REFLECTIONS ON THE LAST 20 YEARS: HOW FAR HAVE WE COME? - INSIGHTS ON THE INVESTMENT OF IPPS AND RENEWABLE ENERGY IN SUB-SAHARAN AFRICA ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Africa

REFLECTIONS ON THE

LAST 20 YEARS:

HOW FAR HAVE WE COME?

INSIGHTS ON THE INVESTMENT OF IPPS AND

RENEWABLE ENERGY IN SUB-SAHARAN AFRICA

in partnership with

Africa

WWW.AFRICA-ENERGY-FORUM.COM | WWW.GSB.UCT.AC.ZA | WWW.IFC.ORG

REFLECTIONS ON THE LAST 20 YEARS: HOW FAR HAVE WE COME?

As we review the progress made in private involvement in the energy sectors in sub-Saharan

Africa over the last 20 years, IFC and the Management Programme in Infrastructure Reform

and Regulation (Graduate School of Business, University of Cape Town) have been invited to

share their perspective and findings on where we’ve been and where we’re going.

IFC has been a large part of a fascinating story. They were there at the start, and have seen

Africa infrastructure business grow, to a level where it is now a billion dollar business for them

each year. It’s not all about volume, however; and, as we look forward to the next 20 years, we

establish what opportunities are growing and who will be at the forefront shaping the agenda.

20 Years of IFC Investment in Sub-Saharan Africa’s Power Sector

FY1998-FY2017

(Graph Source: International Finance Corporation (IFC) World Bank Group)

Azito and CIPREL power plant

WWW.AFRICA-ENERGY-FORUM.COM | WWW.GSB.UCT.AC.ZA | WWW.IFC.ORG

REFLECTIONS ON THE LAST 20 YEARS: HOW FAR HAVE WE COME?

Insights into power generation in sub-Saharan Africa

Sub-Saharan Africa (SSA) has a severe shortage of power. Electricity demand is set to double by 2030, and triple by 2040.

Currently, including South Africa, Sub-Saharan Africa has less generating capacity installed than Spain (110 GW). The

continent also has the lowest electricity consumption globally, measured in kWh per capita. To meet projected demand, a

recent report by a leading consultancy estimates that more than $490 billion will need to be invested in additional power

generation capacity by 2040.

Investment in sub-Saharan African power generation is increasing…

While investment levels in power generation remain far below what is required, there are encouraging signs of acceleration

in investment volumes.

After a disappointing decade in the 1990s, where very little new capacity was added, the past decade and a half has seen

around 20 GW of new generation capacity added (excl. South Africa), concentrated in a dozen countries:

Nigeria (4,6 GW) Cote D’Ivoire (0,8 GW)

Sudan (3 GW) Cameroon (0,7 GW)

Ethiopia (2,2 GW) Zambia (0,7 GW)

Ghana (1,7 GW) Senegal (0,7 GW)

Kenya (1,3 GW) Uganda (0,6 GW)

Angola (1,1 GW)

…though this has been limited to a few large projects…

There have been three main investment peaks in private power generation in sub-Saharan Africa (excl. South Africa), when

a number of large IPPs reached financial close, tempered by troughs in 2002/3 (Enron collapse) and 2009/10 (global

financial crisis) (Figure 1)

IPP capacity additions in sub-Saharan Africa (excl. RSA), 1994 – 2017

(Figure 1)

Source: Graduate School of Business, University of Cape Town

WWW.AFRICA-ENERGY-FORUM.COM | WWW.GSB.UCT.AC.ZA | WWW.IFC.ORG

REFLECTIONS ON THE LAST 20 YEARS: HOW FAR HAVE WE COME?

• THE 1999 SPIKE:

When IFC financed Cote d’Ivoire’s CIPREL and 288 MW Azito Open Cycle Gas Turbine project, justifying the involvement of

DFIs was easy. Providing finance directly, and comfort to co-financiers through the syndications programme, was adding value.

At that time, the IPP market seemed poised to take off with the inclusion of the 220 MW (phase one) of the Takoradi II

OCGT project in Ghana as well as the 75 MW Tsavo (diesel) project in Kenya. Power sector reform and restructuring was

all the rage, and unbundled power markets and spot sales seemed just around the corner.

This did not materialize. IFC is a part of the financing of most big deals – but in the 90s, and through the early years of the

noughties, IFC averaged closing only a deal every other year. The huge infrastructure financing gap, identified by the World

Bank and others (then >US $40bn a year, though it’s thought to be bigger now), was not being filled by the private sector.

And sector reform proved elusive in many cases too. Whilst many countries set up independent regulators, their “independence”

was often challenged by governments reluctant to approve politically unpopular tariff increases. In the meantime, more and

more DFIs entered the fray to try to accelerate things. In the 1990s, IFC had been close to being the only DFI for private

infrastructure in town but by the time Bujagali hydro project was closed, in 2007, there was the, nowadays familiar, alphabet

soup of DFIs in the deal, including FMO, Proparco, ADB, AFD, DEG, EIB, KfW, as well as commercial lenders under IDA partial

risk guarantee cover - Standard Chartered UK, ABSA, BNP Paribas, and Nedbank. And, as the first privately financed hydro deal

in Africa, the development impact of Bujagali was huge – but follow-on hydro deals have been slow in coming down the line.

Source: International Finance Corporation (IFC) World Bank Group

• THE 2007 - 2009 SPIKE:

Projects include:

Rabai (90 MW MSD/HFO, Kenya) Afam VI (630 MW CCGT, Nigeria) and Centrale thermique de Lome (100 MW

DFO, Togo) in 2008; and Dibamba (88 MW HFO, Cameroon), CIPREL (111 MW OCGT, Cote D’Ivoire) and CENIT

Energy (110 MW OCGT, Ghana) in 2009.

Source: Graduate School of Business, University of Cape Town

By then it was becoming clear that the historical shortage of deals wasn’t due to a shortage of finance. IFC had spent

millions of dollars of internal resources working on the Bujagali hydro project, over a period of 10 years, which its lender’s

margins could not recompense. It became increasingly clear that the problem of private power in Africa wasn’t a lack of

funds. Indeed, following the crash of 2008 and the drop in equity return prospects worldwide, there was increasingly no

shortage of equity: for a while, new funds seemed to appear every week.

The problem was (and remains), increasing the pipeline of bankable deals. For IFC, the option of sitting back with other

banks and waiting for deals to happen did not resonate with its development mandate. To have real impact, IFC needed to

change the model and move up the development chain.

Work began on IFC InfraVentures with an initial US$100m, in an attempt to leverage the contribution to the project development

space, acting in a partnership role with other developers. Other DFIs have followed suit: the PIDG group of donors, led by

DFID, has also established InfraCo to do something similar. Bilaterals, such as FMO are also establishing project development

vehicles, often targeting smaller deals, and recently the African Development Bank has created Africa50 with funding mostly

from African governments. IFC has value to add in this space: providing more capital to take early risks in the development of

projects, providing comfort to governments that deals will balance public and private interests, managing environmental and

social concerns in a sustainable fashion, and, at the same time, ensuring that the projects can be banked.

Source: International Finance Corporation (IFC) World Bank Group

Africa

WWW.AFRICA-ENERGY-FORUM.COM | WWW.GSB.UCT.AC.ZA | WWW.IFC.ORG

REFLECTIONS ON THE LAST 20 YEARS: HOW FAR HAVE WE COME?

The period 2012 up to 2014 saw a steady increase in investment, with 2014

accounting for the largest investment in SSA (excluding South Africa) in a

single year.

• THE 2014 SPIKE:

This peak in 2014 was largely associated with the 350 MW CCGT Cenpower Kpone IPP in Ghana and the 300 MW Lake

Turkana wind (onshore) project in Kenya. While investments in 2015 were slightly lower than 2014, it saw the largest

private power capacity (MW) addition to date. The 2015 peak is contributed mainly by three projects: the 459 MW (OCGT)

Azura project in Nigeria, the 300 MW Coal Maamba mining-and-power project in Zambia and the 250 MW (OCGT) Ameri

Project in Ghana.

Source: Graduate School of Business, University of Cape Town

• THE 2016 SPIKE:

While there seems to have been a relative slow-down in capacity (MW) additions in 2016 and 2017, it is striking that these

are the two years that have seen the largest number of private power projects reaching financial close. This trend can in large

part be explained by changes in generation technology, with smaller renewable energy projects (mainly solar PV and small

hydro) procured mainly through competitive bids or feed-in tariffs (for example, GETFiT in Uganda and REFiT in Namibia).

Source: Graduate School of Business, University of Cape Town

Africa

WWW.AFRICA-ENERGY-FORUM.COM | WWW.GSB.UCT.AC.ZA | WWW.IFC.ORG

REFLECTIONS ON THE LAST 20 YEARS: HOW FAR HAVE WE COME?

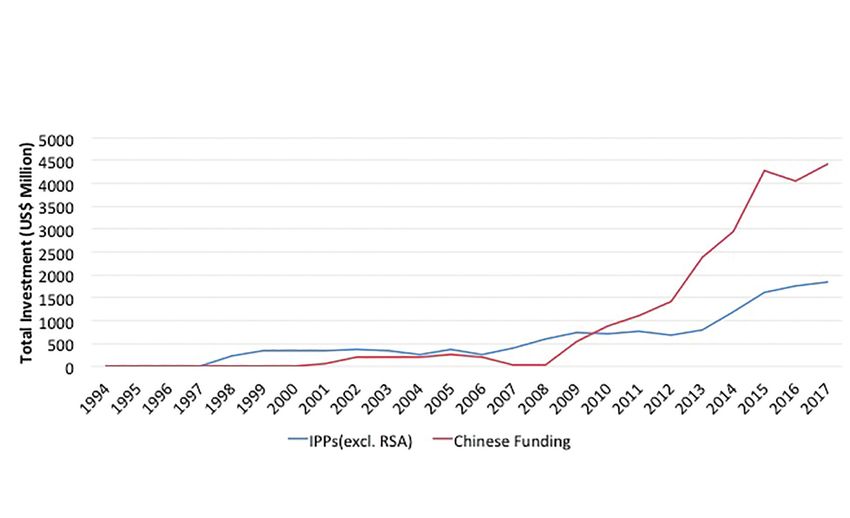

IPP and Chinese power investments in SSA

US$ Million – 5 year rolling average, excluding South Africa

(Figure 2)

Source: Graduate School of Business, University of Cape Town

During the last decade, we have seen new sources of investment, and new types of projects. Chinese funded projects,

along with IPPs, have recently become the fastest growing sources of investment in the region’s power sector (Figure 2).

Source: Graduate School of Business, University of Cape Town

There is also an increasing appetite from Chinese agencies and public and private investors to try out new (for them) business

models in Africa, working much more under classic procurement and project finance paradigms, and paying more attention

to global environment and social performance standards.

Source: International Finance Corporation (IFC) World Bank Group

Renewable energy is also now breaking through (Figure 3), and in many countries is now the cheapest source of grid-

connected power. South Africa’s renewable energy independent power producers procurement programme (REIPPPP) has

now contracted 92 projects and attracted US$ 19bn investment, with solar PV costs falling 80% and wind 50% since 2012.

The IFC Scaling Solar programme auctions in Zambia and Senegal have also delivered highly competitive prices – US $

6 cents per kWh in Zambia on the deal closed recently, and US$4.7 cents per kWh in the recent round of bids in Senegal

– extraordinary, record-low prices for sub-Saharan Africa. Other countries with competitive procurement programmes

include Ghana, Ethiopia, Namibia and Malawi.

Source: Graduate School of Business, University of Cape Town

Africa

WWW.AFRICA-ENERGY-FORUM.COM | WWW.GSB.UCT.AC.ZA | WWW.IFC.ORG

REFLECTIONS ON THE LAST 20 YEARS: HOW FAR HAVE WE COME?

Cumulative private (IPP) MW installed for solar photovoltaic (PV), onshore

wind and small hydro, 1994–2017 in sub-Saharan Africa

(Figure 3)

Source: Graduate School of Business, University of Cape Town

Recent data show that a rapidly growing portion of these IPPs is renewable energy-based (Figure 3), many of which have

been competitively procured (Kruger and Eberhard, 2018).

Three trends represent important departures from the status quo in the sub-Saharan region:

• The surge in private power investment

• The growth in competitively priced renewable energy projects

• The use of competitive procurement (auctions) for IPPs

Auctions, although quite recent, have already delivered more investment in renewable energy at lower prices

than any other procurement or contracting method for the region. In sub-Saharan Africa, at least 18 countries

are currently in the process of developing and implementing a renewable energy auction programme; more than half of

these programmes were launched in 2017 alone (Kruger and Eberhard, 2018). Many African countries have struggled to

successfully address the risks and costs involved in renewable energy auctions, resulting in potentially poor outcomes.

Additionally, many countries are desperate for affordable power generation investment, yet cannot afford the ‘school fees’

involved in a poorly designed and implemented auction programme. There is thus an important need to learn from and

distil current experiences with renewable energy auction programmes for the African context. Fortunately there is a lot of

international experience, with more than 67 countries worldwide having embarked on, or developing, renewable energy

auctions – up from five countries in 2005 (REN 21, 2017).

Source: Graduate School of Business, University of Cape Town

Africa

WWW.AFRICA-ENERGY-FORUM.COM | WWW.GSB.UCT.AC.ZA | WWW.IFC.ORG

REFLECTIONS ON THE LAST 20 YEARS: HOW FAR HAVE WE COME?

Countries in sub-Saharan Africa using renewable energy auctions

(Figure 4)

Source: Graduate School of Business, University of Cape Town

The rising prominence of auctions is primarily due to the introduction of competition into the procurement process, causing

significant downward pressure on renewable energy project prices. The lowest renewable energy prices globally are currently

being announced in auctions in developing countries (Dobrotkova et al., 2018). The result is that the least-cost new-build

electricity generation capacity options in many developing countries are now renewable energy based (McCrone et al.,

2017; CSIR, 2016; Dezem, 2016).

Analysis of renewable energy auction programmes in Latin America, the Middle East and North Africa, Europe,

and Asia has revealed seven major trends with important implications for sub-Saharan Africa:

1. Renewable energy auctions work in many different market contexts with various renewable energy technologies

2. A coherent, clear integration of energy policy, electricity sector master planning, and procurement is essential for

achieving successful auction outcomes

3. Auction participants need to not only have the capacity (financial, technical, etc.) to stand behind their bids, but more

importantly should be committed to realising auction outcomes.

4. Most renewable energy auctions tend to favour simpler, more intuitive design options

5. Deciding beforehand on clear auction objectives is important, since there tends to be a trade-off between different

objectives

6. Project de-risking and credit enhancement have proven to be important for achieving lower prices, and for ensuring

project realisation

7. Effective renewable energy auction implementation requires substantial institutional capacity and commitment at various

levels of government.

Source: Graduate School of Business, University of Cape Town

Africa

WWW.AFRICA-ENERGY-FORUM.COM | WWW.GSB.UCT.AC.ZA | WWW.IFC.ORG

REFLECTIONS ON THE LAST 20 YEARS: HOW FAR HAVE WE COME?

What does the next 20 years hold?

While the current macroeconomic environment is turbulent for many developing countries, in the long term, Africa will

continue to grow. It will offer investment returns that are attractive to foreign investors compared to alternatives elsewhere.

In the power sector this should be obvious – everybody is hungry for power, it has a multiplier effect on economic growth,

and there have to be ways to structure the sector to allow profitable investment. Yet governments are still struggling to get

people to the table. What needs to change?

One of the stumbling blocks for deals to close is the process of procurement, and the integrity concerns that often surround

it. For an increasing number of deals and countries, competitive and transparent procurement, a la REIPP, GET FiT and

Scaling Solar, is the way to go. In the future, organizing bidding processes for solar deals should be de rigeur.

And given the prices that these products are delivering, as well as the availability of subsidies for and increased focus on

renewables, solar, wind and storage are clearly the energy products of the future. Unit prices of storage, in particular, are

falling rapidly and the fall is accelerating – some estimates put the current unit rate of decrease at 20% a year. Has Africa

financed its last peaking plant? Possibly not – but countries are certainly having to come to terms with designing and running

a power system that is increasingly based on low-cost, variable renewable power

A striking verdict on the last twenty years, however, is that the absolute number of Africans without power has not diminished

– it’s still close to 600 million – despite all the developers, bankers and investors who turn out to AEF every year. We obviously

need to do better – but the technological revolution involving household solar and storage, and smart metering and billing

could do the same for the power sector that the mobile phone did for telecommunications.

Meanwhile, organisations, and Government clients, need to be more inventive about bringing the private sector into other

parts of the business, including distribution and transmission. Private transmission is commonplace in Latin America, for

example, and there is no reason why it cannot be a feature of African economies. Even across borders; if a railway line can

be built across Malawi to Nacala in Mozambique, there is no reason for a transmission line to be publicly-funded.

IPPs make an important and growing contribution to meeting Sub-Saharan Africa’s power needs, and are the most obvious

place for private power sector investment. Projects are concentrated in a few countries, but there is scope to widen private

investment across the continent. Current experience with IPPs on the continent offers important lessons around the

enabling environment to accelerate private investment. Key is having a dynamic, least-cost power plan that is translated

into a (competitive) procurement programme in a timely manner. Using competitive bidding or auctions further ensures

that this investment is affordable (i.e. that prices are low), and that the procurement process is transparent and predictable.

But the acceleration in private power has not constituted an explosion; and it still falls way short of what is needed. And

some of the challenges of the past persist today. Most Africa utilities still lose money on every kWh of power they sell.

The major stumbling block to the real take-off of private investment hasn’t changed in 20 years; basic sector bankability.

IFC, in partnership with the World Bank, other DFIs and donors, will continue to engage with Government clients to move

sectors towards bankability – in some cases, restoring a situation that has recently deteriorated. Twenty years ago, many

organisations participated in Parliamentary discussions for fast-track power reform in Nigeria; it took most of the intervening

time and much effort on all sides to get to Azura. And there is a still a long road ahead. Engagement and dialogue upstream

of deal structuring will continue to be a feature of power sectors for many years to come.

Source: International Finance Corporation (IFC) World Bank Group

Africa

WWW.AFRICA-ENERGY-FORUM.COM | WWW.GSB.UCT.AC.ZA | WWW.IFC.ORG

REFLECTIONS ON THE LAST 20 YEARS: HOW FAR HAVE WE COME?

Authors

David Donaldson

Head, InfraVentures, Africa

IFC

Mr. Donaldson has worked for over twenty five years in the fields of economic development and

privatization, and has worked in over forty countries worldwide, focusing mainly on Africa. He

has been with IFC for fifteen years, beginning as an economist in the Africa department, and most

recently as a senior manager for IFC’s Advisory Services, based in Johannesburg. He has worked,

as team member and team leader, on many private-public partnerships in the infrastructure sector.

Prof. Anton Eberhard

Professor HOD Managing Infrastructure Reform & Regulation

University of Cape Town

Prof. Anton Eberhard is Emeritus Professor and Senior Scholar at the University of Cape Town’s

Graduate School of Business, where he directs the Management Programme in Infrastructure Reform

and Regulation. His research and teaching focuses on power sector investment challenges, governance,

and regulatory incentives to improve utility performance, and the political economy of power sector

reform, in sub-Saharan Africa. He has worked in the energy sector across sub-Saharan Africa (and

other developing regions) for more than 35 years.

Wikus Kruger

Researcher

University of Cape Town

Wikus Kruger is a Research Fellow with the University of Cape Town’s Graduate School of Business.

His research and teaching focuses on investment challenges in the African power sector, primarily

in the context of Renewable Energy Auctions. Wikus has more than 10 years’ experience working in

the African energy sector as a researcher, consultant, and business developer.

Olakunle Alao

Research Consultant

University of Cape Town

Olakunle is a research consultant within the (MIR) unit responsible for tracking investments in the African

power sector. Olakunle is completing his master’s degree in electrical engineering at the university

of Cape Town, and holds a B.Eng (first class honours) in electrical and electronics engineering from

Covenant university in Nigeria. Olakunle also worked as an analyst (market competition and rates) with

the Nigerian Electricity Regulatory Commission (NERC) before embarking on his post-graduate studies.

Editor:

Fiona Gleeson

Senior Marketing Executive

EnergyNet

Fiona Gleeson is a Senior Marketing Executive at EnergyNet Ltd. EnergyNet organises a global

portfolio of energy forums, investment meetings, and collaborative dialogues focused specifically on

the power generation and industrial sectors across Africa and Latin America.

Africa

WWW.AFRICA-ENERGY-FORUM.COM | WWW.GSB.UCT.AC.ZA | WWW.IFC.ORGREFLECTIONS ON THE LAST 20 YEARS: HOW FAR HAVE WE COME? References and further reading African Development Bank Group (2017) ‘Annual development effectiveness review 2017’, Abidjan. CSIR (2016) Cost of new power generators in South Africa Comparative analysis based on recent IPP announcements by Dr Tobias Bischof-Niemz, Head of CSIR’s Energy Centre, Ruan Fourie, Energy Economist 1–9. Dezem, V. (2016) ‘Solar sold in Chile at lowest ever, half price of coal’, Bloomberg 1–3. Dobrotkova, Z., Surana, K., and Audinet, P. (2018) ‘The price of solar energy : Comparing competitive auctions for utility- scale solar PV in developing countries’, Energy Policy 118, pp. 133–148. doi:10.1016/j.enpol.2018.03.036 Eberhard, A., Gratwick, K., Morella, E., and Antmann, P. (2016) ‘Independent power projects in sub-Saharan Africa: Lessons from five key countries, directions in development - energy and mining’, The World Bank Group, Washington DC. doi:doi:10.1596/978-1-4648-0800-5 IEA (2014) ‘Africa energy outlook: A focus on prospects in Sub-Saharan Africa’, 1–242, Paris. Kruger, W. and Eberhard, A. (2018) ‘Renewable energy auctions in sub-Saharan Africa: Comparing the South African, Ugandan, and Zambian Programs’, Wiley Interdiscip. Rev. Energy Environ. 1–13. doi:10.1002/wene.295 McCrone, A., Moslener, U., D’Estais, F., and Grünig, C. (2017) ‘Global trends in renewable energy investment 2017’, Frankfurt School UNEP Collaborating Centre for Climate and Sustainable Energy Finance, Frankfurt. REN 21 (2017) ‘Renewables 2017: Global status report’, REN21 Secretariat, Paris. doi:10.1016/j.rser.2016.09.082 International Energy Agency. World Energy Outlook 2015 - Executive Summary - English Version. (2015). Findt, K., Scott, D. B. & Lindfeld, C. Sub-Saharan Africa Power Outlook 2014. (2014). Eberhard, A., Rosnes, O., Shkaratan, M. & Vennemo, H. Africa’s Power Infrastructure: Investment, Integration, Efficiency. (World Bank, 2011). Castellano, A., Kendall, A., Nikomarov, M. & Swemmer, T. Brighter Africa. McKinsey & Company Monthly Journal (2015). U.S. Energy Information Administration. International Energy Statistics. (2018). at

UPCOMING ENERGYNET MEETINGS IN 2018/2019 INCLUDE:

ENERGYNET LATIN AMERICA Latin America

& Caribbean

LATIN AMERICA & CARIBBEAN GAS LATIN AMERICA ENERGY FORUM 2019

CONFERENCE & EXHIBITION March 2019 | Washington DC

8-10 October 2018 | Mexico City The Latin America Energy Forum will bring some of the most

LATIN AMERICA &

CARIBBEAN GAS LGC exciting Latin American economies to a high level investors

CONFERENCE & EXHIBITION

8-10 OCTOBER 2018

MEXICO CITY The Latin America & Caribbean Gas Conference & Exhibition

Latin America

& Caribbean

hosted by EnergyNet and IGU in official partnership with gathering addressing trends and opportunities for power

Arpel reunites the leading gas investors with presence development in the national and regional power markets.

in the LAC region to provide the current private sector www.latam-growingecononomies.com

8 – 10 OCTOBER perspectives on the needs and opportunities across the MARCH

MEXICO LAC gas markets. USA

www.lgc-expo.com

ENERGYNET AFRICA Africa

REGIONAL ENERGY COOPERATION INTERNATIONAL GAS

SUMMIT: WEST COOPERATION SUMMIT

26-28 September 2018 | Accra 10-12 December 2018 | Cape Town

The 3rd Regional Energy Cooperation Summit: West will The 2nd International gas cooperation Summit will put the

take place in Accra, Ghana, in September 2018, exploring objectives of South Africa and the region at the forefront

the country’s vast potential for energy generation of international gas development. IGCS will showcase gas

& discussing opportunities for cross-border project procurement and utilisation strategies, enabling Southern

26-28 SEPTEMBER collaboration in West Africa. 10-12 DECEMBER Africa to achieve its objectives in becoming an energy hub

GHANA SOUTH AFRICA for the region.

www.recs-west.com

www.igcs-sa.com

REGIONAL ENERGY COOPERATION SOUTHERN AFRICA RENEWABLE

SUMMIT: EAST ENERGY SUMMIT

10-12 October 2018 | Kampala 10-12 December 2018 | Cape Town

The 3rd Regional Energy Cooperation Summit: East will The Southern Africa Renewable Energy Summit will focus on

return to Kampala in October 2018 to continue discussions this region’s huge potential for the generation of renewable

around how the region can accelerate the development of energy, outlining objectives for the next decade, uniting

IPPs and promote cross-border energy partnerships. governments, international organizations and private

10-12 OCTOBER 10-12 DECEMBER investors in the aim of securing a sustainable energy future.

UGANDA

www.recs-east.com SOUTH AFRICA

www.igcs-sa.com

AEF: OFF THE GRID BLACK INDUSTRIALISTS

10-12 October 2018 | Kampala ENERGY SUMMIT

The 3rd Africa Energy Forum: Off the Grid meeting will 10-12 December 2018 | Cape Town

return to Kampala in October 2018 to continue the BLACK INDUSTRIALISTS As Africa’s populations continue to grow, programmes such

momentum around off grid solutions for Africa’s power ENERGY SUMMIT

as the Black Industrialists Programme have the potential to

sector. Meet with key players in the off grid space and head off major economic challenges across the continent.

discover the next opportunities. This session will debate what foundations are required

10-12 OCTOBER www.aef-offgrid.com 10-12 DECEMBER by black-owned local companies in order to encourage

UGANDA SOUTH AFRICA investment and facilitate international partnerships.

www.igcs-sa.com

GAS OPTIONS – POWERING AFRICA: SUMMIT

NORTH & WEST AFRICA 2019 | Washington DC

November 2018 | Marrakech Held in Washington DC each year, the 5th annual Powering

Africa: Summit is a global platform to showcase power,

The 5th Annual

After a successful launch in Casablanca in November 2017,

the Gas Options: North & West Africa meeting will return to trade and infrastructure investment opportunities across

Morocco later this year to provide an update on the huge Africa, engaging investors from North America and around

potential of the gas market in Africa. to world to form partnerships and move projects forward.

NOVEMBER

www.gasoptions-nwafrica.com 2019 www.poweringafrica-summit.com

MOROCCO USA

AFRICA RENEWABLE ENERGY FORUM AFRICA ENERGY FORUM 2019

November 2018 | Marrakech 11-14 June 2019 | Lisbon

Now in its 3rd year, the Africa Renewable Energy Forum 21ST ANNUAL

The largest and longest-running meeting in the industry,

will address outcomes of the previous meeting in 2018, the Africa Energy Forum will return to Europe in 2019 to be

to collectively address the potential of renewable energy hosted in the vibrant city of Portugal. Expect 4 packed days

projects in Africa. 11-14 JUNE 2019

of panel discussions, side events and networking functions

LISBON at the industry meeting of the year.

www.africa-renewable-energy-forum.com

NOVEMBER 2019 www.africa-energy-forum.com

MOROCCO PORTUGAL

For information on sponsoring, speaking and attending EnergyNet meetings, please contact Amy Offord on +44 (0)20 7384 8068 or email marketing@energynet.co.uk

WWW.ENERGYNET.CO.UKYou can also read