Seafood Sector Presentation - April 2016 - Fish Pool

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Seafood Sector Presentation – April 2016

12.07.201

1

Seafood sector report – April 2016

Extended super-cycle

2

Extension of the salmon cycle, this cycle looks set to last an unprecedented 8 years…

3 year cycles replaced by a 8 year cycle?

3Structural trends favour seafood…..and poultry

4Structural trends favour seafood…..and poultry

5Structural trends favour seafood…..and poultry

Aquaculture and poultry estimated to contribute 2/3 of volume growth

between 2014-2024

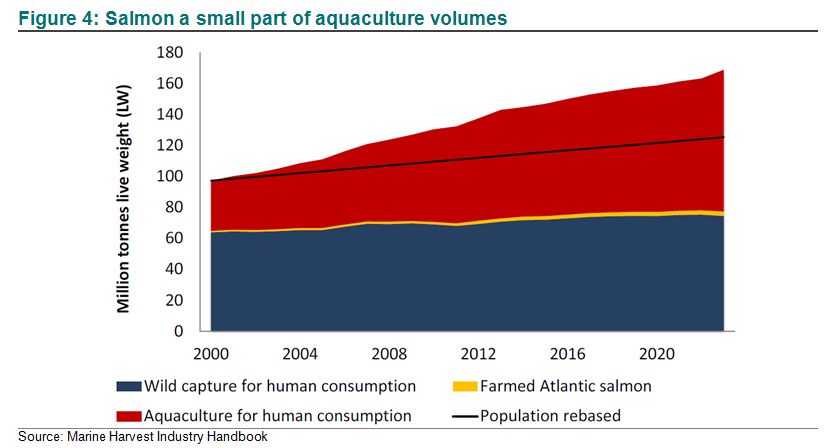

6But salmon unlikely to spearhead growth… At least over the next two years…

Salmon only

account for 4% of

aquaculture

volume

7Top 5 nations salmon producers have hardly grown since 2012

8Top 5 nations salmon producers have hardly grown since 2012

If top 5 regions do not grow, the industry do not grow….

9Supply decline from Chile and Norway trigger the largest negative supply shock in history

6% supply contraction and -140kt dwarfs 2010’s 3.7% and -54kt drop following

the ISA crisis in Chile

10Chile - Algae bloom, or ‘the red tide’ is toxic for many marine animals

11Chile volumes collapsing, lost 120kt or 15% of individuals due to algae…

15% of individuals lost, equivalent to 120kt of lost output in 2016-17e

12Current losses amount to 120kt, but could more than double if region XI is affected

Region X loss of 118kt, but another 179kt if region XI is hit equally hard...

13Chile - Smolt release was dropping sharply even before the algae bloom

Looking at the past three months, smolt releases for atlantics and other species

have taken a nose dive, down 16–28% and 15–39%, respectively

14Chile, what’s next???

Who has the cash to put more fish into the sea?

If they have cash, do they even want to put more fish into the sea?

Record high prices, but no new framework to safeguard against

another collapse… What to do….?

The old proverb: One bird in your hand is better than 10 on the roof…

15Norway - Decline in 2016 is the price to pay for eating into the inventory

Record small harvest size means fewer individuals reach full size, cutting output potential

16Did we ‘overharvest’ 25million individuals? No wonder 2016 supply is tight!

A simple first in, first out model suggest 9% volume decline from Norway in 2016…

17But biomass growth of 15G has been very solid, making up some lost ground

Norwegian biomass growth (%) Total growth in the sea (% of biomass in the beginning of the month)

13%

26%

8% 21%

4% 4% 16%

3% 4% 3%

3%

1%

0% 11%

-1%

-2% -2% -2%

-2%

-3% -3%

-4% 6%

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

-7%

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Max - min 09-14 2013 2014 2015 2016

2013 2014 2015 2016

18Global supply growth estimate

Norway and Chile simultaneous drop cause largest drop in history

19Seafood weekly 22 April 2016

Salmon spot prices at record high levels in both EUR and NOK terms.

EUR/kg

7.5

Salmon price expectations

6.5 DNB 2016e salmon price estimate at

NOK50/kg, and NOK51/kg for 2017e.

5.5 (EUR5.4/kg in 16e and EUR5.5/kg in 17e,

with a EURNOK of 9.3)

4.5

NQSALMON prices are approximately

NOK0.75/kg higher than FHL/NOS prices

3.5

as the NQSALMON prices also include

trader sales margins

2.5

1.5

1 5 9 13 17 21 25 29 33 37 41 45 49

High/Low 00-14 2016 Average 00-14 2015 2014

NOK/kg

65

55

45

35

25

15

Source: DNB Markets, NSL/NOS, Fishpool

1 5 9 13 17 21 25 29 33 37 41 45 49

Analysts: Alexander Aukner (+47 24 16 90 79; alexander.aukner@dnb.no )

High Low 00-14 2016 Average 00-14 2015 2014Seafood weekly 22 April 2016

Chilean and Canadian salmon prices in all time high territory

Chilean salmon (fresh fillets Miami – USD/kg) at USD12.0/kg Seattle price (fresh Atlantic salmon 8-10lbs FOB Seattle)

10.0

14.0

13.0 9.0

12.0 8.0

11.0

7.0

10.0

6.0

9.0

8.0 5.0

7.0 4.0

6.0

3.0

5.0

2.0

4.0 1 5 9 13 17 21 25 29 33 37 41 45 49

1 6 11 16 21 26 31 36 41 46 51

High Low 2015 2014 2016

High-Low 04-14 2015 2014 Average 04-14 2016

Source: Kontali, Urner Barry, DNB Markets Source: Kontali, DNB Markets, Urner Barry

Analysts: Alexander Aukner (+47 24 16 90 79; alexander.aukner@dnb.no )Seafood weekly 22 April 2016

Fishpool forward contracts – Settling down at record high levels.

EUR/kg Last Last Three

EUR/kg Actual week month months

6.8

Q1 2016e 6.19 6.12 5.98 5.35

6.3 Q2 2016e 6.25 6.18 5.98 5.08

5.8 Q3 2016e 5.48 5.43 5.28 4.47

Next 12m 5.87 5.81 5.62 4.89

5.3

2016e 5.92 5.86 5.65 4.88

4.8

2017e 5.51 5.46 5.19 4.57

4.3

Last Last Three

3.8

Oct-15 Nov-15 Dec-15 Jan-16 Feb-16 Mar-16 Apr-16 May-16 Jun-16 Jul-16 Aug-16 Sep-16 Oct-16 Nov-16 Dec-16

NOK/kg Actual week month months

Q1 2016e 58.7 58.1 57.1 50.2

Three months ago One month ago Actual DNB Estimate

Q2 2016e 57.9 58.0 57.0 49.3

Q3 2016e 51.0 51.3 50.5 43.5

NOK/kg

Next 12m 54.9 54.9 53.6 47.0

70

2016e 55.3 55.3 54.0 47.0

65 2017e 51.9 52.0 50.2 45.0

60

55 DNB Estimates:

2016e: EUR5.4/kg, NOK50/kg

50

2017e: EUR5.5/kg, NOK51/kg

45

40

Source: Fishpool, DNB Markets

35 Note: From 2015, Fishpool forward prices include a trading/exporter

Oct-15 Nov-15 Dec-15 Jan-16 Feb-16 Mar-16 Apr-16 May-16 Jun-16 Jul-16 Aug-16 Sep-16 Oct-16 Nov-16 Dec-16 margin of NOK0.75/kg. In order to get the old NOS price delivered Oslo,

NOK0.75/kg must be deducted from the forward price. In order to get

price back to farmer, one must deduct another NOK0.5-1.0/kg for freight

Three months ago One month ago Actual DNB Estimate

cost. Hence a forward price of NOK40/kg corresponds to a price back to

farmer of NOK38.25-38.75/kg

Analysts: Alexander Aukner (+47 24 16 90 79; alexander.aukner@dnb.no )

Source: Fishpool, DNB MarketsSeafood weekly 22 April 2016

How high can the price go…. EUR6/kg and NOK57/kg within reach?

Annual salmon prices (EUR/kg) & global supply growth EUR6/kg? EURNOK rate (2001-2017e)

+EUR1.5/kg

6.0 5.5 25%

5.4

5.0

5.0 4.7 4.7 20%

4.5

3.9 3.9 15%

4.0 3.5 3.5

3.2 3.1 3.2 10%

3.0 2.7 2.7 2.6

2.4

5%

2.0

0%

1.0 -5%

0.0 -10%

FHL NOS(EUR)

Source: FHL/NOS, DNB Markets

CAGR 96-14 Global supply growth (rhs)

Annual salmon prices (NOK/kg) & global supply growth NOK55/kg

55 25%

51

Highest ever EUR/kg change YoY is EUR1.5/kg…

50

50 20%

45

15%

Assuming 2016 will see the same increase, we are

looking at EUR6/kg…which at EURNOK9.2 equals

39 40

39

40 37

10%

35 NOK55/kg

31

30 30 5%

30

25 26 26

25

25 0% Each NOK/kg increase equals ~5% EPS increase

21 22

20 19

20 -5%

15 -10%

NSL/NOS/NQSALMON

Source: FHL/NOS, DNB Markets (NOK) Global supply growth (rhs) CAGR 96-11 (rhs) Source: FHL/NOS, DNB Markets

Analysts: Alexander Aukner (+47 24 16 90 79; alexander.aukner@dnb.no )Historical correlation suggests our estimates are conservative

2016… NOK54/kg

2017…NOK62/kg

Historical correlation suggest NOK54/kg and NOK62/kg, some NOK3/kg and NOK11/kg

above our estimates…

24NOK60/kg… How expensive is it really?

25NOK60/kg… How expensive is it really?

26NOK60/kg… How expensive is it really?

27Retailers still generating good margins

28But growth pains not permanent!

Norway - New technology and green licenses to ensure growth is restored after 2017:

New growth - Green licenses and R&D licenses take effect from late 2017, bringing growth back into positive territory.

Old growth - With the large number and wide variety of sea-lice combating technologies coming on stream, we expect the

challenges with sea-lice to be contained in 2–3 years, allowing growth from regular licenses in Norway to recover.

Chile – Revamp of the regularly system upcoming, with the support of large industry

players should spark a fresh start in Chile as:

Biomass drops;

New vaccines come on stream;

New regulations reduce uncertainty

This could mean Chilean volume growth in 2018-2019?

29Extension of the salmon cycle, this cycle looks set to last an unprecedented 8 years…

3 year cycles replaced by a 8 year cycle?

30Extension of the salmon cycle, this cycle looks set to last an unprecedented 8 years…

Conventional and non-conventional growth resume at the same time?

31Growth is set to gather pace post-2017

32New R&D license applications in Norway mushrooming…

Nr. Applicant Type of concept Output Capex Capex / license

Concept name Licenses MTB (kt) HOG (NOKm) (NOKm)

Nordlaks 'Farming Ship' 1 Nordlaks Oppdrett AS Semi submercibel sea farm 39 30,000 36 2100 54

AkvaFuture (closed concept in the sea)

2 AkvaDesign AS Closed consept 10 7,800 9

Gigante Offshore 3 Gigante Offshore AS "Supertankmerd" - rørkonstruksjon fortøyd på svai 8 6,240 7 500 63

Gifas Marine 4 Gifas Marine AS "SubFishcage" - nedsenkbar stormerd 4 3,120 4 120 30

Atlantis Subsea 5 Atlantis Subsea Farming AS, Sinkaberg Nedsenkbare oppdrettsanlegg 6 4,680 6

The Egg' 6 Marine Harvest Norway AS "Egget" - lukket merdteknologi 14 10,920 13

Aquatraz 7 MNH Produksjon AS "Aquatraz" - semi-lukket merd 8 6,240 7

Slam Collector 8 Blom Fiskeoppdrett AS Teknologi for oppsamling av slam 8 6,240 7

MARKOB 9 Lerow AS "MARKOB" - Semi-offshore messingnettmerd med 8 6,240 7 400 50

Arctic Offshore Farming 10 Norway Royal Salmon ASA og Aker ASA Halvt nedsenkbart offshore oppdrettsanlegg i stål 15 11,700 14 900 60

Akvahub 11 Norsk Marin Fisk AS og Stjernefarm SUS "AkvaHub" - behandling mot lus og AGD med ferskvann i 3 2,340 3 100 33

Steeline 12 Kobbevik og Furuholmen Oppdrett AS "Steelline" - lukket produksjonsenhet i syrefast stål 4 3,120 4 410 103

Eide Fjordbruk 13 Eide Fjordbruk AS Åpen dataplattform og tilhørende systemer 6 4,680 6

Beck-Cage 14 Marine Harvest Norway AS "Beck-cage" - Offshore nedsenkbare bur 6 4,680 6

Marine Donut 15 Marine Harvest Norway AS "Marine Donut" heldekkende, lukkede enheter 8 6,240 7

Pipefarm 16 Lerøy Seafood Group AS "Pipefarm" lukket flytende lengdestrømsanlegg 9 7,020 8

Ocean Farming 17 Ocean Farming AS (SalMar) "Havmerd" basert på offshoreteknologi 8 6,240 7 690 86

HeliXir 18 Måsøval Fiskeoppdrett AS "Helixir" avlusningsflåte 3 2,340 3

Total 167 129,840 156 kt output

Cermaq? ? ? ?

Others….? ? ? ?

• How to differentiate? First come, first served?

• How to define what is technologically new vs. old?

• Legal actions from backers of rejected projects?

Average project cost of NOK63m per license = NOK10.5bn capex need, pre working capital

3356kt of planned land based farming projects…

56kt of planned capacity, but most of the projects are not fully financed and volumes are

unlikely to hit the market until 2017–2020, if they receive financing. To put the volumes into

context, 56kt would represent 2.6% of our 2016 global supply forecast of 2,070kt (HOG)

34Extension of the salmon cycle, this cycle looks set to last an unprecedented 8 years…

?

Conventional and non-conventional growth resume at the same time?

35Protein peer multiples

36Alaska Department of Fish & Game projects 40% less wild salmon in 2016…

37Disclaimer

IMPORTANT/DISCLAIMER

This note (the “Note”) must be seen as marketing material and not as an investment recommendation within the meaning of the Norwegian Securities Trading Act of 2007 paragraph 3-10 and the

Norwegian Securities Trading Regulation 2007/06/29 no. 876. The Note has been prepared by DNB Markets, a division of DNB Bank ASA, a Norwegian bank organized under the laws of the

Kingdom of Norway (the “Bank”), for information purposes only. The Note shall not be used for any unlawful or unauthorized purposes. The Bank, its affiliates, and any third-party providers, as well

as their directors, officers, shareholders, employees or agents (individually, each a “DNB Party”; collectively, “DNB Parties”) do not guarantee the accuracy, completeness, timeliness or availability of

the Note. DNB Parties are not responsible for any errors or omissions, regardless of the cause, nor for the results obtained from the use of the Note, nor for the security or maintenance of any data

input by the user. The Note is provided on an “as is” basis. DNB PARTIES DISCLAIM ANY AND ALL EXPRESS OR IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY

WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE, FREEDOM FROM BUGS, SOFTWARE ERRORS OR DEFECTS, THAT THE NOTE’S

FUNCTIONING WILL BE UNINTERRUPTED OR THAT THE NOTE WILL OPERATE WITH ANY SOFTWARE OR HARDWARE CONFIGURATION. In no event shall DNB Parties be liable to any

party for any direct, indirect, incidental, exemplary, compensatory, punitive, special or consequential damages, costs, expenses, legal fees, or losses (including, without limitation, lost income or lost

profits and opportunity costs) in connection with any use of the Note, even if advised of the possibility of such damages. Any opinions expressed herein reflect the Bank’s judgment at the time the

Note was prepared and DNB Parties assume no obligation to update the Note in any form or format. The Note should not be relied on and is not a substitute for the skill, judgment and experience of

the user, its management, employees, advisors and/or clients when making investment and other business decisions. No DNB Party is acting as fiduciary or investment advisor in connection with the

dissemination of the Note. While the Note is based on information obtained from public sources that the Bank believes to be reliable, no DNB Party has performed an audit of, nor accepts any duty of

due diligence or independent verification of, any information it receives. Confidentiality rules and internal rules restrict the exchange of information between different parts of the Bank and this may

prevent employees of DNB Markets who are preparing the Note from utilizing or being aware of information available in DNB Markets/the Bank which may be relevant to the recipients of the Note.

Please contact DNB Markets at + 47 22 94 89 98 for further information and inquiries regarding this Note, such as ownership positions and publicly available/commonly known corporate advisory

performed by DNB Markets etc, in relation to the Norwegian Securities Trading Act 2007/06/29 no. 75 and the Norwegian Securities Trading Regulation 2007/06/29 no. 876.

The Note is not an offer to buy or sell any security or other financial instrument or to participate in any investment strategy. Distribution of material like the Note is in certain jurisdictions restricted by

law. Persons in possession of the Note should seek further guidance regarding such restrictions before distributing the Note.

The Note is for clients only, and not for publication, and has been prepared for information purposes only by DNB Markets - a division of DNB Bank ASA registered in Norway with registration number

NO 984 851 006 (the Register of Business Enterprises) under supervision of the Financial Supervisory Authority of Norway (Finanstilsynet), Monetary Authority of Singapore, the Chilean

Superintendent of Banks, and on a limited basis by the Financial Services Authority of UK. Information about DNB Markets can be found at dnb.no.

Additional information for clients in Singapore

The Note has been distributed by the Singapore branch of DNB Bank ASA. It is intended for general circulation and does not take into account the specific investment objectives, financial situation or

particular needs of any particular person. You should seek advice from a financial adviser regarding the suitability of any product referred to in the Note, taking into account your specific financial

objectives, financial situation or particular needs before making a commitment to purchase any such product.

Recipients of the Note should note that, by virtue of their status as “accredited investors” or “expert investors”, the Singapore branch of DNB Bank ASA will be exempt from complying with certain

compliance requirements under the Financial Advisers Act, Chapter 110 of Singapore (the “FAA”), the Financial Advisers Regulations and associated regulations there under. In particular, it will be

exempt from: - Section 27 of the FAA (which requires that there must be a reasonable basis for recommendations when making recommendations on investments).

Please contact the Singapore branch of DNB Bank ASA at +65 6212 0753 in respect of any matters arising from, or in connection with, the Note.

We, the DNB group, our associates, officers and/or employees may have interests in any products referred to in the Note by acting in various roles including as distributor, holder of principal

positions, adviser or lender. We, the DNB group, our associates, officers and/or employees may receive fees, brokerage or commissions for acting in those capacities. In addition, we, the DNB group,

our associates, officers and/or employees may buy or sell products as principal or agent and may effect transactions which are not consistent with the information set out in the Note.

Additional Information, including for Recipients in the In the United States:

The Note does not constitute an offer to sell or buy a security and does not include information, opinions, or recommendations with respect to securities of an issuer or an analysis of a

security or an issuer; rather, it is a “market letter,” as the term is defined in NASD Rule 2211.

38You can also read