Principal Financial Group - May 2019

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Principal Financial Group ® May 2019

Use of Non-GAAP financial measures

A non-GAAP financial measure is a numerical measure of performance, financial position, or cash flow

that includes adjustments from a comparable financial measure presented in accordance with U.S. GAAP.

The company uses a number of non-GAAP financial measures management believes are useful to

investors because they illustrate the performance of the company’s normal, ongoing operations which is

important in understanding and evaluating the company’s financial condition and results of operations.

While such measures are also consistent with measures utilized by investors to evaluate performance,

they are not, however, a substitute for U.S. GAAP financial measures. Therefore, the company has

provided reconciliations of the non-GAAP financial measures to the most directly comparable U.S. GAAP

financial measure within the slides. The company adjusts U.S. GAAP financial measures for items not

directly related to ongoing operations. However, it is possible these adjusting items have occurred in the

past and could recur in future reporting periods. Management also uses non-GAAP financial measures

for goal setting, as a basis for determining employee and senior management awards and compensation,

and evaluating performance on a basis comparable to that used by investors and securities analysts.

The company also uses a variety of other operational measures that do not have U.S. GAAP counterparts,

and therefore do not fit the definition of non-GAAP financial measures. Assets under management is an

example of an operational measure that is not considered a non-GAAP financial measure.

2

Forward looking statements

Certain statements made by the company which are not historical facts may be considered forward-looking statements,

including, without limitation, statements as to non-GAAP operating earnings, net income attributable to PFG, net cash flow,

realized and unrealized gains and losses, capital and liquidity positions, sales and earnings trends, and management’s beliefs,

expectations, goals and opinions. The company does not undertake to update these statements, which are based on a

number of assumptions concerning future conditions that may ultimately prove to be inaccurate. Future events and their

effects on the company may not be those anticipated, and actual results may differ materially from the results anticipated in

these forward-looking statements. The risks, uncertainties and factors that could cause or contribute to such material

differences are discussed in the company’s annual report on Form 10-K for the year ended Dec. 31, 2017, and in the

company’s quarterly report on Form 10-Q for the quarter ended Sep. 30, 2018, filed by the company with the U.S. Securities

and Exchange Commission, as updated or supplemented from time to time in subsequent filings. These risks and

uncertainties include, without limitation: adverse capital and credit market conditions may significantly affect the company’s

ability to meet liquidity needs, access to capital and cost of capital; conditions in the global capital markets and the economy

generally; volatility or declines in the equity, bond or real estate markets; changes in interest rates or credit spreads or a

sustained low interest rate environment; the company’s investment portfolio is subject to several risks that may diminish the

value of its invested assets and the investment returns credited to customers; the company’s valuation of investments and

the determination of the amount of allowances and impairments taken on such investments may include methodologies,

estimations and assumptions that are subject to differing interpretations; any impairments of or valuation allowances

against the company’s deferred tax assets; the company’s actual experience could differ significantly from its pricing and

reserving assumptions; the pattern of amortizing the company’s DAC and other actuarial balances on its universal life-type

insurance contracts, participating life insurance policies and certain investment contracts may change; changes in laws,

regulations or accounting standards; the company may not be able to protect its intellectual property and may be subject to

infringement claims; the company’s ability to pay stockholder dividends and meet its obligations may be constrained by the

limitations on dividends Iowa insurance laws impose on Principal Life; litigation and regulatory investigations; from time to

time the company may become subject to tax audits, tax litigation or similar proceedings, and as a result it may owe

additional taxes, interest and penalties in amounts that may be material; applicable laws and the company’s certificate of

incorporation and by-laws may discourage takeovers and business combinations that some stockholders might consider in

their best interests; competition, including from companies that may have greater financial resources, broader arrays of

products, higher ratings and stronger financial performance; technological and societal changes may disrupt the company’s

business model and impair its ability to maintain profitability; a downgrade in the company’s financial strength or credit

ratings; client terminations, withdrawals or changes in investor preferences; inability to attract and retain qualified

employees and sales representatives and develop new distribution sources; an interruption in telecommunication,

information technology or other systems, or a failure to maintain the confidentiality, integrity or availability of data residing

on such systems; international business risks; fluctuations in foreign currency exchange rates; risks arising from participation

in joint ventures; the company may need to fund deficiencies in its “Closed Block” assets; the company’s reinsurers could

default on their obligations or increase their rates; risks arising from acquisitions of businesses; and loss of key vendor

relationships or failure of a vendor to protect information of our customers or employees.

3Company Overview

A leading financial services company

Fortune 500 company; 140 year history; customers in over 80 countries

Non-GAAP pre-tax Assets Under Management2

operating earnings1 $675.4 billion

$2,222.9 million As of Mar. 31, 2019

As of Mar. 31, 2019

RIS - Fee

8% Principal Global Principal Global

Investors Fee

13% Investors

13% 22%

Principal

International

24% Other Entities of

RIS - Spread Spread PFG

19% 63%

25%

Specialty

13% Benefits Risk Third Party Asset

Managers

Individual Life

1 Trailing Twelve Months. Excludes Corporate.

4 2 Assets under management by asset manager.Company Overview

Segment reporting structure

Principal Financial Group

Dan Houston Chairman, President & CEO

Deanna Strable CFO

Retirement Principal Principal U.S. Insurance

and Income Global International Solutions

Solutions (RIS) Investors (PGI) (PI) (USIS) Corporate

Renee Schaaf Pat Halter Luis Valdes Amy Friedrich

President President President President

Specialty

Individual

RIS-Fee RIS-Spread Benefits

Life

(SBD)

Management team averages approximately

30 years of industry experience

5Company Overview

Global Asset Management

Principal Global Asset Management (GAM)

Tim Dunbar

Principal

Global Strategy,

Principal Global International (PI)

General Account RobustWealth Marketing &

Investors (PGI) investment

Product

operations*

Institutional Retirement High net worth/Retail

investors investors investors

*As permitted and in accordance with regulatory guidelines in the markets in which we operate.

6Company Overview

Experienced management team

Name Age1 Title (Industry/PFG)1__

Daniel J. Houston 58 Chairman, President & Chief Executive Officer 35/35

Timothy M. Dunbar 62 President – Principal Global Asset Management 38/33

Amy C. Friedrich 49 President - U.S. Insurance Solutions 23/19

Patrick G. Halter 60 CEO & President – Principal Global Investors 35/35

Renee Schaaf 61 President - Retirement & Income Solutions 39/39

Luis E. Valdes 62 President - International Asset Management and Accumulation 31/28

Julia M. Lawler 59 Executive VP & Chief Risk Officer 37/35

Gary P. Scholten 62 Executive VP, Chief Information Officer & Chief Digital Officer 39/39

Karen E. Shaff 65 Executive VP, General Counsel & Secretary 37/37

Deanna D. Strable 51 Executive VP & Chief Financial Officer 30/30

Jon N. Couture 54 Senior VP & Chief Human Resources Officer 15/2

1 As of 12/2019

7Company Overview

Industry leadership

Global Asset

Management

Best Place to Work in Money Mgmt1

#1 APV - Chile2

Top 10 manager Real Estate3

7th largest manager High Yield 4

ENERGY STAR Partner of the Year5

Global Retirement Risk

and Long-Term Savings Protection

#5 provider of DC plans6 #1 Non-qualified deferred

compensation 13

#1 Pension provider in Latin America7

#3 Non-medical coverages14

#5 AFORE – Mexico 8

#5 Individual Disability

#1 P/VGBL - Brazil9

Insurance15

#6 MPF provider – Hong Kong 10

#1 provider of DB plans11

#1 provider of ESOP plans12

Sources: 1 Pensions & Investments, “The Best Places to Work in Money Management”, PGI recognition 12/10/2018. 2 SVS, SP, December 2018. 3 The 7th

largest manager of worldwide real estate assets out of 88 managers profiled. “Largest Real Estate Managers”, PENSIONS & INVESTMENTS, October 1,

2018. 4 The 7th largest manager of high yield securities, out of 76 managers profiled. Managers ranked by U.S. institutional, tax-exempt assets managed

internally, as of December 31, 2017. “Largest Money Managers”, PENSIONS & INVESTMENTS, May 28, 2018. 5 April 2018, U.S. Environmental Protection

Agency. 6 PLANSPONSOR Defined Contribution Recordkeeping Survey, July 2018. 7 7AUM among multi-country pension providers; Fenaprevi December

2018. 8 CONSAR in terms of AUM, December 2018. 9 Ranking in terms of AUM, Fenaprevi. December 2018. 10 In terms of AUM, Mercer, December 2018.

11 PLANSPONSOR Defined Benefit Administration Survey, May 2018. 12 PLANSPONSOR Defined Contribution Recordkeeping Survey, July 2018.

13 PLANSPONSOR Defined Contribution Recordkeeping Survey, July 2018. 14 LIMRA 2017 survey: Non-medical based on fully insured employer contracts

in force. 15 LIMRA 2018 survey: Individual Disability Insurance (IDI) rank based on in-force premium.

8Company Overview

Current ratings

(As of April 2019)

Moody’s Investors

Fitch Ratings Standard & Poor’s A.M. Best

Service

‘AA-’, Very Strong – ‘A+’, Strong – fifth ‘A+’, Superior –

‘A1’, Good – fifth

fourth highest of highest of 20 second highest of

highest of 21

19 rating levels. rating levels. 13 rating levels.

rating levels.

Outlook: Stable Outlook: Stable Outlook: Stable

Outlook: Stable

Financial Strength ratings related to Principal Life Insurance Company and

Principal National Life Insurance Company.

9Company Overview

The customer remains at the

center of our strategy

Our customers

Small to Medium Sized

Individuals Institutions Customer

Businesses (SMBs)

We help people We help businesses We tailor investment Individuals

save and invest; address risks and solutions to client Institutions

and protect against compete for talent, preferences, risk SMBs

financial risks through insurance, tolerances and long-

through insurance retirement and term investment

and guaranteed other employee benefits. objectives.

income.

Our foundation

Customer Focus | Talent Development | Financial Strength | Integrity | Operational Excellence |

Capital & Risk Management | Diversity & Inclusion | Social Responsibility

10Retirement & Income Solutions

Small to medium businesses (SMBs)

Retirement • Employer-Sponsored Retirement Plans

and Income o Defined Contribution (DC)

o Defined Benefit (DB)

Solutions o Employer Stock Ownership Plan (ESOP)

o Nonqualified Deferred Compensation (NQ)

overview • Pension Risk Transfer (PRT)

• Trust and Custodial Services

SMBs

Individuals

Our mission • Annuities (variable and fixed)

To help more people save • Individual Retirement Accounts (IRA)

enough, protect enough • Certificate of Deposits (CD)

and have enough in • Money Market Accounts (MM)

retirement.

Institutions

• Employer-Sponsored Retirement Plans

• Pension Risk Transfer (PRT)

• Trust and Custodial Services

• Investment Only solutions

o Medium-Term Notes

o Guaranteed Interest Contracts (GIC)

o Stable Value Wraps

11Retirement & Income Solutions

Strong business fundamentals

Net cash flow as a

percent of beginning

of year account value 2015 1Q19 CAGR

(2013-2017 average)

RIS total account value $210B $286B 10%

Principal

RIS-Fee return on net

+1% revenue2

32.0% 31.8%

RIS-Spread return on net

63.0% 70.3%

revenue2

Participants3 4.7M 5.7M 6%

-1%

Industry 1

1 Department of Labor & Cerulli Associates, 2017. 2 For trailing 12 months. 3 Defined contribution and defined benefit.

12Retirement & Income Solutions

Market leading solutions

Principal Total Retirement Suite SM Principal is a leader in retirement

is still a differentiator income

Defined Contribution #3 Pension Risk Transfer4

#5

Recordkeeper1 (number of plans) (by premium)

Defined Benefit Provider3 Individual Immediate Annuities5

#1 (number of clients)

#4 (by premium)

Employee Stock Ownership Plan Deferred Income Annuities5

#1 #4

Recordkeeper1 (number of plans) (by premium)

Nonqualified Deferred Comp

#1

Recordkeeper2 (number of plans)

1 Defined

Contribution and ESOP: PLANSPONSOR Recordkeeping Survey 07/18; 2 Defined Benefit: PLANSPONSOR DB Administration

Survey 05/18; 3 Nonqualified Deferred Compensation: PLANSPONSOR Recordkeeping Survey 07/18; 4 LIMRA Secure Retirement Institute

13 based on premiums as of 12/31/2018; 5 LIMRA Secure Retirement Institute – based on premiums as of 12/31/2018

–Retirement & Income Solutions (RIS – Fee)

Flexible business model serves multiple markets

Bundled

(Full Service) MetLife Fidelity

T.Rowe Price

Prudential

Vanguard

BUSINESS MODEL

Mass Mutual

Empower

Ascensus

Transamerica

VOYA

Nationwide

John Hancock

Unbundled

(TPA)

Small Case TARGET MARKET Large Case

14Retirement & Income Solutions (RIS – Fee)

U.S. retirement market potential remains immense

U.S. retirement system dominant,

Retirement market despite under-savings (in trillions)

opportunities $30

RETIREMENT READINESS: $25

• New plan formation

• Non-participants $20

• Under-saved

$15

INCOME SOLUTIONS:

• Yield/Income $10

• Outcomes:

−Longevity $5

−Market volatility

$0

−Inflation

Defined Benefit (DB)

Private Defined Contribution (DC) and

Individual Retirement Account (IRA)

2nd-15th largest retirement systems

combined

Sources: Retirement Markets 2017, Cerulli Retirement Markets, 2018;

15 https://www.willistowerswatson.com/-/media/WTW/Images/Press/2018/01/Global-Pension-Asset-Study-2018-Japan. pdfRetirement & Income Solutions (RIS – Fee)

Balanced sales approach

Transfer deposits

16 15.2

14

12.4 12.5 3.9

12

9.9 3.3 3.1

10 3.2 4th Quarter

$ Billions

2.5

8 2.6 2.6 3rd Quarter

1.9 3.7 2nd Quarter

6

2.3 2.9 1st Quarter

1.9

4

4.4 5.2

2 3.6 4.2 3.9

0

2015 2016 2017 2018 2019

16Retirement & Income Solutions (RIS – Fee)

The power of payroll deduction

Recurring deposits

25

22.0

• People making a

20.1

deferral +15%1 20 19.0

5.2

17.9

• Avg deferral per 4.5

4.6

member +7%1 15

4.2

5.2

• People receiving a

$ Billions

4.9

4.3 4.6

match +20%1 10

5.8

4.9 5.2

4.6

5

5.0 5.4 5.8 6.3

4.8

0

2015 2016 2017 2018 2019

1st Quarter 2nd Quarter 3rd Quarter 4th Quarter

1 4Q18 compared to 4Q15

17Retirement & Income Solutions (RIS – Fee)

Account value detail

100% 5% 5% 5% 4% 4%

90% 7% 7% 7% 7% 7%

Individual Variable

Annuities

80%

25% 26% 29%

32% 33%

Employer Securities

70%

60% Non-Proprietary

50% Funds

30% 28% 27%

40%

24% 25% Proprietary Funds

30%

Separate Account

20% 27% 29% 29% 28% 27%

10% General Account

6% 6% 4% 5%

0% 4%

2015 2016 2017 2018 1Q19

18Retirement & Income Solutions (RIS – Spread)

The diversified customers we serve

Pension Risk Transfer customers Individual Annuity customers

302,000 lives diversified by age 277,000 lives diversified by age

Age 90+

Age 90+ Below

Below age 60 7%

6% age 60

16% 15%

Age 80-89 Age 80-89

19% 19%

Age 60-69

Age 60-69 30%

Age 70-79

Age 70-79 26% 29%

33%

As of 12/31/2018

19Retirement & Income Solutions (RIS – Spread)

Serving SMBs enhances diversification

Principal’s PRT plans by industry1 PRT new sales market share

Over 90% of plans have under 100 lives by premium and contracts2

Trade 40%

7% Finance

14%

Tax-Exempt 30%

14%

20% #2

Labor

5,250 13%

plans #3

10%

Services

22%

0% Principal

Top competitors

Manufacturing

Premium Contracts

30%

1 As of 12/31/2018

2 LIMRA Secure Retirement Institute, 2018 sales

20Retirement & Income Solutions (RIS – Spread)

Innovative solutions: solving income needs

Multi-product solution set to

transition retirement savings

into income streams SMBs

Our approach:

• Education

• Annuities to provide: • Planning

‒ Fixed returns assistance

‒ Guaranteed income (RetireSecure®)

‒ Protection against volatility • Full array of

options

• Bank products

• Innovative

• Pension Risk Transfer solutions

‒ Defined Benefit plan terminations • Digital advice

21Principal Global Investors

Diversified global asset

management organization

$59 B • Broad range of investors in over 80 countries

• Offices in major money centers worldwide

Fixed Income

$423 B $195 B • Long commitment to corporate stewardship;

Equity

of AUM 1 signatory to United Nations’ Principles for

Alternatives

Responsible Investment (PRI)

$169 B

• Principal ranked among top companies with

$148 B

1,000+ employees in Pensions & Investments’

Best Places to Work in Money Management,

for the seventh year in a row2

$81 B

$137 B PGI Sourced Institutional

$423 B PGI Sourced Retail

of AUM 1 General Account

$97 B Other Proprietary

$108 B

1 AUM as of 03/31/2019. 2 Pensions & Investments, “The Best Places to Work in Money Management”, PGI recognition

22 12/10/2018.

22Principal Global Investors

Overview - key areas of focus

Leverage our client focused business model

• Design and deliver products informed by the voice of the client

• Further enhance our ability to capture client perspectives

• Take advantage of our modernized distribution model

Commitment to further build out of high value, specialist capabilities

• Develop additional capabilities in private assets, including globalization of our

highly successful real estate investment franchise

• Continue build out of systematic beta in equities and fixed income boutiques

Strategically leverage technology across the business

• Use digital technology to improve our core investment processes

• Facilitate delivery of customized solutions to Retirement and Retail investors

• Empower sales and marketing teams with more efficient ways to reach our clients

and their advisors

23

23Principal Global Investors

Broad global distribution in retail and

institutional markets

Distribution Distribution Product

channels partners set

Global Institutional Global Distributors Separate Accounts

US Retail Global Consultants US Mutual Funds

Non-US Retail US Wirehouses UCITS/QIAIFs*

Independent Financial ETFs

and Registered

Investment Advisors SMA/UMA

Private Banks CIT

*Certain vehicles have not been registered with the US Securities and Exchange Commission under the US Securities Act of 1933

and may not be directly or indirectly offered or sold in the US or to any US person.

24Principal Global Investors

Gain from highly focused investment teams

Striving to deliver consistent, risk-controlled results,

flexible investment strategies, and customized solutions –

all through a single, globally integrated investment advisor.

Comprises Leverages Cultivates Integrates

experienced the expertise of a small-company global business

managers, each more than 560 mindset in a large- to provide

offering distinct global investment company clients access to

investment professionals, with environment comprehensive

specialties and a focus on investment

philosophies customized strategies and

solutions solutions

25Principal Global Investors

In-demand, specialist capabilities

Finisterre

Claritas3 Capital LLP

Principal

$1.4 $2.1 Principal Unique hybrid business model

Portfolio Global Fixed

Strategies1 Income2

$124.8

Distinct investment processes

Principal

Real Estate - Post Advisory

Private Group

$53.1 $16.4 Leverage distribution

Principal – Global institutional

Spectrum

Aligned

Investors Global Asset

– Global funds

Management

$26.1

Investors $20.8

Principal $423.1 B Principal

Integrated business processes

Global

Equities

Real Estate -

CMBS $8.6 – Drive scale

$88.9

– Share best practices

Principal Real Edge Asset

Estate - REITS Management

$17.7 Columbus $16.9

Circle Origin Asset Asset Allocation/Multi-Strategy

Investors Management Fixed Income

$4.1 $3.3

Equity

Alternatives

AUM in billions, as of 03/31/2019. 1 Principal Portfolio Strategies allocates investment dollars across PGI boutiques and third-

party managers. 2 Effective 10/1/2018, the Morley Financial Services joined the Principal Global Fixed Income team to align

capabilities and resources. As a result, approximately $17 billion of AUM moved from the Morley Financial Services boutique to

26 the Principal Global Fixed Income boutique. 3 Effective 1/1/2019, Claritas, an investment management company in Brazil, moved

from Principal International to Principal Global Investors.Principal Global Investors

Comprehensive capabilities of

autonomous asset managers

As of 31 March 2019.

Principal Global Investors is a diversified global asset management organization, with a range of investment capabilities provided by

the investment boutiques within the Principal Global Investors group of companies, by its internal boutiques, affiliated companies

27

and ventured partners.Principal Global Investors

Investment performance

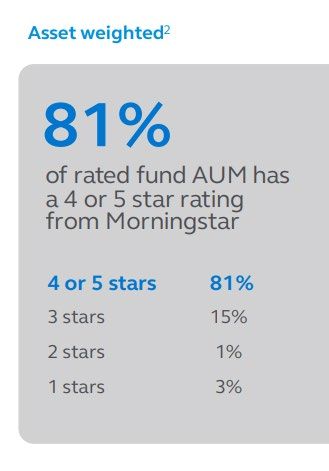

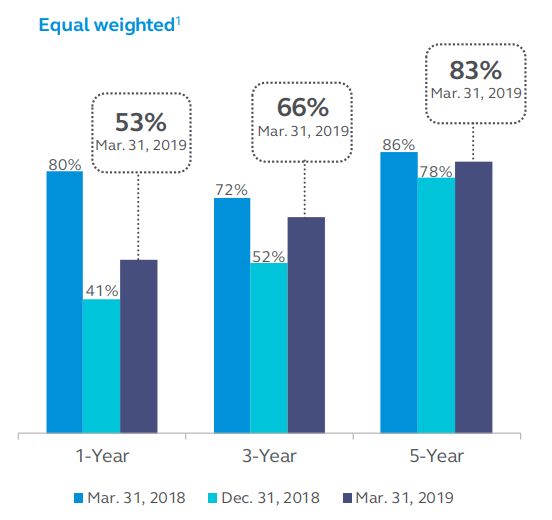

1 Percentage of Principal actively managed mutual funds, exchange traded funds (ETFs), insurance separate accounts,

and collective investment trusts (CITs) in the top two Morningstar quartiles. Excludes Money Market, Stable Value,

Liability Driven Investment (Short, Intermediate and Extended Duration), Hedge Fund Separate Account, & US Property

28 Separate Account. 2 Includes only funds with ratings assigned by Morningstar; non-rated funds excluded (78 total funds

with I-shares, 74 are ranked)Principal Global Investors

Well-positioned for industry trends

• Industry leader in delivering

solutions, including multi-

asset solutions

• Strong and growing suite of Generate

alternatives Income

• Early entrant in the Active

ETF space Client

• Hybrid, Passive and Indexed Needs

offerings on retirement Manage

Grow

platform of the Principal Risk

Assets

Financial Group

• With investment teams that

span asset classes, sector

rotation presents

opportunities

29Principal International

Principal International overview

Mission: Helping 20 million middle class customers in our chosen emerging markets plan and

invest for their financial security through our retirement and long-term savings franchise.

China (2005)

Principal Financial • 11.3M customers Hong Kong (1996)

• AUM of $158.4B

Group • 0.6M customers

• Asset Management, • AUM of $10.2B

Mutual Funds

India (2000) • Mandatory Pensions, Mutual

Mexico (1993) • 0.6M customers Funds, Asset Management

• 3.0M customers • AUM of $1.1B

Thailand (2010)

• AUM of $13.6B • Mutual Funds, Asset

Management, Advisory • 40K customers

• Mandatory Pensions,

Mutual Funds, Asset Services • AUM of $4.2B

Management • Voluntary Pensions, Mutual

Funds, Asset Management

Malaysia (2003)1

Chile (1995) Brazil (1999) • 0.7M customers Indonesia (2007)

• 1.7M customers • 2.4M customers • AUM of $15.8B • 15K customers

• AUM of $46.8B • AUM of $69.1B • Conventional & Islamic • AUM of $0.5B

• Mandatory Pensions, Voluntary • Voluntary Pensions, Asset Management, Mutual • Asset Management, Mutual Funds

Pensions , Mutual Funds, Asset Mutual Funds, Asset Funds, Voluntary Pensions

Management, Annuities Management, Annuities

Singapore (2006)

• Asset Management

(Year) = Principal entered

Covered lives as of March 2019

PI Sourced AUM as of March 2019

30 1 Includes SingaporePrincipal International

Strong growth

Increasing diversification1, 2 Pre-tax operating earnings growth2

(USD millions)

$400

$350

26% $300

$250

2018 $200

Pre-tax OE

$150

$100

74%

$50

$0

2013 2018

Latin America Asia

1 In 2013, Asia and Latin America contributed 5% and 95%, respectively. 2 Pre-tax operating earnings are adjusted for the

impact of the actuarial assumption review in 2018 (-$54 million) and lower than expected encaje (-$32 million). 2013 is

31 adjusted to reflect 2018 exchange rates (-$105 million).Principal International

Sustained global asset growth

AUM growth

Global AUM by region

+5% from 2016-2025e

$80.0 (USD trillions)

$70.0 • Globally: 6%

$60.0 • Non-PI markets: 5%

$50.0 • PI markets: 10%

+6%

$40.0 +11%

$30.0

$20.0

+9%

$10.0 +10%

$0.0

North America Europe Asia-Pacific Middle East + Latin America

Africa

2016 2025e

Principal International (PI) markets

Source: “Asset & Wealth Management Revolution: Embracing Exponential Change,” PwC, 2017. Growth calculations are weighted.

32Principal International

Continued GDP growth

1990 $T 2010 $T 2030E $T 2050E $T

1 U.S. 5.9 U.S. 15.0 China 36.1 China 61.0

2 Japan 3.1 China 5.9 U.S. 25.5 India 42.2

3 Germany 1.7 Japan 5.5 India 17.1 U.S. 41.4

4 France 1.2 Germany 3.3 Japan 6.0 Indonesia 12.2

5 Italy 1.1 France 2.5 Indonesia 5.5 Brazil 9.2

6 UK 1.0 UK 2.3 Brazil 5.0 Mexico 8.0

7 Canada 0.6 Italy 2.0 Russia 4.9 Japan 7.9

8 Spain 0.5 Brazil 2.1 Germany 4.6 Russia 7.6

9 Brazil 0.5 Canada 1.6 Mexico 4.0 Nigeria 7.3

10 China 0.4 Russia 1.5 UK 3.6 Germany 6.3

Current Principal international locations: Asia Latin America

Source: IMF (historical data), PwC (projections), 2015

33Principal International

Strong partnerships

JV partnerships are foundational to our strategy in emerging markets

We leverage our partners strong local presence, brand, and distribution to better serve

middle class customers

Brasilprev CCBPAM CIMB-Principal

Partner Banco do Brasil China Construction Bank CIMB Group

Malaysia, Thailand,

Market(s) Brazil China

Indonesia, Singapore

Mutual funds, asset Pension, mutual funds,

Products Pension

management asset management

Partner’s

66M retail customers1 360M retail customers 2 14M retail customers 3

distribution

4,770 branches1 14,920 branches 2 796 branches3

reach

JV customers 4 2.4M customers 11.3M customers 0.7M customers

1 Banco do Brasil 2017 Annual Report. 2 CCB 2017 Annual Report. 3 CIMB Group 2018 Annual Report. 4 As of March 2019;

34 customer counts based on the number of products they have.Principal International

Strong market presence

Latin America Asia

•

Latin

Chile: #1 provider of

Asia • China: #3 largest retail fund provider1

America

voluntary pension1

• Hong Kong: #6 largest MPF provider1

• Brazil: #1 in total market share2

• SE Asia: #2 in unit trust market (Malaysia) 2

• Mexico: #5 largest mandatory

pension provider1

1 As of December 2018 2 February 2019

35Principal International

AUM evolution fueled by organic growth

42 consecutive quarters of positive net cash flow1

(in billions) PI reported

AUM as of 3Q 2008 $ 29

Net cash flow 75

Investment performance 73

Other (4)

Operations acquired 48

Effect of exchange rates (60)

AUM as of 1Q 2019 $ 161

1 As of March 2019

36U.S. Insurance Solutions

U.S. Insurance Individuals

Solutions • Individual life insurance

• Individual disability insurance

Our mission

Small to medium sized

SMBsbusinesses (SMBs)

Help businesses and individuals by SMBs

offering solutions that grow and • Business Owner & Executive Solutions (BOES)

protect their assets, and enable • Nonqualified Deferred Compensation (NQ)

them to live their best lives.

• Group employer paid and voluntary products

Current customer base:

• 104,000 employers

• Multi-life/employer based disability insurance,

• 4.5 million individuals including business owner solutions

Institutions

• Group employer paid and voluntary products

67% of total PFG employer

relationships are held in USIS

37

37U.S. Insurance Solutions

Market opportunity with small- to medium-sized businesses

33% don’t offer

group insurance2

67% don’t have

59million

6 million an NQ plan 2

SMB employees

employers1 58% don’t have

disability coverage 2

(48% of working

population) 3

43% don’t have

a buy/sell plan 2

1What’s New with Small Business, SBA Office of Advocacy, August 2018

22019 Principal Business Owner survey conducted January 7-25, 2019. 1,020 employed U.S. business owners (of at least 5% of

business), actively making decisions, 2-499 employees

38 3SBA Office of Advocacy, Small Business Profile, SBA, 2018U.S. Insurance Solutions

Market position

Group1 Individual1 Individual

Benefits Disability Life

#3 Total in-force #3 New sales #1 Nonqualified

contracts premium plans2

Total new life

#5 In-force premium #18

sales premium3

#2 Life

#4 Disability Life

#5 Dental

Sources: 1LIMRA, 2017 & 2018 for IDI sales premium; 2Based on total number of Section 409A plans, PLANSPONSOR 2018 Recordkeeping Survey, June 2018;

3LIMRA U.S. Retail + Small Case COLI/BOLI Individual Life Insurance Sales Participant Report, Full-Year 2017

39U.S. Insurance Solutions: Specialty Benefits Insurance

Above industry premium growth and a balanced portfolio

3 Year In-Force Premium Growth 1Q19 TTM Total Premium & Fees

Group

(2014 – 2017 CAGR) Benefits

81%

Specialty

Benefits

Group

7.1% 7.5% Benefits

83%

Individual

Disability

2.1%* 1.8%* 17%

Group Benefits Individual DI Group

Disability

Principal Industry Group 28%

Life 24%

• Stable loss ratios

• Attractive margins Group Dental &

vision 48%

Benefits

40 Source: * Industry figures based on 2014-2017 CAGR, LIMRA 2014-2017U.S. Insurance Solutions

SMB focus

Group Benefits in-force cases New sales premium and fees

Individual

100 to 1,000 1,000 or more 37%

employees employees Individual

5%U.S. Insurance Solutions: Specialty Benefits Insurance

Diversification in Group Benefits

Number of employer Employer paid Employer Dental & Disability

customers plus voluntary paid only vision insurance

72,000

54% 32% 48% 28%

Average case size New sales In-force

37 premium premium

Case retention1

87% Voluntary

only

14%

Life

24%

34% of all new cases sold

include “first-time” benefits

As of 12/31/18

1 Average retention for the period 1/1/2016 – 12/31/2018

42U.S. Insurance Solutions

Focus on the business market

Solutions for businesses,

business owners and key

executives Individual 37%

Business owners’ financial

challenges

• Exiting the business

BOES 31%

• Business transition

• Retaining key employees

• Retirement planning

Solutions for key employees

• Retirement income ER/NQ 32%

• Survivor income

• Business protection

1Q19 TTM Sales

BOES = Business Owner/Executive Solutions

ER/NQ = Employer/Non-qualified

43Distribution

U.S. distribution overview

AFFILIATED THIRD PARTY

PRINCIPAL INVESTMENT- INSURANCE- BANKS

ADVISOR ORIENTED ORIENTED

• Brokerage

NETWORK • Wirehouses General Agents • Banks

• Independent • Broker/

• Regional

Marketing

• 1,200 advisors Broker/Dealers Dealers

Organizations

• Planners • Marketers

• Sell all products • Financial

Advisors/Broker/

• Financial Dealers

Planning

Focused Global Firm Relations

Select 3rd party distributors with dedicated support

STRENGTHENS RELATIONSHIPS AND FUELS SALES GROWTH

WHOLESALE CHANNELS

Investment Retail Disability Group

Retirement Solutions Annuities ESOP NQDC Life Insurance Benefits

All supported by DEDICATED SERVICE TEAMS providing education, training, counseling and retention

44Distribution

Broad and deep distribution

Proprietary provides foundation; 3rd party provides accelerated growth

Product Line New Top 3

1st 2nd 3rd

Sales Represent

NQ Life 42%

Principal

Retail Life Adv isor

Netw ork

62%

Individual Principal

Plus Group Adv isor 33%

Disability Netw ork

Digital

Group Benefits Insurance,

Inc

10%

Principal

Fixed Annuities Adv isor

Netw ork

58%

Variable Annuities Principal

Adv isor

Infinex

Investments, Inc US Bankcorp 98%

Netw ork

Principal

Mutual Funds Adv isor

Netw ork

28%

FSA – New Sales

23%

Assets

FSA – New Sales Principal

30%

Case Counts Adv isor

Netw ork

Rankings and percentages as of 12/31/2018

45Investments

Investment philosophy & strategy

Diversified investment portfolio

Total invested assets & cash

Our strategy hasn’t changed:

Commercial

CMBS

Mortgages High quality, well-diversified portfolio

16%

5% MBS

7%

Liability-driven investment approach

ABS

Corporate 7%

Private Bonds

$90.8B Active asset/liability management

16%

Total invested Government,

Agency, State

assets & cash & Political

Optimized risk adjusted yields and returns

10%

Corporate Other1 Global collaboration and best practices

Public Bonds 12%

25% Cash

2% Portfolio responsibility remains at local country

Total PFG as of 03/31/2019

GAAP carrying value

1 Other includes Equity Securities, Residential Mortgages, Real Estate, Policy Loans, Investment in Equity

46 Method subs, Direct Finance Leases and Other InvestmentsFinancials

Balanced approach to capital deployment

Targeted long-term capital deployment strategy

Capital deployed as a percent of net income

• Capital is deployed to:

Organic - Grow the company

growth Common stock

dividends - Return to shareholders

30-35%

40%

• Every capital deployment

opportunity is evaluated

against a minimum return

of our cost of capital

M&A and share

repurchases

25-30%

47Financials

Balanced capital deployment strategy

Grow capital Return capital Optimize

• Organic growth • Common

capital structure

• Mergers and stock dividends • Financial flexibility

acquisitions (M&A) • Share repurchases

Expect to deploy 65–70% of our net income over the

long-term, with fluctuations in any given year

48Financials

Driving ROE

growth Earnings

+ 4-5% for market

performance

+ 4-5% for growth from

sales/NCF

30-60 bps average + 1-2% operational efficiency

annual ROE ROE =

improvement

Equity

• Organic growth

• Dividend growth

• Opportunistic

share repurchases

49Financials

Acquisition of Wells Fargo Institutional

Retirement & Trust business

• Principal will acquire Wells Fargo’s defined contribution, defined benefit, executive deferred compensation

(non-qualified plans), institutional trust and custody, and institutional asset advisory businesses; expected to

close third quarter 2019

• Brings together two very successful businesses with deep expertise in helping customers achieve their

retirement savings and investment goals

Strategic benefits Transaction details Financial impact4

• Doubles the size of our $1.2B upfront consideration2, When fully integrated in 2022:

retirement business1 funded through: • Annual net revenue of

• Expands scale and • $400-500M in new debt approximately $425M

capabilities in core U.S. • Remainder in cash • Pre-tax return on net

retirement businesses revenue of 28-32%

Earnout of up to $150M3

• Solidifies our footprint in Expected to be accretive to

the SMB market Suspending share buybacks;

net income and non-GAAP

expect to resume no later than operating diluted EPS in 2020

1Q 2020

1 Pro-Forma calculations based upon AUA and participant data as of December 31, 2017 provided by PLANSPONSOR 2018

Recordkeeping Survey and inclusive of shock lapse and new sales assumptions; 2 Net purchase price of $1.05B, reflecting approximately

$150M cash tax benefit from asset acquisition; 3 Earnout payable 2 years post-closing if existing client fee revenue retention exceeds

expectations; 4 Reflects assumed revenue and expense net synergies, excludes transaction and integration costs and earnout liability

accounting.

50Financials

Strengthening our position in the

U.S. retirement market

Becoming the #3 Defined Contribution recordkeeper by participants

18,000 Alight

Conduent

1,600

2,400 BAML

1,400

Schwab

1,200 Wells Fargo

Participants per Plan

Milliman

1,000

Prudential

800

600

T. Rowe Price

Vanguard Principal Fidelity

400

going

John Hancock

Transamerica

TIAA

forward Empower

200 Nationwide Principal

VALIC

MassMutual Voya

0

0 1,000,000 2,000,000 3,000,000 4,000,000 5,000,000 6,000,000 7,000,000 8,000,000 21,000,000

9,000,000

Participants

Source: PLANSPONSOR 2018 Recordkeeping survey. AUA and plan data as of December 31, 2017. Note: Bubble size represents plan assets ($mm).

Principal going forward shown on a pro forma basis – reflects assumed shock lapse and new sales assumptions

51Financials

Increasing our global footprint through M&A

Year

Opportunity Announced Rationale

Enhance our digital capabilities for advisors and

RobustWealth 2018

customers

Increased ownership in our successful joint venture

CIMB-PAM 2018

to 60%

INTERNOS Expand our real estate investment capabilities

2017

in Europe

Strengthen position in Mexico Afore market by

2017

becoming the 5th largest provider

15 year exclusive distribution with 4,440 agents

AXA Hong Kong Pension 2014

Gateway into China

Complete offering in Chile with marquee pension

2012

and savings franchise

Entry into Brazil mutual fund and asset

2012

management market

2011 Enhance global equity investment capabilities

Establish leadership in emerging

2011

52 markets fixed income investingFinancials

Capital deployment

$ in millions

$94 $140

$180

$40

$355

$441 40% of 90% of $599

89% of 65% of

Net Income Net Income Net Income1 Net Income

$465

$193 $540

$257

$650

$275

2015 2016 2017 2018

Deployed $1.1 billion Deployed $856 million Deployed $913 million Deployed $1.4 billion

Common Stock Dividends

Share Repurchases

Strategic Acquisition

Debt reduction

Long term: expect to deploy 65–70 percent of our net income with fluctuations

in any given year

1 2017 net income included benefits from a large real estate transaction and the U.S. Tax Cuts and Jobs Act

53Financials

Capital deployment

$130M $150M

Share repurchases Common stock dividends paid

• $130M - 1Q19 • $150M - 1Q19 ($0.54 per share)

$280M

total capital

deployed

1Q 2019

• Expect to deploy above our guided range of $1.0B to $1.4B of capital in 2019

• Includes $1.2B for the planned acquisition of the Wells Fargo Institutional Retirement and Trust

business that is expected to close in 3Q19, as announced in April

• Announced 2Q19 common stock dividend of $0.54 per share, or $2.15 for 2Q19 TTM;

an 8% increase compared to 2Q18 TTM

• Suspended our share buyback program and plan to resume no later than 1Q20

54Financials

What if things don’t go as expected?

Changes in key macroeconomic conditions have an impact on

Principal’s annual non-GAAP pre-tax operating earnings

If macroeconomics Equity market Interest rates FX: US dollar

change by… return +/- 10% +/- 100 bps changes +/- 2%

Then Principal’s

annual non-GAAP

pre-tax operating +/- 4-6%1 +/- < 1%2 -/+ < 1%3

earnings will change

by…

RIS – Fee RIS – Spread PI

And the primary

businesses PGI Individual Life

impacted are…

SBD

1 Assumes an immediate 10% change in the S&P 500 followed by 2% growth per quarter thereafter. 2 Excludes

the impact of actuarial unlockings. 3 Principal is primarily impacted by changes in Latin American and Asian

currencies. Inverse relationship between movement of the US dollar and impact to Operating Earnings.

Note: The impact to net income attributable to Principal Financial Group, Inc. is materially consistent with the

55 impact to pre-tax operating earnings.Financials

Key business drivers outlook

2019 Long-term 2019 Long-term

Retirement and Income Solutions Principal Global Investors

outlook outlook outlook outlook

Net revenue growth Operating revenues less pass-

(2)-2% 1-5%

CAGR through commissions growth 1-5% 4-7%

RIS-Fee CAGR

Pre-tax return on net

26-30% 28-32%

revenue Pre-tax return on operating

Net revenue growth

revenues less pass-through 34-38% 34-38%

5-10% 5-10% commissions

CAGR

RIS-Spread

Pre-tax return on net

65-70% 65-70%

revenue

2019 Long-term

U.S. Insurance Solutions

outlook outlook

Premium & fees

7-9% 7-9%

growth CAGR

2019 Long-term

Principal International Specialty Pre-tax return on

outlook outlook 12-14% 11-14%

Benefits premium & fees

Combined net revenue growth CAGR 5-9% 11-14% Loss ratio 60-66% 60-66%

(at PFG share, in reported USD)

Premium & fees

4-8% 4-8%

Individual growth CAGR

Combined pre-tax return on net

35-39% 38-43% Life Pre-tax return on

revenue (at PFG share, reported USD) 16-20% 17-21%

premium & fees

Estimated pre-tax operating losses for Corporate anticipated to be above the high end of $300-$320 million in 2019

Total company non-GAAP operating earnings effective tax rate of 16-20% in 2019

Net revenue = operating revenues less benefits, claims & settlement expenses less dividends to policyholders.

RONR = Return on Net Revenue.

56Financials

Non-GAAP financial measure reconciliations

Trailing

Twelve

Months,

Pre-tax Operating Earnings (Losses) 31-Mar-19

Non-GAAP pre-tax operating earnings, excluding Corporate $ 2,222.9

Corporate (286.2)

Non-GAAP pre-tax operating earnings (losses) $ 1,936.7

Pre-tax net realized capital gains (losses) (37.2)

Certain adjustments related to equity method investments and

noncontrolling interest (46.1)

Income (loss) before income taxes $ 1,853.4

57You can also read