Bellevue Investment Strategies - Review 2020 - Markus Peter, Jean-Pierre Gerber, Loreno Ferrari - Senior Product Specialists - Fund ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Bellevue Investment Strategies – Review 2020 Markus Peter, Jean-Pierre Gerber, Loreno Ferrari – Senior Product Specialists Zurich, January 14th 2021

Agenda

Economic & market environment

1

BB Global Macro

Overview

2

Absolute & relative performance, peer-comparison

Healthcare

3

Investment companies, Luxembourg Funds

Spezialized growth strategies

4

BB Entrepreneur Funds, BB African Opportunities

2

1

Economic & market environment

BB Global Macro

3Economic & market environment

COVID-19 led to a very sharp short-term downturn in economic activity

comparable to the 2008 financial crisis…

Sharp decline in the

ISM Manufacturing

Index in Q2 2020

Subsequent rapid

recovery

Source: Bellevue Asset Management, Bloomberg 4Economic & market environment

…the US Federal Reserve responds with an extremely expansive monetary policy

and increases the Fed balance by USD 3,400 billion

USD 3,000 billion

expansion to counter

COVID-19 recession,

USD 3,400 billion

+USD 3,400b since end of QT

Tapering

Stimulus programs

provide additional

QE3

support to the

Operation twist QT economy

QE2

QE1 +USD 3,400b

TARP

Source: Bellevue Asset Management, Bloomberg 5Economic & market environment

Healthcare in the perception of many investors as a winner alongside tech

…but this was no longer the case after the sector rotation in the second half of the year

Total return of the GICS-sectors in USD – Year 2020 Tech leading the way – Energy lagging behind

Information Technology

In H1, cyclical sectors (Energy, Financials, Industrials)

significantly underperformed the overall market, while

Consumer Discretionary defensive sectors significantly outperformed the

overall market

Communication Svcs

The IT sector showed the strongest performance in

Materials

H1, mainly driven by the "stay at home" and "home

MSCI World office" requirements imposed by the lockdowns

Healthcare The 2nd half of the year was characterized by

extremely expansive monetary policies of the major

Industrials central banks, economic stimulus programs of

important industrialized nations and positive trial

Consumer Staples

results of vaccine developers (Pfizer/Biontech,

Utilities Moderna)

Financials Cyclical sectors (Consumer Discretionary, Materials

and Industrials) show strong performance in H2

Real Estate

Energy

-40% -30% -20% -10% 0% 10% 20% 30% 40% 50%

2020 H2 2020 H1 2020

Source: Bellevue Asset Management, data in USD as of December 31, 2020 6Economic & market environment

BB Global Macro ends the year with a positive annual return in a

volatile market environment

The drawdown in March was followed by a strong recovery in performance

The magnitude of the drawdown was primarily due to short-term portfolio management decisions rather than our long-term view

that a portfolio consisting of 75% government bonds and 25% equities is a very solid, neutral portfolio

At year-end, the portfolio held 30% equity exposure, 25% in non-government bonds, and 17% in long-term government bonds

In % Jan Feb Mar Apr May Jun Jul Aug Sep Okt Nov Dez YTD

2010 +0.2 +0.2 +0.4 -0.7 +1.2 +0.3 +0.3 +0.5 +1.6 +4.1

2011 0.1 +0.8 -1.0 +1.5 +0.3 -0.9 +0.8 -6.0 -0.6 +2.3 -1.0 +1.4 -2.5

2012 +0.8 +0.6 -0.7 0.0 -4.1 +2.4 -0.6 +1.1 +0.6 +1.0 +0.8 +1.4 +3.2

2013 +0.5 -0.3 -0.8 +3.4 -0.8 -2.8 +2.8 +0.7 +2.7 +2.3 +0.4 -1.4 +6.9

2014 +2.6 +1.2 -0.2 +0.1 +1.6 +0.3 0.0 +0.9 -0.3 +0.7 +1.5 -0.6 +8.0

2015 +4.2 +0.8 +2.9 -0.5 +0.4 -2.2 +1.7 -1.1 +0.2 +1.4 -0.3 -1.2 +6.2

2016 -0.2 0.0 +2.2 +0.5 +0.3 +0.2 +1.7 +0.5 0.0 0.0 -2.3 +1.4 +4.2

2017 -0.4 +1.3 +0.5 +0.9 +0.2 -0.2 +0.3 +0.3 +0.5 +1.1 -0.4 -0.6 +3.5

2018 -0.8 -0.6 +0.1 +0.1 -0.4 -0.1 +0.8 -0.9 +0.5 -1.2 +0.4 0.0 -2.2

2019 +2.6 +0.7 +1.1 +1.1 -1.2 +1.1 +0.3 -1.1 +1.1 +0.1 +1.4 +0.1 +7.4

2020 -0.7 -2.4 -9.3 +5.9 +2.8 +1.6 -1.3 +1.8 -1.2 -1.2 +6.2 +1.2 +2.7

Note: Performance of the I-EUR share class

The subfund is denominated in a currency that may differ than an investor’s base currency, changes in the rate of exchange may have an adverse effect on prices and incomes.

Performance is shown net of fees and expenses for the relevant share class over the reference period. All performance figures reflect the reinvestment of dividends and do not take

into account the commissions and costs incurred on the issue and redemption of shares, if any. The reference benchmark of this class is used for performance comparison purposes

only (dividend reinvested). No benchmark is directly identical to a subfund, thus the performance of a benchmark is not a reliable indicator of future performance of the subfund it is

compared to. There can be no assurance that a return will be achieved or that a substantial loss of capital will not be incurred.

. Note II: Pro forma performance of the unregulated fund from September 2008 to March 2010; after administration, management and performance fees 72

Overview

Absolute & relative performance, peer-comparison

8Overview

Solid investment performance

Excellent competitiveness, client benefit, stability

72% of AuM in 1st or 2nd quartile YTD 2020

Very competitive

82% of AuM in 1st and 2nd quartile over 3 years

performance of invest-

93% of AuM in 1st and 2nd quartile since inception

ment strategies

80% of AuM in 1st quartile since inception

79% of AuM beat benchmark YTD 2020

Value generation for

investors (“alpha”) * α 75% of AuM beat benchmark over 3 years

84% of AuM beat benchmark since inception

16 of 19 lead portfolio managers in charge since date of launch

High continuity and

No portfolio manager changes in 2020

stability in portfolio

Very low fluctuation rates for >10 years

management

Steady recruitment of new investment professionals and young talents

* Outperformance after expenses, based on institutional share classes

Source: Bellevue Group, as at December 31, 2020 93.1

Healthcare

Investment companies

10Healthcare

BB Biotech AG

Investing in leading science

Currency Share NAV NBI

Strong NAV Outperformance CHF +19.3% +24.3% +15.1%

USD +30.4% +35.9% +25.7%

With Prof. Dr. Mads Krogsgaard Thomsen, CSO of Novo Nordisk and Dr. Susan

Two new, renowned members,

Galbraith, Head of Oncology of AstraZeneca, BB Biotech was able to attract two

joined the Board of Directors renowned new Board Members

Due to the COVID-19 pandemic, M&A activity was severely impacted in H1 2020

Further acquisitions in the portfolio

In the second half of 2020, with Myokardia (Bristol-Myers Skibb) and Alexion

of BB Biotech AG (AstraZeneca) two important portfolio positions have been taken over

USD 47 bn market cap (an investment since Q1 2018)

Pioneering mRNA based medicines – a broad clinical pipeline

COVID-19 prophylactic vaccine candidate within only 42 days from sequence

Moderna receives FDA emergency selection

use authorisation for COVID-19

Initial dosing of healthy volunteers started in mid March 2020

vaccine

Phase III with 30’000 patients – primary efficacy analysis shows vaccine was 94.1%

effective!

FDA - Emergency use authorisation as of December 18, 2020

Source: Bellevue Asset Management, as of December 31, 2020 11Healthcare

BB Biotech AG

Portfolio breakdown

Main focus on US small & mid-cap companies that address unmet medical needs, especially in oncology and

infectious diseases

1 Strong focus remains on high 2 Strong focus on new 3 Mid-cap companies offer ideal

unmet needs technologies risk/reward profiles

0.2%

2.9%

4.9% 7.2% 5.9% 6.5%

7.7%

8.2%

38.2%

8.2%

46.6%

16.2% 30.6%

14.0%

53.9%

21.6%

26.6%

Small Molecule RNA

Orphan Diseases Oncology

> 30 bn 5 bn - 30 bn

Neurological Diseases Others Antibody Gene- and cell therapy 1 bn - 5 bn 500 mn - 1 bn

Cardiovascular Diseases Metabolic Diseases < 500 mn

Infectious Diseases Protein

Note: Portfolio breakdown as of September 30, 2020, in % of securities 12Healthcare

BB Healthcare Trust

Investing in the rapidly evolving healthcare paradigm

MSCI World

Currency Share NAV

Healthcare

Strong outperformance of Share

GBP +29.1% +25.7% +10.3%

and NAV

USD +32.9% +29.3% +13.5%

Re-invention of the entire healthcare system is necessary to meet the requirements

of the 21st century population in a cost-effective manner. (e.g. strong increase in

Investing in the rapidly evolving chronic diseases)

healthcare paradigm Portfolio is highly operationally geared to areas that would benefit from an inevitably

changing healthcare paradigm (e.g. digitalization)

Inclusion in the FTSE 250 The management team currently overweight's the sub-sectors biotech, life science

tools and diagnostic, the strongest underweight is in pharma

BB Healthcare Trust was included in the FTSE 250 Index as of June 19, 2020

CareDx, provides products, drugs, testing services for transplant patients. Surprised

with very strong Q3 2020 revenue numbers

CareDx, Teladoc, Pacific Biosciences Teladoc: telemedicine provider offering the perfect business model during the

und Genmark with strong pandemic. Acquisition of Livongo creates the potential to evolve into a fully

integrated “virtual-care-provider”

performance contributions

Genmark: specialises in “point-of-care” diagnostics for the diagnosis of pathogens

in respiratory, gastrointestinal and blood infections (sepsis). Develops and

distributes COVID-19 tests

Source: Bellevue Asset Management, as of December 31, 2020 13Healthcare

BB Healthcare Trust

Diversified but at the same time concentrated Healthcare Portfolio which offers a high active share

MSCI World Healthcare

Holding Subsektor % Holding Subsektor %

Bristol Myers Squibb Pharma 7.1% Johnson & Johnson Pharma 6.2%

Hill-Rom Holding Medtech 6.0% UnitedHealth Dienstleistungen 5.0%

Vertex Biotech 6.0% Roche Pharma 3.7%

Anthem Dienstleistungen 5.9% Novartis Pharma 3.2%

Jazz Speicialty Pharma 5.4% Pfizer Pharma 3.1%

Insmed Biotech 5.1% Merck & Co Pharma 3.0%

GW Pharmaceuticals Speicialty Pharma 5.0% Abbott Lab. Medtech 2.9%

Alnylam Biotech 4.7% Thermo Fisher Scient. Life Sciences Tools 2.8%

Humana Dienstleistungen 4.1% AbbVie Pharma 2.8%

Amgen Biotech 3.7% Medtronic Medtech 2.4%

Source: Bellevue Asset Management, as of December 31, 2020 143.2

Healthcare

Luxembourg Funds

15Healthcare

Bellevue Healthcare Strategies with strong performance in a challenging

environment

Peformance BB Healthcare strategies in % (USD)

December 31, 2019 – December 31, 2020

MSCI World Healthcare TR (USD):+13.5% +68.4%

+50.7%

+45.0%

+29.2%

+27.9%

+23.9%

+16.6%

Source: Bloomberg, Bellevue Asset Management, data as of December 31, 2020

Note: Performance of the I-USD share classes. Past performance is not a reliable indicator of future results and can be misleading 16Healthcare

US elective procedures have been negatively impacted by the Corona

pandemic but have recovered from April lows

Weekly YoY-growth of elective procedures in the US

Jan Feb Mar Apr Mai Jun Jul Aug Sep Oct Nov

40%

19%

13%

20%

0% 0% 0% 0%

0%

-1% -1% -1%

-3%

-6% -7% -7% -5% -5% -7% -6%

Year over year %

-6% -6%

-8%

-10%-9%-11%-10%-9%

-12%

-14%-14% -15% -20%

-16% -17%

-18%

-23% -24%

-27% -28%

-34% -40%

-43%

-46%

-60%

-60%

-77% -80%

-81%

-84%

-86%

-88%-87%

-100%

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45 46

week

Past performance is not a reliable indicator of future results and can be misleading

Source: IQVIA, Bellevue Asset Management, as of November 30, 2020 17Healthcare

BB Adamant Medtech & Services

Performance – Stability – Diversification

MSCI World HC MSCI World

Fund outperforms broader Fund

Equip. & Supplies Healthcare

healthcare markets despite a

+16.6% +23.9% +13.5%

challenging environment

Demand is basically non-cyclical: health problems must be solved (e.g. heart

COVID-19 affects the fundamental issues, broken bones, glucose measurement and insulin injections)

factors of Medtech & Services only

Certain elective procedures are deferred (e.g. hip and knee implants) as hospital

in the short-term capacity has been used for COVID-19 patients, and will result in pent-up demand

We expect a complete normalization of elective medical procedures

Normalization of investor focus: Fundamental data such as acceleration of

Positive outlook for 2021 organic sales growth, new products & services and clinical data are back in the

spotlight

Further innovations about to be Further innovations will be introduced in 2021 and we expect many new products

introduced and services to fuel sales growth, such as Dexcom G7, the Hugo robotic surgery

system and MitraClip

Managed Care will benefit from the elimination of the Health Insurance Fee (HIF)

Source: Bellevue Asset Management, data as of December 31, 2020

Note: Performance of the I-USD share class 18Healthcare

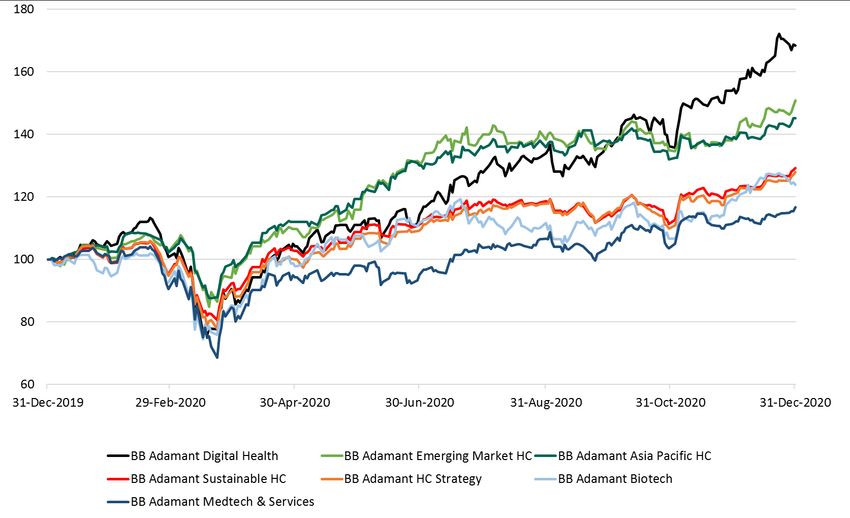

BB Adamant Digital Health

Making the healthcare system more efficient with digital health

Fund Nasdaq 100

Stellar performance, even strongly

outperforming Nasdaq 100 +68.4% +48.9%

Digitization in healthcare is urgently needed and inevitable

The coronavirus crisis has neutralized the natural reflex among the relevant

COVID-19 crisis has accelerated stakeholders – patients, doctors, hospital administrators and payers – to reject such

the Digital Health Investment Case change…

…and even prompted some of them to actively support and invest in digital tools

and solutions

Telemedicine specialists and many other companies have made as much progress

in 2020 as they would have normally made in three or four years

Digital Health Investment Case

The growing acceptance of digital solutions in the wake of the pandemic has pushed

becomes more predictable and even up the potential growth trajectory of the Digital Health Investment Case

more attractive

The strong growth momentum and non-cyclical demand suggest 2021 will be

another pleasing year for Digital Health stocks

Source: Bellevue Asset Management, data as of December 31, 2020

Note: Performance of the I-USD share class 19Healthcare

BB Adamant Digital Health

The fund has participated in 11 Initial Public Offerings (IPOs) in the course of 2020

Portfolio entries through IPOs M&A and transactions

Placed Current Per- Date Ann- Per-

Company Date Issue price (mn) price formance Company ouncement Transaction formance

01/30/2020 $14.00 $282 $43.65 212% Sale of

*89%

07/17/2020 Passport to

**77%

06/12/2020 $16.50 $256 $23.10 40% Molina

06/19/2020 $16.00 $256 $14.00 -13%

$18.5bn

*9%

07/14/2020 $21.00 $914 $13.66 -35% 08/05/2020 takeover by

**458%

Teladoc

07/01/2020 $22.00 $254 $43.50 98%

07/16/2020 $22.00 $205 $89.41 306% $3.3bn

*9%

12/21/2020 takeover by

**24%

Gainwell

09/14/2020 $27.00 $278 $56.84 111%

09/17/2020 $18.00 $853 $25.33 41% *Since announcement to year-end or date of transaction respectively

**Performance full-year 2020

10/15/2020 $18.00 $163 $44.82 149%

12/03/2020 $19.00 $201 $56.14 195%

12/08/2020 HK$70.58 HK$30,997 HK$150.00 113%

Source: Bellevue Asset Management, as per December 31, 2020

Past performance is not a reliable indicator of future results and can be misleading. The performance of a benchmark shall not be indicative of past or future

performance of any Sub- Fund. Holdings and allocations are subject to change. Any reference to a specific company or security does not constitute a

recommendation to buy, sell, hold or directly invest in the company or securities. 20Healthcare

Our global healthcare strategies both outperformed in 2020

BB Adamant Healthcare Strategy & BB Adamant Sustainable Healthcare

Correction Rebound Full year

31.12.2019 – 23.03.2020 23.03.2020 – 31.12.2020 31.12.2019 – 31.12.2020

Funds outperforming its benchmark and Global equity market outperforms healthcare, Strong absolute and relative return of the funds

global equities (MSCI World Index) funds with an outperformance against benchmark compared to benchmark and MSCI World Index

110% 180% 130%

120%

100% 160%

110%

90% 140%

100%

90%

80% 120%

80%

70% 100%

70%

60% 80% 60%

Dec-19 Jan-20 Feb-20 Mar-20 Jun-20 Sep-20 Dec-20 Dec-19 Mar-20 Jun-20 Sep-20 Dec-20

BB Adamant Healthcare Strategy (Lux) I-USD BB Adamant Healthcare Strategy (Lux) I-USD BB Adamant Healthcare Strategy (Lux) I-USD

BB Adamant Sustainable Healthcare (Lux) I-USD BB Adamant Sustainable Healthcare (Lux) I-USD BB Adamant Sustainable Healthcare (Lux) I-USD

MSCI World Healthcare Net MSCI World Healthcare Net MSCI World Healthcare Net

MSCI World Net MSCI World Net MSCI World Net

Source: Bellevue Asset Management, data as of December 31, 2020

Note: Performance of the I-USD share class 21Healthcare

Our global healthcare strategies outperform

40 holdings, four regions, off-benchmark, ESG integration vs. holistic ESG-approach

Fund Benchmark

Both funds clearly outperform the +27.9%

MSCI World Healthcare Index +13.5%

+29.2%

1 Underweight Pharma Diversification pays off again – clearly positive performance contributions from

different sub-sectors, e.g. biotech and life science tools & services

Healthcare in emerging markets, led by China, with compelling performance in

2 Underweight US 2020

Negative performance contributions from underweight in large & mega caps more

3 Mid cap focus than offset thanks to exposure to innovative mid caps

EBITDA-Margin Sales Growth Active Share

Characteristics support ____________ ____________ ____________

attractiveness of both portfolios

and underline our active approach

~28% ~14-17% ~80%

Source: Bellevue Asset Management, data as of December 31, 2020

Note: Performance of the I-USD share class 22Healthcare

Healthcare in Asia and Emerging Markets

Innovation and digitization generate sustainable growth

Local Equity

Fund Benchmark

Market

Very competitive performance +45.0% +32.8% +19.7%*

of both investment strategies

+50.7% +52.8% +18.3%**

*MSCI AC Daily TR Net Asia Pacific USD Index **MSCI Emerging Markets Net TR USD Index

With JD Health and Ali Health, all digital health subsidiaries of major Chinese tech

companies are now listed at the stock exchange (incl. Ping An)

"Facebook for Doctors" M3 in Japan with first-ever drug co-development, focus on

Digitization in Asia is progressing clinical development (IP and revenue share) and use of proprietary digital marketing

after launch

Indian hospital chain Apollo Hospitals successfully established its own

telemedicine app

Private healthcare sector enjoys increasing demand (lack of quality in public sector

resources)

Ongoing consolidation in Brazil Hapvida and Notre Dame have gained policyholders despite recession

Both companies have also taken advantage of the "opportunity" of the poor

economic situation and acquired numerous private providers

Source: Bellevue Asset Management, data as of December 31, 2020

Note: Performance of the I-USD share class 23Healthcare

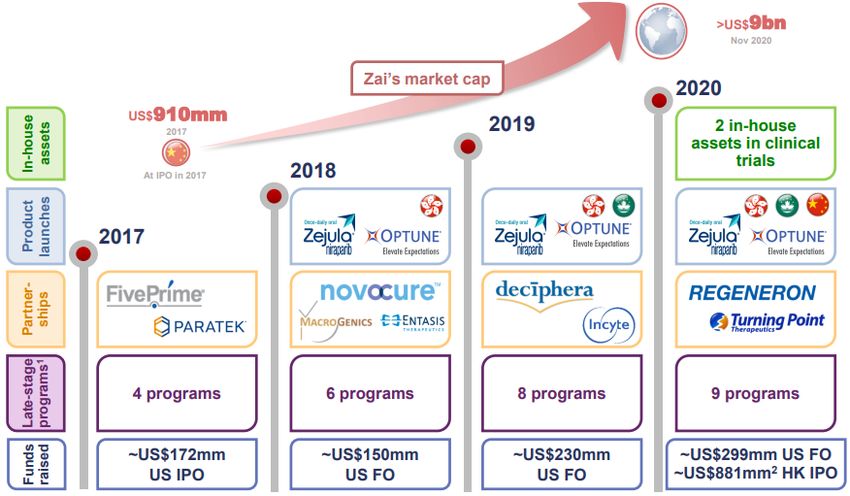

Healthcare in Asia and Emerging Markets

Innovation in China – similar situation to the late 80s/early 90s in the US

Over 50 IPOs in 2020 in the Chinese healthcare sector alone

Progress in biotech company pipelines across the board

First successful steps by Chinese biotechs abroad (e.g. Beigene)

Innovation in China

Wuxi Biologics has established itself as a leading global R&D platform in the wake

of COVID-19

Commercial success of biotech companies in China (e.g., Innovent, Zai Lab)

Source: Bellevue Asset Management, Zai Lab

Any reference to a particular company or security does not constitute a recommendation to buy, sell, hold or invest directly in the company or security 24Healthcare

BB Adamant Biotech

Focused (40–50 holdings), global and mid cap-oriented approach

Fund NBI

Strong absolute performance,

slightly behind benchmark +23.9% +26.4%

mRNA-vaccine with Pfizer

Antiviral medication

Antibody therapy Remdesivir

At peak up to about 35% portfolio (Casirivimab & Imdevimab)

exposure to COVID-19

mRNA-1273-vaccine Competitor of Diagnostics & sequencing

Moderna/BioNtec

New, promising therapeutic indications in immuno-oncology, liver diseases as well

as rare diseases

Favorable outlook for the biotech Political perception changes, added value of medicines becomes visible

sector over the next 12 - 18 months

Biotech sector with sustained, strong sales and earnings growth

Valuations, especially compared to pharma, are attractive

Source: Bellevue Asset Management, data as of December 31, 2020

Note: Performance of the I-USD share class, list of company examples is not exhaustive 254

Spezialized growth strategies

BB Entrepreneur Funds, BB African Opportunities

26Specialized growth strategies

BB Entrepreneur Funds - performance overview

Strong performance in 2020

BB Entrepreneur Funds – Switzerland BB Entrepreneur Funds – Europe

(Performance FY 2020 indexed, in CHF) (Performance FY 2020 indexed, in EUR)

130% 130%

120% 120%

110% 110%

100% 100%

90% 90%

80% 80%

70% 70%

60% 60%

BB Entrepreneur Switzerland I-CHF BB Entrepreneur Europe I-EUR

BB Entrepreneur Swiss Small & Mid I-CHF BB Entrepreneur Europe Small I-EUR

SPI Stoxx Europe 600

SPI Extra MSCI Europe Small ex UK Small

Source: Bellevue Asset Management, data as of December 31, 2020

Note: Performance of the I-CHF and I-EUR share classes 27Specialized growth strategies

BB Entrepreneur Funds (I) – „Shockwave“

Solid balance sheets – the best medicine

Performance in EUR resp. CHF Fund Benchmark

16.3% 11.7%

Strong absolute returns

1.9% -2.0%

Highly competitive vis-a-vis

benchmarks and peer groups 20.4% 8.1%

18.3% 3.8%

(available for distribution in Switzerland only)

Markets collapse by one fifth (SPI) to one third (Europe Stoxx 600 and MSCI Europe

Small ex UK) until mid of March

Advantageous Entrepreneur stocks due to their lower debt quota and less pressure

for dividend cuts

Technology and Healthcare proved supportive throughout all portfolios, particularly

both small and small&mid cap funds outperformed their benchmarks due to IT OW

Phase I – COVID-19 shockwave

31.12.19 – 18.3.2020

+21.5% -6.8% +4.2%

Stock specific events with positive contributions, e.g. Isra Vision (M&A), +23.0%

Increased focus on IT and Healthcare, reduction of cyclicals (e.g. automotive

suppliers) – purchase of CEWE, Huber+Suhner and increasing weight LEM, Logitech

Source: Bellevue Asset Management, data as of December 31, 2020

Note: Performance of I-EUR and I-CHF share classes 28Specialized growth strategies

BB Entrepreneur Funds (II) – „Rebound“

Solid balance sheets - the best medicine

Recovery thanks to global support measures – e.g. EU Recovery Fund and

stimulus package of EUR 750 bn

Partly positive surprises regarding profitability of industrials for Q2/2020, 70% of

companies reported better than expected results for Q3

Phase II – Rebound in Q2 with BB Entrepreneur Funds strongly recovered and returned between 30% to 40%

stagnation during Summer / Selective increase of «fallen angels» in cyclicals (e.g. Moeller Maersk, Swatch,

Breakout of second wave of Arbonia), further addition of IT stocks (e.g. Software-One, VAT, Atea) and other

infections positions (e.g. Husqvarna); partial profit taking in healthcare

On a special note: participation in the IPO Knaus Tabbert (camping cars), Mediaset

Espana (consolidation), Pierer Mobility (e-bikes, e-motorcycles); takeover of Sunrise by

Liberty; reduction of Partners Group following its inclusion in the SMI Index

Positive COVID-19 vaccine studies triggered market rally in Nov/Dec

US Presidential elections and BREXIT agreement supported geopolitical

stability/visibility

Rotation from quality/growth into value/cyclicals

Phase III – Announcement of

Year-end rally of BB Entrepreneur Funds between 16% and 21%

COVID-19 vaccines

Outlook 2021

Outlook 2021 Innovation, new consumer trends, technology and recovery of value stocks

Rebound in GDP growth, the unwinding of pent-up demand in consumer spending and

corporate investments and proactive fiscal policies being the pillar of recovery

Digitalisation and ESG as structural growth themes

Source: Bellevue Asset Management, data as of December 31, 2020

Note: Performance of I-EUR and I-CHF share classes 29Specialized growth strategies

BB African Opportunities

Structural growth opportunities in emerging African frontier markets

Performance in EUR Fund DJ African Titans

Underperformance due to focus on

resilience and liquidity -14.3% -6.5%

Investments only in countries with no currency risks and with functional FX

markets => Nigeria does not form part

Tactical increase in gold mining stocks (very liquid and positive momentum)

High resistance of portfolio stocks

Egypt and Morocco possess sufficient economic buffers and external funding

sources (e.g. IMF, intl. Bond markets) to address balance of payment risks

Focus on companies with high resilience to crises, strong competitive positions, well

managed balance sheets and clear strategic plans – core positions with DivY of 10%

Egypt – exhibiting by far the most attractive valuations amongst EM/FM (P/E <

8x) – notwithstanding a normalisation of economic activities

Return to economic growth and interest rate cuts may lead to a substantial re-

rating of local equity markets

Positioned for a recovery in our Economic recovery of the EU later in 2021 may prove a strong driver for Morocco,

core markets the EU being Morocco’s most important trading partner incl. tourism)

Morocco and Egypt are sufficiently industrialized so as to become key trading /

manufacturing hubs to link Africa with the rest of the World

Increase of tactical exposure in South Africa (access to global risk liquidity)

Yet no engagement in Nigeria (unorthodox monetary policy bears high risks)

Source: Bellevue Asset Management, data as of December 31, 2020

Note: Performance of I-EUR share class 30Bellevue Asset Management – Outlook for 2021

Long-term superior growth prospects – independent from COVID-19 –

Healthcare owing to structural trends, additional diversification potential in case of

dampened global GDP growth

High resilience thanks to solid balance sheets and innovations; global

Entrepreneurs

market leaders in their niches, increased focus on sustainability

«Wildcard» on emerging markets recovery, Africa with highly

Africa

attractive valuations, liquidity and resistance to crisis in the spotlight

«Weatherproof» strategy under all market conditions, attractive return

Global Macro

perspectives at limited volatility risk

Thank you for your confidence –

successful investments in 2021!

31Contact

Bellevue Asset Management AG

Seestrasse 16

CH-8700 Küsnacht

Tel. +41 44 267 67 00

Fax +41 44 267 67 01

E-mail info@bellevue.ch

www.bellevue.ch

32Disclaimer

This marketing communication relates to Bellevue Funds (Lux) (hereinafter the “Fund”), an investment company with variable capital “société à capital variable” (SICAV) under the

current version of the Law of the Grand Duchy of Luxembourg of 10 August 1915 on commercial companies (“Law of 1915”) and is authorized under Part I of the Law of 17

December 2010 relating to undertakings for collective investment (“Law of 2010”) as an undertaking for collective investment (UCITS). The Funds are a subfund of Bellevue Funds

(Lux). This marketing communication is issued by Bellevue Asset Management AG, which is an authorized asset manager subject to the supervision of the Swiss Financial Market

Supervisory Authority (FINMA) and acts as an Investment Manager of the Fund. The Prospectus, statutes, the annual and half-yearly report, the share prices and further information

about the Fund can be obtained free of charge in English and German from the management company of the Fund, Bellevue Asset Management AG, Seestrasse 16, CH-8700

Küsnacht, from the representative, paying, facilities and information agents mentioned below or online at www.bellevue.ch. The Key Investor Information documents are available

free of charge in the languages of the countries of distribution at www.fundinfo.com. This document is neither directed to, nor intended for distribution or use by, any person or entity

who is a citizen or resident of any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. It is particularly

not intended for US persons, as defined under Regulation S of the U.S. Securities Act of 1933, as amended. The information and data presented in this document are not to be

considered as an offer to buy, sell or subscribe to any securities or financial instruments. The information, opinions and estimates contained in this document reflect a judgment at

the original date of release and are subject to change without notice. This information pays no regard to the specific or future investment objectives, financial or tax situation or

particular needs of any specific recipient and in particular tax treatment depends on individual circumstances and may be subject to change. This document is not to be relied upon

in substitution for the exercise of independent judgment. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in the

light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional. The details and opinions

contained in this document are not to be considered as recommendation or investment advice. Every investment involves risk, especially with regard to fluctuations in value and

return, and investors‘ capital may be at risk. If the currency of a financial product is different from your reference currency, the return can increase or decrease as a result of currency

fluctuations. Past performance is no indicator for the current or future performance. The performance data are calculated without taking account of commissions and costs that result

from subscriptions and redemptions. Commissions and costs have a negative impact on performance. For more information about the associated costs, please refer to the related

costs and fees section of the prospectus. Any benchmarks/indices cited herein are provided for information purposes only. No benchmark/index is directly comparable to the

investment objectives, strategy or universe of the subfund. The performance of a benchmark shall not be indicative of past or future performance of the subfund. Financial

transactions should only be undertaken after having carefully studied the current valid prospectus and are only valid on the basis of the latest version of the prospectus and available

annual and half-yearly reports. Please take note of the risk factors.

Countries of distribution and local representatives

The Bellevue Funds (Lux) is registered and admitted for public distribution in AT, DE, LU, ES, UK and CH. Austria: Paying and information agent: ERSTE BANK der

oesterreichischen Sparkassen AG, Am Belvedere 1, A-1100 Vienna. Germany: Information agent: ACOLIN Europe GmbH, Reichenaustrasse 11a-c, D-78467 Konstanz. Spain:

Representative: atl Capital, Calle de Montalbán 9, ES-28014 Madrid - CNMV under the number 938. UK: The Bellevue Funds (Lux) SICAV is recognised for public offering and

distribution in the United Kingdom. Facilities agent: Financial Express Limited, 3rd Floor, Hollywood House, Church Street East, Woking, Surrey GU21 6HJ. Switzerland: The

Bellevue Funds (Lux) SICAV is registered for public offering and distribution in Switzerland with the Swiss Financial Market Supervisory Authority. Representative agent in

Switzerland: ACOLIN Fund Services AG, Leutschenbachstrasse 50, CH-8050 Zurich. Paying agent in Switzerland: DZ PRIVATBANK (Schweiz) AG, Münsterhof 12, P.O. Box, CH-

8022 Zurich. You can obtain the sales prospectus, Key Investor Information Document (“KIID”), statutes and the current annual and half-yearly reports, the current share prices and

further information about the fund free of charge in German from the management company Bellevue Asset Management AG, Seestrasse 16, CH-8700 Küsnacht, the representative

agent in Switzerland or online at www.bellevue.ch. In respect of the units distributed in or from Switzerland, the place of performance and jurisdiction is at the registered office of the

representative agent.

Prospectus, Key Investor Information Document („KIID“), fund contract as well as the annual and semi-annual reports of the BB securities fund under Swiss law are available free of

charge from: Switzerland: PMG Fonds Management AG, Sihlstrasse 95, CH-8001 Zurich or Bellevue Asset Management AG, Seestrasse 16, CH-8700 Küsnacht.

This material is not intended as an offer or solicitation for the purchase or sale of shares of BB Biotech AG. This material may not be distributed within the United States or any other

country where it may violate applicable law.

Copyright©2021 Bellevue Asset Management, Inc. All rights reserved.

33

The most important terms are explained in the glossary at www.bellevue.ch/en/glossaryYou can also read