RIAA NZ Member Forum The future of fossil fuels in default KiwiSaver and other responsible investments How much, how far and by when? ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

RIAA NZ Member Forum The future of fossil fuels in default KiwiSaver and other responsible investments How much, how far and by when?

Speakers Matt Mimms, The Investment Store Nicolette Boele, RIAA Rebekah Swan, AMP Capital Paul Brownsey, Pathfinder David Beattie, Booster

Introduction – Matt Mimms, RIAA NZ Board Member

1. Acknowledgement of Country

2. Upcoming RIAA events

• Impact Investment webinar – 23rd June

• RI Benchmark Report 2020 New Zealand; launch 1 September

• RI New Zealand conference now on March 5th 2021, Auckland

• Half-day virtual conference in September at date of conference – September 15

• 2 further webinars in July and August (dates TBD)

3. RI Recovery Charter – opportunity to sign on

4. How to ask questions during webinar and access recording afterwards

Aims of this webinar

1. Build a common understanding of the issues surrounding screening for fossil fuels

2. Kick-off a process for inviting input into how we may shape the fossil fuel

requirement of default KiwiSavers (RIAA will advocate the range of member views

with the relevant regulators e.g. MBIE, FMA)

3. Start exploring member views

Overview

1. Introduction

2. Background briefer

3. Manager perspectives on screening for fossil fuels – expert panel…

• Rebekah Swan, AMP Capital

• Paul Brownsey, Pathfinder

• David Beattie, Booster

4. Facilitated discussion about default KiwiSaver and excluding fossil fuel producers

5. Participant questions answered

6. Next steps in this engagement

Briefer – Nicolette Boele

1. Consumer expectations around fossil fuel exposures in their investments

2. Government responses to climate change – global and local

3. Investor behaviours – from risk to strategic asset allocation

4. The range of fossil fuel screens applied by issuers with Certified Responsible

Investment products

5. The differences in results provided by ESG research providers

6. Net-zero: what’s enough by when and in which parts of the fossil fuel value-chain?

This is the first in a series of steps to engage RIAA members to help shape up coming

changes.

RIAA’s response March 2020 “The announcement recognises the critical role finance has to play to protect retirement savings from the risks of climate change, at a time when regulators globally are increasingly warning of the financial risks posed by unmitigated climate change, when ever more investors are lessening their exposure to fossil fuels and when consumers are increasingly stating their own savings should not be supporting environmentally harmful businesses."

Rolled into the outcomes of seven-year KiwiSaver review: • Making fees are simple and transparent; using procurement process to put pressure on fees • Engage with members to help them make informed decisions about their retirement savings • Moving default from conservative to balanced • Maintain a responsible investment policy that’s published on their website • Transferring non-active default members [1] of any provider that is not reappointed to one of the appointed default providers [2] (so that these members retain the benefits of being in a default fund) • Excluding investments in fossil fuels and illegal weapons: • Enshrine as a requirement in default fund settings, what many funds have been doing for several years already • Producers and not distributors such as retailers of petrol

What we know so far Default KiwiSaver Members: • Make up 20% (600,000 of 3m) of all KiwiSavers (MBIE January 2020), increased 2% on previous year (IRD) • Have not made a choice to stay there • Are young (as at March 2019 only 8% are over 60 years of age) The changes will impact the nine registered default providers

1. Consumer expectations around fossil fuel exposures in their investments 83% expect their investments to be invested responsibly and ethically (compared with 72% in 2018) 2 in 3 say they would consider moving their investments to another provider, if their current fund engaged in activities not consistent with their values Responsible Investment: NZ Survey 2019 (Colmar Brunton with RIAA & Mindful Money)

1. Consumer expectations around fossil fuel exposures in their

investments

In March 2020 avoiding

fossil fuels was the single Fossil fuels

most selected exclusion for

users of RIAA’s Responsible

Returns.

Human rights abuses

Animal cruelty

Armaments

Logging etc.1. Consumer expectations around fossil fuel exposures in their investments The top barriers to investing responsibly are: • Not enough time to compare the options • Not enough independent information • A lack of credible options • Don’t believe the claims for responsible or ethical investment Responsible Investment: NZ Survey 2019 (Colmar Brunton with RIAA & Mindful Money)

2. Government responses to climate change 2016 October: NZ Parliament ratified the Paris Agreement: • Commits NZ’s economy to a decarbonisation trajectory consistent with “well-below 2 degrees Celsius rise in temperature no later than 2050” 2018 October: Productivity Commission’s Low Emissions Economy Sustainable Finance Forum (The Aotearoa Circle, MfE), including NZ commitment to the Sustainable Development Goals

2. Government responses to climate change 2019 November: Climate Change Response (Zero Carbon) Amendment Act 2019 (to the Climate Change Response Act 2002 (now Zero Carbon Act 2019) Provides a framework by which New Zealand can develop and implement clear and stable climate change policies that: • Contribute to the global effort under the Paris Agreement to limit the global average temperature increase to 1.5° Celsius above pre-industrial levels • Allow New Zealand to prepare for, and adapt to, the effects of climate change

2. Government responses to climate change 2020 March: Commerce and Consumer Affairs Minister Faafoi, announces default KiwiSavers shall exclude armaments, fossil fuel producers as part of seven-year review; change effective December 2021 Signals the pace of policy shift to decarbonise NZ and protect certain groups of consumers and savers from potentially stranded assets

3. Investor Behaviours – from risk to strategic asset allocation

• 72% of the NZ investment industry already has in place some commitment to responsible

investing

• $88 billion is already screened

• Fossil fuels ranks sixth (6th) place after controversial weapons, tobacco, gambling, adult

content and nuclear power

(Responsible Investment Benchmark Report 2019 New Zealand, RIAA)

• A rise in larger regulated pension funds screening against international norms,

specifically the Paris Agreement (this include NZ Super Fund)

(RI Super Study 2019)3. Investor Behaviours – drivers for market growth in RI (Responsible Investment Benchmark Report 2019 New Zealand, RIAA)

3. Investor Behaviours – RI Certification

• From 2015 to 2019 the number of new RIAA Certified funds, superfund options and

banking products grew from 42 to 175

• 87% of all Certified products provide some screening for fossil fuels (as at April 2020)

• Full exclusion 15%

• Partial 72%

• An increasingly larger number of conversations are happening between Certification

team members and RIAA members about the “appropriate level of screening for fossil

fuels in Certified products3. Investor Behaviours – KiwiSavers and fossil fuel screens

Of the total $65.7 billion invested in KiwiSaver funds:

• Default members’ investments are worth $9 billion (MBIE March 2019)

• $1.6 billion are invested in companies that are engaged in fossil fuel production (Mindful

Money, December 2019)

• Less than 3% of KiwiSaver investments are in funds that screen for fossil fuels

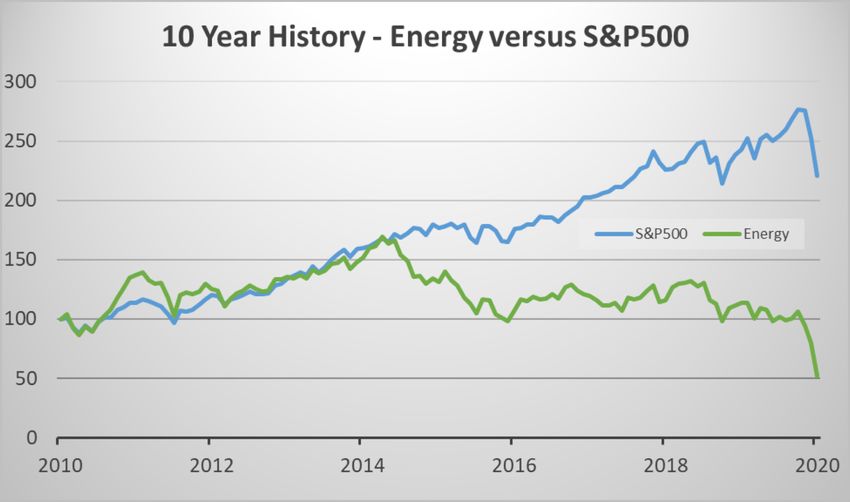

• 6 providers offer 19 KiwiSaver funds that screen for fossil fuels (Mindful Money)3. Investor Behaviours – New Zealand Super October 2016 – Climate change strategy announced August 2017 – Carbon Reduction announced to global passive equity portfolio (constituting 40% of NZ Super); and continue to apply this each year • moving $3 billion (of its 47 billion) out of stocks that exceeded thresholds (reserves) or emission intensity Since then: Applied the strategy to their active equity portfolios and excluded a larger proportion of the Fund via derivatives As well: Approach to managing transition risk is supported by corporate engagement, search for opportunities, and analysis of climate change considerations into investment analysis and decisions (valuation models, risk allocation and member selection)

3. Investor Behaviours – divestment movement

4. Range of screens applied by issuers with Certified RI Products

Companies that hold fossil fuel reserves used for energy purposes

Exploration Reserves

Exposure by ownership

Companies with more than 20% value/revenue from fossil fuel production Value by market cap

Extraction (coal mining) Production (oil, coal to gas)

Revenue for operations

Power production (electricity and gas) based on fossil fuels

Revenue for sales and

distribution

Companies involved in the transportation, distribution and retailing of fossil fuels

Pipelines & freight Retail, service stations, energy utilities

Activity exposure through

sales of goods and services

Companies with 5% revenue exposure to provision of goods and services fossil fuel sector Exposure through

Engineering services Financing finance5. The differences in results provided by ESG research providers • Classification systems • Exposure methodology • Reach along supply chain Just some RIAA members offering tools for screening company exposures:

6. Net-zero: What’s enough, by when and in which parts of the fossil fuel value-chain? Halve emissions by 2030 based on 1990 baseline Net-zero no later than 2050 Easiest and safest for economy/ business = reducing emissions from source • Agriculture • Energy • Transport • Land use, land use change and forestry

Quick note: Fossil fuel screen boundaries

Exploration Oil, gas, coal,

& extraction uranium

Mining,

Energy coal2gas, Production

production refining

Pipelines, Ownership

Distribution petrol &

stations Subsidiary

Finance,

engineering Services

servicesQuick note: Fossil fuel screen boundaries – tricky bits

Chemical

GAS

transport

OIL Polymers

Steel

production

COALKiwiSaver issuer perspectives David Beattie, Booster Paul Brownsey, Pathfinder Rebekah Swan, AMP Capital

Rebekah Swan, AMP Capital

Our Fossil Fuel approach for the Ethical Leaders range Rebekah Swan ESG Investment Specialist, NZ / Client Advocate, Head of Product 2020

Ethical Leaders’ exclusions and integration of ESG

1.

WE AVOID COMPANIES

2.

WE INVEST IN COMPANIES THAT

& ASSETS THAT POSITIVELY CONTRIBUTE TO

NEGATIVELY IMPACT SOCIETY AND ENGAGE ON ESG

OUR WORLD ISSUES THAT ARE IMPORTANT

TO MEMBERS

Nuclear power Armaments Gambling Treatment of Workers / Gender

Tobacco (including uranium) Human Rights Animal Welfare

Child Labour diversity

Alcohol Pornography Fossil Fuels Live animal

(Thermal Coal & Brown exports Responsible

Coal Power Generation)

Environment Governance Pollution Executive Pay Banking

Source: AMP Capital, as at 30 September 2019. Note: We also limit investments into companies that use large amounts of carbon-intensive fossil fuels 2Ethical Leaders’ fossil fuel policy

Rationale Resulting exclusions

> Some fossil fuels will be needed in the transition to a low carbon

economy

> Some do not yet have a renewable alternative e.g. metallurgical coal for Exclude any companies involved in the most

making steel carbon intensive fossil fuels. We apply a 10%

exposure threshold (as measured by % market

> Very active engagement agenda - use our seat at the table to lobby for

capitalisation to one, or combination of the

a transition to renewables and clear disclosure of the path forward

following:

1. Mining thermal coal

2. Exploration and development of oil sands

REFLECTS MEMBERS’ GROWING

INTEREST/ CONCERN IN FOSSIL FUEL 3. Brown coal (or lignite) coal-fired power

INVESTMENT generation

4. Transportation of oil from oil sands

SUPPLEMENTS STRONG 5. Conversion of coal to liquid fuels/feedstock

ENGAGEMENT FOCUS

3Fossil Fuels

Principal: Avoid the most emission intensive

1. Avoid the most emission intensive fossil-fuels for which there is no alternative

Fossil Fuel Emissions (kg CO2-e/GJ)

Coal 88 - 93 Exclude Coal

Oil 60 - 68

Natural gas 51

2. Avoid the most emission intensive oil

• Key issue is the emissions from the extraction of oil, even though 70-80% of total emissions are associated with burning the oil

• Canadian oil sands typically have 70-100% higher emissions in the extraction phase compared to other crude oils

• Also consistent with the concerns over other environmental and social impacts of oil sands

Exclude Oil Sands

|4Fossil Fuels

Principal: Avoid the most emission intensive

Exclude Coal to Liquid and coal to gas processes

3. Avoid emission intensive processing

4. Avoid the most emission intensive downstream use of fossil fuels

Fuel Average emissions intensity of electricity

generation

Emissions intensity (t CO2/MWh)

Exclude brown coal generation

Brown Coal 1.20

Oil 0.97

Black Coal 0.92

Gas 0.54

Renewables 0.00

Aust. coal average 1.00

Aust. Fossil fuel 0.92

average

5. Avoid infrastructure that facilitates the most emission intensive fossil fuels

Avoid oil sands pipelines

|5Fossil Fuels

Principal: Consider alternatives

1. Making steel

• Need a reductant (ie carbon source) to produce steel from iron ore

• No alternative to metallurgical coal

Don’t exclude metallurgical coal

2. Making electricity

• Numerous lower emission and affordable ways to produce, eg gas and renewables

|6Important Note

Neither AMP Capital Investors (New Zealand) Limited, nor any other company in the AMP Group guarantees the repayment

of capital or the performance of any product or any particular rate of return referred to in this presentation. Past

performance is not a reliable indicator of future performance. While every care has been taken in the preparation of this

document, AMP Capital makes no representation or warranty as to the accuracy or completeness of any statement in it

including, without limitation, any forecasts. This document has been prepared for the purpose of providing general

information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should,

before making any investment decisions, consider the appropriateness of the information in this document, and seek

professional advice, having regard to the investor’s objectives, financial situation and needs. This document is solely for

the use of the party to whom it is provided.

|7David Beattie, Booster

Responsible Investing Journey • Cornered the SRI exclusion market by accident • Fossil fuel exclusions a clear preference 5 years ago • Global shortage of suitable product options • Broader the definition, the more the subjectivity • Fully direct the only way to be in total control of SRI • ESG integration ey to future performance www.booster.co.nz

Responsible Investing Journey • Cornered the SRI exclusion market by accident • Fossil fuel exclusions a clear preference 5 years ago • Global shortage of suitable product options • Broader the definition, the more the subjectivity • Fully direct the only way to be in total control of SRI • ESG integration ey to future performance www.booster.co.nz

Responsible Investing Journey • Cornered the SRI exclusion market by accident • Fossil fuel exclusions a clear preference 5 years ago • Global shortage of suitable product options • Broader the definition, the more the subjectivity • Fully direct the only way to be in total control of SRI • ESG integration ey to future performance www.booster.co.nz

Responsible Investing Journey • Cornered the SRI exclusion market by accident • Fossil fuel exclusions a clear preference 5 years ago • Global shortage of suitable product options • Broader the definition, the more the subjectivity • Fully direct the only way to be in total control of SRI • ESG integration key to future performance www.booster.co.nz

Responsible Investing Journey • Cornered the SRI exclusion market by accident • Fossil fuel exclusions a clear preference 5 years ago • Global shortage of suitable product options • Broader the definition, the more the subjectivity • Fully direct the only way to be in total control of SRI • ESG integration ey to future performance www.booster.co.nz

Responsible Investing Journey • Cornered the SRI exclusion market by accident • Fossil fuel exclusions a clear preference 5 years ago • Global shortage of suitable product options • Broader the definition, the more the subjectivity • Fully direct the only way to be in total control of SRI • ESG integration ey to future performance www.booster.co.nz

Responsible Investing Journey • Cornered the SRI exclusion market by accident • Fossil fuel exclusions a clear preference 5 years ago • Global shortage of suitable product options • Broader the definition, the more the subjectivity • Fully direct the only way to be in total control of SRI • ESG integration key to future performance www.booster.co.nz

Paul Brownsey, Pathfinder

Slide 1

Slide 2

Slide 3

Slide 4

Slide 5

Slide 6

Slide 7

Facilitated discussion

Matt Mimms, The Investment Store and RIAA BoardQuestions

Next steps in engagement

• The key objective: Kick-off a process for inviting input and start exploring

member views of the default KiwiSaver-fossil fuel initiative

• Over the coming months, RIAA advocate with the relevant regulators (e.g.

MBIE, FMA) the range of views members have provided

• This webinar is a first step in that member engagement processUpcoming RIAA events

Impact Investment webinar – 23rd June

RI Benchmark Report 2020 New Zealand: launch 1st September

RI New Zealand conference now on 5th March 2021, Auckland

• Half-day virtual conference in September at date of conference – 15th September

• 2 further webinars in July and August (dates TBD)

RI Recovery Charter – opportunity to sign onThank you www responsibleinvestment.org Twitter @RIAANews

You can also read