Warren Buffett's Secret 600% Investment - By Tom Dyson and The Palm Beach Letter Research Team

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Warren Buffett’s Secret 600%

Investment

By Tom Dyson and The Palm Beach Letter Research Team

© 2015 Palm Beach Research Group. All rights reserved. Protected by copyright laws of the United States and international treaties. Any reproduction, copying, or redistribution, (electronic or otherwise) in whole or in part, is strictly prohibited without the express written permission of Palm Beach Research Group, 55 NE 5th Avenue Suite 100, Delray Beach, FL 33483. DISCLAIMER: This work is based on what we’ve learned as financial journalists. It may contain errors and you should not base investment decisions solely on what you read here. It’s your money and your responsibility. Nothing herein should be considered personalized investment advice. Although our employees may answer general customer service questions, they are not licensed to address your particular investment situation. Our track record is based on hypothetical results and may not reflect the same results as actual trades. Likewise, past performance is no guarantee of future returns. Palm Beach Research Group expressly forbids its editors fr m having a financial interest in their own securities recommendations to readers. Such recommendations may be traded, however, by other editors, Palm Beach Research Group LLC, its affiliated entities, employees, and agents, but only after waiting 24 hours after an internet broadcast or 72 hours after a publication only circulated through the mail. Palm Beach Research Group welcomes comments or suggestions here. This address is for feedback only. For questions about your account, or to speak with customer service, call 8885012598 (U.S.) MondayFriday, 9 a.m.7 p.m. EST, or email us here. We look forward to your feedback and questions. However, the law prohibits us from giving individual and personal investment advice. We are unable to respond to emails and phone calls requesting that type of information.

Warren Buffett’s Secret 600% Investment How to Make an Income Extermination Fortune From PreOwned U.S. Government Securities America’s banking industry is on fire… According to American Banker magazine, not counting recent legal settlements, the six largest banks in America generated a combined $90 billion in banking profits in 2013. The previous record was set in 2006 at the peak of the housing bubble. That year, the big six banks generated $85 billion. 2013 was also an incredible year for growth in the banking sector. Seven years ago in 2007, the five largest banks controlled 38.4% of the banking industry. This year, combined, they control 44.2% in assets. That’s up from 2012’s 43.5%. Their troubles with bad loans have also receded. The FDIC said banks set aside $5.8 billion in provisions against loan losses during the third quarter of 2013, a 60% drop from the same period in 2012 and the smallest amount in any quarter since 1999. “Asset quality continues to improve, loan balances are up, and the numbers of unprofitable institutions, problem banks, and bank failures continue to decline,” said The Wall Street Journal recently. But as I’m about to show you, life in the banking industry is about to get even better… I’ve dedicated the last six months of my life to researching, digging up, and reading about ways to profit from the huge megatrend in rising interest rates. In this special report, I’m going to show you why this megatrend of rising interest rates in going to cause bank stocks to soar… Then, I’m going to reveal my two favorite bank stocks. One is a favorite of Warren Buffett. His company—Berkshire Hathaway—has large holdings in this company. The other is one of the largest credit card distributors in the country, with more

than 40 million cardholders. My calculations show these banks could

conservatively rise by 200% and 150% over the next five years.

Finally, I’m going to recommend you buy a very aggressive security—preowned by

the U.S. government—that will amplify the returns of the stocks.

Few people know about these securities, but you can buy them on the stock

exchange as easily any other stock.

If these two bank stocks rise according to my projections, instead of making 200%

in stock No. 1, we could make 600%. And instead of making 160% in stock No. 2,

we could make 340%.

Let’s get to it…

How The U.S. Banking Sector Booked the Largest Ever Banking

Profit in 2013

At its core, banking is a simple business. Banks collect deposits, then lend the cash

to businesses, individuals, and sometimes even the federal or foreign governments.

Have you ever heard banking described as a “363 business”? You borrow at 3%,

you lend at 6%, and you’re on the golf course by 3 o’clock. Minus the golf, that’s

pretty much still the case for most banks in America.

They pay a low interest rate to depositors, but charge a high interest rate to

borrowers. The difference in the interest rates is called the “net interest margin” or

“interest rate spread.” It represents the bank’s revenue.

Here’s how it works: If a bank wants to borrow $10 million from another bank, it

pays 1% in interest per year, or $100,000.

That’s how much it costs the bank to borrow that money.

But if the bank then loans out that money at 5%, it would receive $500,000 on that

same $10 million.

The difference between the income that money generated (5%) and how much it

cost (1%) is the spread or net interest margin.

Assuming nothing bad happened to the loan, the bank would book $400,000 in

annual net interest on this loan.

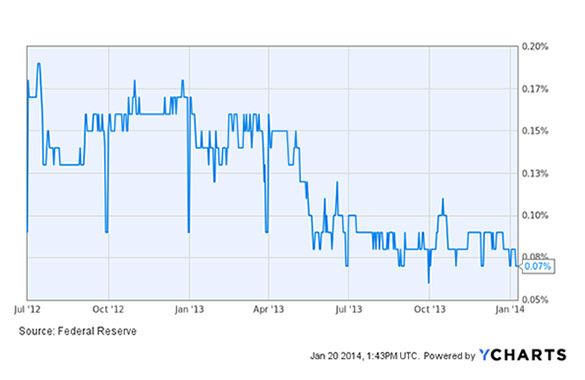

This transaction is the bread and butter of the banking business and accounts forbillions in revenue every single day. So why are banks able to borrow so cheaply and lend at higher rates? Many reasons. But the most important is time. When banks borrow, they take shortterm loans. These loans could be overnight loans… or oneweek loans or onemonth loans. Because there is less chance of something going wrong in the near future, interest rates on these shortterm loans are low… typically less than 1%. But when banks lend this money, they use terms of five, 10, or even 30 years (in the case of a mortgage). Interest rates on longterm loans are much higher. Currently, 30year mortgage loans pay around 4.5%. In the banking industry, this transaction is called “borrowing short and lending long.” The larger the spread between longterm and shortterm interest rates, the more money banks make. So bankers love it when longterm interest rates rise, compared with shortterm interest rates. Their net interest margins expand. Let me give you a reallife example. Below is a chart of the Federal Funds Rate. This is the official rate for shortterm loans between banks and the government. The Fed Funds Rate is the benchmark the markets use to set all other shortterm interest rates. So it’s a close approximation for the rate that banks typically charge each other for shortterm loans.

Currently, Fed Funds are yielding just 0.07%… less than onetenth of 1%. In other words, banks such as Wells Fargo and Citigroup have to pay 0.07% interest to borrow money. Meanwhile, this chart shows 30year mortgage rates, a good proxy for the interest rate that banks earn on their loans.

Right now, rates are around 4.5%. This is the rate banks such as Wells Fargo and Citigroup collect on the loans they make. This is creating a virtual printing press for the banks. The banks can borrow money at rates between zero and 0.5%. Remember, this is how much it costs banks to borrow money. Then they lend it out to the public via 30year mortgages at 4.5%. This difference generates a lot of income. If you subtract the current cost of money (0.07%) from the rate that banks lend it at (4.50%), it equals a spread of 4.43%. This means that for every $100 billion a bank lends out at 4.5%, it’s making approximately $4.43 billion in net interest from its borrowing and lending activities. Wells Fargo has assets of $1.5 trillion. It’s the largest bank in the U.S. And it’s on target to make more than $40 billion in net interest in 2013, with a net interest margin close to 3.5%. These massive earnings have propelled Wells Fargo to become the most profitable bank in America. Here’s the thing… The wider this spread becomes, the more money these banks make. (The converse is true too. If the spread narrows, they’ll make less money.)

Over the last year, longterm interest rates have moved up sharply. Look at the chart of 30year mortgage rates again. Mortgage rates have spiked up from a low of 3.2% to a high of near 4.5% in just a few months. You can see from the chart that, unlike longterm rates, shortterm rates have barely budged. They’ve been fluctuating between 0.06% and 0.2%. If interest rates continue to rise, this gap between shortterm and longterm rates will widen. For example, let’s say those 30year mortgage rates rose only a percentage from 4.5%, to 5.5%. Let’s also say that shortterm rates inched up just a bit to 0.09%. The new spread would be 5.41%. So now, for every $100 billion lent out at 5.5%, the banks will make $5.41 billion in gross annual profits. That’s an additional $1 billion in profits per year for every $100 billion they lend. In the former example, that same bank with an $800 billion loan portfolio would increase its profits by $8 billion. That’s an 18% rise in revenues by increasing the interest rate by just one percentage point. Why LongTerm Rates Will Rise but ShortTerm Rates Will Not In order for the banks to make a fortune, two things have to happen: Longterm rates have to rise. And shortterm rates have to NOT rise. These two things will cause banks’ net interest margins to expand and their profits to soar. The Fed has also started to slow its purchases of longterm government bonds. On December 18, 2013, the Fed announced it would cut its purchases of longterm bonds by $10 billion per month. This action has and will lead to steadily higher longterm rates. I’ve laid out my full case for why interest rates have to rise in this the Income Extermination special report. But what about shortterm interest rates? Here’s how we know that shortterm rates aren’t going up: At its last meeting on December 18, 2013, the Fed publicly announced that it will keep the Fed Funds Rate low for “well past the time that the unemployment rate declines below 6.5%, especially if projected inflation continues to run below the [Federal Open Market Committee’s] 2% longerrun goal.”

What the Fed is saying here is that even if the unemployment rate drops to 6.5%, it

will keep shortterm rates low as long as the inflation rate is below 2.5%. From the

Federal Open Market Committee in December 2013:

The committee also reaffirmed its expectation that the current

exceptionally low target range for the Federal Funds Rate of 00.25% will

be appropriate at least as long as the unemployment rate remains above

6.5%, inflation between one and two years ahead is projected to be no

more than a half percentage point above the committee’s 2% longerrun

goal, and longerterm inflation expectations continue to be well anchored.

This means the Fed is providing a public guarantee it will keep the shortterm

borrowing rate low. The views of the Fed aren’t likely to change anytime soon,

despite Ben Bernanke’s departure as chairman.

The new head of the Fed, Janet Yellen, and Vice Chairman Stanley Fisher voted in

agreement with Ben Bernanke at a Fed meeting on December 18th. This is

important because the upandcoming leadership is on board with keeping short

term interest rates low. If they weren’t, they would have voted against the decision.

Remember, banks make great profits by paying little for borrowed money and then

charging a lot when they loan that money out to homebuyers. This secured Federal

Reserve policy of allowing longterm rates to rise and keeping shortterm rates low

will create an environment for outsized profits for the banks. As shortterm rates

stay low and longterm rates rise, net interest margins of all banks will expand.

This profit margin expansion will lead to an

explosion in earnings. This scenario is exactly what

happened in the early 1990s

The bottom line is that by government policy, as banks were recovering

the Federal Reserve System is creating an from the last real estate bust.

environment in which the difference between

shortterm and longterm rates is engineered to In the chart below, you can

be wider. see that net interest margins

grew from 4% in 1990 to as

The Fed is doing this to incentivize the banks to high as 4.9% in 1994.

lend more. Remember, bigger net interest

margins mean more money for the banks. But During that same period, the

they get to capture that spread only if they earnings of the major banksincrease the volume of their loans.

This brings me to the second reason why I

believe now is the time to make our move into

bank stocks.

Loosening Credit Standards

During the 2008 financial crisis, wary banks exploded higher, as did their

and mortgage lenders scaled back. They made it stock prices.

difficult to borrow, didn’t lend as freely, and

enacted strict vetting standards. But these Citigroup went from $20 to

standards are slowly being loosened. $76. Bank of America grew

from $4.20 to $14.50.

According to data by Ellie Mae, which provides JPMorgan grew from $3.20

mortgage lenders with loan origination systems, to $15.45. And Wells Fargo

the average credit score among borrowers who went from $1.75 to $7.21.

received a mortgage in September 2013 was

732, down from a peak of 750 a year prior. During this period, the

average gain for these big

That’s also the lowest average credit score since banks was 402%.

the company started tracking this data in

August 2011. In addition, greater shares of Currently, the average net

borrowers have lower credit scores. According interest margin of banks

to the findings, 32% of mortgages in September with $1 trillion or more in

went to borrowers with an average credit score assets is 3.03%. The two

of less than 700, compared with 17% a year ago. banks I’ll tell you about

today have net interest

“Lenders are being more lenient,” said Brad margins of 3.38% and

Hunter, chief economist at Metrostudy, a 6.89%, respectively.

housing market research and consulting firm.

Until now, millions of hopeful homebuyers have

been shut out of the housing market. As lending standards continue to drop, these

buyers will come flooding back into the mortgage market.

But there is more behind the banks’ willingness to lower credit standards.

Housing prices are now going up, not down. This means it’s much safer to lend

money against an appreciating asset rather than a declining one. The banks will be

able to extend credit to riskier applicants because, even if the applicants default,

their real estate will be worth more than the amount they borrowed.This scenario hasn’t been true for more than seven years. We are looking at a combination of factors coming together to blast bank earnings higher. The start of a brandnew lending cycle, along with a Fedsanctioned increase in net interest margins, will cause an upward revaluation of bank stocks, just as it did in the early 1990s. Now that you understand what’s behind this onceinageneration moneymaking opportunity, let me tell you about two bank stocks that are poised to cash in on this upcoming trend and how you can get involved. 200% Returns From Warren Buffett’s Largest Investment The first stock I want to tell you about is a major banking name that escaped the financial crisis scandalfree. For decades, Wall Street has priced a premium on this bank’s shares. This is largely due to the bank’s fiscally responsible administration. The company is so well respected that it happens to be the single biggest holding of Warren Buffett’s Berkshire Hathaway. Twenty percent of his $100 billion portfolio is in this one stock. In fact, he boosted his position in this bank by another 4% just this year alone. Let me be clear though… with or without Buffett’s endorsement, this is a cheap stock. I’ll show you why in a minute. But first, you should know that this company also happens to be the largest originator of home mortgages in America. This means it is perfectly positioned to profit from both the Fed’s actions to keep borrowing rates low while loan rates increase and the improving housing market. As the largest U.S. mortgage lender, this bank is in the sweet spot of the new Fed driven boom. The name of the company you want to own is Wells Fargo (NYSE: WFC). Buffett is already entirely behind this company. But that doesn’t mean it’s already past its moneymaking days. This stock is still incredibly cheap. Here’s why… Banks are typically valued using “book value.” Book value is an accounting term used to describe the value of the assets a company holds. Wells Fargo has a projected 2014 book value of $29.15 per share. Over the 20 years before the 2008 financial crisis, Wells Fargo had normally traded at a valuation of 2.53 times book value. Even during the 2002 “tech wreck,” Wells Fargo never got cheaper than 2.2 times book value.

Investor sentiment toward banks is currently so poor that even after surviving the

financial meltdown, Wells Fargo is trading at only 1.5 times the book value. This

low valuation reflects Wall Street’s and Main Street’s irrational fear of banks.

It’s irrational because Wells Fargo has far less debt and far more capital than at

any other time in its 150year history. In 2008, WFC had $192 billion in debt.

Today it has $151 billion. In 2008, it had $1.3 trillion in assets. Today, it has $1.5

trillion. In 2008, it earned $0.70 per share. This year, it’ll earn $3.90 per share.

Wells Fargo is twice the company it was in 2008. Yet it’s trading at a 50% discount

to its historical valuation. That means this stock is cheap.

Remember when I said investors such as Buffett look for massive discounts on

solid companies at very particular times in history? This is one of those discounted

stocks. And this is one of those times. The housing market will continue to recover,

and the Fed will keep shortterm rates low while longterm rates rise.

Wells Fargo’s stock is going to soar…

Here’s what this all means for investors.

What’s the Stock Worth?

Let’s look at a conservative scenario in which I think you can make at least 200%

on your money.

Let me explain…

Since 2001, Wells Fargo has been growing its book value at a 12% compounded

annual growth rate.

Wells Fargo’s Yearly Book Values

Year Price

2001 $8.00

2002 $8.98

2003 $10.15

2004 $11.17

2005 $12.122006 $13.58

2007 $14.45

2008 $16.15

2009 $20.03

2010 $22.49

2011 $24.64

2012 $27.64

Let’s make an assumption that the bank’s book value will grow at a very pedestrian

pace of 8%. Remember that banks are typically valued using their book values,

which is a term describing a company’s asset value. Wells Fargo is currently

trading at only 1.5 times the book value. This is extremely low, because Wells

Fargo typically trades at 2.53 times book value.

We’ll start with a book value of $27.64 for 2012 (2013’s final numbers aren’t out

yet). Even if we make a conservative estimate of 8% growth, that gives us $43.86 of

book value in 2018.

Conservative Prediction of Book Values

Year Price

2012 $27.64

2013 $29.85

2014 $32.24

2015 $34.82

2016 $37.60

2017 $40.61

2018 $43.86

Even if the company stays at its current valuation of 1.5 times the book value, itwill be a $66 stock. Let me remind you that it’s currently around $45.

Under this scenario, that’s close to a 50% gain.

That’s not a bad return, but it’s not exactly what I’m looking for.

You see, the market loves to move in extremes. Right before the financial crisis in

2008, banks routinely traded for three times the book value. This is a normal

range for Wells Fargo. Under this scenario, the stock would be worth $131. That’s a

191% return over five years.

Given the ripening environment, I believe that’s where we are headed. Wall Street

and Main Street will start to realize that the banks aren’t ready to collapse anytime

soon. In a moment, I am going to show you how we can amplify that return to

close to 600%. There is a way for us to do it without using options or leverage.

I’ll explain it to you in detail in just a moment, but first I want to tell you about

another bank stock that can greatly grow your returns.

The 150% Credit Card Giant

The next stock to own is both a commercial bank and the fifth largest credit card

issuer in the world. It is also the ninth largest commercial bank in America.

Before I reveal the stock, I need to tell you that two emerging trends are about to

converge and will greatly benefit this company. The last time these two trends

came together, this stock ran 1,485% higher. That’s not a typo. This time around, I

expect the stock to double in value at the very least. But by using the special

method I mentioned earlier, we could amplify that gain to 230%.

You’re already up to speed on the first upcoming trend, which is the growth that

we will see in net interest margins. This company has net interest margins of

6.89%. That’s more than double what commercial banks make on typical loans.

Why? This is because credit card loans carry much higher interest rates.

This company’s margins already seem high. But they will get higher. This is

because the company benefits from high interest rates as a credit card issuer and

will also capitalize from increasing spreads as longterm rates rise and shortterm

rates stay the same.

But it’s a second trend that deserves your full attention. This second trend, along

with increasing net interest margins, will cause the stock price to explode.The Second Trend No One Is Talking About

The primary driver of credit card growth is the ability and desire to use credit

cards. After all, if people are cutting back on debt (also known as a “deleveraging

period”), credit companies are going to have a harder time getting new business.

They end up growing by wooing business away from other credit card companies.

But when people are adding debt (also known as a “releveraging period”), a very

beneficial trend begins to develop for credit card companies. During releveraging

periods, the whole consumer credit pie gets bigger. So the market for the credit

users expands. This ends up benefiting the entire credit card industry.

The big money in credit cards is made when households start to releverage their

personal balance sheets. This is a slow but inevitable process. The urge to spend is

built into our DNA. As consumer confidence and the economy both improve, so

will credit card spending.

You don’t have to take my word for it. Here’s the proof…

Since the financial crisis in 2008, we have been in a deleveraging period (when

people are paying off their debts and not taking on more debt). People have been

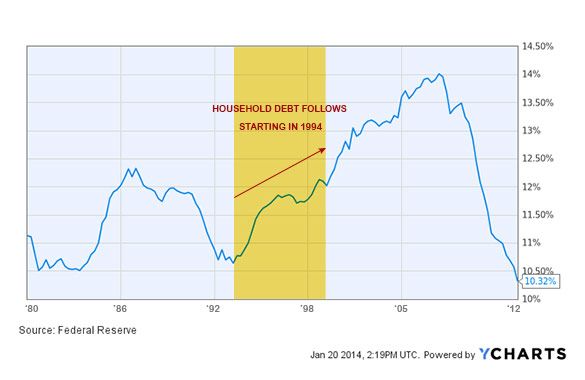

reluctant to take on more debt. Household debt has dropped about 28% since

2008. The chart below illustrates this period.

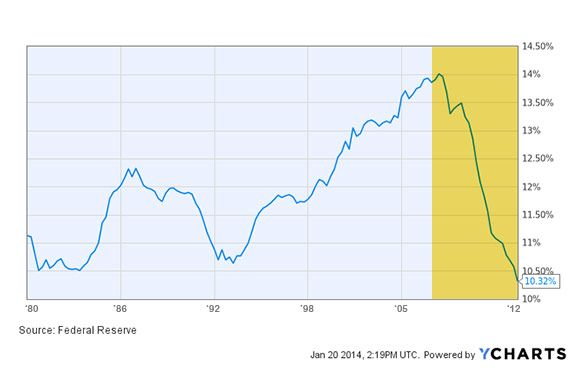

U.S. Household Debt Service 19802012

Between 2008 and 2012, U.S. Households Saved Money and Paid off DebtThe last time the country experienced a deleveraging period this low was in 1994.

Here’s the same chart. Do you see how the Household Debt Service is as low today

as it was in 1994?

U.S. Household Debt Service 19802012

Household Debt Today Is As Low As It Was in 1994The catalyst for consumers releveraging, or taking on more debt, is when gross

domestic product (GDP) starts to increase. Let me explain this. If you think about

it, it makes sense.

As the economy starts to grow, there are more jobs and higherpaying jobs. As

people have more money, they spend more money. You can see from the chart

below that GDP and household releveraging are very closely tied together. In the

next few paragraphs, I’ll point out some key features of these two graphs. Let’s take

a look first.

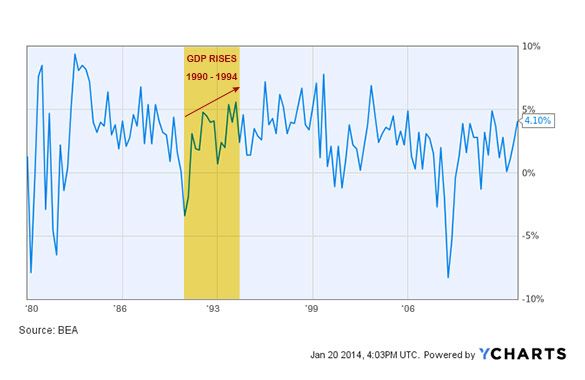

U.S. Real GDP

The rise in GDP comes first, then consumer releveraging comes secondThe last time we faced a similar situation to the one we are in now was in 1990. GDP had dropped from 7% in the 1980s to a low of 0% in 1990 and 1991. From 19901994, GDP moved higher, from 0% to 4%. But you can see from the household debt chart that consumers didn’t start

increasing their borrowings until 1994. That was four years after GDP started rising. The stock I am about to reveal to you exploded in value as this releveraging period took place. Between 1994 and 2000, consumer debt increased almost 23%. During that same period, this stock rose from $4.62 to $73.25, for a total gain of 1,485%. The facts are pointing to a repeat of the same conditions that were present during the early 1990s. GDP has been rising for four years, but consumers haven’t yet initiated the re leveraging period. This is exactly what happened in 1994. The economy bottomed, then it boomed higher from 19911994. But it wasn’t until 1994 that consumers felt safe enough to start borrowing again. This makes sense. People wait a while to feel safe before they start taking on more debt. In my opinion, this is exactly what we are seeing once again. The 2013 third quarter GDP numbers were recently announced. They came in at 4.1%. That’s the highest GDP growth we’ve seen since 1999. It also marks almost four years since GDP bottomed and started rising higher again. Almost four years. That means, based on trends of historical data, the releveraging period will begin soon. That is good news for credit card companies, as Americans are starting to feel safe about taking on more debt. This is setting the stage for a massive revaluation of the entire banking and financial sector. The stock we want to own to take advantage of this new credit boom is Capital One Financial (NYSE: COF). Capital One Financial is the fifth largest credit card company in the world. Credit cards account for 61% of its profits, while consumer and commercial lending accounts for 39%. What’s unique about this company is its ability to access very cheap sources of funding. That means it’s a master at borrowing money at a cheap rate and lending it out at a high rate. Right now, banks can borrow at the Fed Funds Rate of 0.07%. But in order to do so, they have to put up collateral to secure the loan. What’s also unique about Capital One is that it owns an online retail bank. That banking division provides the company with $206 billion in depositor’s cash that it can lend against. That money costs it only 0.79%.

Accessing this money is cheap. Meanwhile, the company doesn’t have to put up any collateral to secure that funding, much as it would have to do to borrow from the Fed Funds. What this means is the company has positioned itself to be able to easily access large amounts of very cheap capital. It can do this without having tie up vast amounts of other assets. Instead, the company can put more of its assets to work, compared with other companies that must rely on less flexible sources of funding. This allows Capital One to enjoy such high net interest margins, giving it an edge over other companies. As the releveraging trend plays out, we will see Capital One Financial become a prime beneficiary. Wall Street hasn’t figured it out yet. How do we know that? We know because Capital One is still very reasonably priced. Let me explain… Like other bank stocks, Capital One is valued by its book value. Recall that book value is a metric used to describe the asset value of a company. In the past, this stock has normally traded at two times book value. Today, the stock trades around $73 per share. And Capital One has a book value of $73 per share. So Capital One trades at just around one times book value. The reason the stock is so undervalued is because no one has realized that consumers are going to begin to take on more debt, just as they did in 1994. This is creating a bargain for us. Let’s assume that book value will grow at 5.5% per year. With a current book value of $73, and looking five years out, we’ll have a book value of $95. That’s a very conservative estimate, because Capital One’s 10 year historical book value growth has been 15%. If the shares just stay at one times book value, the stock will be at $95 and we’ll make about 30% on our money. But I’m not buying this for 30% upside. As net interest margins widen and consumer borrowing increases, so will the valuation that the market places on Capital One. Two times book value is a much more likely scenario, since this is normal for this stock. That’s the valuation we saw from 2008 and prior, even into the 1990s. When the stock returns to two times book value, then this will be a $190 stock. That’s a 160% move higher from here.

How to Amplify Your Profits on Both

of These Stocks Warren Buffett has billion

dollar stakes in some of the

I’ve shown you two stocks that are on the verge America’s top financial

of massive tripledigit moves. I believe Wells companies by owning their

Fargo will move 191% and Capital One Financial warrants, including: General

will rise 460%. But it doesn’t stop here. Now I Electric (GE Capital),

want to show you how to amplify those gains to Goldman Sachs, and Bank of

get up to 600% or more using that secret America.

Warren Buffett strategy I told you about.

In 2008, Buffet invested $3

Buffett has used this method for years to billion into General Electric

dramatically increase the value of his (GE Capital). In exchange,

investments. Governments have also made he received preferred stock

billions of dollars in profits using this very same and warrants for 135 million

strategy. shares. In 2013, the

warrants expired. In total,

Let me give you some background first… the deal generated about

$1.5 billion in profit for

During the depths of the financial crisis in

Buffet and his company.

2008, the U.S. government threw out a financial

lifeline to all of the banks. That lifeline was Buffett also invested $5

called TARP. Under this program, banks had to billion in Goldman Sachs.

give up shares in their companies. Those shares He received $5 billion in

were distributed in the form of warrants. preferred shares and

warrants for 43.5 million

A warrant is a security that gives the holder the

shares (worth another $5

option to buy a stock at a fixed price, until the

billion) at $115 per share. He

warrant expires. They look like checks. It gives

sold this position too.

you the right but not the obligation to buy the

According to CNN, Buffett

stock at a set price over a set period. What’s

made approximately $3.2

great about warrants is that they give you

billion from Goldman.

massive leverage without taking on massive

That’s approximately 64%

risk.

returns on his initial

Here’s what I mean… investment.

For every $1 you invest in a warrant, you can In 2011, Buffett’s company

control $23 worth of stock. The extra bonus is made another $5 billion

that, unlike trading on margin, there is no investment—this time in

interest to pay or margin call risk to worry Bank of America. Berkshire

about. To sweeten the deal, the warrants I’m acquired preferred stock andtalking about don’t expire until 2018. warrants for 700 million

shares of common stock at

Both Wells Fargo and Capital One still have $7.13 per share. They expire

TARP warrants that trade on the open market. in 2021. He still holds this

investment. So far, he has

Let’s discuss the Wells Fargo warrants first. The

collected over half a billion

symbol of the warrant is “WFC.WS.” Each

dollars in dividends, and the

warrant gives you the right to buy one share of

warrants are worth well over

Wells Fargo at $34.01. The warrants extend out

$10 billion.

until October 28, 2018.

Currently, Wells Fargo Stock is at $45, and the

warrants are trading at $15.45.

So if you have $10,000 that you wanted to put into Wells Fargo, let’s imagine you

bought the shares and not the warrants. At today’s price, you would own 222

shares ($10,000 divided by $45). When the stock goes up 200% to $135, you’ll

make a profit of $20,000.

However, if you took the same $10,000 and bought the warrants instead, here’s

what it would look like… Using a round and even price of $15, you’d be able to buy

approximately 670 warrants. Let’s assume the stock goes up 200%, to $135.

To figure out what the warrant is worth, we take the $135 stock price and subtract

the exercise price of the warrant, which is $34.01. This gives us a gain of $100.99

in each warrant. We then subtract the cost of the warrant ($15.45), which gives us

a net gain of $85.54.

Eightyfive dollars times 670 shares equals a profit of $57,000. That’s almost a

600% return on our original $10,000 investment. The warrant gives us close to

three times the return versus holding the stock.

So, you’re wondering now, what’s the risk?

The risk is that if Wells Fargo stock is at or below $34.01 on October 28, 2018,

your warrants will be worthless. In order for you to break even, the warrants must

be trading at $49 or higher by October 28, 2018.

This is why I have two different positionsize recommendations, depending upon if

you are buying the stock or the warrants.

Wells Fargo Stock

Action to take: Buy Wells Fargo stock up to $50 per sharePrice Target: $138 Risk: Medium Position Size: No more than 10% of your stock portfolio Stop Loss: No stop loss Wells Fargo Warrants Action to take: Buy Wells Fargo warrants up to $20 per warrant Price Target: $104 Risk: High Position Size: No more than 2.5% of your stock portfolio Stop Loss: No stop loss Warrant Strike Price: $34.01 Warrant Expiration: October 28, 2018 Warrant Symbol: WFC.WS P.S. If you want the warrants, you should move quickly. Wells Fargo has been the biggest buyer of its own warrants. To date, it has already bought back 63% of them. Just like Wells Fargo, Capital One sold warrants to the government in order to get its piece of the TARP pie. The warrants have a strike price of $42.13 and an expiration date of November 14, 2018. The symbol on the Capital One warrants is “COF.WS.” At the time of this writing, the stock is at $74.60 and the warrants are at $33.50. You have a choice: You can buy one share for $74.60. Alternatively, you can take that same $74.60 and buy 2.25 warrants. Here’s the difference on a $10,000 investment. At $74.60, you can own 134 shares. I’m looking for the stock to go to $190. At that price, you’ll make almost $15,000 on your position… a gain of about 150%. If you buy $10,000 worth of warrants instead, you can own almost 300 warrants. When the stock goes to $190, the warrants will be worth $147.87 (stock price of $190 minus strike price of $42.13). After you back out your purchase price of $33.50, your pre tax gain will be $114.17 on 300 shares, which is roughly $34,000… a gain of 340%. By holding the warrants, you make 340%, instead of 150%. So what’s the risk? Just like the Wells Fargo warrants, the risk is that if Capital One is at or below

$42.13 on November 14, 2018, your warrants will be worthless. In order for you to break even, the stock must be trading at $75.63 or higher by November 14, 2018. This is why I have two different positionsize recommendations depending upon if you are buying the stock or the warrants. Capital One Stock Action to take: Buy Capital One stock up to $85 per share Price Target: $186 Risk: Medium Position Size: No more than 5% of your stock portfolio Stop Loss: No stop loss Capital One Warrants Action to take: Buy Capital One warrants up to $45 per warrant Price Target: $143.87 Risk: High Position Size: No more than 2.5% of your stock portfolio Stop Loss: No stop loss Warrant Strike Price: $42.13 Warrant Expiration: November 14, 2018 Warrant Symbol: COF.WS

©2015 Palm Beach Research Group

55 NE 5th Avenue Suite 100

Delray Beach, FL 33483You can also read