POLITECNICO DI MILANO - School of Architecture Urban Planning Construction Engineering

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

POLITECNICO DI MILANO

School of Architecture Urban Planning Construction Engineering

School of Industrial and Information Engineering

Master of Science Management of Built Environment

Accademic year 2020/2021

Last Mile Logistics

and

Real Estate Market

Relators: Master Thesis of:

Prof Gianandrea Ciaramella Giorgio Ferrari - Matr. 927554

Dr. Alberto Celani

Index

Abstract 4

Sommario 5

Introduction 7

Reasons of the research 7

Chapter 2 13

City Logistic and eCommerce 13

Sustainability of the urban transport 14

City Logistic 20

Last mail logistics models and adopted solutions 25

Regulation 26

Technology 27

Cooperation 29

The logistics of eCommerce 30

Chapter 2 40

Logistics real estate/logistics infrastructure 40

Overview of the logistics real estate sector in the European area 40

The future of logistics 47

Demographic change 48

Technology 49

Sustainability 49

Urbanization 51

Robotics and work 52

Types of warehouses 54

Technical characteristics of logistics buildings 56

Outdoor areas 57

Construction and structural characteristics of the logistic building 58

Areas inside the logistics building 59

New logistic real estate valuation model 63

New or used building? 71

Bibliografia 73

Annex n1 77

List of figure and graph Fig.1 Retail e-commerce sales worldwide from 2014to 2023 - (in bilions U.S. 9 dollars) Fig.2 Internet users who bought or ordered goods or services for private use in 10 the previous 12 month by age group, EU-27, 2010-2020 Fig.3 Supply chains related to traditional retailing and eCommerce shopping 13 Fig.4 Number of registered freight trucks and vans for 1000 inhabitants 14 (FUME) Fig.5 Population affected by Noise pollution and consequences 16 Fig.6 Popultation, mortality and vehicles fleet for income level 17 Fig.7 Impact on the urban environment based on the different categories of 19 transport offer Fig.8 Urban Freight domain 21 Fig.9 Transaction among stakeholders 21 Fig.10 Impact of the technology trends 28 Fig.11 Function of logistic system for eCommerce 30 Fig.12 Factors that affect the logistical model 37 Fig.13 GDP levels and Employment rate in europe from 2005 to 2021 43 Fig.14 Logistic Take-up quarterly evolution, Italy 45 Fig. 15 YTD Q3 2020 investment volumes by geography - Italy 46 Fig.16 Prime headline rents-warehouses over 5000sqm 46 Fig. 17 What do you beleve are the biggest risk to the success of your business? 47 Fig.18 Breakdown of Net Zero Carbon - whole life 50 Fig 19 The WELL Building concepts 51 Fig.20 The modern Suply Chain 54 Fig.21 Main characteristics and differences of the type of warehouses 55 Fig.22 Importance of the features for the future warehouses 62 Fig.23 Factors which influence the performance indexes 64 Fig.24 KPI-1 Personell’s density (worker n°/1000s qm) 64 Fig.25 KPI-3 Personell’s density (worker n°/1000s qm) 65 Fig.26 Scheme Economic Direct Impact 66 Fig.27 Economic Direct Impact for the different chategories 66 Fig.28 Main characteristics for typology of logistics building 68 Fig.29 Functionality level 70 Fig.30 Quality level 70 Fig.31 Square Meter Surface 70 Fig.32 High under the beam 70 Fig.33 Number of bays per squaremeter 70

4 Abstract The research investigates the Logistics sector focusing on the Last Mile segment of the Supply chain. The evolution in recent years of the eCommerce market had a strong impact on the organizational models of the logistics operators which are now obliged to respond to the high standards required by the customers. To limit the negative externalities caused by the increased number of deliveries in the urban context, the City Logistic theory had to evolve at the same time of the augmented freight traffic volume. Although the theory has reached a solid and structured dimension, still it is little applied in the real context. Today the logistics operators and administrators face the challenges of the Last Mile distribution through models which are not integrated and focus only on partial solution, depending on the point of view of interest: private or public. The eCommerce had modified the traditional scheme of the Supply Chain, forcing the Logistics operators to create new business models able to manage the high volume, diversified and volatile demand of the consumers. The extreme importance of the Logistic sector is witnessed by the strong growth of the investment in the real estate market across all the European Union. The Investors and the Logistic operators are focusing on buildings which have high standards and high-quality levels which are fundamental factors of the buildings to respond, not only to the actual need of the Last Mile logistic, but also to the future ones. Indeed, the request of the real estate market for the logistic buildings is rapidly evolving to meet the needs of the “advance logistics” and the environmental and social issues. Robotics, automation, and digitalization are the main drivers which are changing the technical characteristic of the different types of warehouses along the Supply Chain. New assessment models are needed to provide a holistic evaluation of the building which integrate different dimensions: technical characteristics, location, environmental sustainability, workers’ welfare. The essay end with a spark for future research on the reuse of the abandoned industrial building which proliferate in the periphery of the urban areas.

5 Sommario La ricerca indaga il settore Logistico concentrandosi sul segmento del Last Mile della Supply Chain. L’evoluzione degli ultimi anni del mercato dell’eCommerce ha avuto un forte impatto sui modelli organizzativi degli operatori logistici che sono stati obbligati a rispondere agli elevati standard richiesti dai clienti. Per limitare le esternalità negative causate dall’aumento del numero di consegne nel contesto urbano, la teoria della City Logistics ha dovuto evolversi contemporaneamente all’aumento del volume del traffico merci. Sebbene la teoria abbia raggiunto una dimen- sione solida e strutturata, è ancora poco applicata nel contesto reale. Oggi gli operatori logistici e gli amministratori affrontano le sfide della distribuzione Last Mile attraverso modelli che non sono integrati e che si concentrano solo su soluzioni parziali, a seconda del punto di vista di interesse: privato o pubblico. L’eCommerce ha modificato lo sche- ma tradizionale della Supply Chain, costringendo gli operatori logistici a creare nuovi modelli di business in grado di gestire l’elevato volume, la domanda diversificata e vola- tile dei consumatori. L’importanza del settore Logistico è testimoniata dagli elevati investimenti nel mercato immobiliare in tutta l’Unione Europea. Gli Investitori e gli Operatori Logistici si stanno concentrando su edifici con elevati standard e alti livelli di qualità, fattori fondamentali per rispondere alle esigenze attuali e future della logistica Last Mile. La richiesta del mercato immobiliare per gli edifici logistici si sta rapidamente evolvendo per soddisfare le esigenze della “logistica avanzata” e le questioni ambientali e sociali. Robotica, au- tomazione e digitalizzazione sono i principali driver che stanno cambiando le caratteri- stiche delle diverse tipologie di magazzini lungo la Supply Chain. Sono necessari nuovi modelli di valutazione per fornire un giudizio olistico degli edifici che integri le diverse dimensioni: caratteristiche tecniche, ubicazione, sostenibilità ambientale, benessere dei lavoratori. Il saggio si conclude con uno spunto per future ricerche sul riutilizzo degli edifici indu- striali abbandonati disseminati nelle periferie delle aree urbane.

6

Introduction 7

Introduction

Reasons of the research

In everyday life we are now all deeply immersed in a phenomenon of which we only

rarely pause to reflect and become aware of it.

The born of e-commerce can be traced back in 1979 when in England a television was

connected to the telephone network and allowed an elderly lady to make a purchase at

a local Tesco physical store.

However, is only at the beginning of 2000s the is possible to talk about e-commerce as

everyone knows it today: to order any item in few clicks and see it delivered it after a

short time.

Diverse factors deeply connected with the evolution of technology have driven the

growth of the phenomenon. But the availability of new technology itself is not able

to explain the exponential growth trend: it is surely a necessary prerequisite but

not sufficient. The technology penetration into the society is the other key factor to

understand the evolution.

Referring to the Italian eCommerce market one data, elaborated by the observatory of

eCommerce B2C-Consorzio Netcomm/School of Management of Politecnico di Milano,

is able to explain the relation between the technology progresses, the penetration into

the society and the growth of the on-line market.

In the 2019 the value of the on-line shopping in Italy exceeds 5 billion of euros, with a

growth of +18% respect to 2018. But here, the interesting factor isn’t just the total value

and the rate of growth, but the breakdown of the different devices used to purchase

from the internet: even if for the Italians the computer remains the preferred device to

search and chose the items (55% of the purchases is completed through the desktop),

the purchases from smartphones, which is nowadays owned and used every day from

the majority of the population, constitute the 40% of the total value, with a rate growth

of 6% compared with the year before; at the end, to complete the sources of purchases,

the tablet cover the remaining share.

The thesis is corroborated in a report developed by the Observatory on Multi-channel

developer in collaboration with Nielsen on the relation between the technology diffusion

and the eCommerce.

The definition given by the observatory, the multi-channel refers to the ability and the

propensity of the consumer to utilize Internet and other digital devices to take decisions

Politecnico di Milano - Ferrari Giorgio

8 Introduction

on the items to purchase and to find information on the products and services, following

different and mixed routes combining devices and point of contact between the physical

and the digital world.

In 2020 the Observatory has traced 5 different typologies of multichannel consumer:

the Digital Rooted (11% of the total internet users), is the most advanced and mature

category, more sensible to the reviews of other previous costumers and compose

subjects above the mean for the availability of technological devices and familiarity

to on-line shopping; the Digital Engaged (17%), which utilize the web in a intense and

with nonchalance, looking with faith to no form of payments but keeping a link to the

physical stores; the Digital Bouncers (22%) which utilize the internet in the phases pre

and post purchases but still prefer to buy the item in the physical store, even if get the

information and the comparing the characteristic through digital researches; the Digital

Rookies (38%) are the consumers most widespread which still use the internet with some

sort of mistrust and caution, above all warried about the digital payments; and last the

Digital Unplugged (12%) which correspond to users that prefer the traditional channels

respect to the digital world and that research a relation to the vendor in the physical

store also for support and assistance in the choice of the right item.

To explain the importance and the relevance of the reason why today it is not possible

to anymore consider the e-commerce as a minority part of the value creation, it is useful

to observe the graph global volume of sales made by the e-shops. In the considered

period, which exclude the growth happened before 2014 because, even if it has grown

year after year, the increase in rate does not assume a relevant value.

In the last 6 years instead, it is evident the exponential increase of the total value of the

transactions generated in the digital world (fig.1): the on-line businesses had increased

on an annual basis by 21%, considering the total time period 2014-2019 the growth has

been equal to 314.82% with a economic value of 3535 billions of dollars (2913.52 billions

of euros).

The forecast for the next 3 years (2021, 2022, 2023) foresee an annual mean growth rate

around 16%, indeed slightly less than the previous years.

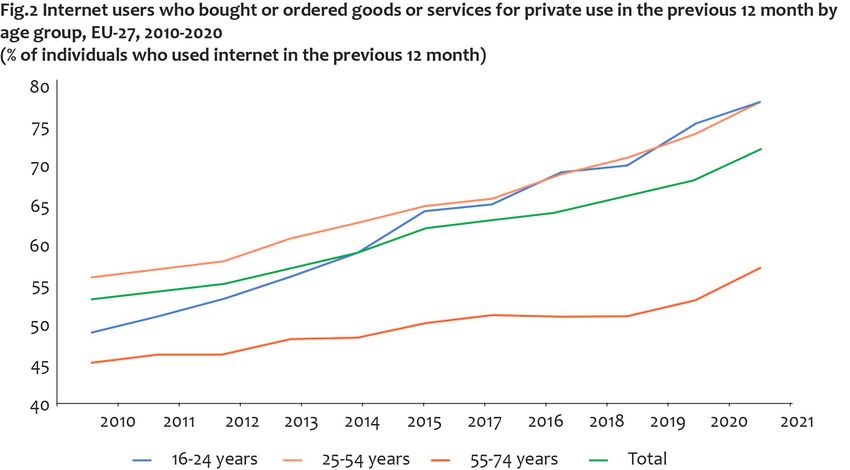

Looking at the evolution trend of the on-line purchases focusing on the European market

the picture that is returned confirm the global frame.

In the European economy, which is mature since many years, is possible to obtain the

horizon of the growth trend considering the last 10 years and highlight an important

factor which also provide a partial explanation to the forecasts.

The graph (fig.2) clearly shows the increase of the number, in percentage, of those who

Politecnico di Milano - Ferrari Giorgio

Introduction 9

carry out on-line purchases respect to the total internet users. The total trend reveals an

increase of 19% in the period 2010-2020.

The breakdown for age bands is highly interesting: as expected the age range that, during

the time period considered, has marked the steps is the European population comprise

between the 25 and 54 years old at least for two reasons: first is the general grater

proclivity to the use of technology and second has the economic availability needed to

purchase from on-line stores; the youngest population range (16 – 24) instead, only in

the last 5 years has equaled the next generation thanks to the diffusion of smartphones

which keep the youngest constantly connected and also thanks to a greater access

to the economy; the oldest European range (55-74 years), the so called Boomers, just

in the last two years has acquired trust in the on-line purchases, more precisely in the

electronic secures payments.

The definition of supply chain is very broad: it starts from the supply of the raw materials

for the production of the goods and ends with the delivery to the final costumer of the

product, passing through the production, warehouses management, the transportation

and, only in the last few years, pushed by the grater focus on the sustainability, it include

also the management of the returned items and the disposal of the product arrived

at the end of their useful life, too much often still considered as waste (the so called

Reverse Logistic). Being the definition of Supply chain so broad it is necessary to narrow

Politecnico di Milano - Ferrari Giorgio

10 Introduction

Surce: Eurostat

the eye to investigate some mechanisms with more precision.

The research focus than on the last ring of the long supply chain: the Last Mile Logistic;

or rather the delivery to the final client at the address that he has specified, which can

be the home, an office, a physical shop, a pickup point.

Logistic and e-commerce are intimately bounded; or more precisely, the logistic has

been constituting itself as a critical factor to the success of any on-line store. Faster

and faster delivery times, customize delivery options and the information on the state

of the delivery of the items have become key factors in the evaluation of similar and

competitive products for the consumers, and they are characterizing more and more

as field of optimization and competition for the on-line colossus, as well as for local

retailers. The ecommerce phenomenon is without any doubt a global disruptor destinate

to expand on the tail of the pluri-studied globalization; however, if the e-commerce is

a global phenomenon which interest the digital world, the purchased goods from the

customer assume a physical dimension, which to finalize the purchase process, need to

be governed in the supply chain, arriving to be managed at the local level to balance the

consumer request and the quality of life of all citizen.

For the digital sellers therefore the selection of the right business model and/or the

logistic partner is of crucial importance to position in the on-line market with a quick,

flexible, and customized offer.

In the supply chain of the good the role of the Last Mile Logistic, that is the part of

the supply chain which directly enters in contact with the final client, has assumed a

fundamental role. From the point of view of the products, with Last Mile Logistic we

Politecnico di Milano - Ferrari GiorgioIntroduction 11

refer to the very last operation that must be done from the stock warehouses closest to

the final destination and the transport of the order to the final customer.

It is particularly interesting to study this segment because it does not constitute just

am organizational busines factor, but it has a number of implications in the physical

world. In particular, the urban areas densely populated are those which pose the grater

challenges: in the urban texture, on which a high number of economic activity and a

multitude of individual interact, the transportation of the goods must untangle and be

able to do not invalidate the quality of life of the inhabitants and the performances of

the other economic activities.

The research work is structured into 2 chapters.

The first chapter identify the correlation between the growth of eCommerce and how it

affects the supply chain especially in the last mile deliveries. In doing so some negative

externalities are described and the related problems that arise when considering the

urban areas. A first part of the solution to these problems refers to the theory of the city

logistic, that is the reason why is given a theoretical framework of the discipline. But the

discipline is not able yet to meet the complexity of the real world. Logistic operators and

administrator are already facing the problem arising both on private and public sphere

trough different model and solutions, which are collected and exposed considering 3

macro-categories.

The second chapter focus on the real estate sector of the logistic.

Starting from an overview of the sector through the analysis of the investments in

Europe and Italy was possible also to understand the drivers that will guide the future

developments. At date, the real estate logistic sector is undergoing a favourable moment

with large private capital looking for secure assets. To ensure the security of the asset the

investors consider as fundamental drivers 4four different areas: demographic changes,

the technological development, the sustainability, and the urbanization.

All these aspects will have in impact on how the logistic will work in the next years. Is

of crucial interest so to understand the relation between those, and in particular the

research focus on the relation between the robotics and the labour.

Identified the different typologies of warehouse which contribute to compose the

supply chain, the research investigates which are the technical characteristics of the

warehouses that are most advanced.

Combining the information about the drivers of the future logistic real estate and the

technical characteristics, the research exposes an innovative model to assess the quality

Politecnico di Milano - Ferrari Giorgio12 Introduction

of the warehouses which could be a useful tool for investors and logistic operators.

At the end, is traced a consideration about the possibility to re-use the existing dismissed

warehouses which can be found in any urban periphery.

Politecnico di Milano - Ferrari GiorgioChapter 1 13

Chapter 2

City Logistic and eCommerce

The transport of the goods in the urban areas has been, and it is forecasted to be, highly

affected by the e-commerce market. In the tradition system of distribution the producer,

the wholesalers and the retailers constitute supply contracts for a given relevant amount

of products, keeping therefore the volume of the transported goods rightly constant

and high; resulting in an efficient utilization of the vehicles and of the other resources.

The distribution in the last miles generated by the request of the consumers endanger

the increment in the volume of traffic in the urban areas to respect the planned delivery.

In the last years, due to the exorbitant increase in the number of on-line purchases and

of the relative home delivery, happened a change in the pattern of the flows of the

goods and of the movement of the vehicles inside the cities. Those changes are affected

and make more complex by factors such as demographic changes and the adoption

of new technologies. The fragmentation of the selling channels, seen the previsions of

growth of the on-line market, could bring to an increase in the volume of the vehicles

used to transport the goods inside the cities, pushed by necessity to offer higher and

higher level of service to the customer most demanding.

If cities, and the administrations, will not be able to respond to the needs of the

transporter, logistic operators, consumers, through the creation of plan of City Logistic

able to rationalize and make more efficient the operation of the transport of the goods

in the urban context, the problems analysed in the previous paragraph will get worst.

Alternatively, according to some theory, if there will be a change in the paradigm of the

model of consumption, the traffic inside the cities could remain balanced: the last mile

Politecnico di Milano - Ferrari Giorgio14 Chapter 1

transport of goods will substitute the consumers travels to purchase the products; it

is possible that the total traffic volume of goods and passengers, in terms of vehicles x

kilometre, will not change radically (fig.3).

Sustainability of the urban transport

The competitiveness of the economic activities inside the urban areas and of the cities

themselves is sustained from the transport of goods, which is itself an economic activity.

Removing the transport activity to eliminate the negative externalities is not a feasible

option: it is necessary to sustain the individual’s life style, maintain the commercial and

industrial activities and support the city. In 2013 has been estimated that the urban freight

traffic, considering all the sectors and the supply chains which need the urban logistic

(retailers, couriers, construction, waste management, reverse logistic, pharmaceutical,

ecc) constitute the 10% – 15% of the total kilometres equivalent vehicles travelled in the

urban areas and up to 3% - 5% of the total surfaces in the cities was destinated to logistic

uses. The cities does not only receive goods, , even if the entry volume generate about

45% of the journeys, but they generate also outwards traffic flows for a 20% - 25%, and

inside the cities itself for the remaining part; even if Eery context is different and need

specific consideration to the problem.

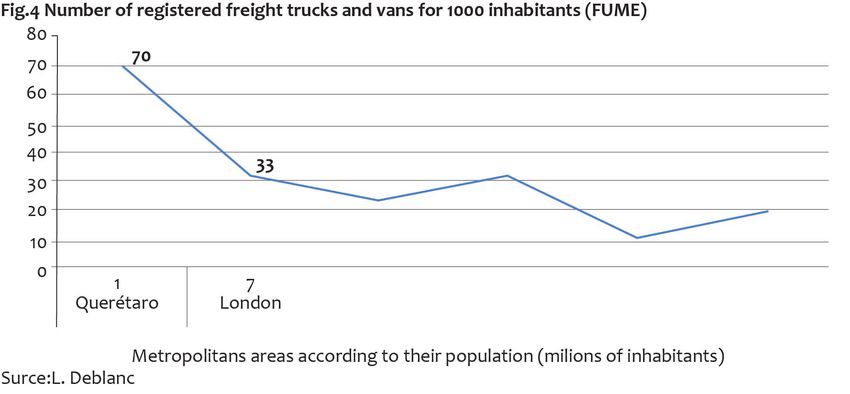

A first index to consider when examining the traffic flow in an urban area is called FUME

(Freight Urban Mobil Equivalent) which measure the total number of freight vehicles in

the cities every 1000 inhabitants (fig.4). According to a study developed by Deblanc L.

in the 2009, using this indicator compared to the city dimension, at the increase of the

number of the inhabitants there is an increase in the efficiency in the goods distribution

service, shown by the minor number of logistic vehicles used.

Politecnico di Milano - Ferrari GiorgioChapter 1 15

Although the share of vehicles used for the urban goods distribution is just a relatively

low percentage respect to the total traffic volume generated by the urban areas, settling

around 12%, it is responsible for 30% of the harmful emissions due to the driving style

which the commercial vehicles are forced to adopt in the dense built areas: frequent

stops and restart, several break, non-optimized good’s loading (as seen up to ¼ of the

journeys are done with empty vehicles).

The urban logistic is without any doubt an increasing phenomenon. It is for a number

of reasons including the eCommerce growth, changing in the lifestyle of the citizens,

ageing of the population, the technology diffusion.

The goods handling for the Last Mile is inherently bounded with read vehicles thanks to

their undeniable advantages in terms of convenience, flexibility, and capillarity without

the need for cargo breakdowns in the journey Door to Door.

The scarce technology innovation of the vehicles used for the deliveries is the first

source of negative externalities; it is true both on the global scale and in the urban and

metropolitan areas where the traffic condenses.

Environmental pollution is certainly the first externality to be taken into consideration.

In fact, one of the key factors that influence the quality of life within cities is the quality

of the air.

In the 2009 the European Parliament resolution “A Europe that protects: clean air for

all”, referring to the European Environment Agency (EEA), estimates that around 90%

of Europeans living in cities are exposed at levels of air pollution deemed harmful to

human health.

Considering that in Europe the road traffic is responsible for around 40% of the total

nitrogen oxide (NOx) emission and that about 80% of the total NOx emissions produced

from traffic is generated by diesel-powered vehicles, which is the principal fuel of the

commercial vehicles. The impact on the European economy of such bad quality air

affecting the human health is a loss of 3% to 9% of the European GDP. Moreover, the EU

notice that one third of the member states does not respect the limit value of PM10 and

NO2, and that one out of five exceed the objectives-value for the PM2.5.

is not difficult to notice than, given the traffic volumes and the relations with the noxious

emissions, the transport sector negatively contributes for a large part to exacerbate the

problem.

The urban distribution is more polluting than the long-distance transport at least for 3

factors:

• Vehicles’ age: usually the vehicles used for the urban distribution are older; it is

Politecnico di Milano - Ferrari Giorgio16 Chapter 1

common that, for this segment of the supply chain, are used vehicles which are

at the end of their useful life since they will have to cover limited distances with a

scares filling rate.

• Vehicles’ dimension: the vehicles used for the urban distribution are usually smaller

due to the limited rooms for manoeuvring and parking.

• Operative speed and inactivity: the traffic admixture and the delivery time slow

down the operations and increase the pollution generated.

The transport activity of the last mile is strongly characterized by inefficiency. The

primary cause is the low load rate of the means of transport which results in the need for

a greater number of vehicles in circulation and an increase in the number of revolutions

which generate both internal and external costs of higher distribution. The average

filling coefficient of commercial vehicles is less than 25% for about 30% of vehicles, while

only 50% reach a filling of 50%. Added to this is the 20-30% share of empty trips. This is

due to the relationship between the loading rate and the size of the packages: as the

size of the packages decreases, the loading rate decreases; the average size of packages

transported decreased with the growth of the eCommerce market. This relationship is

even more pronounced for vehicles with a capacity of less than 3.5 tons, which constitute

the greater number of vehicles used by couriers due to the increasing regulations of

access to urban centers and the low commercial cost of these category vehicle itself.

Air pollution in urban and metropolitan areas is only one of negative externalities of

road transport, perhaps the most discussed. Indeed there are at least 4 other aspects

Fig.5 Population affected by Noise pollution and consequences

Surce: Environmental European Agency, 2020

Politecnico di Milano - Ferrari GiorgioChapter 1 17

that affect the quality of urban life to consider.

According to the Environmental Noise report (fig.5) in 2020 at least 25% of the European

population lives in areas where the level of noise pollution is harmful to health. Vehicular

traffic noise is the predominant source of pollution; about 125 million

people are victims of persistent traffic noise (long-term, day-evening-night), despite the

fact that exposure to high noise has been reduced over the years thanks to technological

progress (engine silence, tyre friction, asphalt characteristics, etc.), and the introduction

of infrastructure works to contain noise by separating residential areas and reads. The

room for improvement, from the point of view of the technologies currently available,

is very narrow: as the volume of traffic expected in urban centres increases, technology

alone will not be able to put a remedy to them.

Road accident are another negative externality. It is not only an economic damage, but

also a question of social equity: a low rate of road safety affects the most vulnerable

groups (the elderly, children and people with disabilities) by reducing their right to

mobility. In addition, high levels of traffic are a barrier and disincentive to the use of

sustainable alternative means (such as bicycles, scooters, longboard, ecc.).

In Europe, thanks to the European policies put in place, in particular through the 2001

White Paper, the accident rate has fallen considerably, even if the objective of halving

road accident mortality is still a long way off.

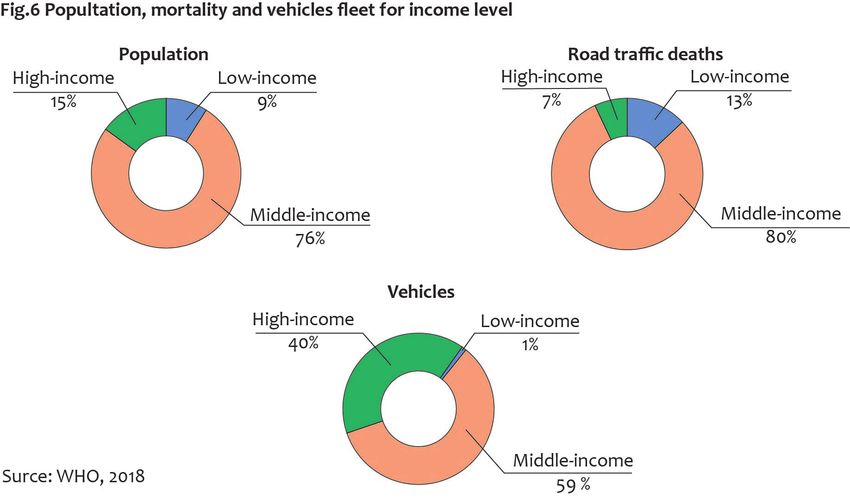

Looking at Who statistics (2018) (fig.6) it is possible to see how in low-income countries

Politecnico di Milano - Ferrari Giorgio18 Chapter 1

circulates around 1% of the global vehicle fleet but register 13% of deadly road accidents

on the global scale. Even in middle-income countries, the proportion of road deaths (80%)

is higher than the percentage of vehicles on the road (59%). The situation is diametrically

opposed in high-income countries where 7% of deaths are recorded compared to a

vehicle fleet comprising 40% of global vehicles.

The last externality that has a significant impact on last mile logistics is congestion.

congestion must be assessed by considering two particular aspects: it not only causes

loss of time both for people and for economic activities due to the promiscuity of traffic

sources (public and private passengers), but also acts retroactively on the management

of courier deliveries. Deliveries in the urban environment are in fact bounded on one

hand by the aforementioned trade-off between the efficiency and effectiveness of the

service and on the other by the socio-economic and environmental context in which

logistics services are organized. Congestion, therefore, causes delays and waste of time

for all those who use the infrastructure; these consequences have direct impacts mainly

of an economic nature.

Highlighted what are the critical factors of urban freight transport, considering the

impact they generate on the operators themselves and on the whole community, it is

useful to identify how the supply of freight transport is available within urban areas.

In Italy, the urban goods distribution can be subdivide into four macro sub-market,

assessable through the technical efficiency and the social welfare, depending on the

business productive process, the typology of the services offered and the modality of

delivery/pickup of the goods.

1- Transport on own account: mode of freight transport which is in general less efficient

because it does not carry out the consolidation of loads. Generally this mode takes place

with single and direct trips, origin-destination, without particular time constraints. The

European Commission estimates that in Europe the urban transport of goods on own

account represents on average about 30-40% of deliveries; In Italy this percentage is

probably higher, and often exceeds 60%. As for the load factor, the operators who use

their own resources, on average reach 50% lower load factor than that of third-party

operators. Production inefficiency is often accompanied by tax evasion of the last mile

transport, in which deliveries are made without packing slip. The promotion of open

municipal logistic platform could be an effective policy which would represent the

solution to the problems of consolidation and illegality of this distribution method.

2- Transport on behalf of third-party logistics operators: the third party operators pick

up the goods in warehouses located outside urban centers, consolidate shipments from

Politecnico di Milano - Ferrari GiorgioChapter 1 19

multiple customers and deliver them to commercial establishments; the vehicles leave

only when they reach a high load, it is therefore irrelevant that operators move for only

one customer: in this case it is a synonymous of a high volume of goods. Structured

third-party transporters adopt more efficient production techniques than own-account

transport: they optimize the routes, has a higher load factor (although rarely optimized

for the return journeys that are often carried out empty), delivers the goods in predefined

time windows and sometimes uses process digital monitoring technologies.

3- Transport on behalf of third parties marginal operators: generally they are family-type

operators who work through subcontracts on an occasional basis. They do not carry out

any form of consolidation, and therefore manage their vehicles with low load factors,

especially for the return journey which is almost always empty.

4- Express courier: the production model of express couriers is based on the optimization

of the service through a high standardization of processes. The added value provided by

express couriers is the ability to ensure absolute certainty in individually agreed delivery

times thanks to tracking & tracing that allows measurement, optimization and more

precise information to the customer on the goods’ shipment.

The different categories of transport offer also reflect different impacts on the urban

environment (fig.7).

Currently, the operators that have the greatest impact on pollution and congestion

are carriers on their own account and marginal third parties operators due to the high

number of vehicles in the fleet and their relative old age. Logistics companies have

a lower impact thanks to the size of the vehicles used. Express couriers are the best

performing in this way: given the intensity of use of vehicles, the vehicle fleet is the most

up-to-date: even if the impact on urban congestion is in line with other operators. Of

particular importance is the qualitative data on the availability of operators to renew the

Politecnico di Milano - Ferrari Giorgio20 Chapter 1

vehicles’ fleet: as mentioned, the express couriers amortize faster the investments and

then replace the vehicles quickly; even the most structured logistic operators have the

propensity to renew their fleet, but given the longer amortization, they require more

time; On the other hand, operators on their own account and unstructured third parties

operators/familiar are totally reluctant to modernize vehicles due to the necessary

investments, which they are often unable to support.

In the urban market the transport demand is mostly consisting of the adoption of the

JIT model (Just in time to reduce the need for warehouse space in central areas where

the cost of the surface is high and economically not profitable). The express courier

companies make around 70% of the deliveries to the businesses which adopt the JIT

model; for which the speed of delivery represent a high-value-added service.

City Logistic

The efficiency of the last mile deliveries is essential for the sustainable growth of cities,

both from an economic as well as from an environmental and social point of view.

Possible solutions to the problems generated by freight transport in the urban

environment have led to the birth of the theory of city-logistics.

The City Logistic institute defines the discipline as “the process for the total optimization

of logistics and transport activities carried out by private companies in urban areas,

considering the environmental impact, traffic congestion and energy consumption within

the framework of the urban economic market”. The negative effects and inefficiencies

of activities related to the transport of goods in cities are therefore the reasons why

analyses are carried out on the handling of goods in the urban environment. Urban

logistics focus on improving the efficiency of urban freight transport while reducing road

congestion and reducing environmental impacts. According to Ogen the main objective

of the City Logistic is to reduce the total social costs generated by the transport of

goods. However, the total costs can be divided into 6 specific objectives pursued by the

discipline: 1. Economic 2. Efficiency 3. Road safety 4. Environmental 5. Management of

infrastructures and 6. Urban structure.

In general terms, the movement of goods in urban areas has its roots at regional,

national and international levels. As we have seen, urban freight transport is generated

by a large number of actors who have also as many interests.

Within the cities, therefore, there are multiple flows of goods corresponding to the

multiple supply chains and the multiple transport needs for the multitude of activities.

Politecnico di Milano - Ferrari GiorgioChapter 1 21

In order to be able to model the transport of goods in the urban environment, it is useful

to know the different stakeholders who are interested in the domain of the city logistics.

Boerkamps provided an urban freight domain (fig.8) identifying 4 different actors

(shippers, couriers, customers, administrators) who operate in a city context.

Those actors are interested in five typologies of actions (Spatial organization of activities,

Trade relations, Transport services, Traffic system, Multimodal intfrasatructure) which

generate some interaction among them. In order to fulfill their need they have to refer to

3 main market (Commodity market, Transport services market, Infrastructure market).

In e-commerce, the relationships between the four types of identified stakeholders take

on different identifications and nomenclatures based on the exchanges between them

(fig.9). The graph shows the relationships between the types of stakeholders and the

acronyms with which trades are defined.

The stakeholders belong to different links in the domain of urban logistic and are directly

connected to at least one pair of transport components, but, on the other hand, little

Politecnico di Milano - Ferrari Giorgio22 Chapter 1

related to the entire chain. However, although a single stakeholder can only influence

the part of the supply chain with which it is closely connected his action affects the

entire supply chain.

The objectives mentioned above within the City Logistic theory are therefore treated

differently depending on the stakeholder considered. However, it is possible to divide

the groups of interests into two main categories:

1. stakeholders belonging to the public sector which include traffic authorities,

infrastructure authorities, municipalities, public transport authorities. This stakeholders

can be named Administrators. Inside this cathegory can be placed also the users of the

urban infrastructures and the residents; even if them are not directly involved in the

process of organization of the urban freight transport.

2. Private sector stakeholders include manufacturers, suppliers, shippers, drivers,

merchants, and customers.

Although all these public and private stakeholders share the objective of transport

goods to/out/in the urban area, their individual interests are often conflicting: for

the Aadministrators, the central issue of decisions is the liveability of cities and the

environmental and economic sustainable development of the area; for shippers

belonging to the private sector the main interest is to minimize the cost of transport. In

particular, private companies are more interested in the Total Logistical Cost than the

specific cost for the last mile transport; they can leverage on several different factor

within the wider supply chain to create margins. Private companies therefore optimize

the Total Logistical Cost against which the cost of goods’ distributin within the city is

only a small part (it is estimated that it represents 2-3% of the entire logistical cost).

Despite the private interests that act on the urban transport of goods, administrators

are a central part of the decision-making process of the domain of the City Logistic

theory and organization. This concept clarifies why most urban logistics models are

developed through the administrative point of view and predominantly without taking

into account the behaviour and/or characteristics of other private stakeholders.

The movement of goods within the urban environment can be analysed from different

perspectives for the same objective pursued. It is therefore important to understand

what different strategic points of view are available and how effective they are in

achieving the proposed objectives. There are four main perspectives in the organization

of urban freight transport:

1. Planner perspective: In an urban area, where space is limited and infrastructure

expansion can be extremely expensive, the importance of proper planning is crucial.

Politecnico di Milano - Ferrari GiorgioChapter 1 23

Planners must manage and organise the flow of vehicles through efficient use of

existing infrastructure and services. Given a set of different parameters,a planner is then

interessed in define which strategies and their combinations produce the best result.

2. Technologial Prospective: the technological innovation happened in the recent

years have opened scenarios of real-time management of the transport. The dynamic

informations based on GPS combined with GIS allow to chose the less chongestionated

route and then save time and money. Commercial vehicles can benefit from this

innovations and increase the efficiency of delivery operations. The technology changes

have transformed the decision-making process of logistic transports.

3. Behavioral perspective: behavioral analysis tries to understand, describe, and

predict the behavior of actors in different scenarios. Behavioral models consider the

attributes of complexity and the ability to make decisions of different stakeholders that

traditional transport organization models are unable to take into account. Boerkamps’

GoodTripmodel, for example, includes the behavioral aspects of administrators,

suppliers, couriers, and consumers to analyze the urban freight system. This model

aspires to help the decision-making process by evaluating new distribution systems and

the impacts of changes in the planning of the distribution of goods.

4. Regulation perspective: the movement of goods in urban environments can be

improved to make it more sustainable in different ways. Van Duin distinguishes two

different groups which are capable of changing the urban distribution system. The first is

the change made by the private sector that seeks to reduce the environmental and social

impact through the reduction of externalities generated by the operational activities of

the vehicle fleet. The second way for the transition to a sustainable freight transport

is operated by administrations through the introduction of policies and measures that

force companies to change their activities and thus become more sustainable and

efficient both at environmental and social level. This therefore means regulatory policies,

incentives, and disincentives to reduce negative externalities related to the movement

of goods in urban areas (e.g. restrictionson weight-based vehicles, size, delivery time).

To develop a City logistics model, however, it is not possible to take into account only

the four types of actors found within the cities, but it is also necessary to understand

the spatial and organizational characteristics that make up the city itself. Since each city

represents a unique given set contituted by the infrastructures and modes of transport,

it is not possible to develop a single general strategy for improving the distribution of

goods in the urban environment that is directly applicable to all cities. Population size

and density are two of the main factors when it comes to urban logistics. Globally, four

Politecnico di Milano - Ferrari Giorgio24 Chapter 1

general patterns of urban logistics can be identified:

1. Big metropolitan areas in advanced economies: logistics organisation in these cities

integrates transport and logistics within the urban environment, where a high number

of retailers prevail. The role of physical stores is changing rapidly through e-commerce

thanks to highly organized transport companies that provide home delivery services or

pick-up points. These companies use information Technology tools.

2. Large metropolitan areas in developing economies: in these booming urban realities

there is a double face of the freight distribution system. On one hand, the needs of

logistics are comparable to the realities of the most advanced urban areas, but it coexists

with a largely informal and untraced delivery system. Added to this problem, it should

be noted that the infrastructure system is poorly maintained

3. Interchange regions: these urban regions concentrate the growth of new terminals

for goods that serve both as distribution facilities for local consumer and urban business

markets, as well as regional hubs for the redistribution of goods at regional, national and

international level. A characteristic feature of these areas is the increase in the number

and size of warehouses and distribution infrastructure located in the metropolitan

periphery.

4. Smart City logistics: these cities, often made up of medium-sized historic centers, adopt

innovative delivery schemes in urban areas with a particular emphasis on environmental

and social sustainability. This type of city can be identified in most European cities.

It has therefore been seen that the urban freight transport system is characterized by

multiple stakeholders, often with competing objectives, and is strongly influenced by

the physical and organizational characteristics of the city. In the absence of a central

authority to guide the different processes of rationalization of City logistics models, each

of these stakeholders would act independently; but in the complex system of the urban

areas, it is clear that the autonomous, non-integrated actions of the different actors

involved in the field of logistics leads to inefficiencies of the city system as a whole.

Over the past decade it has become clear that the organization and rationalization of

logistics and distribution of goods in the urban environment cannot take in consideration

just one of the above perspectives. Takeing into account the multiplicity of stakeholders

and the peculiarities of the city itself the European Union has launched the CIVITAS

initiative. The initiative brings together best practices and provides guidance in

organising a cleaner and more transport-efficient city.

The idea undertaken by the European Union, which is behind the development of a clean

and energy-efficient integrated transport policy, is the most advanced interpretation

Politecnico di Milano - Ferrari GiorgioChapter 1 25

in the implementation of the City logistics plans. In the Policy Advice Notes within

the second edition of the initative CIVITAS II (2005-2009), addressed to municipal

administrations to improve the delivery of goods in the urban centers or in specific

areas of the city, are idenftified what are the possible operational solutions, the target

groups of the measures to be taken and their impacts and benefits for each group.

Besides it also describes the implementation phases, the timing and an indication of the

investments necessary by public administrations to start such projects. It is interesting

to note that the advices suggest to development an urban logistics plan involving all

the different stakeholders that we have identified previously through consultations and

workshops in order to create consensus on the decisions that will be taken. The role of

the administration therefore remains central to the plan to pursue the interests of the

community. Furthermore, the notes state the necessary public economic contribution,

at least at the initial stage of the implementation of the plans, for the success of the

operation which should not be underestimated.

Last mail logistics models and adopted solutions

Within the discipline of City logistics, some solutions have now been implemented for

the efficiency of freight transport in urban areas, while others are still in the study and/

or development phase.

The solutions undertaken or in the theoretical phase of research and experimentation

are also considered as facilitating factors for the transformation and organization of

transport and can be divided into 5 categories:

1- Infrastructures: In recent years, public authorities, distributors and couriers have

been forced to invest in the improvement and optimization of infrastructures that serve

the last mile logistics. These infrastructures are defined as the logistical assets, both

public and private, that form the network through which urban deliveries are made.

Among the logistical assets, the most important are warehouses, lockers and loading/

unloading areas. A particular chapter will be dedicated to these solutions. However, for

infrastructures is essential to be located in optimal locations and to have a high rate of

digitization.

2- Technology: there are numerous technologies that are transforming the supply chain.

These technologies, as well as future ones, need to be integrated into the digitization

process of last mile logistics to meet consumer needs. This category of solutions can be

listed by their level of maturity reached. The new technologies will have to be adopted

Politecnico di Milano - Ferrari Giorgio26 Chapter 1

by distributors and couriers to compete efficiently and to guarantee a high quality of

service to customers.

3- Regulation: As mentioned, public authorities play an important role in implementing

new last-mile logistics models, but it is currently possible to recognize certain inefficiencies

within the regulatory framework that affect the planning and efficiency of logistics. In

adopting future regulations, it will be essential for administrations to implement models

that optimize urban logistics while ensuring the well-being of citizens.

5- Cooperation: the cooperation between different actors involved in the delivery of

goods at different levels will lead to the result of the interactions that will lead to some

form associations. The first and most important of the associations will be cooperation

between public authorities, agents, and companies active in the sector; all together to

implement new logistics models for the last mile.

Regulation

Among the management strategies of freight transport in the urban area is of

fundamental importance to understand the limitations of these strategies: uniformity

in regulations is necessary: in fact today almost each city establishes its own rules

for access and movement of goods within the city; there are delays in the regulation

implemented by public authorities which react late and with inefficiencies trying to

contain negative externalities; and finally, greater cooperation is needed between the

stakeholders involved in the urban environment.

These governance strategies include all those measures that limit access to certain

portions of the city based on certain parameters.

Regulation by time slots:

- access times: prevent access to vehicles for a certain area or road at certain times of

the day. These rules are applied to areas that are more sensitive to the consequences of

congestion (pedestrian shopping areas, residential streets, entire neighborhoods)

- loading and unloading times: they limit the loading and unloading of vehicles on the

road

- preferential lanes for commercial vehicles: the use of certain preferential lanes is

allowed to specific vehicles with the aim of reducing road congestion

- load factor limit: vehicles that do not reach a certain load rate are subject to access

restrictions. This measure requires effective forms of control to verify the real load rate.

- Areas used for loading and unloading of goods: those are spaces dedicated to loading

Politecnico di Milano - Ferrari GiorgioChapter 1 27

and unloading operations, the objective is to reduce the interference of freight transport

with private traffic

- Road pricing: the use or access to particular infrastructures and/or areasis subjected

to the payment of a toll. This measure has three objectives: to generate a cash flow

for the administration, to rationalize the demand for transport in the city center and

to internalize the negative externalities of freight transport. The result that can be

obtained through this solution is the reduction of vehicles used for transporting goods

and the reduction of polluting emissions.

Technology

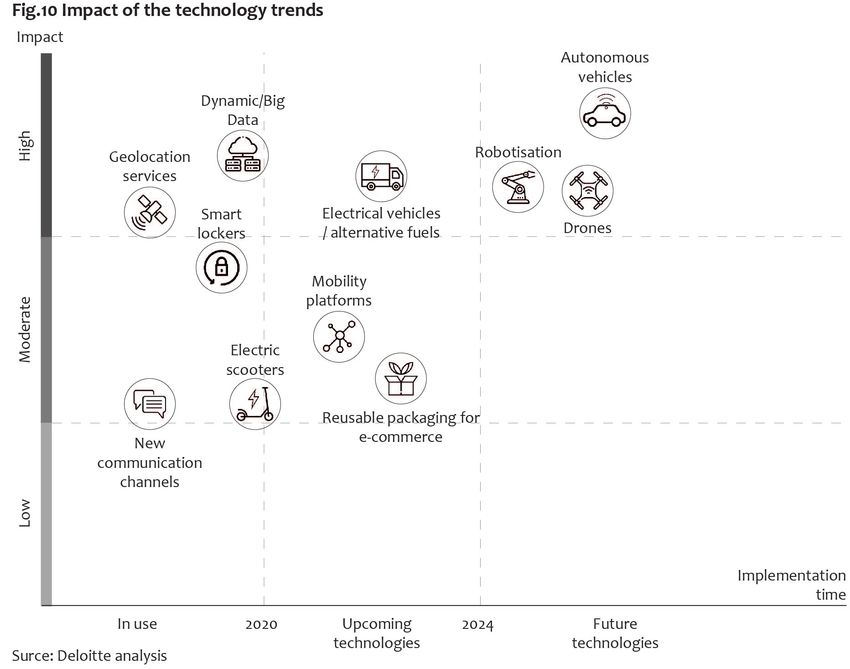

The list of technological solutions presented is to be understood as a chronological

succession and represent the level of maturity reached. Some of these technologies are

therefore already widely used in the management of goods distribution in urban areas,

while others are still under development.

Technology currently available and in use:

- new communication channels: the need to offer an omnichannel experience is

underlined by the need to communicate with customers. Through communication

channels that exploit artificial intelligence it is possible to create effective and real-time

communication with customers (e.g. chatbot)

- geolocation services: traceability and localization within the logistics chain allows

you to know the route and position of the package in real time. Couriers are therefore

able to offer to the consumer the opportunity to make changes with respect to the

delivery point and time, obtaining in exchange the ability to optimize routes and reduce

costs related to delivery failures. This technology is particularly implemented in long-

distance shipments but over 90% of couriers dealing with urban delivery do not use this

technology.

- Big Data: the collection and management of large quantity of information (defined

as Big Data) allows the efficient management of orders and to make correct decisions.

Using Big Data can help logistics companies cut costs by up to 50%

- smart lockers: this service is still not very widespread even if it allows couriers to save

0.8 euro/package by standardizing routes and eliminating delivery failures

- electric scooters: the eCommerce sector is the most capable of exploiting this

technology by reducing emissions from last mile deliveries up to 80%. The use of electric

scooters allows curriers to access faster urban areas even where access to traditional

vehicles is not allowed.

Politecnico di Milano - Ferrari Giorgio28 Chapter 1

Technologies that are expected to become part of the solutions in a consistent way in

the near future:

- Reusable packaging for e-commerce: it involves the use for the delivery of reusable

packages that are returned to special distribution centers in order to be reused. This

type of packaging reduces the environmental footprint for the single package.

- Mobility platforms: using data and information on mobility within the urban area (open

data), transport companies can effectively manage route planning and adapt them to

different circumstances.

- Electric vehicles or vehicles powered by alternative sources: electric motors or

powered by alternative sources (ethanol, methanol, natural gas, hydrogen) are able

to significantly reduce the emissions produced by traditional combustion vehicles. The

emissions produced could even be halved.

Future technologies still under research

- drones: in the urban delivery market of e-commerce products, delivery via drones

seems to be the most successful. Considering the average size of the parcels that are

delivered for the e-commerce market, this technology would reduce the number of

vehicles circulating within the city by up to 60%. However, careful local, national, and

Politecnico di Milano - Ferrari GiorgioChapter 1 29

European regulation is required for the implementation of this technology.

- Self-driving vehicles: the increasing ability of vehicles to move autonomously within

urban areas can allow an increase in the service levels perceived by the customer, who

could decide the day and time of delivery in complete autonomy.

- Robotization: the use of robotics inside the sorting warehouses would eliminate the

need to consider the maneuvering and safety space for workers, thus increasing the

space available for storage by up to 50%. Furthermore, the robotization inside the

warehouses would allow a saving of the cost of operations of about 20%

Of the technologies presented, it is possible to create a graph (fig.10) that shows the

impact on the logistics challenges of the last mile and a rough forecast of the timing for

the necessary implementation times.

Cooperation

The growing need and increasingly stringent needs of consumers, who require

personalized services at lower prices (if not free of charge) push distributors and couriers

who transport goods in the last mile to seek solutions outside of established business

practices. Cooperation with other actors involved in the deliveries of goods has led to

different forms of association. It is possible to group the different forms of associations

into three macro chategories:

- Cooperation between manufacturing and distribution: with the aim of eliminating

interference from the distribution system, reducing costs and increasing end customer

satisfaction, distributors and producers of goods seek optimization in two areas:

1- advanced planning of the services offered through more effective communication

and the use of applications trying to minimize the time needed to manage orders and

maximize efficiency within the warehouses;

2- by simulating consumer demands through IT management systems capable of

processing Big Data, producers and distributors try to predict future consumer demands.

- cooperation between different distributor companies: some of the main urban

distributors, to reduce the cost, need to work together and implement innovative

measures. An example of this cooperation can be found in LOGICOM4.0, a platform that

integrates and digitizes transport documents accessible to all transporters and which is

also able to track delivery in real time.

- cooperation between the private sector and public authorities: the collaboration

between administrations and private transport companies has as its objective the

implementation of urban logistics plans and the identification of strategic locations

capable of satisfying the objectives of all stakeholders.

Politecnico di Milano - Ferrari GiorgioYou can also read