Scenari macroeconomici e finanziari 2020 - Giorgio di Giorgio | Vice Rettore, Università LUISS Roma - Deloitte

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Scenari macroeconomici e finanziari 2020 Giorgio di Giorgio | Vice Rettore, Università LUISS Roma

Agenda

1 – Il quadro congiunturale. Rallentamento verso recessione.

2 – Liquidita’ e rischi finanziari

3 – Le difficolta’ in Europa

4 – L’Italia e i nostri problemi strutturali: una agenda ”vecchia”, sempre attuale

2

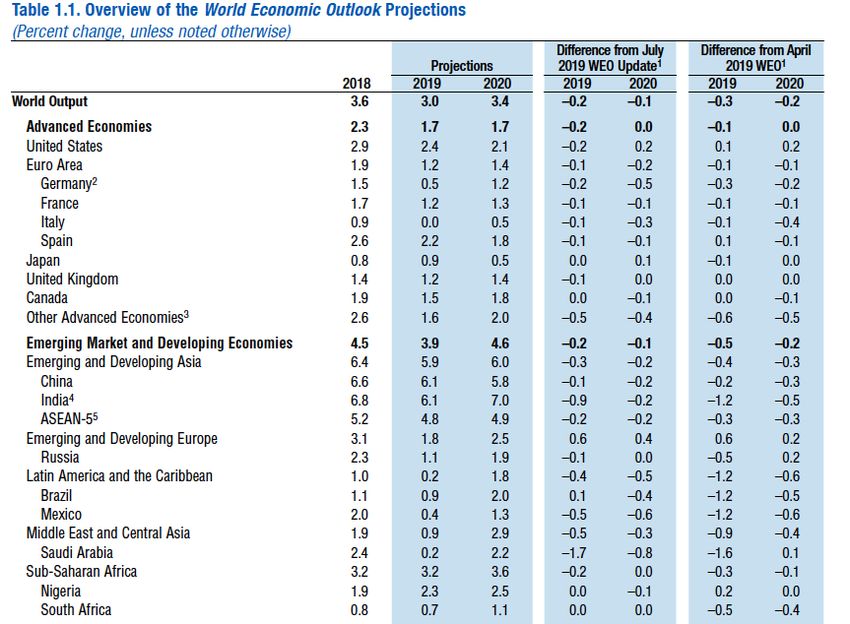

Forecasts revised downward mostly everywhere

3

The medium term macro environment

Growth acceleration of emerging countries (with respect to developed ones) begins in the years 2000. In

the same period inflation rates converge (in part).

Real GDP growth

'80s '90s '00-'07 '08-'18 '19 estim '20 estim

World Economy 3.2 3.1 4.5 3.4 3.5 3.6

Developed countries 3.1 2.8 2.7 1.4 2.0 1.7

Emerging countries 3.2 3.6 6.6 5.0 4.5 4.9

Consumer inflation

'80s '90s '00-'07 '08-'18 '19 estim '20 estim

World Economy 15.8 20.2 4.2 3.7 3.8 3.6

Developed countries 6.5 2.9 2.1 1.6 1.7 2.0

Emerging countries 36.6 55.4 6.8 5.6 5.1 4.6

10

Real GDP grow th (source IMF) Consumer inf lation (source IMF)

8 115

emerging countries

6 95

4 75

2 55

developed countries

0 emerging countries 35

developed countries

-2 15

-4 -5

80 85 90 95 00 05 10 15 20 25 80 85 90 95 00 05 10 15 20 25

Source: IMF

4Who drives global growth

Emerging countries produce almost 60% of global GDP (in 2000 their share was 43%) and represent some

70% of global annual growth.

% 65

Distribution of World GDP

(GDP measured at PPP, source IMF)

60

57%

59%

55

developed countries

50

emerging countries 45

41%

43% 40

35

90 92 94 96 98 00 02 04 06 08 10 12 14 16 18 20

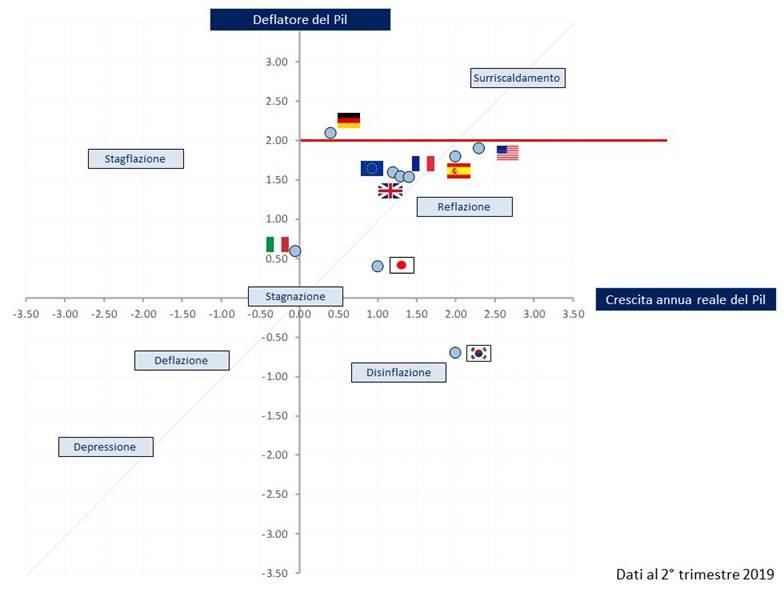

5L’orologio del ciclo nei maggiori paesi (dati terzo trimestre 2019)

628 novembre 2019|Prof. Giorgio Di Giorgio

Risks evident in the world trade fall….

728 novembre 2019|Prof. Giorgio Di Giorgio

….in a reduction of dinamism in China

8Monetary policy challenges

In a world of no inflation to be fought, central banks are again in an expansionary mood

The Fed stopped its normalization path by reducing rates and stopping the downward

adjustment of its balance sheet

The ECB is re activating the bazooka

A fiscal role for monetary policy?

What else in the Eurozone?

9Liquidity and the risks of a new financial crisis

Abundant liquidity keeps being the model

Negative interest rates even for long maturities in gov bonds

Very Low risk adjusted returns in private debt

High indebtness of firms and governments (less worrying for

households)

Asset inflation: high valuations in equity and bond markets

fragility and risks!!!

However: Banks much more capitalized, leverage of brokerage

firms much lower than in 2007, profit conditions of firms still pretty

sound

10German industrial production slowing down, despite many

favourable conditions

135

130

125

120

115

110

Indice 2002=100

105

100

95

90

85

80

75

'02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18

Italia Francia Spagna Germania 100

1128 novembre 2019|Prof. Giorgio Di Giorgio

….and in further damage provoked by a hard Brexit or no deal

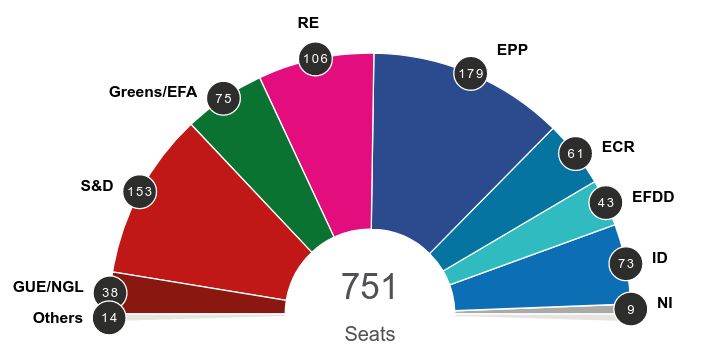

12EU Parliament more fragmented than ever: a large coalition needed

1328 novembre 2019|Prof. Giorgio Di Giorgio

Focus Italy: Italy is the weak link in the Eurozone

GDP Pro-capite 1992-2018: Italy, UK vs major countries

(100 = 31/12/1992)

250

225

200

175

150

125

100

75

92 94 96 98 00 02 04 06 08 10 12 14 16 18

USA United Kingdom Italy Germany France 100

Source: GaveKal, Bloomberg, Profilo Investment Advisory | 14 |28 novembre 2019|Prof. Giorgio Di Giorgio

Long period GDP per capita dynamics

Italy Euro Area USA France Germany UK Spain Japan

1951-60 5,4 4,3 1,8 3,7 7,1 2,3 3,5 7,6

1961-70 4,9 3,7 3,0 4,4 3,5 2,2 6,3 8,9

1971-80 3,1 2,4 2,2 2,7 2,7 1,8 2,4 3,3

1981-90 2,2 1,8 2,4 2,0 2,0 2,8 2,6 4,0

1991-00 1,6 1,5 2,2 1,7 1,6 2,2 2,5 1,0

2001-10 -0,1 0,5 0,8 0,6 1,1 1,0 0,8 0,6

2011-18 -0,1 0,7 1,5 0,8 1,5 1,2 1,1 1,2

1528 novembre 2019|Prof. Giorgio Di Giorgio

Italy: Our Structural Problems

Low productivity

Low competitivity

Fiscal fragility: High public debt-gdp ratio nothwistanding sound fiscal flows

Banking fragility: unprofitable banks, consolidation needed

Inefficient labor and goods markets

High unemployment and low participation in the South, among women and the young

Excessive weight of SMEs, and of micro-firms among the latter

Excessive burocracy, inefficient and costly PA

Service sectors highly regulated and protected

Inadequate infrastructures (material and immaterial)

High costs of politics and too many (and inefficiently coordinated) decision levels

Lack of Assesment-Evaluation-Intervention procedures in public spending

Too many laws, rare enforcement

Slow and inefficient Justice

High taxes on families and firms

Costly and inefficient local public services

Quite Low Social expenditure (excluding pensions) 1628 novembre 2019|Prof. Giorgio Di Giorgio

Long history of (shy) attempts for structural reforms

Change is necessary

All governments have failed, for different reasons

From macro to micro policies, based on right Incentives to agents behavior

Comprehensive fiscal reform needed

Recomposition of public expenditure needed (more infrastructure and human capital,

less subsidies, reduced purchases for the PA, proper dealing with health, ageing and

migration)

Environmental interventions needed (Justice, burocracy..)

Redistribution policies?

Return to dynamism is the true challenge

17You can also read