Polar Capital Technology Trust plc AGM Presentation 2020

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Polar Capital Technology Trust plc AGM Presentation 2020

Results as at 30 April 2020

Year ended Year ended Change

30/04/19 30/04/20 (y/y)

Net Assets £1,935,646,000 £2,308,597,000 +19.3%

NAV per ordinary share 1446.40p 1715.59p +18.6%

Price per ordinary share 1354.00p 1774.00p +31.0%

Benchmark Change +18.1%

Ordinary shares in issue 133,825,000 134,566,000 + 0.6%

Source: Polar Capital, 30 April 2020. Past performance is not indicative or a guarantee of future returns.

For non-US investor use only. Please refer to the Important Information at the end of this presentation. 2

PCT as at 31 July 2020

Year ended Year ended Change As at

30/04/19 30/04/20 (y/y) 31/07/20

Net Assets £1,935,646,000 £2,308,597,000 +19.3% £2,839,527,006

NAV per ordinary share 1446.40p 1715.59p +18.6% 2067.91p

Price per ordinary share 1354.00p 1774.00p +31.0% 1950.00p

Benchmark Change +18.1%

Ordinary shares in issue 133,825,000 134,566,000 + 0.6% 137,315,000

Source: Polar Capital, 31 July 2020. Past performance is not indicative or a guarantee of future returns.

For non-US investor use only. Please refer to the Important Information at the end of this presentation. 3

Full Year Review

DJ World Technology vs. FTSE World TR since April 2019 • Global equities (FTSE World -1.5%) fell

modestly during one of the most remarkable

years in living memory as COVID-19 changed the

world as we knew it.

• This unprecedented challenge was met with

remarkable worldwide monetary and fiscal

support driving a stunning equity market reversal;

after the quickest ever descent into a bear

market, April delivered the best monthly returns

since 1987 (and Q2 proved the best quarter for

US stocks since 1998)

• Technology stocks enjoyed an outstanding year

of absolute and relative returns (DJ World Tech

+18.1% in Sterling terms) due to the sector’s

relative earnings progress and a valuation re-

rating while the Coronavirus crisis highlighted the

sector’s superior growth / balance sheet profile

and its criticality.

Source: Bloomberg, 31 July 2020. Past performance is not indicative or a guarantee of future returns.

For non-US investor use only. Please refer to the Important Information at the end of this presentation. 4

Full Year Review

US technology small caps vs. large caps since April 2019 • Sector strength obscured the growing divergence

between next-generation and legacy companies,

as well as large cap (+21%) and small-cap (-

3%). This divergence extended post COVID with

outstanding outperformance experienced by

companies that benefit from (and capture the

zeitgeist of) the so-called ‘new normal’.

• NAV performance (+18.6%) exceeded the

benchmark by 0.5%.

• The current crisis has shown the modern world is

built on technology while many of the trends we

have written about for years have been

meaningfully accelerated by the crisis. While

valuations appear to capture at least some of this

acceleration, we look forward to many more

years of growth for the technology sector.

Source: Bloomberg, 31 July 2020. Past performance is not indicative or a guarantee of future returns. All opinions and estimates constitute the best judgment of Polar Capital as of the date hereof, but are subject to

change without notice, and do not necessarily represent the views of Polar Capital.

For non-US investor use only. Please refer to the Important Information at the end of this presentation. 5

The Technology Team

• Technology is at the core of the Polar Capital business

• One of the largest technology franchises in Europe with c.US$10.9bn under management

• Nine dedicated technology specialists – strong multi-cycle track record

Global Technology Polar Capital Technology Automation & AI

Funds Fund Trust (LSE listed) Fund

US$6.6bn US$3.7bn US$578m

Nick Evans Ben Rogoff Xuesong Zhao

Partner Partner Fund Manager/Analyst

Investment experience: 22 years Investment experience: 25 years Investment experience: 13 years

Sectors: US Sectors: US Sectors: Asia (all-cap), global

semi / Semi cap equipment

Fund Managers

Fatima Iu Alastair Unwin

Fund Manager/Analyst Fund Manager/Analyst

Investment experience: 14 years Investment experience: 9 years

Sectors: Europe (all-cap), security, Sectors: Global (all-cap) Payments,

networking, energy & med tech SMB software, IT services

Chris Wittstock (based in US) Bradley Reynolds Paul Johnson Nick Williams

Senior Investment Analyst Investment Analyst Investment Analyst Investment Analyst

Investment experience: 36 years Investment experience: 13 years Investment experience: 8 years Investment experience: 4 years

Analysts

Sectors: US Technology/Software Sectors: US (all-cap) – Sectors: Emerging Tech inc. Sectors: Global (all-cap) –

Internet & digital media 3D printing, gaming & autos A&AI Fund

Source: Polar Capital, 31 July 2020.

For non-US investor use only. Please refer to the Important Information at the end of this presentation. 6

Investment Framework

4,000+ universe

Dynamic definition of technology

Thematic overview Real-world changes in userbehaviour

S-Curve inflections

What we look for Secular themes / pure-plays

Last-generation winners

What we avoid Public venturecapital

Growth bias – rev/earnings/ cash flow

Valuation Price targets (bull/base/bear) / Risk reward

Bottom-up stock picking

Portfolio construction Benchmark aware

Mis-execution / modelchange

Sell disciplines Price level attainment

Portfolio

Source: Polar Capital.

For non-US investor use only. Please refer to the Important Information at the end of this presentation. 7

Thematic Investing: Hype vs. Reality

Polar Capital Global Technology Team

Searching for revenue growth and cash flow inflections

R&D High growth Low growth No growth

Pre-Revenue negative OM% expanding OM% stable OM% uncertain / decliningOM%

Payment network

Digital Gaming EM smartphones

Sales (blue)

eCommerce IT Services Value Trap

Unified Communications Streaming media DM smartphones

Digital Twin Simulation Performance Marketing

Pay TV Subscription

5G Devices Factory Automation / Robotics

400G Optical Virtualisation

Block Chain

Robotic Process Autom ation Internet of Things (IoT)

Precision Medicine Clean Energy Cyber Security (Firewall)

Next Gen Memory Software as a Service (SaaS)

EUV Litho ERP / Traditional SW

Edge Computing / Analytics

Autonomous Driving Cloud computing (PaaS/IaaS)

3D Sensing Mainframe

5G mm Wave

SIC/48v Machine to Machine Communication

OLED TV Desktop PC / printers

Low Earth Orbit Satellite Systems Energy Storage Microservices / Containerisation

Hype (orange)

ADAS / Active Safety

Solid State Battery Smart Agriculture 3D Packaging

Light Cargo Delivery Drones Virtual Reality Mobile Payment

Flying Autonomous Vehicles Electric Vehicles Cyber Security (Cloud Security)

Adaptive Machine Learning 3D Printing Data Economy / Machine Learning

5G Network AI (Image Recognition)

Fuel Cell Vehicles

AI (Voice Recognition)

“Blue Sky” Disillusionment Emerging / Adoption Mainstream Maturity

Positioning of themes/products above is only intended to be indicative of approximate penetration/maturity

Source: Polar Capital & Gartner, October 2019. It should not be assumed that recommendations made in future will be profitable or will equal performance of the securities in this document. A list of all

recommendations made within the immediately preceding 12 months is available upon request.

For non-US investor use only. Please refer to the Important Information at the end of this presentation. 8

Thematic Investing: Hype vs. Reality

Consumer Cash Payments, forecasts vs. actual (m)4

• Introduced in late 2016 to derision1

• Analysts estimate that 16m AirPods were

sold in 20182 , 40m in 20193 and as many as “How did you go bankrupt?

100m by 20212.. Two ways. Gradually, then suddenly.”

• This would make them Apple’s second fastest - Ernest Hemingway

selling new product of all time5

Source: 1. OneZero, 2019. 2. Ming-Chi Kuo of TF International Securities. 3. Neil Cybart, Above Avalon, February 2019. 4. UK Finance, Link Network. 5. Cult of Mac, 2019. The stocks represented herein do not

reflect the entire holdings contained within the Fund. It should not be assumed that recommendations made in future will be profitable or will equal performance of the securities in this document. A list of all

recommendations made within the immediately preceding 12 months is available upon request. All opinions and estimates constitute the best judgment of Polar Capital as of the date hereof, but are subject to

change without notice, and do not necessarily represent the views of Polar Capital.

For non-US investor use only. Please refer to the Important Information at the end of this presentation. 9

Technology Outperformance Tech has driven all the earnings growth since 2009 Helping growth stocks sharply outperform value Tech vs. Ex. Tech earnings (1985 – Present) World Value vs. Growth stocks (1974 – Present) Source: FT, Goldman Sachs. Trailing 12-month earnings. It should not be assumed that recommendations made in future will be profitable or will equal performance of the securities in this document. A list of all recommendations made within the immediately preceding 12 months is available upon request. All opinions and estimates constitute the best judgment of Polar Capital as of the date hereof, but are subject to change without notice, and do not necessarily represent the views of Polar Capital. For non-US investor use only. Please refer to the Important Information at the end of this presentation. 10

Eight Core Investment Themes

Core Investment themes (estimated exposure in Fund)

SaaS / Software "Eating the World" 13.3%

Industry 4.0 / Automation 3.7%

Cloud Infrastructure / Security 11.1%

Digital Entertainment 11.6%

Mobility / Connectivity / 5G 17.6%

Payments / Fintech 4.6%

Data Economy / Artificial Intelligence 13.2%

Online Advertising / eCommerce 15.1%

Market Hedge / Beta Offset 1.6%

Other / Cyclical 6.3%

Other / Growth 1.7%

Other / Legacy 0.2%

0% 5% 10% 15% 20%

Source: Polar Capital, 31 July 2020, internal estimates. Past performance is not indicative or a guarantee of future returns. It should not be assumed that recommendations made in future will be profitable or will

equal performance of the securities in this document. A list of all recommendations made within the immediately preceding 12 months is available upon request. All opinions and estimates constitute the best

judgment of Polar Capital as of the date hereof, but are subject to change without notice, and do not necessarily represent the views of Polar Capital.

For non-US investor use only. Please refer to the Important Information at the end of this presentation. 11Investment Themes

Eight core theme breakdown (31 January 2017 – 31 July 2020)

19%

18%

17%

16%

15%

14%

13%

12%

11%

10%

9%

8%

7%

6%

5%

4%

3%

2%

1%

0%

Oct-17

Oct-18

Oct-19

Mar-17

Aug-17

Mar-18

Aug-18

Mar-19

Aug-19

Mar-20

Jul-19

Jul-17

Jul-18

Jul-20

Jun-17

Jun-18

Apr-19

Jun-19

Jun-20

Jan-17

Apr-17

Apr-18

Jan-19

Apr-20

Dec-17

Jan-18

Dec-18

Feb-19

Sep-19

Dec-19

Jan-20

Feb-17

Sep-17

Feb-18

Sep-18

Feb-20

Nov-19

Nov-17

Nov-18

May-17

May-18

May-19

May-20

Data Economy / Artificial Intelligence Cloud Infrastructure / Security Digital Entertainment Online Advertising / eCommerce

Market hedge / beta offset Industry 4.0 / Automation Mobility / Connectivity / 5G SaaS / Software "Eating the World"

Payments / Fintech Other / Cyclical Other / Growth Other / Legacy

Source: Polar Capital, 31 July 2020. Past performance is not indicative or a guarantee of future returns.

For non-US investor use only. Please refer to the Important Information at the end of this presentation. 12Digital Disruption: Demographics

How couples meet (1940 – present)1 Gen Z consumers are different2

96% own a smartphone, more than 50% are online >10 hrs/day4

Generation Z 70% watch more than 2 hours of YouTube/day3, 83% watch Netflix5

62% will not use apps that are hard to navigate6

c.26% of the US pop8

80% feel distressed when away from their devices4

Average attention span = 8 seconds7

Source: 1. https://web.stanford.edu/~mrosenfe/Rosenfeld_et_al_Disintermediating_Friends.pdf 2. Visual Capitalist. 3. www.tvlicensing.co.uk. 4. Visual Capitalist. 5. IBM. 6. Uniquely Generation Z Report. 7. Nola

Research Group. 8. Digital Marketing Community, GenZ: New Insights Into the Mobile-First Mindset of US Teens, August 2016 | Think With Google.

It should not be assumed that recommendations made in future will be profitable or will equal performance of the securities in this document. A list of all recommendations made within the immediately preceding

12 months is available upon request.

For non-US investor use only. Please refer to the Important Information at the end of this presentation. 13Digital Disruption: Artificial Intelligence(AI)

Collapsing computing costs (1950 – 2019)1

“Artificial Intelligence technologies will be the

most disruptive class of technologies over the

next 10 years due to radical computational

power, near-endless amounts of data, and

unprecedented advances in deep neural

networks; these will enable organizations with

AI technologies to harness data in order to adapt

to new situations and solve problems that no

one has ever encountered previously”

- Gartner, July 20172

Source: 1. John C. McCallum; Gordon Moore; The Linley Group; Nielson Normal Group; The Economist. 2. Gartner. The stocks represented herein do not reflect the entire holdings contained within the Fund. All

opinions and estimates constitute the best judgment of Polar Capital as of the date hereof, but are subject to change without notice, and do not necessarily represent the views of Polar Capital.

For non-US investor use only. Please refer to the Important Information at the end of this presentation. 14Digital Disruption: COVID Acceleration

Digital transformation – “the business imperative of responding to needs of a new generation of customers,

partners and suppliers who expect transactions to be seamless, real-time, Facebook-like

in experience, Amazon-like in reliability”1

COVID acceleration – “As COVID-19 impacts every aspect of our work and life, we have seen two years’ worth

of digital transformation in two months. From remote teamwork and learning to sales

and customer service to critical cloud infrastructure and security, we are working alongside

customers every day to help them stay open for business in a world of remote everything.

There is both immediate surge demand and systemic structural changes across all of our

solution areas that will define the way we live and work going forward.”

-Satya Nadella, CEO, Microsoft2

Accelerated US eCommerce3 Online spending by sector (%)5 WFH likely to persist post COVID4

Source: 1. Baird. 2. Microsoft, 30/4/20. 3. Adobe Digital Economy Index May 2020 4 Gartner, compiled by Goldman Sachs Global Investment Research, May 2020. 5. BAC, May 2020. It should not be assumed that

recommendations made in future will be profitable or will equal performance of the securities in this document. A list of all recommendations made within the immediately preceding 12 months is available upon request. All

opinions and estimates constitute the best judgment of Polar Capital as of the date hereof, but are subject to change without notice, and do not necessarily represent the views of Polar Capital.

For non-US investor use only. Please refer to the Important Information at the end of this presentation. 15Investment Themes

Advertising / eCommerce

Internet advertising worth $340bn in 2020E2, 52% of total ad spending2

eCommerce est. $4.2trn in 2020E, c16% of total retail sales1

Brand Building → Transaction facilitation

Payments / Fintech

Global mobile payments worth $2.73tr by 20234

2.1bn consumers to pay via mobile wallet in 20195

eCommerce → behavioural change / disruption

Data Economy / Artificial Intelligence

2.5bn Gb of data generated per day only 1% is stored & analysed7

AI likely largest driver of tech spend over 5-10 years ($127bn by 2025E7)

Rules based engines → Self improving algorithms

Cloud Infrastructure / Security

By 2023, 43% of application workloads expected to run in Cloud services5

Security tailwinds include data breaches, regulation, digitzation, cyberwarfare

Under-utilisation / cost arbitrage → Elastic Compute / TAM expansion

Source: 1. eMarketer, Dec 2019; 2. IAB, Zenith, BoA Dec 2019; 3. BoA / ML / Zenith, US market Jan 18; 4. Payments cards and mobile, 2019. 5. GS CIO Survey (Jan 2020). 6. MS, Geekwire July 2018. 7.

BAML, August 2018. It should not be assumed that recommendations made in future will be profitable or will equal performance of the securities in this document. A list of all recommendations made within the

immediately preceding 12 months is available upon request.

For non-US investor use only. Please refer to the Important Information at the end of this presentation. 16Investment Themes

Software / SaaS “Eating The World”

SaaS market of $141bn in 2019 expected to reach $550bn by 20258

As penetration rises (~30% today5 ) expect more strategic M&A by incumbents

SMB adoption / TAM expansion→ Enterprise / ‘rip and replace’

Digital Entertainment

$146bn 2019 gaming market1 growing to $200bn by 2023E driven by mobile, DLC / MTX 1

Streaming + 5G could open AAA titles to ~2.6bn mobile gamers worldwide2

Leisure → Connected / Competitive

Industry 4.0 / Automation

$381bn TAM by 2023 (c.10% CAGR)3 enabled by advanced components (e.g. sensors, gears)

Position repeatability: 0.01mm (robots) / 0.5mm (humans) VS 0.02mm (iPhone64) / 0.1mm (cars)

Cost savings → Necessity, Flexibility (‘CoBot’) and Consistency

Connectivity / Mobility / 5G

Current networks insufficient to support an increasingly connected world

5G infrastructure spending worth $26bn by 2022E, +118% CAGR (2018-2022)7

Capacity + latency → IoT enablement

Source: 1. Newzoo, April 2020; 2. Newzoo April 2020 3. marketsandmarkets, May 2018; 4. Cult of Mac, 2014. 5. IDC. 6. NewZoo May 2017. 7. ZDNet, 2018. 8. Keybanc. It should not be assumed that recommendations

made in future will be profitable or will equal performance of the securities in this document. A list of all recommendations made within the immediately preceding 12 months is available upon request.

For non-US investor use only. Please refer to the Important Information at the end of this presentation. 17Digital Marketing / Online Advertising

• Global online advertising worth $340bn in 2020E, c. 52% of total worldwide advertising spend1

• Online share of US advertising now commensurate with % time spent in media (51% vs. 20%/33% in 2010)…2

• …but TV + radio + print still c.49% of US ad spending and new dollar pools (trade spend / direct marketing) emerging2

• US digital media consumption accelerated in 2018 (to +7% y/y) aided by highly favourable demographic trends3

Worldwide digital advertising spending ($bn): 2018 – 20233 TAM expansion as new dollar pools emerge4

Sample Holdings

Source: Polar Capital, unless otherwise stated. 1. IAB, Zenith, BoA,, Dec 2019. 2. Bond Internet Trends 2019 3. Bond Internet Trends 2019 BoAML/Zenith, US market January 2018. 4. Morgan Stanley, March 2020. Note:

*Other includes Telemarketing, Event Sponsorship, Business-to-Business Promotion, Directories and Public Relations.. It should not be assumed that recommendations made in future will be profitable or will equal

performance of the securities in this document. A list of all recommendations made within the immediately preceding 12 months is available upon request. All opinions and estimates constitute the best judgment of Polar

Capital as of the date hereof, but are subject to change without notice, and do not necessarily represent the views of Polar Capital.

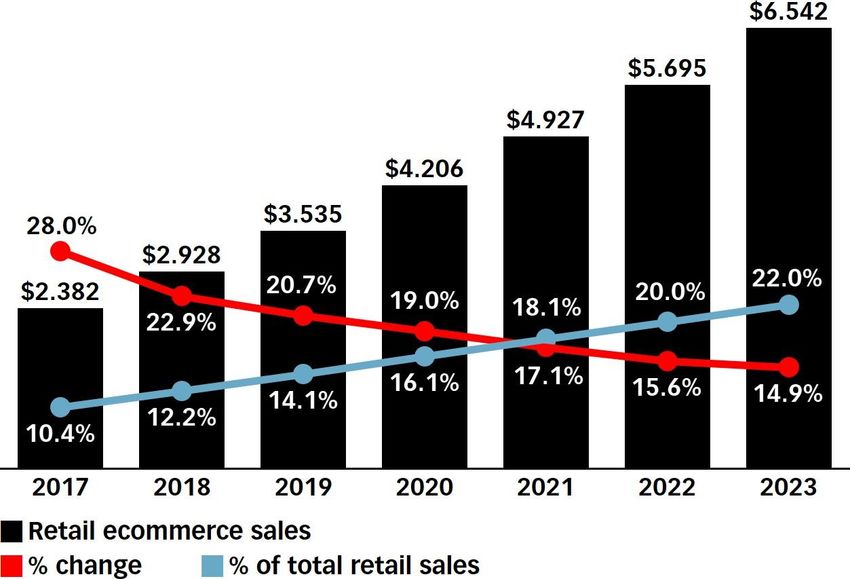

For non-US investor use only. Please refer to the Important Information at the end of this presentation. 18eCommerce

• eCommerce growth continues unabated and is forecast at $4.2tr in 2020E, representing c.16% of total retail sales1

• Amazon’s share of US e-commerce now 38%, 4% of all retail spend2

• Mobile now an integral part of the shopping experience, accounting for 63.5% of all retail eCommerce 2

• Improvements in payments / delivery continue to reduce online buying friction / change user behaviour and expectations

Global eCommerce sales, $bn (2017-2023E)1 Online penetration of US retail categories 20193

Sample Holdings

Source: Polar Capital, unless otherwise stated. 1. eMarketer, June 2019. 2. eMarketer, June 2019. 3. eMarketer, Bernstein, Jan 2020. It should not be assumed that recommendations made in future will be profitable or will

equal performance of the securities in this document. A list of all recommendations made within the immediately preceding 12 months is available upon request. All opinions and estimates constitute the best judgment of Polar

Capital as of the date hereof, but are subject to change without notice, and do not necessarily represent the views of Polar Capital.

For non-US investor use only. Please refer to the Important Information at the end of this presentation. 19Payments / Fintech • Global mobile payment market set to reach $2.73tr by 2023, representing a 25% CAGR 2018-20231 • 2.1bn consumers expected to make a purchase via a mobile wallet in 2019, >50% in China2 • B2B opportunity: $120tr (vs. $45tr consumer volume) largely cheque-based today ($4-20/transaction vs. 30-50c digital)3 • Contactless coming: half of US transactions

Cloud Infrastructure / Security

• Having debunked many of the earlier barriers to adoption, we expect Cloud migration to accelerate over the coming years

• Expect ‘all’ incremental capacity added in cloud: c. 50% of spend by 20192 and 44% of application workloads by 20213

• Cloud deflation to be felt across IT stack – IT Services market worth >$1.1tn in 2019 (2x software + datacentre combined)4

• Cost of cybercrime estimated at $6tr by 2021 with cybersecurity playing a vital role in protecting the digital economy1

Cloud penetration remains low across major IT spend Enterprise computing workloads expectations6

categories5

Sample Holdings

Source: Polar Capital unless otherwise stated. 1. PWC, The cost of inaction on cybercrime in the Middle East, 2018. 2. Deutsche Bank, January 2016. 3. Morgan Stanley / Geekwire August 2018 4. Gartner, May 2020.

5. Gartner, Goldman Sachs Global Investment Research. 6. Goldman Sachs, Global Investment Research. It should not be assumed that recommendations made in future will be profitable or will equal performance of the

securities in this document. A list of all recommendations made within the immediately preceding 12 months is available upon request. All opinions and estimates constitute the best judgment of Polar Capital as of the date

hereof, but are subject to change without notice, and do not necessarily represent the views of Polar Capital.

For non-US investor use only. Please refer to the Important Information at the end of this presentation. 21The Data Economy / Artificial Intelligence (AI)

• 2.5bn gigabytes of data is generated per day but only 1% is stored and analysed; this could increase to 37% by 20251

– e.g. a single AV may generate 4TB of data/ day, equivalent to 3,000 people today1

• AI likely to be the single largest driver of tech spending over the next 5-10 years, worth $127bn by 2025E1

– Only 8% of companies have deployed ML beyond testing1, focus likely to remain narrow / specific use-cases

• Data Economy includes semi / components (DRAM / NAND, GPU / FPGA), Cloud (scale), tools (data prep / analytics) and apps.

The ‘Data Economy’ ecosystem2 AI revenue growth by technology, $bn (2015 – 2025E)1

Apps

Tools

Cloud

Semi / components

Sample Holdings

Source: 1. BAML, August 2018 2. Polar Capital. It should not be assumed that recommendations made in future will be profitable or will equal performance of the securities in this document. A list of all recommendations

made within the immediately preceding 12 months is available upon request. All opinions and estimates constitute the best judgment of Polar Capital as of the date hereof, but are subject to change without notice, and do

not necessarily represent the views of Polar Capital.

For non-US investor use only. Please refer to the Important Information at the end of this presentation. 22Software (Is Eating The World)

• Rental / usage-based model is expanding the software market while threatening incumbent franchises / maintenance

• Software as a service (SaaS) targets a $325bn opportunity by 2022, representing 25% of IT spending1

• Focus on the customer experience (CX) driving a front office transformation CRM, UCaaS, CPaaS, voice, payments

• Agility in the data age requires automation / upgraded core business functions AI, BPA, HR, procurement

US nominal tech capex (1980 – Q1’20)2 SaaS spending (2004 – 2020E)1

Sample Holdings

Source: 1. Statista, 2020. 2. Cornerstone, Q1’20. It should not be assumed that recommendations made in future will be profitable or will equal performance of the securities in this document. A list of all recommendations

made within the immediately preceding 12 months is available upon request. All opinions and estimates constitute the best judgment of Polar Capital as of the date hereof, but are subject to change without notice, and do

not necessarily represent the views of Polar Capital.

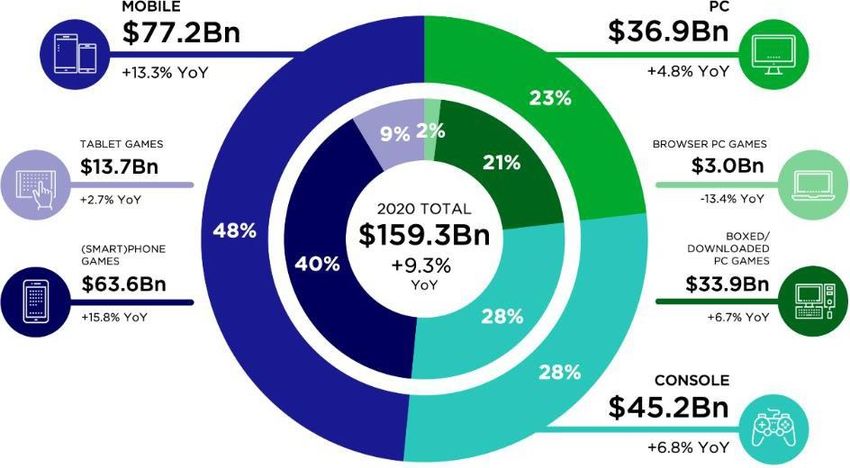

For non-US investor use only. Please refer to the Important Information at the end of this presentation. 23Digital Entertainment

• Video games: $146bn bn market in 2019 → $201bn by 2023E (~8% CAGR), driven by new console cycle, mobile and AR/VR1

• Meteoric rise of Free-To-Play Fortnite (>78m MAU / $2.4bn sales): both risk and opportunity2

• Streaming video : c.200m (vs. 1bn paid TV) subscribers worldwide, Netflix dominates today with 140m (6x closest comp)3

• eSports: modest TAM (~$1.1bn) but massive audience (201m enthusiasts + 253m occasional viewers) watching 6.6bn hours4

2020 global games market1 Total paid US subscriptions5

Sample Holdings

Source: 1. Newzoo, Apr 2020. 2. Polygon, September 2018 & The Telegraph, 2019. 3. RBC, August 2019. 4. Influencer Marketing Hub. 5. Company data, SNL Kagan, Ampere, Moran Stanley Research estimates. It should

not be assumed that recommendations made in future will be profitable or will equal performance of the securities in this document. A list of all recommendations made within the immediately preceding 12 months is

available upon request. All opinions and estimates constitute the best judgment of Polar Capital as of the date hereof, but are subject to change without notice, and do not necessarily represent the views of

Polar Capital.

For non-US investor use only. Please refer to the Important Information at the end of this presentation. 24Digital Entertainment

• Video games: $146bn bn market in 2019 → $201bn by 2023E (~8% CAGR), driven by new console cycle, mobile and AR/VR1

• Meteoric rise of Free-To-Play Fortnite (>78m MAU / $2.4bn sales): both risk and opportunity2

• Streaming video : c.200m (vs. 1bn paid TV) subscribers worldwide, Netflix dominates today with 140m (6x closest comp)3

• eSports: modest TAM (~$1.1bn) but massive audience (201m enthusiasts + 253m occasional viewers) watching 6.6bn hours4

Real meets Virtual – Travis Scott / Fortnite5 Real meets Virtual – F1 eSports Series6

Sample Holdings

Source: 1. Newzoo, Apr 2020. 2. Polygon, September 2018 & The Telegraph, 2019. 3. RBC, August 2019. 4. Influencer Marketing Hub. 5. YouTube, 2020. 6. Autosport, 2020. It should not be assumed that

recommendations made in future will be profitable or will equal performance of the securities in this document. A list of all recommendations made within the immediately preceding 12 months is available upon request. All

opinions and estimates constitute the best judgment of Polar Capital as of the date hereof, but are subject to change without notice, and do not necessarily represent the views of

Polar Capital.

For non-US investor use only. Please refer to the Important Information at the end of this presentation. 25Industry 4.0: Automation / Simulation

• The Fourth Industrial Revolution underway driven by Cyber Physical Systems, Internet of Things and Cloud Services

• Edge AI, low latency from 5G and advanced machine vision should enable cobots to self-learn tasks

• Over 25% of manufacturing tasks that can be automated may be performed by robots over the next decade1

• Service robotics (logistics, domestic, medical) market ($17bn +32% y/y in 2019) now the same size as Industrial robotics market

Connected factory combines multiple technologies2 Annual installations of industrial Robots (2013-2022E)3

Sample Holdings

Source: 1. Boston Consulting Group, September 2015. 2. Analog Devices. 3. World Robotics, 2019. It should not be assumed that recommendations made in future will be profitable or will equal performance of the

securities in this document. A list of all recommendations made within the immediately preceding 12 months is available upon request. All opinions and estimates constitute the best judgment of Polar Capital as of the date

hereof, but are subject to change without notice, and do not necessarily represent the views of Polar Capital.

For non-US investor use only. Please refer to the Important Information at the end of this presentation. 26Connectivity: 5G / IoT / Edge Computing • Current networks insufficient capacity / latency to support an increasingly connected world (c.29bn devices by 2022)1 • 5G up to 100x faster with low latency (

5G – Smartphones / Apple

• The c.1.5bn unit smartphone market is mature: global penetration at c.66%1 and units declined 2% y/y in 20201

• Apple remains unique: premium pricing + services. Wearables (+32% y/y in FQ2’20) AirPod / Watch attach at estimated 7% / 12%2

• Can 5G shorten replacement cycles? Although the PC experience is sobering, sentiment could improve ahead of 5G launch in 2020

• 5G content gains coming at a time of higher capital intensity due to ‘Moore’s Stress’ – favours RF, SPE, IC design, test and materials

Smartphone worldwide unit shipments (2008 - 2022)3 Apple replacement cycles FY16 – FY21E4

Sample Holdings

Source: 1. Gartner, Feb 2020. 2. Bernstein, 3 June 2020. 3. Business Insider, 2018. 4. Bernstein, 2020. It should not be assumed that recommendations made in future will be profitable or will equal performance of the

securities in this document. A list of all recommendations made within the immediately preceding 12 months is available upon request. All opinions and estimates constitute the best judgment of Polar Capital as of the date

hereof, but are subject to change without notice, and do not necessarily represent the views of Polar Capital.

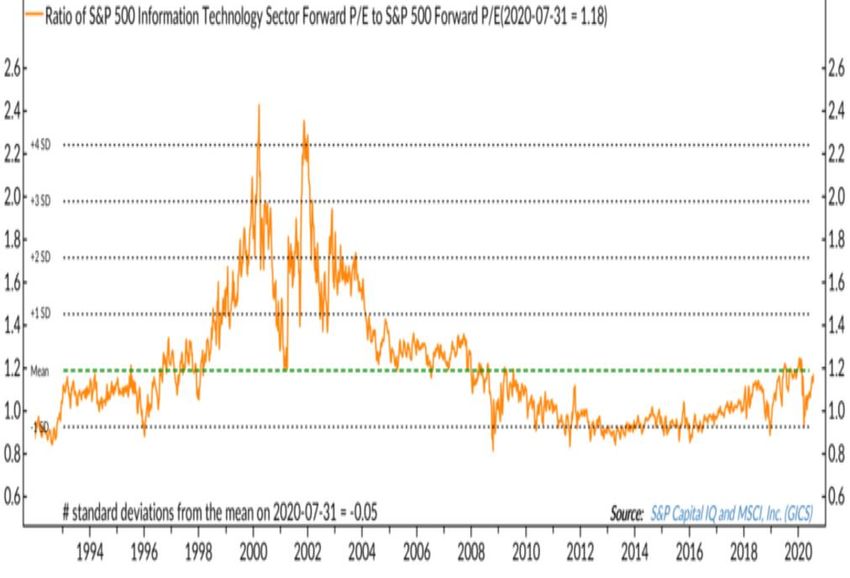

For non-US investor use only. Please refer to the Important Information at the end of this presentation. 28Technology Valuations Absolute sector valuation (PE): Relative sector valuation (PE): At post GFC highs (1992 – present) At / around market level – with superior balance sheet Source: Ned Davis, 31 July 2020. Copyright 2018 Ned Davis Research, Inc. Further distribution prohibited without prior permission. All Rights Reserved. See NDR Disclaimer at www.ndr.com/copyright.html. For data vendor disclaimers refer to www.ndr.com/vendorinfo/. Past performance is not indicative or a guarantee of future returns. For non-US investor use only. Please refer to the Important Information at the end of this presentation. 29

‘Next-Generation’ Valuations

Internet valuation (equal cap weighted): Software as a Service (SaaS) valuation:

EV/forward 2 year EV/EBITDA levels1 EV/forward 12 month revenue multiples2

25

20

15

10

5

0

Oct-17

Jan-13

Jan-15

Jun-16

Jun-18

Mar-19

Feb-17

Nov-19

Sep-13

Sep-15

May-14

Jul-20

ML Internet Index

Source: 1. Bloomberg, 31 July 2020. UCITS Internet sector (AMZN/FB/GOOG/BABA/700HK/PYPL) vs Bank of America Merrill Lynch Internet sector Index. 2. Thomson Reuters, KeyBanc, Capital Markets, July 2020. Includes

the following tickers: ADBE, ALRM, APPF, APPN, AVLR, AYX, BAND, BILL, BL, BNFT, BOX, CDAY, CLDR, COUP, CRM, CRWD, CSLT, CSOD, DBX, DDOG, DOCU, DOMO, DT, ECOM, ESTC, EVBG, FIVN, FSLY,

HUBS, LOGM, MDB, MIME, NET, NEWR, NOW, OKTA, PAYC, PCTY, PD, PFPT, PING, PLAN, PRO, PS, QLYS, QTWO, RNG, RP, RPD, SHOP, SMAR, SPSC, SQ, SVMK, TDOC, TEAM, TENB, TLND, TWLO,

TWOU, VEEV, WDAY, WIX, W K, WORK, YEXT, ZEN, ZM, ZS, ZUO. Past performance is not indicative or a guarantee of futurereturns.

For non-US investor use only. Please refer to the Important Information at the end of this presentation. 30‘Next-Generation’ Valuations

IT security valuation: Cloud vs legacy valuation

EV/forward 12 month revenue multiples1 EV/trailing 12 month revenue multiples2

14x

12x

EV/ trailing 12 month sales

10x

8x

6x

4x

2x

0x

Jan-10

Jan-11

Jan-12

Jan-13

Jan-14

Jan-15

Jan-16

Jan-17

Jan-18

Jan-19

Jan-20

Sep-10

Sep-11

Sep-12

Sep-13

Sep-14

Sep-15

Sep-16

Sep-17

Sep-18

Sep-19

May-10

May-11

May-12

May-13

May-14

May-15

May-16

May-17

May-18

May-19

May-20

LEGACY CLOUD

Source: 1. Citi Research, FactSet, July 2020. 2. Bloomberg, BofA Merrill Lynch Global Research, July 2020. Past performance is not indicative or a guarantee of future returns.

For non-US investor use only. Please refer to the Important Information at the end of this presentation. 31Rhymes, Not Repeats

Technology outperformance Technology outperformance

Sector market cap as % of S&P 500 market cap Market cap weight minus earnings weight

‒ Q1’20: technology earnings +15% y/y vs. +2.5% S&P 500

Source: Ned Davis, July 2020. Past performance is not indicative or a guarantee of future returns.

For non-US investor use only. Please refer to the Important Information at the end of this presentation. 32Rhymes, Not Repeats Concentration risk: Concentration risk: % of S&P 500 accounted for by largest 5 stocks1 Weights of Top 5 / bottom half of stocks in the S&P 5002 Source: 1. BoA Global Investment Strategy / Bloomberg, June 2020 2. Ned Davis, June 2020. Past performance is not indicative or a guarantee of future returns. For non-US investor use only. Please refer to the Important Information at the end of this presentation. 33

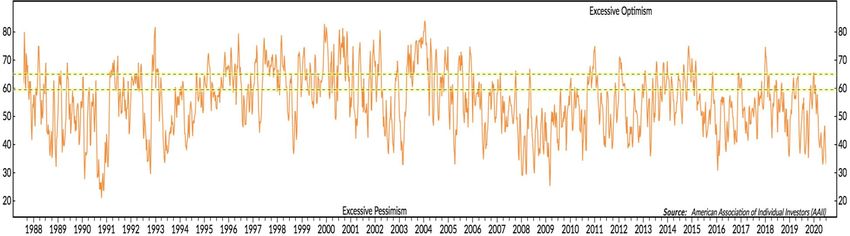

Rhymes, Not Repeats

Investor sentiment

AAII Bulls / (Bulls + Bears)1

Late 1990s exuberance

32.9%

as at

2 July 20201

Post GFC trauma

Source: 1. Ned Davis as at 2 July 2020. Past performance is not indicative or a guarantee of future returns.

For non-US investor use only. Please refer to the Important Information at the end of this presentation. 34PCT Positioning

Sector exposure (%) Market cap exposure (%)

Software 24.1%

Semiconductors & Semiconductor Equipment 17.4% 88.0%

Large Cap (>$10bn)

Interactive Media & Services 16.0%

Technology Hardware, Storage & Peripherals 12.7% Mid Cap (>$1bn - $10bn) 11.2%

Internet & Direct Marketing Retail 8.0% Small Cap (PCT Positioning

Largest overweights Largest underweights Market cap exposure versus benchmark

Activision Blizzard Alphabet

Advanced Micro Devices Analog Devices

Advantest Corp Apple

Large-cap -4.7%

Amazon Applied Materials

Axon Enterprise Autodesk

Blackline Broadcom

CloudFlare Cisco Systems

Crowdstrike Facebook Mid-cap 4.4%

Everbridge IBM

GrubHub Infosys

MediaTek Intel

Netflix Intuit Small-cap 0.3%

PayPal LAM Research

Peloton Interactive Micron Technology

Take-Two Interactive Software Microsoft -20% -15% -10% -5% 0% 5% 10% 15%

Tokyo Electron Oracle

Twilio SAP

Xilinx Shopify

Zendesk SK Hynix

Zoom Video Communications Texas Instruments

Source: Polar Capital, as at 31 July 2020. Bold denotes a zero position. It should not be assumed that recommendations made in future will be profitable or will equal performance of the securities in this document. A

list of all recommendations made within the immediately preceding 12 months is available upon request.

For non-US investor use only. Please refer to the Important Information at the end of this presentation. 36PCT Positioning

Thematic breakdown1,2 Thematic breakdown relative to benchmark (%)1,2

6.0%

Legacy 4.0%

11%

2.0%

Internet

25% 0.0%

-2.0%

-4.0%

-6.0%

Semiconductors

21%

-8.0%

-10.0%

-12.0%

Cloud: applications

13%

-14.0%

-16.0%

Smartphones

Video Games

Legacy

IoT

Cybersecurity

Medical Technology

Electric Vehicles

Internet

3D Printing

Semiconductors

Smartphones

Emerging

Cloud: infrastructure

Automotive

Materials

Payments

Apple

Cloud: applications

Solar

Other

Big data / AI

Factory automation/robotics

2%

Apple

10%

Medical Technology

0%

Cloud: infrastructure

Electric Vehicles 4%

1% Solar

Other Cybersecurity

0%

Emerging Big data / AI 1%

0%

1% IoT PaymentsFactory Automotive 2%

3D Printing automation/robotics

1% 4% 2%

0% 2%

Source: Polar Capital, 31 July 2020. 1. Benchmark: Dow Jones Global Technology Index (TR). 2. Index exposure based on Top 100 index constituents. Figures are shown as gross weightings.

It should not be assumed that recommendations made in future will be profitable or will equal performance of the securities in this document. A list of all recommendations made within the immediately preceding 12

months is available upon request.

For non-US investor use only. Please refer to the Important Information at the end of this presentation. 37PCT Positioning

Index Index

PCT 1 Top ex Sales growth 2020 – PCT vs. benchmark2

100 Apple

60.0

PE (Median) CY 32.8 27.1 27.0

NY 31.7 23.4 23.2

Earnings growth (Median) CY 4.4 3.8 3.7

50.0

NY 29.2 18.0 18.0

EV/Sales (Mean) CY 10.3 9.4 9.4

NY 8.4 7.9 7.9

EV/Sales (Median) CY 8.3 6.7 6.7 40.0

NY 6.8 5.9 5.9

EV/Sales (Weighted)** CY 9.7 8.8 9.2

Weight

NY 8.2 7.6 7.9

30.0

Sales Growth (Mean) CY 11.7 11.3 11.3

NY 19.4 14.8 14.8

Sales Growth (Median) CY 12.0 10.4 10.4

NY 17.5 12.8 12.9 20.0

Sales Growth (Weighted)** CY 13.6 11.5 12.7

NY 17.9 14.5 15.1

Gross Margin (Mean) 55.6 57.6 57.8

10.0

Gross Margin (Median) 54.9 58.6 59.0

Gross Margin (Weighted)** 53.3 56.0 59.7

Net Cash as % mkt cap Avg 7.8 10.4 10.4

Wgtd** 6.5 6.0 6.4 0.0

50

Market Cap ($m) Mean 136,899 121,918 104,135

Best Estimate Sales Growth 2020

Median 20,999 33,328 33,188

Wgtd** 589,801 795,596 579,302 PCT GROSS WEIGHT BENCH GROSS WEIGHT

Source: 1. Polar Capital, 6 August 2020. Figures in blue exclude Apple (16.6% gross) from the Index Top 100. CY = Current Year, NY = 2021 calendar year estimates. 2. Polar Capital, 6 August 2020. Benchmark: Dow

Jones Global Technology Index (TR). Past performance is not indicative or a guarantee of future results. All opinions and estimates constitute the best judgment of Polar Capital as of the date hereof, but are subject to

change without notice, and do not necessarily represent the views of Polar Capital. It should not be assumed that recommendations made in future will be profitable or will equal performance of the securities in this

document. A list of all recommendations made within the immediately preceding 12 months is available upon request.

For non-US investor use only. Please refer to the Important Information at the end of this presentation. 38Appendix For non-US investor use only. Please refer to the Important Information at the end of this presentation. 39

Team Biographies

Ben Rogoff – Partner

Experience: 25 years

Ben joined Polar Capital in May 2003. He is lead manager of Polar Capital Technology Trust plc and is a Fund Manager of the Polar Capital

Global Technology Fund and Polar Capital Automation and Artificial Intelligence Fund. He has been a technology specialist for 25 years. Prior to

joining Polar Capital he began his career in fund management at CMI, as a global technology analyst. He moved to Aberdeen Fund Managers in

1998 where he spent four years as a senior technology manager. Ben graduated from St Catherine’s College, Oxford in 1995.

Nick Evans – Partner

Experience: 22 years

Nick joined Polar Capital in September 2007 and has 22 years’ experience as a technology specialist. He has been lead manager of the Polar

Capital Global Technology Fund since January 2008 and is also a fund manager on the Polar Capital Technology Trust and Polar Capital

Automation and Artificial Intelligence Fund. Prior to joining Polar he was head of technology at AXA Framlington and lead manager of the AXA

Framlington Global Technology Fund and the AXA world fund (AWF) – Global Technology from 2001 to 2007 (both rated five stars by S&P). He

also spent three years as a Pan-European investment manager and technology analyst at Hill Samuel Asset Management. Nick has a degree in

Economics and Business Economics from Hull University, has completed all levels of the ASIP, and is a member of the CFA Institute.

Xuesong Zhao

Experience: 13 years

Xuesong joined Polar Capital in May 2012 and has 13 years’ investment experience. He is a lead manager of the Polar Capital Automation and

Artificial Intelligence Fund and is a Fund Manager on the Polar Capital Technology Trust and Polar Capital Global Technology Fund. Prior to

joining Polar Capital, he spent four years working as an investment analyst within the emerging markets & Asia team at Aviva Investors, where he

was responsible for the technology, media and telecom sectors. Prior to that, he worked as a quantitative analyst and risk manager for the

emerging market debt team at Pictet Asset Management. He started his career as a financial engineer at Algorithmics, now owned by IBM, in

2005. He holds an MSc in Finance from Imperial College of Science & Technology, a BA (Hons) in Economics from Peking University. He is also

a CFA charterholder.

For non-US investor use only. Please refer to the Important Information at the end of this presentation. 40Team Biographies cont.

Fatima Iu

Experience: 14 years

Fatima joined Polar Capital in April 2006 and has 14 years’ experience. She is a fund manager on the Polar Capital Technology Fund, Polar

Capital Technology Trust and Polar Capital Automation and Artificial Intelligence Fund. She is responsible for the coverage of European

Technology, Global Security, Networking, Clean Energy and Medical Technology. Prior to joining Polar, Fatima spent 18 months working at

Citigroup Asset Management with a focus on consumer products and pharmaceuticals. Fatima holds an MSc in Medicinal Chemistry from Imperial

College of Science & Technology in London. She is also a CFA Charterholder.

Alastair Unwin

Experience: 9 years

Alastair joined Polar Capital in June 2019 as a Fund Manager and Senior Analyst. Prior to joining Polar Capital, Alastair co-managed the Arbrook

American Equities Fund. Between 2014 and 2018 he launched and then managed the Neptune Global Technology Fund and managed the

Neptune US Opportunities Fund. Prior to Neptune, Alastair was a technology analyst at Herald Investment Management. Alastair has a BA (1st

Class Hons) in history from Trinity College, Cambridge and is a CFA Charterholder.

Chris Wittstock

Experience: 36 years

Chris joined Polar Capital in July 2017 as a senior technology analyst based in the US. Prior to joining, Chris led the International research sales

effort at Pacific Crest, a technology investment bank that was ultimately acquired by KeyBanc Capital in 2014. Prior to joining Pacific Crest in 2004,

Chris led the International sales effort at Schwab SoundView, the successor company to Soundview Technology Group where he was since 1996.

Chris spent significant time in Europe as a derivative products specialist in the late 80s and 90s, lastly with Morgan Stanley International. He is a

graduate of University of Toronto, Faculty of Engineering (Industrial).

For non-US investor use only. Please refer to the Important Information at the end of this presentation. 41Team Biographies cont.

Brad Reynolds

Experience: 13 years

Brad joined Polar Capital in October 2011 as an Investment Analyst and Trader working as part of the European Market Neutral team with a focus

on media and internet. In 2014, he joined the Technology team as an Investment Analyst. Prior to joining Polar Capital, Brad worked at Ratio Asset

Management as an analyst and trader, and from 2007 to 2011 he worked at F&C as a hedge fund analyst. Brad started his career in 2001 at

Gartmore Investment Management working within the hedge fund team. Brad graduated from the University of Hertfordshire with a degree in

Business Studies.

Paul Johnson

Experience: 8 years

Paul joined Polar Capital in March 2012 as an Investment Analyst on the Polar Capital Technology team. Prior to joining Polar Capital, Paul helped

manage a private investment fund between 2010 and 2012. Paul holds a BA in History and Politics and a Masters in History from Keele University.

He has successfully passed all three levels of the CFA program.

Nick Williams

Experience: 4 years

Nick joined Polar Capital in June 2019 as an analyst on the Polar Capital Technology team. Prior to joining Polar Capital, Nick worked at Neptune

Investment Management as the Assistant Fund Manager on the US Opportunities growth fund. Prior to that he worked in academia at the

University of Oxford. Nick holds an MChem Chemistry from the University of Oxford.

For non-US investor use only. Please refer to the Important Information at the end of this presentation. 42Portfolio Structure – Liquidity Profile

Liquidity horizon evaluation

12,000,000,000 6.00

10,000,000,000 5.00

Days to liquidate

8,000,000,000 4.00

AUM (USDM)

6,000,000,000 3.00

4,000,000,000 2.00

2,000,000,000 1.00

0 -

Sep-18

Aug-18

Aug-19

Sep-19

Feb-18

Jun-18

Feb-19

Jun-19

Mar-18

Mar-19

Feb-20

Jun-20

Mar-20

Jul-20

Dec-17

Nov-18

Dec-18

Nov-19

Dec-19

May-18

May-19

May-20

Global Tech AUM $ Strategy AUM $ Days to liquidate 95% (GT) Days to liquidate 95% (Strat)

Source: Polar Capital, 31 July 2020. Liquidation is calculated assuming 20% of daily volume based on the average volume over the previous 60 days. Past performance is not indicative or a guarantee of future returns.

For non-US professional investor use only. Please refer to the Important Information at the end of this presentation. 43Important Information

Polar Capital

16 Palace Street

London SW1E 5JD

Important Information: This document is provided for the sole use of the intended recipient and is not a financial promotion. It shall not and does not constitute an offer or solicitation of an offer to make an

investment into any fund or Company managed by Polar Capital. It may not be reproduced in any form without the express permission of Polar Capital and is for the intended recipient only. Clients who have

access to this document should make themselves aware of all relevant risk factors relating to these products contained in the Fund or Company’s Prospectus or latest financial report. The law restricts distribution

of this document in certain jurisdictions; therefore, it is the responsibility of the reader to inform themselves about and observe any such restrictions. It is the responsibility of any person/s in possession of this

document to inform themselves of, and to observe, all applicable laws and regulations of any relevant jurisdiction. Polar Capital Technology Trust plc is an Investment Company with investment trust status and as

such its ordinary shares are excluded from the FCA’s (Financial Conduct Authority’s) restrictions which apply to non-mainstream investment products. The Company conducts its affairs and intends to continue to

do so for the foreseeable future so that the exclusion continues to apply. It is not designed to contain information material to an investor’s decision to invest in in Polar Capital Funds Plc – Automation and Artificial

Intelligence Fund, Polar Capital PLC – Global Technology Fund or Polar Capital Technology Trust plc which is an Alternative Investment Fund under the Alternative Investment Fund Managers Directive

2011/61/EU (“AIFMD”) managed by Polar Capital LLP the appointed Alternative Investment Manager. In relation to each member state of the EEA (each a “Member State”) which has implemented the AIFMD,

this document may only be distributed and shares may only be offered or placed in a Member State to the extent that (1) the fund is permitted to be marketed to professional investors in the relevant Member

State in accordance with AIFMD; or (2) this document may otherwise be lawfully distributed and the shares may otherwise be lawfully offered or placed in that Member State (including at the initiative of the

investor). As at the date of this document, the Fund has not been approved, notified or registered in accordance with the AIFMD for marketing to professional investors in any member state of the EEA. However,

such approval may be sought or such notification or registration may be made in the future. Therefore this document is only transmitted to an investor in an EEA Member State at such investor’s own

initiative. SUCH INFORMATION, INCLUDING RELEVANT RISK FACTORS, IS CONTAINED IN THE COMPANY OR FUND’S OFFER DOCUMENT WHICH MUST BE READ BY ANY PROSPECTIVE

INVESTOR.

Statements/Opinions/Views: All opinions and estimates constitute the best judgment of Polar Capital as of the date hereof, but are subject to change without notice, and do not necessarily represent the views

of Polar Capital. This material does not constitute legal or accounting advice; readers should contact their legal and accounting professionals for such information. All sources are Polar Capital unless otherwise

stated.

Third-party Data: Some information contained herein has been obtained from third party sources and has not been independently verified by Polar Capital. Neither Polar Capital nor any other party involved in or

related to compiling, computing or creating the data makes any express or implied warranties or representations with respect to such data (or the results to be obtained by the use thereof), and all such parties

hereby expressly disclaim all warranties of originality, accuracy, completeness, merchantability or fitness for a particular purpose with respect to any data contained herein.

Holdings: Portfolio data is “as at” the date indicated and should not be relied upon as a complete or current listing of the holdings (or top holdings) of the Company or Fund. The holdings may represent only a

small percentage of the aggregate portfolio holdings, are subject to change without notice, and may not represent current or future portfolio composition. Information on particular holdings may be withheld if it is in

the Company or Fund’s best interest to do so. It should not be assumed that recommendations made in future will be profitable or will equal performance of the securities in this document. A list of all

recommendations made within the immediately preceding 12 months is available upon request. This document is not a recommendation to purchase or sell any particular security. It is designed to provide

updated information to professional investors to enable them to monitor the Company or Fund.

Benchmarks: The following benchmark index is used: Dow Jones World Technology Index (Total Return). This benchmark is generally considered to be representative of the Technology Equity universe. This

benchmark is a broad-based index which is used for comparative/illustrative purposes only and has been selected as it is well known and is easily recognizable by investors. Please refer to www.djindexes.com

for further information on this index. Comparisons to benchmarks have limitations as benchmarks volatility and other material characteristics that may differ from the Company or Fund. Security holdings, industry

weightings and asset allocation made for the Company or Fund may differ significantly from the benchmark. Accordingly, investment results and volatility of the Company or Fund may differ from those of the

benchmark. The indices noted in this document are unmanaged, are unavailable for direct investment, and are not subject to management fees, transaction costs or other types of expenses that the Company or

Fund may incur. The performance of the indices reflects reinvestment of dividends and, where applicable, capital gain distributions. Therefore, investors should carefully consider these limitations and differences

when evaluating the comparative benchmark data performance. Information regarding indices is included merely to show general trends in the periods indicated, it is not intended to imply that the fund was similar

to the indices in composition or risk.

For non-US investor use only. Please refer to the Important Information at the end of this presentation. 44Important Information Cont.

Polar Capital

16 Palace Street

London SW1E 5JD

Regulatory Status: Polar Capital LLP is a limited liability partnership number OC314700. It is authorised and regulated by the UK FCA and is registered as an investment adviser with the US Securities &

Exchange Commission (“SEC”). A list of members is open to inspection at the registered office, 16 Palace Street, London SW1E 5JD. FCA authorised and regulated Investment Managers are expected to write to

investors in funds they manage with details of any side letters they have entered into. The FCA considers a side letter to be an arrangement known to the investment manager which can reasonably be expected

to provide one investor with more materially favourable rights, than those afforded to other investors. These rights may, for example, include enhanced redemption rights, capacity commitments or the provision of

portfolio transparency information which are not generally available. The Fund and the Investment Manager are not aware of, or party to, any such arrangement whereby an investor has any preferential

redemption rights. However, in exceptional circumstances, such as where an investor seeds a new fund or expresses a wish to invest in the Fund over time, certain investors have been or may be provided with

portfolio transparency information and/or capacity commitments which are not generally available. Investors who have any questions concerning side letters or related arrangements should contact the Polar

Capital Desk at the Registrar on 0800 876 6889 (PCTT) or Administrator on +353 1 434 5007 (UCITS). The Fund is prepared to instruct the custodian of the Fund, upon request, to make available to investors

portfolio custody position balance reports monthly in arrears.

Information Subject to Change: The information contained herein is subject to change, without notice, at the discretion of Polar Capital and Polar Capital does not undertake to revise or update this information

in any way.

Forecasts: References to future returns are not promises or estimates of actual returns Polar Capital may achieve. Forecasts contained herein are for illustrative purposes only and does not constitute advice or a

recommendation. Forecasts are based upon subjective estimates and assumptions about circumstances and events that have not and may not take place.

Performance/Investment Process/Risk: Performance is shown net of fees and expenses and includes the reinvestment of dividends and capital gain distributions. Factors affecting the Company or Fund’s

performance may include changes in market conditions (including currency risk) and interest rates and in response to other economic, political, or financial developments. Past performance is not a guide to or

indicative of future results. Future returns are not guaranteed and a loss of principal may occur. Investments are not insured by the FDIC (or any other state or federal agency), or guaranteed by any bank, and

may lose value. No investment process or strategy is free of risk and there is no guarantee that the investment process or strategy described herein will be profitable.

Allocations: The strategy allocation percentages set forth in this document are estimates and actual percentages may vary from time-to-time. The types of investments presented herein will not always have the

same comparable risks and returns. Please see the private placement memorandum or prospectus for a description of the investment allocations as well as the risks associated therewith. Please note that the

Company or Fund may elect to invest assets in different investment sectors from those depicted herein, which may entail additional and/or different risks. Performance of the Company or Fund is dependent on

the Investment Manager’s ability to identify and access appropriate investments, and balance assets to maximize return to the Company or Fund while minimizing its risk. The actual investments in the Company

or Fund may or may not be the same or in the same proportion as those shown herein.

Country Specific disclaimers: The Company or Funds have not been and will not be registered under the U.S. Investment Company Act of 1940, as amended (the "Investment Company Act") and the holders

of its shares will not be entitled to the benefits of the Investment Company Act. In addition, the offer and sale of the Securities have not been, and will not be, registered under the U.S. Securities Act of 1933, as

amended (the "Securities Act"). No Securities may be offered or sold or otherwise transacted within the United States or to, or for the account or benefit of U.S. Persons (as defined in Regulation S of the

Securities Act). In connection with the transaction referred to in this document the shares of the Fund will be offered and sold only outside the United States to, and for the account or benefit of non U.S. Persons

in "offshore- transactions" within the meaning of, and in reliance on the exemption from registration provided by Regulation S under the Securities Act. No money, securities or other consideration is being solicited

and, if sent in response to the information contained herein, will not be accepted. Any failure to comply with the above restrictions may constitute a violation of such securities laws.

For non-US investor use only. Please refer to the Important Information at the end of this presentation. 45You can also read