Open Future World Case studies - Case Studies ebook

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

BIANNUAL SERIES, VOLUME 1 Case Studies ebook MARCH 2021 Open Future World Case studies FEATURING Banco Original - Belvo - BNP Paribas - Brankas - CarFinance 247 - Cielo - Credit Kudos - Creditfix - DirectID - eCebuana - equensWorldline - Experian - Freetrade - Greater Than X - Hi Mum! Said Dad - Knab - Konsentus - Mercer - Mobills - Moneyhub - Nutmeg - Ordo - PFP Energy - Regional Australia Bank - Revolut - Schroders - Sensedia - Serve & Protect Credit Union - Snoop - Sugi - Target - Token - tred - TrueLayer SENIOR PARTNERS

FOREWORD OPEN FUTURE WORLD MARCH 2021

With thanks to our partners…

SPONSORS

SENIOR PARTNERS WELCOME

Welcome to the first Open Future World Case

Studies ebook – a collaborative effort to share

Moneyhub is the leading Open Finance platform that enhances the lifetime

financial wellness of people, their communities and their businesses.

some of today’s most interesting examples of

Moneyhub’s APIs and white label solutions power businesses - both from

within and from outside of financial services - with data connections and

intelligence, leveraging Open Banking payments to enable hyper-personalised

experiences that drive customer engagement.

open banking (and open finance).

We’d like to thank all the contributors and supporters who made this possible. It’s an

exciting time to be involved with the open finance community, and these case studies

illustrate just how quickly things are progressing:

• Open banking has a growing role in delivering new, better tools for credit /

Sensedia has extensive experience in helping financial services providers

affordability assessments. The pandemic has shown the community’s remarkable

develop and implement online solutions that enable them to thrive in an Open

ability to deliver new solutions, at speed.

Finance/Open Banking environment. With offices in the UK, Brazil and Peru,

• Consumer-facing apps can have real impact – whether that’s in improving

Sensedia is recognised by Gartner in its Magic Quadrant as ‘visionary’ and by

financial wellbeing or helping us save the planet. It feels as if we’re only in the NICK CABRERA

Forrester Wave as a ‘strong performer'.

early stages of exploiting this potential. CO FOUNDER,

OPEN FUTURE WORLD

• It’s a global movement, and Brazil is clearly one to watch – so brush up your

Portuguese!

• Open banking payments are taking off.

As well as highlighting the benefits that open finance is starting to deliver, this ebook

Token is an open banking payments platform driving the shift from traditional

aims to offer a deeper understanding of what’s involved – how banks, fintechs and other

payment methods to bank payments with best-in-class, Pan-European bank

partners are overcoming challenges to turn opportunities into reality.

connectivity, data and compliance capabilities. With Token’s complete toolkit,

merchants, PSPs, and banks create new capabilities and revenue streams

through our broad connectivity to banks. Token is both bank and developer. This ebook marks the launch of a new series, with the next issue planned for September.

Please get in touch with any feedback and suggestions for how we can improve, or if MARIE WALKER

Token Pay offers the simplest way to bypass traditional methods and accept

you’d like to be involved. CO FOUNDER,

faster, lower cost bank payments. Token Pay provides secure, unified access to OPEN FUTURE WORLD

banks in Europe to initiate real-time account-to-account payments straight

from apps and websites. All from a single interface.

About Open Future World

TrueLayer provides global financial connectivity through open APIs. Our open

banking platform empowers engineers, innovators and enterprises in every Open Future World brings together the best people and ideas from the world of open banking and open finance.

industry to create smarter financial services. Founded in 2016, TrueLayer is We’re supporting innovation and progress in this collaborative community, sharing useful insights and helping to

connected to major banks globally, backed by leading venture capital including

build relationships.

Tencent, Temasek, Northzone, Anthemis, Mouro Capital and Connect Ventures,

and trusted by some of the biggest names in fintech including Revolut,

• Our directory – offers a growing global Who’s Who for the community, helping members raise their profile

Trading 212, and Zopa.

and discoverability.

• The Daily News Edit provides a quick update on the latest news and views, building into a searchable archive

alongside interesting reports and videos.

• We host the global Open Banking World Congress and other virtual / live events.

If you would like to submit a case study, or work with us on future ebooks, please get in touch! www.openfuture.world

Editorial: marie@openfuture.world Partnering: nick@openfuture.world

2 Please follow or connect with us through LinkedIn and Twitter 3

INDEX OPEN FUTURE WORLD MARCH 2021

8 HOW OPEN BANKING POWERED QR CODE 14 PARTNERING TO TRANSFORM DIGITAL 22 AGILE COLLABORATION FOR PSD2 28 EMPOWERING RETAIL INVESTORS WITH

PAYMENTS WITH AUTOMATED GIFT AID FINANCE COMPLIANCE INSTANT BANK PAYMENTS

HELPED RAISE £12,000 AT A VIRTUAL Revolut / TrueLayer Knab / Konsentus Freetrade / TrueLayer

AWARDS DINNER TO TACKLE HOMELESSNESS How the partnership delivered a single app with Online bank Knab’s decision to adopt a Minimum Building and communicating a scalable payment

Moneyhub / Schroders simple account aggregation and funds transfer – Viable Product (MVP) approach before a planned solution amid surging demand. Seamless account

key to the challenger bank’s success refresh to provide a more open architecture, and funding offers better customer experience,

Direct instant payments – convenient for donors, Konsentus’ role in fraud protection improved deposit reconciliation and low costs

cost-effective for charities – offer a model for

micro-donations of the future. Convenience is the

biggest driver to positive behaviours, and finance

16 INSTANT ACCOUNT-TO-ACCOUNT (A2A)

is no different

PAYMENTS FOR FRENCH RETAILERS 24 HELPING EVERYDAY AUSTRALIANS 30 IN

Ordo worked with PFP to enable PFP call centre staff to

THE NEWS...PARTNERSHIP

either the Ordo App and Web solution, or the Ordo bulk

BNP Paribas / Token

UNDERSTANDhave

THEaccess

VALUE to aOF

fullyTHE CONSUMER

secure payment platform, News

uploadhighlights relating

capability when to partnership

sending from for

out mulitiple requests

DATA RIGHT: A BETTER APPROACH TO

myordo.com, allowing them to easily take instant payment recent months…

payment.

10 A MOBILE FINTECH APP FOR THE NEWLY How Token and BNP Paribas collaborated to

DISCLOSURE FOR FINANCIAL SERVICES

from their customers giving both parties confidence the PFP also utilised the Ordo Bridge tool for automatic upload

overcome the challenges of introducing a new

BANKED right amount has been paid and received into the right

Regional Australia Bank / Banking to be able to transfer

of requests for payment to be distributed, saving even more

Profit for Purpose energy

payment method company, PFPAEnergy,

Financial

- in a pandemic. big step and account. Ordo uses Open

X directly and instantly from a customer’s bank 32

time and money and taking the pressure off their business,

eCebuana / Brankas forward for instant A2A payments?

wellbeing Open Banking FinTech, Ordo, make communities better Greater Than

money THE OPEN BANKING CONSUMER CHAMPION

staff and ultimately customers.

account to the businesses bank account, by the business

A hybrid online-offline approach helping toEnergy is proud to be a not-for-profit energy company, A cross-functional collaboration to design

Snoop / Hi

As the Ordo Mum!

service Said

is entirely real Dad

time, the call centre staff

PFP sending a pre-populated digital and

request for payment to

deliver financial inclusion during the pandemic. A to call it ‘Profit for Purpose’. And Ordo is on a deliver the firsttheir

consumer-friendly, interactive CDR receives a secure can talk their customers through payment whilst they’re on

or as they like customer. The customer immediately

Using open banking for hyper-personalised

marketplace of cost-efficient services encourages 18 IN THE NEWS...A2A PAYMENTS

mission to make paying and getting paid easy, meaning policy – empowering consumers and building trust

link or text message which, within a few taps from their

the phone,

insights.

giving both parties

Collaboration

lowering abandonment of on

trust and confidence,

a process

payment of user

to nearly testing

0, unlike other

more transactions in-app, ultimately helping

everyonetocan control their finances…it’s a partnership with – now being openly shared through Australia’s

smart phone, they can authorise payment, directly from

News highlights relating to A2A payments from and continuous

remote improvement

and delayed payment methods.to develop the

push more merchants and products onto thatthe

warm fuzzy feeling. CDR Support Portal

their own bank account.

recent months…. customer experience and build trust

platform We’re pleased to have been able to provide PFP with a

As the country went into Lockdown on 23 March 2020, Ordo With Ordo’s secure bank transfer solution, both payer and

solution that has helped them, their customers and their

launched the UK’s first Open Banking enabled end to end business know they’ve been paid in real time, and the

community. PFP’s Head Of Service Delivery, Natalie

encrypted and wholly digitised request-for-payment service. business receives its money in instantly cleared funds in the

Brundish, says that “Ordo has meant we have been able to

20 THE ROLE OF AISPS IN BRAZIL’S OPEN

At a time when businesses had to find ways to survive

26 RESPONSIBLEaccount

LENDING IN UNCERTAIN TIMES 34 PROFIT

of their choice automatically correctly referenced.

FOR PURPOSE ENERGYthem

COMPANY

12 USING CREDIT BUREAU AND OPEN BANKING

themselves, adjusting to their entire staff working from Both parties know where they are, there is no security like

foster customer relations, supporting when they need

home, furloughed employees andBANKING RISING AND

USING ENRICHED OPEN us by FINANCIAL WELLBEING FINTECH MAKE

cardBANKING

compliance INSIGHTS

giving them a solution that’s easy and allows them to

TO IMPROVE AFFORDABILITY DECISIONS AND colleagues who had PCI DSS needed as no account details are

Mobills

become teachers overnight, they were / aBelvo

offering lifeline of ever shared and no card is ever used.

Serve & Protect Credit Union / COMMUNITIES BETTER

stay on top of their finances. We have been able to reduce

OPTIMISE CUSTOMER EXPERIENCE WHEN

payment holidays while their customers financially strug-

the burden on our staff working from home, often for the

Credit Kudos

By PFP using Ordo in their call centres, it meant PFP staff PFP Energy

and save/costs

Ordo

APPLYING FOR CAR FINANCE gled. How leading LatAm aggregator Belvo helped

had a solution they could readily deploy for use in real time

first time, so we can pass these savings on to

our customers through our tariffs and services.”

personal financial management app Mobills

Experian With cash tight, in 2021 businesses need efficient and

overcome the technical and data challenges in this

Developing a risk

withinsight dashboard,

a customer highgiving

on the phone, level support to both the Collecting payments in a crisis with an ‘efficient

At a time when people and businesses are under stress from

effective, but polite, payment solutions. metrics and ‘traffic light’employee

call centre flaggingand

system forcustomer at this already

the PFP but polite’ request-for-payment service. Giving call

Using different data to serve different types of emerging open banking market all directions, ease, security and certainty are what people

We all appreciate our key workers on the front line, and underwriters – stressful

and then evolving

time. new

PFP saves toolsasto

money Ordo is only 20p max per centre staff access to a secure real-time payments

crave, and that is exactly what Ordo delivers.

customer depending on the risk they present.

there are also essential services like energy, the staff for highlight individuals’ up-to-date financial position

request for payment sent, enabling it to continue pursuing platform

Check Ordo out, book a short demo or try for free

Levels of instant / automated decisions which

and overall

are, for the foreseeable future, now scattered into during the pandemic

it’s purpose of ploughing funding back into the community.

acceptances are up, with 80% of customers who

their individual (hopefully warm!) homes. All this was with zero integration. All PFP needed to do was

share via open banking offered finance register at myordo.com, (which takes 3 minutes, we’ve

How do you support a nation’s energy supply and collecting

payment from people in a crisis, with staff that are also in timed it!), connect the account they want to be paid into,

the same boat, working at home amidst unprecedented and use

change? Keeping a wide-ranging collaboration simple materials to ensure a positive experience, encouraging

Learnings from the Project team Outcome

The answer is, to look at what your customer needs, how This is a complex project involving BNP Paribas, Token, future uptake.

The decision to adopt a Minimum Viable Product (MVP) Knab’s attractiv

merchants and the French banking ecosystem. • Transaction fees. SEPA Instant fees are a potential bar

your business deliver it, and finding a solution that fulfils approach to creating the initial PSD2 service meant that a lot of interest

• BNP Paribas hosted a series of working groups with and make this method of payment most attractive for

those requirments. Knab was able to deploy APIs quicky without having to integrations wi

selected merchant clients, to identify key pain points higher-value purchases. A key aim of the pilot is to

re-engineer a CBS that was due to be replaced.

– such as the abandonment of high-value baskets by While

investigate how to incentivise use of the

the new busin

paymen

Lockdown has meant: Customers want: PFP Energy wants:

Agile collaboration for

This

customers with insufficient also

card gave

credit Knab

available theto

– and added benefit

method.of a first-hand significant AIS

A Financial MOT for consumers where 80% are worried Support Lower costs experience

more closely define the proposed in running a live platform

solution. • Frenchwhile finalising

bank APIs. PSD2-readiness packages, Knab

across Europe is

about money and are cutting back the design of the eventual solution. This provided the border PIS tran

• Getting buy-in from key BNP Paribas internal stakeholders still patchy, and while data APIs have largely stabilised

PSD2 compliance -

Certainty Security

confidence and knowledge to develop a sophisticated With gambling

40% of direct debit users plan to cancel at least one was a key requirement for the success of this radically payments has taken longer. There have been extensive

Security Auto reconciliation and optimal product which would not have been the bad actors, Kna

direct debit, with 40% moving to expensive cards and new proposition. The project team undertook a substantial

discussions and testing with different banks.

case otherwise. account data a

4

Knab / Konsentus 5 practical

30% to hard to process bank transfers and cheques Convenience Liquidity internal marketing and engagement program across • Coronavirus. The pandemic not only caused

checking servic

IT, security and compliance, with high-level security issues, but created a new urgency to the project and

Over 50% of people who cancelled direct debits won’t

validation required even to reach a pilot stage. new need. For e-merchants offering click-and-collect

put them all back once we’re out of lockdown

INDEX OPEN FUTURE WORLD MARCH 2021

36 THE APP THAT HELPS CONSUMERS GREEN 44 COVID AFFORDABILITY INSIGHTS – USING 50 RETHINKING THE MORTGAGE PROCESS 58 USING OPEN BANKING TO PROVIDE

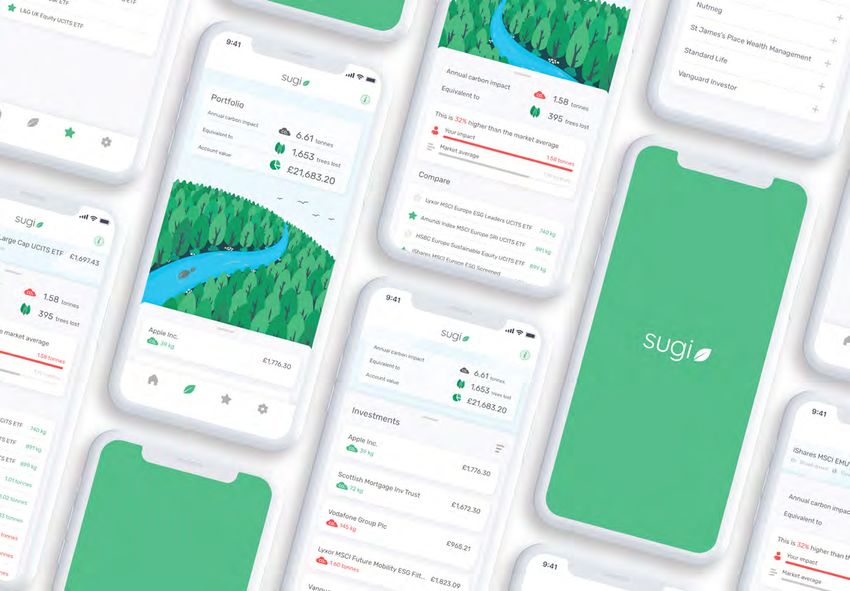

UP THEIR PORTFOLIOS USING THE POWER OF ECONOMIC FORECASTS, CREDIT BUREAU Target / DirectID PERSONALISED DEBT ADVICE TO CONSUMERS

OPEN FINANCE DATA AND OPEN BANKING TO HELP LENDERS The design principles and the reimagined

Experian / Creditfix

Sugi / Moneyhub UNDERSTAND THE IMPACT OF THE PANDEMIC process behind The Mortgage Hub, an end-to- Sharing credit and transaction data with debt

Making sustainable investing accessible for

ON CONSUMER’S FINANCIAL WELL-BEING end mortgage platform aiming to transform an advisers – providing faster, more accurate

experience that has remained largely unchanged

individual investors with portfolio carbon impact Experian information for better debt resolution. The time

for a hundred years taken to collect a customer’s financial information

assessments. Over 75% of UK retail investors want

New approaches to credit assessment in a fast- has fallen by 80%

their investments to have a positive impact – but

changing economic environment. Overlaying

few have been able to follow through

local economic forecasts with an individual’s bank 52 ENHANCED CREDIT DECISIONING IN MOTOR

transaction data enables a more personalised

response

FINANCE USING OPEN BANKING INSIGHTS 60 HELPING USERS TRULY ENGAGE IN

CarFinance 247 / Credit Kudos RETIREMENT PLANNING, WITH A SIMPLE,

40 CASH MANAGEMENT POWERED BY OPEN INTELLIGENT PENSIONS TOOL

BANKING Using open banking for an upgraded affordability

Mercer / Moneyhub

equensWorldline

46 EMPOWERING MORE RETAIL FINANCE and KYC process, with a streamlined customer

CUSTOMERS TO FIGHT CLIMATE CHANGE application journey – document collection time

reduced from 2 hours to 10 seconds – and the

Creating an app that looks beyond pensions,

Developing services to help SMEs overcome USING OPEN BANKING potential for further improvements

allowing individuals to manage all aspects of

liquidity challenges in partnership with alternative their personal finances in one place. Developing a

players – offering advanced but niche solutions, tred

dynamic – and continually tested – user experience

narrowed to address perfectly specific pain points to suit a broad range of users

The story behind pre-launch carbon-tracking

app tred. API and regulation challenges, and user 54 USE BAAS TO TAKE THE LEAD IN THE OB RACE

attitudes towards open banking

Banco Original / Sensedia 62 EMPOWERING CONSUMERS TO GET MONEY TO

42 FROM POS PROVIDER TO TECH INNOVATOR The story behind the Brazilian bank’s pioneering MARKET FASTER

Cielo / Sensedia strategy – now with over 50 fintech partnerships

48 IN THE NEWS...FINANCIAL INCLUSION and 2 year growth in account holders of over 500%

Nutmeg / TrueLayer

The open innovation strategy behind the News highlights relating to financial inclusion

transformation of Brazil’s leading electronic The advantages of fast, low cost open banking

from recent months….

payments provider, and the extraordinary breadth payments – and the importance of customer

of its solutions and partnerships experience in encouraging consumer acceptance

In addition to a full-service p

64 OPEN FUTURE WORLD DIRECTORYinsurance, mobil

platforms,

Featured Premium Organisations

Use BaaS

PicPay – the largest digital w

HE CHALLENGES WE’VE FACED Unit, managing 50+ partner

early stages of open banking integration posed

Open competition

to take the

eral hurdles, the biggest of which were:

Banco Original believes tha

customer experience will be

eciding whether to build our own open banking stimulating competition, te

lead in the

tegration, or go with a third party provider – and innovations, this sector is a

so, which one. Both options come with different

But only those fastest off th

rty open banking providers available. Finally we succeed. Judging by Banco

OB race

ecided to partner with Plaid, based on the range of the start of its digital journe

oviders they support. This ensures as many people had grown to 4 million, an i

possible can use tred, and will put us in good stead

r international expansion.

consistencies

6 between each bank's open banking 7

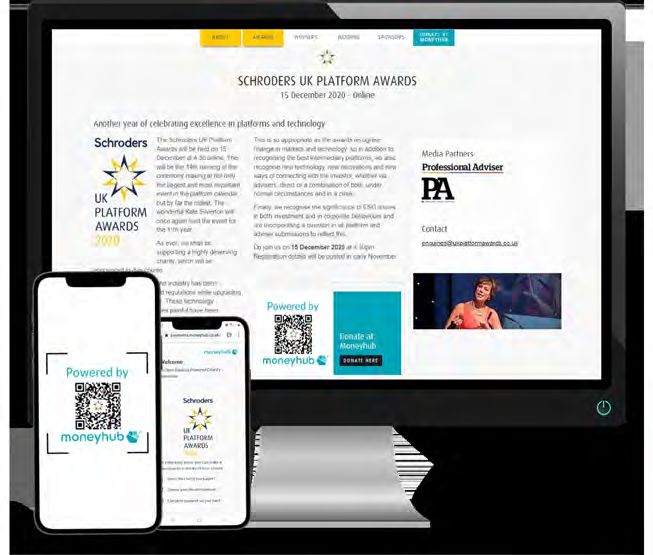

MONEYHUB / SCHRODERS OPEN FUTURE WORLD MARCH 2021

OPEN BANKING FOR GOOD The benefits to charities are endless:

How Open Banking • No more credit/debit card fees, or platform

fees (such as when donations are taken

through Just Giving or similar)

powered QR code payments with • No need to spend on Point Of Sale (POS)

PIN pads or contactless card readers

ABOUT MONEYHUB

Moneyhub is the leading Open Banking and Open

automated Gift Aid helped raise • Instant bank-to-bank payments appear in

the charity’s bank account straight away,

improving cash flow

Finance platform that uses the power of data, intelligence

and payments to enhance the lifetime financial wellness

of people, their communities and their businesses.

£12,000 at a virtual awards dinner • Charitable donations are boosted by 25%

Gift Aid – automatically

Moneyhub’s APIs and white label solutions power

businesses - both within and outside financial services.

to tackle homelessness Schroders UK wanted to harness the benefits of this

technology at their 2020 Platform Awards on the 15th

Find out more at www.moneyhubenterprise.com

or contact hello@moneyhub.com

December, to raise money for their chosen charity

Aims Providence Row, a charity that is tackling the root causes

2020 was a difficult year for charities. Not only have large donor’s consent. UK-based donors can pay directly from

of homelessness. Due to the ongoing pandemic, the awards requires building user trust to enable take-up to reach

fundraising events been postponed or cancelled, but social their bank account to the charity’s account without using

ceremony was to be held online – meaning simple, rapid its full potential – trust that needs to be built over time,

distancing and the demise of cash have also made charity a credit or debit card, and avoiding the complexity of setting

payments were vital to encourage donations. and with education to promote understanding.

canvassing harder. This has meant that charities have up payments in their online banking app.

Most attendees would attend the event on a computer – With the rapid pace of digital transformation that has

struggled to generate income at a time when help Now that fewer people are carrying cash, scanning a QR

so picking up a smartphone and scanning a code on screen occurred in response to the pandemic, the likelihood is that

is needed more than ever. code on the side of a collection bucket, a bus stop poster

represented an easy user journey, with no need to navigate this won’t take long – soon, QR code charity donations will

In September 2020, Bristol-based fintech Moneyhub or Big Issue Magazine means instant, cash-free transactions.

away from the event itself through another on-screen likely be a common sight at bus stops, petrol stations and

launched the world’s first Open Banking powered QR code The payment uses the same Faster Payments

window – potentially missing the action. For those who posters on the London Underground. With micro-donations

payments with Gift Aid, specifically to benefit charities. infrastructure as common bank transfers, meaning it’s fast

couldn’t scan the code, a clickable link was available, now cost effective, and the ability to provide individualised

The Open Banking payment technology is triggered when and safe, but with the huge added benefit of being a lot

allowing users to donate via desktop. financial experiences, it is possible to make donations much

the QR code is scanned with a smartphone, or a link clicked more cost efficient – and in Schroder’s case, free.

more personalised. We expect to see micro-donations where

on a website. This enables users to easily make a donation Moneyhub can reduce payment fees by 90% compared

Implementation people automatically donate based on personalised rules –

to a charity through Moneyhub’s Open Banking Payment to card transaction fees, meaning every pound donated

Moneyhub worked with Schroders on the project, creating for example, every time they buy a coffee, an equal donation

API, which can only be accessed and initiated with the can go a lot further.

a specific QR code for the Schroders UK Platform Awards could be made to their favourite charity.

website and publicised throughout the event. The payment Convenience is the biggest driver to positive behaviours –

journey is simple: the user opens the camera on their and finance is no different. Moneyhub’s technology means

smartphone and hovers over the QR code to initiate the payments can be made faster, more securely and at a lower

Open Banking payment journey. cost. With cost and unnecessary friction reduced, payments

become something that happens as part of an experience,

Outcome rather than as a distraction to it. This means it’s easier than

With match funding from Schroders, the total amount raised ever for people to save for their future or donate to charities

for Providence Row at the event was just under £12,000, with they care about. As we look forward, it really feels as if we’re

UK-based donors £3,000 as the biggest single donation. Moneyhub is leaving at the start of a payment revolution – and the future of

can pay directly from the service running for a year to allow Providence Row to payments starts here.

their bank account to the continue to benefit at future events.

Card-based donation platforms such as Go Fund Me, Just

charity’s account without Try it for yourself...

Giving or similar could see Providence Row losing as much

using a credit or debit as 9% of the total donation amount to fees (dependent

card, and avoiding the on platform), but with Moneyhub’s QR code payments, Scan the code to

Powered by

complexity of setting up Providence Row keeps 100% of the donation. donate to Providence

payments in their online Row. If you’re not able

Challenges and learnings to scan the code,

banking app. The results of the launch night were undeniable, but there visit:

are further developments which could be made. As seen

https://payments.

during the launch of contactless cards, new payment

moneyhub.co.uk/

methods can be met with trepidation from users, and early schroders

adoption of the QR code Open Banking payment technology

8 9

eCEBUANA / BRANKAS OPEN FUTURE WORLD MARCH 2021 10 11

EXPERIAN OPEN FUTURE WORLD MARCH 2021

USING CREDIT BUREAU AND INSTANT

DECISION

OPEN BANKING TO IMPROVE

9%

UP BY

AFFORDABILITY DECISIONS AND AUTOMATICALLY

OPTIMISE CUSTOMER EXPERIENCE ACCEPTED

5%

UP BY

WHEN APPLYING FOR CAR FINANCE

Aims Implementation Outcomes and learnings

This global luxury car manufacturer set itself the The organisation chose to deploy a combination of data Deploying the service enabled the manufacturer to stay ahead of many of its

task of improving its risk assessment process and from Experian including: competitors in analysis of a customer applying for vehicle finance. Access to

reducing the assessment time of a consumer’s bureau data along with new innovative sources of data such as Experian’s trended

• The latest version of its Delphi credit score to

credit worthiness by minimising manual intervention credit information and Open Banking has enabled them to optimise deployment and

understand a customer’s current credit status

in applications. It was essential not to reduce the streamline their credit decisions.

volume of customers accepted for credit, and to • Trended credit data to inform future credit The volume of customers that receive an instant decision on an application has

automate and improve the accuracy of its affordability performance of the individual increased by 9%, with a further 5% increase in the volume of customers who are

checks, whilst making the customer experience as

• Summarised current account data sourced from its automatically accepted for credit.

frictionless and non-intrusive as possible.

bureau to verify an individual’s income The innovative use of Open Banking has enabled the organisation to reduce the

They took the decision to look at a variety of existing time taken to source bank statement data to inform a credit decision from days to

• Automated categorised bank transaction data

and new sources of data to inform and improve its minutes. Data sharing can take place in the dealership, with initial approval for the

sourced – with consent – from a customer’s current

assessment of credit worthiness. This data included loan given in minutes ensuring the dealer can make a sale, and a customer given

account in real-time using Open Banking

the latest credit scores, trended credit information, approval to purchase the car. 80% consumers who agree to share their data via

summarised current account data and detailed bank The data was used for all new vehicle finance Open Banking are offered finance.

transaction data sourced from Open Banking. applications and deployed across the organisation in

Using 12-months of transaction data from Open Banking allows for a more detailed

its engagement with consumers. Registered office address:

An implicit part of this exercise was the principle that assessment of a consumer’s affordability. This ensures the manufacturer can apply

The Sir John Peace Building,

different data can be used to serve different types of Data was sourced in real-time using RESTful APIs and the highest possible regulatory standards to its affordability decisions to deliver Experian Way,NG2 Business Park,

customers depending on the risk they present to the secure URLs to automate credit decisions, whilst a better outcomes for the customer and the manufacturer. Nottingham,NG80 1ZZ

Tel: 0844 481 5638

organisation and value of the car being purchased. web-hosted analytics dashboard was provided to help

The experience of Open Banking has been used to enable additional identify www.experian.co.uk

This approached allowed the manufacturer to with interpretation of categorised bank statement data

verification checks to take place on consumers who want to buy cars online rather © Experian 2020. Experian Ltd

optimise is use of the data to ensure it maximised acquired via Open Banking. This was used to support is authorised and regulated by

than visit a dealership. This has proved particularly useful in the Covid crisis where the Financial Conduct Authority.

its performance whilst creating a more streamlined manual underwriting reviews where a more detailed

online sales have been used as an alternative channel to sell cars to customers Experian Ltd is registered in

experience for customers. analysis of an individual’s finances was required. England and Wales under company

who don’t want face-to-face contact with a dealer. registration number 653331.

The word “EXPERIAN” and the

graphical device are trade marks

For further information of Experian and/or its associated

companies and may be registered

To find out more about how Experian empowers consumers and businesses to in the EU, USA and other countries.

The graphical device is a registered

take control of their finances using open data, contact us on the Directory: Community design in the EU.

WWW.DIRECTORY.OPENFUTURE.WORLD/BUSINESS-DIRECTORY/1194/EXPERIAN All rights reserved.

12 13

REVOLUT / TRUELAYER OPEN FUTURE WORLD MARCH 2021

Partnering with Revolut to

transform digital finance

THE CHALLENGE

Most Revolut customers have a high street bank

account alongside their Revolut account. This made Next, Revolut began using TrueLayer’s Payments API to

it difficult for them to get a complete view of their enable customers to top up and access funds instantly, in

real- time, without having to enter card details or share

With TrueLayer, Revolut enables finances without having to log into multiple websites

and apps. Another problem for Revolut and its their bank credentials. With the Payments API, funds are

customers to manage all of their customers was the cost and complexity associated with transferred directly between bank accounts rather than

finances from a single app. adding funds to a Revolut account. Topping up using through a separate payment network, which minimises

cost and processing times. Payment authorisation takes

traditional methods such as manual bank transfers

Revolut’s ambition is to build a truly global bank that was time-consuming for customers, requiring them place directly with the bank, making the entire process

enables people to manage all of their finances seamlessly to log into their external bank’s website or app to set extremely secure.

from one place. To achieve this, they needed an easy way up and initiate a payment. While adding funds using

to connect their app to external bank accounts, and a a credit or debit card was also a disjointed experience THE RESULTS

payment method that eliminated high transaction fees. for customers and came with a high-risk of fraud and

This led them to TrueLayer. additional transaction fees for Revolut. Today, Revolut uses TrueLayer to enable customers to

instantly link external bank accounts to the app, and to

facilitate top ups and transfers between accounts. This has

The Revolut team were looking for a way to fix

2x Increase in weekly resulted in numerous benefits for Revolut, including:

these broken processes which ultimately resulted in

active users unnecessary costs and mismatched financial products

for customers. They also wanted to contextually - 2x increase in weekly active users

introduce customers to the new financial products that - £600M+ in payments processed with significant cost

Revolut had to offer in a way that was tailored to the savings

£600M+ In payments

processed with

needs of each customer. Using TrueLayer, Revolut were

able to instantly leverage open banking to do this.

When deciding which provider to work with on its open

significant cost banking launch, Revolut chose to work with TrueLayer

savings THE SOLUTION because of its scalability and superior developer experience.

The process to get up and running and start experimenting

First, the team began using TrueLayer’s Data API, with TrueLayer was quick and painless and the Revolut

enabling their customers to connect their external team found the TrueLayer platform to be robust and

bank accounts to Revolut in a few clicks. This developer-friendly.

gave customers greater visibility and control over

spending and budgeting. This also meant Revolut

could recommend new products to help customers

save on things like loans, credit cards, overdrafts,

and international transfers. Delivering a seamless

experience to Revolut’s UK retail and business

customers was hugely important. The team wanted

customers to get instant value from the wide variety of

new features they were building.

14 15

BNP PARIBAS / TOKEN OPEN FUTURE WORLD MARCH 2021

Keeping a wide-ranging collaboration simple materials to ensure a positive experience, encouraging

This is a complex project involving BNP Paribas, Token, future uptake.

merchants and the French banking ecosystem. • Transaction fees. SEPA Instant fees are a potential barrier

• BNP Paribas hosted a series of working groups with and make this method of payment most attractive for

selected merchant clients, to identify key pain points higher-value purchases. A key aim of the pilot is to

– such as the abandonment of high-value baskets by investigate how to incentivise use of the new payment

customers with insufficient card credit available – and to method.

more closely define the proposed solution. • French bank APIs. PSD2-readiness across Europe is

• Getting buy-in from key BNP Paribas internal stakeholders still patchy, and while data APIs have largely stabilised,

was a key requirement for the success of this radically payments has taken longer. There have been extensive

new proposition. The project team undertook a substantial discussions and testing with different banks.

internal marketing and engagement program across • Coronavirus. The pandemic not only caused practical

IT, security and compliance, with high-level security issues, but created a new urgency to the project and a

validation required even to reach a pilot stage. new need. For e-merchants offering click-and-collect, a

• Token’s white-label solution for PSP resellers was further safer, dematerialised alternative to cheques has become

extended, simplifying configuration and roll-out for a priority.

merchants whilst allowing BNP Paribas to fully manage,

onboard and support their clients. A Big Bang for Instant A2A Payments?

• Token’s platform enabled a fully-branded BNP Paribas A successful pilot will be an exciting realisation of the EBA’s

merchant portal. By presenting the new service as just vision of combining two major initiatives, using PSD2 APIs

Instant Account-to-Account another BNP Paribas service – keeping Token’s role behind to drive traffic to the SEPA instant payment rails. It will have

the scenes – the potential for merchant/consumer created a new payment method for French e-commerce

merchants, of particular value to merchants selling higher-value

(A2A) payments for French

confusion was minimised.

• The whole project also relies on making sure that other goods and services.

banks are ready to fulfil their side of the payment. In open

retailers — BNP Paribas / Token banking terms, payments are more demanding than data The merchants involved in the project working group have

suggested an aim of migrating between 2 to 5% of all

– reliable API performance is essential.

transactions to the new payment method – a significant share

Payments are a continuing and complex challenge for The first merchants went live in February 2021 and showcase of a French e-commerce market worth well over €100 billion.*

the flexibility of the solution, from instore payments with a pilot BNP Paribas, one of the world’s largest banks, has access to a

ecommerce merchants. BNP Paribas saw the opportunity

across 200 stores to traditional ecommerce payments for huge range of merchants, and the potential to integrate this

for a new solution, combining PSD2 APIs with SEPA Instant online merchants. This will help to provide feedback from every solution across different platforms. Against the background of

payments to allow e-commerce merchants to accept instant region in the country, and different demographics helping BNP the wider open banking and open finance movement, we are

moving towards a big bang in payments.

A2A payments. The bank looked to Token – with their focus Paribas learn more about customer reactions and the potential

for new services.

on payments, connections to almost 100 French banks

representing about 80% of payments’ accounts in France, Innovating in a Pandemic

understanding of the retail payment channel and technology While getting internal buy-in and security validation were

demanding, these are challenges that are foundational for

stack – as their partner.

almost any bank/fintech collaboration. (It helped that Token is

ISO 27001 and PCI-DSS accredited.)

There were several more specific challenges: * https://ecommercenews.eu/ecommerce-in-france-will-

reach-115-2-billion-euros-in-2020/

• Novelty. Both merchants and consumers will need to

understand how to take advantage of this new payment

method, the first to combine PSD2 and SEPA into a single Find out more about BNP Paribas payment

offering in Europe. BNP Paribas is developing support solutions and Token’s open banking platform.

https://token.io/

16 17

In the news

A2A GO A shift is

Open Future World’s highly acclaimed daily edit of the most interesting

global news headlines provides a rich archive of information, charting progress.

coming

Here are some highlights relating to A2A payments from recent months….

The problem with payments, Payment initiation services: As pioneers in open banking, Token set out

11:FS' Sarah Kocianski [A2A Open banking's big bang in

payments and how to get 2021? Yolt's Leon Muis [certainly to help banks clear the decks of regulatory

there]... feels like a lot of momentum

complexity in 2016.

building for A2A/PIS]...

Today, Token is driving the shift from card

to bank payments with best-in-class,

Pan-European bank connectivity, data and

Open finance platform Subscriptions are shaping the

Ecospend wins UK’s HMRC payments landscape as we compliance capabilities.

open banking contract for A2A know it, Nuapay's Nick Raper

payments… [A2A for Variable Recurring

Payments].. Tomorrow? Subscription payments,

merchant-initiated payments, automated

sweeps, and request-to-pay.

A2A payments provider Mastercard adds A2A And that’s just the beginning.

VibePay launches SME functionality for US business

service… payments…

Follow Token on LinkedIn as we drive the shift

Survey results reveal UK Payment methods: what's

consumer payment card new and what's next, The

concerns, Nuapay [opportunity Paypers' Anda Kania [overview

for open banking A2A of developments including A2A

payments]... payments via open banking;

convenience, cost and reach

are key]...

formerly known as

Try searching the openfuture.world hub for country, company or topic insights & links to the full articles...

18 19MOBILLS / BELVO OPEN FUTURE WORLD MARCH 2021

Use case

One example of how fintechs can benefit from Open Banking is the work that has been developed at Mobills, a money

manager and budget planner app that allows users to create a custom monthly budget and, from there, be in full

control of their finances. Through the application, users can manage their money, track all their credit card spending, set

The role of AISPs in Brazil’s up budgets and plan their financial life, all in one place.

For a personal financial management application to meet their purpose at least one thing is essential: getting categorized

Open Banking rising

transaction data from customers. It was easy for customers to categorize their manually-registered transactions, however,

for the whole process to be automated, a solution that not only collected data from the bank but also offered a reliable

description of each transaction was required.

How Belvo is helping build the next generation of financial services

through technology and Open Banking

The opportunity

Open banking is expected to set the right ground rules for easier data access/sharing in Brazil. Tight deadlines have been

Belvo helps us make the data collection process faster

established by the Central Bank for the largest financial institutions in the country (S1 and S2, the TOP5 banks in Brazil),

to adapt to the new model. There is a lake of opportunities for Open Banking, but the challenge relies on the means, or

and to pay more attention to analyzing this data to

the technology, to reach them. bring more insights to our customers. We have more

categorized transactions that can be shared with the

The challenges customer the moment our platform has access to it

Few are those talking about the technical challenges that banks are facing in the country. Not just at an API level (still

under construction) but also at a deeper level within their core and data bases. Requests to the database or data lakes will

grow exponentially as users start enabling access to a new myriad of fintechs. In today’s scenario, where users typically Rodrigo Matihara, CTO at Mobills

connect to their banks’ app once a day, it might represent 15 to 20 daily connections by all these new fintechs and apps

utilizing users’ banking data to offer new services under Open Banking.

And talking about data, this is the second challenge and one of the most difficult. Data quality from banks tends

And even if Mobills were to integrate with each bank in Brazil, which was already proved to be challenging due to the rigid

to be very poor when it refers to transaction descriptions. Banks typically rely on internal codes in order to manage

structure the biggest and most traditional banks currently have in the country, they would need a way to have all this

data flows properly from system to system and ultimately to bring information to their digital channels (internet and

information ready to be accessed by the consumer, in a standardized way.

mobile banking). There is also no standardization between financial products available from bank to bank. So all that in

conjunction, becomes a bigger challenge to whoever manages to get their hands on this “newly” available banking data.

“Open Banking has allowed us to bring all information in one single

statement to our customers. The automation makes it even more

The solution convenient and expands our customer range,”

adds Rodrigo Matihara.

With the current “pre-open banking” scenario in Brazil, alternative data access technologies are already available. The

challenges posed by this scenario are basically the magic sauce of AISPs (Account Information Service Providers) also

Once the integration was established, Mobills started noticing an increase in the number of users that did not want to

referred to as “Aggregators”. Belvo, an API platform focused on the Latin American market, is offering the technology

manually insert every detail of their spending and felt more comfortable with having all the information automatically

fintechs need to access all the benefits from Open Banking.

available to them.

Understanding bank’s products, labelling incoming/outgoing transactions, simplifying merchant names, categorizing,

There is an interesting perspective for Open Banking in Brazil as it could lead to an increased financial inclusion and

detecting recurrent transactions, incomes, is just some of the initial and complex work that needs to be done on top

education, helping Brazilian consumers have more control over their money and opening room to fintech companies

of these connections so players in the fintech industry can concentrate on providing financial products and services

to innovate and build better services for a digital savvy population.

to millions of users in Brazil in different segments, from credit and lendings to personal financial management.

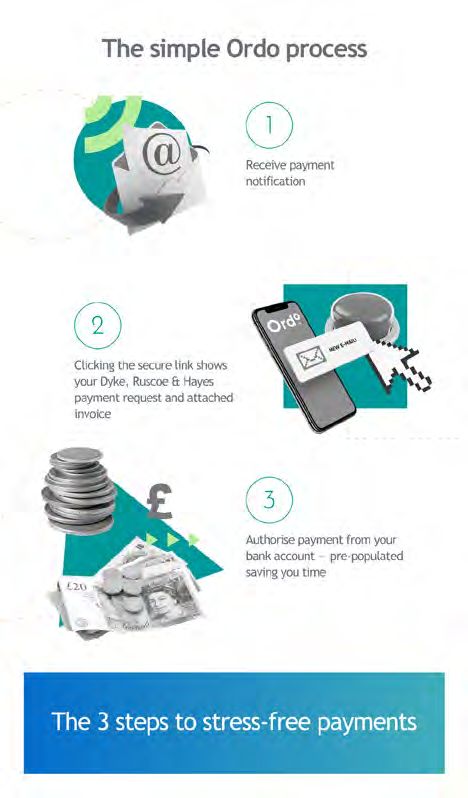

20 21KNAB / KONSENTUS OPEN FUTURE WORLD MARCH 2021

Learnings from the Project team Outcome

The decision to adopt a Minimum Viable Product (MVP) Knab’s attractive customer demographic has generated

approach to creating the initial PSD2 service meant that a lot of interest from many TPPs. To date there are active

Knab was able to deploy APIs quicky without having to integrations with over 30 TPPs from across the EEA.

re-engineer a CBS that was due to be replaced.

While the business accounts of the self-employed drive

Agile collaboration for

This also gave Knab the added benefit of a first-hand significant AIS transactions to support accounting

experience in running a live platform while finalising packages, Knab is also seeing a large number of cross-

the design of the eventual solution. This provided the border PIS transitions to the big gaming companies.

PSD2 compliance - confidence and knowledge to develop a sophisticated

and optimal product which would not have been the

case otherwise.

With gambling being a potential target for fraud and

bad actors, Knab’s customers can rest assured that their

account data and funds are being protected by the TPP

Knab / Konsentus checking services Konsentus Verify provides.

Summary

When they approached Konsentus, they were also The number of connected TPPs and the transaction flows that are already being seen through the platform across

Knab discusses how Konsentus Verify allowed conscious that their PSD2 project was late off the starting multiple markets has justified Knab’s two-phased approach. Their customers are taking advantage of the latest

them to improve the level of security needed blocks and so were looking for a trusted, secure, quick products and solutions from across the EEA to better manage their financial data and information showing open

to protect customers from the risk of Open and effective way to validate TPPs (third party providers) banking at its best.

Banking fraud as part of their overall Open Banking solution.

We take pride knowing that Konsentus Verify was key to both this early delivery and the migration to the new

Knab, a Dutch subsidiary of AEGON The Integration Project architecture. Knab’s customers can now have confidence and trust when transacting in the open banking ecosystem,

Netherlands, was initially set up in 2012 as a knowing that their data and funds are being protected from the risk of fraud.

The team at Knab chose to build their PSD2 service in a

consumer bank offering an affordable online

phased approach. They initially built an interim solution

checking account with smart tools to save

within the constraints of their existing Core Banking

money backed up by excellent customer

Solution (CBS) with the pragmatic approach to quickly

service.

getting a service into market.

Since 2014, the focus has been on business

This initial phase did not have an optimal customer

banking, servicing the needs of the self-

journey or registration process, although it did allow their

employed. And their ‘Knab Zakelijk’

customers to use the services of TPPs and was seen as

has consistently been voted the most

a viable short-term solution whilst the full service was

advantageous business account by MoneyView.

being developed.

The planned refresh of the CBS to provide a more open

architecture, is readily supported by the ‘plug and play’

Background and challenges

Konsentus Verify solution and will allow them to focus

With a customer base actively engaged with different

their efforts on driving significant improvements to the

third-party providers from across Europe, offering

customer experience and other value add features.

innovative accounting and book-keeping solutions, Knab

was aware of the security provisions that needed to be Implementing the Konsentus Verify API to perform TPP

put in place to provide a trusted and safe ecosystem, identity and regulatory checking services saved the team

protecting their customers from the risk of open banking considerable time, technical know-how, legal knowledge

fraud. and of course on-going support and maintenance, whilst

providing a future-proofed solution for a key business “Knowing that we have Konsentus actively

As a specialist online bank, Knab needed to provide its

line. supporting us to provide this vital aspect of

Open Banking service without the support of a large

development project team or investment in additional The service is now fully operational with transactions security in our gatekeeping gives us peace of

infrastructure. In addition, their existing Core Banking being checked by the Konsentus Verify platform from mind. Konsentus Verify is reliable, consistent,

System (CBS) presented challenges and building their across the EEA. The Knab account holders can be and always available – keeping our customers

PSD2 APIs was far from straight forward. They therefore confident that no matter which TPP services are being

safe whilst providing an airtight story for our Further information:

needed to find a solution that would meet their security used, or authority the TPP is regulated by – be that Isabel

requirements whilst being easy to implement. in Belgium or Neo Finance in Lithuania - their data and regulators. What more do you want!?” Visit www.konsentus.com or

funds are being protected.

Ronald van der Horst Product Owner, Knab

contact us at info@konsentus.com

22 23REGIONAL AUSTRALIA BANK / GREATER THAN X OPEN FUTURE WORLD MARCH 2021

Helping everyday PROJECT AIMS

1. To help Australian consumers better understand the

KEY OUTCOMES

Together, Regional Australia Bank and Greater Than

Australian’s understand benefits of data sharing within the Consumer Data

Right Framework

X delivered the first interactive Consumer Data Right

Policy, contributing to Regional Australian Banks' CDR

the value of the Consumer

2. To meet Regional Australia Banks’ regulatory accreditation. Thanks to the openness of Regional Australia

requirements for a Consumer Data Right Policy, and Bank and its leaders, we shared the entire approach and all

related assets openly so that it might be simpler and more

3. To demonstrate a differentiated approach to

Data Right: A better

cost effective for those that follow:

disclosure that could help set a new, consumer-

https://cdr-support.zendesk.com/hc/en-us/community/

friendly standard for the entire Financial Services

posts/900001418303-How-to-create-an-engaging-and-

approach to disclosure

ecosystem.

compliant-CDR-Policy

To date, with hundreds of people actively interacting with

THE IMPLEMENTATION PROCESS

for Financial Services

and engaging with the entire experience, the policy has

received an average rating of 4.9 (out of 5). This is a huge

Instead of leaving the policy ‘design’ to risk and early win, particularly given the negative relationship most

governance - as is commonplace in most organisations consumers have with disclosures of this type today.

- Regional Australia Bank brought together a diverse

team that consisted of lawyers, risk and governance

professionals, copywriters, designers and experts in FOR MORE INFORMATION

evidence-based Better Disclosure from the Greater Than

X team. This enabled cross functional collaboration and Nathan Kinch (CEO of Greater Than X) and Rob Hale (Chief

specific practices like pairing or tripling, throughout Digital Officer of Regional Australia Bank) presented this

the duration of the program. This gave us a brilliant exact case study in detail at Web Directions, a global

foundation from which to do good work. conference for product professionals. You can watch that

presentation here: https://vimeo.com/485365972/754e474cc0

The process started with Better Disclosure workshops.

This was supported by basic policy drafting and in

intensive rules mapping exercise. This supported

For more information about Greater

ticking the boxes with more innovative and modern

approaches. The entire process, although operating Than X, here is their website

within the very tangible constraints of the Consumer www.greaterthanexperience.design/

Data Right Rules, was guided by very clear and distinct

consumer outcomes focused metrics.

And to see the policy in action,

The output of the experience we all engaged in

uses information design patterns, like time to read

click here:

indicators, layered information and illustrations, to help www.regionalaustraliabank.com.au/

bring the policy experience to life and enhance active

our-cdr-policy/our-cdr-policy

engagement and comprehension.

Although there were many hurdles - like overcoming

The problem is well understood. Using The Better Disclosure Toolkit, the status quo bias, challenges of interpretation and

meaning, specific budget and resource constraints that

Traditional policies or disclosures a combination of approaches limited implementation and forced team members to

are long, complex and often hidden informed by Human Centred Design, upskill in order to get the job done - the teams from

away. This leads consumers to the behavioural sciences and Greater Than X and Regional Australia Bank delivered

this market leading experience ahead of time. This gave

feel powerless and apathetic. traditional legal practice, Greater Rob, Regional Australia Banks’ Chief Digital Officer, the

This results in an overwhelming Than X and Regional Australia Bank opportunity to openly share what was being done and

what everyone was learning with other organisations

majority of people bypassing grappling with the same issues. This helped establish a

these disclosures altogether. But it more open dialogue about what was possible and how

doesn’t have to be this way. It can Data Right policy. The best part? The best to deliver consumer outcome focused policies and

disclosures. Although it’s too early to say, we hope this

be better. people actively interacting with it begins setting a new standard for disclosures down under.

seem to love it!

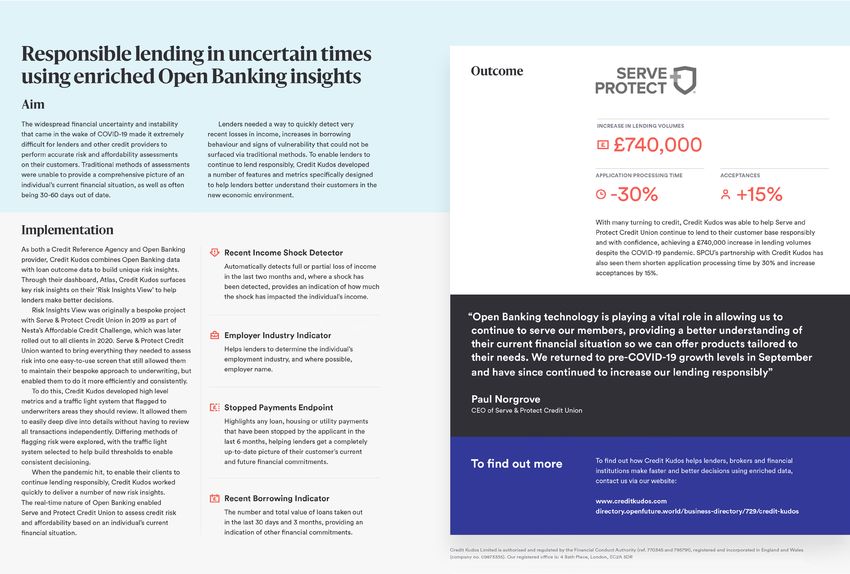

24 25SERVE & PROTECT CREDIT UNION / CREDIT KUDOS OPEN FUTURE WORLD MARCH 2021 26 27

FREETRADE / TRUELAYER OPEN FUTURE WORLD MARCH 2021

Empowering retail THE CHALLENGE

Before partnering with TrueLayer, Freetrade and its

The result was a simplified in-app deposit flow for users,

with cost-effective processing and less operational burden

for Freetrade. Its customers can now make payments

investors with instant customers were finding existing payment methods

painful.

quickly, and for Freetrade, the payment parameters are

all present and ready to be automatically allocated. This

bank payments –

Manual bank transfers were popular but they required simple, low-friction way of depositing is scalable and

users to manually switch between online banking fundamental to the business’ next phase of growth.

screens and the app, copying and pasting details. This

Freetrade / TrueLayer was a clunky experience that often led to drop-off, or

churn as customers made mistakes and looked for an

easier way to make deposits.

OUTCOMES

Implementing the payments API enabled Freetrade to

The Freetrade team were also experiencing issues reduce manual bank transfers from 90% of total deposits to

processing payments. If a deposit had been made just 25% and cards to 5%. In turn, this allowed Freetrade to

without the right information, it would be difficult reduce their total unallocated deposits across all payment

to reconcile. At one point as much as 10% of deposits methods from 10% to just 3% and make significant savings.

were unallocated, meaning Freetrade had to send Just a few months after launch, Freetrade saw a 60%

back £300,000 each month to customers for deposits increase in the total value of open banking deposits, while

they were unable to match. This caused operational the total number of open banking transactions went up

strain, which grew with the business, as more and more by 35%, and the average transaction size increased by 18%.

deposits ended up in the unallocated pool. This validated the payments API as a real growth driver for

Freetrade consistently ranks as the The alternative – card payments – was simpler for Freetrade: not only are more people choosing it, but repeat

first or second largest retail broker customers, but with card networks designed for customers are happy with the payment flow, meaning

purchases (rather than money transfers), the cost they’re ready to deposit more money.

on the London Stock Exchange (LSE) was too high for this to be Freetrade’s primary More than two thirds of all deposits now go through

according to volume of daily orders, payment method in the long term, especially for TrueLayer’s Payments API. TrueLayer was able to support

having grown its customer base high value transactions. The team needed to find a and enable Freetrade through unprecedented growth –

with more to come.

scalable solution that would deliver a great customer

seven fold to 350,000 in 2020. The experience.

GameStop media sensation this year To find out more about payments

led to another surge in customers, IMPLEMENTATION with TruLayer, visit:

with daily sign-ups increasing 10x Freetrade chose to implement TrueLayer’s Payments truelayer.com

at the end of January. With such API. The key to this implementation was getting a

strong growth, Freetrade needed scalable solution up quickly so TrueLayer and Freetrade

had to work closely together.

a payment solution that could TrueLayer’s Client Success and Integration teams

scale with them, reducing their

operational burden and cost,

worked with Freetrade to help them build, test and go

live successfully with open banking payments, and to

keep track of success measures like payment method

70% reduction in total

unallocated deposits

while keeping new customers

60% increase in value

adoption, conversion and average transaction value.

happy with a seamless account In August 2020, Freetrade rolled out open banking

of open banking

funding experience. payments via TrueLayer to Android and then, shortly

afterwards, to iOS users. It’s now available to all new deposits

and existing customers.

18% increase in average

The TrueLayer team worked with Freetrade to give

recommendations on how to optimise the user flow for

conversion and how to position and communicate the transaction size

new payment method with customers. To encourage

2/3 of all deposits go

adoption, Freetrade has also implemented measures

including making this payment method top of the list

in the user flow, adding a ‘recommended’ label and

through TrueLayer’s

capping deposits on cards and ApplePay. Payments API

28 29You can also read