Small Banks in India-Issues and Challenges

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Proceeding of the First American Academic Research Conference on Global Business, Economics, Finance and

Social Sciences (AAR16 New York Conference) ISBN: 978-1-943579-50-1

New York, USA. 25-28 May, 2016. Paper ID: N624

Small Banks in India—Issues and Challenges

Prantik Ray,

XLRI Jamshedpur, India.

E-mail: prantik@xlri.ac.in

___________________________________________________________________________________

Abstract

With the granting of licenses to 11 payments banks and 10 small banks in September, 2015

the Indian banking sector has seen a major evolution in reaching out to a different clientele

and model of delivery which was not previously covered by the scheduled commercial banks.

The objective of the reform is to improve financial inclusion in the country. This paper

discusses the need for financial inclusion of a large priority sector in India that is left

unbanked or informally-banked. It discusses the RBI policy to further financial inclusion and

the recent licensing of Small Finance Banks in order to achieve so. Small finance banks start

with great promise of catering to rural and urban poor and the unbanked segment of

population but they also face huge challenges in terms of building the required capacity,

infrastructure to service a wide variety of clients and also to train its existing manpower to

reorient themselves for offering a more full-fledged service than a typical MFI. The paper

attempts to study the guidelines through which the RBI has licensed these banks, the backdrop

of this new experiment and the issues and concerns shared by a wide body of stakeholders.

The paper would also like to cite the example of Ujjivan, a leading NBFC-MFI, which has got

the small bank license and based on the interactions with the key executives and other

stakeholders of the firm the paper would like to elucidate the kind of future scenario the new

entrants in the banking field would likely to encounter.

___________________________________________________________________________

1

www.globalbizresearch.org

Proceeding of the First American Academic Research Conference on Global Business, Economics, Finance and

Social Sciences (AAR16 New York Conference) ISBN: 978-1-943579-50-1

New York, USA. 25-28 May, 2016. Paper ID: N624

Financial Inclusion

The dynamism of the real economy demands for a flexible and competitive banking

system to meet up the demands for various constituents of the economy. The Indian economy

has grown manifold in the last few decades and there has been progressive liberalization and

globalization of the economy. But there is still a huge chunk of population that remains

unbanked or informally banked. Close to 90 per cent of small businesses do not have formal

financial banking and around 60 per cent of the rural and urban populations have no financial

institution at all.

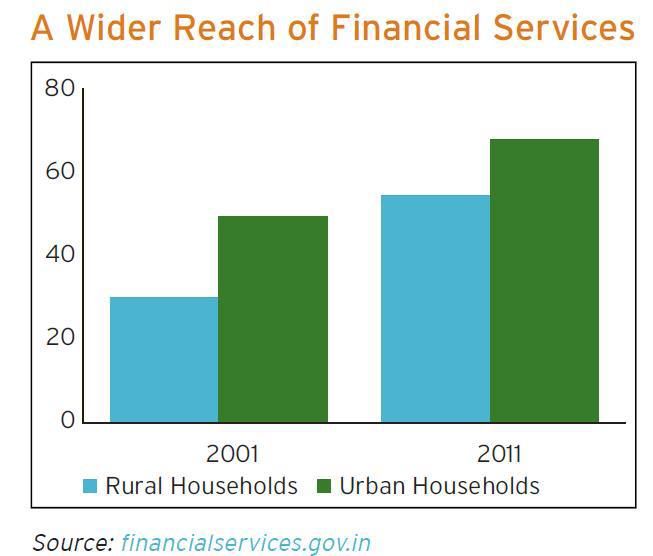

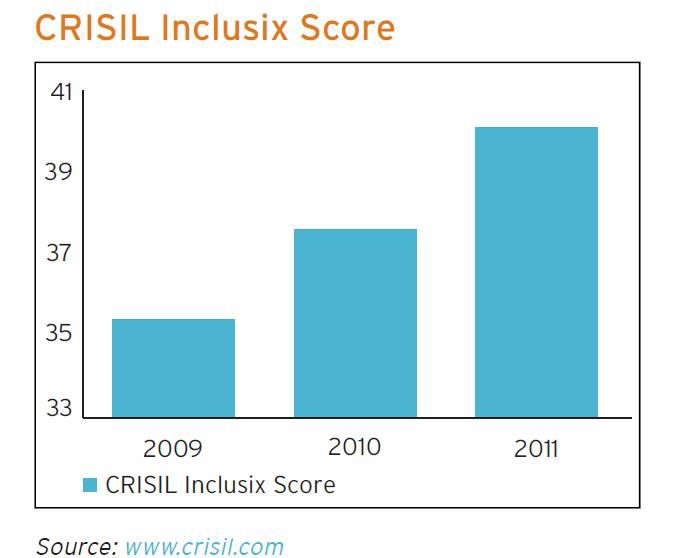

Figure 1 Figure 2

Figure 1 depicts the financial inclusion measured by CRISIL Inclusix based on branch

penetration, deposit penetration and credit penetration. The financial inclusion has clearly

improved from 2009 (35.4%) to 2011 (40.1%), but it is still very low and reflects under-

penetration of banking services in the country. As shown in figure 2, financial inclusion is

even lower in rural areas and this further varies from district to district. For instance, there are

four districts in the Northeast with only one bank branch among them [8].

Figure 3

2

www.globalbizresearch.org

Proceeding of the First American Academic Research Conference on Global Business, Economics, Finance and

Social Sciences (AAR16 New York Conference) ISBN: 978-1-943579-50-1

New York, USA. 25-28 May, 2016. Paper ID: N624

Based on data given in Basic Statistical Returns, it is estimated that rural India had only 7

branches per 1,00,000 adults in 2011 in sharp contrast with most of the developed and even

BRICS economies having over 40 branches [1].

An inclusive development and growth of the economy requires the extension of financial

services to all sections of the society. In a developing country like India, the growth is

accelerated by entrepreneurship, which can in turn be encouraged by improving financial

opportunities to MSMEs. As per a research estimation by KPMG, by the year 2020, the

MSME contribution to GDP is expected to increase from current 8 per cent to 15 per cent and

the generate employment levels to the extent of 50% of the overall employment, more than

doubling the current MSME workforce of 106 million across agricultural, manufacturing and

services sectors [2].

Figure 4

Source: Country Specific MSME Reports, KPMG Data & Estimates

The overall demand for finance in the MSME sector is estimated to be INR 32.5 trillion

($650 billion). The majority of finance demand from these enterprises is in the form of debt,

estimated at approximately INR 26 trillion ($520 billion). Total demand for equity in the

MSME sector is INR 6.5 trillion ($130 billion), which makes up 20 per cent of the overall

demand [3].

3

www.globalbizresearch.org

Proceeding of the First American Academic Research Conference on Global Business, Economics, Finance and

Social Sciences (AAR16 New York Conference) ISBN: 978-1-943579-50-1

New York, USA. 25-28 May, 2016. Paper ID: N624

Figure 5

Source: Report of Working Group on Rehabilitation of Sick MSMEs, Reserve Bank of India

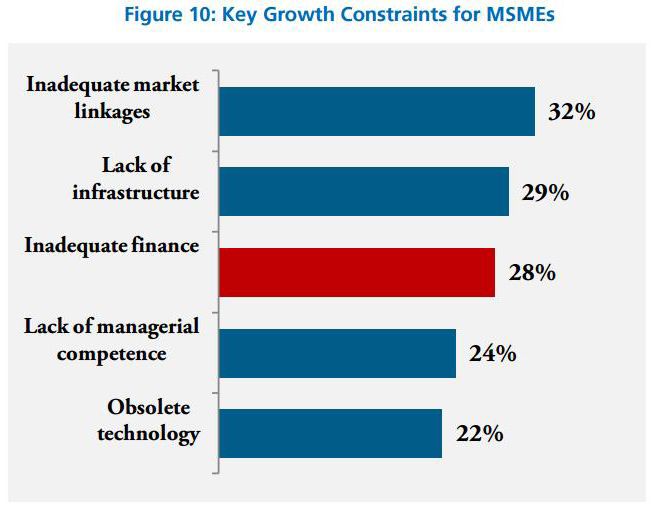

Financial institutions have traditionally limited their exposure to the priority sector due to

the perception that they carry high risk and high cost of delivery, and have limited access to

immovable collateral. Credit doesn't come easy for the businesses that haven't existed for at

least three years, haven't been profitable, and don't have assets to set aside as collateral for

loans.

Why Banks don’t Prefer Lending to Priority Sector?

The priority sector has very small ticket size and high transaction cost. Further, first

generation entrepreneurs lack experience of venturing and also fail to bring promoters

contribution. Their marketing is also generally weak and inadequate and globally

uncompetitive due to lack of product branding. They also lack collaterals and have low or no

credit rating. This makes priority sector lending highly risky, and hence banks avoid lending

to them [12].

These issues have left a huge section unbanked or informally banked. Thus, there is a

requirement to ensure that the financial needs of small businesses, unorganized sector, low

income households and farmers are met. Small finance banks are very important segments for

providing these services to meet the credit and remittance needs of this priority sector .

Local Area Banks

A previous experimentation was done for improving financial inclusion in 1996 by

licensing Local Area Banks. LABs were conceived as low cost structures for providing

efficient and competitive financial intermediation services in rural and semi urban population.

But LABs have since become high cost structures with cost income ratios ranging from 58.24

4

www.globalbizresearch.org

Proceeding of the First American Academic Research Conference on Global Business, Economics, Finance and

Social Sciences (AAR16 New York Conference) ISBN: 978-1-943579-50-1

New York, USA. 25-28 May, 2016. Paper ID: N624

per cent to 87.20 per cent as on March 2012 [1]. So the RBI extended its experimentation by

licensing Small Finance Banks in September 2015.

RBI guidelines: The major highlights of the RBI guideline are mentioned below [4]:

(i) Objective: With the objective to further financial inclusion, RBI granted licenses to 11

payments banks and 10 small banks in September, 2015 by (a) provision of savings vehicles,

and (b) supply of credit to small business units; small and marginal farmers; micro and small

industries; and other unorganized sector entities, through high technology-low cost

operations.

.(ii) Eligibility: Resident individuals/professionals with 10 years of experience in banking

and finance; and Companies and Societies owned and controlled by residents are eligible as

promoters to set up SFBs. Non-Banking Finance Companies (NBFCs), Micro Finance

Institutions (MFI) and LABs owned and controlled by residents are also allowed to opt for the

conversion into SFB.

(iii) Activities: SFBs will undertake basic banking activities of acceptance of deposits and

lending to unserved and underserved sections including small business units, small and

marginal farmers, micro and small industries and unorganized sector entities. A Small

Finance Bank cannot set up subsidiaries to undertake non-banking financial services

activities.

(iv) Capital requirement: The minimum paid-up equity capital for small finance banks shall

be Rs. 100 crore (lower than that for Universal Bank license which was pegged at Rs. 500

crore). In view of the inherent risk of a small finance bank, it shall be required to maintain a

minimum capital adequacy ratio of 15 per cent of its risk weighted assets (RWA) on a

continuous basis.

(v) Promoter's contribution: The promoter's minimum initial contribution to the paid-up

equity capital of such small finance bank shall at least be 40 per cent and gradually brought

down to 26 per cent within 12 years from the date of commencement of business of the bank.

(vi) Foreign shareholding: The foreign shareholding in the small finance bank would be as

per the Foreign Direct Investment (FDI) policy for private sector banks as amended from time

to time. As per the current FDI policy, the aggregate foreign investment in a private sector

bank from all sources will be allowed upto a maximum of 74 per cent of the paid-up capital of

the bank (automatic upto 49 per cent and approval route beyond 49 per cent to 74 per cent).

At all times, at least 26 per cent of the paid-up capital will have to be held by residents.

(vii) Prudential norms: The small finance bank will be subject to all prudential norms and

regulations of RBI as applicable to existing commercial banks including requirement of

maintenance of Cash Reserve Ratio (CRR) and Statutory Liquidity Ratio (SLR). No

5

www.globalbizresearch.org

Proceeding of the First American Academic Research Conference on Global Business, Economics, Finance and

Social Sciences (AAR16 New York Conference) ISBN: 978-1-943579-50-1

New York, USA. 25-28 May, 2016. Paper ID: N624

forbearance would be provided for complying with the statutory provisions. At present, the

CRR is prescribed at 4% and SLR at 21.5% of a bank's total of DTL.

The small finance banks will be required to extend 75 per cent of its Adjusted Net Bank

Credit (ANBC) to the sectors eligible for classification as priority sector lending (PSL) by the

Reserve Bank. At least 50 per cent of its loan portfolio should constitute loans and advances

of upto Rs. 25 lakh.

(viii) Additional conditions for NBFCs/MFIs/LABs converting into a bank:

An existing NBFC/MFI/LAB, if it meets the conditions under these guidelines, could apply to

convert itself into a small finance bank, after complying with all legal and approval

requirements from various authorities. In such a case, the entity shall have a minimum net

worth of Rs. 100 crore or it shall infuse additional paid-up equity capital to achieve net worth

of Rs. 100 crore. It may be noted that on conversion into a small finance bank, the NBFC /

MFI will cease to exist and all its business which a bank can undertake should fold into the

bank and the activities which a bank cannot statutorily undertake be divested / disposed of.

Further, the branches of the NBFC/MFI should either be converted into bank branches or be

merged / closed as per the business plan. The small finance bank and the NBFC / MFI cannot

co-exist.

Banks are precluded from creating floating charge on their assets. For such NBFCs / MFIs,

which succeed in obtaining licenses to convert into small finance banks, if they have created

floating charges on their assets for secured borrowings which stand in their balance sheets on

the day of conversion into a bank, RBI will permit grandfathering of such borrowings till their

maturity, subject to imposition of additional capital charge in order to protect the interest of

the depositors.

Analysis of RBI Guidelines

The guidelines clearly indicate that the objective of this licensing is to further the

financial inclusion of the priority sector. But the local nature of business would expose Small

Finance Banks to higher risks, so care has been taken to license only experienced players in

the field. It is observed that the banks that have done well in the past were those promoted by

financial institutions. These successful banks had adequate experience in the financial

services field, financial resources, a sound business model, and were well equipped in every

way to run a bank. RBI has thus given due importance to the credentials and integrity of

applicants. The 10-year track record criteria will ensure that only experienced applicants with

a sound business model and those that have demonstrated the ability to run a successful

business are given entry into this sector [8].

Further, the guidelines do not allow Small Finance Bank to delve in complex

sophisticated products as the target clientele is expected to be a first-timer or relatively new

6

www.globalbizresearch.orgProceeding of the First American Academic Research Conference on Global Business, Economics, Finance and

Social Sciences (AAR16 New York Conference) ISBN: 978-1-943579-50-1

New York, USA. 25-28 May, 2016. Paper ID: N624

user of financial services. This will ensure that the basic needs of a customer in the unserved

or underserved areas are met and the Small Finance Banks focus on their basic banking

activities and do not take undue risks of expanding to other activities.

The minimum equity capital requirement for Small Finance Bank is kept at Rs. 100 crore

which is lower than that of the Universal Bank. This can be attributed to the small size of

operations and limited scope of activities of the Small Finance Bank compared to a Universal

Bank.

A minimum CAR of 15 per cent is to be maintained by the banks on a continuous basis.

This CAR requirement is higher than the 9 per cent requirement for scheduled commercial

banks as well as 13 per cent for the new Universal Bank licenses. This clearly indicates that a

Small Finance Bank is perceived riskier as compared to the Universal Bank due to its local

nature of business.

The shareholding for promoters is considerably higher compared to the Universal Bank as

the RBI believes that a Small Finance Bank would need greater handholding and it is

important to have the promoter on board for a longer time to preserve the local nature of the

bank. The guidelines also do not put restrictions on foreign shareholding as stringent as that

for the Universal Bank licenses.

The Priority Sector Lending (PSL) target is set at 75 per cent of its ANBC, which is

significantly higher compared to the 40 per cent for scheduled commercial banks. This again

reflects the focus of small finance banks towards the priority sector. The guidelines also

prevent any undue concentration risks and encourage wider customer base of small

borrowers.

RBI has also tried to ensure that only healthy entities opt for SFB licensing and also

restricts the coexistence of any two entities simultaneously. RBI promotes this conversation

and intends to make the conversion as seamless as possible for specific items on the books of

the entity seeking conversion [7].

RBI finally granted approval to 10 of the 72 applicants on September 16, 2015 to set up

Small Finance Banks: Au Financiers India Ltd., Capital Local Area Bank Ltd., Disha

Microfin Private Ltd., Equitas Holdings P Limited, ESAF Microfinance and Investments

Private Ltd., Janalakshmi Financial Services Private Limited, RGVN (North East)

Microfinance Limited, Suryoday Micro Finance Private Ltd., Ujjivan Financial Services

Private Ltd. and Utkarsh Micro Finance Private Ltd. Out of these ten companies, 8 operate in

the microfinance sector, one is NBFC (Au Financiers India Ltd) and one is LAB (Capital

Local Area Bank Ltd.). The “in-principle” approval granted will be valid for 18 months.

7

www.globalbizresearch.orgProceeding of the First American Academic Research Conference on Global Business, Economics, Finance and

Social Sciences (AAR16 New York Conference) ISBN: 978-1-943579-50-1

New York, USA. 25-28 May, 2016. Paper ID: N624

Why MFI/NBFC/LABs?

Micro Finance Institutes, Non-Banking Finance Companies, and Local Area Banks are

concentrated in rural areas and provide services where commercial banks are not available or

unwilling to offer services. They follow relationship banking which makes their network and

customer base really good and helps them reach the targets of opening rural branches and

financial inclusion. The kind of loans they offer can also go a long way in meeting priority

sector requirements. This makes them ideal vehicles for achieving the RBI’s objective of

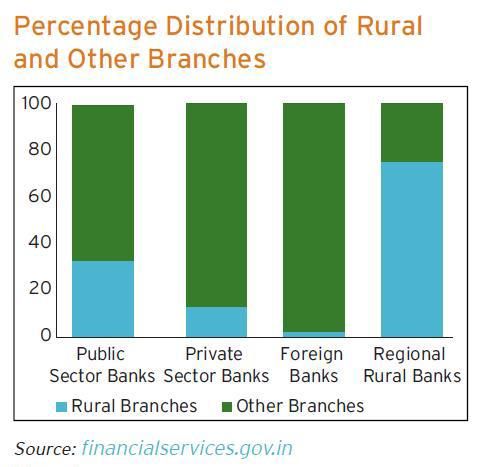

financial inclusion. Figure 6 clearly indicates that private sector banks and foreign banks have

the least number of rural branches. This also promotes to focus more on local financial

service providers for financial inclusion.

Figure 6

On the flip side, such entities can be hampered by low profitability and inferior asset quality

as most of their loan portfolio is unsecured [8].

MFIs to SFBs:

Licensing would help MFIs to raise deposits, which, in turn will bring down their cost of

funds substantially and allow them to lend at more reasonable rates than they do now.

Microfinance institutions currently raise funds from banks for on-lending at 12-14%. RBI

norms issued in February allows large microfinance companies with a loan book of Rs. 100

crore and above to charge up to 10% spread on their cost of funds to customers. For small

microfinance companies, this rate is fixed at 12%. This means the average interest rate in the

microfinance industry is currently 22-24%. Converting to small finance bank would help

these MFIs to cut down their cost of funding substantially. According to the chief executive

officer of MFIN, if the fully loaded cost of funds for a small finance bank comes to 10%, with

a spread of around 6%, they could offer micro-loans at around 16%, a huge drop over the

existing 22-24% levels.

8

www.globalbizresearch.orgProceeding of the First American Academic Research Conference on Global Business, Economics, Finance and

Social Sciences (AAR16 New York Conference) ISBN: 978-1-943579-50-1

New York, USA. 25-28 May, 2016. Paper ID: N624

Advantages of SFBs:

Relationship banking and small capital of SFBs promote the lending to small borrowers,

and hence improve financial inclusion. Their confinement to a particular region helps them

understand the needs and business potential of that area and this develops core competence

through relationship banking in financing agriculture, SMEs, industries, and thus serve their

credit needs better. SFBs require less infrastructure and staff and hence have low operational

expenses. Their simple structure further reduces the contagion and the resolution also

becomes easier.

Limitations and Challenges of SFBs:

Small banks are geographically concentrated and hence are more vulnerable to systemic

risk (weather, crop prices, and regional economic performance) as compared to large banks.

Their local nature also makes them more prone to capture. This could lead to persistent

governance problems and owing to the higher exposure to risk, they have to have to pay a

higher rate to their depositors which in turn, might create the need to make riskier loans

resulting in a vicious cycle of rising non-performing assets.

SFBs are directed to extend 75 per cent of its Adjusted Net Bank Credit (ANBC) to the

sectors eligible for classification as priority sector lending (PSL) by RBI. The priority sector,

comprising of agriculture, small enterprises and low-income earners, intensifies the

vulnerability of these banks to local economy. This demands to maintain a minimum capital

adequacy ratio of 15 per cent of its risk weighted assets (RWAs) which is quite high.

The initial challenge for the newly licensed banks will be to adjust their promoter’s

contribution and foreign shareholding to comply with the RBI guidelines. Many of the

institutions have foreign shareholding as high as 90 per cent, and so they will need to dilute

this to 49 per cent. Some microfinance institutions like Equitas and Ujjivan are releasing IPO

for diluting this shareholding.

The next challenge would be to restructure and transform into a bank from a non-banking

financial institution and offer multiple banking products. It would be a high cost affair for

developing a technologically sound system for low cost products. It requires large capital to

build automated teller machine (ATM), automated banking machine (ABM) or automated

branch network and this will make the delivery of banking services costly.

The institutional transformation will also require the induction of new and diversified talent

from the banking sector as well as training the existing staff to accustom them to this new

system of delivering services.

9

www.globalbizresearch.orgProceeding of the First American Academic Research Conference on Global Business, Economics, Finance and

Social Sciences (AAR16 New York Conference) ISBN: 978-1-943579-50-1

New York, USA. 25-28 May, 2016. Paper ID: N624

Case Study for Conversion of Ujjivan Financial Services Pvt. Ltd. to SFB:

Ujjivan Financial Services, a microfinance institution, is one of the ten institutions which

has been granted license for conversion to small finance bank. Ujjivan Financial Services

started with the mission of providing a full range of financial services to the economically

active poor who are not adequately served by financial institutions. Presently, their operations

is spread across 24 states and union territories, and 209 districts across India, making them the

largest MFI in terms of geographical spread. They serve over 2.77 million active customers

through their 469 branches and 7,786 employees and their Gross assets under management

(AUM) stands at ₹40.88 billion as on September 2015 making them one of India's leading

Microfinance Institutions. Their customer retention ratio was noted as 89.18% as of

September 30, 2015.

Ujjivan's business is primarily based for providing collateral free, small ticket-size loans

to economically active poor women. They also offer individual loans to Micro & Small

Enterprises ("MSEs"). Ujjivan has adopted an integrated approach to lending, which

combines a high customer touch-point typical of microfinance, with the technology

infrastructure and related back-end support functions similar to that of a retail bank. This

integrated approach has enabled it to manage increasing business volumes and optimize

overall efficiencies [13].

Their business model, size, highly cost effective operations, robust technology ecosystem,

committed workforce, target customers and their reach to this target group makes them ideal

player for Small Finance Bank licensing.

As a Small Finance Bank, Ujjivan will provide personal banking as well as MSE banking.

Existing range of credit products will be supplemented by innovative saving and payment

products. The bank will be targeting various segment of financially excluded people through

differentiated product offering.

The company has planned its transition from a microfinance institution to a small finance

bank via a three-phase strategy - Prepare, Transform and Grow. The focus of the company for

the first 2 years would be towards the transition, and afterwards it would be focusing over its

growth. For the transition, the company will be focusing on growing its own individual

portfolios, mainly the micro and small enterprise funding and the housing segment. It would

deter from competing with retail banks and would focus more on unserved or underserved

clientele. As per RBI guidelines, 25 per cent of the small finance bank branches have to be

unbanked areas. So, the major challenge of Ujjivan would be to increase its geographical

footprint in unbanked areas. The company is planning to convert its 469 branches to bank

branches in phases [14].

10

www.globalbizresearch.orgProceeding of the First American Academic Research Conference on Global Business, Economics, Finance and

Social Sciences (AAR16 New York Conference) ISBN: 978-1-943579-50-1

New York, USA. 25-28 May, 2016. Paper ID: N624

Further, Ujjivan will be able to comfortably meet the CRR and SLR limits given its

prudent financial track record. Being a microfinance institution, Ujjivan lends predominantly

to the priority sector as categorized by RBI. Around 87 per cent of the company’s current

asset base is classified as PSL portfolio under PSL rules for NBFCs. Therefore, after the

transition, the company would comfortably meet its priority sector lending target of 75 per

cent as set by RBI.

Ujjivan Financial Services Private Limited will be the promoter of the new small finance

bank. It will float a subsidiary and transfer its business to the subsidiary, which shall be

converted as the small finance bank within the 18 month transition period, on receiving in-

principle approval.

Under the current RBI regulations, the SFB will have to be listed in three years. Ujjivan is

expecting to start small finance banking operations from January 2017. As of 31 March 2015,

their foreign shareholding was 88.69 per cent, and so they have planned to release IPO to

bring this down to 49 per cent. With pre-IPO in February 2016, the foreign ownership has

already been brought down to 77 per cent, and the institution is expecting a post-IPO

shareholding of around 44 per cent, which complies with the guidelines.

Ujjivan currently has a well-defined technology plan, architecture and governance in

place. Technology initiatives such as hand-held devices for last mile connectivity, automated

loan processing, CBS connected branches and repayment through ECS/ACH has set industry

standards in customer service. The small finance bank will leverage the existing technology

platform and build on it to develop and deliver innovative banking solutions to the unbanked.

It also intends to aggressively invest in technology to further increase its reach and better

serve the customer needs on top of its existing microfinance business [15].

The Way Forward

While small banks have the potential for financial inclusion, performance of these banks

in India (Local Area Banks and Urban Co-operative Banks) has not been satisfactory. So if

small banks are to be preferred, the issues relating to their size, numbers, capital

requirements, exposure norms, regulatory prescriptions and corporate governance need to be

suitably addressed.

Further, in a dynamic economy, banks would either grow or fail. So, the number of small

institutions at the root level will likely shrink over a period of time even as the population

needing basic financial services increases. This demands for a regular licensing of institutions

to provide a steady supply of financial services to the priority sector.

11

www.globalbizresearch.orgProceeding of the First American Academic Research Conference on Global Business, Economics, Finance and

Social Sciences (AAR16 New York Conference) ISBN: 978-1-943579-50-1

New York, USA. 25-28 May, 2016. Paper ID: N624

References

Cognizant (Nov 2013), Obtaining New Banking Licenses in India: Challenges and Opportunities, 2-9.

http://blog.microsave.net/small-finance-banks-are-you-ready-the-opportunities-and-challenges/

http://economictimes.indiatimes.com/industry/banking/finance/banking/ujjivan-expects-modest-

growth-on-way-to-becoming-a-small-bank/articleshow/51935266.cms

http://indiamicrofinance.com/small-finance-bank-licences-8-rbi.html

http://ujjivan.com/index.php

http://www.ifc.org/wps/wcm/connect/4760ee004ec65f44a165bd45b400a808/MSME+Report-03-01-

2013.pdf?MOD=AJPERES

http://www.iibf.org.in/documents/reseach-report/Report-30.pdf

http://www.livemint.com/Industry/hNLMqLZPCeY3HR4CVgr1cP/Many-microfinance-institutions-

keen-on-small-bank-licence.html

http://www.tribuneindia.com/news/business/smes-largely-availing-loans-from-nbfcs-for-

expansion/208548.html

http://www2.deloitte.com/content/dam/Deloitte/in/Documents/financial-services/in-fs-deloitte-pov-on-

small-finance-bank-license-guidelines.pdf

https://rbi.org.in/scripts/bs_viewcontent.aspx?Id=2901

https://www.kpmg.com/IN/en/IssuesAndInsights/ArticlesPublications/Documents/The%20new%20wa

ve%20Indian%20MSME_Low%20Res.pdf

Report by Committee on Comprehensive Financial Services for Small Businesses and Low Income

Households (December 2013), 25-51.

Reserve Bank of India (August 2013), Banking Structure in India - The Way Forward, Discussion

Paper, by Department of Banking Operations and Development (DBOD) and Department of Economic

and Policy Research (DEPR), 8-24, 76-80.

Ujjivan Financial Services Private Limited, Application for small finance bank licenses, Executive

Summary, 1-41.

12

www.globalbizresearch.orgYou can also read