Resource Assessment for County Donegal - Donegal Fuel Resource Survey and Biomass Demand - November 2012 - raslres

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Resource Assessment

for County Donegal

Donegal Fuel Resource Survey and Biomass Demand

November 2012

SWEDEN

NORWAY

ICELAND

FAROE

ISLANDS FINLAND

SCOTLAND

NORTHERN DENMARK

IRELAND

Western

Region

IRELAND

UNITED

KINGDOWM

What is RASLRES?

RASLRES (Regional Approaches to Stimulating Renewable Energy Solutions) is an EU bioenergy

project led by the WDC and funded under the Northern Periphery Programme of INTERREG IVB. The

total project budget is €2.8 million over three years. Commencing in September 2009, RASLRES

aims to increase the uptake of locally produced bioenergy solutions through the development and

implementation of market development models. The project focus is on pilot actions in regard to

wood energy, energy crops and marine biomass fuels.

RASLRES is an international partnership which includes:

gg Western Development Commission – Ireland

gg Action Renewables – Northern Ireland, UK

gg Environmental Research Institute, North Highland College – Scotland

gg Municipality of Norsjö – Sweden

In the Western Region RASLRES supports the growth of the wood energy sector by delivering

practical services to market players and by informing policy development. During 2010 and 2011

RASLRES delivered a range of actions with a focus on selected pilot projects. The project aims to:

gg build sustainable local loops of wood fuel supply and demand via new (or existing) wood fueled

boilers

gg offer best practice approaches to support industry development

gg help build critical mass and scale in the wood energy sector of the region

gg support investment plans and help secure project finance

RASLRES adopts a full supply chain approach - looking at the energy chain from supply (i.e. fuel

producers / processors) to demand (i.e. energy users). The services to the wood energy sector include:

gg provision of a range of impartial technical and business advisory support services to selected

clients progressing wood energy projects in the region

gg generation of market information and intelligence to support the sector e.g. resource

forecasting from private sector forestry, assessment of energy crop potential, technical and

business case studies

gg accessing of international expertise and facilitation of networking with EU markets

Disclaimer: All reasonable measures have been taken to ensure the quality, reliability, and accuracy of the information in this report. This report is intended

to provide information and general guidance only. If you are seeking advice on any matters relating to information on this report, you should contact the

WDC with your specific query or seek advice from a qualified professional expert.

Table of

Table of Contents

Table of Contents

Introduction 3

The Forest Estate 3

The Donegal Forest Estate 4

Age Profile 5

The Resource 6

Regional and County Energy Balance and the Requirement for Renewable Energy 8

Barriers to Market Development 13

Proposals for CHP and Bio Refinery - Market Potential and Impacts 17

Meeting the Market Demand 19

Importation 20

Conclusions 21

Resource Assessment for County Donegal Donegal Fuel Resource Survey and Biomass Demand November 2012 1

2 Resource Assessment for County Donegal Donegal Fuel Resource Survey and Biomass Demand November 2012

Introduction Introduction

Introduction

This Resource Assessment is one of seven individual County based resource DONEGAL

assessments prepared by RASLRES and this series follows on from the Regional

Wood Fuel Resources completed by RASLRES in April 20101. The purpose of the

initial regional report was to outline the sources and availability

of wood based fuels and model various supply scenarios at a

regional level. SLIGO LEITRIM

A second study completed by RASLRES examined the MAYO

Regional Heat Market and Biomass Demand Estimates for ROSCOMMON

20202. That study determined the demand for biomass at

a Regional and County level by interpreting the National

GALWAY

Renewable Heat Targets for 2020 agreed by the EU and the

Irish State. The study determined the quantity of wood based

fuels required to meet the 2020 targets.

CLARE

The renewable heat market has the potential to create

considerable levels of employment across the Western Region

and to provide long-term stable markets for low value

wood fuels which can compete with fossil fuels and so

reduce and fix energy prices for end users. In addition,

there are environmental benefits – reductions in CO2

emissions.

The Biomass Heat target is one of a number of national targets which will require significant quantities

of wood biomass. Other sectors for which national targets have been set include CHP, Co-Firing. These

coupled with other markets Bio-Refining, Biomass export and possibly animal bedding will compete with the

Biomass Heat Sector for resources.

The purpose of this report is to provide Local Authorities and other interested parties with an overview of

the potential supply of wood based biomass and estimated demand for renewable heat market within each

county. It will also highlight the issues regarding the potential impacts of large scale projects such as Bio-

Refineries and/or Combined Heat and Power (CHP) plants on county and regional supply chains. At present

there is more than sufficient wood available to meet current demand for wood biomass (estimated to be

about 60,000odt3 annually – most of this is used by sawmills to kiln dry timber) and there is considerable

potential to grow the biomass market from within existing supplies without straining the resource.

Local wood biomass resources are finite and as demand for biomass increases from some or all of the

above markets, planners will require a greater understanding of the available resources at both a county and

regional level. The increased demand for wood biomass will stimulate increased rates of afforestation and

potentially a shift from main stream agriculture into short rotation coppice (SRC) or other energy crops. This

will increase the volume of truck movements hauling the fuel stock from its source to where it is consumed.

At present there are a number of large scale projects being considered for the region should one or a number

of these progress to construction it is likely that the local fuel supply will have to supplement with imported

materials from within the EU and 3rd party countries. The point of importation and the additional traffic

volume generated will need to be given careful consideration because of the urban location of the region’s

ports.

1

http://www.raslres.eu/wp-content/uploads/2010/05/RASLRES-WP3-SS-Wood-fuel-resource-assessment-v01-2010_5_6.pdf

2

http://www.raslres.eu/wp-content/uploads/2010/05/RASLRES-WP3-SS-Regional_Energy_Balance_Method_Results_

Mar2010-v01-2010_3_16.pdf

3

Oven dry tonnes.

Resource Assessment for County Donegal Donegal Fuel Resource Survey and Biomass Demand November 2012 3The Donegal Forest Estate

The Donegal Forest

The Forest Estate

In 2010 the National Forest Estate was estimated to be 745,500ha or 11% of the land mass. By this date

the Western Region’s4 forest estate accounted for 40% of the National Estate - the actual area planted

had reached 295,000ha or 12% of the total land area of the Western Region. 37% of the privately owned

forests and 42% of the public owned forest are situated within the western region. Table 1 summarises the

distribution and ownership of the forest estate at national, regional and county levels.

Ownership by Area Ha Ownership by % Forest Cover %

Level

Private Public Total Private Public

National 347,652 397,805 745,456 47% 53% 11%

Regional 127,842 166,821 294,664 43% 57% 12%

Regional Ownership as % of

37% 42%

National

Counties

Clare 28,234 23,360 51,594 55% 45% 16%

Donegal 22,615 36,407 59,022 38% 62% 12%

Galway 18,887 38,926 57,813 33% 67% 10%

Leitrim 12,553 12,599 25,152 50% 50% 16%

Mayo 23,289 34,465 57,754 40% 60% 11%

Roscommon 12,945 8,436 21,382 61% 39% 9%

Sligo 9,319 12,628 21,947 43% 57% 12%

Table 1 – Forest Distribution and Ownership at National, Regional and County levels – Source: Forest Service 2011

The Donegal Forest Estate

Size and Ownership

The size and ownership of the county’s forest estate and therefore its productive capacity relative to its heat

demand has a direct bearing on the county’s ability to meet its share of National Targets for two reasons.

If a county has a high heat demand but a small forest estate then the demand may out strip the potential

supply and the ownership can determine where harvest is sold. At present, most of the timber (suitable

for biomass) produced by public sector forests are sold on long-term contracts to state owned boardmills.

Therefore, it is expected that increasing demand from the biomass market will be met by increasing supplies

from private sector forests.

By the end of 2010 the forest estate in county Donegal had reached 59,020ha which is approximately 12.2%

of the county’s area. This is slightly above the national average of 10.8%. Figure 1 illustrates ownership

of the forest estate within the county. Private ownership accounts for 22,615ha or 38.3% of the total area.

Over the last five years the county’s private estate has increased by 1,067ha, accounting for nearly 3% of

the national planting programme and is the second lowest afforestation rate in the region for the period ’06

to ‘10. This low rate of planting reflects the increasing number of restriction such SPAs and the exclusion

of unenclosed land with low productivity, both of which are reducing the availability of land suitable for

afforestation, rather than recent reductions in the grants rates. Furthermore, proposed changes in the

4

The Western Region refers to the following counties; Clare, Donegal, Galway, Leitrim, Mayo, Roscommon and Sligo.

4 Resource Assessment for County Donegal Donegal Fuel Resource Survey and Biomass Demand November 2012Age Profile Age Profile Common Agriculture Policy (CAP) may limit the transfer of land out of routine agriculture into forestry post 2014. The proposals have yet to be negotiated, but should they come into effect as currently outlined, only 5% of area currently deemed as agricultural would be eligible for afforestation. Public afforestation accounted for only 18ha over the same timescale (5 years). The figures for public owned forests include all state agencies; Coillte, (amenity and productive forests) and National Parks being the main stakeholders. The forecast discussed below includes the expected yields in all forests. Figure 1 – Ownership of the Donegal Forests - Source: Forest Service and ITGA 2012 Yearbook Age Profile As indicated above the increased demand for biomass is expected to be met by the increasing volume harvested within the private sector. The age profile of the private estate is one of the key factors in determining the annual harvest area and volume produced. Figure 2 illustrates the age profile of the private estate in Donegal. Figure 2 – Age Profile Private Estate – Source: Forest Service 2010 and ITGA Yearbook 2012 In terms of developing the biomass market the age groups 11 to 15 and 16 to 20 are of most interest as these forests are currently at or rapidly approaching the age of first thinning. (Thinning is the removal of a portion of the crop at a rate which does not reduce the overall production of the site and it is therefore considered to be sustainable). These age classes comprise 12,000ha. Their harvest product will be new to the market and will substantially increase the volumes of available timber over the next 10 years. Plantations in the 21 Resource Assessment for County Donegal Donegal Fuel Resource Survey and Biomass Demand November 2012 5

The Resource

The Resource

to 25 and 26> groups, if not already thinned are unlikely to be thinned in the future as they will be past the

recommended age of first thinning.

The age profile for the public forests are not readily available, however, it is safe to assume that the age profile

is evenly distributed as the yield forecasts only fluctuate moderately during the period, which suggests that

a similar area will be harvested annually.

The timber harvested during thinnings and clearfells in both the public and private estates are used to supply

a number of markets. These are discussed in the following section.

The Resource

Wood based biomass comes from three main sources:

gg Private Forests

gg Public Forests

gg Sawmill residues generated from logs purchased from both the private and public forests

When logs are harvested they are generally graded according to their diameter and stem quality; these

‘assortments’ are given in table 2. The two assortments of most interest to the biomass sector are theThe Resource Figure 3 Potential Yields – Source: COFORD 2011 The potential yield for 2012 is expected to be 259,000m³. The yield fluctuates between 196,000m³ and 590,000m³ - but generally it increases through the period of the forecast. Currently the small diameter roundwood produced by the public sector is retained to meet existing contracts with publicly owned boardmills. This situation may change in the future as the boardmills which are situated in the south east begin to source suitable raw material from the private sector within the south east region. Residues are produced when sawmills process round logs into sawn timber. There are three forms of residues; bark, sawdust and woodchips. Residues are also known as co-product. Approximately 50% of the volume of timber delivered as logs to a sawmill ends up as co-product. A significant amount of the co-product is already being used in sawmills to generate heat to kiln dry timber and at a number of other facilities to generate process heat. Figure 4 – Private Sector Pulpwood Logs and Co-product – Source: COFORD 2011 Resource Assessment for County Donegal Donegal Fuel Resource Survey and Biomass Demand November 2012 7

Regional and County

Regional and County Energy Balance and the Requirement for Renewable Energy

There are a number of reasons for the variations which occur in the supply of logs to the market. Different

annual planting rates – planting rates have fluctuated since in the 1980s the lowest private planting rate

recorded for Donegal was in 1985 - 3.64ha, the highest was in 1995 – 2544ha. Thinning commences between

the ages of 15 and 18 so the amount of land available for thinning is depended on the amount of land planted

15 to 18 years earlier. A second factor – thinning is cyclical and therefore the area scheduled for thinning

increases year on year as the plantations mature which increases volume of pulpwood produced. However,

as the crop matures the average log size increases and therefore, less pulpwood is produced per ha from

mature plantations. The forest management assumptions i.e. thinning or non-thin - areas which are left

unthinned due to site exposure, soil type and conditions or plantation size – reduce the volume of pulpwood

produced in the early years but increase it in the later years as these areas are clearfelled.

As the private estate matures and average log sizes increase in later thinnings the amount of palletwood and

sawlog increases. This increases the amount of timber processed by sawmills which increases the volume

of co-product generated by sawmills. Figure 4 above shows that as the private sector matures the volume of

co-product increases from 2020 onwards.

The peaks in production in 2025 and 2027 reflect the peak in planting rates in the mid 90s which are in a

thinning cycle and the start of clearfelling in the private sector. The areas planted between 2010 and 2020

will compensate for the loss of production from areas clearfelled.

The volume of co-product generated within a county depends on the level sawmilling which is basis within

the county. Sawmilling capacity in Donegal is low relative to the size of its forest estate. Therefore, most of

the sawlog, palletwood and stakewood produced in Donegal are exported to other counties or to Northern

Ireland. As a result the co-product associated with round wood sourced in Donegal is generated outside the

county. This movement within the region and outside make forecasting woodfuel supplies at a county level

difficult.

Regional and County Energy Balance and the Requirement for

Renewable Energy

An Energy Balance describes the supply of and demand for energy across various sectors of the economy

and the contributions made by various fuel types. Energy Balance studies can be prepared at international

levels such as EU, National level or at regional and county levels. Typically, the energy market is divided into

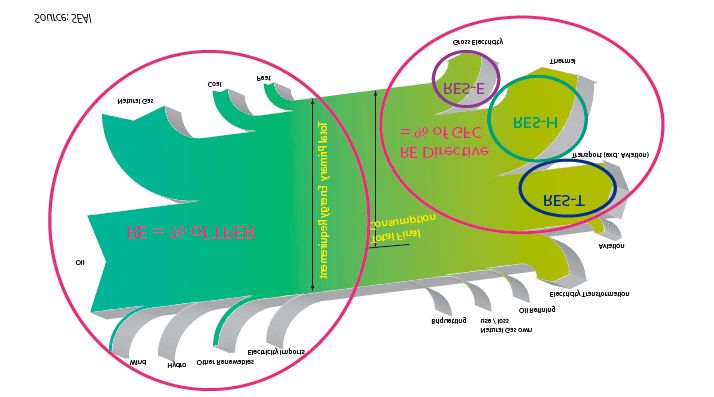

three major groups; Electricity, Transport and Heat. Figure 4 illustrates the energy balance for Ireland based

on data relating to 2011 and published by SEAI in June 2012. The red circle on the left shows the total energy

inputs and the fuel types used to supply Irish demand. This is known as Total Primary Energy Requirement

(TPER). It is clear from the illustration that Ireland is very dependent on fossil fuels which accounted 95.1%,

(inputs with oil and natural gas accounted for 82% of total inputs). Renewables accounted for 4.6% and the

balance is made of wastes and imported electricity. The red circle on right shows the total amount of energy

consumed in the three main energy markets Electricity, Transport and Heat. This is known as Total Final

Consumption (TFC). The fuel used for aviation and energy lost to the system during conversion and delivery

are shown as exiting the system.

8 Resource Assessment for County Donegal Donegal Fuel Resource Survey and Biomass Demand November 2012Regional and County Energy Balance and the Requirement for Renewable Energy

Energy balances are used for planning long-term energy markets and to set realistic goals for switching

from one fuel type to another and for setting renewable energy targets for each of the three principle market

sections.

In 2007 the EU agreed legally binding commitments regarding climate and energy; known as 20:20:20 by

2020 these commitments set out below5:

1. 20% reduction in greenhouse gases by 2020

2. 20% increase in energy efficiency by 2020

3. 20% of the EU’s energy consumption to be from renewable sources by 2020.

The directive 2009/28/EC on the promotion of energy derived from renewable sources sets out how the EU

is to achieve the 20% target by 2020. This Directive also requires each member state to prepare a National

Renewable Energy Action Plan which sets targets for each energy sector, electricity generation, heating and

transport. Ireland has agreed to an overall renewable energy target of 16% 2020. Each energy sector has

been given a specific target for 2020 these are:

1. Electricity – 40% by 2020. SEAI estimated that in 2011 – 17.6% was achieved.

2. Transport – 10% this target is to be achieved by a combination of a 4% biofuels obligation and an

increase in the number of electric cars to 10% by 2020. By 2011 renewables contributed 3.6%

3. Heat – 12% of the heat market. SEAI estimated the contribution made by renewables for 2010 was 5%.

At this level Ireland would be falling behind on the required growth rates if the national target is to be

achieved by 2020.

SEAI’s provisional estimates for 2011 indicate that Ireland’s renewable sector contributed 5.9%6 to overall

energy demand. This suggests that the renewables market needs to treble in size if the overall national target

is to be achieved by 2020. At present only the electricity sector seems to be making sufficient progress to

meet its target.

5

http://www.dcenr.gov.ie/NR/rdonlyres/03DBA6CF-AD04-4ED3-B443-B9F63DF7FC07/0/IrelandNREAPv11Oct2010.pdf

6

http://www.seai.ie/Publications/Statistics_Publications/Renewable_Energy_in_Ireland_2011.pdf

Resource Assessment for County Donegal Donegal Fuel Resource Survey and Biomass Demand November 2012 9Regional and County Energy Balance and the Requirement for Renewable Energy

The Regional Energy Balance & Biomass Heating Demand Estimates for 20207 examines the total demand

from Heat Sector. Demand in the Heat market comes from the following sectors; Residential, Industrial

and Services. Due to poor data collection at regional and county levels various CSO indices are used to

convert National Data to demand estimates for both regional and county levels. The estimate for renewables

assumes that wood based biomass will account for 85% of the renewable heat market target for 2020.

Table 3 sets out the National, Regional and County estimates for wood biomass demand assuming the 2020

targets are achieved. The standard unit of measurement for biomass is the “oven dry tonne” (odt). By 2020

Co. Donegal would require approximately 38,000 oven dry tonnes (odt) of biomass to meet its share of

national targets.

To convert m³OB to oven dry tonnes the volume of timber expressed in m³OB is divided by approximately 2.5.

County

Sector ‘000odt National Regional

CE DL GY LM MO RN SO

Residential 584 105 15 20 31 4 17 8 9

Industry 423 77 13 11 26 3 12 6 6

Services 240 35 6 7 9 1 6 3 3

1,247 35 35 38 66 8 35 17 18

Table 3: Demand for Wood Biomass in 2020 – Requirements in expressed as ‘000 odt – Source: Regional

Energy Balance – RASLRES 2010

Achieving the county targets as set out in the Regional Energy Balance will require a great deal of planning

and highlights the need for the full engagement of all stakeholders; Local Authorities (Planning Section,

Environment Section, Roads and Facilities Managers etc.), Industrial and Commercial Sectors, State Bodies

(Teagasc, NPWS and Forest Service), Heat Entrepreneurs, Forest Managers and Forest Owners Public and

Private. The most important of these are the Private Forest Owners as it is from this sector that the increase

in overall timber supply for the county is to come and key to meeting the county’s target for biomass target

for 2020.

The Regional Wood Fuel Resource Survey – RASLRES April 2010 examines the demand and supply at a

regional level and used four scenarios to model the supply of wood to the heat market. These scenarios

modelled the supply side using a number of assumptions which have an impact on the availability of wood to

the heat market. The scenarios and the assumptions are set out below:

1. Scenario 1 – full availability of roundwood and associated co-product from both the public and private

sectors. This scenario assumes that all of the pulpwood is supplied to the heat market is supplied

directly from the forest. It also assumes that all of the co-product generated in sawmills derived from

palletwood and sawlog produced in Donegal is made available to the Donegal heat market.

2. Scenario 2 – full availability of roundwood and co-product from the private sector only. This scenario

assumes that all of the material sourced from the public sector is used to supply existing contracts and

therefore not available to the local heat market.

7

http://www.raslres.eu/wp-content/uploads/2010/05/RASLRES-WP3-SS-Regional_Energy_Balance_Method_Results_

Mar2010-v01-2010_3_16.pdf

10 Resource Assessment for County Donegal Donegal Fuel Resource Survey and Biomass Demand November 2012Regional and County Energy Balance and the Requirement for Renewable Energy

3. Scenario 3 – 60% availability of roundwood and co-product from the private sector only. As with

scenario 2 above this scenario assumes that the only available material will be sourced from the private

sector. Furthermore, it assumes that only 60% of the potential private sector supply is available to the

local heat market. The reduced supply to the heat market maybe as a result of competition from other

non-heat markets which yield a better return or where the costs of harvesting and road transport result

in the woodchip being uncompetitive with fossil fuels.

4. Scenario 4 - 35% availability of roundwood and co-product from the private sector only. As with

scenarios 2 and 3 above scenario 4 assumes 35% availability from the private sector. This situation

may arise if the rate of boiler deployment does not keep pace with the increasing rate of harvesting.

Forest owners, particularly those with small plantations and/or high harvesting costs will require long

term, stable locally based markets for large volumes of low value pulpwood logs. This is exactly the type

of market provided by a local biomass heat market. Therefore, if demand for wood fuel is low because

of low installation rates many plantations will remain unthinned because poor returns to forest owners.

The results of the modelling are presented in Figure 5a below. As stated above the expected demand from

the biomass market for Donegal in 2020 will be 38,000odt. Under scenario 1 – all material being available

there is a potential supply surplus of 65,000odt. It is unlikely that this situation will arise because currently

most of the pulpwood produced by the public sector forest is retained to supply long-term contracts with

board mills. Therefore the private sector will have to meet the majority of the demand.

Scenario 2 suggests that if all of the pulpwood and associated co-product harvested in the private sector is

made available to the heat market there will be a shortfall of about 5,000odt. A shortage of this sized could

easily be met by adjusting harvesting schedules in the private sector or by purchasing pulpwood from the

public sector.

Scenarios 3 and 4 may arise if certain market conditions apply – low rates of boiler installation or increased

demand for stakewood which attracts a better price. If the rate of boiler installation remains at its current

level there will be insufficient demand and economies of scale required to justify harvesting in remote or

small plantations.

The RASLRES study Wood Energy Installations8 states that there is 1 wood fuelled (woodchip and wood

pellet) boiler installations in Donegal totalling 4,410kW of installed capacity of which 3,500kW are fuelled

by woodchip. These boilers require about 2,500 to 2,800odt annually which is approximately 7% of what is

required to achieve the county’s 2020 target. If a low rate of demand persists only a quarter of the potential

production available from the private sector modelled in scenario 4 – 35% of private sector woodlands

would find a market. This suggests that currently the major barrier to the development of the local wood

fuelled heat market is the low rate of installations. Therefore, it is essential that installation rate increases

dramatically over the next 6 or 7 years.

If Co. Donegal is to meet its renewable heat targets the private sector forests must be fully mobilised and the

public sector will have to make some contribution to the supply chain.

8

http://www.raslres.eu/wp-content/uploads/2011/06/Wood-Energy-Installations-WR-2011.pdf

Resource Assessment for County Donegal Donegal Fuel Resource Survey and Biomass Demand November 2012 11Regional and County Energy Balance and the Requirement for Renewable Energy

Figure 5a – County Donegal Results Scenarios 1 to 4 Roundwood and Co-Product included – Source: DARE

Ltd.

The supply of biomass modelled above and presented Figure 5a assumes that both pulpwood and co-

product are available in varying volumes according to each of the scenarios. However the market is further

complicated because the amount of co-product available will depend on where the pallet and sawlog are

processed. The quantity of co-product produced within a county depends on the number and size of sawmills

based within the county relative to the volume of timber harvested in that county. Co. Donegal has a number

of small scale sawmills, therefore most of the palletwood and sawlog is exported to sawmills based in other

counties or to mills based in Northern Ireland. This means that the vast bulk of co-product associated with

timber harvested in Donegal is generated outside the county and not readily available to the Donegal heat

market.

To illustrate the impact caused by the loss or removal of co-product from the heat market a second set of

scenarios were modelled where only round logs (pulpwood) is available and co-product is excluded but the

participation rates remain the same i.e. Full Private and Public Sector, Full Private Sector only, 60% Private

Sector and 35% Private Sector. The results are presented in Figure 5b.

Figure 5b – County Donegal Results Scenarios 1 to 4 Roundwood only

12 Resource Assessment for County Donegal Donegal Fuel Resource Survey and Biomass Demand November 2012Barriers to Market Barriers to Market Development Again, the results modelled in scenario 1, full availability of logs from both the public and private sectors, there is sufficient supply to meet the estimated demand for 2020. However, in scenario 2, full private sector pulpwood only, the supply of pulpwood would be 23,000odt or approximately 60% of the potential demand. The shortfall will be about 15,000odt per annum. The results for scenarios 3 and 4 are; supply 14,000odt or 37% of market demand and 8,000odt or 21% of market demand respectively. The results modelled above for scenarios 3 and 4 and presented in Figure 5b still suggest that the biggest barrier to market development is the low rate of wood chip boiler installations. At present demand is estimated to 2,500odt to 2,800odt per annum which is equivalent to 23% of material available modelled in scenario 4 – pulpwood only. Therefore, demand needs to increase four fold before supply constraints impact on the market in the worst case (scenario 4 Figure 5b). To put this in context the installed capacity of wood chip boilers would need to increase from 3,500kW to 10,000kW to 12,000kW depending on the operating hours and the duration of the heating season or from 15 boilers to 25 to 30 boilers depending on boiler size. Even this modest expansion would not achieve counties biomass targets. The scenario 2 would allow for a much greater expansion from the current 3.5MW (3,500kW) to 28.7MW before supply becomes a constraint as set out in Figure 5b. Expansion beyond this level will require the use of wood fuels (co-product and wood pellets) imported into the county, much of which would have been exported as logs to sawmills or by the greater use of wood fuels sourced from public sector forests within the county. Barriers to Market Development There are a number of factors which act as barriers to the development of the wood energy in the private sector woodlands. The impact of each barrier will change as the market matures. In most counties the biggest barrier is a lack of demand from the wood chip market which has stagnated. However, the addition of the boiler to Connacht Gold site will stimulate demand in the private sector. Other factors also act as barriers to market development and the main barriers are list below it is important to remember that the impact of each and its priority will change over time and others may arise in the future but the main ones are listed below: 1. Stagnation of demand and low rates of boiler installation 2. Lack of awareness and/or understanding amongst potential end users 3. Lack of awareness and/or understanding of the process of harvesting 4. Plantation size 5. Access to plantations along public and private roads. 6. Competition from other markets for pulpwood These barriers are discussed in greater detail below. 1. Stagnation of the wood chip market In recent years the number of boilers installed annually has decreased and with the removal of the grant aid, end users must now fund the entire cost of the boiler installation. Woodchip boilers are considerably more expensive to install but the fuel cost are stable and cheaper than fossil fuels. Given the current economic climate and difficulties accessing funding many potential end users in the private sector are not considering wood fuel at present. Public Sector bodies with high stable heat loads are the best opportunity at present, given the Government’s drive for greater energy efficiency and requirements to reduce greenhouse gas emissions. An unpublished RASLRES survey of eight publicly owned buildings in Co. Donegal suggests that if these buildings were switched from fossil fuels to woodfuels demand for woodchip in the county would increase by 1,000odt per annum. This increase would require an additional harvest area of circa. 150ha per annum supporting 10 to 12 farm families and support the six months work for harvesting crews and transport plus increased activity for chip suppliers. Resource Assessment for County Donegal Donegal Fuel Resource Survey and Biomass Demand November 2012 13

Barriers to Market Development

2. Lack of awareness and/or understanding amongst potential end users

In some cases potential end users are not aware of the alternatives to fossil fuels thankfully this number

is now falling. There are still some misconceptions regarding the quality and reliability of supply and the

location of wood chip suppliers. At present there is one supplier operating in the western region who has

attained certification from the Wood Fuel Quality Assurance scheme (WFQA). This scheme certifies that the

wood chip is produced in compliance with EU standards and that the moisture content and chip size comply

with heat supply agreements and that the timber used to produce the wood chip has been sources from

sustainable managed plantations and has been legally felled. Further information regarding installations,

suppliers of wood chip and the WFQA is available from www.RASLRES.eu and www.WFQA.ie

3. Lack of awareness and/or understanding amongst forest owners

Forestry is a long term investment and once planted and the premia secured many owners let the management

of their plantations slip down the list of priorities. In some case the ownership of the plantation may change

and the new owner might not be familiar with forest management processes and the processes involved in

bring timber to the market. The National Forestry Inventory NFI completed in 2007 estimated that only 25%

of the private estate ready for thinning at that time had been thinned. This highlighted the need to put in place

a forum through which forest owners could improve their understanding of forest management. The Forest

Service and Teagasc and many of the Leader Companies in the region have promoted the development of

producer groups. There are a number of producer groups scattered throughout the region at various stages

of development.

Donegal has the most active and developed producer group in the country – Donegal Woodland Owners

Association DWOS. This producer group represents the interests of owners who own plantations situated

in the county. They have put huge effort into getting owners actively involved in the management of their

plantations and have adopted a group approach to the harvesting and marketing of the timber products. The

group have also developed a small scale ESCO contract model where the DWOS will install, finance and

maintain log gassifiers boilers. These boilers are ideal for small scale installations and the fuel handling is

labour intensive creating employment opportunities for members. Similar projects exist in other counties

through the region.

The County Clare Wood Energy Project CCWEP has led the way in this area and it has a membership of c.

450 and represents an area of 4,500ha. The county has been divided up into 21 geographical clusters. Once

a cluster is identified the owners can seek tenders from suppliers via the CCWEP website for the following

services; inventory, road construction, harvesting and other forest management activities. By adopting the

cluster approach sufficient economies of scale are achieved making the works more attractive to contractors.

4. Size of plantations

The average size of privately owned plantations in the western region is 9ha with a median of 5.5ha, making

it difficult to achieve any economies of scale in terms of roading and harvesting – some these plantation have

been excluded from the thinnings forecast. However, the yield is included in the expected clearfell volume.

If these plantations are to be harvested they need to be grouped so that economies of scale can be achieved

- this is one of the strengths of the producer group approach to harvesting.

5. Access to Plantation along Public and Private Roads

Forest Roads - A critical issue over the coming years will be the construction of forest roads. At present

forest owners are eligible for grant aid for the construction of Forest Roads. To be eligible a plantation must

be within two years of thinning. There is a three to four year window within which thinnings must be carried

out if the stability of the crop is to be assured. Failure to do so will leave the crop vulnerable to wind throw.

The available funding is limited and is decided on a year to year basis. Without grant aid many plantations

14 Resource Assessment for County Donegal Donegal Fuel Resource Survey and Biomass Demand November 2012Barriers to Market Development will be left unthinned because the cost of roading relative to the value of the material harvested cannot be justified. Evidence from the Cork and Galway Forest Producers Group Project confirms this to be the case. If long-term funding is not put in place and this issue is not resolved many owners will leave their plantations unthinned, thereby reducing the supply of wood to the biomass and other timber processing sectors in the short and medium term. This timber would not be lost entirely but instead of having a regular supply on a five year cycle there would be a once off yield at the end of the rotation as unthinned areas are clearfelled. Figure 6 presents a summary of the required level of investment and amount of road to be constructed using the current scheme rates of 20 linear meters per ha and a maximum rate of 700 euro per ha. The cost for the period 2012 to 2026 would be approximately €4.7m and the length of road required would amount to 158km servicing an area of 7,875ha scheduled for first thinning. Further roading will be required to services areas schedule for clearfelling. The figure assumes that roads are constructed two years in advance of thinnings. Figure 6 – Roading requirement areas scheduled for first thinning – Source: COFORD 2009 Access via public roads – Local Authorities have become more concerned regarding potential damage to or the inability of some local roads to support the weight of timber lorries. It is becoming more common for Local Authorities to restrict the weights to be carried on 3rd class roads to approximately 15t. This restriction means that the timber has to be double handled increasing the cost of harvesting significantly. By way of example, a plantation due for clearfell was recently granted a new felling licence which included a new weight restriction on the access road. The weight restriction was not in place on the previous felling licence which is still valid. The cost of harvesting under the old licence was agreed at €18/t. However, to comply with the weight restriction imposed by the new licence the timber has to be hauled from the forest to a transfer depot on a main road where it is reloaded for onward shipping. This has increased the cost of harvesting by €2.50 to €3.00 per tonne, the average cost has increased from €18/t to €22/t. This increases the harvesting cost by €12,375 or represents a 15% increase in the cost of harvesting. If this increase was applied to a thinning the returns would not cover the cost of harvesting. These restrictions should they continue to be applied will significantly reduce the volume of timber harvested and may jeopardise the region’s timber processing industry. Most of the sawn timber produced in Ireland is exported to the UK and Europe and our exports must compete with timber produced in areas where scale and direct access to markets means that the price for sawn timber is low. Irish timber will not be able to compete if our cost base increases at the rates described above. If the adhoc nature approach to harvesting was removed by using the COFORD forecast model to identify plantations in an area which are due for thinning, the thinning dates could be moved forward or back so that all of the timber to be harvested in the area would be harvested within a specified time frame. This process Resource Assessment for County Donegal Donegal Fuel Resource Survey and Biomass Demand November 2012 15

Proposals for CHP

Proposals for CHP and Bio Refinery - Market Potential and Impacts

could be repeated in line with thinning cycles. This would enable forest owners, the Forest Service and

Local Authorities to plan for road repairs and also provide detailed information to the processors as to the

availability of timber within their areas. This information would allow timber processors secure a greater

proportion of their timber closer to the mills thereby reducing road haulage costs. Some of these savings

could be used to offset the cost of double handling or result in higher prices paid to forest owners which

in turn would encourage more forest owners to thin their plantations. It is the authors understanding that

Coillte, the Forest Service and Local Authorities already discuss harvest plan and transport routes using

information similar to that on which the COFORD forecast is based.

The recently enacted planning legalisation now stipulates that some forest entrances require planning

permission. It is not clear from the legislation exactly which forest entrances require planning permission

and those that don’t. This situation and the cost associated with planning permission need to be agreed at a

National Level.

6. Competition from other Markets

Competition for the wood resource will come from various markets, at a large scale these markets include;

CHP, Co-Firing and Bio refining. On a small scale competition will come from the stake and fencing market

and animal bedding. As stated above, Ireland’s National Targets for Renewable energy extend to electricity

generation market and it is acknowledged that wind power will be largest supplier of renewable power to the

grid. However, two other generation types CHP and Co-Firing will compete for wood biomass.

The Government have set very ambitious targets for both of the sectors:

gg CHP – 800MWe by 2020, this target includes both renewable and fossil fuelled CHP plants. By 2010

installed capacity had reached 307MWe of which 284MWe were operational.

gg Co-Firing to replace 30% of the energy inputs by 2015 this will require approximately 900,000t of

biomass annually. The three mid-land peat fired plants are to deliver this target. Moneypoint in Co. Clare

are still assessing the possibility of co-firing.

Combined Heat and Power (CHP) plants serve two markets because they generate electricity and heat at the

same time. Most of the energy inputs i.e. woodchip or other fuel, is recovered as either electricity which is

sold to the grid and the heat which can be used in district heating networks or to supply process heat to a

factory. SEAI estimated that the overall efficiency of CHP to be 84%. New plant in the “high-efficiency class”

recover from the total input between 85% and 95% making CHP an extremely energy efficient process and

maximises the returns from a limited resource. There are three wood fuelled CHP plants operation on the

island of Ireland.

Co-Firing refers to the substitution of a fossil fuel, usually coal or peat, with biomass. An example of this

would be peat fired power station in Edenderry, Co. Offaly. At present Edenderry consumes about 110,000t

of wet woodchip and other biomass annually. This is set to increase to 300,000t per annum by 2015. In a

co-firing plant the only energy recovered is electricity, most of the heat element is not recovered - the heat

generated is lost to the atmosphere through water cooling towers. Co-firing recovers about 30% of the

energy inputs which is a very poor recovery rate from a finite resource.

The introduction of the Renewable Heat Incentive (RHI) in Northern Ireland will impact on the demand for

wood fuel in the border region, Donegal, Donegal and Leitrim. Under this scheme end users receive an

incentive for using renewable fuels ranging from 1.5p/kWh up to 6.2p/kWh. For a typical 350kW boiler,

running at full load for 2890 hours delivering 1012MWh per annum the incentive received could be as high as

£15,180stg per annum. This amounts to a subsidy of about £46stg per tonne of woodchip delivered at 35%

moisture content. These incentives are payable for twenty years and will no doubt promote greater rates of

boiler deployment in Northern Ireland and inevitably heat entrepreneurs will have to look south to secure

supplies.

16 Resource Assessment for County Donegal Donegal Fuel Resource Survey and Biomass Demand November 2012Proposals for CHP and Bio Refinery - Market Potential and Impacts The stake and fencing and animal bedding markets are expected to continue at the current rates and while they experience increased competition from the biomass markets it is likely that they will be able to secure their requirements because of a price premium paid for better quality logs suitable for stake production. At present the premium is four times the value of logs destined for the woodchip market. Proposals for CHP and Bio Refinery - Market Potential and Impacts Over recent years there have been several announcements regarding the development of the CHP sector across the western region. Planning permission has been granted for one CHP plant in North Mayo. Imperative Energy has also announced plans to develop a CHP/Bio refinery plant at Claremorris, Co Mayo. Combined Heat and Power plants have the potential to deliver significant benefits to the region in terms of employment stimulation, diversification for farm enterprises and rural incomes, stable energy prices not to mention the potential environmental benefits. RASLRES is aware of seven CHP proposals throughout the region. The total installed capacity for these proposed plants at present is approximately 124MWe (311MWth). Data regarding fuel requirement was received from six of the proposed plants their total annual demand is estimated to be 1085kt wet weight basis. Most of the plants intend to use wood as their primary fuel and where possible to source this locally. The annual demand estimates for these plants range from 60,000 green tonnes to 350,000 green tonnes per annum. Therefore, it is necessary to assess potential combined impacts of these plants at a regional and county level as it unlikely that any county will be able to accommodate even a small scale plant without drawing fuel supplies from neighbouring counties. It is also critical to know where the plants are based and that there is sufficient heat demand close to the CHP to ensure that all of the heat produced is used. The demand must also be considered in the light of targets and existing markets. If these plants are to be constructed within the region planners must assess each one with an understanding of the available fuel resources and the demand from other plants with in the region. The following section is intended to give planners an understanding of some of the issues involved in establishing a sustainable CHP and Bio Refining industry. CHP is the most efficient use of fuel in that approximately 85% of the energy inputs are recovered in the form of electricity exported to the grid and heat sold on as process heat or for space heating. The Commission for Energy Regulation (CER) hosted a consultation process the aim of which was to agree exactly what constitutes “useful heat”. Useful heat is defined in the CER consultation paper as “heat produced in a cogeneration process to satisfy an economically justifiable demand for heating or cooling”. Examples include process heating, space heating, district heating and the use of exhaust gases for drying. The CER outlined two options in the consultation paper. Following the consultation process the CER have decided that “useful heat” shall include heat sold on to 3rd parties and heat recycled back into the plant to process and dry fuel stocks. Promoters of CHP must also comply with other conditions relating to the sale of heat to 3rd parties and that such sales are economically justifiable and would otherwise be met at market conditions. The rollout of CHP in the western region will impact on the regions heat market and the extent of this impact will depend largely on were a plant is situated. If a CHP plant is situated adjacent to a medium sized town or industrial area and the heat is sold to 3rd parties as process heat or as spacing heating through a district heating network then the heat supplied will displace an existing heating system, in most cases this will an existing fossil fuel system. In these circumstances the existing heat market may increase moderately but the percentage met by renewables will increase substantially. If the CHP plant which is not connected by way of a district heating network to either a town or industrial complex it will not displace any of the existing heat market. Therefore, any heat generated will increase the overall size of the heat market. RASLRES has estimated that 217,000odt will be required to meet the Regions 2020 renewable heat targets. The combined fuel requirement for the six CHP plants for which data was supplied is 477,000odt. Heat accounts Resource Assessment for County Donegal Donegal Fuel Resource Survey and Biomass Demand November 2012 17

Proposals for CHP and Bio Refinery - Market Potential and Impacts

for 71.5% of the output of these plants, therefore, it could be argued that 341,000odt of the fuel input is part of

the Region’s heat market. This in theory implies that CHP could meet 157% of the Region’s 2020 renewable

heat market estimates. However the reality is that by allowing recycling of heat, the regional heat market will

increase to provide heat for new manufacturing processes associated with the proposed CHP plants. The size

of this increase will only become apparent as when developers make their plans and how they intend to treat

the heat generated known to Local Authorities. The impact of this increase demand is discussed below. By

locating a CHP plant close to an existing heat load there is the possibility to displace fossil fuels.

Previous RASLRES studies have indicated that by 2020 the total potential forest based biomass resource

in the region is 526,000odt (Public and Private sector woodlands and Co-product). If the current market is

assumed to continue then a significant quantity of the resource will be diverted into other markets including

the existing biomass market. The total demand from all markets will be 816,000odt which exceeds the

potential supply by 289,000odt. Figure 7 illustrates the composition of the market and assumes that all the

heat generated by CHP is included as useful heat.

Notes:

1. Potential CHP includes fuel requirement for both heat and power and that all heat produced is

deemed to be useful heat

2. The Region’s Share of National targets for Co-Firing and Board Mill requirements are based on the

Regions forest area circa 36%

3. Current Biomass market estimated to be 40,000odt

4. An allowance is included for continued demand for the stake market

Figure 7 – Regional Supply and Market Demand 2020

18 Resource Assessment for County Donegal Donegal Fuel Resource Survey and Biomass Demand November 2012Importation Importation

Meeting the Market Demand

In the short to medium term conventional forestry cannot meet the potential increase in demand because of

the length of time between planting and 1st thinning – from 15 to 20 years. There are a few ways in which

the shortfall identified in Figure 1 can be met;

1. Locally sourced energy crops.

2. Importation of biomass from outside the region or from other countries.

3. Utilisation of biomass fraction of waste or agricultural residues

4. Development of further feedstock conversion technology (e.g. torrefaction9)

Table 4 presents the current levels of deployment for energy crops in the western region. It must be

remembered that these crops are likely to be grown under contract. The source is the SEAI Bioenergy Maps

2011.

Crop Current Area ha Oven dry tonnes/year Toe/year Potential Area ha

Miscanthus 240 2888 897 433,721

SRC 44 891 176

420,328

Willow 39 785 155

Table 4 – Current and potential energy crop production – Source: SEAI Bioenergy maps 2011

The shortfall in Figure 7 is 289,000odt which converts to approximately 130,072toe. If miscanthus were

used to meet this level of demand, it would require the planting of about 35,000ha by 2020. If short rotation

coppice (SRC) were used the level of planting required would be 33,000ha by 2020. This would amount to

1.5% of the total geographical area of the region. This would require an investment of approximately €70m

and would represent a major shift in the agriculture base.

The Bioenergy maps have indicated that energy crops could provide significant quantities of biomass within

25km of each proposed plant and that all of the shortfall could theoretically be met by planting energy crops

within 50km of the proposed plants. Further studies are required to determine which energy crops are best

suited to a given area. Where possible this information should be gathered during the initial or concept phase

of project development as the fuel mix will need to be considered during the design phase of the biomass

plant and an over dependence on a scarce or imported fuel may put a project at risk.

The ideal situation would be for project promoters and growers to enter into an option agreement which

specifies the terms and condition of a supply contract and is executed by the promoter once all necessary

permissions for the project have been granted. The option agreement would have a specified duration. This

method would allow detailed planning of the fuel supply and mix. Once permissions have been secured the

construction time for a plant would be up to two years. This lead in time would facilitate the establishment of

the energy crops which take three to five years to mature, thereby limiting the operational phase for which

fuel may need to be imported. This approach would also demonstrate to the CER, Planning Authorities,

financiers and the end user that there is a secure, traceable fuel supply in place and there is firm basis for

long term energy price stability.

9

Torrefaction is pre-treatment technology to make biomass more suitable for cofiring applications. It is a thermo chemical treatment

method carried out under atmospheric conditions in the absence of oxygen.

Resource Assessment for County Donegal Donegal Fuel Resource Survey and Biomass Demand November 2012 19Importation

Importation

Importation

The option to import biomass is also open to project promoters. Some of those who provided data have said

that it is their intention to import significant quantities of biomass in the short term, while trying to establish

energy crops on long term contracts with local growers. However, there are a number of considerations

which must be addressed before opting for importation in the long term. Demand for internationally traded

biomass is likely to increase as a large number of biomass plants with good access to port infrastructure

are built in the UK and Europe. The majority of the fuel required for some of these plants will be imported,

increasing the demand for internationally traded biomass which leaves Irish biomass procurers operating

in a very competitive supply chain. At a policy level energy security must be considered as importation of

biomass is just substitution of one imported fuel with another.

The island of Ireland enjoys a disease free status under the European Plant Health Directive, this status

benefits our agricultural, horticultural and forest industries all of which contribute significantly the national

exchequer through taxation and exports. The importations of significant quantities of biomass increase

the risk of accidental introduction of pests and/or disease which would have devastating consequences

for timber production through loss of vigour or the total destruction of the commercial conifer crops and

undermine our disease free status and the image of our products abroad.

The Forest Service is charged with the inspection and control of wood imports. They have given the

following advice regarding the importation of wood biomass; wood fuels sourced from within the EU require

as a minimum a plant passport identifying the source, type of material and compliance with phytosanitary

regulations. Some EU areas are excluded because of bark beetles and other forest pest and diseases. The

Forest Service has also confirmed that timber sourced from the Americas will have to be heat treated to

prevent the spread of nematodes and other sources will be considered on a case by case basis.

At present there are no proposals to require the fuel be certified to FSC or PEFC standards as is the case

in the UK. The certification of fuels provides greater confidence that the source is managed in a sustainable

manner.

Moving low value bulky fuels requires significant logistical planning and the cost of road transport and

shipping will have a significant impact on the cost of fuel delivered to a CHP plant. Therefore, if biomass

is imported it needs to be through the port closest to the plant to minimise transport costs. There are

a number of ports operating on the west coast through which biomass could be imported; Foynes and

Limerick, Galway, Sligo and Killybegs. Galway and Sligo are restricted in the size of vessel which can be

accommodated. Acceptable vessel sizes range from 3,500dwt to 4,500dwt. Foynes and Killybegs can handle

larger vessels in the Panamax Class.

The most efficient way of importing biomass would in the form of wood pellets at 8%MC as they are energy

dense containing 17GJ/t or 11GJ/m³ loose volume. Woodchip at 50%MC contains approximately 8.4GJ/t or

2.5GJ/ m³ loose volume. Table 5 illustrates the relationship between moisture content, energy content and

the frequency of shipments and truck loads assuming deliveries through both small ports and the larger

ports. If either of the smaller ports, Galway and Sligo were used the number of loads delivered would exceed

400 per annum to meet the maximum theoretical biomass imports i.e. 1.1 loads per day. Using the larger ports

would reduce frequency to approximately one load every 10 days.

Assuming that either a volume (72m³) or weight (24t) restriction applies to road haulage between 26,100 and

26,760 truck journeys will be required to move the biomass from the ports to the CHP plants. Table 5 below

demonstrates the logistics involved in importing and transferring the biomass from the ports to processing

plant.

20 Resource Assessment for County Donegal Donegal Fuel Resource Survey and Biomass Demand November 2012You can also read