Property Watch - Property Industry Ireland

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Property Watch Q2’16 From Property Industry Ireland, the most influential property organisation in Ireland Inside this Issue: Government launches wide-ranging Housing Action Plan with a supply target for the private housing sector of 25,000 per annum by 2020 Census 2016 shines light on housing shortages with low growth of the housing stock and almost 260,000 vacant houses Dublin prime office rents the eighth most expensive in Europe with rents at around €619 - €643 per m2 Investment turnover highest on record in Q2’16, with the acquisition of Blanchardstown Centre resulting in turnover of €2.2 billion AIB - a key player in the Irish real estate investment market AIB is actively supporting home buyers, SMEs, corporates, developers and investors in the property market

Introduction One of the main purposes of Property Watch is to make

the Irish property market as transparent as possible. It

provides a handy map for those looking to find the

Approximately 50% of house sales in Ireland are funded

without a mortgage. Therefore, the CSO Residential

Property Price Index is only counting half the activity in

sources of the most recent information on all parts of the housing market in any month.

The improved coverage the property sector.

In September, the CSO will launch a new Residential

of the CSO Property Access to timely and accurate data on the property

market is vital both for policy-makers and potential

Property Price Index (RPPI) for Ireland. The new

property price index will be based on Stamp Duty

Price Index from investors to make informed decisions. Of course,

published data on market activity is backwards looking

returns made to the Revenue Commissioners and

will now cover all market purchases of houses and

September will mean and can – at best – give a snapshot of an often very

fast-moving sector, but, when used properly, a

apartments by households, both cash and

mortgage-based transactions.

better house

collection of facts and figures will always give a

better indication of future trends than anecdotes This will undoubtedly help increase the accuracy of the

and guesswork. data which is put into the public domain. Interestingly,

price data In Ireland, we remain heavily indebted to the estate

the CSO notes that the physical characteristics of the

dwellings will be obtained by matching the Stamp Duty

agencies who publish statistics from their own returns with Building Energy Rating (BER) certification

transactions to provide that information. A leaf through data provided by the Sustainable Energy Authority of

Property Watch shows that, without the support of Ireland (SEAI). Locational characteristics of the

estate agency firms, our knowledge of the market would dwellings will be obtained by matching to the

be severely limited. Of course, there are still gaps in the GeoDirectory and Census 2011 Small Area Population

data, and I hope that Property Watch will give agencies Statistics (SAPS).

an indication of where there is a gap in the publicly-

available market information which they can fill. Houses, by their nature, are seldom identical. As

generations of owners make their mark on a property, it

One of the most newsworthy property datasets is the looks less and less like its neighbour’s and so its market

monthly Residential Property Price Index, published by value will never be identical to that in the same

the CSO. It is designed to measure the change in the neighbourhood or even the same street. There is an

average level of prices paid for residential properties inherent danger in trying to determine the price trends

sold in Ireland. While the monthly report inevitably of all houses or apartments in Ireland. Therefore, a

gathers massive media coverage, especially when the larger sample size is vital to ensuring that the individual

monthly headline figure shows a severe escalation or characteristics of the houses sold each month can

drop in house prices, very few people investigate what be accounted for.

the CSO actual measures.

Dr Peter Stafford

It is compiled using data on mortgage drawdowns Director, Property Industry Ireland

provided on a monthly basis by eight of the main

mortgage lending institutions. The data is recorded at

the point at which the sale occurs, so it gives a fairly

timely report on what is taking place. However, as the

CSO itself acknowledges, “not all residential property

transactions are funded by a mortgage (i.e. they are

cash based) and these transactions are excluded

from the scope of the index.”

2

Property Irish employment levels breaking the 2 million barrier

in Q2’16 for the first time since Q4’08 is one factor

of European cities. If this upward trend continues, this

development could damage the city’s competitiveness.

Overview

explaining the robust activity in the property market.

With employment growth recorded in twelve out of The notable difference outside of Dublin is the level of

fourteen sectors across the economy and an additional office rents. There is a strong development pipeline

56,200 persons at work over the past year, this will have in Cork where prime rents are less than half the

lifted consumer confidence, increased incomes and corresponding levels in Dublin, while in Galway, where

Rising rents at risk of resulted in more spending and investment. This is all

good news for the property market.

rents are almost 25% lower than in Cork, the office

market was exceptionally quiet in Q2. Activity in the

Limerick office market was subdued, with take-up

damaging Dublin city’s The housing challenge continues as supply edges

upwards. The strong growth in commencements - up

levels almost unchanged. Of the four main markets,

prime rents are lowest in Limerick at €172/m².

competitiveness

49% QoQ - is welcome, but has yet to translate into

supply on the ground. The more modest growth in Prime rents in the Dublin industrial market have

house completions to under 3,500 units nationally in increased throughout H1 2016, and are expected to

Q2’16 shows the scale of the housing supply challenge reach €94/per m² during H2 2016. Rents in Cork are

when set against the targets in the Action Plan for expected to be in excess of €85/m² for new

Housing and Homelessness. The Plan contains developments.

ambitious targets to double the annual level of

residential construction to 25,000 homes and deliver The reality is that Brexit happened at the end of Q2 and

47,000 units of social housing in the period to 2021. while the uncertainty it created began well in advance of

Achieving these targets will be conditional on the most the 23rd June, total investment market activity was

pressing issues being addressed by policy makers to estimated at around €2.3 billion in Q2’16, more than

ensure confidence returns to housebuilders and three times the corresponding level in the same period

house buyers. of 2015. CBRE suggest that Q2’16 had the largest

quarterly turnover on record, reflecting the largest single

Meanwhile the volume of residential property asset sale ever in Ireland of the Blanchardstown Centre

transactions fell YoY, while national and Dublin house for a reported €950 million.

prices (CSO) recorded annual growth rates of 7% and

5% respectively, with prices outside Dublin up by 9%. The proposed sale of the Project Tolka loan portfolio

Lending activity for house purchase is increasing by NAMA is now expected to happen much later than

strongly, with the average mortgage drawdown for first planned (summer 2015), and other loan portfolios in line

time buyers at €182,894 in Q2’16, almost 5 times for disposal later this year include Projects Gem, Ruby

average annual earnings. The finding which is of most and Emerald, all of which are expected to sell at

concern is the quarterly increase of 4% in residential substantial discounts.

rents across the board (Daft.ie), implying the upward

pressure on rents continues. Despite uncertainty and mixed reports, Brexit should

positively affect Ireland’s attractiveness for FDI. The

Reports on the Dublin office market were mixed, with magnitude of the effect is however unknown and any

one view expressed that take-up levels were below changes in demand will likely be gradual, but the Dublin

normal in Q2’16. Supply remains constrained, office (and residential) market will need to ensure

particularly for Grade A office accommodation. Rents any new demand from firms relocating can be

have therefore continued to increase significantly accommodated. Conversely, there is the risk that less

Annette Hughes and, although they were unchanged QoQ for most investment will be forthcoming from UK sources, and

Director, DKM Economic Consultants contributors, prime office rents are currently reported this could jeopardise commercial (and housing)

by CBRE to be the eighth most expensive in a survey projects relying on non-domestic sources of finance.

3

Latest The much anticipated Housing Action Plan

is published

However, as an immediate response, the Plan also

committed to providing funding support for a dedicated

News

Student Housing Officer to work with the USI, local

The Housing Action Plan promised by Government authorities, AHBs and housing providers as well as

was published on the 19th July 2016, well within the others stakeholders, to identify and expand short-term

timeframe of 100 days set out in the Government capacity enhancing measures in the student

Programme. The plan, ‘Rebuilding Ireland – an Action accommodation sector and to assist students in finding

Plan for Housing and Homelessness’, provides a appropriate accommodation. The intention here is to

Housing, Student multi-stranded, action-oriented approach to achieving

many of the Government’s key housing objectives,

identify new accommodation not currently available for

rent. The USI expects to increase to 1,000 the number

Accommodation, as set down in the Programme for a Partnership

Government. These include to significantly increase the

supply of social housing, to double the output of overall

of additional places via the “digs” service they run

which last year assisted a total of 600 students to find

rooms in private homes.

2016 Census and housing from current levels to at least 25,000 per annum

by 2020, to service all tenure types, and to tackle In addition the range of wider initiatives in the Action

homelessness. It is a comprehensive, albeit ambitious, Plan includes the potential for Higher Education

the Cost of Unused plan that addresses all aspects of the housing system

and contains 84 time-bound actions across a range of

Institutions to access low cost funding from the Housing

Finance Agency in a similar manner to approved

Accommodation Government departments and agencies. Its success

will be measured by how quickly it is implemented and

thus the work of the new dedicated Housing Delivery

housing bodies (AHBs), further funding from the Irish

Strategic Investment Fund (ISIF), fast-tracking large

student accommodation complexes through the

Office, set up to measure and report on progress planning process and the provision of access to large

regularly, is likely to be closely monitored. publicly owned zoned sites at reasonable prices.

A national student accommodation strategy to be 2016 Census of Population - average annual

delivered in the first half of 2017 population growth of 0.7% between 2011 and 2016

As another academic year commences, the issue of Preliminary results from Census 2016 were released in

student accommodation is back on the agenda. The July and showed that the Irish population reached 4.76

special topic in this issue examines the role for the million in April 2016, 3.7% above the previous Census

private sector in addressing the shortage of bespoke population figure for 2011. The largest proportional

student housing stock. The Housing Action Plan intercensal increases were recorded in the counties of

identified the expanded provision of student Meath (+5.9%), Dublin (+5.7%) and Kildare (+5.6%). The

accommodation as a key area to be addressed. It populations of the large counties of Cork and Galway

identifies the importance of providing dedicated and also expanded but at lower rates of 4.5% and 3.2%

additional student accommodation to avoid putting respectively. Population growth was recorded in all

additional pressures on the private rental sector, other counties over the intercensal period with the

particularly in and around the many universities and exception of the western counties of Donegal (-1.5%),

third-level institutions in urban areas. With this in mind, Mayo (-0.2%) and Sligo (-0.1%).

the Government has committed to the development of a

national student accommodation strategy in the first half Such demographic changes can have significant

of 2017, led by the Department of Education and Skills implications for the residential stock, particularly where

in conjunction with the Higher Education Institutions substantial population growth has occurred. In this

(HEIs), the Department of Housing, Planning, regard, the Census 2016 housing statistics show that

Community and Local Government (DHPCLG) and despite population growth of 3.7% since 2011, Dublin’s

other key stakeholders. housing stock rose by only 1% over the period. This

illustrates the seriousness of the shortage of housing in

the Capital and may partially explain the sustained

upward pressure on residential rents and prices which

has arisen over the past number of years.

4

Housing stock increased by 18,981 between 2011 these 36,732 dwellings are available for immediate

and 2016; yet the level of housebuilding completions occupancy and one suspects that a number of them

increased by 51,329 over the same period are still tied up with receivers and a further amount are

believed to be vacant, but not available, due to their

The Census also reported preliminary housing figures elderly owners transitioning into nursing homes.

which indicated that the housing stock was 2.023

million dwellings in April 2016, which represented an Commercial market - The cost of leases for

increase of 18,981 dwellings since the previous Census unused accommodation for State Agencies

in 2011. This contrasts with statistics from the DHPCLG

which show that 51,329 dwellings were completed in An interesting analysis of the annual accounts prepared

the same period. The difference of 32,348 dwellings is by the Comptroller and Auditor General for a selection

substantial. While the stock figure should include units of state agencies reveals the substantial cost to the

lost through obsolescence of dwellings during the five State from the payment of leases for unused

year period, it is unlikely that 32,348 dwellings were accommodation. The analysis by the Sunday

lost, particularly given the housing shortage that has Independent (14th August) concluded that more than

prevailed in recent years. One explanation may be that €1 million has been spent by seven state agencies on

units built and remaining vacant at the time of the last leases for unused accommodation due to

boom would have been counted as vacant in the 2011 amalgamations and staff cuts which left those agencies

Census but would have been connected for electricity with leases for office space that they no longer require.

post the year in which they were built. This would imply Based on an estimated average office rent of €250 per

the measure of house completions may overstate the square metre (€23.22/sq foot) across the country, this is

true level of housebuilding in the intervening years, due equivalent to 4,000m2 for those seven agencies alone.

to the peculiar issues to do with the surge in vacant The agencies included a number of Education and

dwellings left over after the construction boom. The Training Boards across the country, the National

Housing Agency estimated a figure of 23,250 dwellings Transport Authority, the Law Reform Commission, Safe

complete and vacant and a further 10,000 dwellings Food Ireland, the Health Research Board and IDA

near completion in the 2010 Survey of Unfinished Ireland. Indeed the figure excludes the cost of breaking

Developments. These 33,250 dwellings could have been leases on unused buildings which was reported, for

connected for electricity, and hence regarded as example, to have cost IDA Ireland €9.4 million this year

‘completed’, as they become occupied in the years for an unused building in Ballsbridge.

following 2010.

Although the analysis relates to only seven agencies,

In a related perspective, the level of vacant dwellings the report does raise the question about the State’s

both in Dublin and across the country is problematic for property portfolio and the full extent of the cost of

the residential market. Almost 13% of the Irish housing leases on office accommodation which is surplus to

stock was vacant in April 2016, down from 14.4% in requirements. The office portfolio of the State is

2011. The total number of vacant dwellings was comprised of 368 leases in 315 buildings, according to

259,562 in April 2016, around 30,000 below the figures from the Office of Public Works, which provide a

corresponding figure in 2011. The highest vacancy rate total of almost 360,000m2 of accommodation (41% of

was in Leitrim (29.5%) and the lowest vacancy rate was the total State portfolio). Separately, in regard to the 59

in Kildare at 6.3%. The vacancy rate in Dublin was per cent of the State portfolio which is owned, the OPW

6.9%, which amounted to 36,732 dwellings. These developed and implemented a coordinated disposals

vacancy rates are problematic, especially in the context policy on surplus property during 2015. It has previously

of the extremely weak housing supply which currently been suggested by some AHBs that some of these

pertains in Dublin, where the average additional housing disposals could be suitable for conversion to social

requirement has been estimated by the Housing Agency housing accommodation.

at almost 9,400 on average in the period 2014-2018.

The real question is how many of

5

Economic Last year, Irish GDP grew by a staggering 26.3%, higher

than any other developed country in the world. The

The full implications of Brexit are still unknown as it will

depend on, amongst other things, the future trading

Outlook

majority of this growth however came from the relationship between the UK and the EU. For 2016, Irish

movement of Intellectual Patents (IP) into Ireland. As growth will still be high due to the strong performance in

Ireland is a relatively small economy, these assets have the first half of this year but it may start to slow over the

a much bigger impact on GDP making it much more coming months. The exchange rate is already having a

volatile. As a result this headline rate provides a poor negative impact on those firms exporting into the UK.

reflection of underlying growth in the Irish economy. Since the beginning of this year, sterling depreciated

A potential slowdown Other measures however, do suggest that the economy

by 15% against the euro. This rapid weakening and

unprecedented uncertainty puts those exporting into the

in the UK could bring grew steadily in the first half of this year. While tax

receipts were lower than expected in July, they are still

UK at a competitive disadvantage. It also puts domestic

firms under pressure as they are now facing the

many challenges 8.5% higher than they were in the first seven months

last year. Growth in consumer spending has been

prospect of cheaper UK imports entering the Irish

market. An Ibec survey of members on Brexit found that

for Ireland strong and was up 5% in Q1’16. Investment (excluding

intangibles and transport) on the other hand, was down

the exchange rate was by far their biggest concern.

Only a quarter of exporters have hedging arrangements

4% year-on-year in Q1 primarily due to a decrease in in place and this protection will expire in the near future.

housing which fell by 5.2%. Exports in the first five Over the coming months, it is likely that sterling will

months of this year were only up by 1%. This slowdown depreciate further which will put increased pressure

in trade was due to a fall-off in pharma exports which on Irish business.

saw a record year in 2015.

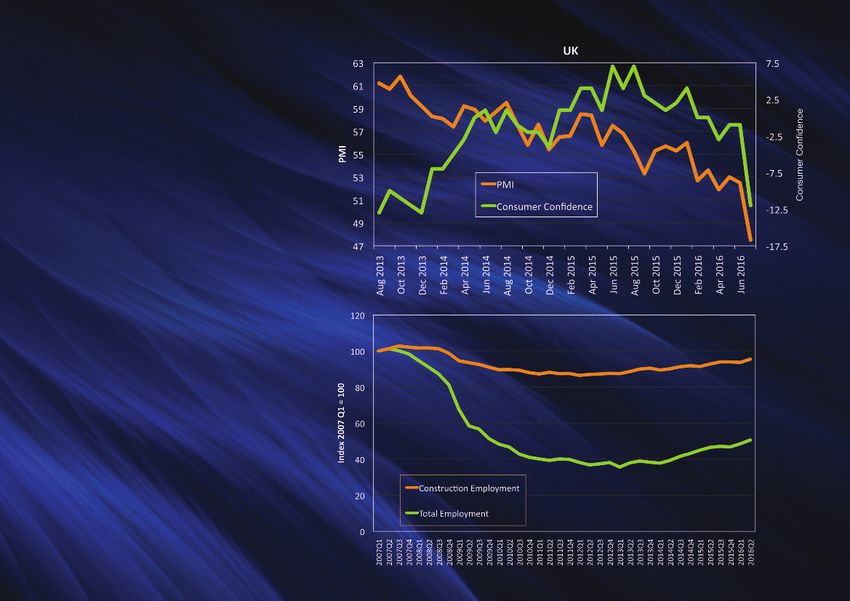

A clearer picture of the impact of Brexit on the UK

CSO figures showed annual employment growth of will unfold over the coming months as more data is

2.9% in Q2. This was ahead of expectations, with more released. Expectations of a slowdown have emerged in

than two million people now in employment for the first the UK as both businesses and consumers re-evaluate

time since 2008.This progress was spread across the their position. In July, PMI’s and consumer confidence

economy with positive employment growth in 12 of the were down. The Bank of England has cut its growth

14 sectors. Construction continued to be a strong forecasts for 2017 from 2.3% to 0.8% in light of Brexit,

performer as it was up 8.7%. However, compared to the largest downgrade in more than 20 years. Estimates

total employment it still has a lot more catching up to suggest that a 1 percentage point fall in UK growth

do before it reaches peak levels. leads to a knock on in Ireland of between one-quarter

and one-third of a percentage point. A potential

slowdown in the UK could therefore bring many

challenges for Ireland.

6UK PMI and Consumer Confidence

Employment Index Ireland

7Residential For the second quarter in a row, commencements

experienced doubt digit QoQ growth as the number of

The total number of loan approvals rebounded

impressively to 9,419 in Q2’16, with QoQ and YoY

Market

residential units commenced amounted to 3,065. This growth of 58% and 22% respectively. Such a quarterly

increase led to a robust annual growth rate of 33%. Of upsurge can be predominantly credited to an increase in

the total, just fewer than 40% or 1,179 commencements the number of loans approved for house purchases

were one-off units. From a regional point of view, (+58%), while the less numerous top-up/re-mortgage

Activity

Dublin continued to record the highest level of loan approvals were 60% higher. The value of loan

commencements in Ireland, accounting for 28% of the approvals also rose sharply, with high quarterly and

national total. This was followed closely by the Mid-East annual growth rates recorded in Q2’16. In total, €1.86

(Kildare, Meath and Wicklow) where commencements billion worth of loans were approved in Q2’16, an

rose to 790 in Q2’16. This may be a reflection of increase of 66% relative to the previous quarter. The

construction activity spilling over to commuter belt vast majority of these loan approvals related to house

Commencements counties due to viability issues in Dublin. Following a

remarkable start to 2016, the annual rate of growth in

purchases (€1.65 billion) following striking QoQ and YoY

growth of 66% and 28% respectively.

continue to record registrations eased to 12% in Q2’16, with 1,291

registrations in the quarter. The total number of mortgage drawdowns rose by 11%

double digit The level of completions in Q2’16 rebounded strongly to

YoY in Q2’16 to reach 6,803. Further examination of

the data shows that the number of house purchase

growth as loan 3,498, which represented an annual increase of 17%. As

expected, Dublin accounted for the largest share of this

drawdowns increased by 24% QoQ, and by 6% YoY.

The top-ups/re-mortgage segment also experienced

approvals rise total, with 28% of all completions for Q2’16 recorded

in the Capital. The next highest shares were recorded

noteworthy growth of 27% QoQ and 52% YoY. From a

monetary perspective, drawdowns in Q2’16 amounted

in the South West and the Mid-East (both 14%). to a value of €1.29 billion, having registered a YoY in-

Completions for 2016 year-to-date amounted to crease of 18% along with a robust QoQ growth of 29%.

6,642, which was 18% higher relative to the same A similar QoQ growth rate was recorded for drawdowns

period in 2015. relating to house purchases. For the second quarter in a

row, the average mortgage drawdown for first time

The 2016 Census provided an up to date estimate buyers increased, reaching €182,894 in Q2’16, which

for the housing stock of 2,022,895, which has led to corresponds to almost 5 times average annual earnings.

revisions to the quarterly estimates included in Such an improvement reflected QoQ and YoY growth of

previous Property Watch publications. 3% and 7% respectively.

The level of transactions recorded in the Property

Price Register rose to 10,928 in Q2’16, which was an

improvement of 19% relative to the previous quarter. Of

these transactions, Dublin accounted for just over 30%

of the total, while both Carlow and Monaghan

accounted for the lowest shares (both 0.8%).

8Residential Market Activity

Q4’15 Q1’16 Q2’16 QoQ YoY Loan Approvals Q4’15 Q1’16 Q2’16 QoQ YoY

Units Granted Planning 4,017 3,091 N/A -23% -4% Total Number of Loan Approvals 7,219 5,956 9,419 +58% +22%

- Houses 2,754 2,534 N/A -8% +1% - House Purchase 6,185 5,149 8,126 +58% +19%

- Apartments 1,263 557 N/A -56% -20% - Top-Ups/Re-mortgages 1,034 807 1,293 +60% +49%

Total Loan Approval €m €1,352 €1,121 €1,859 +66% +32%

Commencements 1,742 2,059 3,065 +49% +33% - House Purchase €m €1,188 €998 €1,654 +66% +28%

of which one-offs 765 803 1,179 +47% +30% - Top-Ups/Re-mortgages €m €164 €123 €204 +67% +80%

Registrations* 859 1,263 1,291 +2% +12% Mortgage Drawdowns

Total Number of Drawdowns 7,993 5,447 6,803 +25% +11%

Completions** 3,752 3,144 3,498 +11% +17% - House Purchase 6,780 4,634 5,767 +24% +6%

- Top-Ups/Re-mortgages 1,213 813 1,036 +27% +52%

Transactions*** 13,316 9,215 10,928 +19% -2% Total Drawdowns €m €1,438 €999 €1,286 +29% +18%

- House Purchase €m €1,264 €888 €1,141 +28% +14%

National Housing Stock (000s) 2,019 2,020 2,023 0% 0% - Top-Ups/Re-mortgages €m €174 €111 €145 -31% +59%

FTB Drawdown - Average €172,188 €177,331 €182,894 +3% +7%

Regional Commencements Q2’16 Regional Completions Q2’16 Regional Transactions Q2’16

800 4,000

700 3,500

600 1,200 3,000

500 1,000 2,500

400 800 2,000

300 600 1,500

200 400 1,000

100 200 500

0 0 0

Border

West

Midlands

MidEast

Dublin

SouthEast

SouthWest

MidWest

Border

West

Midlands

MidEast

Dublin

SouthEast

SouthWest

MidWest

Border

West

Midlands

MidEast

Dublin

SouthEast

SouthWest

MidWest

Source: www.environ.ie Source: www.environ.ie Source: www.propertypriceregister.ie

*Mid-West includes all of Tipperary. *Mid-West includes all of Tipperary.

*Registrations refer to the number of units registered with Home Bond and Premier Guarantee. **Completions are measured as connections to ESB. *** Transactions exclude properties that are not full market price and those under €20,000 and over €5 million.

There have been some revisions to earlier data following updates on the PPR. QoQ refers to the latest quarter on quarter percentage change (Q2 on Q1). YoY refers to the latest year on year percentage change (Q2 2016 on Q2 2015).

Loan Approval and Mortgage drawdown data from www.bpfi.ie 9Residential Asking prices for residential properties increased at

the national level in Q2’16 according to Daft.ie. The

An analysis of the Property Price Register (not mix-

adjusted) found that the national average transaction

Property

strongest growth rates occurred outside of Dublin where price was €236,363, which represented a YoY increase

prices rose by 10% YoY. The corresponding rise in the of 10%. This was well below the average transaction

quarter was 3%. Asking price growth was more modest price of €388,320 recorded in Dublin, with the Capital

in Dublin at 1% YoY and 1% QoQ, and this is further registering YoY growth of 20%. When Dublin is

Prices

evidence of the two-speed recovery in Irish residential excluded, the national average transaction price falls

asking prices which has emerged in recent quarters. considerably to €168,374, highlighting the effect of the

Overall YoY price growth for the country was 6% Capital on national prices.

in Q2’16.

Mix-adjusted transaction prices, as produced by Daft.ie,

According to MyHome, asking prices on the national portrayed a different picture in Q2’16 with prices outside

Modest quarterly scale continued to grow in Q2’16. Prices rose by 5%

YoY and a similar YoY increase was recorded in Dublin.

the Capital rising by 3% QoQ. This contrasted with

Dublin where prices fell by 1% QoQ. Cumulatively

growth in residential Both the national and Dublin series recorded quarterly

growth of between 2% and 3%.

prices rose by 1% QoQ at the national level. Compared

to Q2’15, transaction prices were up by 1% in Dublin

prices while rents Based on price valuations recorded by Sherry

and 8% outside Dublin, which contributed to a YoY

national growth rate of 5% in the quarter.

rise strongly FitzGerald, residential property prices increased by 1%

QoQ both nationally and in Dublin in Q2’16. The The pace of growth in the RTB’s standardised rent index

national index increased 4% YoY, which was above the eased considerably at both the national and Dublin

2% YoY growth reported in Dublin. Knight Frank‘s levels in Q1’16. Rents nationally rose at a weakened

Prime Dublin Residential index showed that prices in rate of 1% QoQ, but remained 9% above the same

the Capital experienced a YoY increase in Q2’16 of 5%. period in 2015. In the Capital, rents were stable on a

This index also recorded a modest QoQ expansion of quarterly basis, but also stood 9% above levels in

1% in the Capital. Q1’15. Daft.ie’s analysis for Q2’16 produced slightly

different results with rents in Dublin and across the rest

Q2’16 recorded further growth in the CSO’s residential of the country rising at a stronger rate of 4% QoQ.

price index (based on mortgage-based transactions Rents in Dublin, the rest of the country and at the

only), with national and Dublin house prices recording national level all stood 11% above Q2’15 as upward

YoY growth rates of 7% and 5% respectively. However, pressure on rents continues.

the highest YoY rate of growth was recorded in the

national excluding Dublin index with prices up by 9%.

On a quarterly basis, prices rose by 2% in Dublin but

remained flat in the rest of the country.

10Residential Property Prices Average Sold Price by

ASKING PRICES Q4’15 Q1’16 Q2’16 QoQ YoY County Q2 2016

Daft.ie National MAAA* (€) €204,175 €210,333 €214,954 +2% +6% Dublin €388,230

Daft.ie Dublin MAAA* (€) €306,613 €312,642 €314,311 +1% +1% Wicklow €309,866

Daft.ie National ex. Dublin MAAA* (€) €164,838 €171,045 €176,799 +3% +10% Kildare €264,142

MyHome National MAAA* (€) €205,031 €207,596 €212,725 +3% +5% Meath €228,200

MyHome Dublin MAAA* (€) €285,921 €290,301 €296,190 +2% +5% Cork €201,853

PRICE VALUATIONS Galway €179,370

Sherry FitzGerald: National (Index 1999 =100) 123.2 124.7 126.5 +1% +4% Kilkenny €173,344

Sherry FitzGerald: Dublin (Index Q4 1996 =100) 402.9 405.6 409.6 +1% +2% Louth €163,383

Wexford €147,519

Knight Frank Prime Dublin Residential 134.0 135.9 136.6 +1% +5% Carlow €147,064

(Index Dec 2012 = 100) Limerick €146,266

PRICES BASED ON MORTGAGE TRANSACTIONS Kerry €145,833

CSO National (Index 2005=100) 86.7 86.5 87.1 +1% +7% Clare €137,946

CSO Dublin (Index 2005=100) 86.6 85.2 87.0 +2% +5% Offaly €139,395

CSO National ex. Dublin (Index 2005=100) 82.5 83.3 82.9 0% +9% Waterford €136,389

SOLD PRICES Laois €130,359

PPR National Average €227,612 €235,706 €236,363 0% +10% Tipperary €124,572

PPR Dublin Average €377,981 €368,980 €388,320 +5% +20% Monaghan €123,276

PRR National ex. Dublin Average €168,490 €168,992 €168,374 0% +7% Donegal €122,436

Daft.ie National MAAA* €199,139 €200,258 €203,024 +1% +5% Westmeath €119,943

Daft.ie Dublin MAAA* €303,773 €309,616 €306,347 -1% +1% Mayo €116,657

Daft.ie National ex. Dublin MAAA* €158,958 €158,263 €163,346 +3% +8% Cavan €105,874

RESIDENTIAL RENTS Sligo €105,169

RTB National Standardised Rents €917 €922 N/A +1% +9% Leitrim €88,651

RTB Dublin Standardised Rents €1,311 €1,314 N/A 0% +9% Roscommon €80,922

Daft.ie National MAAA* (€) €979 €998 €1,037 +4% +11% Longford €76,976

Daft.ie Dublin MAAA* (€) €1,435 €1,464 €1,520 +4% +11% Source: Property Price Register, DKM Analysis.

Transactions price data excludes properties that are not full market price

Daft.ie National ex. Dublin MAAA* (€) €727 €740 €770 +4% +11% and those under €20,000 and over €5 million, but includes VAT. Not Mix-Adjusted.

** Transactions price data excludes properties that are not full market price and those under €20,000 and over €5 million but includes VAT. Not Mix-Adjusted.

* MAAA = Mix-Adjusted Annual Average.

QoQ refers to the latest quarter on quarter percentage change.

YoY refers to the latest year on year percentage change.

11Commercial Dublin office take-up recorded between 37,200m²

(CBRE) and 66,300m² (Cushman & Wakefield Research)

The vacant stock in Dublin was reported at between

231,500m² (JLL) and 400,200 m² (Cushman & Wakefield

Office

in Q2’16 bringing the H1’16 take-up to between Research) in Q2’16. The stock has thereby continued

87,600m² (Lisney) and 126,200m² (Cushman & Wakefield the downward trend since the first PII Property Watch

Research). Commercial office take-up was therefore data in Q3’15. A lot of the available supply is however

significantly lower compared to H1’15 which saw take- substandard or was occupied previously. Consequently

Market

up between 92,900m² (Cushman & Wakefield Research) all but one contributor (Lisney) recorded lower vacancy

and 133,000m² (Lisney). The volume of take-up has rates in Dublin in Q2’16 ranging from 6.7% (JLL) to

however been below normal as several sizeable 12.0% (Cushman & Wakefield Research). The Dublin

Prime rents in Dublin

transactions are in negotiations and are expected to be city centre vacancy rate was lower than the overall rate

signed during the next quarter (CBRE). ranging between 3.3% (JLL) and 8.7% (Lisney). By the

are the eighth most

end of June, one agent reported that 27 office schemes

Given the continuing constrained supply situation, the or 345,000m² were under construction in Dublin, of

market conditions have favoured landlords seeking which 22% had been pre-let (CBRE).

expensive in Europe

longer leasing periods (20 to 25 years with a 10 to 12

year commitment) and offering shorter rent free periods Brexit is causing a great deal of uncertainty for the

(less than six months/city centre and less than a property market in Ireland. While reports on the specific

year/suburbs). Rents have therefore increased impacts have been mixed, the result should positively

significantly during the last few years and this trend has affect Ireland’s attractiveness for foreign direct

continued throughout H1’16. According to the Lisney investment in the medium- and long-term. The

rental index for Dublin, rents increased 17.7% in the 12 magnitude of the effect is however unknown and any

months to June 2016 with city centre rents increasing changes in demand will likely be gradual. Some financial

by 18.7%. Since early 2013 the city centre rent index services firms, technology companies and other

has increased 110.6% though the rate of increase is organisations may decide to relocate to alternative and

stagnating (Linsey). Dublin prime rents did however Euro-denominated cities in order to stay in the internal

remain constant between Q1 and Q2 for most market. Consequently the Dublin office (and residential)

contributors, with rents recorded between €603 per m² market will need to ensure any new demand can

(Lisney) and €646 per m² (JLL). However, prime office be accommodated.

rents are currently reported by CBRE to be the eighth

most expensive in a survey of European cities. Conversely, with regard to the availability of finance,

there is the risk that less investment will be forthcoming

The IT and Pharma / Health sectors accounted for the from UK investment companies and financial

largest proportions of the total Q2’16 take-up (30% and institutions, and any finance made available from UK

24% respectively) as the five largest deals were in these sources could be very costly. This could jeopardise

industries (Lisney). Looking at H1’16, the State and the commercial (and housing) projects relying on

Financial sector dominated take-up representing 31% non-domestic sources of finance.

and 30% of all transactions respectively (Lisney). Of the

65 transactions in Q2’16 reported by CBRE, 28 were

signed by Irish occupiers, 21 by American companies

and 8 by UK companies (CBRE).

12Snapshot of Dublin Office Property Market Indicators

Dublin Take-Up (‘000m2) Q4’15 Q1’16 Q2’16 YTD Dublin Vacancy Rates (%) Q4’15 Q1’16 Q2’16 QoQ

CBRE 75.2 52.4 37.2 89.2 CBRE 9.4 8.6 8.4 -0.2pp

Cushman & Wakefield Research 45.0 59.9 66.3 126.2 Cushman & Wakefield Research

Sherry Fitzgerald 14.1

13.0 -0.9pp

13.2 -0.9pp

12.0 -0.9pp

-1.2pp

JLL 90.8 45.1 49.8 95.0 JLL 10.2

7.8 -0.9pp

8.0 -0.9pp

6.7 -0.9pp

-1.3pp

Knight Frank 87.5 67.2 40.4 107.6 Knight Frank 8.8 8.3 8.2 -0.1pp

Lisney 91.6 44.0 43.6 87.6 Lisney 11.2 10.9 11.0 +0.1pp

Dublin City Centre Take-Up (‘000m2) Dublin City Centre Vacancy Rates (%)

CBRE 53.1 39.8 31.2 71.0 CBRE 7.4 6.9 6.6 -0.3pp

Cushman & Wakefield Research 11.8 25.3 27.5 52.8 JLL 3.7 3.7 3.3 -0.4pp

JLL 54.5 24.2 27.3 51.5 Lisney 9.3 8.7 8.7 0.0pp

Knight Frank 46.6 31.4 23.7 55.1 Dublin CBD Vacancy Rates (%)

Lisney 58.8 37.0 27.0 64.0 CBRE 6.0 5.8 6.1 +0.3pp

Dublin Vacant Stock/Availability (‘000m2) Cushman & Wakefield Research 8.9 10.0 8.9 -1.1pp

Cushman & Wakefield Research 435.1 439.9 400.2 Lisney 7.8 8.2 8.3 0.1pp

JLL 268.9 275.3 231.5 Dublin Office Yields (%)

Lisney 396.2 385.8 390.0 CBRE 4.65 4.65 4.65 0.0pp

Dublin City Centre Rents (€/m ) 2

Q4’15 Q1’16 Q2’16 QoQ Cushman & Wakefield Research 4.25 4.25 4.25 0.0pp

CBRE 592 592 619 +5% JLL 4.50 4.50 4.50 0.0pp

Cushman & Wakefield Research 592 592 592 0% Knight Frank 4.50 4.50 4.50 0.0pp

JLL 592 646 646 0% Lisney 4.25 4.25 4.40 +0.2pp

Knight Frank 619 619 619 0%

Lisney 480 492 537 +9%

Dublin Prime Rents (€/m2)

CBRE 592 619 619 0%

Cushman & Wakefield Research 592 592 592 0%

JLL 592 646 646 0%

Knight Frank 619 619 619 0%

Lisney 592 592 603 +2%

QoQ refers to the latest quarter on quarter percentage or percentage point change (Q2 on Q1). YTD refers to 2016 to date, i.e. the latest two quarters

13Industrial Based on data from three agents, industrial take-up in

Dublin totalled between 46,000m² (JLL) and 54,988m²

JJM Transport Unit comprising 6,050m² in Damastown

Industrial Park (Lisney). Based on the transactions

Property

(CBRE) in Q2’16 bringing take-up in the first half of 2016 reported by one agent, most (53%) ranged between

to between 97,100m² (JLL) and 119,700m² (CBRE). The 1,858m² and 4,645m² with transactions between 929m²

level of take-up in H1’16 is therefore much lower and 1,858m² accounting for 15% of the total in Q2’16

compared to the same period in 2015 which recorded (CBRE). Another agent stated that lettings dominated,

Market

between 182,100m² (Lisney) and 219,964m² (Cushman accounting for 58% of total take-up in the quarter (JLL).

& Wakefield Research) of take-up. Take-up is however in In volume terms take-up was significantly lower (-39%)

line with the mid-year average over the past five years in Q2’16 compared to Q2’15 and compared to Q1’16

of 102,200m² (JLL). This development is due to the (-33%), even though the number of transactions

continued scarcity of high quality modern industrial remained constant (40 in total) according to Lisney.

facilities in prime locations as opposed to a lack of Q2’16 also saw more lettings than sales, for the first

Still a scarcity of demand according to CBRE. time since 2012 (Lisney). A third agent reported a

similar story, with lettings and sales accounting for

modern industrial Prime industrial rents have continued to increase

throughout 2016 reaching between €80 (Lisney) and €85

approximately 60% and 40% of transactions

respectively, with the majority of sales being less than

facilities in good (CBRE) per m². Additionally CBRE expect prime rents to

increase to €94/per m² during the second half of 2016.

1,000m² and centred in the South West region (Lisney).

Consequently sales prices remained below replacement

locations This development in prime rents is highly likely as

speculative warehouse projects in Dublin Airport

costs, but the gap is expected to close (Lisney).

Logistics Park and the North City Business Park are The UK referendum in June to leave the European Union

expected to seek rents of €96/per m² and €108/per m² has caused some uncertainty in the sector but the

respectively (Lisney). As prime industrial rents increase, full extent of the effect on the Irish market remains

more speculative developments will start to emerge unknown. The outcome of the referendum will affect

which will ease supply pressures. Many occupiers will, some occupiers in the short term especially if they are

however, have to employ ‘design to build’ solutions in net exporters to the UK and therefore vulnerable to

the meantime to satisfy their requirements, according exchange rate fluctuations. The extent of any

to CBRE. The supply shortage is therefore likely to expansions or relocations is therefore difficult to

continue into the second half of 2016 pushing rents gauge, until the terms of Brexit are fully known.

up and increasing pre-letting negotiations.

Similarly to Q1’16, transactions centred around the

North East corridor with 35% of all sales and lettings in

Q2’16 and 22% of all activity in H1’16 occurring there

according to CBRE. In contrast to several quarters in

2015, there were no lettings or sales of facilities

exceeding 9,290m² recorded in Q2’16 (CBRE). The

largest transaction in Q2’16 was the sale of the former

14Snapshot of Dublin Industrial Property Market Indicators

Dublin Take-Up (‘000m2) Q4’15 Q1’16 Q2’16 YTD

CBRE 115.6 64.7 55.0 119.7

Cushman & Wakefield Research 102.9 59.4 45.5 104.9

JLL 97.5 51.1 46.0 97.1

Lisney 86.0 60.9 50.1 111.0

Dublin Vacant Stock/Availability (‘000m2)

Cushman & Wakefield Research 633 582 N/A

Dublin Prime Rents (€/m ) 2

Q4’15 Q1’16 Q2’16 QoQ

CBRE 75.0 80.0 85.0 6%

Cushman & Wakefield Research 75.0 81.0 81.0 0%

JLL 78.0 80.7 80.7 0%

Lisney 78.0 78.0 80.0 3%

Dublin Vacancy Rate (%)

Cushman & Wakefield Research 15.6 14.3 14.0 -0.3pp

Dublin Yields (%)

CBRE 5.75 5.75 5.75 0.00pp

Cushman & Wakefield Research 5.75 5.75 5.75 0.00pp

JLL 6.00 5.25 5.25 0.00pp

Lisney 5.90 5.70 5.70 0.00pp

QoQ refers to the latest quarter on quarter percentage or percentage point change (Q2 on Q1).

YTD refers to 2016 to date, i.e. the latest two quarters. N/A = not available.

15Commercial Information on the regional property market in the main

urban areas – Cork, Galway and Limerick – is based

In terms of new developments in the pipeline, in the

Regional

region of 64,200m² of office development is reported to

on data provided by Cushman & Wakefield Research. be under construction in the Cork market, according to

Lisney also monitors the Cork property market and Lisney, comprising 3,000m² in the mixed use

their data is also included. development under construction at the Capitol site on

the Grand Parade and 32,500m² at the Central Plaza in

Market

There is a consensus amongst the two agents around Mahon, both being brought to the market by John

the level of take-up in the Cork office market in Q2’16, Cleary Developments. Meanwhile, CIE has signed

with both Lisney and Cushman & Wakefield Research contracts with Clarendon Properties and BAM Ireland,

reporting a figure around 4,000m². However Lisney for development of a mixed use density and relatively

suggest that take-up levels doubled while Cushman & high-rise scheme, on its six-acre portion of its station

Wakefield Research suggest that they more than halved site at Horgan’s Quay in the city. This project is at the

in the quarter. This may be a timing issue in regard to early pre-planning stages.

Strong development when transactions are recorded. However, the total

take-up in H1’16, according to Cushman & Wakefield

pipeline in Cork where Research, was 13,700m², over twice the estimate from

Lisney of 6,100m². According to Lisney, the professional

Rents in the Cork industrial market expected to

be in excess of €85/m² for new developments

prime rents are less services sector dominated, accounting for 30% of total

transactions in the first six months, and were followed Total take-up in Cork in Q2’16 was reported at 2,750m²

than half the levels

by the IT and pharmaceutical sectors. In regard to the compared with 2,350m² in Q1’16. The total represented

other locations, the Galway market was exceptionally a quarterly increase of 17% but was well down on the

quiet with no take-up recorded in the quarter, while 5,750m² recorded in Q4’15. The quantum of stock

in Dublin activity in the Limerick market remain subdued, with

take-up levels almost unchanged in the quarter.

available in Q1’16 was up only marginally in the quarter,

from 206,600m² in Q1’16 to 210,000m². This is just over

half of the total available stock in the Dublin office

Between 88,450m² and 94,000m² of space was market, according to Lisney data. Much of the available

available in Cork at the end of Q2’16, almost unchanged stock is reported to be older stock or in less sought

from the position at the end of 2015. An analysis by after locations, with a limited supply of modern well

Lisney suggests that over 40% of the stock is in the located units on the market. The vacancy rate for the

city centre, much of which is older stock in need of overall market was estimated at 16.3%, ranging from

refurbishment. Limerick was not far behind Cork with an around 7% in the West suburbs to over 25% in the

estimated 71,450m² of available accommodation, North suburbs. The first spec-built warehouse in the

almost 5% above the corresponding level in Q1’16. The Cork area for a number of years was completed in Little

Galway market had a substantially lower amount of Island by the O’Connell Group with the rent sought at

vacant stock at 15,450m² in Q2’16, while the office €81/m². This is above the prevailing market rent but

vacancy rate overall was in single digits at 5.1%. rents in excess of €85/m² are expected to be the levels

Elsewhere, vacancy rates were in double digits, ranging required to support any new development,

from 15.7% to 18.6% overall in Cork and were higher, at according to Linsey.

19.5%, in Limerick overall, although they were closer to

30% in the Limerick Shannon Free Zone.

The notable difference outside of Dublin, when

compared with the Dublin market, is the level of office

rents. With prime rents in Dublin reported to be the eight

most expensive in Europe, office rents in Cork, Galway

and Limerick are substantially lower. Prime rents were

highest in Cork at €290/m², less than half the

corresponding level in Dublin. They were lower in

Galway at €220/m² and lowest in Limerick at €172/m².

16Regional Market Indicators

OFFICES INDUSTRIAL

TAKE-UP (m2) Q4’15 Q1’16 Q2’16 YTD Q4’15 Q1’16 Q2’16 YTD

Cork* 4,880 2,050 4,050 6,100 5,700 2,350 2,750 5,100

Cork 1,550 9,700 4,000 13,700 4,100 1,100 6,250 7,350

Galway 2,250 2,600 0 2,600 200 1,750 350 2,100

Limerick 5,700 1,100 1,150 2,250 13,950 3,700 8,300 12,000

VACANT STOCK/AVAILABILITY (m2)

Cork* 95,000 97,300 93,797 217,000 206,600 210,000

Cork 85,550 94,300 88,450 152,650 157,650 164,450

Galway 13,600 14,200 15,450 42,500 43,450 50,950

Limerick 66,800 68,300 71,450 166,800 169,100 173,100

PRIME RENTS (€/m2) Q4’15 Q1’16 Q2’16 QoQ Q4’15 Q1’16 Q2’16 QoQ

Cork 250 270 290 +7% 55.0 55.0 70.0 27%

Galway 220 220 220 0% 54.0 54.0 75.0 39%

Limerick 172 172 172 0% 43.0 43.0 48.0 12%

VACANCY RATE (%)

CORK

Cork Overall* 15.6 19.3 18.6 -0.7pp

Cork Overall 15.6 16.7 15.7 -1.0pp

Cork City Centre 16.2 18.5 16.7 -1.8pp

Cork Suburbs 15.2 15.5 14.9 -0.6pp

GALWAY

Galway Overall 4.5 4.7 5.1 +0.4pp

Galway City Centre 5.5 5.2 6.1 +0.9pp

Galway Suburbs 3.9 4.3 4.4 +0.1pp

LIMERICK

Limerick Overall 18.2 18.7 19.5 +0.8pp

Limerick City Centre 16.8 17.7 19.2 +1.5pp

Limerick Suburbs 14.5 14.0 14.7 +0.7pp

Limerick Shannon Free Zone 29.7 29.7 29.7 0.0pp

*Source is Lisney. All other data from Cushman & Wakefield Research.

QoQ refers to the latest quarter on quarter percentage of percentage point change (Q2 on Q1). YTD refers to 2016 to date, i.e. the latest two quarters.

17Investment Perhaps the main repercussions of Brexit will be felt in

the investment market. To quote from Lisney’s Q2’16

Retail Park in Naas for €25.5 million and the Kilkenny

Retail Park for €23.5 million. One other major Dublin

Market

Investment Update shopping centre expected to attract significant interest

from international investors is the Liffey Valley Shopping

“Investment is a confidence business and Centre which is expected to be put up for sale by owners

uncertainty hammers confidence.” Hines, the Grosvenor Group and HSBC Alternative

Investment with an estimated asking price of €600

However, this review of investment market activity in million. There was also substantial activity in the offices

Turnover in Q2 the Property Watch since the first issue in Q3’15 has

demonstrated the substantial acquisitions made in the

sector which accounted for 36% of the total turnover in

Q2’16. The most substantial transaction was the sale of

largest level on record, Irish commercial property market by a mix of domestic

and international funds. According to an analysis of

PWC’s building of 21,000m² in Spencer Dock for a

reported €240 million.

notwithstanding investment activity in H1’16 by CBRE and Allsop, just

6% of the total value of income producing commercial Meanwhile the sale of the Project Jewel loan portfolio by

uncertainty

property purchased for less than €1 million, and 13% of NAMA, comprising the Dundrum Town Centre and loans

assets purchased above €1 million, went to UK financial attached to 50% stakes in the Ilac Centre in Dublin City

around Brexit

institutions and pension funds. As the Brexit plans unfold, and the Pavilions Shopping Centre in Swords, to UK

the uncertainty generated plus the depreciation of the property group Hammerson and its joint venture partner

Sterling exchange rate may adversely impact future Allianz Real Estate for €1.85 billion last year, concluded

investment decisions by UK investors in Ireland. in July 2016.

The reality is that Brexit happened at the end of the The proposed sale of the Project Tolka loan portfolio by

second quarter and while the uncertainty it created NAMA is now expected to happen much later than

began well in advance of the 23rd June, the total planned (summer 2015) due to the complex nature of the

investment market activity was estimated at €2.3 billion loans in the portfolio. The most significant assets are the

(JLL) in Q2’16, more than three times the corresponding Burlington Plaza office complex on Burlington Road in

level of investment in the same period of 2015. JLL Dublin, the Clarion Hotel and the Belfield headquarters of

estimate the mid-year investment total at €2.95 billion, Paddy Power and the former Harcourt Street children’s

versus their total figure for 2015 of €3.4 billion. Once hospital. Other loan portfolios in line for disposal by

again Dublin accounted for the vast majority of turnover NAMA later this year include Project Gem, which is

in Q2’16, estimated at between 90% (CBRE) and 92% reported to have a face value of around €4 billion, while

(JLL) of the total. However, according to the CBRE/Allsop the preferred bidders, Oaktree Capital, were selected by

analysis of investment activity in H1’16, Dublin accounted NAMA for projects Ruby and Emerald, a package of

for 56% of transactions in H1’16, with a further 15% loans with a combined face value of €4.7 billion. All three

located elsewhere in Leinster. portfolios are expected to sell at a substantial discount.

CBRE suggest that turnover in Q2’16 was the largest

quarterly turnover on record. This reflects the sale of the

Blanchardstown Centre by Green Property to Blackstone

for a reported €950 million, the largest single asset sale

ever in Ireland, accounting for around 45% of CBRE’s

total Q2 turnover estimate of €2.1 billion. This deal made

Retail the dominant sector, although other notable, albeit

much smaller, retail transactions which took place in

regional towns included the sale of the Bridgewater

Shopping Centre in Arklow for €32.5 million, the Globe

1819

AIB AIB continues to be very active across the property

market spectrum, supporting consumers, SMEs,

As well as supporting our local market teams, the

Property Lending Unit continues to provide larger ticket

supporting

corporates, developers and investors. funding for the commercial property investment market

in Ireland.

AIB has been particularly busy providing mortgage

finance at market- leading rates and remains the largest Property is a key sector for AIB and for the Irish

the

provider of new mortgages in the market this year with a economy. We has been working closely with SME and

34% share of new mortgage business drawn down by corporate customers facilitating the development of

the end of May 2016. nursing homes, primary care centres, hotels and

manufacturing capacity. We have also facilitated the

Across the country, 19 local market teams have been financing of the transfer of leasehold to freehold

Property

supporting personal and business customers with particularly for retailers.

commercial property investment finance. This has been

supported by our Property Lending Unit which is the AIB is also supporting student housing this year with

bank’s centre of excellence for property. This unit was a number of key transactions and is also actively

Market in

established more than a year ago and has a team of supporting the development of social and affordable

property specialist lenders supported by a number of housing working closely with approved housing bodies

chartered surveyors and engineers who work closely (AHBs) and experienced developers. We have been

alongside the lenders providing specialist support to exclusive finance partner with the Irish Council for

them and to our customers. Social Housing over the past 3 years and are

Ireland

sponsoring its finance conference in Kilkenny on

The Property Lending Unit has also been busy providing Oct 20th and 21st this year.

finance and supporting a number of residential and

commercial development property transactions. AIB We are focused on meeting the financing needs of our

continues to be committed to working with capable existing and prospective customers operating in the

parties to deliver homes in locations where demand is property market, as well as providing the appropriate

evident and developments are economically viable. We sector expertise to our SME and corporate customers

Providing finance are also supporting commercial office development in

Dublin City Centre with strong partners and covenants.

requiring finance for development of their business

model regardless of the sector.

across the property Development of housing supply and suitable

commercial office space are important for both Foreign We have an active pipeline and continue to look for

market spectrum Direct Investment and the Irish corporate and

SME market.

lending opportunities in the commercial and residential

investment and development markets.

20Contact Details for the AIB Property Lending

Unit are as follows:

Donall O’Shea,

Head of Property Lending Unit

Tel; 01 7720302

Email; donall.a.o’shea@aib.ie

Derek O’Shea,

Head of Residential Development & Specialist Assets

Tel; 01 6414431

Email; derek.p.o’shea@aib.ie

Ciaran Mooney,

Head of Commercial Real Estate Investment

Tel; 01 7726355

Email; Ciaran.e.mooney@aib.ie

Contact details for our Local Market

teams are as follows:

Joanna McFadden

Head of New Business Dublin & East

Tel; 086 7947804

Email; Joanna.p.mcfadden@aib.ie

John Heapes

Head of New Business Galway & West

Tel; 086 381 2554

Email; John.heapes@aib.ie

Michael Hayes

Head of New Business Cork & South

Tel; 086 465 8530

Email; Michael.g.hayes@aib.ie Unit

21You can also read