RACE TO THE POST COVID-19 RECOVERY: 7 OBSTACLES TO OVERCOME - ALLIANZ RESEARCH 01 April 2021 - Euler Hermes

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Photo on Unsplash ALLIANZ RESEARCH RACE TO THE POST COVID-19 RECOVERY: 7 OBSTACLES TO OVERCOME 01 April 2021 04 A multi-speed global recovery 14 Regional outlooks

Allianz Research

The global recovery is on the right track albeit conditional on key differentiating

elements across countries. Global GDP is expected to rebound by +5.1% in 2021,

EXECUTIVE with one fourth of the recovery being driven by the US, while China should con-

tribute less to growth by progressively adopting a less accommodative economic

policy. In 2022, world GDP growth should reach +4.0%. Europe should recover its

SUMMARY Covid-19 losses only at this horizon against H2 2021 for the US. The race to re-

covery will hinge on seven key obstacles.

Obstacle 1: Formula 1 race on vaccination. Execution risks will remain a key

differentiator between countries, with the pace of vaccination campaigns driving

a multi-speed recovery and keeping divergence at high levels. At the current

pace of vaccination, the US and the UK will reach herd immunity in May. While

Ludovic Subran, Chief Economist

Europe should be able to vaccinate its vulnerable population by the summer,

+49 (0) 1 75 58 42 725 herd immunity is not likely to be reached before the fall at the current pace. On

the other hand, most governments (France) are speeding up the vaccination

ludovic.subran@allianz.com pace to reach herd immunity during the summer.

Obstacle 2: Excess savings will still hover around 40% above pre-crisis levels at

end-2021. In a relatively optimistic scenario, excess savings from households

Alexis Garatti, Head of Economic Research

should provide a tailwind to consumer spending to the tune of +1.5% of GDP in

alexis.garatti@eulerhermes.com Europe and more than +3% in the US in 2021. Close to the same amount could be

added on top for investment or consumption abroad purposes should confi-

Eric Barthalon, Head of Capital Markets Research dence effects play a positive role. We calculate that around EUR163bn could be

eric.barthalon@allianz.com transformed into private consumption in the Eurozone, equivalent to 30% of the

Ana Boata, Head of Macroeconomic Research Covid-19 excess savings. However, in the US, we expect 50% of the current excess

ana.boata@eulerhermes.com savings to be spent in 2021 as an earlier loosening of restrictions and more pow-

erful fiscal impulses should boost the confidence effect. The US household sav-

Jordi Basco Carrera, Fixed Income Strategist

ings rate should be back to a normal level at close to 7% of gross disposable in-

jordi.basco@allianz.com

come at end-2021.

Georges Dib, Economist for Latin America, Spain and

Portugal

Obstacle 3: Phasing out assistance mechanisms is not a zero-sum game and the

georges.dib@eulerhermes.com risk of policy mistakes remains high. After the “whatever it takes” consensus in

2020, fiscal policy will march to the beat of national drums going forward. In

Françoise Huang, Senior Economist for APAC 2021, the consensus to do “whatever it takes” is already giving way to more het-

francoise.huang@eulerhermes.com erogeneous policy prospects. In China, the path towards a policy normalization

Patrick Krizan, Senior Economist for Fixed Income has already started, with official targets implying a clear withdrawal of policy

patrick.krizan@allianz.com support in 2021, even if some flexibility will be kept to manage credit risk if need-

ed. The global demand torch will pass to the US, with its gigantic USD1.9trn fiscal

Ano Kuhanathan, Sector Advisor and Data Scientist

stimulus (9% of GDP) and a new gigantic infrastructure plan to come. Europe's

ano.kuhanathan@allianz.com

fiscal response pales in comparison: the Next Generation (NGEU) fund will only

Selin Ozyurt, Senior Economist for France and Africa extend a helping hand from H2 2021 onwards and the growth impact (a cumula-

selin.ozyurt@eulerhermes.com tive +1.5pp until 2025) should prove moderate and delayed, given its focus on

Manfred Stamer, Senior Economist for Emerging

the supply side – 2/3 of the EUR313bn grants are likely to be used for investment

Europe and the Middle East

– and drawn-out payments. It will be difficult to operate a smooth phasing out of

manfred.stamer@eulerhermes.com job retention schemes, transfers to the most impacted sectors and public credit

guarantees, without adding to difficulties of non-financial companies. Corporate

Katharina Utermöhl, Senior Economist for Europe bond redemptions will increase by more than 70% in 2022 and double in the US.

katharina.utermoehl@allianz.com

Obstacle 4: Crowding-in vs. crowding-out effects on investment are not yet re-

solved. Joe Biden’s “Build Back Better” in the US (potentially USD2.3trn), the EU

Next Generation of EUR725bn fund and China’s infrastructure plan totaling

more than USD1.5trn by 2025 will all contribute to support demand and the

global economy’s growth potential over the medium-term. But their success de-

pends on whether governments can channel excess savings to productive pro-

jects and boost private sector. We find a positive impact of excess savings on

business investment in the US, Germany, France and the UK, but much of this will

depend on future tax policies and the funding conditions (e.g. recovery state-

guaranteed loans).

2

01 April 2021

Obstacle 5: Bottlenecks in the global supply chain are as high as during the

peak of the pandemic and should push global trade into a borderline recession

in Q2. Global trade growth will rebound to +7.9% in 2021 in volume terms, but

excluding the positive carryover effects from 2020 will stand at +5.4%. More im-

portantly, we expect a temporary slowdown in Q2 2021 due to prevailing supply

-chain disruption: for the full year 2021, we estimate that the impact of supply-

chain disruptions could weigh on global trade growth by -1.7pp. In addition,

trade in services will remain impaired by the delayed reopening of sectors most

impacted by Covid-19-restrictions and continued barriers to cross-border travel.

Obstacle 6: Temporary overshoot of inflation. A temporary overshoot of inflation

is likely to be driven by temporary base effects. Hence, companies’ pricing power

is likely to remain limited, given subdued demand dynamics: (i) excess savings

from households and NFCs that act as a drag on money velocity; (ii) persistently

negative output gaps due to lower capacity utilization and (iii) rising unemploy-

ment rates that will keep a lid on wage growth (below 3%). Therefore, we don’t

expect central banks to stage a policy U-turn as a reaction to inflation temporar-

ily overshooting in the US at 3.5% by mid-2021 and hitting the 2% target for a

few months in the Eurozone.

Obstacle 7: Not putting an end to the sweet music of market’s reflation. Risky

assets are operating under the assumption that what is good for them – uncon-

ventional monetary policy and fiscal profligacy – is necessarily good for the real

economy, which will ultimately validate their optimism. For the time being, how-

ever, what we see is a widening divergence between asset prices and their un-

derlying value. Amplified by various investment management techniques (ETFs,

risk-parity) that put asset allocation on automatic pilot, this divergence is a vul-

nerability. An inadvertent escalation in geopolitical tensions between the US

and China, surging inflation that wrong-foots the subdued inflation expectations

held by central banks or nationalistic impulses prevailing over the common

good in Europe are all exogenous triggers that could put its widening in reverse.

But exogenous sources of risk are always easier to identify than endogenous

ones: the danger is more likely to come from within capital markets. As shown by

the rise of options trading and margin debt, leveraged investing is pervasive,

and so is the confusion about liquidity: especially in capital markets, the velocity

of money (the flow of liquidity) is far more volatile than its quantity (the stock of

liquidity). In the presence of leverage and overtrading, risk-taking is prone to

running amok and even a minor shock to confidence can lead to a sudden dry-

ing up of liquidity, forced liquidations and/or default.

+5.1%

Forecast for global GDP growth in 2021.

3

Allianz Research

A MULTI-SPEED RECOVERY,

SEVEN OBSTACLES TO OVERCOME

From China saving the world to the US. paigns driving a multi-speed recovery valent to EUR123bn of economic losses

Global GDP is expected to rebound by and keeping divergence at high levels. (see Figure 2), or more than twice as

+5.1% in 2021, with one fourth of the much as the EU Generation Fund’s

recovery being driven by the US, while Obstacle 1: Formula 1 race on planned disbursement for 2021. Asym-

China should progressively adopt a less vaccination. metries will be also be the result of dis-

accommodative economic policy. In At the current pace of vaccination, the synchronized economic policies. The US

2022, world GDP growth should reach US and the UK will reach herd immunity will remain at the forefront of fiscal

+4%. The over-expansionary stance of in May (see Figure 1). While Europe initiatives, while delays in execution will

the global policy mix explains this re- should be able to vaccinate its vulne- be visible in Europe. The early positio-

bound in 2021 and 2022, compared rable population by the summer, herd ning of China in the current cycle will

with the contraction of –3.6% in 2020. immunity is not likely to be reached allow the central government and the

However, execution risks will remain a before the fall at the current pace of PBoC to start a reining in of their ex-

key differentiator between countries, vaccination. Overall, the seven weeks pansionary policies.

with the pace of vaccination cam- of vaccination delay in Europe is equi-

Figure 1: Expected date of herd immunity Figure 2: Cost of vaccination delay

100

1.5 Today

Tripling of current

Chile

USA Morocco Germany EU

South Africa 0

70% of adult

1

Israel France Argentina Brazil Lost output EUR123bn

UK Serbia

Doubling of current

-100

0.5

0 -200

-0.5 -300 Doubling of current

USA

Chile

Argentina

vulnerable Serbia

Brazil

-1

population

Israel

UK EU -400

Morocco France Germany

-1.5

later than

09-20 01-21 04-21 07-21 10-21 02-22 05-22 08-22 12-22 03-23 -500

11-20 01-21 03-21 05-21 07-21 09-21 11-21

Sources: Our World in Data, Duke University, Euler Hermes, Allianz Research Sources: Our World in Data, Duke University, Euler Hermes, Allianz Research

4

01 April 2021

Obstacle 2: Excess savings will still ho- EUR180bn to be unleased in 2021 in valent to around half a point of GDP

ver around 40% above pre-crisis levels the Eurozone, equivalent to 1.5% of this year. Overall, at end-2021, we ex-

at end-2021. GDP (see Figure 3). At end 2021, this pect Eurozone savings to still remain

Excess savings from households should would mean a fall of a bit more than 37% above pre-pandemic levels (or

provide a tailwind to economic growth 50% in excess savings compared to end close to EUR350bn, 2.9% of GDP). In the

to the tune of +1.5% of GDP in Europe -2020. Looking at the structure of sa- US, we expect 50% of the current excess

and more than +3% in the US in 2021. vings by income level and the propensi- saving to be spent in 2021 as an earlier

In 2020, Eurozone household savings ty to spend, we calculate that around loosening of restrictions and more po-

increased by EUR530bn or +40% com- EUR163bn could be transformed into werful fiscal impulses should boost the

pared to pre-pandemic levels. Out of private consumption, equivalent to 30% confidence effect. The US household

this, and taking into account the pace of the Covid-19 household excess sa- savings rate should be back to a nor-

of dissaving from 2020 during de- vings, and to half of the depleted mal level at close to 7% of gross dispo-

confinement periods, we expect household savings in 2021. This is equi- sable income at end 2021.

Figure 3: US and European households’ savings, % of GDP (expected unleashed in 2021)

7.0

6.0

5.0

4.0

3.0

2.0

1.0

0.0

US

UK

Czechia

France

Norway

Austria

Germany

Sweden

Poland

Netherlands

Portugal

Belgium

Italy

Finland

Spain

Eurozone

Denmark

EU

Remaining HH excess savings potentially unleashed for investment or consumption purposes (% of GDP)

HH excess savings likely to flow into consumption (minimum, % of GDP)

Sources: : FRED, Eurostat, Euler Hermes, Allianz Research

Obstacle 3: Phasing out assistance me- Europe, meanwhile, has learned from no sooner than fall 2021, given the de-

chanisms is not a zero-sum game and its 2011-12 policy mistakes, when it pur- layed recovery prospects, which is

the risk of policy mistakes remains sued a pro-cyclical fiscal stance, but its bound to trigger a rise in unemploy-

high. Covid-19 fiscal response still pales in ment and insolvencies. Fiscal stimulus

In 2020, unprecedented monetary and comparison to the US. On the surface, may even surprise on the upside as Eu-

fiscal stimuli to the tune of 20% of GDP the story is one of the US doubling rozone governments underspent in

helped cushion the economic blow to down with an unprecedented fiscal 2020, as the sharp rise in government

global GDP. By early 2021, the consen- bazooka at a time when a recovery is deposits suggests (we estimate excess

sus to do “whatever it takes” is giving already starting to unfold, while Europe deposits at 3% of GDP). The EU’s Next

way to more heterogeneous policy has spent all its political capital on a Generation fund will only extend a

prospects. In China, for instance, policy stimulus that is too small, too drawn- helping hand from H2 2021 onwards

stimulus has already passed its zenith out and subject to heightened imple- and the growth impact (a cumulative

in line with the advanced economic mentation risk. However, headline fi- 1.5pp until 2025) should prove mode-

recovery. In fact, the path towards poli- gures are deceiving: we estimate Eu- rate and delayed, given its focus on the

cy normalization has already started, rope’s stimulus to be closer to 2/3 of the supply side – 2/3 of the EUR313bn

with official targets implying a clear US response when factoring in automa- grants are likely to be used for in-

withdrawal of policy support in 2021, tic stabilizers in 2020-21 (see Figure 4). vestment – and drawn-out payments.

even if some flexibility will be kept to For now, national fiscal policy continues Nevertheless, with NGEU funds not

manage credit risk if needed. The glo- to lead the show in Europe via ongoing counted under national deficits, they

bal demand torch will pass to the US, targeted support measures aimed at will help cushion the normalization of

where the gigantic fiscal stimulus to the keeping a lid on economic scarring i.e. fiscal policy. This is particularly true for

tune of USD1.9tn (9% of GDP) will pro- job retention schemes, transfers to the recovery laggards, including Spain and

vide a much-welcomed boost to global most impacted sectors and public cre- Italy. In any case, we expect EU fiscal

exports (USD362bn in 2021-2022, 2% of dit guarantees. We expect most EU rules to remain suspended until 2023.

total nominal trade). flagship fiscal policies to be phased out

5

Allianz Research

Figure 4: Infrastructure spending vs estimate gap, % of GDP Figure 5: Increase of working capital requirements and tax deferrals vs. NFC

“excess cash”, bn LCU, as of February 2021

45%

40% 180

Infrastructure Gap as % GDP (2020-30)

Tax deferrals, bn LCU

35% Infrastructure Plan as % GDP 160

Expected increase in WCR, LCUbn

30%

140 Remaining excess cash

120 100.3

25%

100

20% 95.0

80

15%

60 19.5

57.9

10%

40

5% 20 26.7

0% 0 -5.5

USA* EU ** China *** France UK Italy Germany Spain NDL

-20

* Build Back Better: $2 Trillion

** Next Generation EU 2021-23

*** China Infrastructure Plan 2020-25

Sources: Various, Euler Hermes, Allianz Research Sources: Various, Euler Hermes, Allianz Research

Most countries will continue to inject the new loans given in 2020 is expected neling excess savings to productive

liquidity and support companies and and would be equivalent to an increase projects. In addition to potential

jobs to avoid the sanitary and econo- of close to close to EUR15bn in the Eu- growth, we estimate that in advanced

mic crisis morphing into a financial and rozone as a whole or a rise of +0.8pp of economies, households’ financial assets

social crisis. Hence, the risk of policy the operating surplus to close to 4%. In (i.e. excess savings) are a key long-term

mistakes is high, negative externalities terms of the impact on NFC margins, determinant of the investment cycle

are visible (disconnect between finan- for the Eurozone countries on average (see Figure 6). The positive impact of

cial markets and the real economy; it would go from -0.3pp in 2022 to close excess savings on the durability and the

lack of price for credit risk, inequalities) to -2pp in 2023. The impact is expected magnitude of the new investment cycle

and rolling back state and central to be above Eurozone average in Bel- is significant in the US, Germany,

banks’ support will prove complicated. gium, Italy and Spain. Another credit France and the UK.

The risks are further protectionism, di- market risk: corporate bond redemp-

sorderly exists (taper tantrum for tions will increase by more than 70% in Besides the question of capital alloca-

example), scarring effects (private debt 2022 and double in the US. tion, tax policies will also play a deci-

levels) and more entropy across coun- sive role in funding these long-term

tries (especially as the political calen- Obstacle 4: Crowding-in vs. crowding- projects. In the US, Biden’s administra-

dar is heavy in Europe). out effects on investment are not yet tion aims at increasing the corporate

2022 will bring an (economic) reality resolved. The multiple initiatives in income tax from 21% to 28% and taxes

check for companies. Higher interest terms of infrastructure projects, inclu- on capital gains and the incomes of the

charges for non-financial corporates ding Joe Biden’s “Build Back Better” in wealthiest households. One of the pro-

are likely from next year onwards and the US (potentially USD2.3trn), the Next bable long-term legacies of the Covid-

we forecast a cumulated impact of Generation EU EUR725bn fund and 19 crisis, alongside the significant jump

close to -2pp at end-2023 for Eurozone China’s infrastructure plan totaling in public debt, relates to a probable

NFCs’ margins on average. An increase more than USD1.5trn by 2025, will all redefinition of the value-added sharing,

of low bank interest rates offered by contribute to support demand and the less in favor of profits and more in favor

the state-guaranteed loans will push global economy’s growth potential of salaries. The long-term success of

NFC interest payments on the upside over the medium-term (see Figure 5). In the new upcoming investment cycle will

as soon as 2022. An incremental in- this respect, their success will also rely certainly hinge on the progressiveness

crease of at least +50bp per year for on the efficacy of governments in chan- of these new fiscal orientations.

6

01 April 2021

Figure 6: Fiscal deficit, % of GDP

16.0%

14.0%

12.0%

10.0%

8.0%

6.0%

4.0%

2.0%

0.0%

USA China Eurozone UK

2020 2021 2022

Sources: Various, Euler Hermes, Allianz Research

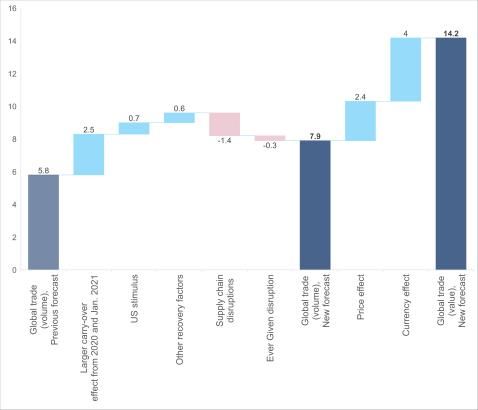

Obstacle 5: Bottlenecks in the global el. In 2020, trade in goods fell by -8.1% impact of supply-chain disruptions

supply chain are as high as during the in volume terms and -10.8% in value could weigh on global trade growth by

peak of the pandemic and should push terms. This was less than previously ex- -1.4pp, and by -0.3pp for the one week

global trade into a borderline recession pected, thanks to the rapid recovery in of immobilization in the Suez Canal. On

in Q2. Global trade growth will re- Asia and China. However, the tempo- the positive side, positive carryover

bound to +7.9% in 2021 (+5.4% exclud- rary supply-chain disruptions in H1 effects should boost global trade

ing positive carryover effects from 2021 (container shortages, higher growth by +2.5pp more than previously

2020) and +6.0% in 2022 in volume transportation costs, shortages of some expected, while the US super stimulus

terms, but a temporary slowdown is inputs such as semiconductors and raw and other recovery factors could add

expected in Q2 2021 due to prevailing materials, as well as the temporary +1.3pp. Overall, we expect global trade

supply-chain disruption (estimated to blockage of the Suez Canal) are likely to grow by +7.9% in 2021 in volume

cut 2021 volume growth of global to slow the flow of trade in goods. More terms (see Figures 7 & 8 and here for

trade in goods by -1.7pp). Trade in ser- specifically, we expect sequential more details). In value terms, strong

vices will remain impaired by the de- growth in trade to be only slightly posi- price and currency effects should push

layed reopening of sectors most im- tive in Q2 2021 and at risk of turning growth to +14.2% in 2021.

pacted by Covid-19-restrictions and negative if disruptions linger. For the

continued barriers to cross-border trav- full year 2021, we estimate that the

Figure 7: Global trade growth, goods and services, % y/y Figure 8: 2021 global trade forecast, % y/y

Asia Pacific North America Western Europe

Central and Eastern Europe Latin America Middle East and Africa

World (volume) World (value)

14.2%

15%

10.2% 9.8%

10% 8.6%

7.9%

6.0%

5% 5.3%

4.7%

3.9%

3.1% 2.8%

1.9% 0.9%

0%

-1.9% -1.6%

-5%

-8.1%

-10%

-10.8% -10.8%

-15%

14 15 16 17 18 19 20 21 22

Sources: IHS Markit, Euler Hermes, Allianz Research Sources: IHS Markit, Euler Hermes, Allianz Research

7

Allianz Research

Figure 9: Central bank’s balance sheets (Index Jan2005=100)

1400

1200 ECB Fed PBoC

1000

800

600

400

200

0

01/05

10/05

07/06

04/07

01/08

10/08

07/09

04/10

01/11

10/11

07/12

04/13

01/14

10/14

07/15

04/16

01/17

10/17

07/18

04/19

01/20

10/20

07/21

04/22

01/23

10/23

Sources: Refinitiv, Euler Hermes, Allianz Research

Obstacle 6: Temporary overshoot of Meanwhile, the ECB will continue to Obstacle 7: Not putting an end to the

inflation. Inflationary pressures will con- “walk the talk” in 2021 by boosting the sweet music of market’s reflation. The

tinue to increase notably in 2021, pace of asset purchases made under market frothiness following the Covid-

thanks to (i) the recent input cost bo- the PEPP in line with its stepped-up 19 shock has sparked claims of a fun-

nanza, driven above all by strained verbal intervention to protect favorable damental change in the functioning of

supply chains and the oil price recov- financing conditions. In 2022, the ECB capital markets. But have capital mar-

ery; (ii) higher services inflation along may get away with a slower pace of kets really detached from traditional

with the economic reopening in H2 and monthly QE purchases without endan- market cycles thanks to cryptocurren-

(iii) strong pandemic-related roller gering the strengthening recovery but cies and retail trading? The outreach,

coaster base effects. But we do not see in terms of active normalization steps it speed and amplification of market ral-

inflation embarking on structural up- will clearly lag the Fed as inflation will lies have certainly changed by the ex-

side trend as subdued demand dynam- remain subdued at 1.2% in 2022 after tensive use of new social networks, new

ics point to a potential head fake: (i) 1.4% in 2021. In contrast, in many online platforms and new digital assets.

excess savings from households and Emerging Markets, inflation has al- However, the underlying market pat-

NFCs that act as a drag on money ve- ready staged a meaningful comeback, terns seem all but new to us. The recent

locity; (ii) persistently negative output which central banks are unlikely to ig- rallies unite all patterns of a classical

gaps due to lower capacity utilization nore. In Africa, countries such as Ango- “late” market cycle boom: reliance on

and (iii) rising unemployment rates will la, Ethiopia, Nigeria and Zambia now leveraged investing to quickly multiply

keep a lid on wage growth (below 3%). boast double-digit inflation rates be- gains, stretched return expectations,

Therefore, we don’t expect central cause of FX depreciations and food appearing signs of market manipula-

banks to stage a policy U-turn as a re- shortages. In LatAm, we see Brazil most tion/fraud and overtrading due to Fear

action to inflation temporarily over- at risk, with high input price pressures of Missing Out (Figure 10). These are

shooting in the US at 3.5% by mid-2021 driven by supply-chain disruptions and worrying signs, but for the time being

and hitting the 2% target for a few FX depreciation now passing through the expansionary monetary and fiscal

months in the Eurozone (see Figure 9). to CPI. Inflation in Turkey, the Philip- policies shield risky assets from nega-

In fact, we expect policy normalization pines and India have also exceeded tive shocks. As long as this protection is

to proceed at a very gradual pace in central bank targets. in place, risky assets will be supported,

the US, kicking off with a first tapering even though late cycle phenomena will

step in H2 2022, while China will take occur more frequently and trigger epi-

credit growth lower very gradually. sodes of increased volatility.

8

01 April 2021

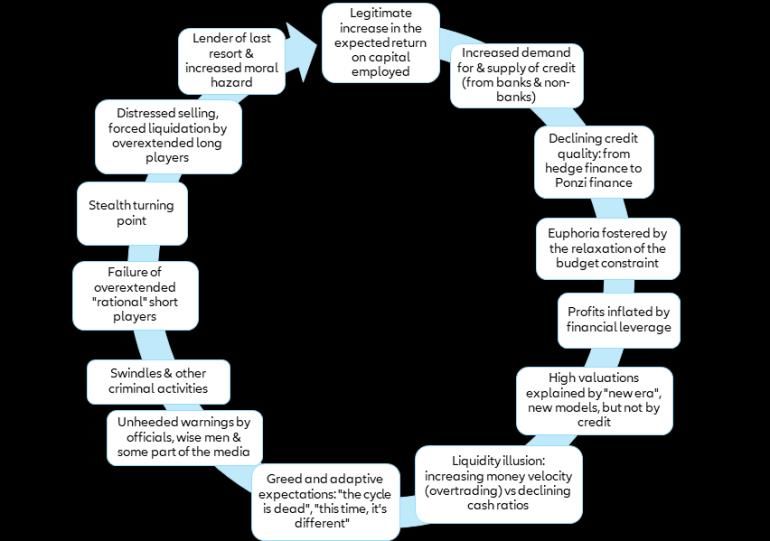

Figure 10: The Fisher-Minsky-Kindleberger model

Sources: Adapted from Charles Kindleberger’s Manias, Panics and Crashes a history of financial crises, 1978

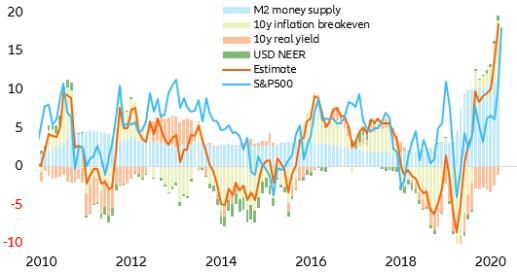

Is it a game of chicken or a tea party? is it possible that rising inflation expec- repricing of the uncertainty about the

However, on the bond markets, notably tations drive up US yields to an extent Fed policy timeline (tapering) and the

in the US, expectations have built up where they destabilize risky assets? extent of inflation overshoot tolerated

that central banks could withdraw their From a fair value perspective, the up- within the Fed’s “Average Inflation Tar-

support sooner against the backdrop of side for US long-term market-based geting” (AIT) framework. When correct-

stronger confidence in the global re- inflation expectations (breakeven rate) ing breakeven rates by its risk compo-

covery and rising inflationary pressure. seems limited. At currently 2.3% they nents (term and liquidity premia) -

Yields on 10y US Treasuries have al- trade more than 1 standard deviation which is recommended to obtain satis-

ready risen 70bp since the beginning of above our fair value estimate (2.3% vs factory predicting power on future in-

the year to 1.6%. So far, the pressure on 1.6%) (Figure 11). flation1 - we can see that inflation ex-

equity valuations has not been suffi- pectations already peaked at the end

cient to cause major market turbulenc- Indeed, the recent rise in breakeven of December (Figure 12).

es, also because valuation metrics rates is in fact not due to a shift in long-

might count less in such late cycles. But term expectation. It is rather due to a

Figure 11: US 10y breakeven inflation rate model (in %)

Sources: Refinitiv, Euler Hermes, Allianz Research

1

Andreasen, Martin M., Jens H. E. Christensen, Simon Riddell. 2020. “The TIPS Liquidity Premium,” Federal Reserve Bank of San Francisco Working Paper 2017-11

9Allianz Research

Figure 12: Uncertainty not expectations are repriced in breakeven rates

(in %)

Sources: Euler Hermes, Allianz Research

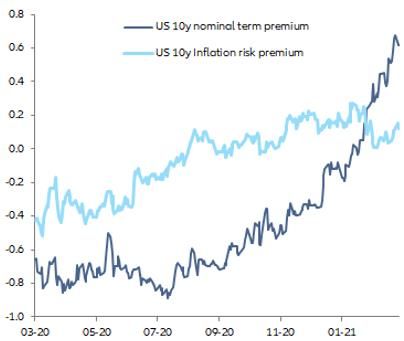

Accordingly, the recent rise of long- demand dynamics in US long-term the 2.0% or even 2.5% level (equal to

term US nominal yields is not due to treasuries. This means many market FOMC long-term rate target and cur-

higher expectations for short-term participants are betting on an early rent 10y10y forward) for 10y US

rates or long-term inflation, but to a tapering. This expectation could be Treasuries

higher risk component (Figure x). The further reinforced in the coming weeks

strong contribution of the term pre- when high CPI figures heavily distorted

mium in the recent increase indicates by base effects seemingly support this

an expected change in the supply- narrative. We could then see a test of

Figure 13: Decomposition of recent US yield rise (10y maturity)

Sources: Refinitiv, Euler Hermes, Allianz Research

1001 April 2021

If such a movement occurs quickly with having a tea party instead of playing a outside the Fed’s sphere of influence. A

erratic jumps it could cause a serious game of chicken over dominance. De- major risk from inside is a relapse to a

self-enforcing downwards spiral for spite a volatile episode in the coming mechanistic inflation targeting policy,

risky assets. However, our decomposi- months, we expect 10y US Treasuries including rapid rates hikes and early

tion shows that the Fed exerts full con- not to exceed current yield levels at the tapering. To gauge that risk, interven-

trol over the financial cycle. It can man- end of the year. In the range around tions of FOMC members must be

age the uncertainty on tapering, infla- 1.6%, some air seems to go out of hot watched closely. Currently we would

tion or rates by targeted statements market segments without creating ma- consider this risk to be rather low. The

without affecting long-term expecta- jor disruptions which the Fed may not risks from the outside could be related

tions – at least for now. In case of a ma- dislike. But with the cooperation of ex- to a market accident (liquidity, default

jor market turmoil, it would certainly pansive fiscal policy and loose mone- or fraud related), excessive regulatory

make use of this. There are indeed no tary policy, we will have to live with a tightening or strong taxation of profits

signs indicating the Fed might be stretched US curve prone to volatility. and/or transactions. In the current high

tempted to put an end to the current volatility environment, we see a market

cycle. It seems thus overly risky to bet The question is whether the financial accident as the biggest source of risk.

on an early tapering, especially when cycle could be stalled this or next year

monetary and fiscal policy seem to be and whether the cause will lay inside or

Figure 14: Markets are testing the Fed on early tapering

Sources: Refinitiv, Euler Hermes, Allianz Research

In the Eurozone, long-term market- Corporate credit remains strongly de- 16). For the moment, this is a correction

based inflation expectations have re- pendent on monetary policy. Like their after a strong rally, but the US high-

cently converged towards our fair value sovereign counterparts, corporate yield sector in particular remains a frag-

estimate of 1.3%. We believe that 10y bond yields also remain under the con- ile spot, especially given the large refi-

EUR inflation breakeven rates could still trol of central banks. In the near future, nancing needs in the course of 2022.

rise by around 20-30bps as the refla- the balance of risk might be skewed

tionary pressures are yet less present in towards higher spreads. However, cen-

the Eurozone. However, we believe that tral bank market intervention allows

a significant pricing out of the QE effect corporate spreads to navigate through

(strong increase in term premium) is pockets of equity volatility. We expect

very unlikely. In fact, the risks here are investment grade spreads to widen

currently more oriented in the other timidly in the US and Eurozone as QE

direction. Accordingly, we expect yields compensates for extra volatility and

of the 10y German Bund to remain sentiment deterioration (Figure 15).

broadly unchanged over the year and High-yield bonds, however, have been

only rise moderately in 2022. European under pressure recently, experiencing

risky assets could even find themselves substantial outflows and widening

in a favorable position, offering more spreads. The Covid-19 exposed sectors

upside potential than their US counter- (eg. energy and travel & leisure) seem

parts due to the delayed recovery. to have been the most targeted. (Figure

11Allianz Research

Figure 15: US y/y change in IG corporate spreads decomposition (in bps) Figure 16: US high-yield long-term fund flows

Sources: Bofo, Refinitiv, Euler Hermes, Allianz Research Sources: Bofo, ICI, Refinitiv, Euler Hermes, Allianz Research

Equity returns still a function of money What is happening with the USD? What about Emerging Markets?

supply. The USD is on appreciation trend vs the After a great divergence between Asia

Equity returns also remain strongly re- EUR on the back of faster-than- and other regions last year, some con-

lated to monetary conditions. Our US expected US economic growth and an vergence among EMs could be ex-

equity model shows that the monetary acceleration of foreign investment in- pected. However, in the first quarter of

component of equity returns remains flows int. But is this USD strengthening the year two key markets - Turkey and

the biggest contributor. Since the be- trend here to stay? Speculative positio- Brazil - are experiencing high volatility

ginning of 2021, the inflation compo- ning is now USD long. But the market- due to political turbulence.

nent has been gaining some traction, implied interest rate differential has yet In line with recent yield movements in

but the composition of equity return still to confirm the USD appreciation. Cur- the US, yields on local currency sove-

shows that central banks cannot wi- rently money markets still price in a flat reign bonds have been rising, especial-

thdraw monetary support without crea- interest rate differential until 2024. The ly for longer maturities. However, we do

ting a strong equity market correction current trend direction could well turn not think that this is a repeat of the

that would spill over into credit markets out temporary. As fundamentals do not 2013 tantrum. Growth forecasts are

and deteriorate the financing condi- give much leeway for a quick repricing well oriented and yield changes are

tions for the whole economy (Figure of monetary policy, we still believe in a contained so far. What remains the

17). In this context, we expect equity range trading EURUSD for 2021 (1.22 same is that in EMs the Fed still largely

markets to close the year with timid with upside volatility pockets) with a determines the financial cycle. So if a

single digit returns but to accelerate in mild structural (+2 to +3% yearly) ap- bumpy 2021 unfolds on US and Euro-

2022 on the back of a palpable econo- preciation of the USD in 2022. pean markets, EMs might see quite

mic recovery and still accommodative some agitation also, especially since

monetary policy. more than USD1trn of debt will have to

be rolled over in 2021 and 2022.

Figure 17: US equities yearly return decomposition (in y/y%) Figure 18: EURUSD and the interest rate differential

Sources: Refinitiv, Euler Hermes, Allianz Research Sources: Refinitiv, Euler Hermes, Allianz Research

1201 April 2021

Figure 19: Movements in EM yields. Bps change in the 10Y local currency bond since 01.02.2021 (LHS). Spreads in the HC sovereign bonds (RHS)

Sources: Refinitiv Datastream, BofA, Allianz Research. Only the biggest increases (LHS), and widest spreads (RHS) are displayed. In the RHS, the * indicates the Hard

Currency is the EUR, otherwise USD. The spread in the RHS accounts for Asset Swap Spread.

USD vs EM currencies. The USD has leading this trend. But there have been economic targets, Chinese equities

strengthened against most EM curren- also some other movements in Eastern have been correcting by more than

cies recently. Some Asian currencies Europe and Asia. We think that in the 10%. We now see signs of stabilization.

such the Thailand Baht or the Indone- current context slightly higher inflation Those signs are also observed in Tai-

sian Rupiah still have room for further will not harm and could even support wanese equities, which have been the

depreciation, while others already cor- the recovery, but a cocktail of stimuli clear winners of the equity rally in the

rected strongly in 2020 and could re- and unconventional monetary policies EMs so far. However, as the sector com-

cover some ground lost. However, idio- could trigger a dangerous spiral if the position is quite different, sector rota-

syncratic risks will remain high in the economic recovery disappoints. tion in an economic recovery could play

latter, making this recovery fragile and in favor of the Chinese equity market

unstable. Like in the US, inflation expec- Asian equities, the rally continues? instead of the heavily tech-

tations are also on the rise in EMs. The Since the return from Chinese New concentrated Taiwanese market.

usual suspects Turkey and Brazil are Year holidays and the release of official

Figure 20: Evolution of MSCI$ indexes since 31.12.2019 (rebased). Selected EM + US

Sources: Refinitiv, Euler Hermes, Allianz Research

13Allianz Research

REGIONAL

OUTLOOKS

In the US, President Biden’s stimulus households. There is a good chance sage a revaluation of salaries. Increa-

packages are set to create a strong that this will face political opposition, sing salaries in a too rapid manner

confidence effect on domestic de- including from moderate Democrats. would have been a too large burden

mand. In January 2021, the household Given the fact that the government will for the supply side of the US economy,

savings rate reached 20.5% of gross have to compromise, we consider a especially if the government targeted

disposable income. The success of the USD2.3trn infrastructure plan has a tax increases to fund its announced

vaccination campaign and the higher chance of being passed. Should infrastructure program. In the current

strength of the US fiscal stimulus, as the second leg of the plan be voted, it circumstances, we expect the US CPI

well as a healthy progression of hou- has the potential to boost growth si- inflation to reach 2.5% y/y in 2021, 2%

sing prices, will boost consumer confi- gnificantly above +6% y/y in 2021 and y/y in 2022 and 2.1% y/y in 2023.

dence, which for now remains below +4% y/y in 2022 compared to the

pre-crisis levels. On the back of this +5.3% y/y and +3.8% y/y we expect in The Fed in a wait-and-see mode does

confidence effect, accompanying stea- our current scenario. not mean an absence of volatility. Ta-

dy progress on the job front, we expect king into account the new fiscal im-

excess savings to be unleashed, gene- Positive externalities for US trade part- pulses of the US government, uur esti-

rating a strong impetus for consump- ners. The stimulus will also boost busi- mate of the Fed’s reaction function

tion. All in all, we expect household ness confidence, supporting non- suggests that a phase of monetary

consumption to grow by +5.5% y/y in residential investment. This increase in policy normalization could take place

2021 and +4.1% y/y in 2022 against – domestic demand will not be fully ab- much earlier. However, despite this

3.9% y/y in 2020. sorbed by US producers. We expect mechanical reaction suggested by the

the US trade deficit to widen to -4.5% model and a rapid disappearing of an

Fiscal policy will turbo-charge growth. of GDP on average over 2021-2022, output gap at -3.6% of potential GDP

On top of the recently announced compared with -2.9% on average over in Q4 2020, we continue to believe that

USD1.9trn fiscal package, the US go- the past five years. More precisely, we a first tapering phase will only be vi-

vernment wants to add another round estimate that a +1% increase in domes- sible starting in H2 2022. The current

of stimulus with a USD2.3trn infrastruc- tic demand leads to a +2.6% rise in proximity between the Fed Funds tar-

ture program to renovate roads and imports in the US. The wage–inflation get rate and the natural rate of inte-

bridges and develop new types of digi- loop will not be re-activated as the rest (point below which the monetary

tal infrastructure, while continuing to doubling of the federal minimum policy exerts significant inflationary

invest in health and education to re- wage was not voted in the Congress. pressures on the economy) shows that

duce inequalities. The first leg of this We calculated that this initiative had the Fed, in line with the recent commu-

infrastructure program would be fun- the potential to install CPI inflation nication stance of Chairman Powell,

ded via an increase of the corporate durably above 4% y/y. The government has some time before really envisa-

tax rate from 21% to 28%. The second will give the priority to fiscal incentives ging a tightening in US monetary poli-

social leg of this program would have targeting small- and medium-sized cy. We don’t expect a rate hike before

to be financed via higher capital gains companies in particular in order to H2 2023.

taxes and higher tax rates on wealthy encourage the business sector to envi-

1401 April 2021

Europe remains the eternal recovery not fully compensate for the delayed phase of the recovery. Nevertheless, in

laggard compared to other economic reopening as 20% of economic activity comparison to other economic heavy-

heavyweights. In 2021, we expect the remains heavily impacted by Covid-19 weights, Europe’s recovery looks set to

European economy to race at a rapid restrictions. From mid-2021 onwards, all disappoint, with key drivers being its

pace through the entire economic cy- eyes will be on the strength of the con- delayed vaccine rollout and its smaller

cle, from a double-dip recession at the sumption-led reopening rebound fol- and more drawn-out fiscal response.

start of the year to a consumption-led lowing an extended period of econom- Even though base effects should prove

catch-up growth spurt in the second ic hibernation. We expect pent-up de- favorable for Europe, given that it rec-

half of the year. The third wave of mand to supercharge growth in 2021, orded a larger GDP contraction in 2020

Covid-19 infections, which saw several with around one third of the EUR530bn than the US, growth prospects for 2021

Eurozone heavyweights including Ger- in excess household savings to be un- are notably lower. We expect Eurozone

many, France and Italy prolong and/or leashed. At the same time, policymak- GDP to expand by +4.0% in both 2021

retighten lockdown measures, will post- ers will continue to do “whatever it and 2022, while acknowledging elevat-

pone the expected economic resurrec- takes” to safeguard the recovery and ed downside risks for H1 2020 should

tion until mid-Q2, when progress on the shore up public support ahead of key the lockdowns be tightened further

vaccination front should allow for a elections in Germany (September 2021) and/or be prolonged and for thereafter

gradual, and most importantly sustain- and France (April 2022). Flagship fiscal should the vaccination rollout fall be-

able, economic reopening. Thankfully, measures including furlough schemes hind our expectations. Overall, we ex-

strong export demand – driven by the (which will see the unemployment rate pect the Eurozone economy to recover

ongoing Chinese recovery and super- peak below 9%) and public guarantees to pre-crisis GDP levels in H1 2022, al-

charged, stimulus-induced US GDP will be extended at least until fall 2021, most a full year after the US, whereas

growth – will extend a helping hand to whereas the ECB will continue to lean some member states, including Spain

European economies in 2021, in turn against rising yields by front-loading and Italy, will need an additional year

exacerbating the divergence between PEPP purchases to ensure favorable to heal.

manufacturing and services. But it can- financing conditions during the early

Figure 21: Real GDP, Q4 2019 = 100, pre and post Covid-19 Figure 22: Global GDP growth, %, for 2021 and 2022

120

115

110

105

100

US

95 US pre-Covid

Eurozone

90 Eurozone pre-Covid

China

China pre-Covid

85

2019-10 2020-04 2020-10 2021-04 2021-10 2022-04 2022-10

Sources: National sources, Euler Hermes, Allianz Research Sources: Various, Euler Hermes, Allianz Research

15Allianz Research

Germany’s GDP will expand by +3.4% in to support the green and digital transi- contribution to GDP growth of 0.3pp. The

2021 and +3.8% in 2022 as external tail- tion, with a return to the debt brake not Biden stimulus plan will give a significant

winds make up for the delayed recovery before 2023. boost (9 bn EUR) to exports in pharma-

in domestic demand, allowing for a re- ceuticals, transport equipment and agri-

turn to pre-crisis GDP levels by early We expect the French economy to grow food in 2021 and 2022.

2022. With Germany moving into its third by +5.4% in 2021 and by +3.6% in 2022, France’s corporate debt overhang will

lockdown just ahead of Easter, its do- thanks to recovering demand (both do- certainly become a long-lasting issue.

mestic economic resurrection will face mestic and external). A return to a nation Already high, French corporate debt soa-

another delay until mid-Q2 2021. Howe- -wide confinement, with school closures red to 86% of GDP (+12pt) in Q3 2020,

ver, strong extra-EU export demand for four weeks in April, is expected to well above the Eurozone average of 68%

should once again help Europe’s largest reduce growth by -1.5pp in Q2. On the of GDP (+6pt). The repayment of state-

economy weather this renewed setback other hand, the speeding up of the vacci- guaranteed loans will start as of March

for private consumption better than its nation pace (with herd immunity to be 2022 but these loans are only a small

European peers. After all, supercharged, reached in June instead of in October) part of the indebtedness problem. In

fiscal stimulus-induced US import de- will enable a stronger economic rebound order to sustain the new investment cycle

mand, together with resilient appetite in July and August. Strong state support and the solidity of the banking sector,

from China – German exports to both (EUR30bn has been spent for the partial the French government ought to provide

countries tally up to a combined 15% – unemployment scheme) helped preserve a comprehensive roadmap. Consolida-

should provide a further tailwind to al- household incomes and build excess ting all corporate debt (regular loans +

ready booming industrial production, in savings to around EUR130bn. After a state-guaranteed loans + unpaid tax

turn exacerbating the divergence bet- slight increase (+0.6%) in 2020, we ex- and social contributions) under a single

ween buoyant industry and depressed pect households’ purchasing power to umbrella and restructuring it over a lon-

services. In the short-run, supply-chain decline only marginally (by -0.6%) in ger period could be a viable solution.

strains including long delivery times and 2021 on the back of accelerating infla-

input shortages could weigh on activity tion (1%). Pent-up demand after the ea- Itay’s GDP contracted by -1.9% q/q in Q4

but we don’t expect widespread produc- sing of sanitary restrictions will boost 2020, driven primarily by lower private

tion disruptions to derail the manufactu- consumption in the second half of 2021. consumption and a reversal in net trade.

ring upswing. If 50% of it consumed, excess savings However, manufacturing still runs at full

accumulated could add up 3pp to GDP speed, driven by the production of in-

Meanwhile, private consumption mean- growth this year. The government will termediate goods, confirming Italy good

while is ready for take-off as soon as late most probably extend the partial position in global value chains. Industrial

-Q2 when sufficient progress on the vac- unemployment scheme for Covid- production stands at only 2.4% below the

cination front will allow for a gradual sensitive sectors as hidden unemploy- level one year before. Services and retail

easing of Covid-19 restrictions. Services ment and under-employment may continue to bear most of the recessive

activity should further shift into overdrive become an important issue ahead of the effects of the restrictions. This divergence

in H2 2021 as excess savings to the tune Presidential elections in 2022. is going to intensify as Italy entered a

of at least 1% of GDP are unleashed till third lockdown in mid-March. The speed

year-end, helped by the relatively solid The recovery of corporate investment of the 2021 economic recovery will there-

labor market outlook (unemployment proved to be resilient in France as of the fore be even more dependent on the

rate forecast at 5.5% in 2022 after 6% in second half of 2020. The need to adapt pace of vaccinations. Italy is in the Euro-

2020). to the Covid-19 environment, the liquidi- pean average here (11% of population

ty support from state -guaranteed loans vaccinated). In this context, we expect

Fiscal policy will remain very supportive and the normalization of demand will another GDP contraction of -0.6% in Q1

in 2021 and unspent funds earmarked continue to support the new investment 2021. However, with the recovery picking

for 2020 (around 3% of GDP) pose an cycle in 2021. Covid-19 state support up speed in mid-Q2, Italy’s GDP should

upside risk to fiscal stimulus. The sharp measures to non-financial companies still grow by +4.1% this year and +4.2%

acceleration in consumer prices towards (Empowered Solidarity Fund, state- next year. Private consumption will be

3% y/y in H2 2021, due to the marked guaranteed loans, social contribution the main driver of this recovery as the

pick-up in growth momentum, rising and tax deferrals/cancellations) conti- short-term work scheme and the redun-

energy prices and strong base effects nue to support businesses’ cash positions. dancy ban continue to stabilize employ-

from the H2 2020 VAT reduction should We expect business margins to recover ment and disposable income. The priori-

prove to be temporary and any calls for moderately to 31.1% in 2021 (after a ty for the Draghi government is the com-

monetary policy tightening at that stage sharp decline of 3.8% in 2020) on the pletion and implementation of the Ita-

would be clearly premature. The back of recovering demand and the ea- lian recovery plan. The current draft in-

unusually uncertain September election sing of sanitary restrictions (i.e. higher cludes expenses of EUR310bn over six

outcome will set the course for fiscal poli- productivity). years (EUR210bn comes from the EU

cy in the coming years. The still most li- We have revised our international trade recovery fund), of which 70% should be

kely scenario of a CDU-Green party coa- forecast upwards. In 2021, we expect allocated to investments.

lition will probably see higher investment exports to grow by +9.4% in 2021, which

and social spending in the coming years will translate into a positive net trade

1601 April 2021

If invested wisely, it has the capacity to (GBP101.4bn at the end of January, or manner. On the fiscal side, we estimate

lift potential output by up to 8% over the 4.5% of GDP). The hyper-amortization that after 7.1% of GDP in 2020, support

next 10 years. This would also make pu- scheme at 130% coupled with excess will decline to 4.6% of GDP in 2021, with

blic debt more sustainable (topping cash and the state-guaranteed recovery less infrastructure spending. But this re-

close to 160% of GDP). The main levers loan scheme should help business in- mains relatively generous compared to

for achieving this remain structural re- vestment recover fast in 2021 (we expect the past (2.9% on average in 2018-2019).

form in institutions (juridical system, red +12.5% vs. the +17.2% needed to catch On the monetary side, the policy stance

tape) and increasing the participation up with the fall in the capacity utilization already started to tighten in Q4 2020,

rate, especially among women. rate). In addition, positive confidence and this should continue in 2021 through

effects linked to the vaccination cam- liquidity and regulation (see more details

In Spain, four in 10 companies ended paign (herd immunity expected in May) here). In this context, there is room for

2020 subjected to great financial pres- and to the reopening of the services sec- further appreciation of the renminbi, al-

sure, as measured by the Bank of Spain, tor should feed into a strong depletion of though most of it may already be past.

a +27pp increase compared to 2019. excess savings from households (1.9% of We expect the USDCNY onshore rate

Despite the new EUR11bn plan to bolster GDP). towards 6.3 at the end of 2021 (vs. 6.5 at

solvency, the risk of high insolvencies this end-2020 and 7.0 at end-2019).

year and in 2022 remains elevated. On the other hand, Brexit is expected to

Renewed targeted sanitary restrictions cost growth around 1pp to 2pp in 2021. In Asia-Pacific as a whole, we expect

and a fall in mobility could lead to a In January, UK exports of goods fell by GDP to expand by +6.6% in 2021 (after -

renewed GDP contraction in Q1 2021, more than GBP5.6bn and we expect bet- 1.1% in 2020) and +4.7% in 2022. These

delaying the recovery. On the other ween GBP12bn and GPB24bn of losses solid rates of growth mask uneven reco-

hand, a slow vaccination rollout should in 2021 depending on how long-lasting very speeds, given different states of the

allow Spain to only gradually remove the disruption at the border will be. Addi- pandemic, external exposure and policy

restrictions in Q2. We thus expect a tional downside risks to the scenario are reactions. While the pandemic is overall

stronger recovery in the second half of linked to potential tariff increases from under better control in Asia-Pacific than

the year, with real GDP growing +4.8% the EU side as a retaliation to the UK’s in other regions, India and the Philip-

this year after falling -11% last year, fol- unilateral decision to extend the transi- pines are showing signs of renewed

lowed by growth of +5.7% in 2022. We tion period for full border checks in Nor- outbreaks. Vaccination is lagging

expect the unemployment rate to peak thern Ireland. Finally, negotiations have (except in Singapore), with some econo-

at 16.5% this year before gradually de- started on the equivalence for financial mies not in a sanitary urgency (eg. Tai-

creasing but remaining at an elevated services, on which both the EU and the wan, China, Vietnam, Australia etc.),

level (15.2% in 2022). The government’s UK maintain a hard stance. while others more in need face supply

stimulus should focus on public in- and distribution issues (eg. Indonesia,

vestment, which could lead to a higher In China, the post-Covid-19 recovery is Malaysia, the Philippines and India to a

fiscal multiplier. In 2021, the government well underway, and 2021 will focus on lesser extent). Policy space for further

is looking at EUR25bn of measures, mos- policy normalization. The 2020 rebound economic support is also more limited in

tly in public infrastructure investment was mostly a story of policy-driven areas some of these latter countries, given debt

(green and innovation). However, the such as the real estate and infrastructure sustainability concerns and inflation

previous take-up of EU funds is low (34%) sectors. In 2021, household consumption pressures. Externally, the environment

in Spain and public sector effectiveness and business investment could become will drive growth for economies exposed

also relatively low (lower than France, the growth drivers. The external environ- to the early recovery of China, the elec-

Portugal but higher than Italy): this ment will continue to be supportive as tronics value chain and the US super sti-

means Spain risks missing out the full many of China’s trading partners are still mulus (in particular for Taiwan, Vietnam,

potential of the EU-led recovery. battling the pandemic and their policies South Korea and Singapore), while the

are in full easing mode. We expect the Philippines and Thailand’s strong expo-

In the UK, the fast vaccination campaign Chinese economy to grow by +8.2% in sure to tourism will weigh on their econo-

is counterbalancing negative effects 2021 (after +2.3% in 2020) and +5.4% in mic recovery. The Regional Comprehen-

from Brexit: We have revised on the up- 2022. Should China’s quarterly GDP in sive Economic Partnership should further

side our GDP growth forecast for the UK 2021 be unchanged from Q4 2020, foster regional trade integration after it

from +2.5% to +3.7% in 2021. This is growth in 2021 overall would still land at enters into force likely in 2022. Overall,

driven by the additional fiscal spending the relatively high level of +6.2%. This upward revisions to the 2021 economic

announced within the 2021 budget (3.2% means that the official target of “above outlook in the Asia-Pacific region are

of GDP), which will provide a tailwind of 6%” will be very easy to achieve, allowing mostly led by Singapore, Vietnam and

up to +1.1pp to real GDP growth in 2021. policymakers’ focus to shift away from Taiwan, while Malaysia, Thailand and

Support measures have been prolonged short-term stimulus to financial vulnera- the Philippines were revised on the

to three months beyond the date of all bilities and asset price bubbles (in real downside.

restrictions being lifted (until end- estate and capital markets). We don’t

September) and should continue to pro- expect a policy cliff and normalization

tect companies' excess cash should be done in a flexible and gradual

17Allianz Research

Emerging Markets (EMs) are heading for already returned to Africa in 2020: Ango- cast to recover to +3.7% in 2021 (from -

a multi-speed recovery amid vaccination la, Ethiopia, Nigeria and Zambia are 2.7% in 2020), followed by +3.4% in 2022.

hurdles as well as diverging space for struggling with double-digit inflation on Third waves of Covid-19 infections are

fiscal stimulus to boost growth. The UAE, the back of strong currency deprecia- underway, especially in Central Europe,

Chile and Bahrain are top performers in tions in 2020 and food shortages due to and lockdown measures have been

the vaccination rollout, with 26%-76% of adverse climate events. raised to relatively stringent levels in the

the populations having received at least The Covid-19 shock has also accelerated major economies towards the end of Q1

one dose. However, vaccination rollout is the ongoing debt accumulation trend in 2021, except for Russia. Since the pro-

progressing very slowly in most EMs, in- EMs. The time bomb of record-high pu- gress on vaccination is slow, we expect

cluding Brazil, Mexico, Colombia, Peru, blic debt is ticking ahead of substantial the lockdown measures to be relaxed

Saudi Arabia, most Central European debt refinancing needs in 2022-2023. only gradually in the course of Q2,

countries, Indonesia, Malaysia the Philip- Overall external financing requirements pushing the recovery of Covid-19-

pines and a large part of the African are very high for Turkey, Romania, Hong sensitive services sectors to H2 2021. Ac-

continent. Less developed and poor Kong, Pakistan, Argentina and Chile, cordingly, consumer sentiment has re-

countries relying on the COVAX initiative while debt sustainability is at risk in Bra- mained subdued. However, the outlook

for vaccine supply are very unlikely to zil, Argentina, India, Malaysia, Angola, for the industrial sector is fairly positive

reach her immunity this year. Tunisia and Ethiopia. as reflected in solid growth rates and

manufacturing PMIs. Occasional supply-

Besides the speed of vaccine roll out, After a tumultuous 2020, currency pres- chain disruptions will make the recovery

fiscal leeway for stimulus is another key sures eased in early 2021, except for Ar- bumpy but not affect the full-year perfor-

determinant of EM growth prospects in gentina, Brazil and Turkey. Although cur- mance. Meanwhile, accommodative

2021-2022. We expect a K-shaped reco- rent account balances are in better monetary and fiscal policy will continue

very in EMs as larger countries in Emer- shape than in 2013, a repeat of the taper to support most economies over the next

ging Asia and Central Europe as well as tantrum in the event of the eventual two years or so. Ukraine and Russia,

Turkey manage to provide relatively tightening of US monetary policy cannot however, have already began a moneta-

strong fiscal support to their economies, be excluded for EMs. Turkey, Nigeria, ry tightening cycle as inflation exceeded

while there is more limited fiscal space in Ukraine, Argentina, Kenya, South Africa central bank targets but we expect poli-

Argentina, Brazil, Russia, the GCC and and Chile are currently the weakest cies to remain credible.

most African countries struggling with spots in this context, owing to still relati-

debt. On the positive side, the recovery of vely large current account deficits, mo- The same cannot be said for Turkey,

commodity prices and sustained Chinese derate to low FX reserves, elevated infla- which fired its central bank governor in

demand should be a tailwind for expor- tion rates as well as currency volatility March after six months of appropriate

ters such as Nigeria, Algeria, Angola, and high sovereign bond spreads. Loo- interest rate hikes that had calmed fi-

Chile, Peru and Brazil in 2021. Econo- king ahead, EMs over-relying on short- nancial markets. Turkey will most likely

mies that are dependent on trade in term foreign financing and having poor revert to its known unorthodox monetary

goods (particularly electronics/ growth prospects (i.e. large real interest policy style, which could maneuver the

technology goods) or have strong trade rate-economic growth differentials) will economy once again close to the next

links to China are set to continue to per- be more vulnerable to the changing ap- currency crisis. We also identify Hungary,

form better (e.g. South Korea, Taiwan, petite of global investors. Romania, and to a lesser extent Poland

Vietnam). and Czechia, as facing increased infla-

Finally, rising unemployment is a key tionary pressures in the next two years,

However, the return of inflation, after a area of concern that could feed political though rising unemployment should mo-

few quiet years, is bad news for the post- and social tensions. Official unemploy- derate wage growth and mitigate these

Covid economic recovery. In Latin Ameri- ment rates rose to record high levels in pressures in 2021 at least. Fiscal policy

ca, Brazil is most at risk of high inflation, most EMs (South Africa 30.8%, India leeway is diverse amid rising public debt

with high input price pressures due to 10.6%, the Philippines 10.3%, Indonesia levels. Czechia and Poland are stimula-

supply-chain disruptions and the curren- 7.9%, Colombia 17.3%, Brazil 13.8%, Chile ting their economies the most, while ele-

cy depreciation now passing through to 10.2%) yet these numbers are only the tip vated public debt in Croatia, Hungary,

consumer prices. Turkey has exceeded of the “hidden unemployment” iceberg. Romania and Ukraine require close mo-

the central bank inflation target for ma- nitoring.

ny years and the Philippines has done so In the Emerging Europe region as a

since the beginning of 2021. Inflation whole, annual real GDP growth is fore-

18You can also read