h e ma rket .

Co nsume rs are all diffe ren t: som e wan t the simplest and cheapest prod u cts; others seek to redu ce

t he ir e nviron m e n tal im pac t an d be mo re en erg y ef ficien t or generate their own ren ewable

Reality elec tricity. S o m e e ngage d consu m e rs will wan t mo re complex tari ffs, su ch as Time of Use.

T h e refo re , l im it ing th e n um b er o f o f fe rs - as experim en ted or co nsidered in s om e coun tries - is

no t the rig ht way fo r war d. The b e haviou r of consu mers - a nd their under lying m otivati o ns - are

n otori o usl y dif f icul t to measure , unde rstan d and pre dict . Wh ilst it may h el p reassu re consumers

t hat t h e n u m b er o f op tio ns the y face is n ot in timidating, it may also redu ce in centives for the m

to engage, for exam ple by re d u ci ng dif feren tiati on b etwee n su ppl iers and weaken ing suppl iers’

a bility to tail or p ro d uc ts to the n ee ds an d preferen ces of differen t consu me rs.

Th ere are many ways to he l p co nsu m e rs choos e the prod u cts best su ited to the ir nee ds withou t

hamper i ng in n ovati o n , e.g . p rice com paris on tools, perso nal ised advice by e nerg y su ppl iers o r

consu m er asso cia tio ns, etc.

Three examples of 4-member families with similar appliances, but different lifestyle and load curves

Evidence

Source: Smart Electric Lyon, EDFConsumer segments have different values and preferences when it comes to energy management

Self-reliants

Tech-savvys

14% 13%

Social

independents

Traditionalists 15% 18%

18%

22%

Service-centrics

Cost-sensitives

Base: All respondents

Methodology note: Results based on a conjoint analysis

Source: Revealing the Values of the New Energy Consumer, Accenture 2011, www.accenture.com

The majority of consumers appreciate a company that allows tailoring of products and services

82% 6%

Agree + strongly agree

Disagree + strongly disagree

Base: All respondents

Source: Building a Differentiated Service Experience Strategy, Accenture 2010, www.accenture.com

“ Th e inc reasi ng dive r si t y a nd varie t y o f o ffer s, including t hose wit h ad dit ional ser vi ces, is a si gn

of mo re i nn ova t io n in t h e sec t o r. Such o ffe rs help ra ise consumer inte rest in p rice co mp arison

Quote to ol s and the m a rke t in ge ne ral. ”

(2015 ACE R/C EE R Market Mo nito ri ng Repo r t , p. 50 )

“ We conside r t ha t t h e rest ric t i o ns im p osed by the Re ta il Ma r ket Review (RM R) fo ur- tari ff rule

lim it th e a bil it y o f su ppl ie rs to i nn ovate a nd p rov ide prod uc t s which m ay be beneficial t o

c u sto mer s a nd co m p e t it i o n. This is o f pa rtic ula r concern over the longer term a s RM R ru l es co uld

p ote nti ally st if l e i nnova t io n a ro u nd s m a rt meters. ”

(UK Compe t it io n & Market s Autho rit y, Energy market investigat ion , No t ice o f poss ibl e re medies, 20 15, p 3 1)ELECTRICITY COMPANIES INTENTIONALLY MAKE IT

DIFFICULT FOR CONSUMERS TO COMPARE OFFERS

Supplier s are often t h oug ht to make off er s overly complex so t hat t he m ajorit y of co nsu mers

can n ot under st and and co m pa re t h em. This w o ul d m ake it difficu lt f or co nsum ers t o det erm i ne

i f th ey sh o u l d swi t ch th ei r su ppl ier or n ot

N ot all co nsu m e rs have th e sam e ne e ds an d prio rities wi th regard to e nerg y. It is therefore cru cial

to ensure that the y can f re e l y cho ose f rom a range of prod u cts, ser vices and contrac t types, l ike

Reality in any ot he r mar ke t . T he y sho uld b e able to base t he ir cho ice n ot only on pri ce an d b ra n d, but

a lso o n featu res such as billing types an d f requ en c y, contract du rati on, te rm s of paym en t, ser vice

level , g ran ularit y o f i n fo rmat io n a n d source of elec tricity.

E nerg y com pan i es are wo r king hard to facilitate comparabil ity of of fers e.g. by f in ding im proved

ways to expla in ta r if fs . S im plif ying t he pres en tati on of of fers sho uld however n ot lead to rules

w h i ch re du ce in n ovatio n an d re du ce consum er choice.

Th ere are many ways to h e l p co nsu m e rs cho ose the produ c ts that are b est su ited to t he ir n eeds

wit ho u t ha m pe r ing in n ovat io n:

Pr ice co m pa riso n to ols can he l p consumers unde rstand the charac teristics of en erg y

pro d u c t s by displaying the m i n a clear ma n ne r an d by using sim ple langu age

E ne rg y su ppli e rs a n d En e rg y S e r vice Compan ies (ESCO s) can – an d already d o – provid e

pe rso nal ise d advice to th e i r custome rs, e.g. what is the cheap est a nd m ost appro priate

ta rif f co nside ring the i r si tu a tio n an d consu mpt ion p ro file

Regulato rs , busin esses a n d co nsu mer asso ciations ca n wo rk toge ther on co nsu mer

i nfo r mati o n an d e du cat io n to im prove understan d ing a n d engagem en t in retail ene rg y

mar ke ts

I mprove d transpar e n c y in price an d o f fers is also l in ked to bet ter regulati on . Pol icy-makers n eed

to assess the im pac t o f cu rre n t legislative pr ovisions regulating the presen tation of prices an d

o ffe rs to str ike a balan ce b e twe e n sim pli cit y an d un de rstan dabil it y.

Many suppliers display their offers on a like for like manner as much as possible:

Evidence

Engie/Electrabel - Belgium EDF energy – UKIn Februar y 2016 EUREL ECTRIC co-signe d a statement wi th Eurogas and the European

consumer’ s organ isati on BEUC through w hich su pplie rs commit to fur th er suppo r t the

compara bility of energ y offers by providing 5 key elements to consumers in one place ,in a

short, easily understandable, prominent and accessible manner:

http://www.eurelectric.org/media/263669/joint_statement_-_improved_

comparability_of_energy_offers_-2016-030-0116-01-e.pdf

Pri ce co mpa riso n websites a re available in most EU coun tries:

Availability of price comparison websites

Country Electricity Gas

AUSTRIA http://www.e-control.at/haushalts-tarifkalkulator http://www.e-control.at/haushalts-tarifkalkulator

BELGIUM http://www.brusim.be/ http://www.brusim.be/

BULGARIA Information from NRA Information from NRA

CROATIA https://kompare.hr/ Supplier’s site: http://www.gpz-opskrba.hr/

CZECH REPUBLIC http://kalkulator.eru.cz/ and http://www.cenyenergie.cz http://www.cenyenergie.cz

CYPRUS Information from NRA n.a.

DENMARK http://www.elpristavlen.dk/ http://gasprisguiden.dk

ESTONIA https://minuelekter.ee/calc Supplier’s site: http://www.gaas.ee

FINLAND http://www.sahkonhinta.fi/ http://www.gasum.fi/Yksityisille/Kodin-lammitys/hinnastot/

Supplier

FRANCE

s are sowww.energie-info.fr

m et i mes said to make off ers overly co mwww.energie-info.fr

plex so t h at the maj orit y of co nsu mers

can n

GERMANY

ot u nder st and and com

www.verivox.de

pare th em, m aking it di ffi cu lt to det erm i ne i f t hey sho u l d swit ch

www.verivox.de

su ppl ier or n ot . NRA

GREECE http://www.aerioattikis.gr/default.aspx?pid=34&la=1&artid=135

HUNGARY Information from NRA and other offers from 3 suppliers http://www.vasarlocsapat.hu

IRELAND http://www.bonkers.ie/compare-gas-electricity-prices/electricity/ http://www.bonkers.ie/compare-gas-electricity-prices/gas

ITALY http://trovaofferte.autorita.energia.it/ http://trovaofferte.autorita.energia.it/

LATVIA Information from NRA Information from NRA

LITHUANIA Information from NRA Information from NRA

LUXEMBOURG www.calculix.lu http://www.ilr.public.lu/gaz/fournisseurs/

MALTA Information from NRA n.a.

NETHERLANDS http://www.energieleveranciers.nl/energie-vergelijken http://www.easyswitch.nl/energie

NORTHERN IRELAND http://www.consumercouncil.org.uk/energy/price-comparison-/ n.a.

NORWAY http://www.konkurransetilsynet.no/en/Electricity-prices/Check- power-prices/ n.a.

POLAND http://ure.gov.pl/ftp/ure-kalkulator/ure/formularz_kalkulator_html. php Information from NRA

PORTUGAL http://www.erse.pt / Simulador de Preços de Energia Elétrica http://www.erse.pt / Simulador de Preços des Gas Natural

ROMANIA Information from NRA Information from NRA

SLOVAKIA http://www.urso.gov.sk:8088/CISRES/Agenda.nsf/ KalkulackaElektrinaNewWeb http://www.urso.gov.sk:8088/CISRES/Agenda.nsf/ KalkulackaPlynNewWeb

SLOVENIA http://www.agen-rs.si/primerjalnik/index.php?/kalkulatorelektrika/ http://www.agen-rs.si/primerjalnik/index.php?/kalkulatorplin/

SPAIN http://comparadorofertasenergia.cnmc.es/comparador/ kalkulator/action/korak2/redirected/1/

http://comparadorofertasenergia.cnmc.es/comparador/

SWEDEN http://www.ei.se/elpriskollen/ http://www.energimarknadsbyran.se/Gas/Dina-avtal-och- kostnader/Gaspriskollen/

Source: ACER, November-December 2014

“ Th e Forum welco m es t he j o i nt state me nt o f BEUC , EUR E LECTR IC a nd EU R OGAS o n imp roved

co m parabil it y o f e ne rgy o f f ers t o allow consumer s to ma ke choices that best m eet their needs,

Quote and en co urag es rel evant m a r ke t a c t o rs t o f ollow these princ iples . ”

(Conclu si ons fro m t he 8th EU Cit izens ‘Energy Fo ru m, 2016)

“ Th e inc reasi ng dive r si t y a nd varie t y o f o ffer s, including t hose wit h a d dit ional ser vi ces, is a sign

of mo re i nn ova t io n in t h e sec t o r. Such o ffe rs help ra ise consumer inte rest in p rice co mp arison

to ol s and the m a rke t i n ge ne ral. ”

(2015 ACE R/C EE R Market Mo nito ri ng Repo r t , p. 50 )CONSUMERS ACROSS EUROPE ARE NOT

SATISFIED WITH ELECTRICITY COMPANIES

Th e Eu ro pean Com m i ssi on ’ s co nsu m er scorebo ard regul arly pictures t he energy sector as one

of th e wor st per f or m i ng f or co nsu m e r s at EU level.

We do a cknowle d ge that su ppl ie rs, n e w and old, have had a l ot to learn and are still learning.

Clearl y, co m pan ies m ust fu r the r wo r k to en ha n ce consu mers’ trust – in pre-sale areas like

Reality marke ti ng an d co n tra c ti ng a n d i n post-sale operations like consu mer satisfaction , billing, and

d ispu te resol utio n – an d to design o f fers that respon d to consu mers’ n eeds.

Howe ve r, we als o th i n k i t is fa i r to obser ve that:

Th e le ve l o f co nsum e r sa tis fa c tion is quite high a n d is improving in several countries,

e .g . Be lgiu m , Finla n d , Fran ce , the Net herlands, Nor way, Sweden , the UK, etc.

Ma ny co nsu m e rs ’ co m pla i n t s a re a b o u t i n creasi ng p r i ces – s o m e t h i ng su ppl i e rs a re

ma rgina ll y resp o nsible fo r as rising prices are mainly du e to govern men t add- ons (strong

r ise o f taxes a n d su pp o r t costs for ren ewable en erg y, social suppor t and en erg y

effici e n c y )

Many o p ti o ns wh ich will all ow suppliers to improve the consu mer’s experien ce are n ot

ye t in pla ce , e .g. s mar t m e te rs, bill ing on a ctu a l consu mption , etc.

Consumer satisfaction with electricity suppliers in Sweden, Finland and Norway:

Evidence

76

74

72

% 70

68

66

64

2011 2012 2013 2014 2015

Sweden Finland Norway

Source: EPSI Rating Danmark, 2015

Consumer satisfaction with electricity suppliers in Belgium (Flanders):

Complaints about suppliers Suppliers with 5 VREG stars for

to Ombudsman quality of service

80%

63%

6.759

- 41% 3.982

20%

Complaints

2012 2014 2012 2013 2014

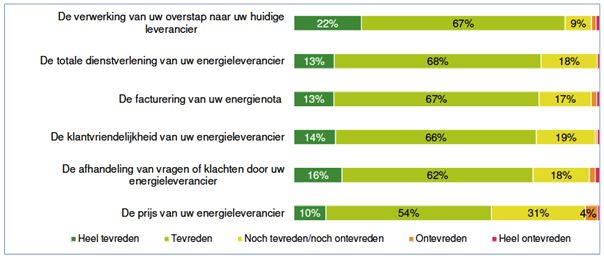

Source: Ombudsman Energie, Activiteitenverslag 2012, 2013, 2014 VREG service checks, 12 January 2015, Accenture analysisConsumer satisfaction with the services provided by their energy supplier in the Netherlands:

Switching 22% 67% 9%

Overall service 13% 68% 18%

Energy bills 13% 67% 17%

Customer-friendliness of 14% 66% 19%

your energy supplier

Handling questions 16% 62% 18%

or complaints

Price 10% 54% 31% 4%

Source: Consumentenmarkt elektriciteit en gas eerste helft 2015 (National Regulatory Authority)

Most household customers are not yet equipped with smart meters for electricity – 2014 (%)

100

90

80

70

60

%

50

40

30

20

10

0

PL

NL

AT

CY

LT

PT

MT

IT

BG

DE

GR

HR

HU

IE

LU

RO

SK

LV

FR

BE

CZ

GB

NO

ES

SI

DK

EE

FI

SE

2013 2014

Source: CEER Database, National Indicators (2014–2015).

“ The most co m m o n com plai nt s by ho u se hold c ust omers a re rela ted to p rice, co nt ra ct or billing

issu es (…) . T his is tru e f o r t he el ect ricit y as well as for the ga s reta il market.”

Quote

( 2015 AC E R/CE E R Mar ket Mo nito ring Rep ort , p. 13 3)SUPPLIERS ARE AGAINST ENERGY EFFICIENCY,

SELF-GENERATION AND ENERGY COOPERATIVES

Su p pl ier s a re oft en t h o u g ht t o o ppose t he develo pment of energy efficiency, self-generat ion

and ene rgy co ope rat iv es because i t wo u ld unde rm ine t heir business m o del.

Su ppl iers’ traditi o nal co re busi n ess is progressivel y changing and their poten tial growth

o ppo r tun i ty pre cis e l y l ies in a n um b e r of n ew produ cts a n d ser vices for consu mers. Suppliers

Reality in creasi ng l y o f fe r n e w val u e packages aroun d deman d response, sel f-gen eration , batter y

sto rage, en e rg y e f f icie n c y in cl uding building ren ovation , as well as quick win sol u tions like smar t

t h erm osta ts . T h e y a re at th e fo re f ro n t of in n ovation in many European marke ts, sometimes taking

u p th e role o f En e rg y S e r vice Co mpa ny (ESCO) or aggregator, sometimes par tn ering with them .

Su ppl iers a ls o have co m m e rcial in ce n tives to devel op en erg y ef f icien cy ser vices (e.g. interac tive

tools to h el p co nsum e rs regulate t he i r consu mption ) which are a means to reduce peak load

cu r ves and to make ro o m fo r n e w de man ds for elect ricity such as electric vehicles.

Many su ppl ie rs su pp o r t t heir custo mers who want to invest in jointly-own ed photovoltaic

sch emes o r wi n d fa rm s . T h e y ca n ta ke on the constru ct ion and opera ting risks con n ected to the

p ro du c tio n o f e le c tr i cit y, wh ile all owing people to buy stakes in the projects, inciden tally

in creasi ng th e acce p tan ce o f thes e te chnol ogies.

Fina ll y, so m e su ppl i e rs su pp o r t co nsu m ers who wa n t to set up an en erg y cooperative, by e.g.

ma na gi ng all adm in istra ti ve p ro cesses and fina n cial f l ows, hel ping them bu ild the ir own green

en erg y su ppl y ste p by ste p, a n d backing them u p with 100% ren ewable electricity as l ong as

needed.

Utilities’ traditional core business is shrinking, but new growth areas can offset the decline

Evidence

European industry EBIT, EUR billions

45%

138

114 14

1 6 6

Downstream

31

T&D 2 25

RES 16 30

Conventional

generation 3 55 49

2012 Decline in Growth in RES Downstream 2020

conventional traditional

generation T&D

1 Includes power sales and new downstream (distributed generation and storage, electric vehicle infrastructure, new downstream products

and services, power flow optimization)

2 Includes smart grids

3 Assuming no change in commodity prices vs. today

Source: McKinsey Industry VisionExamples of innovative services by suppliers are featured in EURELECTRIC’s innovation website

45%

Source: EURELECTRIC - http://www.eurelectric.org/innovation/

“ Ove r th e la st f ew yea r s, re ta i l e nergy ma rket s have w it nessed inc rea sed eviden ce o f p ro duc t

inn ova tio n o f f ered by bo th well-esta bl ished sup pliers a nd by smaller niche pl ayers. ( …) T he

Quote in nova tio n in re tail p ro d u ct s may i nc lude cha ra c ter ist ic s such a s co nt ra c t dura tio n, price

p rese rva tion p e rio ds, dual-f uel o f f e rs, a dd it io n al ser vice p rovisi on o r re newa bl e/green features.

Th ese innova t ive p rodu ct s o f f er m o re choi ce t o consumer s in a n indust ry tha t wa s once considered

to be co mple tely h o m o ge neo u s . ”

(ACER/C EE R 2014 Market Mo nito r i ng Repo r t , p. 66 )

“ In so m e cou nt r ies ( e .g . Great Br itain a nd Irela nd), elec t ric it y a nd ga s su ppliers a re al so

e x panding t heir bu siness a reas a nd m ovi ng towa rds becoming ‘ energy ser vi ce p roviders’. Most

su ppl ier s o f f e r h o m e i nsu lat io n , bo ile r insura nce a nd s ma rt m etering produ c t s a nd serv ices.

A no th e r em e rgi ng m arke t is t h a t o f m i cro-genera t io n. Most su pplie rs offe r p roduc t s and se rvices

in th i s area , inc ludi ng install at io ns of technolog ies such a s Ph ot ovoltaic s (P V), wind, sola r

th e rm al, biom a ss a nd hea t p u m ps. B o iler installat io n and ot her t y p es of home im proveme nt , su ch

a s insu la tio n a nd bo i le r m a inte na nce , a re al so o ffered by many sup plie rs. Some supplie rs al s o

o f f er plu m bing, dra inage a nd el e c t rical i nsurance (… ). A limited n u mbe r of sup plie rs al so o ffer

ph o ne a nd/o r bro adba nd se rv ices. ”

(2014 ACE R/C EE R Market Mo nito ri ng Repo r t , p. 67)SUPPLIERS INTENTIONALLY MAKE BILLS

COMPLEX TO CONFUSE CONSUMERS

Energy b i ll s are often repor ted t o be t oo com plex . Many co nsum ers – and co nsu m er associa t ions

– th i n k t h ei r su p pl ier s are respo nsible f or t h at . As t he situ at io n do es n ot seem t o im prove,

so me su ggest st andardi sing t h e b ill’ s f ormat .

Su ppl iers are in co nstan t dia l ogu e with their custome rs (e.g. consu mer pa n els) a nd they are

taking steps to make e n e rg y bills clearer 1.

Reality

Howe ve r, in m ost EU Me m b e r States, bills are heavil y regulate d. While many co nsu mers in d ee d

com plain t hat the re is to o m uch in fo r mation o n their bills, ma king t hem diff icult to read, suppl iers

a re of ten n ot all owe d to sim plif y o r i m prove t hem.

Before co m ing u p wi th m o re regulation , polic y- makers sho uld assess the impac t of cu rren t

Euro pean an d national legislative provisio ns regula ting th e presen tati on of bills. The re would

be m eri t i n e n co u ragi ng m ore e vi de n ce and principl e- base d regula ti on rather than dictati ng the

fo rmat an d co n te n t o f bills .

Features of electricity bill mandated by regulation in France (in yellow)

Evidence

20160115_003215_00014_HP0_PAR011_222

NOUS CONTACTER

h

Document à conserver 5 ans Page 1/4

N° client : 6 007 344 399 Document à conserver 5 ans Page 2/4

Identifiant Internet :

SBOUTHEON@GMAIL.COM

Détail de la facture du 14/01/2016 N°35005875346

G Par Internet

edf.fr

sur Smartphone et Tablette

I Votre contrat Electricité

Télécharger l'appli mobile EDF&MOI

BOUTHEON SOIZIC

Nom, Prénom

"Tarif Bleu" - 12 kVA - Option Heures Pleines/Heures Creuses - Compteur électronique n°141

mail : serviceclient@edf.fr

M. Adresse

DAGNICOURT MARC

de facturation Horaires heures creuses - 22H30-6H30 - (peuvent varier de quelques minutes)

F Par téléphone 67 ROUTE DE FONTAINEBLEAU

Du lundi au samedi dès 8h et jusqu’à 21h 91490 MILLY LA FORET

09 69 36 66 66 Consommation

EDF Société anonyme au capital de 930 004 234 € Siège social : 22-30 avenue de Wagram 75382 Paris Cedex 08 - France R.C.S. PARIS 552 081 317 N.I.T.V.A. FR 03 552 081 317

(Service gratuit + prix appel)

Régularisation tarifaire Base - 06kVA - du 30/07/2013

D Par courrier 9 0,0041 0,04 19,6%

au 31/07/2013 (1)

EDF SERVICE CLIENTS TSA 20012

TA

ERDF ERDF

41975 BLOIS CEDEX 9

Base - 06kVA - du 20/06/2014 au 24/09/2014 16851 18374 1523 0,0883 134,48 20,0%

B Nos boutiques

Retrouver la boutique la plus proche de ERDF ERDF

chez vous sur boutiques.edf.com K Facture du 14/01/2016 Heures Creuses - 12kVA - du 25/09/2014 au

0 1230 1230 0,0620 (2)

76,24 20,0%

Urgence dépannage Electricité (ERDF) N° 35 005 875 346 Montant total 22/12/2014

A

09 726 750 91 (Service gratuit + prix appel) 2 015,02 € Heures Pleines - 12kVA - du 25/09/2014 au

0 3862 3862 0,1014 (3) 391,52 20,0%

Electricité (relevé ERDF) 2 606,10 € TTC 22/12/2014

A

A V T € 0 6 , 6 9 4 ERDF ERDF

B Lieu de consommation Paiements déjà effectués -1 087,68 € A payer avant Heures Creuses - 12kVA - du 23/12/2014 au

BRT DE CHANTIER le 29/01/2016 1230 4855 3625 0,0623 225,84 20,0%

67 ROUTE DE FONTAINEBLEAU

19/06/2015

C T T e r u t c a F € 2 0 , 5 1 0 2

AT

91490 MILLY LA FORET Heures Pleines - 12kVA - du 23/12/2014 au

C

3862 14586 10724 0,1019 1 092,78 20,0%

19/06/2015

Titulaire du contrat

Mme BOUTHEON SOIZIC

Total Consommation (dont acheminement 665,34 €) 20973 1 920,90

M. DAGNICOURT MARC f Les prochaines étapes Prix €HT/mois Montant €HT TVA

LI

Votre contrat • Prochaine facture vers le 19/06/2016. Abonnement

N° de client : 6 007 344 399

N° de compte : 4 02 4 010 586 041 • Prochaine relève ERDF vers le 19/06/2016. Déduction - Base - 06kVA - du 20/06/2014 au 20/07/2014 5,56 -5,56 5,5%

(numéro à transmettre pour le règlement de

vos factures) Régularisation tarifaire Tarif Bleu 06 kVA Base - du 30/07/2013 au 31/07/2013 (1) 0,27 0,01 5,5%

Electricité "Tarif Bleu" Base - 06kVA - du 20/06/2014 au 31/07/2014 5,56 7,68 5,5%

P

• Point de livraison (PDL) : Base - 06kVA - du 01/08/2014 au 24/09/2014 5,56 10,05 5,5%

IC

N° 22 251 085 317 651

• Puissance : 12 kVA Heures Pleines/Heures Creuses - 12kVA - du 25/09/2014 au 31/10/2014 13,01 15,83 5,5%

• Heures Pleines/Heures Creuses

22H30-6H30 Heures Pleines/Heures Creuses - 12kVA - du 01/11/2014 au 19/06/2015 13,28 100,86 5,5%

U

Heures Pleines/Heures Creuses - 12kVA - du 20/06/2015 au 20/07/2015 13,28 13,28 5,5%

Total Abonnement (dont acheminement 102,31 €) 142,15

Conso kWh Prix du kWh Montant €HT TVA

D

Taxes et Contributions

Taxe sur la Consommation Finale d'Electricité (TCFE) 20964 0,00618 (5) 129,63 20,0%

PL

Contribution au Service Public d'Electricité (CSPE) 20964 0,01840 (4) 385,76 20,0%

C Comment payer ? Contribution Tarifaire d'Acheminement Electricité (CTA) 27,66 5,5%

Par Internet : choisir « Payer ma facture ». Total Taxes et Contributions 543,05

Par téléphone : choisir « Payer ma facture ».

Par TIP : détacher le TIP et suivre les instructions sur l’enveloppe jointe.

Total Electricité hors TVA 2 606,10

Par chèque : à l’ordre d‘EDF en joignant le TIP.

En espèces : dans un bureau de poste avec votre facture. En conclusion : situation de votre compte depuis le démarrage de votre échéancier

H Tenez compte des délais postaux : la date de paiement sur votre facture est celle à

laquelle nous devons avoir reçu votre règlement. Total facture hors TVA 2 606,10 €

U

TVA 19,60 % sur un montant total de 0,04 €

g Pour vos prochaines factures, simplifiez-vous la vie !

TVA 20,00 % sur un montant total de 2 436,25 €

0,01 €

487,25 €

TVA 5,50 % sur un montant total de 169,81 €

Montant total

Payez par prélèvement automatique mensuel ou bimestriel. 9,34 €

Connectez-vous dès maintenant sur votre espace Client.

Total facture TTC 3102,70 €

2 015,02 €

TTC

D

Paiements déjà effectués -1087,68 €

h

Document à conserver 5 ans Page 3/4

IS 552 081 317 N.I.T.V.A. FR 03 552 081 317

Document à conserver 5 ans Page 4/4

A Evolution de votre consommation facturée en kWh

Relevé ERDF Relevé Client Relevé estimé Consommation

(1) Régularisation tarifaire : le montant de cette régularisation est calculé en application de l'arrêté du 28 juillet 2014 relatif aux Tarifs Réglementés de Vente de

l'électricité qui modifie rétroactivement les barèmes de prix pour la période comprise entre le 23 juillet 2012 et le 31 juillet 2013. Le prix unitaire appliqué correspond à la

différence entre le prix publié dans le nouvel arrêté et celui qui vous a été précédemment facturé. Pour plus de détails, connectez-vous sur regultarifpart.edf.com.

I Votre consommation en Electricité Le montant total de votre régularisation tarifaire, pour la période du 30/07/2013 au 31/07/2013, est égal à 0,07 € HT pour la consommation (17 kWh) et 0,02 € HT pour

l'abonnement. Il n'est soumis qu'à la TVA. Selon votre situation contractuelle et votre rythme de facturati on, ce montant vous sera facturé sur une ou plusieurs lignes

EDF Société anonyme au capital de 930 004 234 € S i è g e s o c i a l :22-30 avenue de W agram 75382 Paris Cedex 08 - France R.C.S. PAR

(identiques) en une ou plusieurs fois. - (2) Evolution au 01/11/2014 : sur les 1230 kWh facturés, 305 kWh à 0,0610 €/kWh et 925 kW h à 0,0623 €/kWh - (3) Evolution au

01/11/2014 : sur les 3862 kWh facturés, 960 kWh à 0,0998 €/kWh et 2902 kWh à 0,1019 €/kWh - (4) Evolution au 01/01/2015 : sur les 20964 kWh facturés, 7680 kWh à

0,01650 €/kWh et 13284 kWh à 0,01950 €/kWh - (5) Evolution au 01/01/2015 : sur les 20964 kWh facturés, 7680 kWh à 0,00317 €/kWh et 13284 kWh à 0,00319 €/kWh

Taxes et contributions

HP 10724

CTA électricité : 27,04% de la part acheminement de l'abonnement

HP 3862

HC 3625

Pénalités de retard

HC 1230

TA

De plus, conformément aux conditions générales de vente, à défaut de paiement intégral dans le délai prévu pour leur rège l m ent, les sommes dues seront

majorées de plein droit de pénalités de retard calculées surla base d’ une fois et demie le taux d’intérêt légal appliqué a

u montant de la créance TTC. Le montant

de ces pénalités ne peut être inférieur à 7,50 €.

de Sep14 à Déc14 de Déc14 à Jun15

Mentions relatives à votre contrat d'électricité :

Résiliation possible du contrat à tout moment sans préavis n i pénalité.

Offre à tarif réglementé.

TA

A

Origine 2014 de l'électricité : 82,2 % nucléaire, 13,6 % renouvelables(dont 7,9 % hydraulique), 1,6 % charbon, 1,3 % gaz, 1 % fioul et 0,3 % autres. Indicateurs

d'impact environnemental sur www.edf.com

E Des infos à portée de main ! Vous souhaitez faire une réclamation écrite ?

Vous pouvez vous adresser à EDF, qui met à disposition un parcours en trois étapes, pour vous assurer une réponse dans les meilleurs délais :

C

Des explications concernant les taxes et contributions sur · Etape 1 : vous adressez votre réclamation par internet à particulier.edf.fr ou par courrier à EDF Service Client - TSA 20012 - 41975 BLOIS CEDEX.

taxes.edf.com · Etape 2 : la réponse apportée par le Service Client ne vous satisfait pas, vous pouvez alors envoyer votre réclamation par internet à particulier.edf.fr ou par

courrier à EDF Service Consommateurs - TSA 20021 - 41975 BLOIS CEDEX 9.

Mieux comprendre les détails de votre facture sur

· Etape 3 : vous restez en désaccord avec la réponse du Service Consommateurs, vous pouvez dans ce cas solliciter le Médiateur EDF par internet sur

facture.edf.com

https://mediateur.edf.fr ou par écrit au Médiateur EDF - TSA 50026 - 75804 PARIS CEDEX 8.

A

LI

Etre informé sur les prix sur

infoprix.edf.com Si dans un délai de deux mois, votre réclamation écrite auprès d'EDF n'a pas permis de régler le différend, en cas de litige lié à l'exécution du contrat, vous pouvez

saisir le médiateur national de l'énergie sur www.energie-mediateur.fr ou par écrit au Médiateur national de l'énergie - Libre Réponse n°59252 - 75443 PARIS CEDEX 9.

Tout sur vos démarches, vos droits et les économies d'énergie : www.energie-info.fr, le site d'information des pouvoirs publics,

C

A Pour votre information Pour de plus amples informations, reportez-vous aux Conditions Générales de Vente ou rendez-vous sur cgv.edf.com

P

Prix et Réglementation

Electricité : Vos Conditions Générales de Vente ont été modifiées au 15/07/2015. Sur décision des pouvoirs publics, le Tarif Réglementé de Vente a évolué au

01/08/2015. Le montant de la CTA a évolué au 01/08/2015. Selon la réglementation en vigueur, les montants de la CSPE et des TCFE ont évolué au 01/01/2016. Plus

d'information sur le site edf.fr

Nouveau taux de taxe : TCFE 0,0062€/kW h à compter du 01/01/2015

U

LI

TRE0240240105860410000002015024O Q

D

TIPS€PA

ICS : FR47EDF001007 Marc DAGNICOURT

Montant en euros

RUM : TIP044024010586041350058753461401 M. DAGNICOURT MARC

67 ROUTE DE 2 015,02

P

FONTAINEBLEAU 91490

Flashez-moi pour MILLY LA FORET

payer en ligne

IBAN : FR76 3000 3013 4700 0501 0065 149

EN CAS DE MODIFICATION JOINDRE UN RELEVÉ D'IDENTITÉ BANCAIRE

Identification

règlement

4 02 4010586041 35005875346

DATE SIGNATURE

U

EDF

Q

Mandat de prélèvement SEPA ponctuel : en signant ce formulai re de mandat, vous autorisez EDF à envoyer TSA 60002

ces instructions à votre banque pour débiter votre compte, e t votre banque à débiter votre compte

conformément aux instructions de EDF. Vous bénéficiez du dro it d'être remboursé par votre ba nque selon les

75937 PARIS CEDEX 19

conditions décrites dans la convention que vous avez passée avec elle. Une demande de remboursement

doit être présentée dans les 8 semaines suivant la date de déb it de votre compte pour un prélèvement

autorisé. Vos droits concernant le présent ma ndat sont expl iqués dans un document que vous pouvez obtenir

D

auprès de votre banque.

Le présent document a valeur de mandat de prélèvement SEPA ponctuel. Votre signature vaut

autorisation pour débiter, à réception, votre compte pour le montant in diqué.

350058753469 MARC DAGNICOURT 30003013470005010065149

070150140117 41402401058604135005875346680104 201502

Source: EDF

1 See for instance: http://sse.com/newsandviews/allarticles/2016/02/new-sse-bill-design-aims-to-end-energy-bill-confusion/Information suppliers must provide on household customer bills in Member States (MSs) – 2014 (number of countries)

Evidence

Single point of contact

45%

Customers’s rights regarding dispute settlement

Switching infromation

Payment modalities

Suppliers’ details

DSO details

Consumption period

Breakdown of price

Actual consumption

Estimated consumption

Duration of contract

Energy mix

Price comparison tools

Other

0 5 10 15 20 25 30

Number of jurisdictions

Electricity Gas

Source: CEER Database, National Indicators (2014–2015), figure 55

“ Mem ber Sta tes h ave p u t in place regu la t io ns o n t he dist r ibut io n o f informa t i on t o consu mers

on energy related t o p ic s, su ch a s ( …) info rma t io n p rovid ed on bill s a nd billing in forma tion ba sed

Quote o n ac tu al consu m pt io n. ”

(2015 ACER/CE ER Mar ket Monit o ring Repo r t , p. 1 2 8)

“ I n m ost MS s, m a ny o f t he in f o rm a t i o n ele m e nt s li sted in figu re 5 5 a re inc lu ded o n t he bill.

G iv ing i nf o rma t ion t o consu m e r s i n an easy a nd u nder standa ble way is imp orta nt . Yet , the da nge r

pe rsist s tha t prese nt ing t o o m any di ff e rent pieces o f informa t ion o n t he bill m ight ma ke it less

accessible t o t he co nsu me r, beca use o f t he plet hora of de ta il s which a re all prese nted at on ce a t

long inter val s. Whe n co m m unicat ing w ith co nsumers, o t her co mmunica tion cha n nel s m ay be at

least as ef f ic ie nt as t h e bill, su ch a s reg ul a r ema il or t he consumer’s ‘my pag e ’ on t he su p plier

and/or DSO websi te . ”

(2015 ACER/CE ER Mar ket Monit o ring Repo r t , p. 1 2 5)

“ We wo uld urge ( t he Co m m i ss ion ) t o cons ide r ca refully the level o f p resc ript ion in rela t ion to

th e co ntent or f o rm a t o f bill s and o the r c ust omer co mmu n ica tions. Anecdo tal evidence sugg est s

th a t co nsu m e r s al rea d y receive a lot o f informa t io n and tha t t his ca n lead t o less ra t her t ha n more

e ngage me nt in ce rta in circum stances. Deta il ed req uirement s can al so reduce t he scop e for

in n ova ti o n a m o ng su p plie rs and coul d become o utdated quickly (e.g. as m ore p eople opting for

elec tro nic billing ) . ”

(C E ER Response to Euro pean Com missi o n Pu bl ic Co nsultatio n

o n th e Rev iew o f Directive 201 2/27/ EU o n Energy Effi c ien cy, 2016, p. 2)© photo: fotolia Union of the Electricity Industry - EURELECTRIC Boulevard de l’Impératrice, 66 boîte 2 T.: + 32 (0)2 515 10 00 - F.: + 32 (0)2 515 10 10 1000 Brussels website: www.eurelectric.org Belgium twitter.com/EURELECTRIC EU Transparency Register number: 4271427696-87

You can also read