Quarterly Market Update - Fidelity Institutional Asset ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

LEADERSHIP SERIES FOURTH QUARTER 2019 Quarterly Market Update PRIMARY CONTRIBUTORS Lisa Emsbo-Mattingly Jake Weinstein, CFA Director of Asset Allocation Research Research Analyst, Asset Allocation Research Dirk Hofschire, CFA Ryan Carrigan, CFA SVP, Asset Allocation Research Research Analyst, Asset Allocation Research

Table of Contents 1. Market Summary 2. Economy/Macro Backdrop 3. Asset Markets 4. Long-Term Themes

Market Summary

Global Monetary Easing Amid Trade and Growth Headwinds

SUMMARY

During Q3, the Federal Reserve and other central banks eased monetary policy in an effort to counter flagging

global-growth momentum. However, further escalation of the U.S.-China trade conflict continued to weigh on

confidence, and it remains unclear whether monetary easing alone is sufficient to catalyze economic

acceleration. The mature global business cycle continues to warrant smaller cyclical allocation tilts.

MACRO ASSET MARKETS

Q3 2019 • Monetary policymakers lowered interest rates, • Government bond yields continued to drop, and

but global growth remained tepid. global equity prices were range-bound.

• The U.S. is firmly in the late-cycle phase. • Late-cycle phases typically exhibit higher

OUTLOOK

volatility along with a more asymmetric risk-

• Improvement in China’s economy has stalled. return profile.

• Global policy support remains insufficient to • Wide dispersion of outcomes warrants smaller

reaccelerate global growth. allocation tilts than earlier in the cycle.

• The global liquidity backdrop remains • Prioritize diversification amid significant

challenged despite Fed rate cuts. uncertainty.

• U.S.-China trade policy uncertainty is an

ongoing drag on corporate confidence.

Diversification does not ensure a profit or guarantee against a loss.

4Less Risky Assets Led During Mixed Quarter of Performance

SUMMARY

With lackluster global growth and increased policy uncertainty, the continued drop in government bond yields

during Q3 spurred gains across less risky bond categories, gold, and interest rate-sensitive equity sectors such

as real estate investment trusts (REITs). Year-to-date returns for all major asset categories remained in positive

territory, with U.S. stock and bond markets registering strong gains.

Q3 2019 (%) YTD (%) Q3 2019 (%) YTD (%)

Real Estate Stocks 7.8 27.0 High Yield Bonds 1.2 11.5

Long Government & Credit Bonds 6.6 20.9 U.S. Mid Cap Stocks 0.5 21.9

Gold 4.5 14.8 Non-U.S. Small Cap Stocks -0.4 12.1

U.S. Corporate Bonds 3.0 12.6 Non-U.S. Developed-Country Stocks -1.1 12.8

Investment-Grade Bonds 2.3 8.5 Commodities -1.8 3.1

U.S. Large Cap Stocks 1.7 20.6 U.S. Small Cap Stocks -2.4 14.2

Emerging-Market Bonds 1.3 12.1 Emerging-Market Stocks -4.2 5.9

20-Year U.S. Stock Returns Minus IG Bond Returns since 1926

Annualized Return Difference (%)

14

12

10 Average since 1926: 5%

8

6

4

2 1.0%

0

-2

1946 1950 1954 1958 1962 1966 1970 1974 1978 1982 1986 1990 1994 1998 2002 2006 2010 2014 2018

Past performance is no guarantee of future results. It is not possible to invest directly in an index. All indexes are unmanaged. See Appendix for important index

information. Assets represented by: Commodities—Bloomberg Commodity Index; Emerging-Market Bonds—JP Morgan EMBI Global Index; Emerging- Market

Stocks—MSCI EM Index; Gold—Gold Bullion, LBMA PM Fix; High-Yield Bonds—ICE BofAML High Yield Bond Index; Investment-Grade Bonds— Bloomberg

Barclays U.S. Aggregate Bond Index; Non-U.S. Developed-Country Stocks—MSCI EAFE Index; Non-U.S. Small Cap Stocks—MSCI EAFE Small Cap Index; Real

Estate Stocks—FTSE NAREIT Equity Index; U.S. Corporate Bonds—Bloomberg Barclays U.S. Credit Index; U.S. Large Cap Stocks—S&P 500® Index; U.S. Mid

Cap Stocks—Russell Midcap Index; U.S. Small Cap Stocks—Russell 2000 Index; Long Government & Credit Bonds—Bloomberg Barclays Long Government &

Credit Index. Source: Bloomberg Finance L.P., Haver Analytics, Fidelity Investments Asset Allocation Research Team (AART), as of 9/30/19.

5Long-Running Style and Regional Equity Trends Persist

SUMMARY

Several extreme trends in relative equity performance continued to persist. The outperformance of U.S. growth

stocks versus value stocks has extended more than a decade, and U.S. equities have outpaced their foreign

counterparts for roughly the same time span. Meanwhile, the performance of U.S. minimum-volatility stocks has

benefited from declining bond yields and surpassed the broader equity market during the bull-market upswing.

U.S. Equity Style Relative Performance Equity Relative Performance

Value vs. Growth U.S. Min Vol vs. U.S. Broad Market U.S. vs. Rest of World

Log Return (Index 1929=100) Relative Return (Index: 2006=100)

500 200

450

180

400

350

160

300

250 140

200

120

150

100

100

50

0 80

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

1929

1939

1949

1959

1969

1979

1989

1999

2009

2019

LEFT: Source Fama/French Research Factors—High Minus Low. Shading represents the peak of the value versus growth equity style.

RIGHT: U.S. Min Vol: MSCI USA Minimum Volatility Total Return Index. US Broad Market: MSCI USA Total Return Index. US: MSCI USA

Total Return Index. Rest of World: MSCI ACWI ex USA Total Return Index, as of 9/30/19.

6Falling Government Bond Yields Around the World

SUMMARY

Government bond yields continued to decline amid concerns about global economic weakness, trade

confrontation, and low inflation. Yields on 10-year government bonds in Germany and Japan fell further into

negative territory. The drop in U.S. 10-year yields resulted from a decline in both inflation expectations and

real interest rates, with both measures decreasing to near multi-year lows.

10-Year Government Bond Yields 10-Year U.S. Treasury Bond Yields

5-Year Range 1 Year Ago 9/30/19 Inflation Expectations Real Yields Nominal Yield

Yield Yield

3.5% 3.75%

Q3 Yield Change (bps)

3.0% Breakevens -16

3.25%

Real Yields -16

2.5% Nominal Yield -32

2.75%

2.0%

2.25%

1.7

1.5% 1.7%

1.75%

1.0%

1.5%

1.25%

0.5% 0.5

0.75%

0.0%

-0.2

-0.5% 0.25% 0.2%

-0.6

-1.0% -0.25%

Sep-2015

Jan-2016

Sep-2016

Jan-2017

Sep-2017

Jan-2018

Sep-2018

Jan-2019

Sep-2019

May-2016

May-2017

May-2018

May-2019

Germany Japan UK U.S.

7 LEFT and RIGHT: Source: Bloomberg Finance L.P., Fidelity Investments (AART), as of 9/30/19.Economy/Macro Backdrop

Multi-Time Horizon Asset Allocation Framework

ECONOMY

Fidelity’s Asset Allocation Research Team (AART) believes that asset-price fluctuations are driven by a

confluence of various factors that evolve over different time horizons. As a result, we employ a framework that

analyzes trends among three temporal segments: tactical (short term), business cycle (medium term), and

secular (long term).

DYNAMIC ASSET ALLOCATION TIMELINE

HORIZONS

Secular

(10–30 years)

Business Cycle

(1–10 years)

Tactical

(1–12 months)

Portfolio Construction

Asset Class | Country/Region | Sectors | Correlations

9 For illustrative purposes only. Source: Fidelity Investments (AART), as of 9/30/19Mature U.S. and Global Business Cycles

ECONOMY

The global business cycle continues to mature, with the U.S. and most major economies in the late-cycle

phase. China’s economy has stabilized, but a reacceleration from its growth recession has remained elusive.

Overall, a global industrial and trade recession has shown few signs of abating, and it remains to be seen

whether policy easing measures will prove sufficient to stimulate a sustained global reacceleration.

Business Cycle Framework

Spain

Brazil, India, Australia, Canada

U.S., France, Japan,

South Korea, Mexico

UK

Germany, Italy

China*

Note: The diagram above is a hypothetical illustration of the business cycle. There is not always a chronological, linear progression among the

phases of the business cycle, and there have been cycles when the economy has skipped a phase or retraced an earlier one. * A growth

recession is a significant decline in activity relative to a country’s long-term economic potential. We use the “growth cycle” definition for most

developing economies, such as China, because they tend to exhibit strong trend performance driven by rapid factor accumulation and

increases in productivity, and the deviation from the trend tends to matter most for asset returns. We use the classic definition of recession,

10 involving an outright contraction in economic activity, for developed economies. Source: Fidelity Investments (AART), as of 9/30/19.Global Backdrop Weak Despite China’s Industrial Stabilization

ECONOMY

Sagging trade and industrial activity continued to weigh on global growth, with the share of major countries with

expanding manufacturing sectors dropping to its lowest level since 2012. This weakness occurred despite an

upturn in our diffusion index of China’s industrial production. For the first time in the past decade, China’s

stimulus measures and manufacturing upswing have failed to lift global trade and industrial activity.

Global Manufacturing Activity and China Industrial Production

AART China Industrial Production Diffusion Index Share of Global PMIs >50

Share

100%

90%

80%

70%

60%

50%

40%

30%

20%

10%

0%

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

AART China Diffusion Index represents share of components rising over last 12 months. Gray bars represent China growth recessions as defined

11 by AART. Source: ISM, Markit, China National Bureau of Statistics (official data), Haver Analytics, Fidelity Investments (AART), as of 8/31/19.China Key to Global Growth; Policy Proving Insufficient

ECONOMY

Unlike the late 1990s, in recent years China’s contribution to global growth has been greater than that of the

United States. China’s monetary and fiscal policy easing has helped stabilize industrial activity, but credit

growth stayed subdued, implying that high debt levels are inhibiting the policy response. U.S. trade uncertainty

remains another headwind, supporting our stance that material economic reacceleration is unlikely.

Contribution to Global GDP Growth China Credit and Property Market

China U.S. Total Credit Growth Housing Sales

Share Year-over-Year Year-over-Year

29%

30% 35% 60%

50%

25% 30%

22% 40%

30%

20% 25%

20%

15% 13% 20%

12% 10%

0%

10% 15%

-10%

5% 10% -20%

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

2015

2017

2019

LEFT: Five-year averages. Source: International Monetary Fund, Fidelity Investments (AART), as of 9/30/19. RIGHT: Gray bars represent China

growth recessions as defined by AART. Source: China National Bureau of Statistics (official data), Haver Analytics, Fidelity Investments (AART),

12 as of 8/31/19.European Growth Slumping as Trade Headwinds Persist

ECONOMY

Smaller and more open economies are most susceptible to global trade risk, but employment in many large

economies, including Germany, is highly influenced by trade. The impact of deteriorating global trade

conditions has begun to affect some European domestic economies, with consumer confidence and the

employment outlook in Germany deteriorating markedly over the course of 2019.

Employment Reliance on Foreign Trade German Labor Market and Consumer

Consumer Confidence Business Employment Plans

Share of Employment from Exports Index

30% 110 0

25%

105

20%

100

15%

95

10%

90

5%

0% 85 0

1999

2001

2003

2005

2007

2009

2011

2013

2015

2017

2019

Sweden

Canada

Mexico

U.S.

Germany

Japan

S. Korea

UK

China

LEFT: Share of domestic business sector employment sustained by exporting activities. Source: OECD, Fidelity Investments (AART), as of 9/30/19.

RIGHT: Shading represents Germany economic recession as defined by the Economic Cycle Research Institute (ECRI). Source: European

13

Commission, Ifo, ECRI, Haver Analytics, Fidelity Investments (AART), as of 9/30/19.U.S. Firmly in Late Cycle

ECONOMY

Late cycle often is characterized as the phase during which capacity constraints emerge and economic activity

peaks. Inflation rates are not always high, but tight labor markets tend to spur higher wage growth and more

restrictive monetary policy. Late-cycle trends are now well entrenched, with peaking profit margins, slower

employment growth, and an inverted yield curve. Credit, though, remains favorable versus previous late cycles.

INDICATOR CURRENT TREND LATEST READINGS

Labor markets tighter, wages higher

Employment/Wages Pace of improvement has stalled

than 2–3 years ago

Monetary Policy Fed policy tighter than 2–3 years ago Fed cut rates

Yield Curve Flattening Inverted

Credit Some tightening of lending standards Credit accessible, spreads tight

Corporate Profits Margins declining Earnings growth slightly positive

14 Source: Fidelity Investments (AART), as of 9/30/19.Healthy Labor Market and Consumer Typical of Late Cycle

ECONOMY

The U.S. economy remains supported by consumption, which represents around 70% of GDP. Historically,

consumer spending and employment growth stay positive during late cycle, typically not falling until the onset

of recession. Several leading indicators suggest the labor market is nearing peak levels, including consumers’

extremely favorable assessment of the job market, which tends to be most elevated just prior to recession.

Activity around Recessions (1948–2011) Consumer Assessment of Labor Market

Goods Consumption Employment

Conference Board Survey

Housing Business Investment

Index: 100 = Recession Onset Jobs: Plentiful Minus Hard to Get

60%

115 Recession

Onset t=0

40%

110

20%

105

0%

100

-20%

95

-40%

90

-60%

85 -80% 0

1968

1971

1974

1977

1980

1983

1986

1989

1992

1995

1998

2001

2004

2007

2010

2013

2016

2019

t-8 t-7 t-6 t-5 t-4 t-3 t-2 t-1 t t+1 t+2 t+3 t+4 t+5 t+6 t+7 t+8

Quarters

LEFT: Source: Bureau of Economic Analysis, Bureau of Labor Statistics, Haver Analytics, Fidelity Investments (AART), as of 9/30/19.

RIGHT: Shading represents U.S. economic recession as defined by the National Bureau of Economic Research (NBER). Source: Conference

15 Board, NBER, Haver Analytics, Fidelity Investments (AART), as of 9/30/19.U.S. Profit Margins Declining, Exposed to Global Cycle

ECONOMY

Over the past several years, corporate profit margins have declined from record levels due to higher wages

and other costs, which is typical during the transition to late cycle. The level of economy-wide profit margins

remains healthy. However, the earnings of large multi-national U.S. companies tend to follow the highly global

manufacturing cycle, whose weakness has been exacerbated by the U.S.-China trade conflict.

U.S. Economy Profit Margins U.S. Manufacturing and S&P 500 Earnings

Profits as a Share of GDP S&P 500 Profit Growth Y/Y ISM Manufacturing PMI

4-quarter average Year-over-Year Index,Inflation Firm While Tariffs Add Uncertainty to Outlook

ECONOMY

Core inflation has been generally stable at about 2% in recent years, but tariff hikes have lately pushed goods

prices upward, helping boost core CPI to a multi-year high. Tariffs also have negatively impacted demand—for

example, last year’s tariffs on washing machines both boosted prices and lowered consumption. The near-

term inflation outlook remains balanced amid uncertain trade policy and downside economic risk.

U.S. Inflation Tariff Impact on Household Appliances

Core CPI AART Estimate Price Consumption

Year-over-Year Year-over-Year

U.S. implements

2.5% 15% tariff on washing

machines

10%

2.3%

5%

2.0% 0%

-5%

1.8%

-10%

1.5% -15%

Jan-2014

Jan-2015

Jan-2016

Jan-2017

Jan-2018

Jan-2019

Jul-2013

Jul-2014

Jul-2015

Jul-2016

Jul-2017

Jul-2018

Jul-2019

Apr-2013

Apr-2014

Apr-2015

Apr-2016

Apr-2017

Apr-2018

Apr-2019

Apr-2020

Oct-2013

Oct-2014

Oct-2015

Oct-2016

Oct-2017

Oct-2018

Oct-2019

LEFT and RIGHT: Core CPI: Consumer Price Index excluding food and energy. Source: Bureau of Labor Statistics, Haver Analytics, Fidelity

17 Investments (AART), as of 8/31/19.Yield Curve Inversion Typical During Late Cycle

ECONOMY

Ten-year Treasury bond yields remained below 3-month Treasuries, keeping the yield curve inverted. Curve

inversions have preceded the past seven recessions and may be interpreted as the market signaling weaker

expectations relative to current conditions. The time between inversion and recession has varied considerably,

however, and the curve also has flashed two “head fakes” in which expansion lasted for at least two more years.

U.S. Treasury Yield Curve

10-Year Minus 3-Month Yield

Yield Spread

6%

5% Yield Curve Inversions

4% • Occurred before the last 7

recessions

3%

• Occurred twice without a

2% recession (1966,1998)

1% • Recessions started 4 to 21

months after inversion

0%

• Un-inversions often occurred

-1% prior to recession

-2%

-3%

-4% 0.1

1965

1968

1971

1974

1977

1980

1983

1986

1989

1992

1995

1998

2001

2004

2007

2010

2013

2016

2019

Shading represents U.S. economic recession as defined by the National Bureau of Economic Research (NBER). Source: Bloomberg

18 Financial L.P., NBER, Fidelity Investments (AART), as of 9/30/19.Rate Cuts Better for Risk Assets in Mid Cycle Versus Late

ECONOMY

Since 1984, the Fed has initiated seven monetary easing cycles through cuts to its policy interest rate. When

the rate cuts were started during the mid-cycle phase, they consistently boosted global equities and tightened

credit spreads over the next 12 months. Rate cuts beginning in late cycle, however, resulted in a broader range

of outcomes with negative average equity returns and wider credit spreads.

Equity Returns After Initial Fed Cut (1984–2007) Credit Spreads After Initial Fed Cut (1984–2007)

U.S. Emerging Market High Yield OAS

12-Month Returns Basis Points Change (12 Months)

60% 700

Maximum

50% 600

40%

500

30%

400

Average

20%

300

10%

200

0%

Minimum 100

-10%

0

-20%

-30% -100

-40% -200

Mid-Cycle Late-Cycle Mid-Cycle Late-Cycle

OAS: Option-Adjusted Spread, U.S: S&P 500 total returns. Emerging Market: MSCI Emerging Market total returns from 1988. High Yield: ICE BofAML

U.S. High Yield Index. Source: Standard & Poor’s, MSCI, Barclays Capital, Bloomberg Financial L.P., Fidelity Investments (AART), as of 9/30/19.

19Dovish Global Central Bank Shifts Offset by U.S. Treasury

ECONOMY

During Q3, global central banks eased policy by lowering interest rates, and the Fed ended its balance-sheet

drawdown while the ECB re-initiated QE. However, the global liquidity backdrop is much less favorable than

2016–17, with U.S. Treasury increases of cash held at the Fed offsetting recent central-bank accommodation.

Monetary policy may be showing its limitations, with a number of challenges blunting the effects of easing.

Central Bank Balance Sheets

G4 Central Banks U.S. Treasury Cash at Fed Challenges to Monetary Policy

• Large U.S. Treasury issuance Billions (3-Month Change)

Billions (12-Month Change)

• Lower bank reserves

$2,500 • Repo market dislocations -$2,500

$2,000 -$2,000

$1,500 -$1,500

$1,000 -$1,000

Estimate

$500 -$500

$0 $0

-$500 $500

-$1,000 $1,000

Jan-2014

Jan-2015

Jan-2016

Jan-2017

Jan-2018

Jan-2019

Jan-2020

Jul-2014

Jul-2015

Jul-2016

Jul-2017

Jul-2018

Jul-2019

Bars represent estimates: Federal Reserve and BOE keep constant balance sheet, European Central Bank (ECB) to purchase EUR20B per month, and

Bank of Japan to purchase at annualized rate of average purchases over last 12 months. Dashed line represents estimate of Treasury increasing cash

20 held at the Federal Reserve to $400 billion in the fourth quarter. Source: Haver Analytics, Fidelity Investments (AART), as of 9/30/19.U.S. versus China: Strategic Competition and Trade Conflict

ECONOMY

The U.S. and China raised the stakes again during Q3. Tariffs were pushed above 20%, on average, further

disrupting the world’s largest trading relationship and casting a shadow over corporate confidence in the

highly integrated global economy. While hope remained that a truce could avert additional planned escalation,

the deepening geopolitical rift makes a variety of other bilateral commercial issues less tractable.

U.S.-China Relationship Average Tariff Rates

U.S. Tariffs on Chinese Goods China Tariffs on U.S. Goods

30%

25%

Geopolitical Strategic Trade

Rivalry Competition 20%

Military IT Sector/ Consumer

Hegemony Advanced and Other

in Asia Industrials Goods 15%

10%

Industrial Tariffs/ 5%

Policy Issues Market Access

• IP protection

• Export controls

0%

• Investment restrictions

2017 2018 Sep-19 Oct-19 Dec-19

RIGHT: Shaded areas are announced changes as of 9/30/19. Source: Peterson Institute for International Economics, Fidelity

21 Investments (AART) as of 9/30/19.Outlook: Market Assessment

ECONOMY

Fidelity’s Business Cycle Board, composed of portfolio managers responsible for a variety of global asset

allocation strategies, believes global economic momentum has peaked and that trade-policy friction is

negatively influencing capital expenditures. While monetary policymakers around the world have shifted to a

more accommodative stance, some level of uncertainty about the effectiveness of the policy response remains.

Business Cycle Risks

U.S. firmly in late-cycle phase Monetary and trade policy uncertainty

China’s economic slowdown is weighing China’s uncertain outlook and policy

on the global economy response

Asset allocation implications

Current environment warrants smaller asset allocation

tilts and a diversified strategy

Policymakers’ shift to a more accommodative stance

may support global asset markets

Inflation-sensitive asset valuations appear attractive

though near-term inflation risks are muted

22 For illustrative purposes only. Diversification does not ensure a profit or guarantee against a loss. Source: Fidelity Investments (AART) as of 9/30/19.Asset Markets

ASSET MARKETS

Defensive Equity and Fixed Income Sectors Led the Way

In Q3, equity sectors and factor segments that typically are less cyclical and may benefit from lower interest

rates led the equity markets: Utilities, real estate, consumer staples, and minimum-volatility stocks fared best.

Treasury bonds and other less risky debt types were the top performers among fixed income sectors. Gold

was the best-performing commodity segment. Emerging-market equities struggled.

International Equities and Global

U.S. Equity Styles Total Return Assets Total Return Fixed Income Total Return

Q3 YTD Q3 YTD Q3 YTD

Large Caps 1.7% 20.6% ACWI ex-USA -1.8% 11.6% Long Govt & Credit 6.6% 20.9%

Value 1.2% 17.5% Credit 3.0% 12.6%

Japan 3.1% 11.1%

Growth 1.1% 22.7% Treasuries 2.4% 7.7%

Canada 0.5% 21.6%

Mid Caps 0.5% 21.9% Aggregate 2.3% 8.5%

EAFE Small Cap -0.4% 12.1%

Small Caps -2.4% 14.2% CMBS 1.9% 8.6%

EAFE -1.1% 12.8%

Agency 1.7% 6.0%

Europe -1.8% 13.7%

U.S. Equity Sectors Total Return Municipal 1.6% 6.7%

EM Asia -3.4% 6.0%

MBS 1.4% 5.6%

Q3 YTD Emerging Markets -4.2% 5.9%

TIPS 1.3% 7.6%

Utilities 9.3% 25.4% Latin America -5.6% 6.3%

EM Debt 1.3% 12.1%

Real Estate 7.7% 29.7% EMEA -7.0% 5.1%

High Yield 1.2% 11.5%

Consumer Staples 6.1% 23.3% Gold 4.5% 14.8% Leveraged Loan 1.0% 6.8%

Info Tech 3.3% 31.4% Commodities -1.8% 3.1% ABS 0.9% 4.1%

Communication Services 2.2% 21.7%

Financials 2.0% 19.6% U.S. Equity Factors Total Return

Industrials 1.0% 22.6%

Q3 YTD

Consumer Discretionary 0.5% 22.5%

Min Volatility 3.3% 23.5%

Materials -0.1% 17.1%

Yield 2.7% 14.5%

Health Care -2.2% 5.6%

Quality 1.5% 18.3%

Energy -6.3% 6.0%

Value 1.4% 16.8%

Size -0.2% 16.5%

Momentum -0.9% 19.1%

EM: Emerging Markets. EMEA: Europe, the Middle East, and Africa. For indexes and other important information used to represent above asset

categories, see Appendix. Past performance is no guarantee of future results. It is not possible to invest directly in an index. All indexes are

unmanaged. Sector returns represented by S&P 500 sectors. Sector investing involves risk. Because of its narrow focus, sector investing may be

24 more volatile than investing in more diversified baskets of securities. Source: Bloomberg, Fidelity Investments (AART), as of 9/30/19.ASSET MARKETS

Late Cycle: Less Favorable Risk-Return Profile

Typically, the mid-cycle phase has favored riskier asset classes, resulting historically in broad-based gains

across most asset categories. Meanwhile, late cycle has produced the most mixed performance results of any

business cycle phase. Another frequent feature of late cycle has been an overall more limited upside for a

diversified portfolio, although returns for most asset categories have, on average, been positive.

Asset Class Performance in Mid- and Late-Cycle Phases (1950–2016)

Stocks High Yield Commodities Investment-Grade Bonds

Annual Absolute Return (Average)

20%

10%

0%

Mid Cycle: Strong Asset Class Performance Late Cycle: Mixed Asset Class Performance

• Favor economically sensitive assets • Favor inflation-resistant assets

• Broad-based gains • Gains more muted

Diversification does not ensure a profit or guarantee against a loss. Past performance is no guarantee of future results. It is not possible to

invest directly in an index. All indexes are unmanaged. Asset class total returns are represented by indexes from the following sources: Fidelity

Investments, Morningstar, and Bloomberg Barclays. Fidelity Investments source: a proprietary analysis of historical asset class performance,

25 which is not indicative of future performance.ASSET MARKETS

Stocks’ Return Profile Less Favorable During Late Cycle

Historically, this phase of the business cycle has had implications for asset market forward returns. When the

U.S. economy has been in the mid-cycle phase, forward 12-month real returns have been generally positive,

displaying a favorable distribution skewed to above-average returns. But as expansion matures into late cycle,

the forward distribution of real equity returns has typically displayed a less favorable, more negative skew.

Subsequent Stock Market Returns Given Business Cycle Phase (1952–2018)

Late Mid

Frequency

4

3

2

1

0

-48% -43% -38% -33% -29% -24% -19% -14% -10% -5% 0% 5% 9% 14% 19% 24% 28% 33% 38% 43%

Total Return over the Next 12 Months

Past performance is no guarantee of future results. The above charts are density plots generated from the 12-month forward returns of a U.S. Equity

26 Index sourced from Fidelity Investments. Source: Standard & Poor’s, Fidelity Investments (AART), as of 9/30/19.ASSET MARKETS

Muted Inflation Expectations Relative to Recent History

Historically, the late cycle has often experienced rising inflation pressures, which has tended to enhance the

attractiveness of inflation-sensitive assets such as TIPS and commodities. Our near-term outlook for inflation

is relatively range-bound, but market expectations for inflation (represented by TIPS breakeven rates) are at

the lower end of their decade-long range, suggesting inflation protection is relatively inexpensive.

Relative Asset Performance by Cycle Phase (1950–2016) U.S. Treasury Breakeven Inflation Rates

Mid Late 10 Year LT Average (Since 1998)

Hit Rate

100% 2.8%

90% 2.6%

80%

2.4%

70%

2.2%

60%

2.0%

50%

1.8%

40%

30% 1.6%

20% 1.4%

10%

1.2%

0%

TIPS vs. Commodities vs. 1.0%

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

IG Bonds U.S. Equities

Past performance is no guarantee of future results. It is not possible to invest directly in an index. All indexes are unmanaged.

TIPS: Treasury Inflation-Protected Securities. Hit Rate: frequency of one asset class outperforming another. Results are the difference between total

returns of the respective periods represented by indexes from the following sources: Fidelity Investments, Morningstar, and Bloomberg Barclays.

27 Fidelity Investments source: proprietary analysis of historical asset class performance, which is not indicative of future performance, as of 6/30/19.ASSET MARKETS

Expectations for Global Earnings Growth Convergence

U.S. earnings growth continued to decelerate during Q3, after receiving a boost from corporate tax cuts in

2018. Meanwhile, profit growth in non-U.S. developed and emerging markets stayed in negative territory during

the quarter. Forward estimates point to market expectations of a convergence of global profit growth in the

mid-single-digit range over the next 12 months.

Global EPS Growth (Trailing 12 Months)

U.S. DM EM

Change (Year-over-Year)

40%

30%

Forward

EPS

20%

10% 8.5%

7.8%

5.1%

0%

-10%

-20%

2012 2013 2014 2015 2016 2017 2018

Past performance is no guarantee of future results. DM: Developed Markets. EM: Emerging Markets. EPS: Earnings per share. Forward EPS:

28 Next 12 months expectations. Source: MSCI, Bloomberg Financial L.P., Fidelity Investments (AART), as of 9/30/19.ASSET MARKETS

Equity Valuations Mixed Relative to History

Continued rising stock prices in the U.S. moved equity valuations higher during Q3, pushing them further

above their long-term historical average. Price-to-earnings (P/E) ratios for Non-U.S. developed and emerging

markets remained below their long-term averages.

Global Market P/E Ratios

DM Trailing P/E EM Trailing P/E U.S. Trailing P/E Forward P/E

Ratio

30

25

Forward

P/E

20 DM Long-Term Average

U.S. Long-Term Average

U.S.

EM Long-Term Average

15

DM

EM

10

5

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

DM: Developed Markets. EM: Emerging Markets. Past performance is no guarantee of future results. It is not possible to invest directly in an index. All

indexes are unmanaged. See Appendix for important index information. Price-to-earnings ratio (P/E): stock price divided by earnings per share. Also

known as the multiple, P/E gives investors an idea of how much they are paying for a company’s earnings power. Long-term average P/E for Emerging

Markets includes data for 1988–2017. Long-term average P/E for Developed Markets includes data for 1973–2016, U.S. 1926–2017. Foreign

29 Developed—MSCI EAFE Index, Emerging Markets—MSCI EM Index. Source: Bloomberg Financial L.P., Fidelity Investments (AART) as of 9/30/19.ASSET MARKETS

Non-U.S. Equity and Currency Valuations Still Attractive

Using 5-year peak inflation-adjusted earnings, P/E ratios for international developed- and emerging-market

equities remained lower than those for the U.S., providing a relatively favorable long-term valuation backdrop

for non-U.S. stocks. After moving sideways during the first half of 2019, the U.S. dollar appreciated during Q3,

resulting in generally expensive valuations versus many of the world’s major currencies.

Cyclical P/Es Valuation of Major Currencies vs. USD

8/31/19 20-Year Range Last 12-Month Range 9/30/19

Price/5-Year Peak Real Earnings Valuation of Real Exchange Rates

20%

60

10% Expensive vs. $

50

40 0%

Cheap vs. $

30 -10%

20 -20%

10 -30%

0 -40%

EM

Mexico

Canada

Turkey

Japan

Spain

Brazil

U.S.

Germany

UK

DM

South Korea

China

Italy

France

Australia

Russia

Indonesia

Philippines

India

GBP JPY MXN CAD EUR CNY

DM: Developed Markets. EM: Emerging Markets. Past performance is no guarantee of future results. It is not possible to invest directly in an index. All

indexes are unmanaged. See Appendix for important index information. LEFT: Price-to-earnings (P/E) ratio (or multiple): stock price divided by

earnings per share, which indicates how much investors are paying for a company’s earnings power. Five-year peak earnings are adjusted for

inflation. Source: FactSet, countries’ statistical organizations, Haver Analytics, Fidelity Investments (AART), as of 8/31/19. RIGHT: GBP—British

pound; MXN—Mexican peso; JPY—Japanese yen; EUR—euro; CAD—Canadian dollar. Source: Federal Reserve Board, Haver Analytics, Fidelity

30 Investments (AART), as of 9/30/19.ASSET MARKETS

A High Equity Risk Premium Does Not Make Stocks Cheap

Plunging bond yields widened the gap between the equity earnings yield (reciprocal of the P/E ratio) and the

10-year U.S. Treasury bond yield—a measure of the equity risk premium (ERP). However, standalone valuation

metrics such as the P/E have a stronger relationship than the ERP to forward equity returns. The ERP, though,

may be better at identifying equity attractiveness relative to expected bond returns.

P/E Relation to Equities (1926–2019) Equity Risk Premium Relation to Equities

(1926–2019)

4-Quarter Forward S&P500 Average Return 4-Quarter Forward S&P500 Average Return

16% 16%

Correlation Correlation

1-year 10-year 1-year 10-year

0.4 0.6 0.2 0.3

12% 12%

Current

ERP: 3.8%

8% 8%

Current

P/E: 19.3

4% 4%

0% 0%

1 2 3 4 5 1 2 3 4 5

Quintile Quintile

Expensive Cheap Expensive Cheap

Price-to-earnings ratio (P/E): stock price divided by earnings per share. Source: Fidelity Investments, Robert Shiller, Standard & Poor’s,

31 Bloomberg Barclays, Haver Analytics, Fidelity Investments (AART), as of 9/3019.ASSET MARKETS

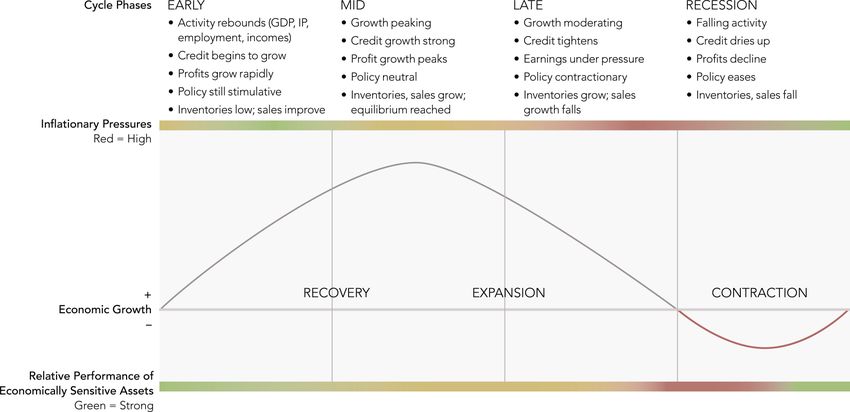

Business-Cycle Approach to Equity Sectors

A disciplined business-cycle approach to sector allocation can generate active returns by favoring industries

that may benefit from cyclical trends. Economically sensitive sectors historically have performed better in the

early and mid-cycle phases of an economic expansion. Meanwhile, companies in defensive sectors that have

more stable earnings have tended to outperform late in the cycle and, in particular, during recessions.

Business-Cycle Approach to Sectors

EARLY CYCLE MID CYCLE LATE CYCLE RECESSION

Sector

Rebounds Peaks Moderates Contracts

Financials +

Real Estate ++ --

Consumer Discretionary ++ - --

Information Technology + + -- --

Industrials ++ --

Materials + -- ++

Consumer Staples ++ ++

Health Care -- ++ ++

Energy -- ++

Communication Services + -

Utilities -- - + ++

Economically sensitive sectors Making marginal portfolio Defensive and inflation- Since performance is generally

may tend to outperform, while allocation changes to manage resistant sectors tend to negative in recessions,

more defensive sectors have drawdown risk with sectors perform better, while more investors should focus on the

tended to underperform. may enhance risk-adjusted cyclical sectors most defensive, historically

returns during this cycle. underperform. stable sectors.

Past performance is no guarantee of future results. Sectors as defined by GICS. White line is a theoretical representation of the business cycle as it

moves through early, mid, late, and recession phases. Green and red shaded portions above respectively represent over- or underperformance

relative to the broader market; unshaded (white) portions suggest no clear pattern of over- or underperformance. Double +/– signs indicate that the

sector is showing a consistent signal across all three metrics: full-phase average performance, median monthly difference, and cycle hit rate.

32 A single +/– indicates a mixed or less consistent signal. Return data from 1962 to 2016. Source: Fidelity Investments (AART), as of 9/30/19.ASSET MARKETS

Yields Fell Due to Lower Rates; Spreads Remained Tight

Modest inflation, flagging growth expectations, and the Federal Reserve’s dovish shift pushed bond yields

lower for the third quarter in a row. Credit spreads experienced some volatility but ended the quarter roughly

unchanged. Many fixed income categories have dropped to the bottom yield deciles relative to their own long-

term histories. Credit spreads also are generally below their long-term averages.

Fixed Income Yields and Spreads (1993–2019)

Treasury Rates Credit Spread Yield Percentile Spread Percentile

Yield Yield and Spread Percentiles

8% 100%

90%

7%

80%

6%

70%

60%

5%

60%

48%

4% 45% 50%

37% 37%

40%

3% 32%

30%

2%

20%

1% 7% 6% 6%

3% 10%

13% 0%

0% 0%

U.S. Aggregate MBS Long Gov/Credit Corporate Corporate Emerging-Market

Bond Investment Grade High Yield Debt

Past performance is no guarantee of future results. It is not possible to invest directly in an index. All indexes are unmanaged. See Appendix for

important index information. Percentile ranks of yields and spreads based on historical period from 1993 to 2019. MBS: mortgage-backed

33 security. Source: Bloomberg Barclays, Bank of America Merrill Lynch, JP Morgan, Fidelity Investments (AART), as of 9/30/19.Long-Term Themes

Performance Rotations Underscore Need for Diversification

LONG-TERM

The performance of different assets has fluctuated widely from year to year, and the magnitude of returns can

vary significantly among asset classes in any given year—even among asset classes that are moving in the

same direction. A portfolio allocation with a variety of global assets illustrates the potential benefits of

diversification.

Periodic Table of Returns

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 YTD Legend

66% 32% 14% 26% 56% 32% 35% 35% 40% 5% 79% 28% 8% 20% 39% 28% 5% 21% 38% 0% 27% REITs

34% 26% 8% 10% 47% 26% 21% 33% 16% -20% 58% 27% 8% 19% 34% 14% 3% 18% 30% -2% 23% Growth Stocks

27% 12% 5% 4% 39% 21% 14% 27% 12% -26% 37% 19% 4% 18% 33% 13% 1% 18% 26% -2% 21% Large Cap Stocks

24% 8% 2% -2% 37% 18% 12% 22% 11% -34% 32% 18% 4% 18% 32% 12% 1% 12% 22% -3% 17% Value Stocks

60% Large Cap

21% -1% -2% -6% 31% 17% 7% 18% 7% -36% 28% 17% 2% 16% 23% 11% 1% 12% 15% -4% 16%

40% IG Bonds

21% -3% -4% -9% 31% 11% 5% 16% 6% -36% 27% 16% 2% 16% 19% 6% 0% 11% 15% -4% 14% Small Cap Stocks

Foreign-Developed

12% -5% -4% -15% 29% 11% 5% 12% 5% -37% 26% 15% 0% 16% 7% 5% -4% 9% 13% -9% 13%

Country Stocks

7% -9% -12% -16% 28% 9% 5% 11% 2% -38% 20% 15% -4% 15% 3% 3% -4% 8% 9% -11% 12% High-Yield Bonds

Investment-Grade

3% -14% -20% -20% 24% 8% 4% 9% -1% -38% 19% 12% -12% 11% -2% -2% -5% 7% 8% -11% 9%

Bonds

Emerging-Market

-1% -22% -20% -22% 19% 7% 3% 4% -2% -43% 18% 8% -13% 4% -2% -4% -15% 3% 4% -11% 6%

Stocks

-5% -31% -21% -28% 4% 4% 2% 2% -16% -53% 6% 7% -18% -1% -10% -17% -25% 2% 1% -14% 3% Commodities

Past performance is no guarantee of future results. Diversification/asset allocation does not ensure a profit or guarantee against loss. It is not possible

to invest directly in an index. All indexes are unmanaged. See Appendix for important index information. Asset classes represented by: Commodities—

Bloomberg Commodity Index; Emerging-Market Stocks—MSCI Emerging Markets Index; Non-U.S. Developed-Country Stocks—MSCI EAFE Index;

Growth Stocks—Russell 3000 Growth Index; High-Yield Bonds—ICE BofAML U.S. High Yield Index; Investment-Grade Bonds—Bloomberg Barclays

U.S. Aggregate Bond Index; Large Cap Stocks—S&P 500 Index; Real Estate/REITs—FTSE NAREIT All Equity Total Return Index; Small Cap

Stocks—Russell 2000 Index; Value Stocks—Russell 3000 Value Index. Source: Morningstar, Standard & Poor’s, Haver Analytics, Fidelity Investments

35 (AART), as of 9/30/19.Secular Trend: Peak Globalization

LONG-TERM

After decades of rapid global integration, economic openness stalled in recent years amid geopolitical shifts

and domestic political pressures in many advanced economies. Changes to global rules may pose risks for

incumbent companies, industries, and countries that have benefited the most from the rise of a rule-based

global order. These risks include greater uncertainty and lower productivity and corporate profit margins.

Trade Globalization

Secular Risks for Asset Markets

Global Imports/GDP

• Less rules-based and less market-

Ratio

oriented global system

25%

More Globalized • Higher political risk

• Inflationary pressures

20% • Pressures on productivity growth

and corporate profit margins

15%

10%

Less Globalized

5%

1961

1964

1967

1970

1973

1976

1979

1982

1985

1988

1991

1994

1997

2000

2003

2006

2009

2012

2015

2018

36 Source: International Monetary Fund (IMF), World Bank, Haver Analytics, Fidelity Investments (AART), as of 9/30/19.Secular Forecast: Slower Global Growth, EM to Lead

LONG-TERM

Slowing labor force growth and aging demographics are expected to tamp down global growth over the next

two decades. We expect GDP growth of emerging countries to outpace that of developed markets over the

long term, providing a relatively favorable secular backdrop for emerging-market equity returns.

Real GDP 20-Year Growth Forecasts vs. History

Developed Markets Emerging Markets Last 20 Years

Annualized Rate

10%

Global Real GDP Growth

9%

Last 20 years 20-year forecast

8% 2.7% 2.1%

7%

6%

5%

4%

3%

2%

1%

0%

Japan

Netherlands

Canada

Mexico

Colombia

Peru

Spain

Sweden

U.S.

Brazil

Germany

Turkey

South Africa

UK

Australia

Italy

France

South Korea

China

Indonesia

Russia

Thailand

India

Malaysia

Philippines

Past performance is no guarantee of future results. EM: Emerging Markets. GDP: Gross Domestic Product. Source: OECD, Fidelity Investments

37 (AART), as of 5/31/19.Slower U.S. Economic Growth Likely over the Long Term

LONG-TERM

Slower population growth and aging demographics provide a more challenging backdrop for U.S. growth over the

next 20 years. Labor force growth has continued to decelerate from its peak in the 1960s and ‘70s, and since 2000

nearly half of this growth came from immigration. Even if productivity rates reaccelerate, it will be difficult for the

U.S. to return to the roughly 3% real GDP growth average since World War II.

Real GDP Components 20-Year AART

Projections

Labor Force Productivity Real GDP

Labor Force Growth 0.5%

Year-over-Year Growth (20-Year Average)

Labor Market Productivity 1.2%

4.5%

Real GDP Growth 1.7%

4.0%

3.5%

Productivity Peak

3.0% (1949–1969): 3.0%

2.5%

2.2%

2.0%

Labor Force Peak

(1962–1982): 2.3%

1.5% 1.4%

1.0%

0.5% 0.8%

0.0%

1969

1971

1973

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

2015

2017

2019

38 Source: Bureau of Economic Analysis, Bureau of Labor Statistics, Haver Analytics, Fidelity Investments (AART), as of 6/30/19.Secular Rate Outlook: Higher Than Now, Lower Than History

LONG-TERM

Over long periods of time, GDP growth has had a tight positive relationship with long-term government bond

yields (yields generally have averaged the same rate as nominal growth). We expect interest rates will rise over

the long term to an average that is closer to our 3.7% nominal GDP forecast, but this implies that rates would

settle at a significantly lower level than their historical averages.

Nominal Government Bond Yields and GDP Growth

U.S. Secular Growth Forecast Historical Observations of Various Countries

10-Year Sovereign Yield (20-Year Average)

18%

16%

14%

12%

10%

8%

6%

4%

U.S. Next 20 Years Forecast Yield (3.7%)

2%

U.S. Current Yield (1.7%)

0%

0% 2% 4% 6% 8% 10% 12% 14% 16% 18%

GDP Growth (20-Year Average)

39 GDP: Gross Domestic Product. Source: Official Country Estimates, Haver Analytics, Fidelity Investments (AART), as of 9/30/19.Unintended Consequences of Extraordinary Monetary Policy

LONG-TERM

Starting in 2014, five major central banks, including the BOJ and ECB, enacted negative policy rates in an effort

to boost inflation, bank lending, and economic growth. In fact, the impact of negative rates in Europe and Japan

has run counter to the intended goals. Aging consumers raised savings rates amid lower interest income, bank

lending stayed weak as low loan rates pressured banks’ profit margins, and inflation remained well below target.

Negative Policy Rate Considerations Global Bank Stocks

Intended Central Unintended U.S. Japan Europe

Bank Goals Consequences Price Index: June 30, 2014 = 100

170

Stimulates savings 160

Stimulates

consumption (German consumers

increased savings rate) 150

140

Hurts bank margins,

Incentivizes reduces loan supply 130

bank lending (European/Japan banks

in doldrums) 120

110

Reduces debt Keeping weak firms alive, 100

service burden low productivity

90

80

Weakens Limited impact in a world of 70

currency low policy rates

Mar-15

Mar-18

Dec-15

Dec-18

Jun-14

Sep-16

Jun-17

Sep-19

Bank stocks represented by MSCI Financials Index at regional level in local currency. Source: Bloomberg Finance L.P., Fidelity Investments

40 (AART), as of 9/30/19.Secular Inflation: Risks on the Upside?

LONG-TERM

Recent decades of disinflation have dragged down many investors’ long-term inflation expectations.

Technological progress and aging demographics might help keep inflation low; however, we believe several

factors, including policy changes and “peak globalization” trends, could influence the secular path of inflation,

potentially causing inflation to accelerate faster than today’s subdued expectations.

U.S. Inflation Expectations vs. Fed Target Possible Secular Impact on Inflation

Fed Inflation Target 20-Year Inflation Swap PCE

Secular Possible Risks to

Year-over-Year (2-year moving average)

Factors Developments Inflation

3.0%

Fed targets higher inflation

Policy

2.5% More stimulative fiscal policy

Elderly people:

2.0% Aging

• Spend less (reducing demand)

Demographics

• Work less (reducing supply)

1.5%

Peak

More expensive goods/labor

Globalization

1.0%

Technological

More robots, Amazon effect

Progress

0.5%

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

LEFT: PCE: Personal Consumption Expenditures. Source: Bureau of Labor Statistics, Bloomberg Finance L.P., Fidelity Investments

(AART), as of 5/31/19.

41 RIGHT: Fed: Federal Reserve. Source: Fidelity Investments (AART), as of 6/30/19.Market Downturns Can Cause Investors to De-Risk

LONG-TERM

Data from millions of retirement plan participants can illustrate how investor behavior may change under

varying market conditions. During the past two bear markets, many long-term investors reduced allocations to

equities and took years to return to their prior equity contribution rates. Excessive focus on short-term market

volatility may hamper the ability to achieve the objectives of a sound, diversified, long-term investment plan.

Fidelity Plan Participants’ Contribution to Equities

S&P 500 Percentage of New Contributions to Stocks

Price Contributions

3000 85%

2800 83%

2600

81%

2400

79%

2200

2000 77%

1800 75%

1600 73%

1400

71%

1200

69%

1000

800 67%

600 65%

Jun-00

Jun-01

Jun-02

Jun-03

Jun-04

Jun-05

Jun-06

Jun-07

Jun-08

Jun-09

Jun-10

Jun-11

Jun-12

Jun-13

Jun-14

Jun-15

Jun-16

Jun-17

Jun-18

Jun-19

Shaded areas represent periods when the stock market (S&P 500 Index) fell by 20% or more peak to trough. Stock contributions: the

percentage of all new directed deferrals (contributions) into stocks by participants via the available investment options in defined contribution

plans administered by Fidelity Investments. Diversification does not ensure a profit or guarantee against loss. Standard & Poor’s, Bloomberg

42 Financial L.P., Fidelity Investments as of 6/30/19.Myopic Loss Aversion Prompts Risk-Averse Behavior

LONG-TERM

Myopic loss aversion describes a common bias in which greater sensitivity to losses than to gains is

compounded by the frequent evaluation of outcomes. Historically, investors who review their portfolios more

frequently have tended to shift toward more conservative exposures, as increased monitoring raises the

likelihood of seeing (and reacting to) a loss.

Impact of Feedback Frequency on Investment Decisions

Monthly Yearly

Bonds

Stocks 30%

41%

Stocks

Bonds

70%

59%

In a study, subjects were assigned simulated conditions that were similar to making portfolio decisions on a monthly or yearly basis.

Source: Thaler, R.H., A. Tversky, D. Kahneman, and A. Schwartz. “The Effect of Myopia and Loss Aversion on Risk Taking: An Experimental Test.”

The Quarterly Journal of Economics 112.2 (1997), used by permission of Oxford University Press; Fidelity Investments (AART), as of 9/30/19.

43Appendix: Important Information

Information presented herein is for discussion and illustrative purposes only and is not a Stock markets, especially non-U.S. markets, are volatile and can decline significantly in

recommendation or an offer or solicitation to buy or sell any securities. Views expressed are as response to adverse issuer, political, regulatory, market, or economic developments. Foreign

of the date indicated, based on the information available at that time, and may change based on securities are subject to interest rate, currency exchange rate, economic, and political risks, all

market and other conditions. Unless otherwise noted, the opinions provided are those of the of which are magnified in emerging markets.

authors and not necessarily those of Fidelity Investments or its affiliates. Fidelity does not

assume any duty to update any of the information. The securities of smaller, less well-known companies can be more volatile than those of larger

companies.

Information provided in this document is for informational and educational purposes only. To the

extent any investment information in this material is deemed to be a recommendation, it is not Growth stocks can perform differently from the market as a whole and from other types of

meant to be impartial investment advice or advice in a fiduciary capacity and is not intended to stocks, and can be more volatile than other types of stocks. Value stocks can perform differently

be used as a primary basis for you or your client's investment decisions. Fidelity and its from other types of stocks and can continue to be undervalued by the market for long periods

representatives may have a conflict of interest in the products or services mentioned in this of time.

material because they have a financial interest in them, and receive compensation, directly or Lower-quality debt securities generally offer higher yields but also involve greater risk of default

indirectly, in connection with the management, distribution, and/or servicing of these products or or price changes due to potential changes in the credit quality of the issuer. Any fixed income

services, including Fidelity funds, certain third-party funds and products, and certain investment security sold or redeemed prior to maturity may be subject to loss.

services.

Floating rate loans generally are subject to restrictions on resale, and sometimes trade

Investment decisions should be based on an individual’s own goals, time horizon, and tolerance infrequently in the secondary market; as a result, they may be more difficult to value, buy, or

for risk. Nothing in this content should be considered to be legal or tax advice, and you are sell. A floating rate loan may not be fully collateralized and therefore may decline significantly

encouraged to consult your own lawyer, accountant, or other advisor before making any in value.

financial decision. These materials are provided for informational purposes only and should not

be used or construed as a recommendation of any security, sector, or investment strategy. The municipal market can be affected by adverse tax, legislative, or political changes, and by

the financial condition of the issuers of municipal securities. Interest income generated by

Fidelity does not provide legal or tax advice and the information provided herein is general in municipal bonds is generally expected to be exempt from federal income taxes and, if the bonds

nature and should not be considered legal or tax advice. Consult with an attorney or a tax are held by an investor resident in the state of issuance, from state and local income taxes.

professional regarding your specific legal or tax situation. Such interest income may be subject to federal and/or state alternative minimum taxes.

Past performance and dividend rates are historical and do not guarantee Investing in municipal bonds for the purpose of generating tax-exempt income may not be

future results. appropriate for investors in all tax brackets. Generally, tax-exempt municipal securities are not

appropriate holdings for tax-advantaged accounts such as IRAs and 401(k)s.

Investing involves risk, including risk of loss.

The commodities industry can be significantly affected by commodity prices, world events,

Diversification does not ensure a profit or guarantee against loss. import controls, worldwide competition, government regulations, and economic conditions.

Index or benchmark performance presented in this document does not reflect the deduction of The gold industry can be significantly affected by international monetary and political

advisory fees, transaction charges, and other expenses, which would reduce performance. developments, such as currency devaluations or revaluations, central bank movements,

economic and social conditions within a country, trade imbalances, or trade or currency

Indexes are unmanaged. It is not possible to invest directly in an index. restrictions between countries.

Although bonds generally present less short-term risk and volatility than stocks, bonds do Changes in real estate values or economic downturns can have a significant negative effect on

contain interest rate risk (as interest rates rise, bond prices usually fall, and vice versa) and the issuers in the real estate industry.

risk of default, or the risk that an issuer will be unable to make income or principal payments.

Leverage can magnify the impact that adverse issuer, political, regulatory, market, or economic

Additionally, bonds and short-term investments entail greater inflation risk—or the risk that the developments have on a company. In the event of bankruptcy, a company’s creditors take

return of an investment will not keep up with increases in the prices of goods and services— precedence over the company’s stockholders.

than stocks. Increases in real interest rates can cause the price of inflation-protected debt

securities to decrease.

44Appendix: Important Information

Market Indexes Bloomberg Barclays U.S. Treasury Inflation-Protected Securities (TIPS) Index

(Series-L) is a market value-weighted index that measures the performance of inflation-

Index returns on slide 24 represented by: Growth—Russell 3000®

Growth Index; Large protected securities issued by the U.S. Treasury. Bloomberg Barclays U.S. Treasury

Caps—S&P 500® index; Mid Caps—Russell MidCap® Index; Small Caps—Russell 2000® Bond Index is a market value-weighted index of public obligations of the U.S. Treasury

Index; Value - Russell 3000® Value Index; ACWI ex USA—MSCI All Country World Index with maturities of one year or more. Bloomberg Commodity Index measures the

(ACWI); Canada—MSCI Canada Index; Commodities—Bloomberg Commodity Index; performance of the commodities market. It consists of exchange traded futures contracts

EAFE—MSCI EAFE (Europe, Australasia, Far East) Index; EAFE Small Cap—MSCI EAFE on physical commodities that are weighted to account for the economic significance and

Small Cap Index; EM Asia—MSCI Emerging Markets Asia Index; EMEA (Europe, Middle market liquidity of each commodity.

East, and Africa)—MSCI EM EMEA Index; Emerging Markets (EM)—MSCI EM Index;

Europe—MSCI Europe Index; Gold—Gold Bullion Price, LBMA PM Fix; Japan—MSCI Dow Jones U.S. Total Stock Market IndexSM is a full market capitalization-weighted index

Japan Index; Latin America—MSCI EM Latin America Index; ABS (Asset-Backed of all equity securities of U.S.-headquartered companies with readily available price data.

Securities)—Bloomberg Barclays ABS Index; Agency—Bloomberg Barclays U.S. Agency

Index; Aggregate—Bloomberg Barclays U.S. Aggregate Bond Index; CMBS (Commercial FTSE® National Association of Real Estate Investment Trusts (NAREIT®) All REITs

Mortgage-Backed Securities)—Bloomberg Barclays Investment-Grade CMBS Index; Index is a market capitalization-weighted index that is designed to measure the

Credit—Bloomberg Barclays U.S. Credit Bond Index; EM Debt (Emerging-Market Debt)— performance of all tax-qualified REITs listed on the NYSE, the American Stock Exchange,

JP Morgan EMBI Global Index; High Yield—ICE BofAML U.S. High Yield Index; Leveraged or the NASDAQ National Market List. FTSE® NAREIT® Equity REIT Index is an

Loan—S&P/LSTA Leveraged Loan Index; Long Government & Credit (Investment- unmanaged market value-weighted index based on the last closing price of the month for

Grade)—Bloomberg Barclays Long Government & Credit Index; MBS (Mortgage-Backed tax-qualified REITs listed on the New York Stock Exchange (NYSE).

Securities)—Bloomberg Barclays MBS Index; Municipal—Bloomberg Barclays Municipal ICE BofAML U.S. High Yield Index is a market capitalization-weighted index of U.S. dollar-

Bond Index; TIPS (Treasury Inflation-Protected Securities)—Bloomberg Barclays U.S. denominated, below-investment-grade corporate debt publicly issued in the U.S. market.

TIPS Index; Treasuries—Bloomberg Barclays U.S. Treasury Index.

JPM® EMBI Global Index, and its country sub-indexes, tracks total returns for the U.S.

Bloomberg Barclays ABS Index is a market value-weighted index that covers fixed-rate dollar-denominated debt instruments issued by emerging-market sovereign and quasi-

asset-backed securities with average lives greater than or equal to one year and that are sovereign entities, such as Brady bonds, loans, and Eurobonds.

part of a public deal; the index covers the following collateral types: credit cards, autos,

home equity loans, stranded-cost utility (rate-reduction bonds), and manufactured housing. MSCI All Country World Index (ACWI) is a market capitalization-weighted index designed to

measure the investable equity market performance for global investors of developed and

Bloomberg Barclays CMBS Index is designed to mirror commercial mortgage-backed emerging markets. MSCI ACWI (All Country World Index) ex USA Index is a market

securities of investment-grade quality (Baa3/BBB-/BBB- or above) using Moody’s, S&P, capitalization-weighted index designed to measure the investable equity market performance for

and Fitch, respectively, with maturities of at least one year. Bloomberg Barclays Long global investors of large and mid cap stocks in developed and emerging markets, excluding the

U.S. Government Credit Index includes all publicly issued U.S. government and corporate United States.

securities that have a remaining maturity of 10 or more years, are rated investment-grade,

and have $250 million or more of outstanding face value. MSCI Emerging Markets (EM) Index is a market capitalization-weighted index that is designed

to measure the investable equity market performance for global investors in emerging markets.

Bloomberg Barclays Municipal Bond Index is a market value-weighted index of MSCI EM Asia Index is a market capitalization-weighted index designed to measure equity

investment-grade municipal bonds with maturities of one year or more. Bloomberg market performance in Asia. MSCI EM Europe, Middle East, and Africa (EMEA) Index is a

Barclays U.S. Agency Bond Index is a market value-weighted index of U.S. Agency market capitalization-weighted index that is designed to measure the investable equity market

government and investment-grade corporate fixed-rate debt issues. Bloomberg Barclays performance for global investors in the emerging-market countries of Europe, the Middle East,

U.S. Aggregate Bond is a broad-based, market value-weighted benchmark that measures and Africa. MSCI EM Latin America Index is a market capitalization-weighted index that is

the performance of the investment-grade, U.S. dollar-denominated, fixed-rate taxable bond designed to measure the investable equity market performance for global investors in the

market. Bloomberg Barclays U.S. Credit Bond Index is a market value-weighted index of emerging-market countries of Latin America.

investment-grade corporate fixed-rate debt issues with maturities of one year or more.

MSCI Europe, Australasia, Far East Index (EAFE) is a market capitalization-weighted index

Bloomberg Barclays U.S. MBS Index is a market value-weighted index of fixed-rate that is designed to measure the investable equity market performance for global investors in

securities that represent interests in pools of mortgage loans, including balloon mortgages, developed markets, excluding the U.S. and Canada. MSCI EAFE Small Cap Index is a market

with original terms of 15 and 30 years that are issued by the Government National capitalization-weighted index that is designed to measure the investable equity market

Mortgage Association (GNMA), the Federal National Mortgage Association (FNMA), and performance of small cap stocks for global investors in developed markets, excluding the U.S.

the Federal Home Loan Mortgage Corp. (FHLMC). and Canada.

45You can also read