SoCash Whitepaper - soCash: Commercialization and Results

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

soCash Whitepaper soCash: Commercialization and Results January 2018 Distributed Cash circulation network This whitepaper covers the key operational aspects of soCash’s distributed network for cash circulation during the proof of concept period. It covers the below aspects 1. Insights into Neighborhood Shops and Small merchants 2. Feasibility of offering cash services at retail outlets 3. User Segment insights, Cash demand and seasonality 4. Challenges & Opportunities 5. Conclusion

Insights into Neighborhood shops and Small retailers While Singapore has clocked impressive economic growth at a macro-economic level over last 3 years, sector specific growth rates have varied. Retail industry specially has seen an overall slowdown. 2016 saw consumer prices drop by 1% from the previous year; nevertheless, major retail channels registered further slumps in sales, including grocery retailers and department stores. While the drop is often attributed to the rapid growth being seen in internet retailing, there is more than that meets the eye. While E-commerce continues to grow rapidly, physical retail still accounts for more than 95% of retail sales by volumes 2

Singapore has an estimated 22,200 retail establishments generating a total sales of over SGD 44 billions, of which super markets, department stores & convenience stores account for over 25% (SGD 11 billion). (Source: www.singstat.gov.sg) The decline in retail industry is primarily is because of the consolidation of business volumes in the organized retailers who run large format stores, increased cost of doing business (including payment processing costs) and technology driven operations that generate productivity gains. The growth in the mall based retailing has shifted customer preference from value to experience and pushed footfalls to malls from residential neighborhoods. While it is true to the small retailers have been cash dependent and slow to adopt technology to drive productivity / differentiation, it should be understanding that their capacity for capital expenditure is limited by their operational size, margins and capacity for capital expenditure. However, it is important to note that the small retailers are finding their niche and restructuring their product mix from pure retail of goods to adding services into their offering. This is particularly suited given their physical proximity to customers in residential neighborhoods. On an aggregate basis, given their sheer reach and the network size of the small retailers, they are increasingly offering services that require an online to offline handoff (O2O) and vice versa. Online shoppers expect speedier delivery services and convenience stores are utilising their wide location coverage to offer click- and-collect services for online retailers and pure-play internet retailers. In addition, more retailers are revamping their store-based retailing strategies as the role of physical stores is constantly evolving, depending on the nature of the specific retailer. 3

Cash withdrawal is a basic need for the common man and this fits into the

service framework of most of the retailers. Given the necessity to generate

footfalls the progressive retailers who have adopted other digital services (like e-

commerce last mile delivery) have also embraced the idea of soCash. In addition

to generating repeated visits, they also see opportunities in using soCash app as

a marketing platform for both local and foreign tourists.

With practically the entire population requiring cash as a basic necessity and the

proof that ATMs attract crowd & footfalls, more retailers are looking at soCash to

provide cash transactions and other basic banking facilities, provided they are

not subjected to additional risks. In general, we found the below features to

categories our network of shops

Early Adopter ‘Try it out’ Status Quo

Minimarts

offering, specially Super markets

Convenience

Segment those offering and Old retail

Stores

Telco top up and chains

SIM card sales

Sole

Proprietorships Corporate (New

Ownership Large Corporates

but usually more retail chains)

than 1 outlet

Business Vol per SGD 10,000-

SGD500-10,000 NA

day in Cash 50,000

Liquidity for

Cash 20% 30% NA

withdrawal

4

Banking Local Bank /

Local Banks NA

relationships Foreign banks

Other payment Typically, fully NETS/Debit /

NA

services Cash Credit

Locations Heartlands & Heartlands &

NA

details Residential areas Residential areas

Offers other

Yes Yes NA

services

Minimal – May

Point of Sale, ERP

Technology have a Point of NA

& Accountings

Sale

What are the characteristics for a retailer to be part

of soCash network?

Our learnings indicate that the product fit of soCash is with a specific segment of

retailers. Typical attributes and the nature of business are highly influenced by

the customers that they serve or generate business.

If their clientele is familiar with technology and is open to engagements via

digital platform, then the retailers also get aligned in pushing such services at

their outlet. The services could be

• Mobile top ups

• Digital wallet balance top ups

• App store credits, game credits

• Laundry collection & e-Commerce pick up

5

High adoption of smartphones and increased adoption of digital services is also

generating demands from the network where offline / physical fulfillment is

required.

The typical profile of the early adopters are

• Second generation owners

• Hyper local business (Inside residential or industrial areas)

• Run multiple outlets to generate volume discounts

• Omni channel services (offer online ordering & delivery)

• Price leaders

• Inventory dominated by daily consumables

• Long opening hours, often 24hrs shops

Neighborhood shops and small retailers

6

7

Feasibility of offering cash services at small merchants As per data from MAS, Singapore generates over 19 million ATM withdrawal transactions worth over SGD 5 Billion every month. This indicates the cash circulating in the economy. Given that it in local economy, cash is always a ‘flow’ , the float in the economy should be able to meet the demand for cash. While the supply side is often compared to the maximum cash holding possible in ATMs, it should be noted that the number of retail outlets is around 10 times the number of ATMs in Singapore. Typical consumption behavior is that the cash is spent on low value purchases like food and daily consumption needs. These demands can be easily met provided each outlet accepting cash also gives out cash. Given the residential layout in Singapore which consists of primarily 3 types (HDB estates, Condominiums and Landed properties, a distributed cash network can easily meet average cash withdrawal demand. The reason is that all three formats drive hyper local consumption and generates a lot of cash within the local economy. As the local banks are reducing their physical footprint of branches and cash deposit machines, businesses are finding it harder to deposit cash because they have to make longer trips and bear longer queues at the branches. This implies that there is a larger amount of float sitting with the businesses and this can be circulated back to the people in the neighborhood. Given that the inventory cost and rentals of the outlets is mostly paid in cheques, the daily cash receivables are usually used for incidental expenses and salary. The medium sized shops that comprise most of our network have indicated that 8

typically deposit cash into their banks 2-3 times a week. In our platform they are typically willing to provide SGD 500 – SGD 2,000 cash float as the initial trial amount. As the consumer demand increases with more banks participating in the network, we estimate that the low value cash withdrawals (say SGD 200 and below) can be easily met by retailers. As the economy shifts to cashless mode, the demand for large value cash withdrawal is likely to reduce. This trend fits perfectly to redesign the cash circulation system in Singapore and shift to lower cost models compared to ATMs, CDMS and branches. Empirically it is possible to shift at a significant part of the low transactions away from ATMs to retailers provided the local banks participate in the soCash network. The volume shift depends on the participation of banks on our platform where the customer funds are held. However, it should be noted that for soCash’s distributed network requires banks to provide the digital payment and settlement capabilities. Also, the shift of customer preference will only happen if the bank’s digital platforms have adoption and transactional behavior across segments. On the positive side, assuming that consumer adoption of digital banking will grow and the banks eventually participate in the soCash network in Singapore, a shift of 30% of ATM withdrawals would mean a tremendous business opportunity for participating retailers. It would mean that over 6 million footfalls can be shifted to retailer outlets compared to people standing queues for cash withdrawal. This alone can give a fillip to the falling traffic to small retailer as well as generate organic revenue growth for small businesses. Increasing foot falls is likely to generate a domino effect for higher adoption of technology and 9

digital services at the small retailer, creating a sustainable ecosystem running on smart technology to deliver multiple digital services for the consumers. It has been proven that cash circulation can be hyper localized. The convenience for the consumers and the business model for the retailers has the potential to create the consumer shift similar to what has been witnessed in transportation industry. However, it is essential to drive consumer as well as retailer adoption to deepen the user base and the network size. We estimate that the key milestone for scaling the cash circulation network and growing usage by segments (early adopters and followers) would be to reach 100,000 active user base. This would generate the recurring visits for the retailers and give us data to predict and meet the cash float in the network to match the consumer demand. This would avoid scenarios of cash denial which may be a concern for many. There is sufficient liquidity floating in the economy to meet the average demand for cash. soCash provides the fulfillment platform. Given the above factors, with efficient execution of the product development and network expansion, it would be a realistic to assume that a distributed cash circulation network would be a sustainable alternative to existing network of ATM and Cashback via EFTPOS. The decoupling of the requirement for physical infrastructure and capital expenditure enables the model to scale in an Uber like fashion that can shift the mix of cash circulation infrastructure from ATMs and branches to a more efficient supply-chain running on distributed cash network. 10

Transaction and User segment insights

While cash usage is universal in Singapore, the adoption of a new platform

primarily is based on the adoption of mobile and user interests. From our

analytics, the usage indicates a big skew towards males.

SOCASH User Demographics

11From a user preference perspective, we find the adoption of soCash is very

broad-based and across categories

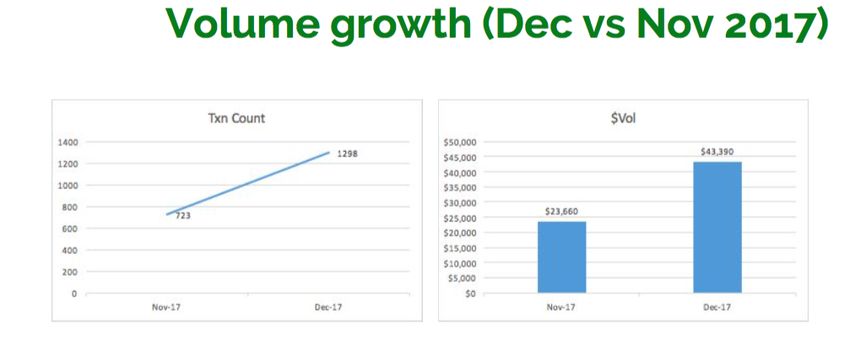

Transaction and usage details on our platform (as of Dec 31 2017) are the below

SCB DBS Total

Active Users 577 1,522 2,099

Transactions 1,170 1,987 3,157

$ Withdrawn $50,770 $43,830 $94,600

12It is clear the while users are open to try a more convenient alternative (during

the proof of concept period), incentivizing and sustained education on benefits of

digital banking is essential to drive adoption.

It is often seen that customers do not have internet & mobile banking credentials

or they find the second factor authentication (2FA) too intimidating and

cumbersome to try it out.

User retention and Cohort analysis

13Cash demand and seasonality In Singapore, demand for cash and ATM queues are fairly standard and stable. People have built routines to meet their cash needs. Typically, the cash withdrawal schedule is a routine that matches their outdoor activities. It is noticed that cash withdrawal volumes are high during the below hours. • Withdraw cash on their way to work • Withdraw cash during lunch break • Withdraw cash while returning from work For many cash withdrawal is a chore and hence the transactions are typically a weekend or monthly activity. While the daily average cash float in Singapore is approximately 5 Billion SGD, there are seasonal increases in demand for cash particularly around festivals like Chinese New Year. There is very little data at transactional level to analyze. It can be assumed that research in developed markets can be used to be a proxy of the behavior in Singapore as well. In most developed countries, the ratios of currency in circulation (CIC) relative to nominal GDP generally declined at least through the 1980s or even late 2000s. Since then, however, these ratios have stayed flat or even increased. This indicates that the payment choices made by individuals continues to be dominated by cash. Nevertheless, persistent holding and use of cash in these industrial countries during the spread of electronic alternatives highlights a need for an updated comparative study of payments that includes the use of cash. Furthermore, evidence on consumer holding and use of cash is even rarer, which implies that the cash volumes are stable at a per capita level 14

Challenges and Opportunities

As with any experiment with the financial service & banking, the challenges and

opportunities are immense. We feel that that we are probably 2 years early into

the vision of running a full-fledged distributed cash circulation platform in

Singapore because may enablers required to build a better platform than ATMs

are still falling into place.

Challenges

1 Convincing banks on the opportunity / possibilities

2 Vintage bank technology (makes integration a challenge in some cases)

Tight control on payment infrastructure by banks restricts product

3

innovation

4 Getting the right engineering talent to build the platform

5 Driving consumer adoption (in a crowded payments market)

6 Lack of funds to experiment (There is no scope for failure)

Rapid growth in network is required to drive shift from the current cash

7

circulation model to the soCash’s distributed cash circulation model.

8 Lack of awareness & adoption on digital banking

9 It is a challenge to build an engineering team in Singapore

Banks typically negotiate hard and don’t pay small companies. They

10 want everything free from startups but are willing to pay any amount to

established technology veterans

15Along with challenges also comes opportunities. As innovators, our goal has been

to understand the adversities and convert into opportunities in cash circulation.

We have gained a lot of insights into the current challenges around cash and we

have the ability to use soCash to drive efficiency in scenarios where the

transactions amounts are typically small but involve large volumes.

We have been fortunate that the product development and go-to-market has

went reasonably well.

Opportunities

Scaling the platform beyond Singapore for universal application and

1

adoption

Provide cost efficient alternative to cross border cash withdrawal to

2

monetize tourist demand

Launch a completely peer to peer cash exchange product. This would

3

mean that the network will auto scale and self-perpetuate

4 Creation of the largest virtual retailer network using soCash platform

Creation of the island wide network using which we can enable many

5

banking services which require offline fulfillment

Reducing the cost of cross border cash transaction and increasing

6

transparency for general public

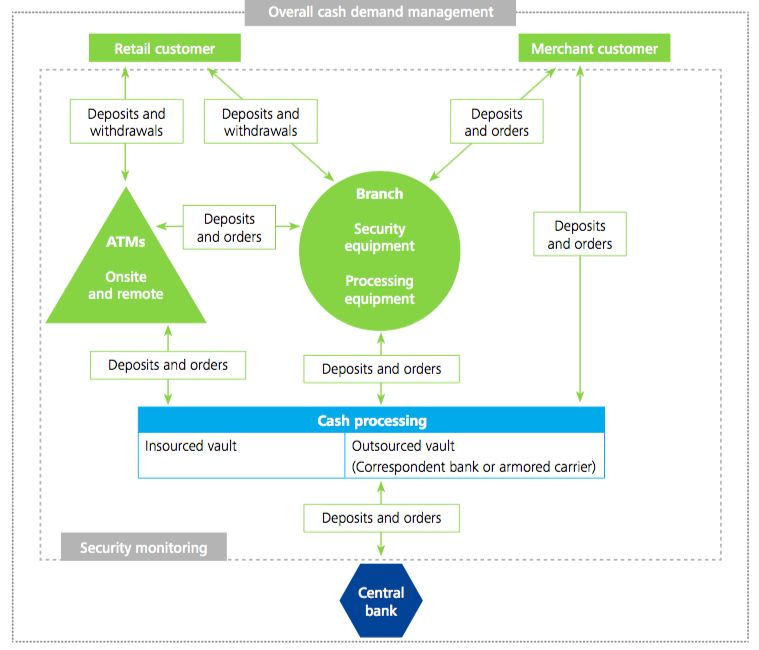

16Conclusion Even with an explosion of new methods of payment, cash in circulation globally has increased year after year and plays a major role in advancing economic growth. The recent demonetisation experiment in India is an interesting validation for the importance of cash liquidity in any large economy. ATMs have become the primary distribution point for small value cash demands while consumers who need large amounts of cash invariably go to bank branches. Beyond their convenience, automated teller machines (ATMs) and other technologies make cash easily available to customers. For retail banks, however, the cost and complexity of operating these technologies continues to rise across the entire cash supply chain–from holding, counting and validating cash to processing, transporting and protecting it. In fact, the worldwide cost of handling cash already exceeds $300 billion per year. To reduce these costs and improve productivity, retail banks need new methods. One good way to adopt a fresh perspective is by looking at how leading consumer business organizations move goods through their supply chains. By thinking of cash as goods, retail banks can apply proven supply chain strategies to reduce excess inventory, lower handling and processing costs, improve operating efficiency and optimize their network of ATMs. More critically, banks that manage their cash supply chain more effectively can also improve productivity and better position themselves to compete in the marketplace. 17

Retail banks operate some of the largest, most complex and most secure supply chains in the world, transporting and storing cash across thousands of locations every day. The cost of operating these supply chains extends to spending on all the equipment and services required to process and distribute cash throughout the bank’s network–from the central bank through to branches/ATMs and ultimately to customers. These costs are high and growing due to two main drivers: the rising demand for cash and the increasing use of more complex technology across the supply chain. Source Delloite In addition to the growing use of equipment to manage the cash supply chain, the equipment itself is becoming more complex and sophisticated. ATMs today 18

provide more functionality through more advanced operating systems, enhanced security features and additional account services. Similarly, more advanced hardware features include cash recycling and optical scanning to improve counting accuracy. However, the cost per ATM has steadily risen as a result. To gain a fresh perspective on this problem, compare the retail bank cash supply chain with e-commerce supply chains in retail industry, which transform raw materials to end products and distribute these products to consumers. By viewing cash as “inventory” moving through the retail bank supply chain, it becomes apparent that retail banks and e-commerce face very similar challenges. As a result, retail banks can apply proven strategies from the e- commerce industry to reduce excess inventory, lower handling and processing costs, improve operating efficiency and optimize their ATM networks The core principles of e-commerce supply chain are • Eliminate Inventory (static) • Eliminate transport (value stuck in supply chain) In the above context, rather than running a linear supply chain, a distributed network of hyper local cash is probably the best model for the future or cash circulation. Data from soCash indicates that consumers need cash, they do not need ATMs and hence it is possible to shift their transaction channels to soCash from ATMs. Combined the with growing adoption digitisation of banking, the relevance of physical network is increasingly under question. Branches and ATMs being the high cost physical assets being fed by a vintage supply chain that lacks efficiency, the current cash circulation process is ripe for disruption. 19

You can also read