Proven Team, Proven Approach: The First and Only Pure Play Uranium Royalty Company

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

UROY : NASDAQ

URC : TSX-V

Proven Team, Proven Approach:

The First and Only Pure Play Uranium Royalty Company

Corporate Presentation

June 2022

2 FORWARD-LOOKING STATEMENT Forward-Looking Information The information contained herein contains “forward-looking statements” within the meaning of the United States Private Securities Litigation Reform Act of 1995 and “forward-looking information” within the meaning of applicable Canadian securities legislation. “Forward-looking information” includes, but is not limited to, statements with respect to the activities, events or developments that Uranium Royalty Corp. (“URC” or the “Company”) the Company expects or anticipates will or may occur in the future, including the completion of tentative transactions. Forward-looking information and statements are based on the then current expectations, beliefs, assumptions, estimates and forecasts about URC’s business and the industry and markets in which it operates. Forward-looking information and statements are made based upon numerous assumptions and although the assumptions made by the Company in providing forward-looking information or making forward-looking statements are considered reasonable by management at the time, there can be no assurance that such assumptions will prove to be accurate. Forward-looking information and statements also involve known and unknown risks and uncertainties and other factors, which may cause actual results, performances and achievements of URC to differ materially from any projections of results, performances and achievements of URC, including, without limitation, URC's limited control and access to data to the projects underlying its interests, commodity, commodity and investment price risks, currency risks, counterparty risks, proposed acquisitions may not be completed as contemplated or at all, risks faced by the operators and owners of the projects underlying URC's interests and the other risk factors described in the Annual Information Form and other filings with Canadian securities regulators and the U.S. Securities and Exchange Commission. Although the Company has attempted to identify important factors that could cause actual results to differ materially from those contained in the forward-looking information or implied by forward-looking information, there may be other factors that cause results not to be as anticipated, estimated or intended. There can be no assurance that forward-looking information and statements will prove to be accurate, as actual results and future events could differ materially from those anticipated, estimated or intended. Accordingly, readers should not place undue reliance on forward-looking statements or information. The Company undertakes no obligation to update or reissue forward-looking information as a result of new information or events except as required by applicable securities laws. Technical Information Certain scientific and technical information in this presentation is based on information prepared under the Joint Ore Reserves Committee (JORC) 2004 or 2012 code, the terms Inferred Mineral Resources, Indicated Mineral Resources, Measured Mineral Resources, Ore Reserves, Proved Ore Reserves and Probable Ore Reserves are substantially similar to the terms Inferred Mineral Resources, Indicated Mineral Resources, Measured Mineral Resources, Mineral Reserves, Proven Mineral Reserves and Probable Mineral Reserves, respectively, used in Canadian National Instrument 43-101 (“NI 43-101”). Darcy Hirsekorn, the Company's Chief Technical Officer, has supervised the preparation of and reviewed the technical information contained in this presentation. Darcy holds a B.Sc. in Geology from the University of Saskatchewan, is a qualified person as defined in National Instrument 43-101 and is registered as a professional geoscientist in Saskatchewan. External Information Where this presentation quotes any information or statistics from any external source, it should not be interpreted that the Company has adopted or endorsed such information or statistics as being accurate. The Company also advises investors that some of the information presented herein is based on or derived from statements by third parties, has not been independently verified by or on behalf of the Company, and that no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, completeness or correctness of this information or any other information or opinions contained herein, for any purpose whatsoever. No Investment Advice This presentation is not, and is not intended to be, an advertisement, prospectus or offering memorandum, and is made available on the express understanding that it does not contain all information that may be required to evaluate, and will not be used by readers in connection with, the purchase of or investment in any securities of any entity. This presentation accordingly should not be treated as giving investment advice and is not intended to form the basis of any investment decision. It does not, and is not intended to, constitute or form part of, and should not be construed as, any recommendation or commitment by URC or any of its directors, officers, employees, direct or indirect shareholders, agents, affiliates, advisors or any other person, or as an offer or invitation for the sale or purchase of, or a solicitation of an offer to purchase, subscribe for or otherwise acquire, any securities, businesses and/or assets of any entity, nor shall it or any part of it be relied upon in connection with or act as any inducement to enter into any contract or commitment or investment decision whatsoever. Readers should not construe the contents of this presentation as legal, tax, regulatory, financial or accounting advice and are urged to consult with their own advisers in relation to such matters. U.S. Non-Solicitation This presentation is not an offer of securities for sale in the United States and is not an offer to sell or solicitation of an offer to buy any securities of URC nor shall it form the basis of, or be relied upon in connection with any contract for purchase or subscription. The securities of URC have not been and will not be registered under the Securities Act or the securities laws of any state and may not be offered or sold in the United States absent registration or pursuant to an applicable exemption therefrom.

3

INVESTMENT HIGHLIGHTS

▪ URC is the first company to apply the successful royalty and streaming business model

First Mover Advantage exclusively to the uranium sector

C$127M ▪ Strong balance sheet, which positions it to capitalize on accretive uranium royalty and

Liquid Assets streaming acquisition opportunities

▪ Through opportunistic market purchases, the supply stream with CGN Global, and its

Physical Uranium

approximate 3.8% stake in London-listed Yellow Cake plc, URC holds interests in physical

Ownership uranium, acquired at cyclical lows

▪ Portfolio includes interests on 15 development, advanced, permitted and past-producing

Large & Diversified

uranium projects in multiple jurisdictions, including royalties on the world class McArthur

Royalty Portfolio River and Cigar Lake mines

▪ Management and board possess decades of uranium industry experience, including senior

Expertise executive and advisory roles to prominent companies and governments in the sector

URC is well positioned to take advantage of current market conditions as a provider of

alternative capital to the uranium sector

4

MANAGEMENT & BOARD

Management Board of Directors

AMIR ADNANI (Chairman)

SCOTT MELBYE (President, CEO & Director)

• Entrepreneur and Founder, President & CEO of Uranium Energy Corp

• Uranium industry veteran with 37 years experience including Executive (UEC: NYSE American)

roles with Cameco, Uranium One & Uranium Participation Corp. • Chairman of GoldMining Inc. (GOLD: TSX, GLDG: NYSE American)

• Former Strategic Advisor to Kazatomprom • Based in Vancouver

• Executive VP of UEC

• Based in Denver

VINA PATEL (Director)

• 18 years experience raising capital from U.K. and European institutional investors

DARCY HIRSEKORN (Chief Technical officer) in mining and exploration equities, including uranium companies

• Formerly: Head of London Institutional Sales for Haywood Securities

• Professional geoscientist with over 25 years experience at Cameco and • Based in London, U.K.

Uranium Royalty Corp.

• Part of exploration groups that outlined over 200Mlbs of uranium

• Based in Saskatoon NEIL GREGSON (Director)

• Qualified mining engineer with over 30 years experience in asset management

in the resources sector

• Formerly: Portfolio Manager J.P. Morgan Asset Management Global Equities Team

JOSEPHINE MAN (Chief Financial Officer) based in London; Senior Portfolio Manager, Natural Resources of CQS Asset

Management; Head of Emerging Markets of Credit Suisse Asset Management

• Former partner at Ernst & Young LLP • Based in London, U.K.

• Over 20 years experience working with public companies

primary in the mining industry

• Based in Vancouver JOHN GRIFFITH (Director)

• 30 years experience in financial services sector in 3 continents, including 26 years

of global investment banking expertise

• Formerly: Managing Director and the Head of Americas

Strategic Partner Metals & Mining Investment Banking for Bank of America

• Based in South Carolina

URANIUM ENERGY CORP

(UEC: NYSE American)

▪ Initial shareholder

▪ Strategic partner, ongoing technical and

operational support

5

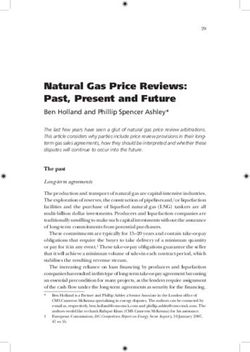

URANIUM SPOT PRICE REACHES ELEVEN-YEAR HIGH

Spot Daily Long Term

$138.00

$140

$120

$70.00

US $/lb U308

$100

2011:

Fukushima $50.25

$80 event

$52.00

$60

$40

Financial Crisis

$20

Nov 2016: $17.75/lb

12 year low

$0

Jun 2006 Jun 2010 Jun 2014 Jun 2018 Jun 2022

Source: TradeTech; UxC, LLC: www.uxc.com June 7, 2022

6

CAPITALIZATION & OWNERSHIP PROFILE

SHARE STRUCTURE RECENT ACTIVITY

Shares Outstanding 94.5 Million US$3.20

UROY: Nasdaq

Avg. Daily Vol.: 691,936

Warrants 17.6 Million(1) C$4.02

URC : TSX-V

Avg. Daily Vol. (3-mo): 204,676

Options 0.8 Million URC.WT : TSX-V C$2.17

Market Cap C$380 Million

Fully Diluted(2) 112.9 Million As of Jun 7, 2022

KEY SHAREHOLDERS Marketable Securities and C$127 Million

Physical Holdings(3)

Uranium Energy Corp. Extract Capital Listed Securities 7.0 Million shares (~3.8%) in

Yellow Cake plc

Altius Resources Inc. Rick Rule

ANALYST COVERAGE

Mega Uranium Ltd. Sprott Global

Marin Katusa Commodity Capital Katie Lachapelle

KCR Fund Heiko Ihle

Gordon Lawson

(1) All, except 0.1 million common share purchase warrants, are trading on the TSX-V Exchange; $35M cash to be received should all warrants are exercised

(2) Refer to the latest Company’s filing for the quarter ended January 31, 2022

(3) Represents inventory holdings of 1,548,068 pounds U3O8 at a weighted average cost of US$42.20 per pound and marketable securities measured at fair value on June 9, 2022

OUR STRATEGY: 7 7

BUILDING A DIVERSIFIED PORTFOLIO

Geographical

Multiple countries

Counterparty

Range of market capitalization

Various Stages of Development

Near, Medium, and Long-term Assets

Invest Across the Cost Curve

Maximizes leverage to uranium recovery

Physical Ownership

Direct Exposure to Current Spot Price

URC’s Diversified Approach is Well Suited to Uranium

8 URC's Portfolio

9 STRONG COUNTERPARTIES/OPERATORS Counterparties and Operators include many of the sector’s leading growth-oriented uranium companies

10

GLOBAL DIVERSIFIED ASSET PORTFOLIO

Africa

Note: Physical storage of Yellow Cake material is provided at Cameco’s

Blind River facility11

STRATEGIC PARTNERSHIP –

YELLOW CAKE PLC INVESTMENT

Supply Agreement with Kazatomprom Blind River Uranium Storage Facility

▪ Yellow Cake has a long-term supply agreement with Kazatomprom, the world's largest

uranium producer

Overview

▪ The supply agreement enables Yellow Cake to purchase up to US$1.07bn (including

existing purchases) of uranium from Kazatomprom over a 10-year period

▪ Yellow Cake's U₃O₈ current holdings as at May 20, 2022 was 17.86Mlbs pursuant to

YCA’s Regulatory News dated May 20, 2022.

Purchasing

▪ Pursuant to YCA’s Regulatory News dated May 20, 2022, 0.95Mlbs of U₃O₈ will be

purchased from Kazatomprom JSC for delivery by June 2022.

URC Investment in Yellow Cake

Ownership: Approximately 3.8%

Rights ▪ URC has the option to acquire up to US$31.25M (US$2.5M – US$10M per year) of uranium between Jan 2019 – Jan 2028

▪ URC has an option to participate in any and all future uranium royalty and stream transactions Yellow Cake pursues on a 50:50 basis

▪ URC and Yellow Cake also plan to collaborate on future opportunities involving physical uranium

▪ In the event URC exceeds 10% ownership, URC has the right to nominate one director to the Yellow Cake Board, currently have observer rights

Source: Yellow Cake Plc12

STRATEGIC ASSETS –

PHYSICAL URANIUM INVESTMENT

▪ Increased total physical uranium concentrate inventory to 1,548,068 pounds at a weighted average

cost of US$42.20 per pound(1)

▪ Approx. US$77.8M in market value at $50.25/lb spot price as of June 7, 2022 (~US$12.46M in net

realizable value since the date of acquisition)

▪ Stored at Cameco’s Blind River facility in Ontario, Canada

▪ Recently entered into a Supply Stream Agreement with CGN Global

Uranium Limited to purchase 500,000 pounds of U308 for delivery at

Cameco from 2023 through 2025 at a weighted average price of

$47.71 per pound (fixed prices and delivery dates)(2).

(1) See URC news release dated Mar 28, 2022 (2) See URC news release dated Dec 2, 2021ROYALTY PORTFOLIO 13

World Class Athabasca Basin Royalties

McArthur River Cigar Lake/Waterbury Roughrider

Royalty 1% GOR on 9% share(1) 20% NPI on 3.75% share(2) 1.97% NSR

Location Saskatchewan, Canada Saskatchewan, Canada Saskatchewan, Canada

Owner / Operator Cameco Corporation Cameco Corporation Rio Tinto Canada

Orebody Type Unconformity Unconformity Unconformity

Mine Type Underground Underground Underground

Stage Production Resuming In Production Development

▪ Along with the Key Lake Mill, licensed to produce 25 ▪ Licensed to produce 18 Mlbs per year ▪ Roughrider was discovered by Hathor Exploration in 2008

Mlbs per year ▪ Historical production of 105 Mlbs as at December 31, ▪ In 2011, Cameco made a hostile bid for Hathor

Overview

▪ Total historical packaged production of 325.4 Mlbs U3O8. 2021 ▪ Rio ultimately outbid Cameco and acquired Hathor for

▪ Mine expected to resume production in 2022 with ▪ Production resumed in April of 2021 C$654M

anticipated production of 5 Mlbs U3O8.

Reserves U3O8 (Mlbs) (3)

Proven 328.9 95.0 17.2

Probable 65.1 57.4 40.7

Resources U3O8 (Mlbs) (3,4)

Measured 5.3 4.5

Indicated 3.7 99.3 17.2(5)

Inferred 2.6 22.9 40.7(5)

(1) The royalty acquired by URC does not apply to the entirety of the project but covers 100% of the reserves and resources attributed to the McArthur River project.

(2) The NPI percentage will adjust to 10% in the future upon production of 200 million pounds from the combined royalty lands of the Dawn Lake and Waterbury Lake / Cigar Lake Projects. As a profit-based interest, this royalty will begin to generate revenue after cumulative expense accounts, including development costs,

are exhausted. The royalty acquired by URC does not apply to the entirety of the project but covers 100% of the reserves and resources attributed to the Cigar Lake/Waterbury project.

(3) Cameco Corporation – Management’s Discussion and Analysis for the year ended December 31, 2021, copies of which are available under Cameco's profile at www.sedar.com

(4) Mineral resources do not have demonstrated economic viability and do not include mineral reserves

(5) The estimates for Roughrider based on the 2011 PEA Technical report are historical in nature and are not being treated as current resources or reserves by URC as a qualified person has not done sufficient work on behalf of URC to classify such historical estimates as current mineral resources or reserves. The disclosure of

these historical estimates have been included herein as URC believes that it provides an indication of the potential for the properties underlying its royaltiesROYALTY PORTFOLIO 14

Athabasca Basin Royalties

Dawn Lake Option Russell Lake

Royalty 20% NPI on 7.5% share(1) 1.97% NSR

Location Saskatchewan, Canada Saskatchewan, Canada

Owner / Operator Cameco Corporation Skyharbour Resources

Orebody Type Unconformity Unconformity

Mine Type Open Pit/Underground N/A

Stage Development Early Exploration

▪ Resources outlined in table below stated by Cameco for the Tamarack deposit ▪ Exploration Project Operated by Skyharbour, partnered with Rio Tinto

▪ Large mature project with multiple historical deposits including Dawn Lake, La ▪ Comprised of the Russell Lake and Russell South projects

Rocque Lake, Natona Bay, and Thorburn Lake ▪ 15 - 60 km from Key Lake Mill

Overview ▪ Approx. 47,000 hectares of royalty coverage on highly prospective ground ▪ Approx. 72,000 hectares of royalty coverage on highly prospective ground

Resources U3O8 (Mlbs) (2,3)

Indicated 17.9

Inferred 1.0

(1) The NPI percentage will adjust to 10% in the future upon production of 200 million pounds from the combined royalty lands of the Dawn Lake and Waterbury Lake / Cigar Lake Projects. As a profit-based interest, this royalty will begin to generate revenue after cumulative

expense accounts, including development costs, are exhausted. The royalty option acquired by URC does not apply to the entirety of the project but covers 100% of the reserves and resources attributed to the Dawn Lake project.

(2) Cameco Corporation – Management’s Discussion and Analysis for the year ended December 31, 2021, copies of which are available under Cameco's profile at www.sedar.com

(3) Mineral resources do not have demonstrated economic viability and do not include mineral reservesROYALTY PORTFOLIO 15

15

World Class Athabasca Basin Royalties

McArthur River (1% GOR on 9% share)(1)

▪ The mine is currently owned by a joint venture between Cameco (69.805%) and

Orano (30.195%)

▪ Along with the Key Lake Mill, licensed to produce 25 Mlbs per year

▪ Historical production of 325.4 Mlbs since it went into production in 1999

Overview(1) ▪ In 2018, Cameco disclosed that the operation was put on care and maintenance

due to weak uranium market conditions.

▪ In 2022, Cameco announced the intention to begin restart of the operation,

projecting up to 5.0 Mlbs of production in 2022 on a 100% basis and a plan to

produce 15 Mlbs per year by 2024.

Reserves(2) Project Location

Tonnage Grade U3O8

Category (kt) (% U3O8) (Mlbs)

Proven 2,140 6.97% 328.9

Probable 575.1 5.13% 65.1

Resources(2,3.4)

Tonnage Grade U3O8

Category (kt) (% U3O8) (Mlbs)

Measured 91.7 2.63% 5.3

Indicated 74.5 2.26% 3.7

Inferred 41.0 2.85% 2.6

(1) The royalty acquired by URC does not apply to the entirety of the project area but covers 100% of the reserves and resources attributed to the McArthur River project.

(2) Cameco Corporation – Management’s Discussion and Analysis for the year ended December 31, 2021, copies of which are available under Cameco's profile at www.sedar.com

(3) Mineral resources do not have demonstrated economic viability

(4) Mineral resources do not include mineral reservesROYALTY PORTFOLIO 16

16

World Class Athabasca Basin Royalties

Cigar Lake/Waterbury (20% NPI on 3.75% share)(1)

▪ The Cigar Lake Joint Venture partners are currently Cameco (54.547%), Orano

Canada Inc. (40.453%), and TEPCO Resources Inc. (5%)

▪ Licensed to produce 18 Mlbs per year

▪ Historical production of 105 Mlbs as at December 31, 2021

Overview ▪ Production resumed in April of 2021, with first shipments of ore to McClean

Lake at the end of April

▪ Total production in 2021 of 12.2 Mlbs on a 100% basis

▪ Operation expected to produce 15 Mlbs of U3O8 in 2022

Reserves(2) Project Location

Tonnage Grade U3O8

Category (kt) (% U3O8) (Mlbs)

Proven 271.0 15.90% 95.0

Probable 177.5 14.67% 57.4

Resources(2,3,4)

Tonnage Grade U3O8

Category (kt) (% U3O8) (Mlbs)

Measured 26.8 7.55% 4.5

Indicated 313.3 14.37% 99.3

Inferred 186.4 5.58 22.9

(1) The NPI percentage will adjust to 10% in the future upon production of 200 million pounds from the combined royalty lands of the Dawn Lake and Waterbury Lake / Cigar Lake Projects. As a profit-based interest, this royalty will begin to generate revenue

after cumulative expense accounts, including development costs, are exhausted. The royalty acquired by URC does not apply to the entirety of the project but covers 100% of the reserves and resources attributed to the Cigar Lake/Waterbury project.

(2) Cameco Corporation – Management’s Discussion and Analysis for the year ended December 31, 2021, copies of which are available under Cameco's profile at www.sedar.com

(3) Mineral resources do not have demonstrated economic viability

(4) Mineral resources do not include mineral reservesROYALTY PORTFOLIO 17

US ISR Royalties

Reno Creek(1,3) Lance(1) Dewey-Burdock(1) Church Rock

Royalty 0.5% NPI 1% GRR / 4% GRR 30% NPI 4% NSR

Location Wyoming Wyoming South Dakota New Mexico

Geological District Powder River Basin Powder River Basin Black Hills Uplift Grants Mineral Belt

Owner / Operator Uranium Energy Corp. Peninsula enCore Energy Laramide Resources

Orebody Type Sandstone-Hosted Sandstone-Hosted Sandstone-Hosted Sandstone-Hosted

Stage Development Production Idled Development Development

Resources U3O8 (Mlbs) (2,4,5,6)

Measured 12.9 3.7 14.3

Indicated 13.1 12.1 2.8

Inferred 1.5 37.8 0.7 50.8

▪ Project is fully permitted and construction ▪ 1% GRR covers the entirety of current Ross, ▪ Recent PEA report estimates a post-tax NPV ▪ Laramide holds several regulatory

ready Kendrick and Barber production areas at an 8% discount of US$147.5M at a clearances for the project

Overview ▪ With UEC’s acquisition of Uranium One ▪ 4% GRR royalty covers a portion of the constant US$55 price per pound ▪ Project currently undergoing additional field

Americas, is now part of UEC’s planned Kendrick and Barber production areas ▪ Direct Operating Costs of $10.46 per pound work and studies to lead to an updated PEA

“Hub and Spoke” production strategy ▪ Production currently suspended as project produced, excluding royalties, severance and report

centered on the Irigaray Central Processing undergoes transition to low-Ph mining conservation taxes

Plant in Wyoming. methodology. Updated Feasibility report in

progress.

(1) Reno Creek, Dewey-Burdock, and the 4% GRR royalty on Lance do not apply to the entire project area covered by this estimate

(2) Reno Creek resources sourced from technical report titled "Technical Report and Audit of Resources of the Reno Creek ISR Project, Campbell County, Wyoming, USA" dated December 31, 2018 and authored by Robert E. Cameron, Ph.D., MMSA, and Robert Maxwell, CPG, AIPG and made in

accordance with NI 43-101,

(3) Uranium Energy Corporation S-K 1300 Technical Report Summary dated April 5, 2022

(4) Lance resources sourced from Peninsula Energy Limited September 30, 2021 quarterly activities report and made in accordance with JORC.

(5) Dewey-Burdock resources sourced the technical report titled "NI 43-101 Technical Report, Preliminary Economic Assessment, Dewey-Burdock Uranium ISR Project, South Dakota, U.S.A.", with an effective date of December 3, 2019, prepared for Azarga Uranium Corp. and authored by Steve

Cutler, P.G. and Douglass H. Graves, P.E. and made in accordance with NI 43-101,

(6) Church Rock resources sourced from the technical report titled "Technical Report on the Church Rock Uranium Project, McKinley County, State of New Mexico, U.S.A." with an effective date of September 30, 2017, prepared for Laramide Resources Ltd. and authored by Mark B. Mathisen,

C.P.G. and made in accordance with NI 43-101,ROYALTY PORTFOLIO 18

Global Conventional Royalties

Langer Heinrich(1) Michelin(3.4)

Past Producer Ready for Restart Large Resource in Top Jurisdiction

Royalty A$.012/kg U3O8 Production Royalty 2% GRR

Location Erongo, Namibia Labrador, Canada

Owner / Operator Paladin Energy/CNNC Paladin Energy

Orebody Type Surficial Calcrete Metasomatic

Mine Type Open Pit Open Pit/Underground

Stage Production Idled Development

▪ Paladin releases updated Restart Plan on November 4, 2021 ▪ Historical PEA issues by Fronteer in 2009

▪ Restart capital re-affirmed at US$81M ▪ Paladin acquired Michelin in 2011 for C$260.9M

Overview

▪ 17-year mine life with production target of 77.4 Mlbs. U3O8 ▪ Low technical risk project in a premier uranium jurisdiction

▪ Targeting production to resume in CY2024

Resources U3O8 (Mlbs) (2,3)

Measured 100.2 38.0

Indicated 19.5 67.6

Inferred 8.4 22.1

(1) Data based on ASX release from November 4, 2021 titled “Langer Heinrich Restart Plan Update, Mineral Resource and Ore Reserve Update” and an ASX release from April 1, 2022 titled “Successful Completion of a A$200 million Placement”

Resources as of November 4, 2021, prepared under JORC 2012. Measured and Indicated Resources are inclusive of those Mineral Resources modified to produce the Ore Reserves and includes stockpiled material as Measured resources. Further details

available in the company’s ASX announcement.

(2) This PEA is not being treated as current by URC.

(3) Sourced from Paladin Energy Ltd August 28, 2020 Annual Report. Resources were estimated in accordance with JORC 2012 with cut-off grades ranging between 0.2% - 0.5% and with an assumed uranium price of US$85/lbROYALTY PORTFOLIO 19

US Conventional Royalties

Anderson(1) Slick-Rock(2) Workman Creek Roca Honda(4,5)

Royalty 1% NSR 1% NSR 1% NSR 4% GRR

Location Arizona Colorado Arizona New Mexico

Geological District Date Creek Basin Grants Mineral Belt Sierra Ancha/Apache Basin Grants Mineral Belt

Owner / Operator Uranium Energy Corp. Anfield Energy Uranium Energy Corp. Energy Fuels

Orebody Type Sandstone-Hosted Sandstone-Hosted Sandstone-Hosted Sandstone-Hosted

Stage Advanced Advanced Development Development

Resources U3O8 (Mlbs) (1,2,3,5)

Indicated 17.0

Inferred 12.0 11.6 5.5

▪ Preliminary economic assessment disclosed a ▪ Preliminary economic assessment disclosed a ▪ The property comes with extensive historic ▪ The Section 17 area has a partially developed

Overview post-tax NPV(10%) of US$101.1M utilizing a post-tax NPV(10%) of US$31.9M utilizing a data consisting of 400 exploration and vertical mine shaft and haul road

fixed US$65 per pound uranium price model fixed US$60 per pound uranium price model development holes, geological mapping, ▪ Energy Fuels plans to integrate the Section 17

▪ Average life of mine operating cost of regional and detailed geochemical, area covered by the royalty into the company’s

US$30.68 per contained pound. petrographic, mineralogical paragenetic and permitting efforts

metallurgical studies

(1) Anderson resource sourced from the the technical report titled "Technical Report and PEA on the Anderson Uranium Project, Yavapai County, Arizona, USA", with an effective date of July 6, 2014, prepared for Uranium Energy Corp. and authored by Douglas Beahm, PE, PG,

Terence P. McNulty, D. Sc., P.E., Bruce Davis, FAusIMM, and Robert Sim, P.Geo. estimated in accordance with NI 43-101.

(2) Slick Rock resources sourced from the technical report titled "Technical Report Preliminary Economic Assessment, Slick Rock Project Uranium / Vanadium Deposit, San Miguel County, Southwest Colorado, USA" with an effective date of April 8, 2014, prepared for Uranium

Resources Corp. and authored by Douglas Beahm, PE, PG, Bruce Davis, FAusIMM, and Robert Sim, P. Geo. estimated in accordance with NI 43-101;

(3) Workman Creek resources sourced from the technical report titled "Technical Report on the Workman Creek Project, Central Arizona", with an effective date of March 2, 2012, prepared for Uranium Energy Corp. and authored by Neil G. McCallum, B.Sc, P.Geo., and G.H.

Giroux, MASc, P.Eng. estimated in accordance with NI 43-101.

(4) The Roca Honda royalty only applies to Section 17 of the project. The Roca Honda Technical Report with an effective date of October 27, 2016 included a preliminary economic assessment on the Roca Honda project, the assessment did not include the area covered by the Roca

Honda Royalty.

(5) Energy Fuels Form10-K for the fiscal year ended December 31, 202020 Royalty Model & Our Approach

21

21

URC OFFERS PARTNERSHIP “VALUE-ADDED” RELATIONSHIPS WITH

PORTFOLIO COUNTERPARTIES

URC is vested in the success of its portfolio counterparties

Thorough due diligence and

Ability to provide selection process offers third party

non-dilutive Project Financing endorsement to projects in

the URC portfolio

Experienced URC team offers

uranium market and

URC capital markets presence

development insights

provides expanded visibility

to counterparty management

and Boards22

THE RIGHT MODEL FOR AN IMPROVING MARKET

Operating Physical Funds

Royalty Companies vs. Operators Uranium ETF

Companies

Exposure to Uranium Price ✓ ✓ ✓ ✓

Fixed Operating Costs ✓ ✓ ✓

No Development or Sustaining

Capital Costs

✓ ✓ ✓

Exploration & Expansion Upside

Without the Associated Costs

✓

Diversified Asset Portfolio ✓ ✓ ✓

Ability to Grow Without Increased

Management

✓ ✓ ✓23

OUR STRATEGY: ROYALTY OPPORTUNITY

▪ To date URC’s strategy has been primarily ▪ Large number ▪ Focused

of active discussions

focused on acquiring existing royalties dialogues with priority

targets

▪ Typically for

shares and/or ▪ Typically cash

cash transaction

▪ The next wave of acquisitions are

anticipated to focus on new royalties,

streams, additional physical uranium, and

other uranium interests

▪ On a case by case basis

URC has a flexible strategy and desire to be a partner in growth24 Uranium Market Overview

25 Nuclear Energy Clean, Safe, Reliable & Economic Perfect Compliment to Renewable Wind and Solar Provides Hedge Against High Natural Gas Prices Saves Lives and Improves Quality of Life

26

26

NUCLEAR POWER = CARBON FREE - CLEAN ENERGY

55% OF AMERICA’S CLEAN ENERGY

The only low

carbon energy

source that

provides scalable,

24-7 baseload

power

Source: World Nuclear Association – Harmony Program27

27

NUCLEAR POWER = SAFEST FORM OF ELECTRICITY GENERATION

Source: World Nuclear Association – Harmony Program

https://world-nuclear.org/our-association/what-we-do/the-harmony-programme.aspx28

2021 POLAR VORTEX – NUCLEAR RELIABILITY AT 95%

28

CAPACITY FACTOR BY ENERGY SOURCE IN 2020

Nuclear 92.5%

Geothermal 74.3%

Natural Gas 56.6%

Hydropower 41.5%

Coal 40.2%

Wind 35.4%

Solar 24.9%

Source: U.S. Energy Information Administration29

29

NUCLEAR POWER = LOWEST LEVELIZED COST OF ELECTRICITY

FOR EXTENDED LIFE PLANTS VS ANY OTHER SOURCE

Most nuclear plants in the U.S. have or will extend their operational lives by at least 20 - 40 years

Projected Costs of Generating Electricity, 2020 Edition, International Energy Agency and Nuclear Energy Agency30

30

Global Approval for Nuclear Power

Continues to Grow

EU Taxonomy Includes Nuclear

as an Environmentally

Sustainable Investment

Source: U.S. Energy Information Administration; Orano Group31

31

SUPPORT FOR NUCLEAR ENERGY IS STRONG AND INCREASING

Favorability to Nuclear Energy 1983-2021

Overall, do you strongly favor, somewhat favor, somewhat oppose the use of nuclear

energy as one of the ways to provide electricity in the United States?

Source: NuclearNewswire – ANS; Nuclearmatters.com/jobs

https://www.ans.org/news/article-2974/support-for-nuclear-energy-grows-with-climate-change-concerns/32

32

ROBUST NUCLEAR POWER GROWTH

Global investments in nuclear energy generation are projected to average well over $100 billion per year

through mid-century8

441 53 63 3.1%

Operable Reactors Units Under New Reactors Connected CAGR Uranium Demand Growth

Worldwide Construction since 2013 Expected (2020-2040)1

CHINA approves 6 new reactors9 JAPAN 33 operable reactors. Energy U.A.E. completed 3 reactors; 1 unit U.K. upgrading nuclear fleet to new

and is planning for 70 GW of Plan targeting 20-22% nuclear under construction3 advanced reactors - wants 25% of its

installed nuclear capacity by 2025, power, nuclear deemed essential to electricity from nuclear power, signals a

at least 150 new reactors in the next achieve net-zero target by 2050. The RUSSIA is building 36 reactors in significant shift in the country’s energy

15 years2 majority of Japanese support China, India, Bangladesh, Turkey, mix

restarting idled nuclear reactors for Egypt, Iran, Finland, Belarus, Slovakia,

SOUTH KOREA incoming the first time in over a decade6 Armenia, Uzbekistan and Hungary FRANCE to build 6-14 new reactors4

government will reverse the

country’s nuclear phaseout plan7 INDIA plans for 21 new reactors by FINLAND - New survey from Finnish U.S. has maintained a 20% market share

2031; 10 new plants over next 3 Energy reveals that support for nuclear for 30 years with power uprates and

years5 is higher than ever10 efficiency = to 32 new reactors –

A Stealth Growth Story!

Source: IAEA PRIS Jun 7, 2022; (1) WNA Fuel Report Sep 2021; (2) South China Morning Post Mar 24, 2022; Bloomberg Green Nov 2, 2021; (3) WNN; NEI Dec 2020, Mar 2021 (4) France 24, Feb 10, 2022 (5) Bloomberg Mar 28, 2022 (6) Power-Technology.com

Mar 2022 (7) Financial Times Apr 13, 2022 (8) NEI.org - United Nations IPCC Report, Apr 2022 (9) AsiaNikkei.com, Apr 22, 2022 (10) TVO.FI May 13, 202233 REACTOR DEMAND SIGNIFICANTLY EXCEEDS 33 PRIMARY PRODUCTION U.S. Uranium Production Needed to Fill Gap 2022 Demand expected = 205 M lbs. 2022 Production expected = 134 M lbs. 2022 Production gap is 71 M lbs. below requirements Cumulative gap through 2029 is 305 M lbs., 440 M lbs. by 2032 Source: UxC Market Outlook Q2 2022

34

34

URANIUM SUPPLY – ACCELERATED REBALANCING

Restricted Primary Supply 2016 – 2035

Mine Curtailments, Depletion and Speculative Interest Accelerating Market Rebalancing

Source: TradeTech May 31, 202135 URANIUM DEMAND Need for New Production – Beyond Existing Mines ▪ Inventory Overhang Drawing Down ▪ Uranium Price Too Low to Stimulate New Production ▪ Within the Permitting and Development Lead Times to Bring On New Mines Source: TradeTech November 2021

36

UTILITY PROCUREMENT CYCLE: 36

Old Contracts Rolling Off… New Contracts Need to be Signed

1.3 Billion Pounds of Contracting needed by 2035!

Utility Uncommitted Demand Historic Long-Term Contracting

Source: UxC Market Outlook Q1 202237

37

U.S. URANIUM MINING & NUCLEAR ENERGY

Enjoying Historic Support in Washington D.C.

▪ Bi-Partisan Support for Nuclear Energy – ▪ The U.S. has set a goal to reach 100% carbon pollution-free

All-time high in public support with Democrat electricity by 2035 – Nuclear Energy “Absolutely Essential”

and Republican voters now equally in favor of (US Energy Secretary Jennifer Granholm)

nuclear energy.

▪ World’s Largest Nuclear Reactor

▪ Biden Administration wants Congressional

Fleet Over Reliance on Imports

approval allowing DOE to purchase $4.3B of

Prompts National Security

domestic uranium, conversion and enrichment -

Concerns – No U.S. Production

end U.S. reliance on nuclear fuel from Russia

and support a U.S. supply chain for existing and ▪ Nuclear Fuel Working Group

new advanced reactors. The $1.5B Strategic Develops Strategy to Restore

Uranium Reserve would likely be rolled into the America’s Nuclear Fuel Supply

new program Chain & Global Market Position

▪ Bipartisan Infrastructure Bill Signed Into ▪ DOC Amends Russian

Law that provides a $6B nuclear credit program Suspension Agreement to Limit

for qualifying nuclear plants with priority given and Reduce Imports from Russia –

to reactors using uranium produced in the United up to 75% Compared to Prior RSA

States38 INVESTMENT SUMMARY URC OFFERS INVESTORS: ▪ First mover pure-play uranium royalty exposure ▪ Royalty portfolio covering array of development projects in key jurisdictions with the right partners ▪ Emerging need for new production creates mutually beneficial royalty financing opportunities ▪ Team with extensive uranium industry experience, knowledge and access ▪ Nuclear energy gaining broader acceptance in a carbon-constrained world ▪ Robust uranium demand and curtailed mine production have rebalanced market fundamentals ▪ $1.5B for a Strategic Uranium Reserve over 10 years for U.S. domestic uranium and conversion ($75M in Appropriations expected for fiscal 2022) ▪ Market Fundamentals continue to improve with a growing deficit between primary production and reactor requirements

39 Appendix

40

40

ROYALTY AND STREAMS 101

“Royalties” are a payment to a royalty holder by a property owner, or project operator, and is typically based on a

percentage of the minerals produced and the revenues or profits generated from the property

“Streams” are physical commodity purchase agreements where, in exchange for an upfront deposit and ongoing

payments for metal delivered, the holder purchases all or a portion of one or more metals produced from a mine, at a

preset price.

Up-front payment for Operating

Royalty Company Company

royalty or stream

Payment for stream

delivery Operating

Royalty Company Company

Royalty or stream

delivery41

TYPES OF ROYALTIES

▪ Based on the total revenue stream from the sale of production from the property, which can sometimes include

Gross Overriding Royalty

deductions.

(GOR)

▪ URC GOR royalties include McArthur River

▪ Based on the total revenue stream from the sale of production from the property, which can sometimes include

Gross Revenue Royalty

deductions.

(GRR) ▪ URC GRR royalties include Michelin, Lance, Roca Honda, and the option on Diabase.

Net Profit Interest ▪ Based on the profit realized after deducting costs related to production.

(NPI) ▪ URC has a NPI royalty on Reno Creek, Dewey-Burdock, Cigar Lake, and the option on Dawn Lake

Net Smelter Returns ▪ Based on the value of production or net proceeds received by the operator from a smelter or refinery.

(NSR) ▪ URC NSR royalties include Roughrider, Church Rock, Anderson, Slick Rock, and Workman Creek.

Production Royalty ▪ Based on metal produced, often at a predetermined fixed price.

(PR) ▪ URC has a PR on the Langer Heinrich Project.

▪ Streams are distinct from royalties. They are metal purchase agreements where, in exchange for an upfront

deposit and ongoing payments for metal delivered, the holder purchases all or a portion of one or more metals

Metal Streams produced from a mine, at a preset price.

▪ URC does not currently hold any streaming interests. However, part of its strategy includes the potential

acquisition of streams on primary uranium and uranium by-product assets.

▪ Widely used in the global mining sector.42

UROY: NASDAQ | URC: TSX-V

The First and Only Pure Play Uranium Royalty Company

Uranium Royalty Corp. Corporate Office: President & CEO:

Toll Free: 1.855.396.8222 1030 West Georgia Street, Scott Melbye

Phone: 604.396.8222 Suite 1830, Vancouver,

Email: Info@UraniumRoyalty.com BC, V6E 2Y3 Investor Relations:

www.UraniumRoyalty.com Canada Phone: 604.396.8222

Email: Info@UraniumRoyalty.comYou can also read